EMC Shielding And Test Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

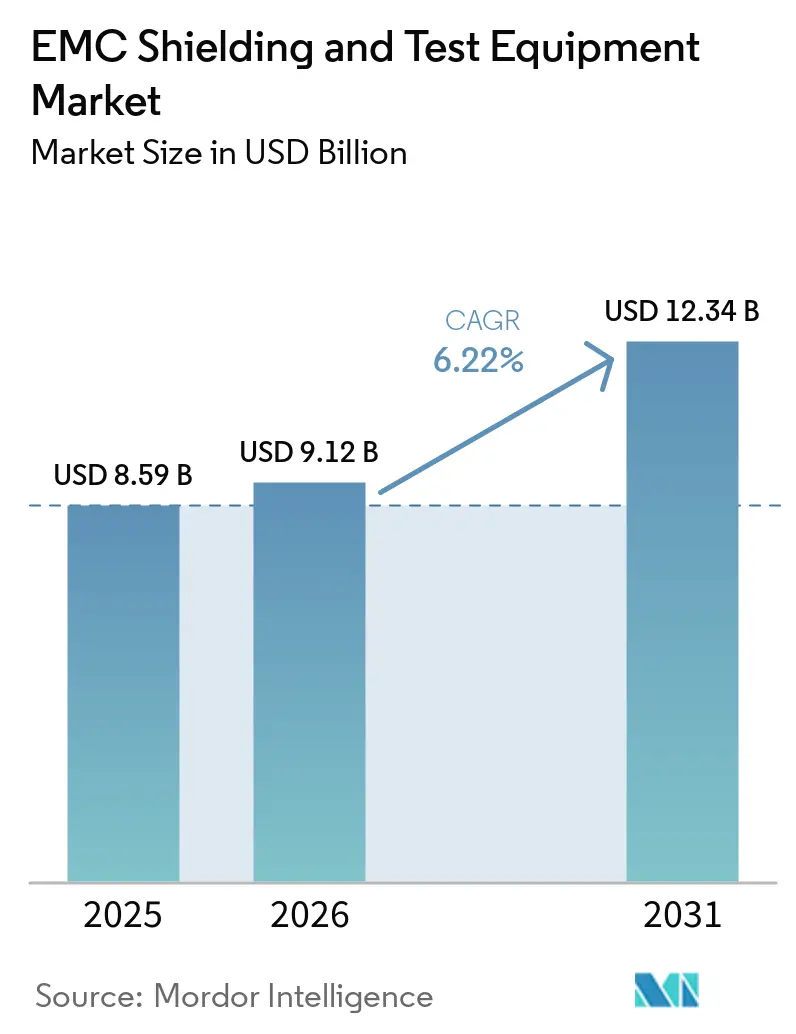

| Market Size (2026) | USD 9.12 Billion |

| Market Size (2031) | USD 12.34 Billion |

| Growth Rate (2026 - 2031) | 6.22% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

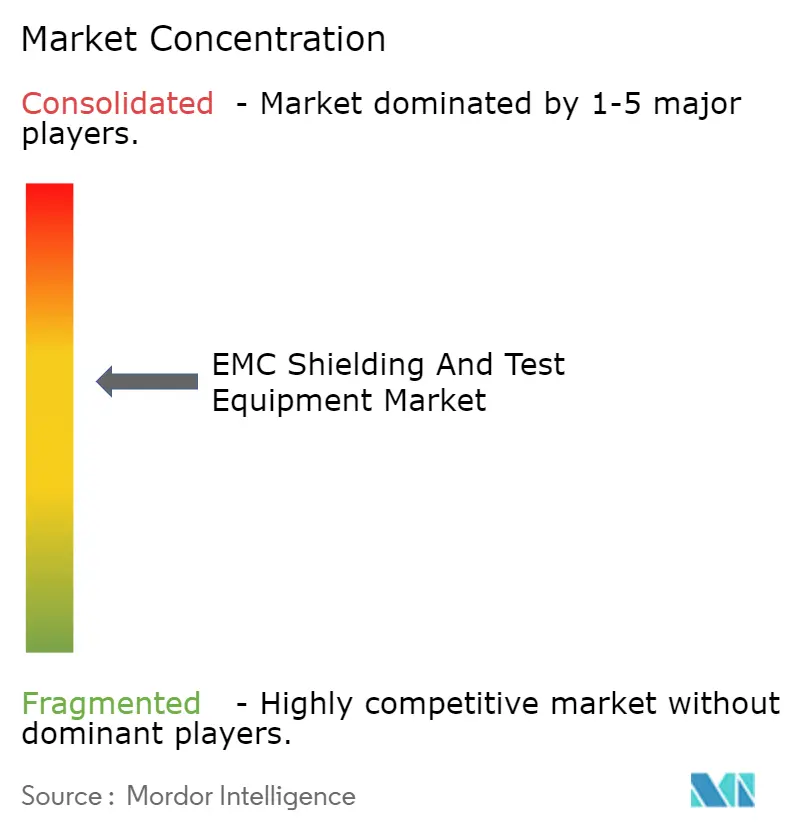

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

EMC Shielding And Test Equipment Market Analysis by Mordor Intelligence

The EMC shielding and test equipment market was valued at USD 8.59 billion in 2025 and is estimated to grow from USD 9.12 billion in 2026 to reach USD 12.34 billion by 2031, growing at a CAGR of 6.22% from 2026 to 2031. The EMC shielding and test equipment market is being shaped by mandatory type-approval rules that apply across major electronics categories and keep compliance spending tied to device launches in every large economy. Demand is rising from several directions at the same time, with 5G infrastructure, electric vehicle production, and dense AI compute systems each adding more EMC-sensitive assemblies and more testing events to product cycles. The EMC shielding and test equipment market also reflects a split competitive structure, where large measurement specialists compete on software, calibration, and standards coverage, while materials suppliers compete on attenuation, thermal performance, and integration into OEM production lines. Growth is supported by the shift toward higher frequency operation, tighter packaging, and more complex electronics content per platform, which raises the need for shielding at enclosure, module, and PCB levels. The main constraints remain the high cost of full-compliance laboratories and the shortage of specialized EMC engineers, both of which can slow certification throughput even when underlying product demand is strong.

Key Report Takeaways

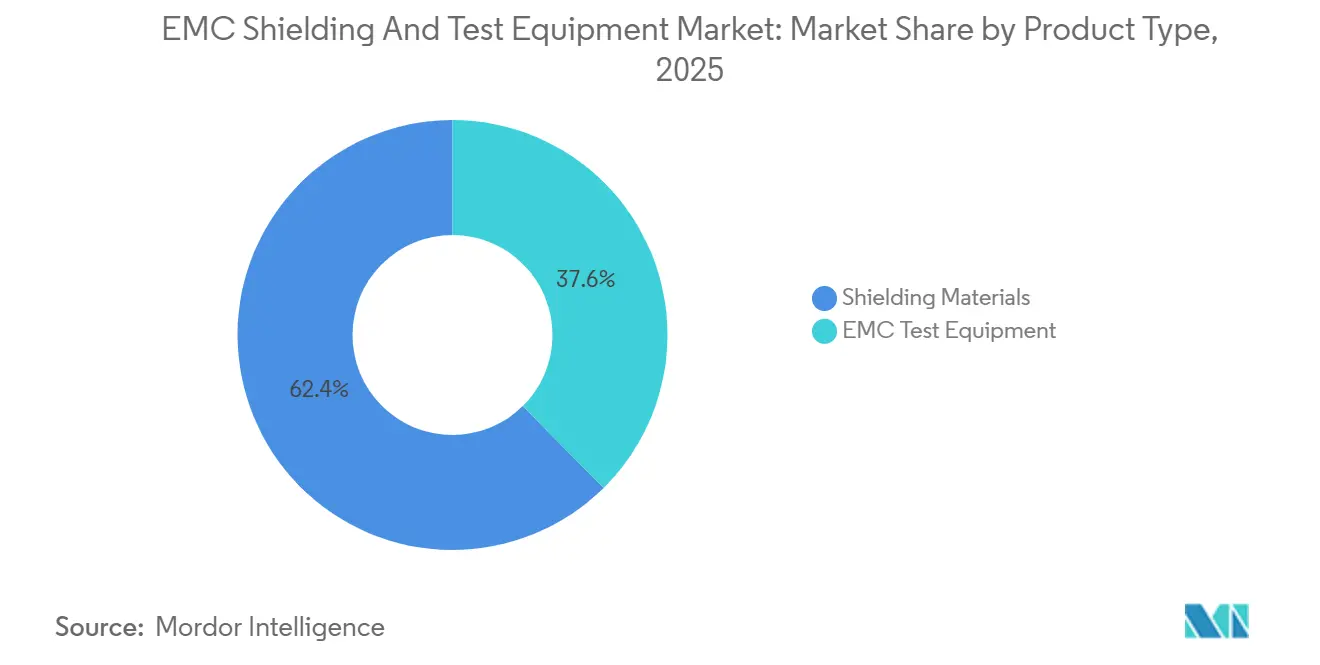

- By product type, shielding materials held 62.41% share of the EMC shielding and test equipment market in 2025, while EMC test equipment is forecast to grow at 6.35% CAGR through 2031.

- By shielding material type, conductive coatings and paints held 31.63% share of the EMC shielding and test equipment market, while laminates/tapes, and foils are forecast to expand at an 6.42% CAGR through 2031.

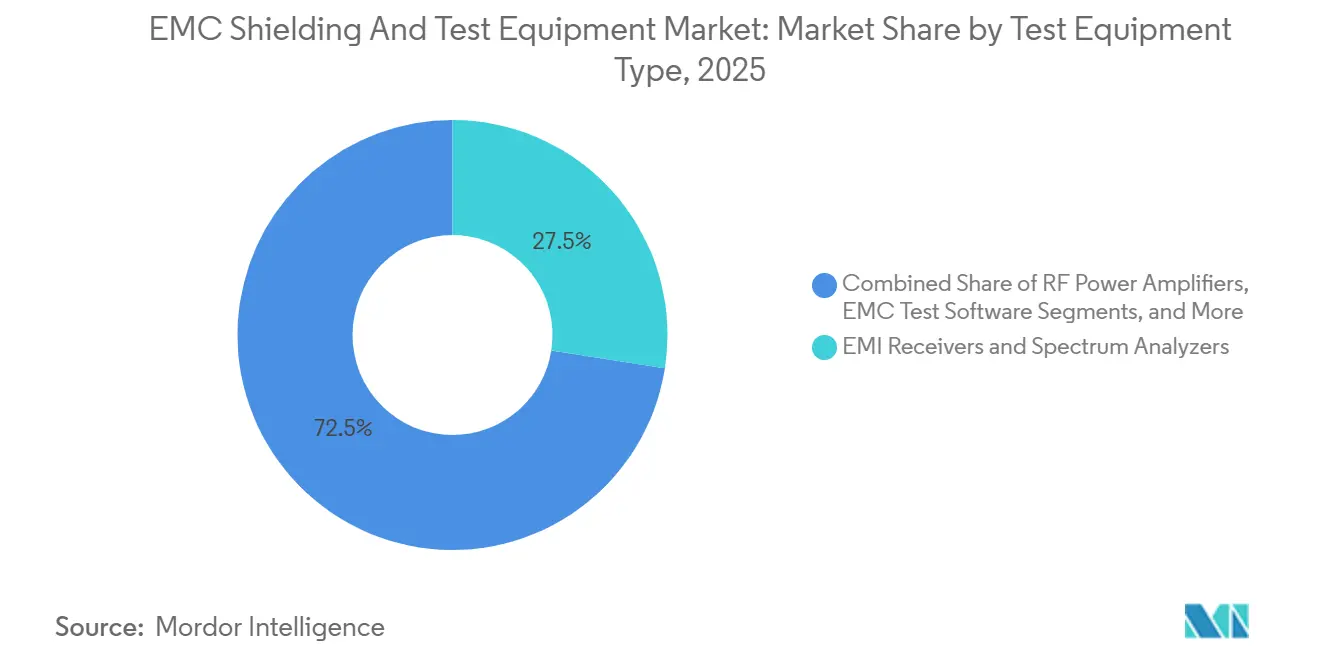

- By test equipment type, EMI receivers and spectrum analyzers accounted for a 27.48% share of the EMC shielding and test equipment market, while EMC test software is forecast to grow at 6.79% CAGR through 2031.

- By end-user industry, consumer electronics accounted for a 36.22% share of the EMC shielding and test equipment market, while automotive is forecast to expand at a 6.69% CAGR from 2026 to 2031.

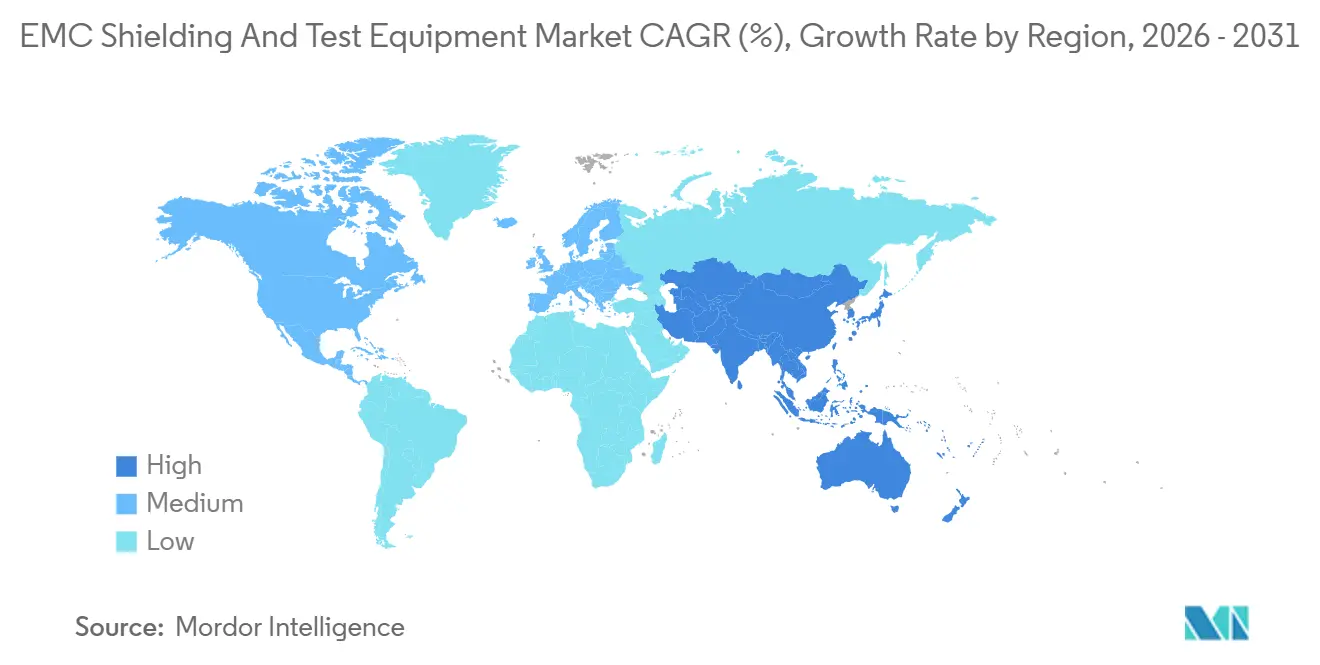

- By geography, Asia-Pacific held a 47.84% share of the EMC shielding and test equipment market, and is forecast to expand at a 6.51% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global EMC Shielding And Test Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV and ADAS Electrification Raising EMC Content per Platform | +1.8% | Global, core demand in China, Germany, South Korea, and United States | Medium term (2-4 years) |

| 5G and High-Frequency Wireless Expansion | +1.6% | Global, Asia-Pacific core, with spill-over to Europe and North America | Short term (≤ 2 years) |

| Stricter EMC Regulations and Certification Mandates | +1.2% | Global, EU and ETSI, and FCC primary anchors | Short term (≤ 2 years) |

| AI Server and 800G Infrastructure EMI Hot Spots | +1.0% | North America and Asia-Pacific hyperscale hubs | Medium term (2-4 years) |

| Device Miniaturization and Higher Electronics Density | +0.7% | Global, Asia-Pacific consumer electronics concentration | Long term (≥ 4 years) |

| Expanded Automotive EMC Test Scope Under UNECE and GB/T Updates | +0.5% | UNECE contracting parties, China domestic GB/T jurisdiction | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EV And ADAS Electrification Raising EMC Content Per Platform

Electric drivetrains are pushing the EMC shielding and test equipment market toward more complex shielding architectures because traction inverters above 10 kHz and up to 800 V create conducted and radiated interference across battery cables, chassis grounds, and ADAS harnesses.[1]TE Connectivity, “EMC Shielding Guide for Automotive Applications,” TE Connectivity, te.com TE Connectivity identified 3 separate shielding layers for EV platforms: enclosure, module, and PCB level, and each layer has its own attenuation target and validation requirements. A 2025 study in Energies found that standard LISNs do not fully capture differential-mode conducted EMI in traction drives, which means more custom measurement setups and longer test cycles for EV programs. Material design is also shifting, as Neklar introduced dual-function shielding for EV battery enclosures that combines EMC containment with flame resistance in one structure. UNECE Regulation No. 10, Revision 7, also extended the upper radiated emissions frequency for electronic sub-assemblies from 2,000 MHz to 6,000 MHz in June 2025, raising the antenna and receiver requirements for every automotive laboratory seeking UNECE accreditation.

5G And High-Frequency Wireless Expansion

The EMC shielding and test equipment market is also benefiting from the 5G rollout, as operators and device makers need new over-the-air test systems and shielding materials that remain effective across the 24 GHz to 44 GHz range. ETSI EN 301 489-50 V2.4.1 formalized updated EMC conditions for cellular base stations, repeaters, and related equipment in September 2025, which supports fresh demand for revised OTA test configurations. Research in the Journal of Computational Electronics demonstrated a conformal frequency-selective surface design with stable suppression from 0° to 80° incidence at the 26 GHz 5G n258 band, underscoring the need for precise material performance at the production scale. The same shift favors precision fabrication, because mmWave performance depends heavily on geometry, fit, and consistency rather than only on bulk conductivity or filler loading. National adoption of ETSI EN 301 489-50 V2.4.1 across European Union member states is due by June 2026, and conflicting standards are scheduled for withdrawal by June 2027, which keeps the compliance transition active across the EMC shielding and test equipment market.

Stricter EMC Regulations And Certification Mandates

Regulatory tightening is creating direct revenue events for the EMC shielding and test equipment market rather than distant compliance milestones. The FCC revoked recognition for 23 TCB-affiliated laboratories in May 2025, redirecting certification work to a smaller set of approved facilities and lengthening queues for affected manufacturers. EN 61000-6-4:2026 became mandatory on May 1, 2026, and older test reports based on the 2019 edition were no longer valid, triggering a new industrial re-certification cycle. EN IEC 61000-4-41:2025 added a dedicated test category for broadband radiated disturbances from 5G and industrial sources, so qualification budgets now include a test item that did not exist in earlier editions. MIL-STD-461H was released in April 2026 and updated defense EMC requirements, and that change is likely to flow into procurement specifications across allied defense programs over the next 18 to 24 months.

AI Server And 800G Infrastructure EMI Hot Spots

High-density AI compute is opening a newer demand layer in the EMC shielding and test equipment market because 800 Gbps links and tightly packed racks create interference conditions that older server layouts did not face. EDN noted that 800 Gbps transceivers operate near 28 GHz Nyquist frequencies, and shielded openings at that frequency range must remain below 0.536 mm, which clashes with standard rack ventilation designs. That tradeoff is pushing enclosure and gasket design toward finer tolerances and more deliberate coordination between airflow, thermal management, and EMC performance. Laird Performance Materials has already moved in this direction with CoolZorb D, a hybrid absorber that combines 3.0 W/mK thermal conductivity with EMI absorption above 20 GHz in one interface layer. As hyperscale operators expand AI and 800G deployments, this part of the EMC shielding and test equipment market is moving from a niche server issue to a repeat requirement for commercial data center hardware.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Intensity of Chambers and RF Instrumentation | -1.2% | Global, most acute in emerging Asia and South America | Long term (≥ 4 years) |

| EMC Engineering Talent Shortage and Test Complexity | -0.8% | Global, Europe more than 100K deficit, Asia-Pacific more than 200K deficit | Long term (≥ 4 years) |

| Mmwave and Above-40 Ghz Calibration Uncertainty | -0.5% | North America, Europe, East Asia | Medium term (2-4 years) |

| Thermal-Airflow and Emi Redesign Tradeoffs in Advanced Electronics | -0.3% | Global, 800G data centers, EV weight-sensitive architectures | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity Of Chambers And RF Instrumentation

The EMC shielding and test equipment market still faces a significant adoption barrier because full-compliance chambers and RF instrumentation require substantial upfront spending.[2]ATEC, “ATEC Partners With NTD Shielding for EMC Chamber Rental Pool in the UK and EMEIA,” ATEC, atecorp.com New fully anechoic chambers cost USD 500,000 to USD 2 million; refurbished systems cost USD 80,000 to USD 400,000; absorber replacement runs USD 40,000 to USD 200,000; and annual calibration adds USD 3,000 to USD 15,000. UNECE R10 Revision 7 adds reverberation chamber requirements for some automotive tests, so labs seeking full compliance may need more than one chamber type instead of a single anechoic setup. That cost burden pushes many small and mid-sized manufacturers toward third-party labs, which concentrate test capacity and create scheduling pressure during launch periods across the EMC shielding and test equipment market. ATEC and NTD Shielding responded with a shared-chamber rental pool in June 2025, demonstrating that equipment-as-a-service models are becoming a practical answer when outright ownership is difficult.

EMC Engineering Talent Shortage And Test Complexity

The EMC shielding and test equipment market is also limited by a shortage of engineers who can work across RF measurement, hardware design, and regulatory compliance at the same time. EMSNow estimated a shortfall of 59,000 to 146,000 skilled technicians and engineers in electronics and semiconductors by 2029, and EMC work is especially exposed because it needs a narrow mix of practical and standards-based knowledge. The SEMI Foundation launched a regional credentialing program in spring 2026 and expanded it nationally in fall 2026, but that effort is more relevant to technician training than to senior EMC systems roles. Vendors are responding by adding automation, guided workflows, and AI-assisted diagnostics, which helps the EMC shielding and test equipment market sell more usable systems to teams with limited in-house expertise. The limit appears when product complexity moves into mmWave certification and OTA chamber alignment, because those tasks still need experienced judgment that current software cannot fully replace.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Shielding Materials Lead Revenue As Test Equipment Accelerates

Shielding materials accounted for 62.41% of the EMC shielding and test equipment market in 2025, reflecting their use across nearly every electronics manufacturing category, from consumer devices to aircraft avionics. This side of the EMC shielding and test equipment market covers conductive coatings, gaskets, laminates, tapes, foils, and metal enclosures, and many products use more than one of these layers in the same assembly. That broad distribution across enclosures, modules, and PCB structures explains why materials revenue outpaced test equipment revenue in 2025. At the same time, EMC test equipment with 6.35% CAGR is the faster-growing product type through 2031 because revised standards keep changing what qualified laboratories and OEM design teams need to measure.

The line between the 2 product groups is narrowing across the EMC shielding and test equipment industry, because pre-compliance benches are increasingly sold with reference shielding assemblies and application guidance for design teams. Automotive suppliers are also buying pre-compliance benches that mirror the transient immunity profiles required under UNECE R10 Revision 7, thereby reducing dependence on external labs during early design work. Nolato reported FY2025 Engineered Solutions revenue of SEK 4,101 million (USD 424 million), which was approximately USD 387 million, and its materials sub-segment posted adjusted growth of nearly 10% in Q4 2025, led by data center and telecom demand. That mix shift suggests the EMC shielding and test equipment industry is rewarding suppliers that can serve newer compute and communications programs, even as in-process conductive coatings make switching easier in parts of the materials tier.

By Shielding Material Type: Laminates And Foils Post Fastest Expansion On Flexible Substrate Demand

Laminates, tapes, and foils are the fastest-growing subsegment of shielding materials, with the EMC shielding and test equipment market for this category forecast to expand at a 6.42% CAGR from 2026 to 2031. Their advantage lies in flexibility, as curved EV battery housings, ribbon cables in ADAS modules, and foldable display assemblies often cannot use rigid shielding structures without incurring space or weight penalties. Metal enclosures and cabinets remain important where bulk shielding matters more than mass, especially in industrial power electronics, servers, and rack systems.

Conductive coatings accounted for 31.63% share of the EMC shielding and test equipment market due to their ability to combine effective shielding performance with lightweight characteristics, production flexibility, and cost efficiency. The growing use of smartphones, tablets, laptops, wearable devices, IoT products, and 5G technologies has significantly increased the demand for EMI shielding solutions that protect electronic components from signal interference. These coatings and paints are extensively adopted because they can be easily applied to compact device enclosures and printed circuit boards. Unlike conventional metal shielding, conductive coatings provide reliable electromagnetic protection without adding substantial weight or bulk, making them highly suitable for compact, portable electronic devices.

By Test Equipment Type: EMIReceivers Lead Revenue As Software Monetization Expands

EMI receivers and spectrum analyzers accounted for 27.48% of the EMC shielding and test equipment market share in 2025, which reflects their central role in both pre-compliance and accredited compliance measurements. Their position is reinforced by regular calibration requirements and by standards updates that require facilities to upgrade hardware, even when their older setups remain functional for legacy programs. EMC test software, with a 6.79% CAGR, is the fastest-growing sub-segment through 2031 because vendors are building recurring license models around automation, guided workflows, and interference diagnostics. RF power amplifiers, antennas, and probes, and transient and ESD generators remain stable supporting categories, with antenna demand lifted by OTA testing for 5G base stations and V2X radios.

Rohde & Schwarz launched the portable R&S EPL1001 and EPL1007 EMI receivers in Q2 2025, extending receiver use from fixed laboratories into the field and distributed pre-compliance work. At EMV 2026 in Cologne, the company also introduced the BBA300-DE1000, rated at 1,000 W from 1 GHz to 6 GHz, to meet the power levels required by EN 61000-6-4:2026 for industrial immunity testing. Keysight launched the Infiniium XR8 real-time oscilloscopes in February 2026 with sub-13 femtosecond intrinsic jitter at 8 GHz and compliance suites for USB4 Version 2, DisplayPort 2.1, and DDR5, which supports programs where signal integrity and EMI analysis overlap.[3]Keysight Technologies, “Infiniium XR8 Real-Time Oscilloscopes,” Keysight Technologies, keysight.com Eretec added an AI-based layer to the EMC shielding and test equipment market with EMINT in late 2025, which introduced autonomous interference classification into commercial EMI countermeasure software.

By End-User Industry: Automotive Leads Growth As Per-Platform EMC Content Rises

Automotive is the fastest-growing end-user segment, with the EMC shielding and test equipment market size for this vertical forecast to advance at a 6.69% CAGR from 2026 to 2031. Growth reflects the added shielding and testing burden from 800 V battery systems, radar arrays, and V2X transceivers, along with the higher upper frequency limits now embedded in automotive regulations. Telecom and IT infrastructure also remain important, because 5G base station rollout and 800G optical interconnects in hyperscale data centers are expanding both enclosure shielding and chamber testing needs. Consumer electronics, with a 36.22% market share, retained the largest end-user revenue share in 2025, supported by the volume of smartphones, wearables, IoT nodes, and display devices that must meet regional emission rules.

Aerospace and defense remain high-value buyers as MIL-STD-461H updates the qualification cycle for defense electronics and platform upgrades. Medical devices continue to operate under IEC immunity and radiated emission frameworks, which are under tighter scrutiny as wearable and implantable electronics operate in denser wireless environments. Industrial and energy applications faced a direct 2026 trigger when EN 61000-6-4:2026 became mandatory on May 1, 2026, invalidating reports prepared under the superseded 2019 version and prompting a new wave of retesting in accredited laboratories. ETS-Lindgren's January 2026 launches, including the Model 3170 Intell-I-Tune Antenna, the Model 2171C Boresight Plus Tower, and the Model 5903-HST high-speed tuner, show how suppliers are aligning new products with defense and industrial re-certification demand in the EMC shielding and test equipment market.

Geography Analysis

Asia-Pacific held a 47.84% share in 2025, and the regional EMC shielding and test equipment market is forecast to grow at a 6.51% CAGR through 2031. China remains the center of that lead because EV production, 5G deployment, and domestic semiconductor investment all carry mandatory EMC compliance spending at scale.[4]Standardization Administration of China, “GB/T 18655-2025,” SAC, sac.gov.cn GB/T 18655-2025 extended vehicle EMC test coverage to 5,925 MHz and added EV-specific setups and V2X protection requirements in February 2025. GB/T 46894-2025, published in December 2025, introduced IC-level vehicle EMC testing and included Huawei and Chery Automobile among the drafters, which points to a more independent automotive EMC standards path in China. Japan and South Korea add strong demand from displays, power semiconductors, and consumer appliances, while India is emerging as a manufacturing base, with Nolato opening an EMC-capable facility in Bangalore to support local electronics production.

North America is the second-largest regional market for EMC shielding and test equipment, supported by mature commercial test capacity and high-value demand from the aerospace and defense sector. FCC actions across 2025 and 2026, including revoked lab recognitions, the proposed phase-out of non-reciprocal country testing, and the Trusted Test Lab process effective June 15, 2026, are reshaping where certification revenue goes within the United States. The United States and Canada also anchor much of the AI data center build-out, which is adding a fresh demand stream for shielded enclosures, gaskets, and high-frequency validation tools tied to 800G hardware. Mexico is benefiting from nearshored automotive assembly, especially in EV battery pack manufacturing corridors, which is raising local demand for pre-compliance capability and shielding integration.

Europe remains a policy-led market for EMC shielding and test equipment, as EN 61000-6-4:2026, ETSI EN 301 489-50 V2.4.1, and UNECE R10 Revision 7 are all in active adoption or implementation. Germany remains the instrumentation hub through Rohde and Schwarz, while France-based Emitech strengthened its automotive EMC service position by acquiring ExoTest 3E assets effective January 2026. South America is smaller but growing steadily, driven by ANATEL-related compliance demand and local automotive assembly, while the Middle East is building future demand through 5G densification and data center investment led by the United Arab Emirates and Saudi Arabia. Africa still relies mainly on European-accredited laboratories for certification, which limits local testing infrastructure but leaves room to shield material demand in telecom and industrial equipment imports.

Competitive Landscape

The EMC shielding and test equipment market exhibits a medium concentration, with one competitive group centered on instruments and software and another on shielding materials and engineered components. Rohde & Schwarz and Keysight lead the instrumentation side, and Rohde & Schwarz reported FY2024/25 net revenue of EUR 3.16 billion (USD 3.57 billion), approximately USD 3.41 billion, across more than 15,000 employees. Their edge comes from software integration, calibration traceability, and tools built around specific compliance tasks rather than from hardware alone. In materials, Parker Hannifin, TE Connectivity, and Laird Performance Materials compete on attenuation performance, qualification credentials, and ease of integration into OEM production lines. The EMC shielding and test equipment market is also seeing faster patent and product activity around conformal mmWave shielding, hybrid thermal and EMI absorbers, and AI-assisted test workflows as standards move toward higher frequencies.

M&A is one of the clearest strategic tools in the EMC shielding and test equipment market right now. Boyd Corporation completed the sale of its thermal business to Eaton for USD 9.5 billion in March 2026, leaving its Engineered Materials shielding activities under independent ownership backed by Goldman Sachs and sharpening its focus on EMC-related materials.[5]Boyd Corporation, “Thermal Business Sale to Eaton for USD 9.5 Billion,” Boyd Corporation, boydcorp.com Aeromed Group, backed by Gemspring Capital, acquired HITEK Electronic Materials in the United Kingdom in March 2026 and created a dedicated military EMC shielding platform for European defense programs. Emitech also expanded test service capacity through its January 2026 acquisition of ExoTest 3E EMC assets, including Faraday cages and mode-shuffling chambers for EV powertrain certification.

Lockmasters added another example when it acquired Signals Defense in April 2025, extending its offering to include TEMPEST- and ICD-705-compliant RF shielding for secure facilities. Product launches remain just as important as acquisitions, with Rohde and Schwarz, Keysight, Parker, and ETS-Lindgren each using new releases to capture revised requirements in industrial, defense, automotive, and high-speed digital applications. White-space opportunities still exist in portable mmWave calibration tools, AI-guided pre-compliance software for smaller manufacturers, and shielded enclosure design services for space and satellite ground systems, where the EMC shielding and test equipment market remains less crowded than in mainstream lab instrumentation. That leaves competition active but not consolidated, with specialists still able to win share when they solve a narrow standards-driven problem better than broader platform vendors.

EMC Shielding And Test Equipment Industry Leaders

Rohde & Schwarz GmbH & Co. KG

Keysight Technologies, Inc.

ETS-Lindgren Inc.

3M Company

Parker-Hannifin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The FCC published new rules establishing a fast-track process for Trusted Test Lab PAG designation and enhanced TCB disclosure requirements, effective June 15, 2026. The action is expected to accelerate accreditation of domestic U.S. test facilities and reduce compliance queue times for approved manufacturers, further concentrating certification revenue toward allied-country test houses.

- April 2026: Rohde and Schwarz presented the R&S HF1444G20 (EMS) and HF1444G14 (EMI) antenna systems covering 14.9-44 GHz at APEMC 2026 in Kuala Lumpur, alongside MIL-STD-461H-compliant test workflows. The introduction positions the company at the leading edge of the defense spectrum's new compliance cycle triggered by the April 2026 standard release.

- March 2026: Boyd Corporation completed the sale of its thermal interface and heat management business to Eaton for USD 9.5 billion, with the Engineered Materials shielding division continuing under Goldman Sachs-backed independent ownership. The separation concentrates the remaining business on EMC shielding and advanced materials for aerospace, data centers, and EVs.

- February 2026: Keysight Technologies launched the Infiniium XR8 real-time oscilloscopes featuring sub-13 femtosecond intrinsic jitter at 8 GHz, with integrated validation suites for USB4 Version 2, DisplayPort 2.1, and DDR5. The platform targets semiconductor and systems designers certifying next-generation high-speed interface standards where signal integrity and EMI analysis overlap.

Global EMC Shielding And Test Equipment Market Report Scope

The Transformerless UPS Market Report is Segmented by Product Type (Shielding Materials, and EMC Test Equipment), Shielding Material Type (Conductive Coatings and Paints, Conductive Gaskets and O-rings, Laminates / Tapes and Foils, and Metal Enclosures and Cabinets), Test Equipment Type (EMI Receivers and Spectrum Analyzers, RF Power Amplifiers, Antennas and Probes, Transient / ESD Generators, and EMC Test Software), End-user Industry (Consumer Electronics, Automotive, Telecom and IT Infrastructure, Aerospace and Defense, Medical Devices, and Industrial and Energy), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Shielding Materials |

| EMC Test Equipment |

| Conductive Coatings and Paints |

| Conductive Gaskets and O-rings |

| Laminates / Tapes and Foils |

| Metal Enclosures and Cabinets |

| EMI Receivers and Spectrum Analyzers |

| RF Power Amplifiers |

| Antennas and Probes |

| Transient / ESD Generators |

| EMC Test Software |

| Consumer Electronics |

| Automotive |

| Telecom and IT Infrastructure |

| Aerospace and Defense |

| Medical Devices |

| Industrial and Energy |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Shielding Materials | |

| EMC Test Equipment | ||

| By Shielding Material Type | Conductive Coatings and Paints | |

| Conductive Gaskets and O-rings | ||

| Laminates / Tapes and Foils | ||

| Metal Enclosures and Cabinets | ||

| By Test Equipment Type | EMI Receivers and Spectrum Analyzers | |

| RF Power Amplifiers | ||

| Antennas and Probes | ||

| Transient / ESD Generators | ||

| EMC Test Software | ||

| By End-user Industry | Consumer Electronics | |

| Automotive | ||

| Telecom and IT Infrastructure | ||

| Aerospace and Defense | ||

| Medical Devices | ||

| Industrial and Energy | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the EMC shielding and test equipment market?

The EMC shielding and test equipment market stands at USD 9.12 billion in 2026 and is projected to reach USD 12.34 billion by 2031 at a 6.22% CAGR.

Which product category leads revenue in this space?

Shielding materials led revenue with a 62.41% share in 2025, reflecting their use across enclosures, modules, and PCB-level designs.

Which end-user group is expanding the fastest?

Automotive is the fastest-growing end-user segment, with a forecast CAGR of 6.69% from 2026 to 2031, driven by EV architectures, ADAS, and V2X electronics.

Why is Asia-Pacific the leading regional hub?

Asia-Pacific held 47.84% of revenue in 2025 because China, Japan, South Korea, and India are combining EV production, 5G investment, and electronics manufacturing growth with rising compliance needs.

What is driving test equipment demand faster than before?

Regulatory updates, 5G and OTA requirements, AI server design issues, and industrial re-certification cycles are pushing companies to upgrade receivers, amplifiers, antennas, and compliance software.

What are the main barriers to faster adoption?

The biggest barriers are chamber and instrumentation costs, which can reach USD 2 million for new installations, and a shortage of EMC-skilled engineers that can slow test throughput and lab expansion.

Page last updated on: