Radiation Hardened Electronics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

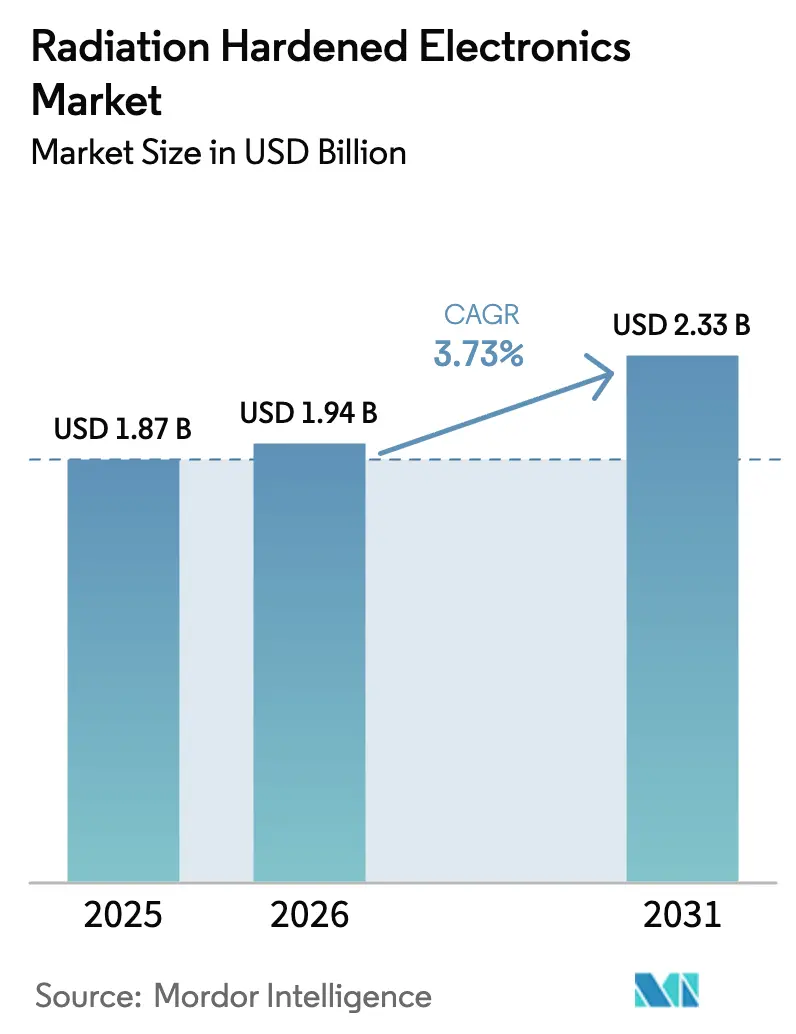

| Market Size (2026) | USD 1.94 Billion |

| Market Size (2031) | USD 2.33 Billion |

| Growth Rate (2026 - 2031) | 3.73% CAGR |

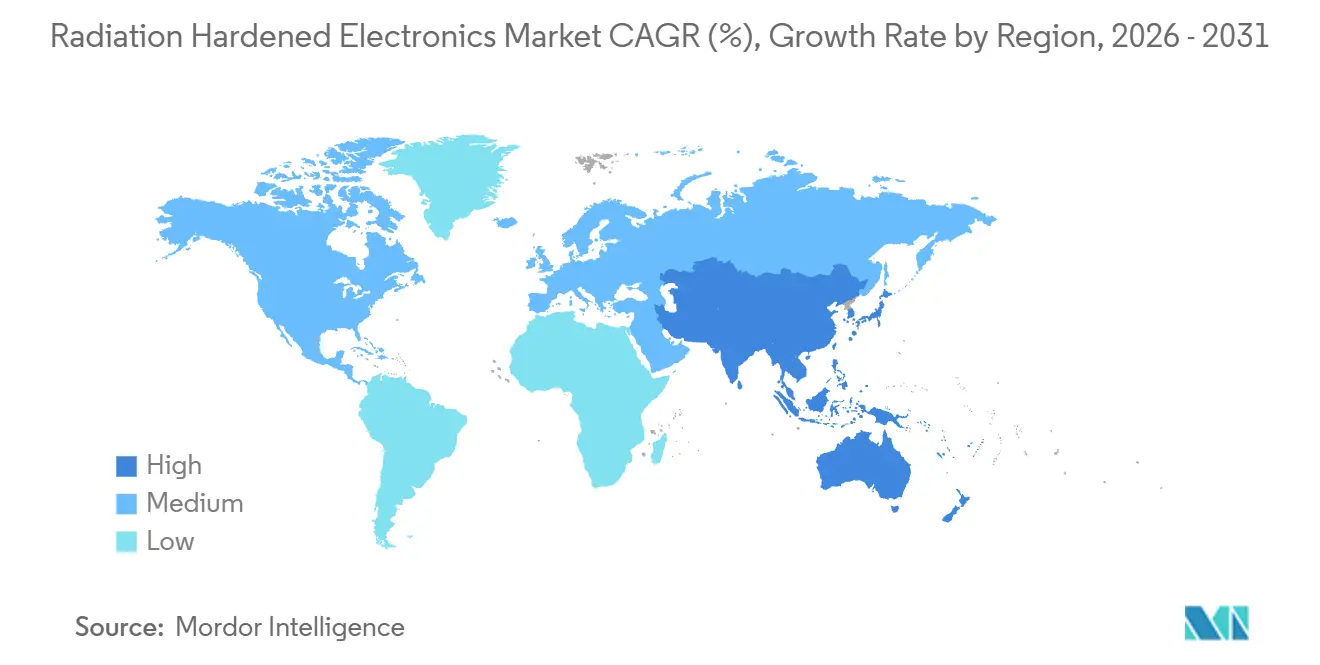

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

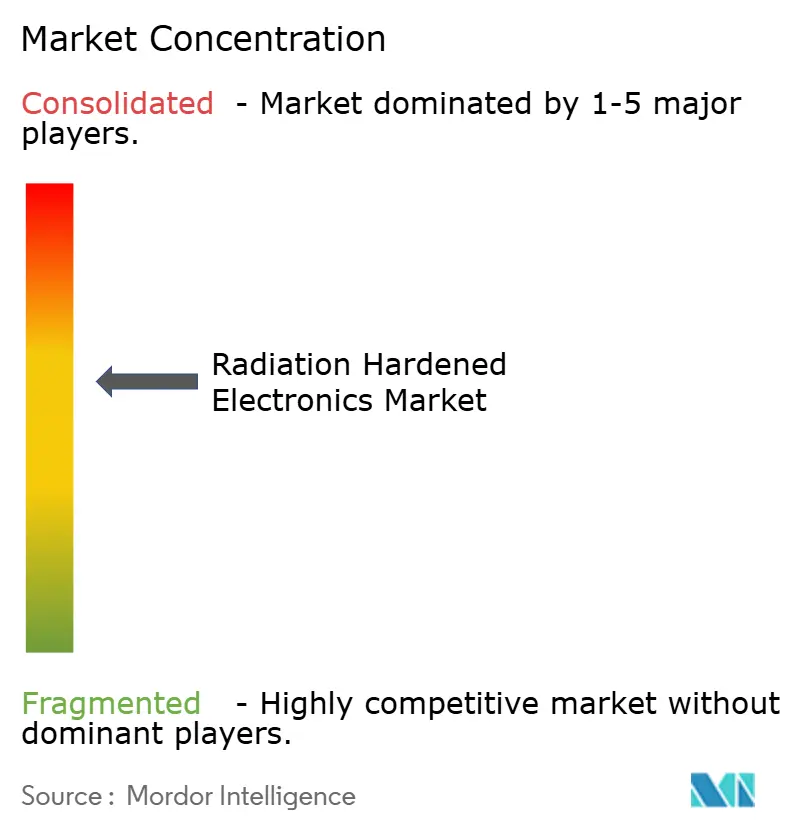

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Radiation Hardened Electronics Market Analysis by Mordor Intelligence

The Radiation Hardened Electronics Market size was valued at USD 1.87 billion in 2025 and is estimated to grow from USD 1.94 billion in 2026 to reach USD 2.33 billion by 2031, at a CAGR of 3.73% during the forecast period (2026-2031).

Demand continues to come from three structural outlets, namely mega-constellations in low Earth orbit, the modernization of NATO airborne and missile platforms, and the wave of new nuclear reactors in Asia and the Middle East. Product lifecycles are long because every part must clear multi-year qualification gates, yet suppliers are still expanding capacity for field-programmable gate arrays, gallium-nitride power devices, and mixed-signal front ends that can tolerate 100 kilorads or more. Program funding from the United States Space Force, the European Space Agency, and Asian nuclear utilities underpins steady unit volumes, while export-control rules and restricted foundry access temper upside growth.

Key Report Takeaways

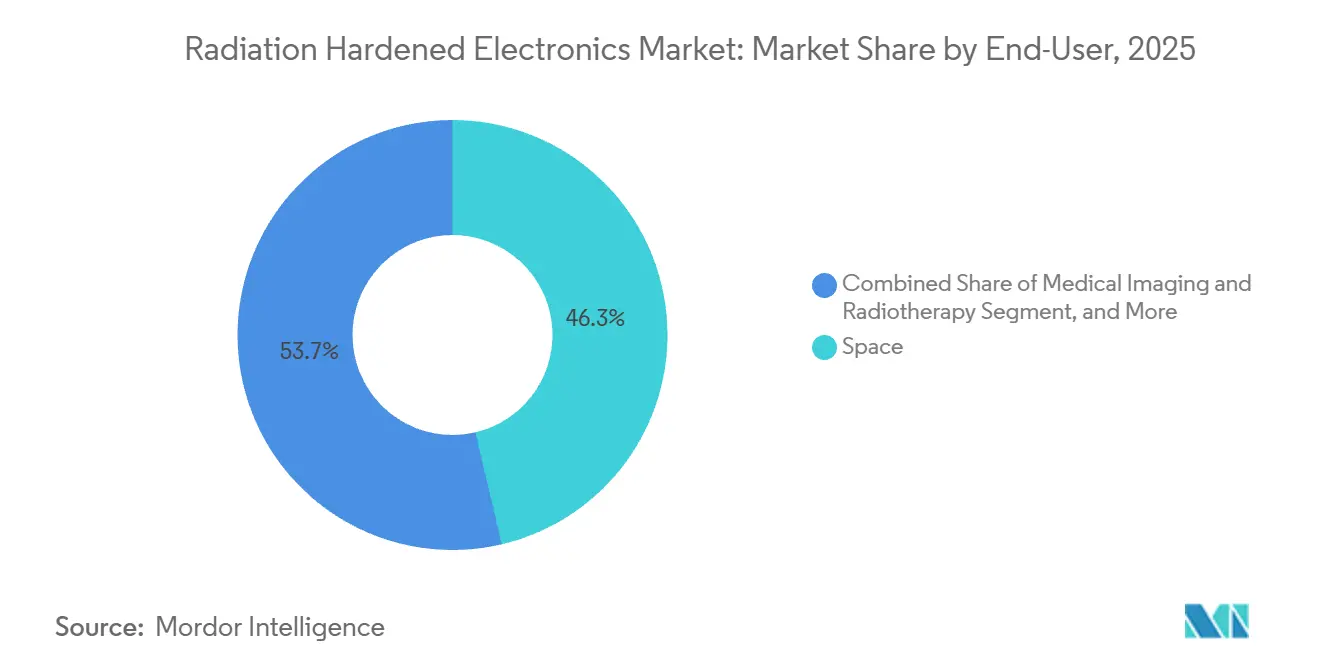

- By end-user, space applications held 46.32% of 2025 revenue, while high-altitude unmanned platforms are advancing at a 4.11% CAGR to 2031.

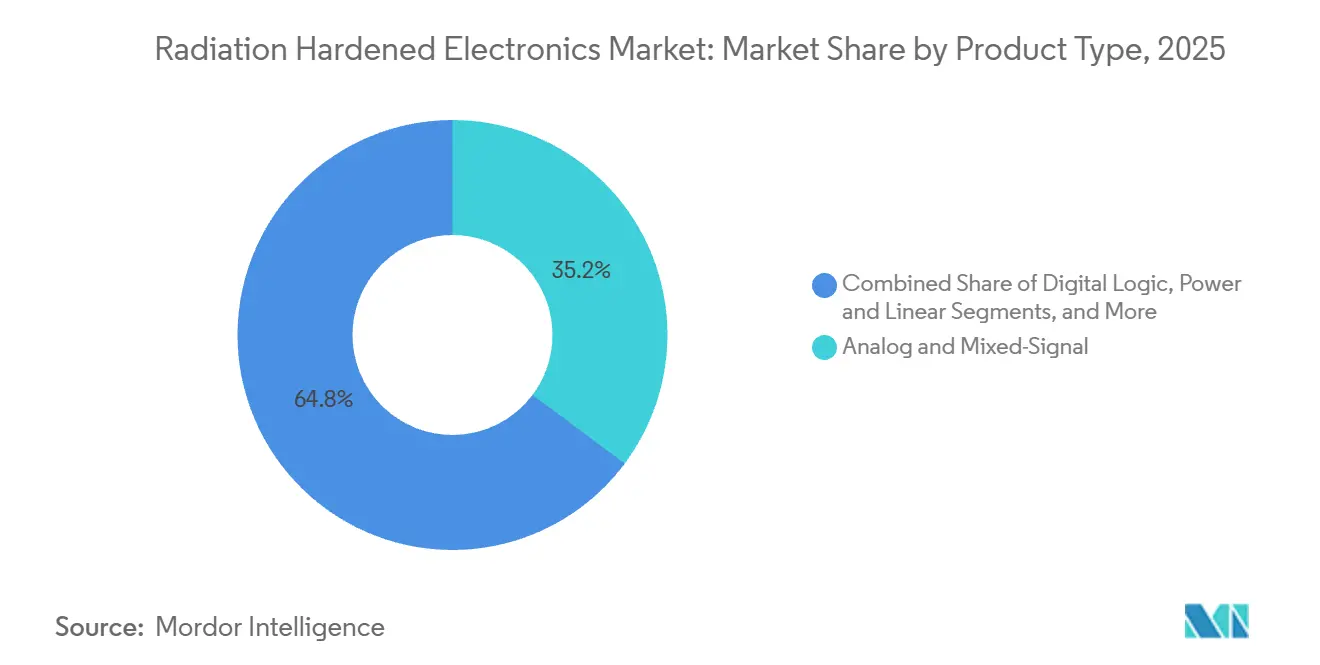

- By component, analog and mixed-signal ICs captured 35.21% radiation hardened electronics market share in 2025, and field-programmable gate arrays represent the fastest component line, expanding 4.41% per year to 2031.

- By manufacturing technique, radiation-hard-by-design solutions accounted for 52.43% of 2025 sales and are forecast to climb 4.12% annually, eclipsing radiation-hard-by-process nodes held back at 150 nanometers.

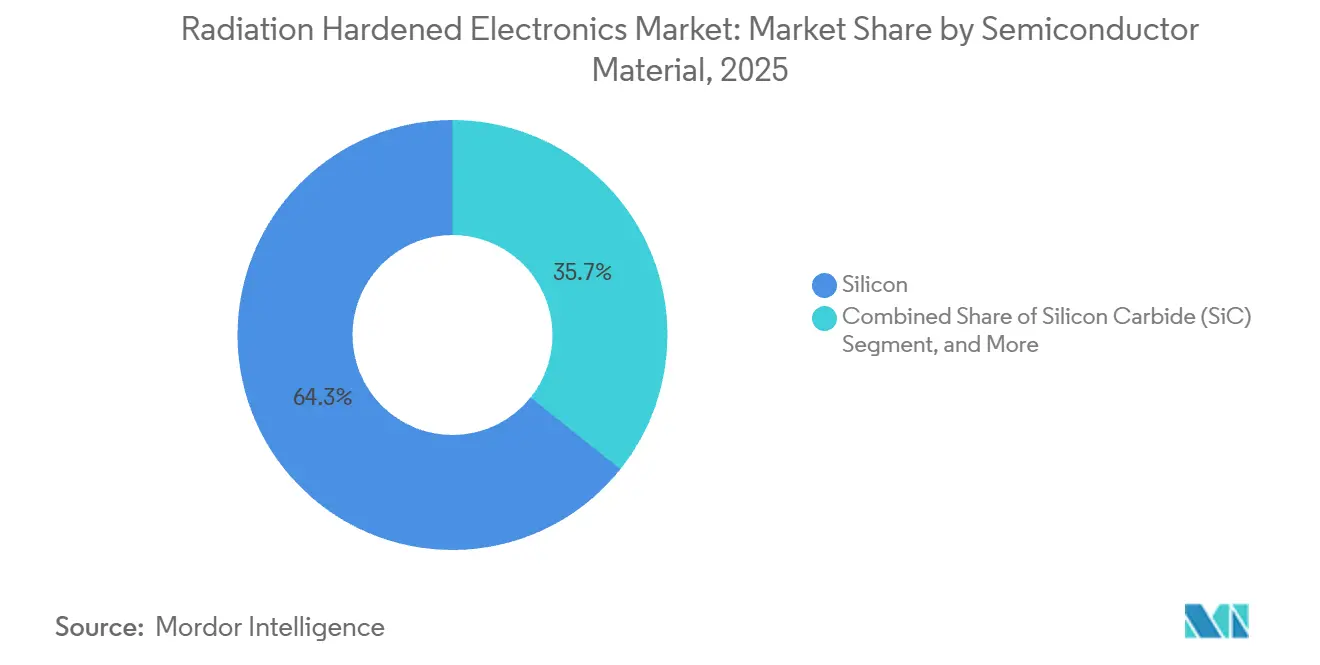

- By semiconductor material, silicon retained 64.27% of 2025 revenue, while gallium nitride devices for power-processing units are growing 4.51% a year to 2031.

- By radiation type, total ionizing dose protection contributed 48.33% in 2025, yet single-event effects mitigation leads growth at 5.13% through 2031.

- By geography, North America generated 41.63% of 2025 sales, whereas Asia Pacific is set to record the fastest 4.99% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Radiation Hardened Electronics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in LEO and Deep-Space Satellite Constellations | +1.2% | Global, concentration in North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Modernization of Strategic and Tactical Defence Electronics in NATO Region | +0.9% | North America and Europe | Long term (≥ 4 years) |

| Nuclear-New-Build Momentum in Asia and Middle East | +0.6% | Asia Pacific and Middle East, spillover to Europe | Long term (≥ 4 years) |

| High-Altitude UAV and Supersonic Aircraft Electronics Resilience Needs | +0.4% | Global, early adoption in North America and Middle East | Medium term (2-4 years) |

| Mandated Radiation-Tolerance Standards in Medical Imaging | +0.3% | North America and Europe | Short term (≤ 2 years) |

| Rapid Adoption of SiC or GaN Rad-Hard Power Devices | +0.4% | Global, led by North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in LEO and Deep-Space Satellite Constellations

Orders for thousands of satellites per operator have changed purchasing patterns in the radiation hardened electronics market. Amazon committed USD 10 billion to Project Kuiper through 2026, while OneWeb finished its first constellation in 2024 and has green-lit a second cluster with laser inter-satellite links that require 10 gigabit-per-second single-event-latchup-immune transceivers. ESA’s Galileo Second Generation payloads are specified for 15 years on-orbit, demanding oscillators hardened to 15 years of radiation exposure. Deep-space projects add extreme needs; NASA’s Europa Clipper carries electronics verified to 2.9 megarads, removing most commercial parts from contention.[1]NASA Communications Office, “Europa Clipper Mission Electronics,” nasa.gov The dual pull of higher volume and harsher physics pushes suppliers to lower unit costs while lifting the ceiling on total ionizing dose.

Modernization of Strategic and Tactical Defence Electronics in NATO Region

Defense ministries are replacing 1990s-era avionics with parts rated to today’s single-event-upset benchmarks. The United Kingdom earmarked GBP 24 billion to refresh Tornado and Typhoon mission computers, and BAE Systems won GBP 317 million for gallium-nitride electronic-warfare suites on the Tempest fighter. The United States Air Force allocates USD 28 billion for Next Generation Air Dominance, specifying autonomous flight computers qualified to MIL-STD-883 Class S. Lockheed Martin’s hypersonic projects carry rad-hard inertial sensors to survive plasma blackout, showing that tactical missiles are aligning with space standards. Together, these budgets anchor multi-year demand for processors qualified above 100 kilorads.

Nuclear-New-Build Momentum in Asia and Middle East

IAEA projects global nuclear capacity to rise to 436 GWe by 2030, with 68% of new reactors in Asia and the Middle East. China connected eight Hualong One reactors during 2024-2025, each calling for control modules that survive 10^14 neutrons per cm² and 100 kilorads over six decades. India’s Kakrapar-3 and -4 reactors source rad-hard multiplexers under domestic self-reliance policies, while the United Arab Emirates finalized its fourth APR1400 unit with neutron monitors based on European space heritage. Saudi Arabia’s planned small modular reactor fleet will add fresh demand from 2028 onward. These programs translate directly into steady orders for neutron-flux sensors, gamma-tolerant processors, and hardened analog front ends.

High-Altitude UAV and Supersonic Aircraft Electronics Resilience Needs

Operating above 60,000 feet raises radiation dosage and single-event-upset rates by an order of magnitude relative to sea level. Airbus’s Zephyr HAPS platform set a 64-day endurance record in 2025 with flight controllers hardened for cosmic-ray flux. The United States is pursuing hypersonic glide vehicles that re-enter with plasma sheaths demanding rad-hard inertial measurement units. Gulf nations are trialing high-altitude long-endurance drones for border security, further broadening the addressable customer set. The shift from tactical aircraft to stratospheric UAVs therefore lifts incremental volumes for radiation hardened electronics market suppliers serving aerospace primes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Design-for-Reliability Cost and Long Qualification Cycles | -0.7% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Restricted Foundry Capacity for RHBP Nodes ≤ 90 nm | -0.5% | Global, concentrated in North America and Asia Pacific | Medium term (2-4 years) |

| Performance Trade-Offs Versus COTS Chips | -0.3% | Global, affects radar and signals intelligence payloads | Medium term (2-4 years) |

| ITAR or Export-Control Bottlenecks | -0.3% | U.S. exports to Europe, Asia Pacific, Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Design-for-Reliability Cost and Long Qualification Cycles

Non-recurring engineering for a single mixed-signal IC often tops USD 5 million, and qualification may last 24-36 months. MIL-STD-883 testing demands multiple dose rates and temperatures, while heavy-ion beam time at ESA’s RADEF or Texas A&M’s cyclotrons can cost USD 3,000 per hour with queues that stretch a year.[2]U.S. Department of Defense, “MIL-STD-883 Test Methods,” defense.gov ESA’s destructive-analysis flow pushes total outlay above USD 8 million for complex parts. Smaller satellite firms therefore select commercial chips with shielding and software scrubbing, accepting higher in-orbit failure risk in exchange for 60% lower cost and one-year shorter lead time.

Restricted Foundry Capacity for RHBP Nodes ≤ 90 nm

Only a handful of fabs run silicon-on-insulator flows tailored for radiation-hard-by-process production. BAE Systems’ Manassas plant is the sole North American line, fixed at 150 millimeter wafers and 150 nanometer geometry with roughly 12,000 wafer starts per year. Tower Semiconductor’s Israeli facility offers 180 nanometer SOI capacity yet prioritizes automotive contracts, leaving aerospace with 52-week waits. With no commercial-scale sub-90 nanometer RHBP node in sight, designers rely on radiation-hard-by-design redundancy that inflates die area by up to 80% and still cannot meet Jupiter mission LET thresholds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Space Dominance Drives Innovation Priorities

Space platforms represented 46.32% of 2025 revenue, underscoring how mega-constellations and science craft consume the largest share of the radiation hardened electronics market. Operators ordered more than 120,000 integrated circuits during 2025, and ESA’s lunar programs keep demand resilient. Growth will trail the overall market because low Earth orbit constellations increasingly adopt selective shielding with commercial parts. High-altitude UAV and HAPS systems provide the fastest 4.11% CAGR lane as Airbus and U.S. primes validate stratospheric drones. Their avionics must survive cosmic rays at 70,000 feet, so every flight computer integrates triple-modular redundancy and error-correction logic. Classic aerospace and defense equipment - fighters, missiles, and naval combat systems - claimed about 28% of revenue, led by NATO modernization budgets that fund MIL-STD-883 Class S processors and gallium-nitride transmit-receive modules. The nuclear sector added around 12% thanks to the Kakrapar and Barakah reactors, while medical imaging and particle-physics labs filled the remainder.

The 2025 sales mix illustrates how the radiation hardened electronics market size remains weighted toward orbital platforms, yet faster unit expansion is visible in stratospheric drones and emerging hypersonic weapons. Defense primes increasingly blend space-qualified processors with Gallium-Nitride power stages to achieve weight savings. Nuclear utilities prioritize neutron-hard sensors that align with IAEA safety targets. Imaging system OEMs, guided by new FDA and EU rules, now specify rad-tolerant analog front ends for CT and PET scanners. Scientific facilities such as CERN’s High-Luminosity Large Hadron Collider refresh detector electronics every shutdown using custom application-specific ICs built on radiation-hard-by-design libraries. Collectively, these shifts point to a gradual broadening of the customer base beyond traditional satellite integrators while keeping qualification pedigree at the center of procurement.

By Component: Mixed-Signal ICs Lead, FPGAs Gain Share

Analog and mixed-signal devices captured 35.21% of component revenue in 2025, reflecting their ubiquity in telemetry, sensor interfaces, and power conditioning. Voltage references, operational amplifiers, and high-precision data converters from Texas Instruments ship in every satellite bus, often rated to 100 kilorads total ionizing dose and single-event-latchup-immune. Field-programmable gate arrays expand at 4.41% per year, the fastest track among components. Microchip Technology’s RT PolarFire, built on 28 nanometer process nodes with radiation-hard-by-design cells, logged 14 orbital prime wins in 2025 and enables on-orbit reconfiguration of phased-array antennas and synthetic-aperture radar processors. Microcontrollers and microprocessors add roughly 18% of revenue, anchored by BAE Systems’ RAD5545 and Honeywell’s RAD750 lines that meet 1 megarad tolerance for deep-space jobs.

Complementary components fill critical roles. Non-volatile memory, including spin-transfer-torque MRAM, accounts for about 15% of revenue, valued for its immunity to single-event upsets at LET levels above 80 MeV·cm²/mg. Discrete semiconductors and power management ICs comprise the balance, and their relevance rises with electric propulsion. Infineon’s CoolGaN devices reach 98% efficiency in power-processing units, translating into lighter thermal systems for satellite buses. Taken together, the component breakdown shows a migration from fixed-function ASICs toward reconfigurable or software-defined elements that cut life-cycle cost and enable late-stage feature updates, a shift that benefits the radiation hardened electronics market.

By Product Type: Processors Outpace Analog Growth

Processors and controllers post a 5.01% CAGR through 2031, underscoring how software-defined payloads lean on high-clock-speed cores and embedded AI accelerators. AMD’s radiation-tolerant Versal platform stitches Arm cores, DSP blocks, and FPGA fabric on one die, letting operators run machine-learning inference for Earth observation without back-hauling raw imagery. Analog and mixed-signal lines remain the largest 35.21% revenue block thanks to precision power conversion and radio-frequency front ends, though digital filter chains are eating into legacy analog filtering. Digital logic devices, mainly FPGAs and ASICs, hold roughly one-third share as satellite cameras and radar arrays demand onboard data crunching.

Power and linear products have their own momentum. Texas Instruments’ TPS7H4003-SEP buck converter, qualified to 100 kilorads, delivers 97% peak efficiency, shaving 18% thermal mass versus older linear regulators. STMicroelectronics responds with system-basis chips that merge power sequencing, voltage monitoring, and CAN transceivers, reducing connector count by 30%. These hybrid devices illustrate how integration continues even in niche rad-hard categories, adding volume to the radiation hardened electronics market.

By Manufacturing Technique: RHBD Dominates Amid Foundry Constraints

Radiation-hard-by-design solutions delivered 52.43% of 2025 sales and will climb 4.12% yearly. Circuit-level redundancy, guard rings, and error-correcting code achieve acceptable cross-sections without exotic wafers so designers can tape out at mainstream fabs like TSMC. Microchip’s RT PolarFire demonstrates upset cross sections below 10^-9 cm²/bit at 37 MeV·cm²/mg, enough for geostationary missions. Radiation-hard-by-process flows remain vital for parts headed to Jupiter yet hold only 38% share due to 150 nanometer limits at the Manassas line. Software and firmware mitigation captures about 10%, evident in SpaceX Starlink satellites that rely on commercial SoCs with Linux-based scrubbing software. Hybrid schemes join both tactics as ESA’s ARTES program pursues 40% cost cuts with mixed RHBD cores and software-level correction.

The technique split spotlights a material cost lever inside the radiation hardened electronics market. RHBD runs can harness 28 nanometer or even 7 nanometer fabs, upping logic density while cutting power. RHBP parts remain crucial for deep-space probes, yet their wafer supply is capped and their die sizes stay large. Over the forecast window, design-centric hardening should seize more compute-intensive payloads, leaving specialized RHBP nodes for outer-planet science or human-rated systems.

By Semiconductor Material: GaN Gains on Silicon Legacy

Silicon still generated 64.27% of semiconductor revenue in 2025, anchored by bipolar-CMOS-DMOS analog flows that support operational amplifiers and precision ADCs. Gallium nitride advances 4.51% a year, the radiation hardened electronics market’s fastest material track. Infineon’s CoolGaN 650 V HEMTs pass 100 kilorads and single-event burnout at 75 MeV·cm²/mg, achieving 98% efficiency in Hall-effect thruster power supplies. Silicon carbide supplies roughly 8% and shows 38% year-over-year unit growth, especially in Schottky diodes for 600 V thruster controllers.

Other III-V materials, including gallium arsenide power amps and indium phosphide photodetectors, fill optical and RF niches, contributing the remaining 28% slice. Horizon Europe’s EPOSIC program delivered 1,200 V gallium-nitride on silicon prototypes to ESA in 2025, showcasing volume cost paths. The mix indicates that silicon’s dominance will shrink but not vanish, while GaN and SiC capture incremental power-conversion and high-frequency sockets.

By Radiation Type: SEE Mitigation Accelerates

Total ionizing dose shielding accounted for 48.33% of 2025 revenue, reflecting universal gamma accumulation in orbit. Components qualified to 100 kilorads are baseline for 15-year GEO missions. Single-event effects mitigation is rising fastest at 5.13% CAGR as medium Earth orbit constellations and deep-space craft face heavier ion flux than low Earth orbit.

Europa Clipper’s electronics needed LET immunity above 80 MeV·cm²/mg, removing over half the market’s part numbers during design reviews. Displacement damage dose solutions serve optoelectronics, while neutron-hard parts underpin nuclear-reactor sensors. The widening orbit altitudes and more ambitious science missions sustain investment across all three categories, yet SEE-focused ASICs and FPGAs stand out as the headline growth vector.

Geography Analysis

North America delivered 41.63% of 2025 revenue as the United States Space Force budgeted USD 29 billion for space systems and NASA bought hardware for Artemis lunar-gateway modules. Ongoing F-35 avionics and Next Generation Air Dominance flight computers extend demand. Canada contributes through star trackers and ground stations built by MDA, preserving share in niche sensors. The region’s future growth slows to the market average because NewSpace primes in California and Colorado have pivoted to commercial processors with software fault coverage, trimming the bill of material per spacecraft.

Asia Pacific is projected to expand at a 4.99% CAGR, the fastest regional clip in the radiation hardened electronics market. China’s eight newly connected Hualong One reactors each mandate neutron-hard control electronics rated to 10^14 neutrons per cm². India’s Gaganyaan crewed capsule specifies 50 kilorad avionics with triple-modular redundancy, while South Korea’s Nuri launch vehicle and lunar orbiter plans generate local sourcing mandates. Southeast Asian nuclear aspirations, led by Indonesia’s 2 GWe partnership with Rosatom, will surface near 2028 and 2029. Japan’s H3 launch vehicle and JAXA science missions continue to import mixed-signal ICs yet will localize microcontrollers through the Renesas-JAXA alliance.

Europe accounted for roughly 32% of 2025 revenue, centered on ESA’s EUR 1.8 billion Galileo Second Generation and Airbus OneWeb spacecraft builds.[3]European Space Agency, "Galileo Second Generation," esa.int The United Kingdom’s Tempest fighter piles on gallium-nitride demand, and EU Medical Device Regulation rules enlarge need for rad-tolerant CT scanner channels. The Middle East delivered about 6%, dominated by UAE’s Barakah nuclear program. South America and Africa stayed below 5%, although Brazil’s planned small modular reactor and South Africa’s Koeberg life-extension project form a pipeline. The dispersion shows how regional defense and energy strategies map directly onto capital flows in radiation hardened electronics.

Competitive Landscape

Market concentration is moderate. Honeywell, BAE Systems, CAES, Texas Instruments, and STMicroelectronics together hold about 60% of revenue, giving them scale to fund long qualification cycles. Each maintains spots on NASA and ESA qualified parts lists, which raises switching costs for integrators. BAE Systems runs the only North American RHBP fab, while Microchip’s 2018 purchase of Microsemi secured FPGA and discrete portfolios under one roof. Niche challengers include Vorago Technologies in microcontrollers, Everspin Technologies in MRAM, and Frontgrade Technologies in power management ICs, all thriving in cost-sensitive NewSpace constellations willing to adopt RHBD devices at 40% lower price points.

Technology roadmaps define share shifts. AMD’s 7 nanometer Versal ACAP offers gigabit throughput beyond legacy FPGAs, carving space in synthetic-aperture radar. Infineon filed 14 patents on GaN transistor layouts to cut single-event burnout, targeting electric-propulsion units that dominate geostationary telecom buses. Analog Devices purchased a 150 millimeter SOI line from X-FAB, adding 8,000 wafer starts per year and ensuring European RHBP supply. Export-control friction remains a wildcard; ITAR delays of nine months in 2024 allowed European and Asian vendors to win NATO satellite payload slots.

Company strategies are splitting. Incumbents double down on vertical integration, from wafer to packaged part, securing total ionizing dose and single-event guarantees. New entrants exploit mainstream foundries’ sub-28 nanometer nodes, bundling robust firmware scrubbing rather than costly process hardening. Both paths will coexist, with legacy players defending deep-space and human-rated missions while disruptors grab constellations refreshed every five years.

Radiation Hardened Electronics Industry Leaders

-

Honeywell International Inc.

-

BAE Systems plc

-

CAES (Cobham Advanced Electronic Solutions)

-

Texas Instruments Inc.

-

STMicroelectronics N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Microchip Technology announced that RT PolarFire FPGA-ES reached 100 kilorads total dose and LET immunity at 80 MeV·cm²/mg, adding 14 satellite design wins during 2025.

- October 2025: BAE Systems won a USD 89 million order to supply RAD5545 processors for the Next Generation Overhead Persistent Infrared constellation, with deliveries set through 2028.

- August 2025: Frontgrade Technologies secured USD 23 million to deliver power management ICs for the Space Development Agency transport layer of 150 satellites.

- June 2025: BAE Systems received GBP 317 million to build electronic-warfare suites for the Tempest fighter, embedding 300 kilorad gallium-nitride TR modules.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the radiation-hardened electronics market as new semiconductor devices and board-level modules purposely designed, processed, or firmware-shielded to survive total ionizing dose, displacement damage, and single-event effects in space, high-altitude defense assets, nuclear reactors, and medical accelerators. According to Mordor Intelligence, covered value streams span rad-hard ICs, power devices, sensors, and power-management subsystems supplied to satellite, defense, nuclear, medical, and research operators worldwide.

Scope exclusion: Discrete shielding materials, stand-alone test services, and refurbished legacy parts sit outside this scope.

Segmentation Overview

-

By End-User

- Space

- Aerospace and Defense (Air Land Naval)

- Nuclear Power Generation and Fuel Cycle

- Medical Imaging and Radiotherapy

- High-Altitude UAV/HAPS Platforms

- Industrial Particle Accelerators and Research Labs

-

By Component

- Discrete Semiconductors

- Sensors (Optical Image Environmental)

- Integrated Circuits (ASIC SoC)

- Microcontrollers and Microprocessors

- Memory (SRAM MRAM FRAM EEPROM)

- Field-Programmable Gate Arrays (FPGA)

- Power Management ICs

-

By Product Type

- Analog and Mixed-Signal

- Digital Logic

- Power and Linear

- Processors and Controllers

-

By Manufacturing Technique

- Rad-Hard-by-Design (RHBD)

- Rad-Hard-by-Process (RHBP)

- Rad-Hard-by-Software/Firmware Mitigation

-

By Semiconductor Material

- Silicon

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Other Semiconductor Materials

-

By Radiation Type

- Total Ionizing Dose (TID)

- Single-Event Effects (SEE)

- Displacement Damage Dose (DDD)

- Neutron and Proton Fluence

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Southeast Asia

- Rest of Asia Pacific

-

Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview spacecraft program managers, foundry engineers, radiation test-lab specialists, and procurement leads across North America, Europe, and Asia-Pacific. Their insights confirm dose thresholds, launch backlogs, price progressions, and adoption timing that documents alone cannot reveal.

Desk Research

We begin with open, high-quality data from NASA and ESA launch logs, US DoD budget books, IAEA reactor counts, Semiconductor Industry Association shipment series, IEEE papers, and customs trackers. Public company 10-Ks, investor decks, and reputable news accessed through Dow Jones Factiva and D&B Hoovers refine selling prices and vendor footprints. These references outline historical demand pools; many other repositories supported validation.

Market-Sizing & Forecasting

A top-down rebuild starts with satellite launches, reactor inventories, defense platform counts, and LINAC installs, then multiplies each pool by rad-hard content and refreshed average selling prices. Supplier roll-ups and targeted channel checks offer a bottom-up sense check. Key variables like launch cadence, semiconductor load per satellite, SiC/GaN yield trends, and defense modernization outlays feed a multivariate regression blended with scenario analysis through 2030; expert ranges close remaining gaps.

Data Validation & Update Cycle

Outputs pass variance screens, peer review, and anomaly checks. Models refresh annually, with interim updates after material events, and we run a fresh audit before delivery.

Why Mordor's Radiation Hardened Electronics Baseline Earns Trust

Published values often diverge because firms vary component mix, price decks, and refresh cadence. By anchoring scope strictly to rad-qualified electronics and updating variables each year, our team delivers a balanced baseline users can trace.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.88 B (2025) | Mordor Intelligence | |

| USD 1.69 B (2024) | Global Consultancy A | narrower component set; military emphasis |

| USD 1.60 B (2024) | Industry Analyst B | bundles shielding alloys; mixes currencies |

| USD 1.73 B (2024) | Trade Journal C | omits medical and research demand |

Taken together, the comparison shows our disciplined scope choice, traceable variables, and quicker refresh cadence make Mordor's numbers the dependable starting point for decision-makers.

Key Questions Answered in the Report

How large is the radiation hardened electronics market today?

The radiation hardened electronics market size reached USD 1.94 billion in 2026 and is expected to grow to USD 2.33 billion by 2031 at a 3.73% CAGR.

Which region expands fastest over 2026-2031?

Asia Pacific shows the strongest 4.99% CAGR, fueled by nuclear-new-build projects and growing domestic launch vehicle programs.

What component category grows quickest?

Field-programmable gate arrays register the highest 4.41% annual pace as satellite primes adopt on-orbit reconfigurable logic.

Why do qualification cycles restrain new entrants?

A single mixed-signal IC can incur USD 5-8 million in non-recurring engineering costs and 24-36 months of MIL-STD-883 or ESCC testing, delaying time to revenue.

How are wide-bandgap materials affecting product design?

Gallium nitride and silicon carbide devices reach 98% power-processing efficiency, cutting thermal mass and enabling higher-voltage electric propulsion units.

Which companies dominate the competitive landscape?

Honeywell International, BAE Systems, CAES, Texas Instruments, and STMicroelectronics together account for about 60% of market revenue.

Page last updated on: