Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

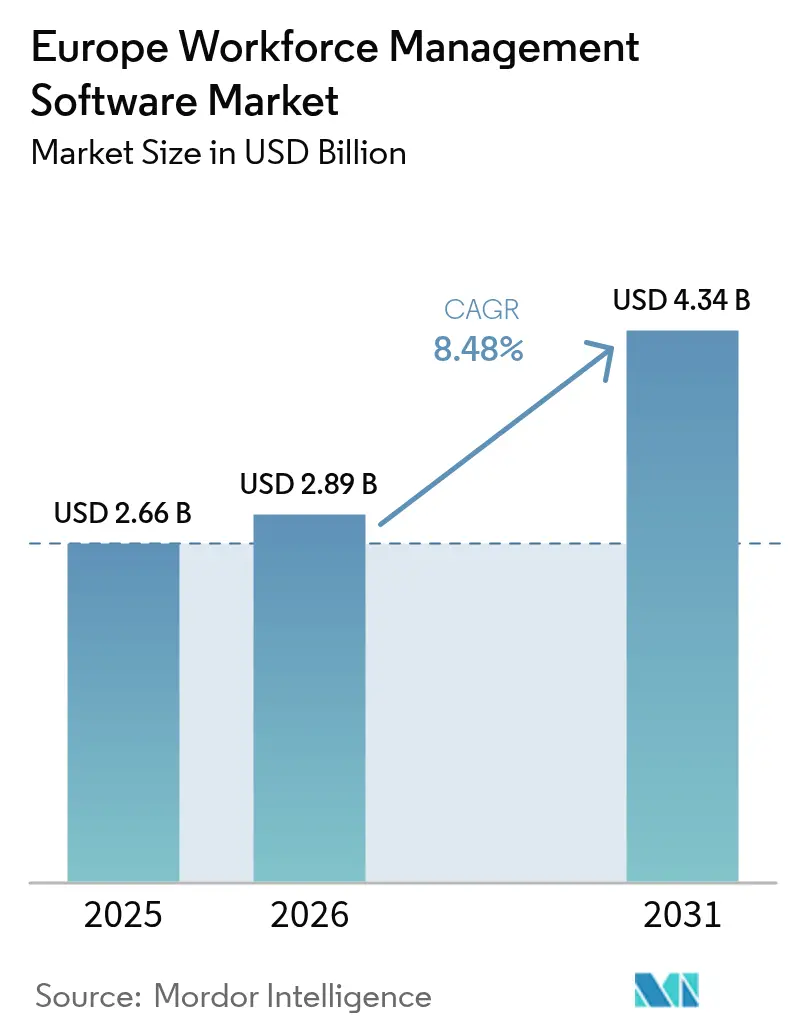

| Base Year Market Size (2025) | USD 2.66 Billion |

| Market Size (2026) | USD 2.89 Billion |

| Market Size (2031) | USD 4.34 Billion |

| Growth Rate (2026 - 2031) | 8.48% CAGR |

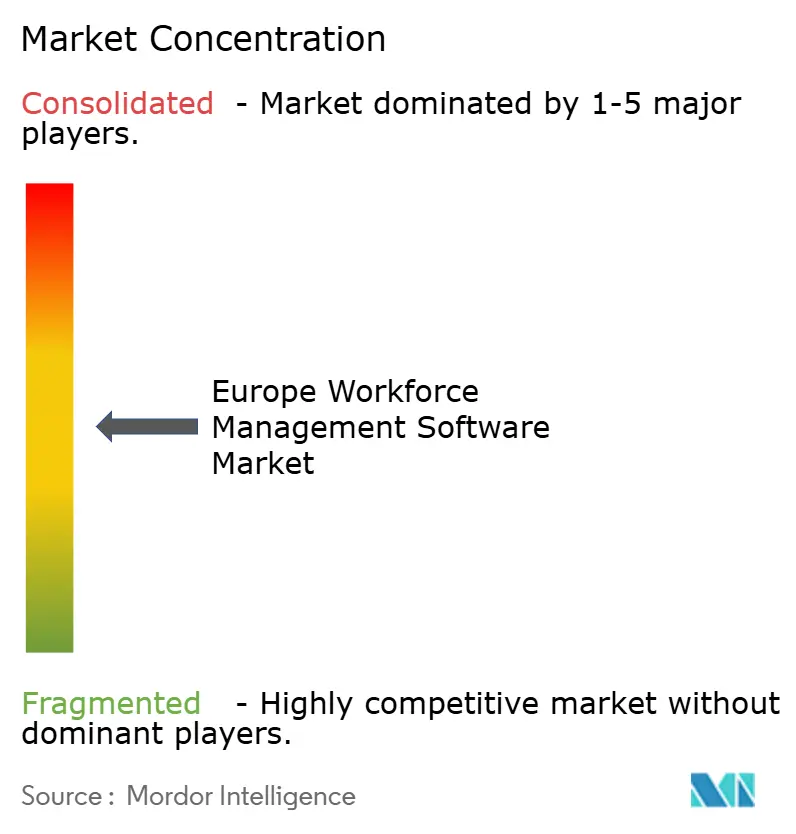

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Workforce Management Software Market Analysis by Mordor Intelligence

The Europe Workforce Management Software Market size in 2026 is estimated at USD 2.89 billion, growing from 2025 value of USD 2.66 billion with 2031 projections showing USD 4.34 billion, growing at 8.48% CAGR over 2026-2031.

Growth is propelled by the region’s digital transformation agenda, mounting regulatory obligations, and the need to manage labor costs in tight labor markets. The 2019 European Court of Justice ruling that mandates objective time-tracking elevated workforce management from convenience to compliance. Cloud deployments dominate as mid-market employers move off legacy systems, while artificial-intelligence (AI) modules advance labor forecasting and scheduling accuracy. Consolidation among software vendors is accelerating as enterprise-resource-planning (ERP) providers acquire specialized platforms to deliver integrated human-capital suites. Country-level dynamics are equally influential: the United Kingdom leads adoption, Italy records the fastest growth, and Germany’s manufacturing sector drives specialized energy-aware scheduling solutions.

Key Report Takeaways

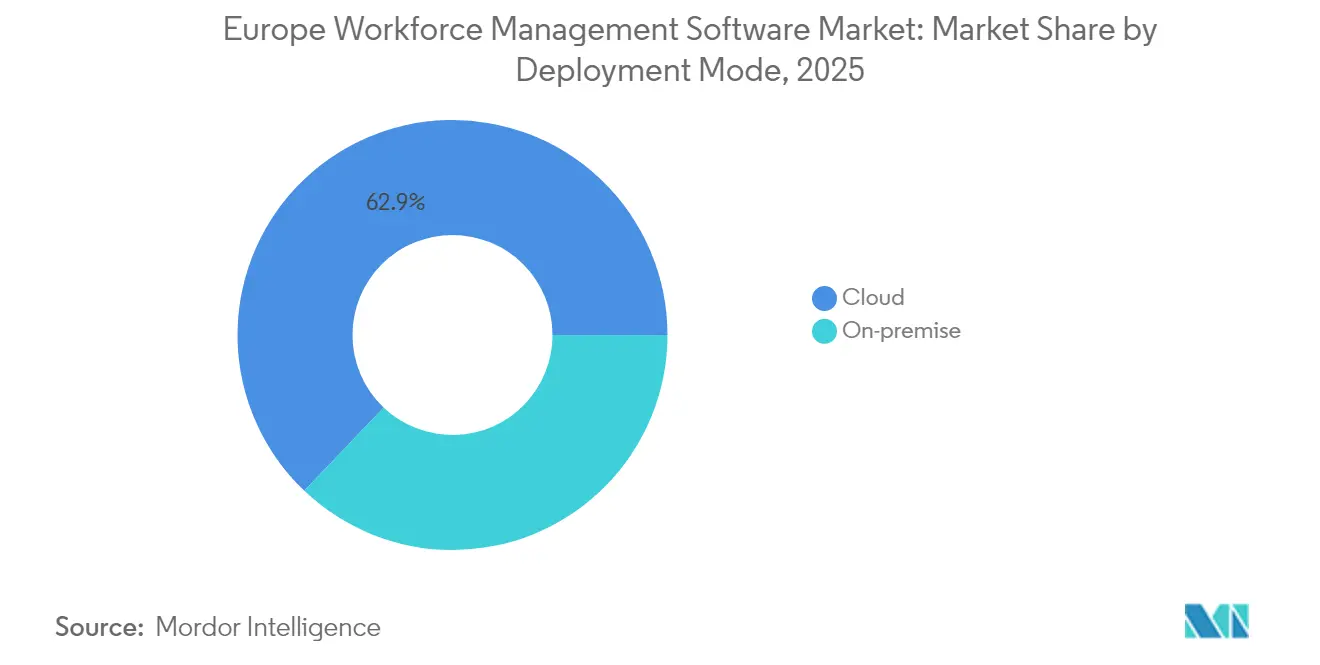

- Cloud deployment captured 62.90% of Europe workforce management software market share in 2025, while the segment is set to grow at an 11.17% CAGR to 2031.

- Small and medium enterprises recorded the highest projected CAGR at 10.63% through 2031, although large enterprises held 54.60% of the Europe workforce management software market size in 2025.

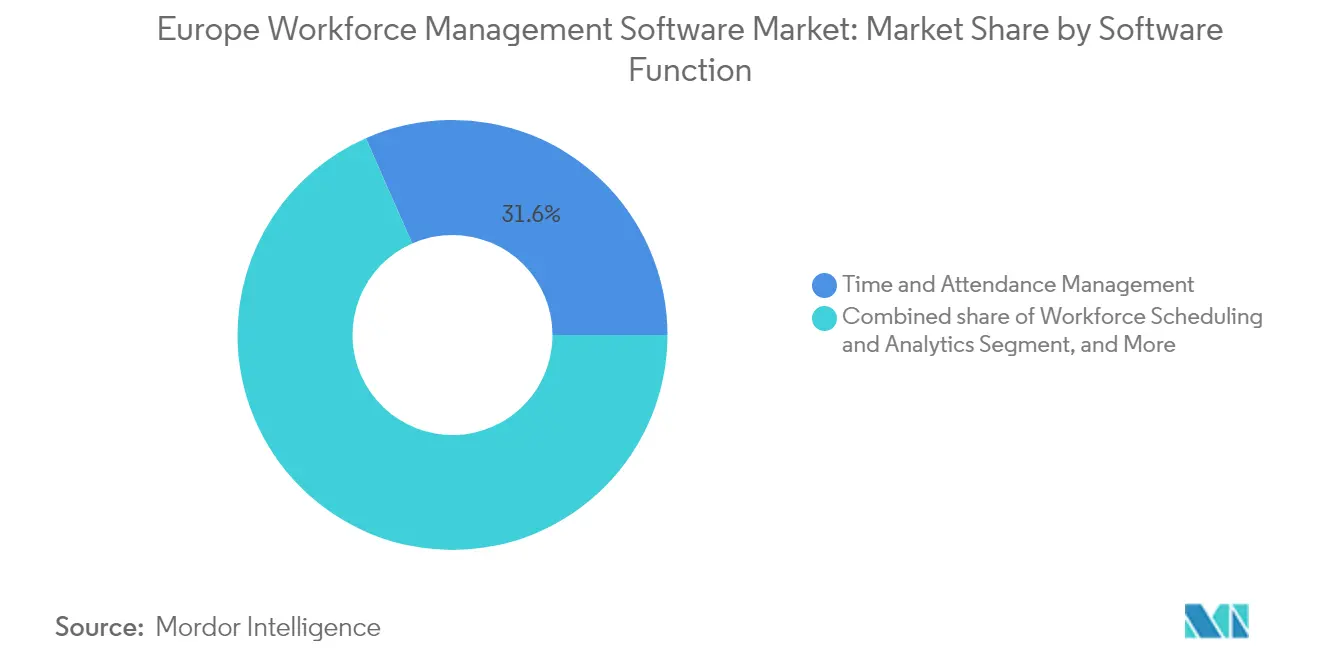

- Workforce scheduling and analytics advanced at a 13.35% CAGR, whereas time and attendance management retained 31.60% of the Europe workforce management software market share in 2025.

- Healthcare is forecast to expand at a 9.66% CAGR, while Banking, Financial Services, and Insurance contributed 24.20% revenue share in 2025.

- By geography, the United Kingdom led with 22.40% revenue share in 2025, whereas Italy is expected to grow at an 8.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Workforce Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first migrations among mid-market employers | +2.1% | Pan-European; strongest in UK and Germany | Medium term (2-4 years) |

| AI-driven labor forecasting and scheduling adoption | +1.8% | UK, Germany, France, Netherlands | Long term (≥ 4 years) |

| EU Working-Time-Directive compliance automation | +1.5% | All EU member states | Short term (≤ 2 years) |

| Algorithmic scheduling for energy-cost optimization | +1.2% | Germany, Italy, Spain | Medium term (2-4 years) |

| Worker well-being and fatigue analytics integration | +0.9% | Healthcare and transportation sectors | Long term (≥ 4 years) |

| Generative-AI assistants for frontline managers | +0.7% | UK, France, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Migrations Among Mid-Market Employers

Mid-market firms are abandoning on-premise installations for cloud platforms that offer rapid scalability, integrated security, and real-time visibility across multiple sites [1]Workday, “Retail Customer Stories eBook,” workday.com. companies lead the shift, with one-third of mid-size enterprises already live on cloud systems by 2025. Lower total cost of ownership cut by more than one-third over five years further accelerates movement away from self-hosted servers. Vendors that lack cloud-native architectures face erosion of Europe workforce management software market share as subscription models become the norm. The migration also raises the bar for service-level expectations, including continuous feature updates and zero-downtime releases.

AI-Driven Labor Forecasting and Scheduling Adoption

AI modules elevate scheduling from reactive roster management to predictive optimization. Machine-learning models ingest historical demand, seasonal trends, and external factors such as local events to reach forecast accuracy above 80% in controlled pilots. Retailers and logistics operators report 20-30% productivity gains when AI recommendations are coupled with human oversight. Despite accuracy improvements, enterprises still allocate resources for data-quality audits and manual overrides, highlighting the need for robust training data pipelines before full automation. AI adoption acts as a stepping-stone toward conversational assistants that let frontline managers revise rosters by voice or chat.

EU Working-Time-Directive Compliance Automation

Full enforcement of the Working Time Directive in July 2024 created unprecedented demand for solutions that automatically record hours, rest periods, and overtime. Approximately 200 million employees fall under the directive, forcing companies to embed compliance checks into daily operations. Modern platforms now trigger real-time alerts when scheduled shifts risk breaching national limits, reducing legal exposure while tightening payroll accuracy. Compliance functionality also drives adoption among export-oriented manufacturers where labor-audit readiness is a prerequisite for international contracts.

Algorithmic Scheduling for Energy-Cost Optimization

Volatile power prices, particularly in energy-intensive manufacturing, spur interest in scheduling engines that align labor-heavy tasks with low-tariff periods. German factories using algorithmic scheduling cut energy-related operating costs by up to 20% while preserving throughput. Platforms integrate real-time utility prices and renewable-availability forecasts, enabling automatic shift rescheduling that balances worker availability, skill needs, and production deadlines. This dual focus on cost efficiency and sustainability lifts the attractiveness of advanced workforce management tools in heavy industry.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR-driven data-sovereignty concerns | -1.4% | Germany and France most affected | Short term (≤ 2 years) |

| Complex legacy ERP/WFM integration costs | -1.1% | Large enterprises across Europe | Medium term (2-4 years) |

| Union push-back on opaque scheduling algorithms | -0.8% | Germany, France, Belgium | Medium term (2-4 years) |

| Shortage of certified WFM implementation talent | -0.6% | Nordic markets and Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GDPR-Driven Data-Sovereignty Concerns

Strict interpretation of GDPR elevates compliance costs as firms must prove lawful bases for processing location, biometric, and behavioral data[2]European Agency for Safety and Health at Work, “The Rise of AI-Based Worker Management Systems: What’s in It for OSH?,” osha.europa.eu. In Germany and France, data-protection authorities impose heavy fines for cross-border transfers lacking explicit consent, lengthening implementation cycles by as much as one year. Vendors respond with regional data centers and privacy-by-design architectures, yet these measures drive up development expenses and delay new features, tempering the overall expansion of the Europe workforce management software market.

Complex Legacy ERP/WFM Integration Costs

Large manufacturers frequently deploy customized ERP landscapes that date back decades. Connecting modern workforce management modules to those systems demands bespoke middleware and prolonged testing, pushing project costs 40–60% above budget. Extended timelines favor incumbent ERP vendors that bundle pre-built connectors, raising entry barriers for specialist providers. For buyers, integration risk often overshadows feature considerations, slowing decisions and shrinking near-term demand growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Dominance Accelerates

Cloud deployment accounted for 62.90% of Europe workforce management software market size in 2025 and is on track to grow at an 11.17% CAGR through 2031. Rapid rollouts, automatic updates, and subscription pricing resonate strongly with organizations seeking to conserve capital and ensure regulatory compliance across multiple jurisdictions. Mid-market firms drive adoption, yet large enterprises increasingly migrate individual business units to cloud instances as part of wider digital-transformation programs.

On-premise installations persist within highly regulated sectors and entities with stringent data-sovereignty mandates. These users value direct control over data storage and system customization, but growth remains limited because hardware refresh cycles and skilled in-house support inflate lifetime costs. Hybrid models are emerging as a transition strategy, allowing sensitive data to stay on-site while analytics and mobile access run in the cloud.

By Organization Size: SME Growth Outpaces Enterprises

Large enterprises generated 54.60% of Europe workforce management software market revenue in 2025, reflecting complex scheduling, payroll, and compliance requirements that span multiple geographies. Consolidated suites tie workforce modules to broader human-capital, payroll, and finance systems, locking in vendor relationships for years. As digital strategies mature, upgrades center on AI analytics rather than wholesale platform replacement.

Small and medium enterprises delivered a 10.63% CAGR outlook to 2031. Cloud availability and pay-as-you-go pricing have removed prohibitive upfront fees, democratizing access to enterprise-grade functionality. SME buyers, pressured by rising wage bills and complex overtime regulations, adopt workforce tools to cut administrative overhead and keep audit-ready records—capabilities previously out of reach.

By Software Function: Analytics Drive Innovation

Time and attendance management held 31.60% of Europe workforce management software market share in 2025, underscoring its role as the data backbone for payroll accuracy and compliance reporting. However, workforce scheduling and analytics posted the highest 13.35% CAGR to 2031, signaling a shift from static record-keeping toward predictive optimization. Analytics engines that forecast staffing needs, detect absence trends, and flag compliance breaches elevate labor planning from a cost center to a strategic lever for service differentiation.

Performance and goal management, absence and leave management, and task or fatigue management remain niche but are gaining ground in healthcare and transportation, where safety and staff well-being are regulated performance indicators.

By End-User Industry: Healthcare Acceleration

Banking, Financial Services, and Insurance (BFSI) contributed 24.20% revenue share in 2025 as financial institutions juggle regulatory oversight, service-level guarantees, and multi-time-zone staffing. Continuous certification tracking and branch-level scheduling further intensify adoption.

Healthcare is projected to expand at a 9.66% CAGR, the fastest within end-user segments. Post-pandemic staffing shortages, mandated nurse-to-patient ratios, and growing emphasis on clinician well-being raise the stakes for precision scheduling. Manufacturers, retailers, logistics operators, and hospitality brands each leverage specialized modules that accommodate seasonal peaks, skill-based assignments, or union agreements.

Geography Analysis

The United Kingdom led with 22.40% of Europe workforce management software market share in 2025, supported by a mature cloud ecosystem and stringent service-sector compliance requirements. Brexit-driven labor scarcity compels firms to optimize productivity using AI scheduling and mobile self-service.

Italy is positioned for an 8.28% CAGR through 2031 as government digitization incentives and EU structural funding spark adoption among industrial mid-caps. Germany, France, Spain, the Netherlands, Belgium, and the Nordic region each demonstrate distinctive patterns shaped by labor law, union influence, and sectoral composition.

Regulatory Landscape

EU compliance requirements continue to shape product design for workforce management software, particularly for time tracking, scheduling, and analytics that touch employee monitoring and decision-making. The 2019 European Court of Justice ruling on objective time recording remains a foundational compliance driver, and GDPR (Regulation (EU) 2016/679) governs the handling of employee data such as location and biometric identifiers; GDPR Article 88 allows Member States to set additional employee-data rules, creating cross-country fragmentation that vendors must address through localized configurations and data-residency options.

Regulation (EU) 2024/1689 (EU AI Act) adds a new layer for AI-enabled workforce tools: AI systems used in employment and worker management are categorized as high-risk, increasing obligations around governance, documentation, logging, and human oversight for deployers and providers. In parallel, Directive (EU) 2024/2831 (Platform Work Directive) strengthens rights around algorithmic management for platform workers, with Member States required to transpose the directive by 2 December 2026, reinforcing transparency and human review expectations for automated monitoring and decision-making features that also appear in modern workforce management platforms.

Value Chain Analysis

The value chain starts with platform vendors (specialists and ERP/HCM suite providers) building core modules such as time and attendance, scheduling, and analytics, then layering AI capabilities and sector-specific compliance packs. Delivery commonly relies on cloud and hosting infrastructure, implementation partners (systems integrators and regional consultancies), and connectivity into adjacent enterprise systems, especially payroll and HR suites (for example, SD Worx and other regional payroll providers, alongside ERP ecosystems). Distribution is largely direct enterprise sales for large accounts, with channel-led and app-marketplace-led routes for mid-market buyers who prioritize pre-built integrations and faster rollouts.

Integration and compliance represent the primary bottlenecks across the chain. Buyers frequently demand certified connectors to legacy ERP, payroll, and identity systems, while GDPR-driven data-sovereignty and evolving algorithmic management requirements push vendors and cloud partners toward regional data-center strategies and privacy-by-design controls. This increases the relative influence of infrastructure and integration partners and raises switching costs, favoring suppliers that package workforce management with broader HCM and payroll capabilities or maintain robust APIs and integration tooling.

Competitive Landscape

Competitive Landscape

The Europe workforce management software market is moderately fragmented. Global ERP vendors such as SAP, Oracle, and Workday leverage integrated suites to cross-sell scheduling modules into payroll and human-capital installations. Specialized providers like Quinyx, ATOSS, and Tamigo differentiate through vertical templates and mobile-first interfaces. Competition increasingly centers on AI capabilities, API openness, and real-time analytics rather than feature checklists.

Consolidation is accelerating. ADP’s USD 1.2 billion purchase of WorkForce Software in October 2024 married global payroll coverage with advanced scheduling algorithms. Private-equity investors are also active: GFOS secured growth capital from The Riverside Company to scale its cloud footprint across German-speaking markets.

Product roadmaps highlight conversational AI, embedded analytics, and sector-specific compliance packs. Vendors race to release generative-AI assistants that draft schedules, answer HR queries, and surface compliance warnings using natural language. Open-ecosystem strategies are favored, as mid-market buyers require plug-and-play integrations with payroll, learning, and financial applications already in place.

Europe Workforce Management Software Industry Leaders

Oracle Corporation

IBM Corporation

Automatic Data Processing, Inc. (ADP)

Calabrio, Inc.

Infor Global Solutions, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-led feature demand creates whitespace for vendors that can operationalize transparent, auditable workforce AI. The EU AI Act classification of employment and worker-management AI as high-risk and the Platform Work Directive transposition deadline of 2 December 2026 elevate demand for productized controls, such as human-in-the-loop workflow design, worker notifications, automated logs, and configurable policy rules that map to country-specific labor and employee-data requirements under GDPR Article 88. Vendors with strong compliance packs and data-residency options gain differentiation as cross-border deployments face heightened scrutiny in Germany and France.

SME modernization and AI-enabled scheduling remain under-penetrated areas, particularly for predictive analytics and workforce optimization in firms with fewer than 250 employees. Market activity in adjacent European enterprise operations supports this opportunity: July 2026 reporting around Deutsche Telekom scaling ChatGPT Enterprise internally underscores the broader shift toward embedding AI in day-to-day operational workflows, which increases demand for workforce management products with API-first integration, packaged connectors, and interoperable analytics across HCM, payroll, and operational systems.

Recent Industry Developments

- May 2026: Deutsche Telekom scaled ChatGPT Enterprise internally, signaling deeper AI integration in enterprise operations and potential demand for AI-enabled workforce management features. The move demonstrates enterprise appetite for AI-enabled workflows that can be governed and audited across large multi-country teams, potentially boosting adoption of integrated scheduling, time and attendance, and analytics tools.

- June 2026: Cognizant selected Oracle Fusion Cloud Recruiting to support AI-driven talent acquisition for its global workforce. The win strengthens Oracle's footprint in cloud HCM and adjacent workforce workflows, improving integration opportunities for enterprise-wide workforce management modules in multi-country setups.

- November 2025: ADP announced availability of ADP WorkForce Suite integrated within ADP Workforce Now, ADP Lyric HCM, and ADP Global Payroll, extending unified workforce management capabilities across its HCM platforms. The rollout reduces procurement and integration complexity for buyers standardizing time, attendance, and scheduling across multiple countries.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers software used by employers in Europe to plan, schedule, track, and analyze workforce time and labor activities, and to support compliance and productivity reporting. Values are captured as software revenue generated within Europe across deployment types and user organizations.

Scope exclusions: We exclude pure staffing and recruitment tools, standalone payroll processing, and general HR suites where workforce management features are not sold or priced as a distinct software offering.

Segmentation Overview

- By Deployment Mode

- On-premise

- Cloud

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By Software Function

- Workforce Scheduling and Analytics

- Time and Attendance Management

- Performance and Goal Management

- Absence and Leave Management

- Task / Fatigue Management

- By End-User Industry

- Healthcare

- BFSI

- Manufacturing

- Consumer Goods and Retail

- Transportation and Logistics

- Hospitality

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Belgium

- Nordics (Sweden, Norway, Denmark, Finland)

- Rest of Europe (Austria, Portugal, etc.)

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting frame for Europe demand, supply, and adoption patterns before the assumptions were stress-tested inside the sizing model. We leaned on public sources such as Eurostat labor statistics, European Commission policy and digital economy releases, national statistics offices, and OECD labor productivity series to understand employment mix, shift-heavy industries, and macro sensitivity.

To anchor the vendor and pricing context, we reviewed company annual reports, regulatory filings, investor presentations, and credible press coverage on cloud transitions and subscription pricing. Patent databases were used selectively to track feature direction (for example, scheduling optimization and analytics) so the feature scope stays consistent year to year. Where needed, a paid subscription for company financials and a news and financials database helped cross-check revenue disclosures and major contract signals. These sources are illustrative, and many other public and paid references were also used to collect data, validate it, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on validating what is actually being bought in Europe, and how pricing and adoption differ by country, company size, and industry. We spoke with a mix of software providers, implementation partners, and enterprise buyers across major European economies so the desk assumptions on modules, cloud mix, and typical contract values could be adjusted where they did not fit observed market behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | |

| Mid tier: 53% | Functional/Unit leaders: 30% | |

| Smaller Players: 19% | Managers: 57% |

Market-Sizing & Forecasting

The sizing starts with a top-down demand pool reconstruction based on Europe employment levels and the share of workers in shift-led and regulated environments, which then gets filtered through software adoption rates for workforce scheduling, time and attendance, absence management, and analytics. Those adoption rates and average contract values were adjusted by country maturity, cloud penetration, and typical buying units (per employee per month subscriptions versus enterprise licenses).

To keep the totals realistic, selective bottom-up checks were run using a sample roll-up of vendor revenues tied to Europe exposure, channel feedback on deal sizes, and ASP x user-count approximations for common buyer profiles. Key model inputs included sector employment in retail, healthcare, manufacturing, and logistics, replacement cycles for legacy on-premise deployments, cloud subscription mix, average seats per customer by company size, and compliance-driven purchase triggers linked to working time tracking and reporting requirements. For forecasting, we relied on scenario analysis supported by expert views on budget growth, cloud migration pace, and tightening labor availability, and then the trajectory was smoothed so that one-off spikes from large tenders did not distort the long-term curve. When bottom-up signals were missing for smaller countries, gaps were handled through peer-country benchmarks based on similar industry mix and digital adoption.

Data Validation & Update Cycle

Validation is done through multiple checks so the final numbers stay tied to observable market signals. Model outputs are compared with independent indicators such as cloud software spending direction, vendor pipeline commentary, and cross-country adoption patterns, and then outliers are investigated before the estimates move to internal review.

If a country-level result looks inconsistent with employment structure or typical pricing, we re-check assumptions, revisit interview notes, and, when needed, re-contact sources to clarify the point of variance. Each report is refreshed annually, and interim updates are made when material events occur such as major regulatory changes, pricing shifts, or large-scale vendor consolidation. Before delivery, a final analyst pass is completed so clients receive the most current view available at the time of publication.

Mordor Intelligence's Europe Workforce Management Software Market Market Size Compared With Other Published Estimates

Published market sizes for Europe workforce management software often do not match because the boundary is set differently and the inputs are not built from the same demand pool. Differences also show up when some sources mix software with services, include broader workforce management categories beyond software, or use a different base year and currency timing.

In practice, the largest gaps usually come from what is counted as workforce management software modules, how cloud subscription revenue is annualized, and whether country coverage goes beyond the largest economies into the rest of Europe. Pricing logic also shows up in blended ASP approaches, since per-employee pricing and enterprise licensing behave differently across buyer sizes and industries, which can shift the 2025 market size even when the overall growth story looks similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.66 B (2025) | |

| Industry Data Publisher A | USD 2.27 B (2025) | Uses a broader workforce management scope that can blend software with related service and technology layers, and the base-year value is not clearly reconciled back to module-level subscription annualization. |

| Regional Consultancy B | USD 2.72 B (2025) | Leans on a higher assumed cloud and analytics attach rate across Europe, and it appears to apply a more aggressive average pricing path without consistent buyer-size normalization by country. |

Vendor revenue signals and Europe-wide adoption checks are what keep the estimate anchored, and this evidence-first approach is the reason Mordor Intelligence lands at USD 2.66 B for 2025 rather than following broader or more pricing-led assumptions. Reading the table together, the spread is explainable once scope boundaries, annualization rules, and country coverage rules are kept consistent and then reviewed against real buying behavior.

Key Questions Answered in the Report

What is the current value of the Europe workforce management software market?

The market is valued at USD 2.89 billion in 2026 and is forecast to reach USD 4.34 billion by 2031.

Which deployment model is growing fastest?

Cloud deployment leads with an 11.17% CAGR through 2031, driven by lower ownership costs and rapid scalability.

Why is healthcare the fastest-growing industry segment?

Post-pandemic staffing pressures and mandatory nurse-to-patient ratios are pushing hospitals to adopt advanced scheduling tools at a 9.66% CAGR.

How does the Working Time Directive influence software adoption?

The Directive mandates objective time-tracking, compelling employers across the EU to implement compliant workforce management systems or risk penalties.

Page last updated on: