Market Overview

| Study Period | 2020 - 2031 |

|---|---|

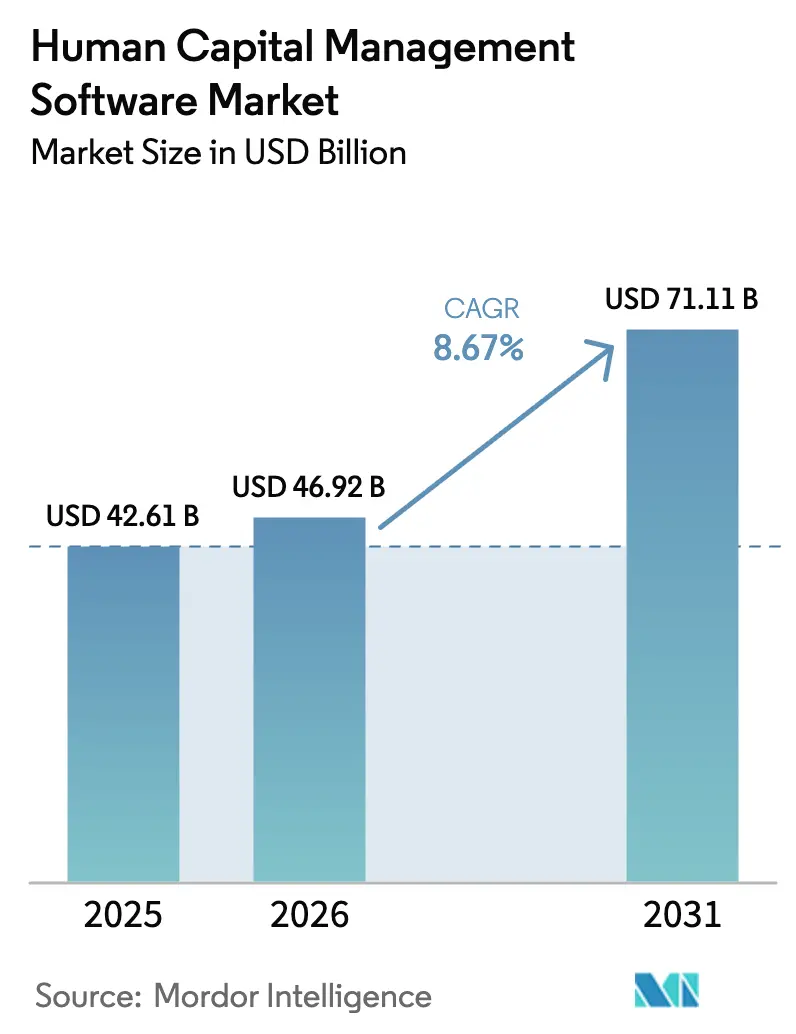

| Market Size (2026) | USD 46.92 Billion |

| Market Size (2031) | USD 71.11 Billion |

| Growth Rate (2026 - 2031) | 8.67% CAGR |

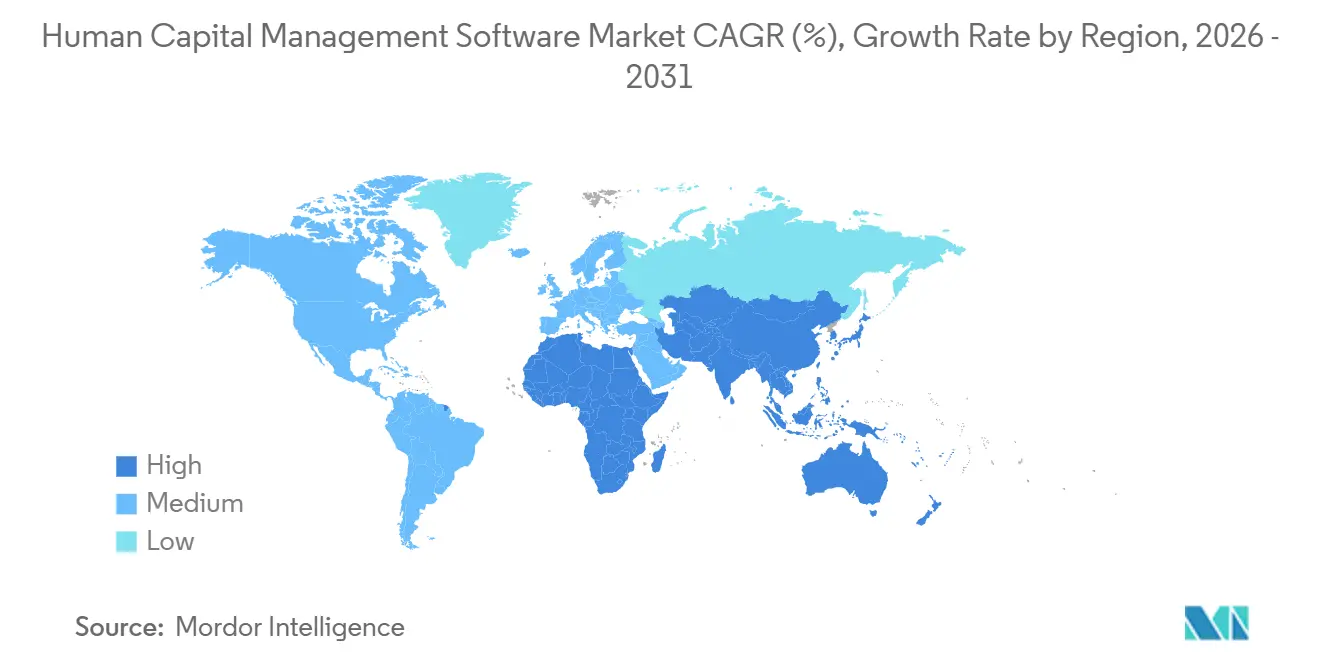

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Human Capital Management Software Market Analysis by Mordor Intelligence

The human capital management software market size is expected to grow from USD 42.61 billion in 2025 to USD 46.92 billion in 2026 and is forecast to reach USD 71.11 billion by 2031 at 8.67% CAGR over 2026-2031. Enterprises are prioritizing cloud-native suites that embed generative-AI copilots into payroll, talent, and learning workflows, enabling real-time analytics and reducing service-desk resolution times from days to minutes. Demand also rises as governments digitize tax administration and impose real-time payroll reporting, intensifying the need for automated compliance engines. Vendors differentiate through ISO 27001 and SOC 2 Type II certifications, which calm data-sovereignty concerns without sacrificing scalability. Competitive intensity remains elevated as legacy providers defend their installed bases while venture-backed disruptors attract substantial funding, underscoring a market that rewards continuous product innovation.

Key Report Takeaways

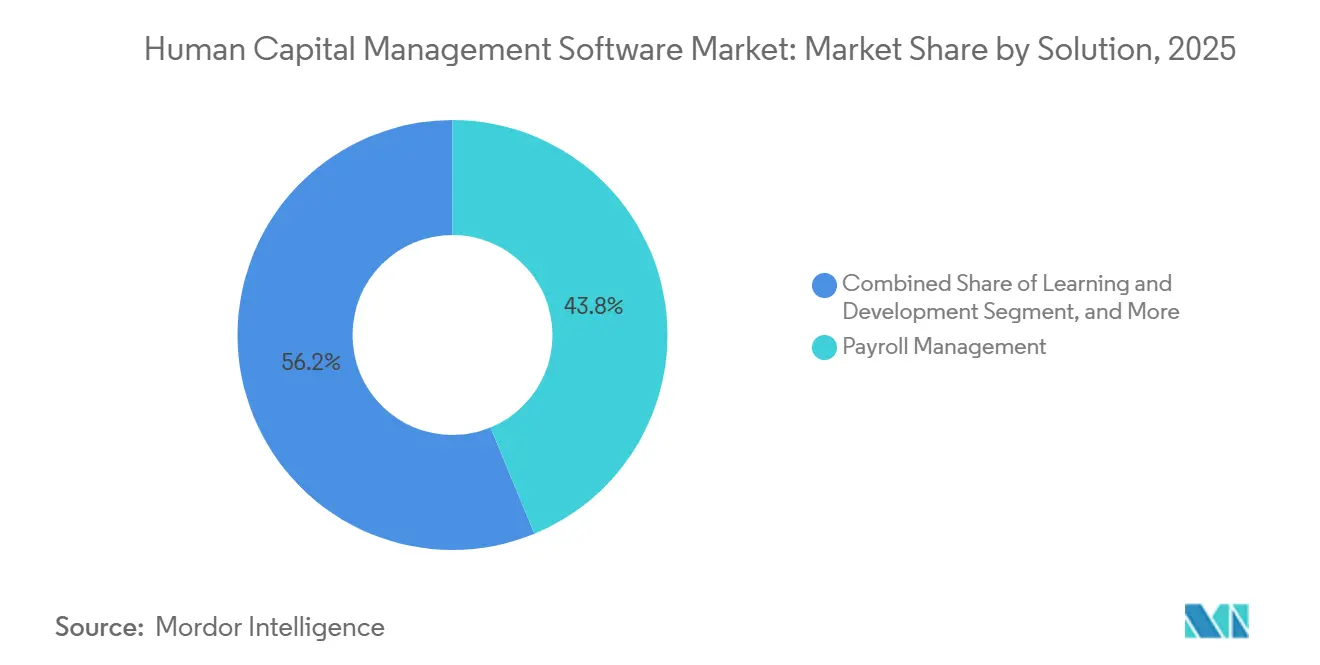

- By solution, payroll management led with 43.78% revenue share in 2025, while learning and development posted the fastest 9.72% CAGR to 2031.

- By deployment, on-premises captured 55.83% of revenue in 2025; cloud is forecast to expand at a 9.11% CAGR through 2031.

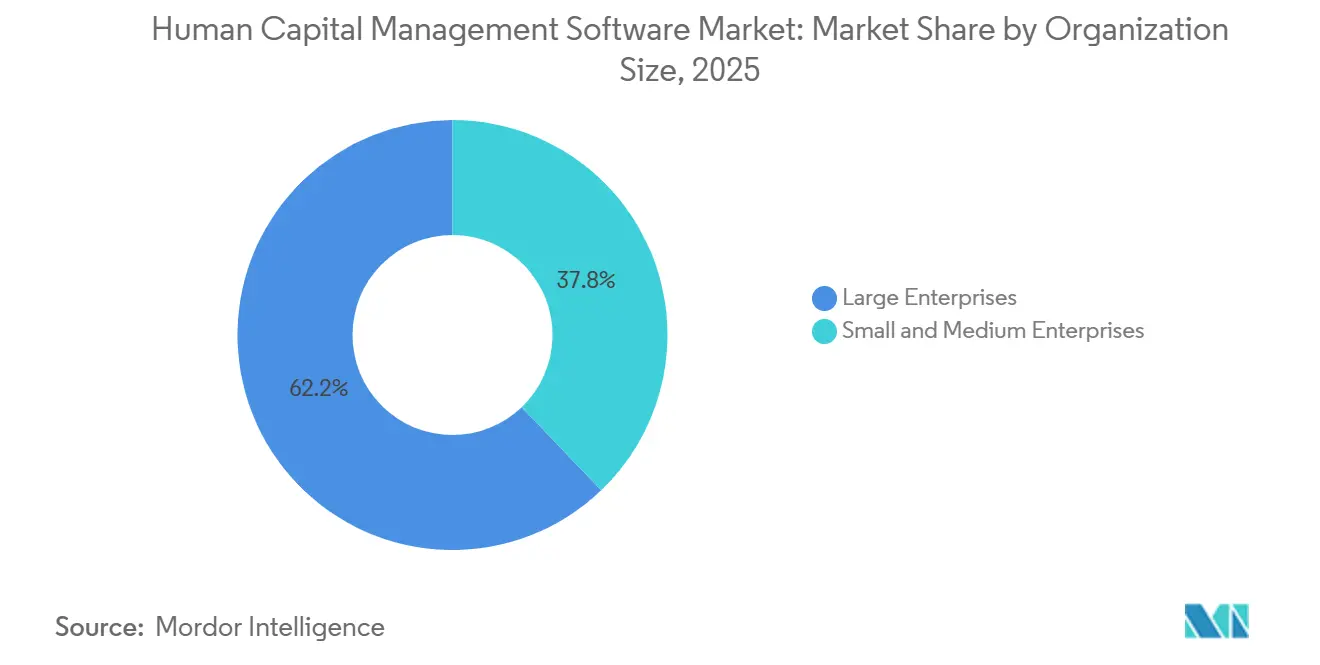

- By organization size, large enterprises accounted for 62.17% of spending in 2025, yet SMEs are advancing at a 9.04% CAGR through 2031.

- By industry vertical, Banking, financial services, and insurance (BFSI) commanded 22.89% of the human capital management software market in 2025, whereas healthcare is projected to grow at a 10.93% CAGR through 2031.

- By geography, North America led with 37.62% revenue in 2025, while Asia-Pacific is set to climb at a 9.61% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Human Capital Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to Cloud-Native HCM Platforms | +2.1% | Global, with acceleration in North America and Europe | Medium term (2-4 years) |

| Integrated Talent and Payroll Suites Gain Traction | +1.8% | Global, particularly North America and Asia-Pacific | Medium term (2-4 years) |

| Workforce Analytics and AI for Strategic HR | +1.5% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Compliance Mandates for Global Payroll and Taxation | +1.3% | Global, with highest impact in Europe, Asia-Pacific, and multi-country operations | Long term (≥ 4 years) |

| Generative-AI Co-Pilots Accelerate HR Service Delivery | +1.2% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| Skills-Based Workforce Planning Models Replace Job-Centric Structures | +0.9% | Global, with early gains in North America, Europe, and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift to Cloud-Native HCM Platforms

Cloud-native architecture decouples the compute, storage, and application layers, enabling vendors to deliver weekly feature updates that accelerate innovation cycles. Workday Data Cloud, released in September 2025, streams real-time employee, financial, and operational data through open APIs, eliminating batch ETL and supporting cross-functional analytics.[1]Workday Inc., “Workday Data Cloud Launch,” investor.workday.com Enterprises gain the ability to align workforce capacity with demand forecasts, improving decision speed and reducing integration costs. Deloitte’s 2025 migration survey showed that 68% of firms selected faster innovation over cost savings as the primary driver of cloud adoption. Security remains crucial, so ISO 27001 and SOC 2 Type II attestations are now embedded directly into procurement workflows to shorten risk reviews. Combined, these factors add durable lift to the human capital management software market by lowering technical debt and increasing time-to-value.

Integrated Talent and Payroll Suites Gain Traction

Organizations are collapsing multiple point solutions into unified suites to remove reconciliation delays that can consume 15-20 finance hours per pay cycle. ADP Workforce Suite, launched in November 2025, bundles payroll, time tracking, benefits, and talent modules for sub-1,000-employee firms, cutting implementation timelines from quarters to weeks. Deel processes USD 22 billion in global payroll across 150 countries, automating social-insurance and tax filings that shift quarterly, illustrating the compliance advantage of consolidated data flows.[2]Deel Inc., “Series E Funding Announcement,” deel.com Unified platforms also enable predictive analytics that link compensation changes to attrition risk, a capability McKinsey identified as critical for retaining high performers. By resolving operational pain points and enabling strategic insights, integrated suites materially expand the addressable user base.

Workforce Analytics and AI for Strategic HR

Real-time analytics ingest performance, engagement, and skills data to flag succession gaps before they disrupt operations. ADP Assist, introduced in September 2025, offers conversational queries that compress report creation from hours to seconds. Workday’s AI Agent Partner Network lets third-party agents execute benefits enrollment or PTO approvals, lowering HR ticket volumes by up to 40% in early pilots. Predictive attrition models enable interventions 60-90 days before voluntary exits, delivering measurable savings in replacement costs. As analytics migrate from descriptive to prescriptive, HR shifts from record-keeping to proactive workforce shaping, strengthening the growth trajectory of the human capital management software market.

Compliance Mandates for Global Payroll and Taxation

Governments are digitizing tax and employment regulations, forcing enterprises to modernize payroll engines. India’s GST e-invoicing and monthly reconciliations, China’s province-specific social-insurance matrices, and the EU AI Act’s bias-audit rules all raise the penalty of non-compliance. PwC’s 2025 global payroll survey found 72% of multinationals incurred at least one payroll penalty, averaging USD 250,000 in the prior 24 months. Embedding regulatory intelligence into HCM platforms mitigates these risks, sustaining premium pricing and adoption across regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity and Data Privacy Concerns | -1.4% | Global, with heightened impact in Europe and North America due to GDPR and CCPA enforcement | Short term (≤ 2 years) |

| Legacy Migration Cost and Complexity | -1.1% | Global, particularly in large enterprises with on-premises systems in North America and Europe | Medium term (2-4 years) |

| Low End-User Adoption of Complex Suites | -0.8% | Global, with higher impact in SMEs and emerging markets | Medium term (2-4 years) |

| Algorithmic Bias Litigation Risk Restricts Roll-outs | -0.6% | North America and Europe, with emerging regulatory scrutiny in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security and Data-Privacy Concerns

HCM platforms store sensitive personal and compensation information, making them prime targets for ransomware. The Cleo breach in December 2024 exposed payroll records at multinational employers and highlighted vulnerabilities in third-party file-transfer tools. GDPR and CCPA fines can reach hundreds of millions, exemplified by Meta’s EUR 1.2 billion (USD 1.41 billion) penalty in 2023, increasing buyer scrutiny of vendor controls.[3]Financial Times, “Meta Fined EUR 1.2 Billion for GDPR Violations,” ft.com Enterprises now demand zero-trust architectures, multifactor authentication, and encryption at rest and in transit as baseline requirements, raising development costs for smaller suppliers and slowing procurement cycles.

Legacy Migration Cost and Complexity

Moving from heavily customized on-premises suites to cloud platforms can last 12-18 months and cost USD 5-10 million for companies with over 10,000 employees. Custom business rules often clash with standardized cloud data models, forcing painful trade-offs between process redesign and customization. Deloitte reported that 43% of firms delayed or abandoned projects after underestimating integration workloads. The financial burden extends to training, consultant fees, and productivity dips during cutovers, dampening near-term adoption rates even as long-term benefits remain clear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Payroll Still Dominates, Learning Accelerates

Payroll management accounted for the largest slice of 2025 revenue at 43.78%, a position underpinned by increasingly complex tax codes, social-insurance mandates, and real-time filing obligations. Deel’s automation of USD 22 billion in annual payroll across 150 nations shows why enterprises prioritize platforms that embed local statutory logic and currency conversion at scale. The human capital management software market share of payroll reflects the direct financial penalties tied to pay inaccuracies. Meanwhile, learning and development advanced at a 9.72% CAGR, the quickest among solution segments, as McKinsey recorded 87% of executives facing critical skills shortages. Workday’s USD 1.1 billion Sana acquisition in November 2025 integrated AI-driven knowledge management, enabling upskilling paths to adapt to employees' proficiency in real time.

The convergence trend blurs traditional solution lines. Talent modules now tap payroll data to correlate compensation shifts with attrition risk, while workforce management engines integrate learning records to verify compliance with training requirements. ADP Workforce Suite bundles payroll, time tracking, and benefits in a single subscription to eliminate reconciliation delays and lower the total cost of ownership for mid-market buyers. As vendors package once-discrete functions into cohesive workflows, buyers judge offerings by the breadth of embedded intelligence rather than module count, a dynamic that will keep the human capital management software market growing above GDP levels through 2031.

By Deployment: Cloud Momentum Outpaces On-Premise Holdouts

On-prem deployments still accounted for 55.83% of 2025 spending, chiefly in BFSI and government organizations that cite data-sovereignty and audit-trail mandates. Yet cloud subscriptions are projected to rise at a 9.11% CAGR through 2031 as ISO 27001 and SOC 2 Type II certifications foster trust across regulated sectors. Workday Data Cloud’s real-time API access eliminates the batch latency of legacy ETL processes, enabling finance, supply chain, and HR teams to operate from a common dataset without local servers. Deloitte’s 2025 survey revealed that 68% of cloud adopters valued weekly innovation cycles above cost savings, indicating a strategic, not merely economic, rationale for migration.

Hybrid models offer a transition path, with companies anchoring statutory payroll on-premises while shifting talent and learning modules to the cloud. Vendors are responding by localizing data centers to comply with GDPR and CCPA rules, even though such expansion increases infrastructure expenses by 20-30%. As compliance engines and AI copilots are released cloud-first, on-premises lag will widen, incentivizing late adopters to re-evaluate risk-reward trade-offs. These dynamics reinforce the long-term tilt toward subscription revenue streams in the human capital management software market.

By Organization Size: SMEs Close the Functionality Gap

Large enterprises accounted for 62.17% of spending in 2025, reflecting multi-country complexity, union rules, and advanced role-based access controls. However, SMEs are forecast to expand at a 9.04% CAGR, driven by subscription pricing that removes upfront license fees and compresses implementation to weeks. ADP Workforce Suite targets firms with fewer than 1,000 employees with predictable per-employee-per-month plans that align costs with headcount. Deel surpassed USD 1 billion in annual recurring revenue in 2025 by serving 37,000 companies seeking multi-country hiring compliance, proving that SMEs value global reach as much as local functionality.

Rippling’s USD 450 million raise in May 2025 highlighted the appetite for platforms that merge payroll, benefits, IT provisioning, and device management, allowing small teams to replace five-plus-point solutions. Vendors now deliver self-service configuration wizards, intuitive user interfaces, and template workflows that reduce reliance on consultants. As a result, adoption barriers linked to usability and change management are falling, widening the opportunity pool for the human capital management software market among resource-constrained organizations.

By Industry Vertical: Financial Controls Drive BFSI Spend, Skills Gaps Propel Healthcare

Banking, financial services, and insurance (BFSI) captured 22.89% of 2025 revenue because Basel III, Dodd-Frank, and MiFID II rules mandate audit trails that connect compensation decisions to risk frameworks. Automated payroll engines simplify variable pay calculations and deferral schedules that traditional spreadsheets cannot manage at scale. Conversely, healthcare is the fastest-growing vertical, with a 10.93% CAGR, but is pressured by nursing shortages that exceeded 200,000 vacancies in 2024, according to the American Hospital Association. Workforce management modules optimize shift scheduling, track license expirations, and flag credential gaps to avoid regulatory fines.

IT and telecom firms deploy learning systems to combat rapid tech skill obsolescence, while manufacturers adopt HCM suites to manage collective bargaining clauses and safety-training compliance. Retail relies on demand-driven labor forecasting to staff stores efficiently during peak periods. Government adoption skews toward on-premises or open-source stacks to address sovereignty and budget constraints, slowing cloud adoption relative to private-sector peers. These differentiated needs ensure that the human capital management software market continues to diversify its feature roadmaps by vertical.

Geography Analysis

North America accounted for 37.62% of 2025 revenue, driven by high labor costs, mature SaaS penetration, and an active regulatory landscape that fosters continuous platform upgrades. The region’s buyers quickly embrace AI copilots to reduce manual HR workloads and speed insight generation. Europe follows closely, but GDPR-driven data-localization obligations force vendors to operate regional data centers and invest in advanced encryption, elevating the total cost of ownership. The EU AI Act, effective in August 2024, further distinguishes the market by requiring bias audits and explainability reports, thereby raising barriers to entry for newcomers.

Asia-Pacific is set to lead with a robust 9.61% CAGR growth rate through 2031. This surge is driven by India's push for GST digitization, the introduction of province-level social-insurance grids in China, and Japan's new overtime limits, all of which heighten payroll complexities. Local players like Ramco Systems are capitalizing on this trend, adapting indigenous payroll rules across over 45 countries. Their efforts ensure cultural resonance and compliance, making them a preferred choice for regional clients.

Middle East and Africa uptake clusters in Gulf Cooperation Council economies, where expatriate workforce management and nationalization programs require multi-currency payroll and visa-tracking features. South America faces currency volatility and frequent tax rule changes, making real-time compliance intelligence critical. Together, these regional catalysts push the human capital management software market beyond its historical strongholds and diversify revenue streams.

Competitive Landscape

The competitive field blends entrenched enterprise vendors with high-growth startups. SAP, Oracle, and Workday protect extensive installed bases by embedding generative-AI features across modules and pursuing targeted acquisitions. Workday’s November 2025 purchase of Sana for USD 1.1 billion added AI knowledge management, while its pending buyout of Pipedream extends agent-based workflow automation. ADP countered by launching Workforce Suite and introducing ADP Assist to fuse conversational analytics with anomaly detection. Oracle’s October 2025 white paper comparing Fusion Cloud HCM AI to peers highlighted heightened feature-parity battles.

Disruptors leverage API-first design and remote-first hiring trends. Deel and Rippling secured over USD 750 million combined funding in 2025, packaging payroll, benefits, and IT administration at pricing that undercuts legacy stacks by up to 40%. White-space opportunities revolve around multi-country payroll for SMEs, skills-based workforce planning, and algorithmic bias mitigation tools aligned with new regulations.

Regional data center presence, embedded security certifications, and self-service configurations that reduce consulting expenses now define technological differentiation. These factors enable businesses to enhance operational efficiency, ensure data security, and minimize reliance on external consulting services. In light of these trends, the human capital management software market has become a competitive arena where the pace of innovation frequently eclipses the weight of brand legacy, compelling companies to continuously adapt and innovate to maintain their market position.

Human Capital Management Software Industry Leaders

SAP SE

Oracle Corporation

Workday Inc.

ADP LLC

Ultimate Kronos Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Workday completed its USD 1.1 billion acquisition of Sana, adding AI-powered knowledge management to its learning suite.

- November 2025: Workday agreed to acquire Pipedream, an AI agent connectivity platform that automates benefits enrollment, PTO approvals, and onboarding tasks.

- November 2025: ADP launched Workforce Suite, bundling payroll, time, benefits, and talent for organizations under 1,000 employees with subscription pricing.

- October 2025: Deel closed a USD 300 million Series E round at a USD 17.3 billion valuation, surpassing USD 1 billion in annual recurring revenue.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Human Capital Management (HCM) software, as defined by our study, covers licensed or subscription-based platforms that digitize core HR records, payroll, talent, learning, workforce management, and analytics for employees, contractors, and contingent staff across every industry. Revenues reflect new license sales, SaaS fees, and maintenance tied to these modules.

Scope exclusion: Advisory services, standalone payroll outsourcing, and one-off customization projects are not counted.

Segmentation Overview

- By Solution

- Payroll Management

- Talent Management

- Workforce Management

- Core HR Administration

- Learning and Development

- By Deployment

- On-Premise

- Cloud

- By Organization Size

- Large Enterprises

- Small and Medium Enterprises

- By Industry Vertical

- IT and Telecom

- Banking, Financial Services, and Insurance (BFSI)

- Manufacturing

- Healthcare

- Retail and E-Commerce

- Government and Public Sector

- Other Industry Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with product leaders at global HCM vendors, regional payroll specialists, systems integrators, and HR heads from manufacturing, BFSI, retail, and healthcare firms across North America, Europe, Asia-Pacific, and the GCC. These conversations filled data gaps on contract values, module mix, and cloud migration rates that open sources left unclear.

Desk Research

We mapped publicly available, high-authority datasets such as World Bank ICT spend, U.S. Bureau of Labor Statistics employer counts, Eurostat cloud-use surveys, and customs filings that detail enterprise software imports. Insights from IEEE journals, HR Tech Alliance white papers, and national labor-law portals clarified adoption triggers and compliance catalysts. Subscription resources, D&B Hoovers for vendor revenues, Dow Jones Factiva for deal flow, and Questel for patent velocity, let us benchmark supplier reach and innovation pace, anchoring regional splits and pricing ranges. The sources named are illustrative; many additional records were reviewed to verify consistency and scope.

Market-Sizing & Forecasting

A single top-down build converts employer head counts and per-employee HCM spend into an initial demand pool, which is then balanced against sampled supplier bookings to refine totals. Key variables like SaaS price bands, cloud HR penetration, mid-market hiring trends, regional GDP growth, regulatory deadlines, and exchange rates feed a multivariate regression that projects values to 2030. Where supplier roll-ups are thin, interview-based channel ratios bridge the gap.

Data Validation & Update Cycle

Outputs face algorithmic anomaly checks, peer review, and senior sign-off. Models refresh every year, with interim updates triggered by major M&A moves, new payroll mandates, or sudden currency swings.

Why Mordor's Human Capital Management Software Baseline Earns Confidence

Published estimates vary because firms select different module sets, base years, and refresh cadences.

Key gap drivers include narrower scope at some publishers, reliance on vendor press releases without field checks, and older baselines that miss 2024 cloud price resets.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 43.02 B (2025) | Mordor Intelligence | - |

| USD 34.12 B (2025) | Global Consultancy A | Excludes workforce analytics, uses press-release revenues, biennial updates |

| USD 27.5 B (2024) | Industry Forecasting House B | Tracks only core HR, employs top-down only, minimal primary validation |

The comparison highlights how Mordor's balanced variable set and annual refresh give decision-makers a clearer, reproducible baseline.

Key Questions Answered in the Report

How large is the human capital management software market in 2026?

The human capital management software market size is USD 46.92 billion in 2026 with an 8.67% CAGR outlook to 2031.

Which segment leads revenue among HCM solutions?

Payroll management captured 43.78% of 2025 revenue due to rising multi-jurisdictional compliance demands.

Why is Asia-Pacific expected to outpace other regions?

India’s GST digitization, China’s province-level social-insurance rules, and Japan’s labor shortages raise demand for automated payroll and workforce management, driving a 9.61% CAGR through 2031.

What factors restrain rapid cloud adoption?

Cybersecurity concerns and the high cost of migrating customized on-premises systems slow some enterprises from moving to cloud subscriptions.

How are vendors responding to new AI regulations?

Leading suppliers embed bias-audit tools, explainability reports, and regional data centers to comply with the EU AI Act and similar statutes.

Which customer segment is growing fastest?

Small and medium enterprises are expanding adoption at a 9.04% CAGR as subscription pricing lowers upfront costs and self-service tools simplify deployment.

Page last updated on: