Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.91 Billion |

| Market Size (2031) | USD 5.69 Billion |

| Growth Rate (2026 - 2031) | 7.78% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

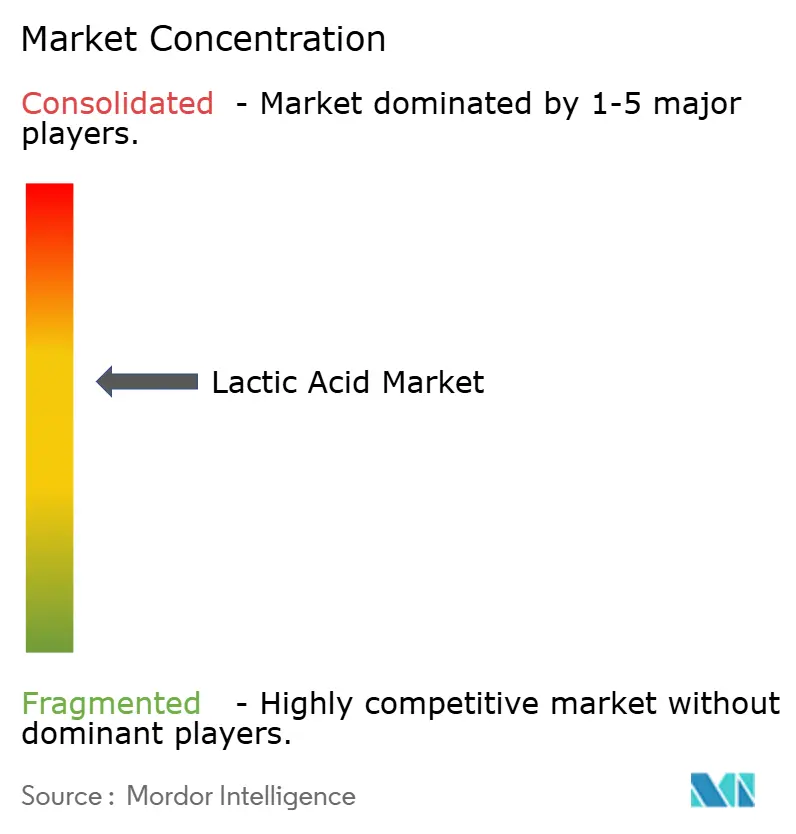

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lactic Acid Market Analysis by Mordor Intelligence

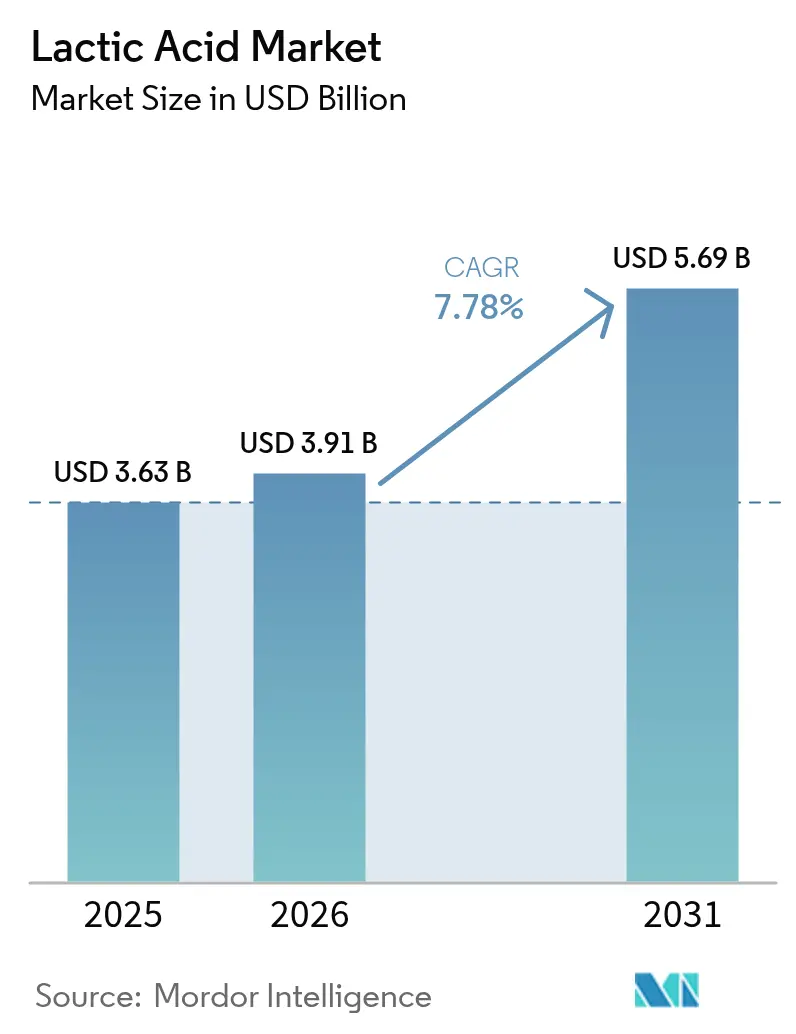

The lactic acid market size was valued at USD 3.63 billion in 2025 and estimated to grow from USD 3.91 billion in 2026 to reach USD 5.69 billion by 2031, at a CAGR of 7.78% during the forecast period (2026-2031). The market expansion is primarily driven by increasing applications in biodegradable plastics, pharmaceutical excipients, and industrial cleaning products. The biodegradable plastics segment is growing due to environmental concerns and strict regulations on conventional plastics. In pharmaceuticals, lactic acid is essential for drug formulations and controlled-release systems. The industrial cleaning sector uses lactic acid for its antimicrobial properties and environmental compatibility. Growth enablers include integrated manufacturing facilities in Asia-Pacific, European regulations limiting single-use plastics, and the US FDA's GRAS (Generally Recognized as Safe) status.[1]Source: U.S. Food and Drug Administration, “Food Additives Status List,” fda.govThe 3D printing segment benefits from lactic acid-based materials that provide enhanced mechanical properties and biocompatibility. The industry maintains competitiveness through vertical integration, diverse feedstock sources, and process optimization, enabling manufacturers to manage raw material price fluctuations effectively. This includes implementing advanced fermentation technologies, efficient purification processes, and developing strategic partnerships throughout the value chain.

Key Report Takeaways

- By source, natural fermentation captured 87.62% of the lactic acid market share in 2025 and is forecast to grow at 8.21% CAGR through 2031.

- By form, the liquid segment accounted for 64.10% share of the lactic acid market size in 2025; the solid form exhibits an 8.53% CAGR through 2031.

- By grade, food grade led with 42.20% revenue share in 2025; industrial grade is projected to expand at an 11.08% CAGR to 2031.

- By application, food and beverages held 32.65% of the lactic acid market share in 2025, whereas the PLA and bioplastics segment is advancing at an 11.49% CAGR through 2031.

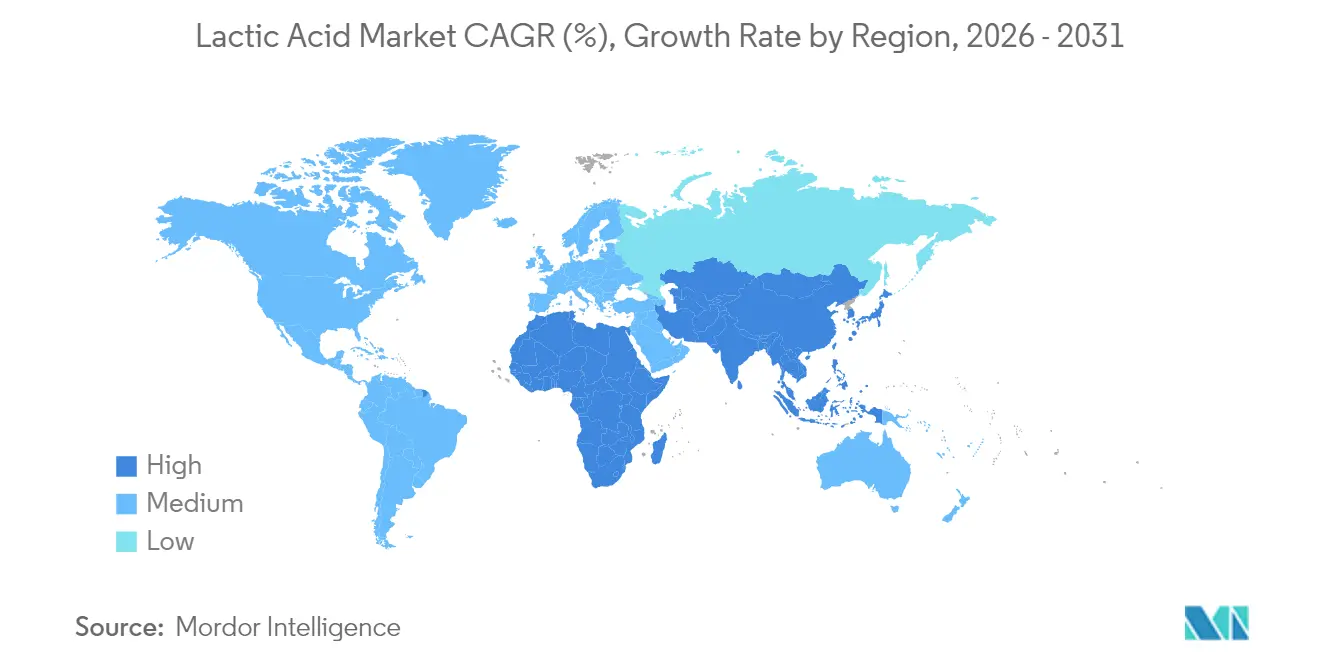

- By geography, Asia-Pacific commanded 30.72% of the lactic acid market share in 2025 and is forecast to grow at 8.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Lactic Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PLA-driven demand for biodegradable plastics | +2.1% | Global with APAC and Europe leadership | Long term (≥ 4 years) |

| Food and beverage preservative and flavor uses | +1.8% | North America and Europe | Medium term (2-4 years) |

| Pharmaceutical formulations and excipients | +1.3% | North America and Europe | Long term (≥ 4 years) |

| Personal care and cosmetics expansion | +0.9% | Premium markets worldwide | Medium term (2-4 years) |

| Industrial cleaning formulations | +0.7% | Global industrial hubs | Short term (≤ 2 years) |

| Animal feed additives | +0.5% | APAC and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

PLA-driven Demand for Biodegradable Plastics

The evolution of lactic acid from a food additive to a polymer precursor is driving significant market growth, with Polylactic Acid (PLA) applications contributing to the overall market CAGR. NatureWorks' USD 600 million facility in Thailand, scheduled for commercial operation by 2025, demonstrates this transition by combining lactic acid production, lactide synthesis, and PLA polymerization in a single facility. The facility's integrated approach aims to optimize production efficiency and reduce operational costs. The European Union's Single-Use Plastics Directive supports market growth by requiring biodegradable alternatives for specific packaging applications, creating a regulatory framework that favors PLA adoption[2]Source: USDA Agricultural Research Service, “Poultry Pathogen Reduction With Lactic Acid Rinses,” usda.gov. The planned Emirates Biotech facility in the UAE, set to become the world's largest PLA plant, indicates increasing Middle Eastern investment in this market and highlights the region's commitment to sustainable materials production. The expansion of PLA technology into 3D printing filaments and medical devices has broadened its market potential, offering innovative solutions for manufacturing and healthcare applications. FDA approval of poly-L-lactic acid for facial fat loss treatment demonstrates its versatility and safety profile in high-value medical segments. The combination of supportive regulatory frameworks, continuous technological progress, and increased manufacturing capacity establishes PLA as the main driver of lactic acid market growth through 2030, reshaping the industry landscape and creating new opportunities for sustainable material solutions.

Food and Beverage Preservative and Flavor Uses

The food and beverage sector remains the largest end-market for lactic acid, with growth supported by increasing demand for clean-label products and natural preservation methods. The FDA's designation of lactic acid as Generally Recognized as Safe (GRAS), with restrictions limited to good manufacturing practices, provides food manufacturers with comprehensive regulatory guidance for product formulation, safety compliance, and quality control measures. USDA research confirms lactic acid's effectiveness in reducing Salmonella in poultry applications, demonstrating pathogen reduction rates in controlled studies and expanding its use beyond traditional dairy fermentation processes.[3]Source: European Commission, “Directive on Single-Use Plastics,” ec.europa.euThe antimicrobial properties of lactic acid have been extensively documented across various food matrices, showing particular efficacy in meat and poultry processing environments. The European Food Safety Authority encourages lactic acid concentrations of 2-5% for beef carcass decontamination, strengthening its role in food safety protocols, microbial control strategies, and overall meat processing hygiene standards. In the plant-based dairy segment, manufacturers utilize specific lactic acid bacteria strains to reduce off-flavors, enhance nutrient absorption, and improve texture profiles, creating product differentiation opportunities through improved organoleptic properties, functional benefits, and extended shelf life. The application of lactic acid in plant-based dairy alternatives has also shown promising results in protein stabilization and flavor development, particularly in fermented products like yogurt alternatives and cheese substitutes.

Pharmaceutical Formulations and Excipients

The pharmaceutical industry's adoption of lactic acid derivatives is driven by their biocompatibility, proven safety record, and regulatory acceptance in parenteral formulations. Corbion maintains a unique market position as the only supplier of calcium lactate with a Certificate of Suitability from the European Directorate for the Quality of Medicines, reflecting strict quality requirements and comprehensive documentation standards in pharmaceutical-grade applications. The FDA's acceptance of ASTM F2579-18 as a standard specification for amorphous poly(lactide) resins in surgical implants has expanded the use of lactic acid derivatives in medical devices, particularly in biodegradable implants and drug delivery systems. Recent research focuses on L-lactide synthesis from lactic acid for PLA pellet production, establishing comprehensive laboratory-scale technology for medical applications, including controlled release formulations and tissue engineering scaffolds. L-lactic acid's function extends beyond its role as an excipient, serving as an agonist of hydroxycarboxylic acid receptor 1 (HCA1), which opens possibilities for targeted therapeutic interventions. The combination of therapeutic potential, proven safety profiles, established manufacturing processes, and stringent regulatory compliance makes pharmaceutical applications a high-value market segment with substantial entry barriers, including extensive documentation requirements and specialized production capabilities.

Personal Care and Cosmetics Expansion

Personal care and cosmetics applications growth is driven by lactic acid's effectiveness as an alpha-hydroxy acid and supportive regulations. The Australian Government permits lactic acid use in cosmetic products at concentrations up to 30%, with requirements for appropriate labeling due to potential skin sensitization. This regulation ensures consumer safety while enabling manufacturers to develop effective skincare formulations across various product categories, including serums, moisturizers, and chemical peels. The European Commission's Scientific Committee on Consumer Products sets safety parameters, recommending lactic acid use at 2.5% maximum concentration with pH 5.0, which balances product efficacy with user safety. These guidelines have facilitated the development of innovative formulations in both mass-market and luxury skincare segments. The European Chemicals Agency's REACH registration, covering 100-1,000 tonnes annually in 2023, indicates established supply chains for cosmetic applications and demonstrates the ingredient's widespread adoption across the European personal care industry. Consumer demand for natural active ingredients, combined with lactic acid's exfoliating and moisturizing benefits, supports growth in premium personal care formulations that offer higher margins compared to commodity uses. These properties make lactic acid particularly valuable in anti-aging products, facial cleansers, and professional skincare treatments, where its ability to improve skin texture, reduce fine lines, and enhance cellular turnover drives product efficacy and consumer satisfaction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs compared to conventional alternatives | -1.4% | Global, particularly affecting price-sensitive applications | Medium term (2-4 years) |

| Fluctuating raw material prices, particularly corn and sugarcane | -0.8% | Americas and APAC agricultural regions | Short term (≤ 2 years) |

| Competition from synthetic alternatives | -0.6% | Global industrial applications | Long term (≥ 4 years) |

| Storage and transportation challenges due to chemical properties | -0.3% | Global supply chain operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Industrial Cleaning Formulations

Production costs significantly constrain market growth, particularly affecting lactic acid's competitiveness in price-sensitive industrial applications. The fermentation-based production process requires substantial capital investment in specialized bioreactors, advanced separation equipment, and complex purification systems compared to synthetic chemical routes, despite its environmental advantages. Corbion's 2024 capital market presentation emphasizes comprehensive operational efficiency improvements and strategic restructuring initiatives to address persistent cost competitiveness challenges. The current cost structure substantially impacts commodity applications where lactic acid directly competes with synthetic preservatives and acidulants, limiting market penetration in price-sensitive segments despite its superior environmental benefits and sustainable characteristics. The high production costs affect the entire value chain, from raw material procurement to final product distribution, creating additional challenges for manufacturers seeking to maintain competitive pricing while ensuring product quality and sustainability standards.

Raw-material Price Volatility

The natural lactic acid market relies heavily on agricultural commodities, with corn and sugarcane serving as the primary feedstocks for production. The integrated sugar mill approach implemented in India provides significant cost benefits through the efficient utilization of sugarcane bagasse, transforming agricultural waste into valuable products. However, this method faces considerable limitations due to seasonal availability patterns and unpredictable agricultural market fluctuations. NatureWorks' strategic facility placement in Thailand enables local sugarcane sourcing, which effectively reduces transportation costs and minimizes supply chain vulnerabilities. Nevertheless, the facility's operations remain subject to regional agricultural conditions that directly influence raw material availability and quality. Current research initiatives exploring corn stover for lactic acid production demonstrate promising potential for reducing dependence on food-grade feedstocks, though the commercial implementation of these processes requires further development and validation. The market faces additional complexity due to intense competition from ethanol and biofuel producers targeting the same agricultural feedstocks. This competition generates significant upward pressure on raw material costs, particularly during periods characterized by elevated energy prices or when governments expand biofuel mandates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Natural Fermentation Dominates Amid Bio-Based Preferences

Natural fermentation accounts for 87.62% of the lactic acid market share in 2025 and is expected to grow at an 8.21% CAGR through 2031. Consumer preference for bio-based products stems from increasing awareness of sustainable production methods and environmental concerns. Food safety regulations supporting naturally derived acids, particularly in food and beverage applications, further reinforce the dominance of this production method. Synthetic production, primarily from petroleum intermediates, serves specific industrial segments where cost is the primary consideration, such as in chemical manufacturing and industrial applications.

Technological advancements in natural fermentation include multi-substrate processing, which allows for simultaneous fermentation of different raw materials, gene-edited Lactobacillus strains that improve conversion efficiency, and in situ product removal techniques that increase production yields. The successful implementation of demonstration projects using fruit waste and lignocellulosic residues indicates the potential for scaled production without competing with food crops. These alternative feedstock sources include agricultural residues, food processing waste, and forestry byproducts. This feedstock diversification helps protect the lactic acid market against fluctuations in grain prices while promoting circular economy principles.

By Form: Liquid Applications Drive Market Despite Solid Growth Potential

Liquid lactic acid held a 64.10% revenue share in 2025, due to its compatibility with direct pumping systems in food, pharmaceutical, and clean-in-place (CIP) applications. This form maintains its market dominance because most industrial bioreactors and downstream filling equipment are specifically designed and optimized for liquid handling operations. The extensive infrastructure investment in liquid handling systems across industries further reinforces this dominance. The solid form segment is growing at an 8.53% CAGR, driven by increased adoption in animal feed premixes and dry-blend personal care products, particularly in regions with challenging storage and transportation conditions. The growth is also supported by the rising demand for extended shelf-life products and easier handling in bulk manufacturing processes.

Recent technological advancements in spray drying and crystallization processes enable manufacturers to maintain high product purity levels while significantly reducing shipping weights. These improvements include optimized particle size distribution and enhanced moisture control systems. New hybrid systems combining membrane technology and evaporation processes reduce energy consumption by more than 10%, according to pilot studies conducted across multiple production facilities. These efficiency improvements are gradually reducing the historical price difference between liquid and solid forms, making solid lactic acid increasingly competitive in various applications. The development of specialized packaging solutions and improved storage stability has further enhanced the appeal of solid lactic acid in emerging markets.

By Grade: Industrial Applications Accelerate Beyond Food Dominance

Food-grade lactic acid held 42.20% of the market share in 2025. The segment's dominance stems from widespread use in food preservation, flavor enhancement, and pH regulation across the food and beverage industry. The increasing consumer preference for natural preservatives and clean-label products further strengthens its market position. Industrial grade is experiencing significant growth with an 11.08% CAGR, driven by increased demand in PLA polymerization and environmental cleaning applications. The expanding bioplastics sector, stringent regulations on conventional plastics, and growing preference for eco-friendly cleaning solutions contribute to this growth trajectory. The pharmaceutical grade segment maintains high profit margins due to GMP certification requirements and limited supplier availability, as demonstrated by Corbion's exclusive European rights for calcium lactate production.

Industrial applications prioritize optical purity over food safety requirements. This allows manufacturers to reduce decolorization processing steps, increasing production capacity and reducing operational costs. The streamlined manufacturing process enables producers to maintain consistent quality while optimizing resource utilization. The resulting production flexibility enables competitive pricing for bioplastics contracts, contributing to market expansion. This cost advantage has particularly strengthened the position of industrial-grade lactic acid in emerging applications and new market segments, including biodegradable packaging materials, sustainable textiles, and green solvents for industrial cleaning.

By Application: PLA Transformation Reshapes Traditional Food Focus

Food and beverages maintain a 32.65% share of 2025 revenue, while PLA demonstrates strong growth at 11.49% annually. Traditional applications include dairy fermentation, meat processing, and beverage acidification. Packaging regulations, increased adoption of 3D printing, and expanding medical applications support this growth trajectory. The market's diversification across personal care, pharmaceuticals, and industrial cleaners helps mitigate cyclical risks.

While food applications provide a stable baseline demand, manufacturers are directing new investments toward polymer production capabilities in response to supportive regulations and increased commitment to bio-based plastics from brand owners. Personal care and cosmetics applications benefit from established regulatory frameworks and consumer acceptance of alpha-hydroxy acids in skincare formulations. Pharmaceutical and healthcare applications command premium pricing due to stringent quality requirements and specialized manufacturing processes. Industrial and chemical processing represents an emerging growth area, particularly in cleaning formulations where lactic acid's antimicrobial properties and biodegradability offer advantages over synthetic alternatives. The application diversification reflects lactic acid's evolution from a single-use food additive to a platform chemical with multiple high-value end markets.

Geography Analysis

Asia-Pacific held a 30.72% market share in 2025 and is expected to grow at a 8.95% CAGR through 2031. The region maintains a competitive advantage through integrated manufacturing facilities in Thailand, China, and India, which benefit from readily available sugarcane and corn feedstock, along with lower capital expenditure requirements per installed ton. NatureWorks' Thailand facility exemplifies this regional strategy by combining local feedstock availability, economies of scale, and strategic proximity to export ports. The market growth is further supported by increasing domestic demand for disposable food service items and regulatory requirements for compostable shopping bags.

North America maintains its market position through established corn-wet-milling infrastructure, sophisticated bioprocessing capabilities, and well-defined regulatory frameworks. The region focuses on high-value applications in medical, personal care, and food safety sectors. Despite increased PLA packaging imports from Asia, the North American market remains stable due to corporate preferences for local sourcing to reduce scope 3 emissions.

Europe's market growth is primarily driven by the Single-Use Plastics Directive, which encourages manufacturers to adopt compostable alternatives. Companies like Galactic and Jungbunzlauer have adapted to regulatory requirements, establishing strong positions in pharmaceutical and cosmetic applications. While agricultural price fluctuations affect adoption rates, Green Deal initiatives continue to support investments in regional fermentation facilities.

Competitive Landscape

The market demonstrates moderate competition, with the top five companies accounting for a major share of total revenue. Corbion, Cargill, and Galactic maintain their market positions through established fermentation expertise, proprietary bacterial cultures, and integrated polymer production facilities. NatureWorks, a joint venture between Cargill and PTT Global Chemical, benefits from secured internal polylactic acid (PLA) production capabilities.

Companies are forming strategic partnerships to access new raw materials and strengthen customer relationships. Corbion's expansion of production capacity in Thailand complements its PLA joint venture operations, highlighting the significance of regional manufacturing centers. Emirates Biotech's collaboration with Sulzer for its UAE-based PLA facility signals the Gulf region's entry into the market, supported by strong financial resources and economic diversification initiatives.

While technology barriers remain moderate, established companies maintain competitive advantages through regulatory approvals in pharmaceutical and food applications. Start-up companies are developing alternative production methods, including lignocellulosic feedstock processing, electro-fermentation, and enzyme recycling technologies. These innovations could reduce production costs by 20-30% at commercial scale. Patents covering modified Lactobacillus strains and solvent-free separation processes are becoming crucial for competitive advantage in the industry.

Lactic Acid Industry Leaders

Corbion NV

Henan Jindan Lactic Acid Technology Co., Ltd

Galactic S.A.

Cargill Incorporated

Jungbunzlauer Suisse AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Sulzer signed a supply contract with Emirates Biotech to provide proprietary equipment for a large-scale Polylactic Acid (PLA) production facility in the United Arab Emirates.

- August 2024: Jungbunzlauer expanded its biocidal product range by introducing L(+)-lactic acid as an environmentally sustainable disinfectant. The product effectively eliminates gram-negative bacteria and enveloped viruses at low concentrations while remaining biodegradable, addressing the growing market demand for sustainable antimicrobial solutions.

- April 2024: SK Geo Centric has developed a technology to produce lactic acid, the primary raw material for PLA (Polylactic Acid) bio-based plastic. The production method, developed by the research team at SK Innovation's Institute of Environmental Science and Technology, uses microbial fermentation to minimize costs and chemical byproducts.

- December 2023: Sulzer Chemtech developed SULAC technology to address the growing demand for lactide biopolymer and support the adoption of sustainable, high-quality plastics. The technology enables polylactic acid (PLA) manufacturers to integrate lactic acid to lactide production capabilities into their operations.

Global Lactic Acid Market Report Scope

Lactic acid is a colorless or yellowish, syrupy, water-soluble liquid, C3H6O3, abundant in sour milk, made mainly by fermentation of cornstarch, molasses, potatoes, etc., or synthesized. It is used mostly in dyeing and textile printing, as a flavoring agent in food, and in medicine. By source, the market is segmented into natural and synthetic. By application, the market is segmented into meat, poultry and fish, beverage, confectionery, bakery, fruits and vegetables, and dairy. By region, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD).

By Source

| Natural |

| Synthetic |

By Form

| Liquid |

| Solid |

By Grade

| Food Grade |

| Industrial Grade |

| Pharmaceutical Grade |

| Cosmetic Grade |

By Application

| Food and Beverages | Meat, Poultry and Seafood |

| Dairy Products | |

| Bakery | |

| Confectionery | |

| Beverages | |

| Others Food and Beverage Applications | |

| Polylactic Acid (PLA) and Bioplastics | |

| Personal Care and Cosmetics | |

| Pharmaceutical and Healthcare | |

| Industrial and Chemical Processing |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Source | Natural | |

| Synthetic | ||

| By Form | Liquid | |

| Solid | ||

| By Grade | Food Grade | |

| Industrial Grade | ||

| Pharmaceutical Grade | ||

| Cosmetic Grade | ||

| By Application | Food and Beverages | Meat, Poultry and Seafood |

| Dairy Products | ||

| Bakery | ||

| Confectionery | ||

| Beverages | ||

| Others Food and Beverage Applications | ||

| Polylactic Acid (PLA) and Bioplastics | ||

| Personal Care and Cosmetics | ||

| Pharmaceutical and Healthcare | ||

| Industrial and Chemical Processing | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the lactic acid market?

The lactic acid market is valued at USD 3.91 billion in 2026 and is projected to reach USD 5.69 billion by 2031

Which region holds the largest share of the lactic acid market?

Asia-Pacific commands the largest regional share at 30.72% in 2025 and is also the fastest-growing region with a 8.95% CAGR through 2031

What application is expanding most rapidly for lactic acid?

Polylactic acid (PLA) and other bioplastics use is the fastest-growing application, advancing at an 11.49% CAGR thanks to demand for compostable packaging and 3D-printing materials

Who are the leading players in the lactic acid market?

Corbion, Cargill/NatureWorks, and Galactic lead global supply with integrated fermentation and PLA operations, together holding roughly two-thirds of worldwide revenue.

Page last updated on: