Microencapsulated Food Ingredient Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

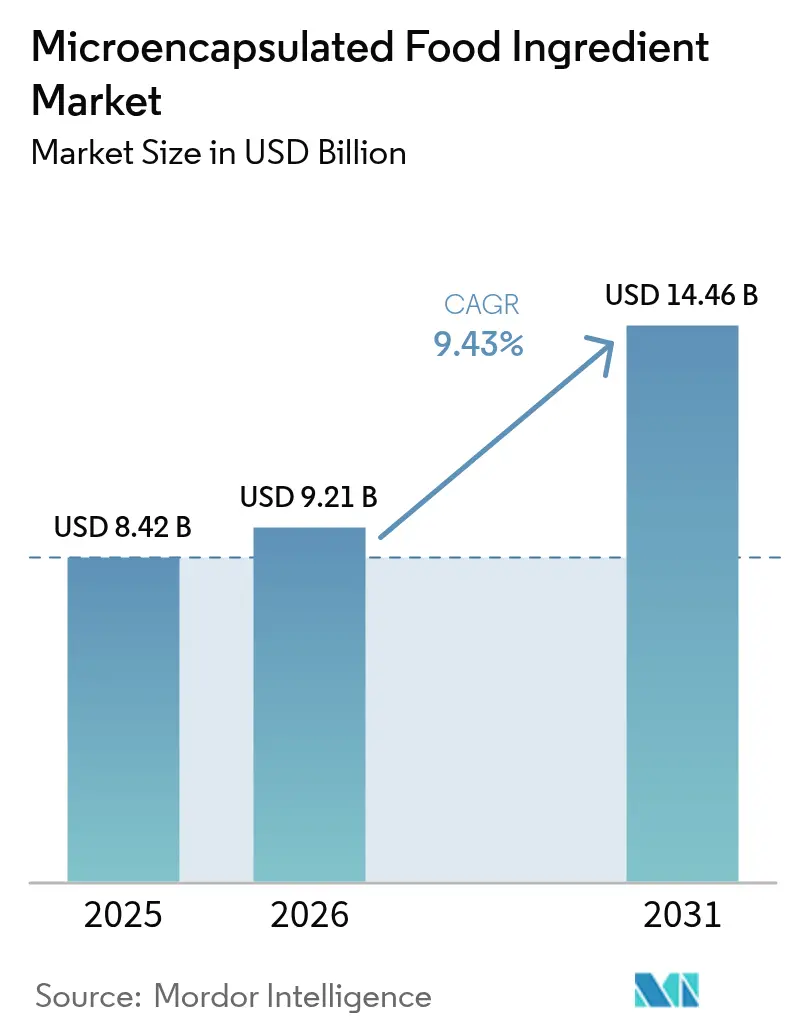

| Market Size (2026) | USD 9.21 Billion |

| Market Size (2031) | USD 14.46 Billion |

| Growth Rate (2026 - 2031) | 9.43% CAGR |

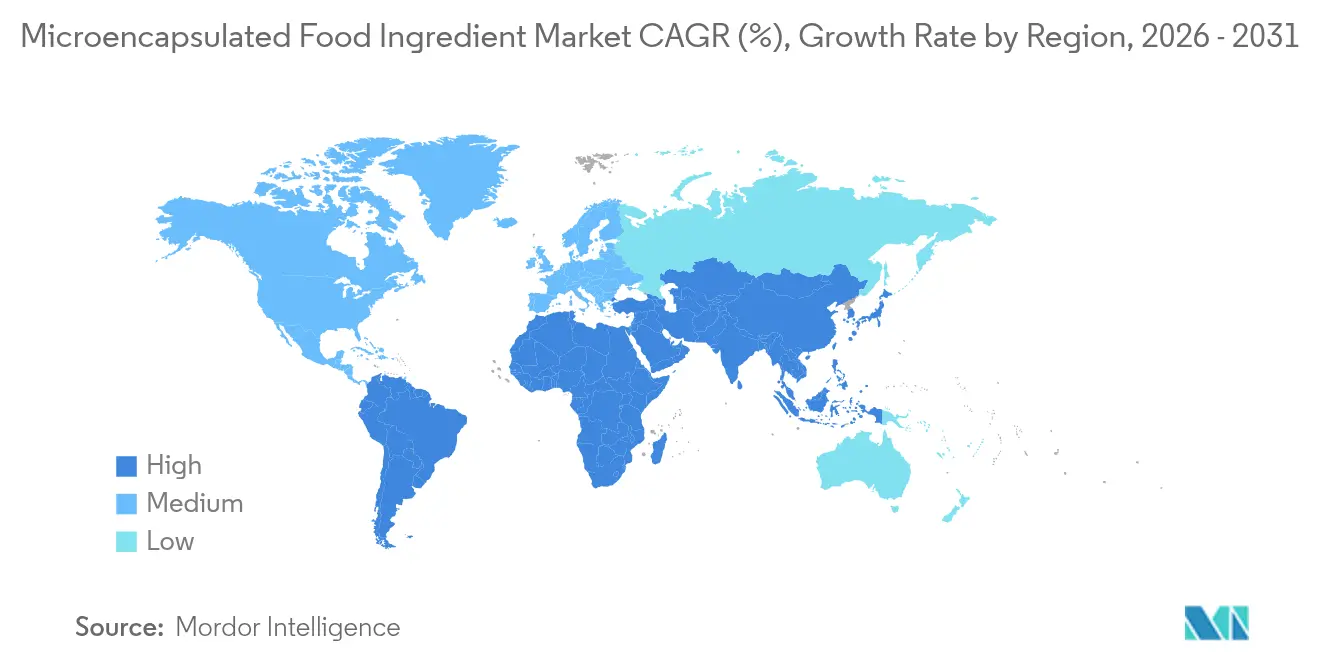

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Microencapsulated Food Ingredient Market Analysis by Mordor Intelligence

The Microencapsulated Food Ingredient Market size is expected to grow from USD 8.42 billion in 2025 to USD 9.21 billion in 2026 and is forecast to reach USD 14.46 billion by 2031 at 9.43% CAGR over 2026-2031. This expansion reflects the industry's strategic pivot toward sophisticated ingredient protection technologies that address mounting consumer demands for functional nutrition and extended product stability. Macro forces reshaping the market landscape include the accelerating convergence of health consciousness and convenience-driven consumption patterns, particularly evident in the sports nutrition sector, where microencapsulated creatine formulations are enabling liquid-format applications previously constrained by stability limitations. The regulatory environment is simultaneously evolving, with the FDA's recent approval of butterfly pea flower extract for ready-to-eat cereals and snack applications signaling expanded opportunities for natural color encapsulation [1]Source: Federal Register, "Listing of Color Additives Exempt From Certification; Butterfly Pea Flower Extract", federalregister.gov.

Key Report Takeaways

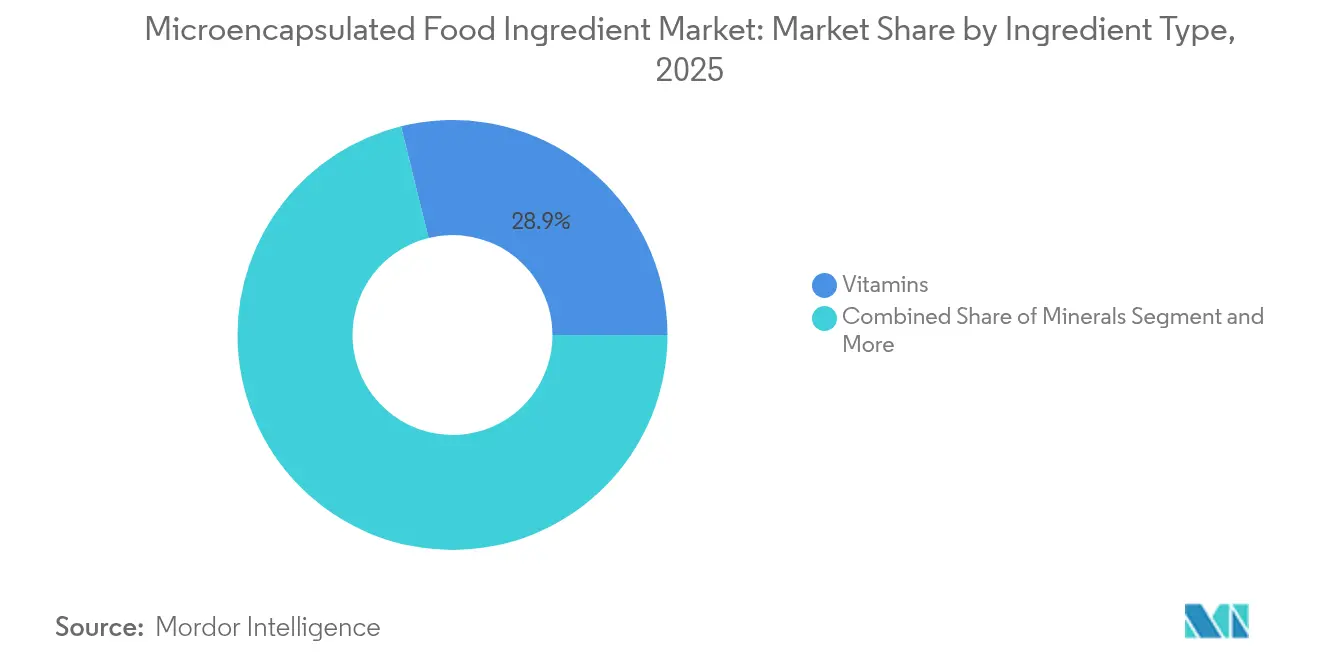

- By ingredient type, vitamins led with 28.85% of the microencapsulated food ingredient market share in 2025, while probiotics and prebiotics are projected to expand at a 12.02% CAGR through 2031.

- By form, solid formats held 67.76% of the microencapsulated food ingredient market size in 2025; liquid encapsulation is forecast to rise at 11.11% CAGR between 2026-2031.

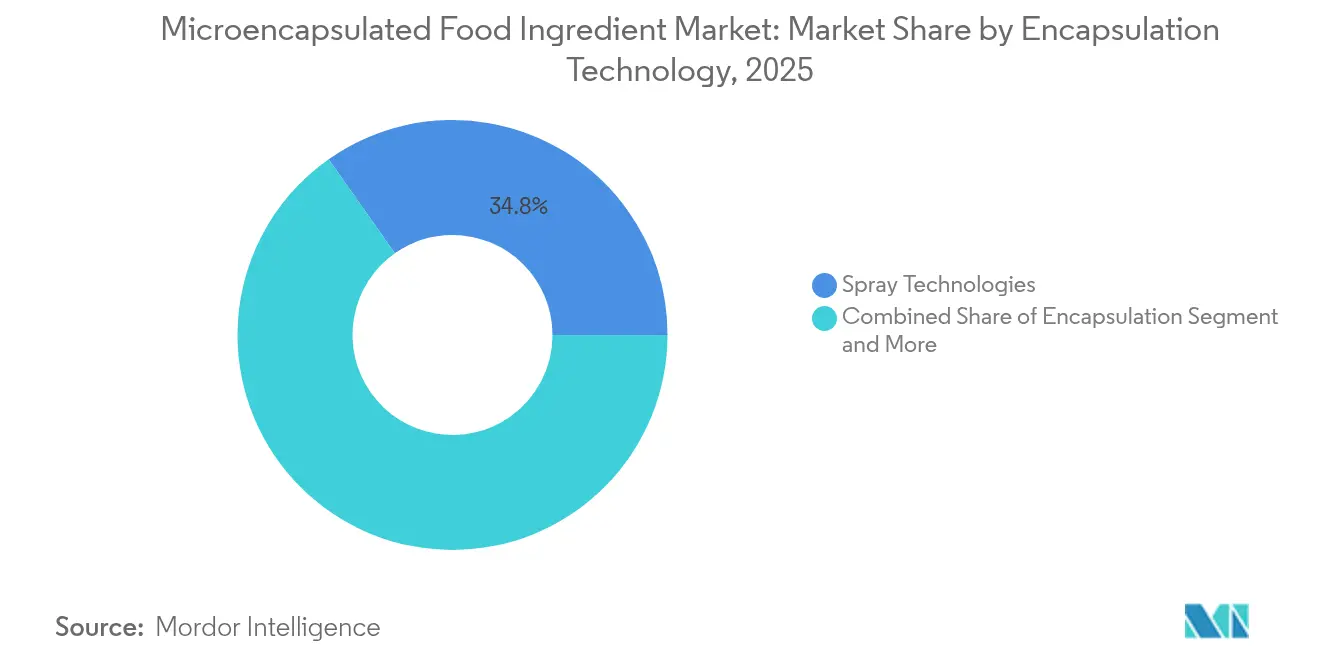

- By encapsulation technology, spray processes commanded 34.77% revenue share in 2025; emulsion methods are advancing at 11.55% CAGR through 2031.

- By application, functional foods accounted for 44.32% of the microencapsulated food ingredient market size in 2025, whereas dietary supplements exhibit the highest projected CAGR at 11.44% to 2031.

- By geography, North America held 36.60% revenue share in 2025, while the Asia Pacific shows the fastest growth at a 10.52% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Microencapsulated Food Ingredient Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for controlled release of flavors and nutrients | +1.2% | Global, with concentrated growth in North America & Europe | Medium term (2-4 years) |

| Rising demand for functional and fortified foods | +1.8% | Global, with accelerated adoption in Asia Pacific urban centers | Long term (≥ 4 years) |

| Growing focus on extended shelf life and stability of food products | +1.5% | Global, particularly relevant in emerging markets with limited cold chain | Short term (≤ 2 years) |

| Increasing Applications in Sports Nutrition and Dietary Supplements | +0.9% | North America & Europe core, expanding to Asia Pacific | Medium term (2-4 years) |

| Expanding applications in bakery and confectionery products | +1.1% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Development of innovative delivery systems for sensitive ingredients | +0.7% | Technology hubs in North America, Europe, and select Asia Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Controlled Release of Flavors and Nutrients

The increasing demand for enhanced sensory experiences is significantly expanding microencapsulation applications beyond conventional taste masking methods. Food manufacturers extensively use microencapsulation technology to develop sophisticated time-released flavor profiles that activate during specific consumption phases, enabling substantial product differentiation in competitive categories such as functional beverages and snack foods. The technology effectively protects volatile compounds from degradation during processing while ensuring comprehensive targeted release in the digestive system, addressing both manufacturing efficiency requirements and bioavailability optimization needs. This precise control of nutrient delivery timing has become increasingly crucial as regulatory authorities implement stringent requirements for documented bioavailability data to validate functional food claims in the market.

Rising Demand for Functional and Fortified Foods

The growth of the functional foods market is changing ingredient sourcing practices as manufacturers aim to enhance nutritional content while maintaining product taste and texture. This transformation is particularly evident in developed markets where consumers increasingly demand foods that combine health benefits with traditional sensory appeal. Microencapsulation technology allows the integration of ingredients such as omega-3 fatty acids, plant-based proteins, and botanical extracts into food products that previously faced consumer resistance due to flavor issues or processing limitations. This technical advancement has enabled manufacturers to create products that meet both nutritional and organoleptic requirements. The combination of an aging population and increased focus on preventive healthcare continues to drive demand for fortified products that provide proven health benefits through effective delivery systems. This trend is further supported by growing consumer awareness of the relationship between diet and long-term health outcomes, leading to increased adoption of functional foods across various demographic segments.

Growing Focus on Extended Shelf Life and Stability of Food Products

Supply chain disruptions and sustainability concerns are elevating ingredient stability as a strategic priority, with microencapsulation offering solutions that extend product viability without synthetic preservatives. The technology's protective barrier function prevents oxidative degradation of sensitive compounds like vitamins C and E, enabling manufacturers to maintain nutritional claims throughout extended distribution cycles typical of global food supply chains. Encapsulation's capacity to reduce water activity around hygroscopic ingredients addresses moisture-related degradation challenges, particularly relevant in tropical and subtropical markets where ambient humidity accelerates product deterioration. This stability enhancement is crucial for emerging market penetration, where cold chain infrastructure limitations require ingredients capable of maintaining functionality under ambient storage conditions for extended periods.

Increasing Applications in Sports Nutrition and Dietary Supplements

The sports nutrition market's shift toward mainstream consumers is increasing the demand for encapsulated ingredients that enable new product formats and enhanced bioavailability. Microencapsulation allows creatine to be incorporated into liquid formulations, overcoming its traditional instability in water-based environments that previously restricted it to powder forms. This technological advancement has opened new possibilities for product development and formulation flexibility. Encapsulation effectively masks the bitter taste of amino acid supplements while maintaining quick dissolution properties needed for pre- and post-workout products. The process involves coating individual ingredient particles with protective materials that shield unpleasant flavors without compromising functionality. The technology also enables sustained-release formulations, allowing once-daily dosing that improves consumer adherence compared to traditional multiple-dose supplements. This controlled release mechanism ensures a steady supply of nutrients throughout the day, optimizing the supplement's effectiveness and convenience for users.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic relevance | Impact Timeline |

|---|---|---|---|

| High initial investment costs for encapsulation equipment and technology | -0.8% | Global, particularly constraining for small-to-medium food manufacturers | Short term (≤ 2 years) |

| Limited shelf life of certain encapsulated ingredients | -1.2% | Global, with heightened impact in regions with extended distribution cycles | Medium term (2-4 years) |

| Elevated production costs compared to non-encapsulated ingredients | -0.6% | Cost-sensitive markets in developing regions and price-competitive categories | Short term (≤ 2 years) |

| Technical challenges in maintaining stability during food processing | -0.9% | Global, with particular relevance for high-temperature processing applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Investment Costs for Encapsulation Equipment and Technology

High initial investment costs remain a significant restraint in the microencapsulated ingredients market. Implementing advanced encapsulation technologies, such as spray drying, fluid bed coating, and coacervation, requires not only specialized equipment but also precision-engineered systems, which substantially increase capital expenditures. These financial challenges often prevent small and medium-scale manufacturers from adopting these technologies, creating a notable barrier to entry. Additionally, the ongoing costs associated with maintenance, the requirement for skilled technical expertise, and the need for rigorous process validation further compound operational expenses. As a result, the elevated setup and operational costs restrict new entrants and slow down capacity expansion, particularly in developing regions where financial resources and infrastructure may be limited.

Technical Challenges in Maintaining Stability During Food Processing

Food manufacturing environments face challenges in maintaining consistent processing conditions, which affects the performance of encapsulated ingredients and product quality. In high-temperature applications like baking, extrusion, and retort processing, thermal stress can break down encapsulation wall materials and cause early release of core ingredients, reducing their functional effectiveness. During processing and storage, moisture variations can cause water-absorbing wall materials to expand or shrink, which changes release patterns and may create texture issues in final products. The pH levels in different food matrices can compromise protein-based encapsulation systems, requiring specific formulation modifications that may not work across a manufacturer's various product lines. The requirement for process-specific adjustments reduces the efficiency benefits of standardized ingredient systems, as manufacturers must develop custom solutions when implementing encapsulated ingredients across multiple products, leading to longer development times and increased technical demands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Vitamins Lead While Probiotics Drive Innovation

Vitamins maintain 28.85% market share in 2025, reflecting their established role in food fortification programs and consumer familiarity with nutritional benefits, yet probiotics and prebiotics are emerging as the fastest-growing segment with 12.02% CAGR through 2031 as gut health awareness reshapes functional food development priorities. The vitamin segment's dominance stems from regulatory clarity around health claims and well-established manufacturing processes that enable cost-effective encapsulation at commercial scales.

Minerals represent a stable but mature segment focused on bioavailability enhancement through chelation and microencapsulation technologies that reduce metallic off-tastes in fortified products. Enzymes are gaining traction in specialized applications where targeted release timing is crucial for functional benefits, particularly in digestive health formulations. Amino acids benefit from encapsulation's taste-masking capabilities, enabling incorporation into mainstream food products without compromising palatability.

By Form: Solid Dominates the Market, While Liquid Innovation Challenge

Solid encapsulation forms a command 67.76% market share in 2025 due to manufacturing simplicity and storage stability advantages, while liquid encapsulation technologies are advancing at 11.11% CAGR as manufacturers overcome historical stability limitations through innovations in emulsion science and protective coating systems. The solid form's market leadership reflects established spray-drying infrastructure and consumer acceptance of powder-based functional ingredients in applications ranging from infant formula to sports nutrition products.

Recent advances in microfluidic encapsulation technologies are enabling precise control over particle size distribution and release characteristics in liquid systems, addressing previous limitations around batch-to-batch consistency. The liquid segment's expansion is particularly notable in beverage applications where encapsulation enables incorporation of traditionally incompatible ingredients like probiotics and plant proteins without compromising product clarity or mouthfeel. Solid forms retain advantages in shelf-stable applications and cost-sensitive markets where processing simplicity and storage economics favor powder-based delivery systems over more complex liquid formulations.

By Encapsulation Technology: Spray Technologies Dominate the Market

Emulsion technologies are experiencing 11.55% CAGR through 2031, challenging spray technologies' 34.77% market share in 2025 as manufacturers seek superior encapsulation efficiency and controlled release characteristics for high-value bioactive compounds. Spray drying's market leadership reflects its scalability advantages and compatibility with heat-stable ingredients, making it the preferred choice for vitamin and mineral encapsulation in large-volume food applications. The technology's established infrastructure and operator familiarity enable rapid production scaling, though thermal stress limitations restrict applications for heat-sensitive compounds like probiotics and certain enzymes.

Emulsion technologies offer superior protection for sensitive ingredients through gentler processing conditions and enhanced barrier properties, enabling applications in premium functional foods where ingredient integrity is paramount. Dripping technologies serve specialized applications requiring precise particle size control, particularly in pharmaceutical-grade nutraceuticals, where release timing is critical for therapeutic efficacy. The competitive landscape is evolving toward hybrid approaches that combine multiple encapsulation techniques to optimize both protection and release characteristics, with companies like Givaudan expanding production capacity for encapsulation technologies in November 2024.

By Application: Functional Foods Scale Meets Dietary Supplement Growth

Functional foods maintain a 44.32% market share in 2025 through established distribution channels and mainstream consumer acceptance, yet dietary supplements are advancing at an 11.44% CAGR as personalized nutrition trends drive demand for targeted delivery systems and bioavailability enhancement technologies. The functional foods segment's leadership reflects successful integration of encapsulated ingredients into everyday food products like fortified cereals, enhanced dairy products, and functional beverages, where health benefits complement familiar consumption patterns.

Dietary supplements benefit from encapsulation's capacity to improve ingredient stability and enable innovative delivery formats like time-release capsules and effervescent tablets that enhance consumer convenience and compliance. Bakery and confectionery applications are expanding as encapsulation technologies enable heat-stable vitamin and mineral fortification in products subjected to high-temperature processing conditions. Dairy products represent a growing application area where encapsulation protects probiotics and sensitive nutrients through pasteurization and fermentation processes while maintaining product functionality throughout shelf life. The convergence of health consciousness and indulgence is driving encapsulated ingredient adoption in traditionally non-functional categories like confectionery, where manufacturers seek to add nutritional value without compromising sensory appeal.

Geography Analysis

North America accounted for 36.60% of global revenue in 2025 due to its transparent regulatory framework, robust R&D infrastructure, and consumers seeking verified health benefits. The FDA's Generally Recognized as Safe (GRAS) notifications accelerate innovation cycles and provide competitive advantages to companies with regulatory expertise. The market maintains consistent demand through meal-replacement shakes, fortified snacks, and natural color systems. Well-developed cold chain networks reduce stability concerns, enabling suppliers to focus on release-profile innovation rather than basic protection measures.

Asia Pacific exhibits the highest growth potential with 10.52% CAGR through 2031, reflecting rapid urbanization, expanding middle-class purchasing power, and increasing health consciousness that is driving demand for functional foods and dietary supplements across diverse cultural contexts. The region's growth trajectory is supported by government initiatives promoting food fortification to address nutritional deficiencies, particularly in developing markets where microencapsulation enables stable vitamin and mineral delivery in challenging distribution environments.

Europe represents a mature but innovation-driven market where sustainability concerns and clean label trends are influencing encapsulation technology selection toward natural wall materials and environmentally responsible processing methods. The region's stringent regulatory environment, exemplified by EFSA's updated novel foods guidance effective February 2025, creates barriers to entry but also ensures market stability for approved technologies and ingredients .

Regulatory Landscape

Microencapsulated food ingredients are regulated mainly through the permitted status and use conditions of the core ingredient and the encapsulating (wall) materials, along with any technology-specific safety considerations. In the United States, ingredients and carriers used for microencapsulation generally need to be either authorized food additives or Generally Recognized as Safe (GRAS) under intended conditions of use, with FDA oversight covering food additives, GRAS, and color additive requirements where applicable. The U.S. GRAS governance pipeline has also been under scrutiny, including an OIRA-listed proposed rule (RIN 0910-AJ02, October 2025 agenda) on mandatory notification for GRAS determinations, which increases compliance expectations for suppliers commercializing novel delivery systems and new encapsulants.

In the European Union, microencapsulated ingredients have to fit within the Union food additives framework (including Regulation (EC) No 1333/2008) and can trigger Novel Food Regulation (EU) 2015/2283 considerations when encapsulants or process outcomes introduce novelty, for example modified biopolymers or nano-related features. Product-specific requirements for sensitive nutrition applications are becoming more granular; for example, Commission Regulation (EU) 2025/2058 (October 2025) set specific maximum levels for sodium ascorbate in microencapsulated vitamin A preparations used in infant and follow-on formulae, reinforcing the need for tight compositional control and robust analytical substantiation from premix and encapsulation suppliers.

Value Chain Analysis

The value chain starts with sourcing core actives (for example vitamins, minerals, probiotics, amino acids, essential oils, and colors) and wall materials such as plant proteins and polysaccharides, along with processing aids and solvents where relevant. Encapsulation R&D and formulation design then translate target outcomes, such as taste masking, oxidative protection, shelf-life, and controlled or enteric release, into manufacturable specifications. Scale-up follows using established methods like spray drying, spray cooling, fluidized bed coating, extrusion, and complex coacervation, with precision approaches such as microfluidic core-shell fabrication increasingly used to refine particle and release characteristics.

Quality management and testing, including stability, release kinetics, and in-matrix performance, remain important midstream steps because processing stresses in beverages, bakery, and dairy can undermine capsule integrity and weaken functional claims. Commercialization and distribution typically run through ingredient suppliers and distributors that integrate encapsulation platforms into customer formulations and premix systems for functional foods and supplements. Recent ecosystem activity points to tighter linkages between technology developers, distributors, and large end-users: Xampla partnered with Lehmann Ingredients (August 2024) to supply nutrient microencapsulation technology to food and beverage manufacturers, and Xampla also announced a pilot with Yili Innovation Centre Europe (July 2024) to validate natural polymer capsules for dairy fortification. Downstream adoption depends on application support and regulatory-ready documentation, while upstream constraints include capex and specialized know-how for encapsulation lines, which can limit smaller manufacturers and encourage collaboration with specialized contract or technology partners.

Competitive Landscape

The microencapsulated food ingredient market exhibits moderate concentration with established players leveraging technological expertise and manufacturing scale advantages, while emerging opportunities in specialized applications create entry points for innovative companies with novel delivery systems or niche ingredient focuses. Market leaders like BASF SE, DSM-Firmenich AG, Cargill, Incorporated, and Ingredion Incorporated maintain competitive advantages through integrated research and development capabilities that span from ingredient sourcing to final product formulation, enabling comprehensive solutions that address customer needs across multiple application areas.

Strategic positioning increasingly emphasizes sustainability credentials and clean label compatibility as food manufacturers respond to consumer demands for transparent ingredient sourcing and environmentally responsible processing methods. Technology differentiation centers on encapsulation efficiency, release control precision, and processing stability, with companies investing in proprietary coating materials and specialized equipment to create competitive moats around core capabilities.

The FDA's GRAS Notice approval for Bacillus subtilis NRRL 68053 illustrates the regulatory pathway complexity that favors companies with established regulatory affairs capabilities and scientific substantiation resources. White-space opportunities exist in emerging applications like plant-based protein encapsulation and sustainable packaging integration, where technological innovation can create first-mover advantages in rapidly evolving market segments driven by changing consumer preferences and regulatory developments.

Microencapsulated Food Ingredient Industry Leaders

-

BASF SE

-

Cargill, Incorporated

-

DSM-Firmenich AG

-

Ingredion Incorporated

-

Royal FrieslandCampina N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Clean-label fortification and stability-driven reformulation continue to create opportunities for microencapsulation in beverages, dairy, and functional foods, especially where off-notes, oxidation, or processing losses constrain direct addition of bioactives. A commercialization cue is the shift toward plant-based, food-grade carrier systems: Xampla has demonstrated pea protein-based microcapsules for vitamin D protection (published May 2025) and has advanced access through its distribution partnership with Lehmann Ingredients (August 2024) and dairy validation work with Yili Innovation Centre Europe (July 2024). These activities support broader supplier opportunities to package encapsulation as an enabling platform for vitamin and probiotic dosing, while helping reduce overage tied to processing losses.

Technology opportunity is also moving beyond high-throughput methods like spray drying alone toward approaches that improve control of particle size, morphology, and release kinetics. This includes microfluidics, electrospraying/electrospinning, and tailored coacervation systems discussed in recent peer-reviewed literature (2024-2026). Demand signals are tied to sports nutrition and supplements, where microencapsulation helps enable liquid-format creatine and improves taste masking for amino acids. At the same time, investment and platform-building activity indicates continued innovation in bio-based encapsulation, including Big Idea Ventures launching BioCloak (June 2024) to develop bio-based encapsulation technologies for nutrients and biologicals across food and agriculture.

Recent Industry Developments

- April 2026: INNOBIO launched DurOmega Algal DHA 20% as a water-dispersible microencapsulated powder designed to reduce odor and improve oxidative stability in applications such as beverages and infant formula. The launch supports wider use of omega-3 fortification in formats where sensory issues and stability have limited inclusion rates.

- October 2025: BASF launched Lutavit A/D3 1000/200 NXT, a microencapsulated vitamin A and D3 combination produced at its Ludwigshafen site. The product strengthens BASF's fortification portfolio for customers seeking more stable, easier-to-handle vitamin systems for challenging processing and storage conditions.

- August 2024: Lehmann Ingredients partnered with Xampla to supply Xampla's nutrient microencapsulation technology to food and beverage manufacturers. The collaboration broadens route-to-market for enteric and performance-oriented microcapsule formats through an established ingredient distribution channel.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of food ingredients that are microencapsulated to protect sensitive actives, improve stability, mask taste, or control release, and then sold for use in food and beverage formulations across major regions.

Scope exclusions: It excludes microencapsulation used only for pharmaceutical, cosmetic, industrial, or packaging-only applications, where the end use is not a food ingredient.

Segmentation Overview

-

By Ingredient Type

- Vitamins

- Minerals

- Enzymes

- Amino Acids

- Probiotics and Prebiotics

- Essential Oils

- Others

-

By Form

- Solid

- Liquid

-

By Encapsulation Technology

- Spray Technologies

- Emulsion Technologies

- Dripping Technologies

- Others

-

By Application

- Functional Foods

- Dietary Supplements

- Bakey and Confectionary

- Dairy Products

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Rest of Europe

-

Asia Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with building a clear view of how encapsulated ingredients are produced and where they are consumed, so we could anchor the model to real food output and ingredient demand signals. We referred to public sources such as the US FDA (food additive and color-related updates), the USDA and Eurostat (food production and price series), FAO (commodity and processed food indicators), and UN Comtrade (trade flows for relevant ingredient categories and carriers).

To connect the above to company reality, we also reviewed annual reports, investor presentations, product brochures, press releases, and association websites related to flavors, functional ingredients, and probiotics. A few paid subscriptions for company financials and intelligence, news and financials, patent databases, and shipment-level import and export data were used selectively to cross-check expansion plans and technology activity. The sources listed here are illustrative, and other public references were used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions around which applications are actually being microencapsulated, how pricing moves by ingredient family, and what adoption looks like across mature and emerging food markets. We spoke with a mix of ingredient suppliers, encapsulation solution providers, food manufacturers, and distributors, and then reconciled differences by region so the final model stayed realistic for APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 14% | APAC: 53% |

| Mid tier: 56% | Functional/Unit leaders: 37% | EMEA: 29% |

| Smaller Players: 14% | Managers: 49% | Americas: 18% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where food and beverage production, trade patterns, and the penetration of encapsulated actives were used to reconstruct the demand pool for microencapsulated ingredients by region. After the demand pool was set, it was translated into value using application-level pricing logic, where we adjusted for typical dosage rates and the price premium created by encapsulation.

To keep outputs grounded, we corroborated the results with selective bottom-up approximations, including supplier revenue disclosure checks, sampled price per kilogram ranges, and channel feedback on volumes moving into key applications. Inputs used in the model included adoption of functional foods and beverages, probiotic and vitamin fortification intensity, stability and shelf-life needs in processed foods, relative pricing of carriers and coatings, and import dependence for specialized ingredients in certain regions. Where bottom-up inputs were incomplete, gaps were handled through proxy ratios from comparable ingredient families, then re-checked through follow-up calls.

For forecasting, we used scenario analysis supported by a light multivariate regression view, where demand growth was linked to packaged food output, health and wellness product launches, and regional income and urbanization trends. Assumptions for penetration and price progression were tuned based on what practitioners said about reformulation cycles and the pace of new encapsulation formats entering food manufacturing.

Data Validation & Update Cycle

Validation was done in steps so outliers could be found early and corrected before sign-off. We compared modeled totals against independent signals such as regional processed food growth, relevant ingredient trade trends, and the direction of pricing seen in public statistics and in interviews, and then variances were reviewed by another analyst.

When a data point moved the market size more than expected, the underlying assumption was revisited and, when needed, respondents were re-contacted to confirm the driver. Reports are refreshed annually, and interim updates are made when material events occur, such as major capacity additions, regulatory changes affecting encapsulated additives, or sudden input cost shocks. Before delivery, a final review pass is completed so clients receive the latest updated view available at that time.

Mordor Intelligence's Microencapsulated Food Ingredient Market Estimate Compared With Other Published Estimates

Published market values for microencapsulated food ingredients can vary even when the headline topic looks the same, since each publisher sets its own scope and timing for what counts as a food ingredient. Differences also come from how pricing is handled for high-value actives, and whether the estimate is kept current with recent formulation and regulatory shifts.

Food packaging-only microencapsulation and non-food end uses are kept outside Mordor Intelligence's scope, which is one reason our 2026 figure does not line up with estimates that blend in broader microencapsulated ingredients. Some sources also use earlier base years and then extend the series using a single CAGR, which can miss mix shifts between vitamins, probiotics, flavors, and enzymes, and it can also apply currency conversion assumptions that do not match the year being reported.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.21 B (2026) | |

| Global Consultancy A | USD 10.20 B (2026) | Uses a broader inclusion set that extends beyond food ingredients into adjacent end uses like dietary supplements and other non-food applications, which lifts the addressable value in the same year. |

| Industry Publisher B | USD 8.34 B (2024) | Anchors the series on an earlier base year and applies a longer forecast runway, and the estimate can shift depending on how it treats distribution-channel markups and average price progression between ingredient families. |

The table shows that the spread is mostly explained by what is counted as a food ingredient, plus year alignment and how price and penetration are updated. By tying the model to observable food production signals and then checking penetration and pricing with practitioners, our estimate stays traceable to clear drivers and can be repeated with the same steps when the market updates.

Key Questions Answered in the Report

What is the current value of the microencapsulated food ingredient market?

The market stands at USD 9.21 billion in 2026 and is forecast to achieve USD 14.46 billion by 2031.

Which ingredient type dominates revenue?

Vitamins lead with 28.85% microencapsulated food ingredient market share in 2025, owing to cost-efficient processes and clear regulatory frameworks.

Why are probiotics considered a high-growth segment?

Probiotics register a 12.02% CAGR through 2031 because encapsulation boosts survival in foods and matches rising consumer focus on gut health.

What regions offer the fastest growth opportunities?

Asia Pacific expands at 10.52% CAGR, driven by urbanization, middle-class spending, and government-backed fortification initiatives.

Page last updated on: