Europe Passive Electronic Components In Aerospace And Defense Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

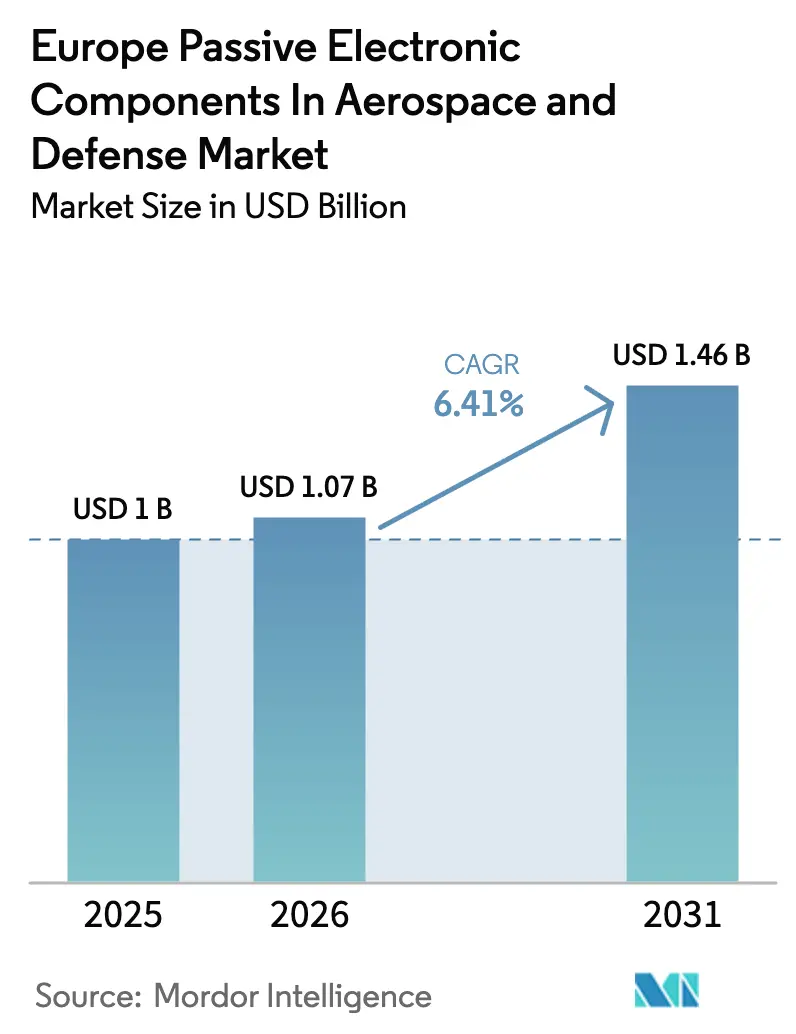

| Base Year Market Size (2025) | USD 1 Billion |

| Market Size (2026) | USD 1.07 Billion |

| Market Size (2031) | USD 1.46 Billion |

| Growth Rate (2026 - 2031) | 6.41% CAGR |

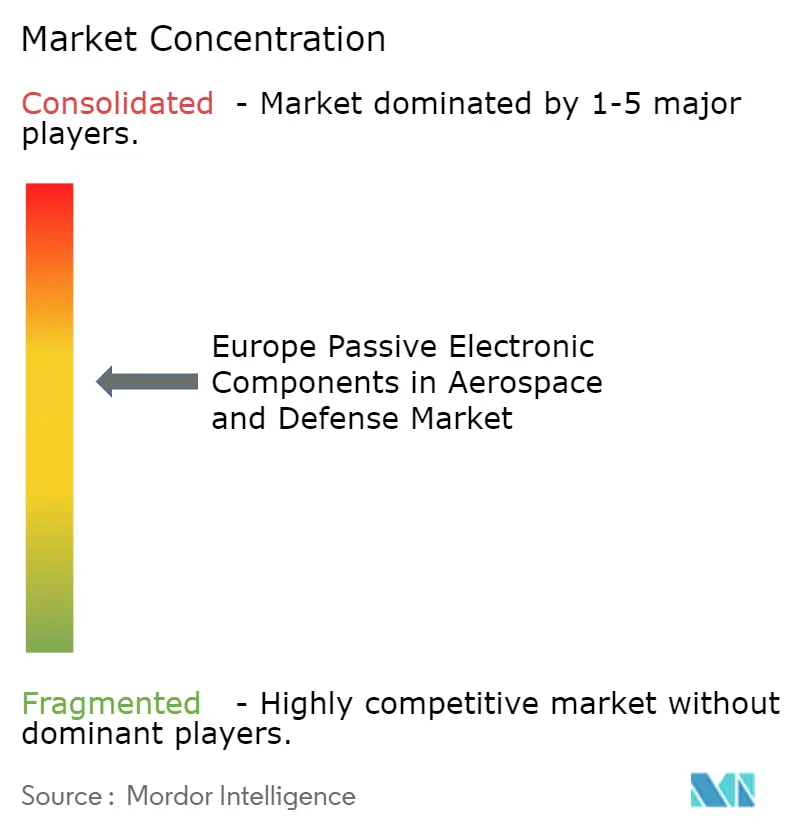

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Passive Electronic Components In Aerospace And Defense Market Analysis by Mordor Intelligence

The Europe passive electronic components in aerospace and defense market size is projected to expand from USD 1.07 billion in 2026 to USD 1.46 billion by 2031, registering a CAGR of 6.41% over 2026-2031. Electrified aircraft power-distribution architectures, sovereign defense-electronics priorities, and the accelerated fielding of counter-drone systems are converging to elevate unit demand as well as average content value per platform. Product qualification cycles remain long, yet recent European Union funding rounds have reduced time-to-market for high-temperature capacitors and low-loss RF filters, shortening historic design-in periods by as much as 20 months. At the same time, offset and localization clauses embedded in major airframe and missile procurements are channelling purchasing toward suppliers that operate fabrication or final-assembly assets inside the bloc, creating both entry barriers and pricing power for compliant vendors. Finally, sustained procurement of small satellites and tactical unmanned aerial vehicles is widening the addressable base beyond traditional fighter, transport, and rotorcraft programs, smoothing order volatility and supporting mid-single-digit growth momentum.

Key Report Takeaways

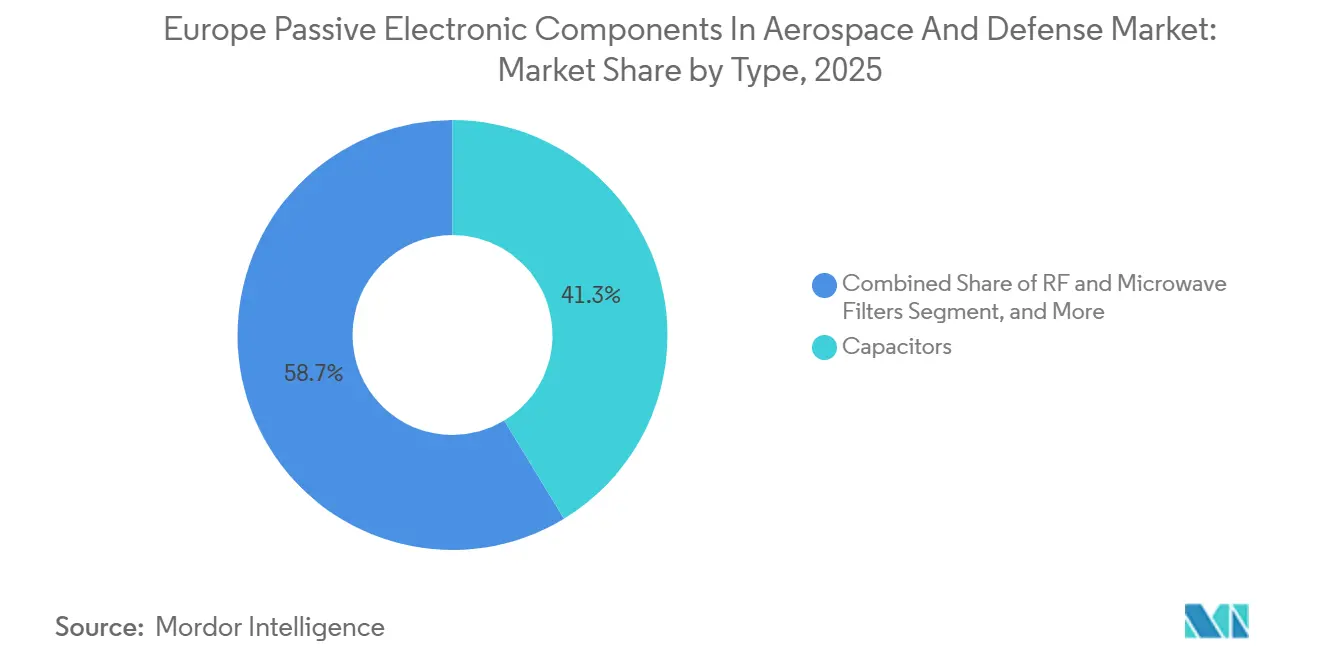

- By type, capacitors accounted for 41.32% of the Europe passive electronic components in aerospace and defense market share in 2025 while RF and microwave filters are forecast to expand at a 7.11% CAGR through 2031.

- By material, ceramic substrates commanded 36.91% of the Europe passive electronic components in aerospace and defense market size in 2025 and are projected to advance at a 6.97% CAGR over 2026-2031.

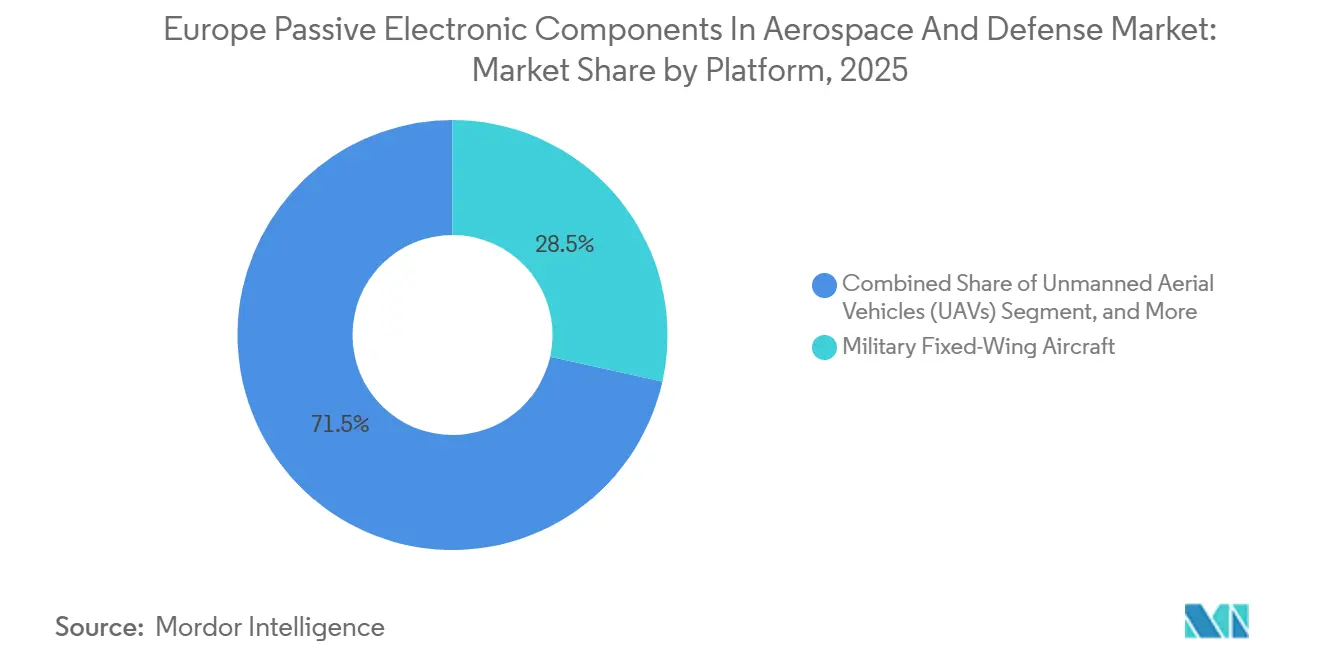

- By platform, military fixed-wing aircraft held 28.47% revenue share in 2025, whereas unmanned aerial vehicles are poised to record the highest growth at a 6.88% CAGR to 2031.

- By end-user, OEM production lines represented 52.18% of overall value in 2025 and are set to expand at a 7.23% CAGR, outpacing maintenance, repair, and overhaul channels.

- By geography, Germany led with 23.73% share in 2025, yet Spain is projected to post the fastest expansion at a 6.91% CAGR through 2031 as A400M output rises.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Passive Electronic Components In Aerospace And Defense Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in European defense-electronics modernization programmes | +1.20% | Germany, France, United Kingdom, Italy | Medium term (2-4 years) |

| Demand spike from small-sat and launch-service build-up in the United Kingdom, France and Germany | +1.00% | United Kingdom, France, Germany | Medium term (2-4 years) |

| More-Electric-Aircraft architectures driving high-temperature passives | +1.50% | Europe-wide, concentrated in France, Germany, United Kingdom | Long term (≥ 4 years) |

| EU-backed GaN power R&D catalyzing advanced passives integration | +0.90% | Europe-wide, led by Germany, France, Netherlands | Long term (≥ 4 years) |

| Offset and localization mandates favoring regional passive suppliers | +0.70% | France, Germany, Italy, Spain, Poland | Short term (≤ 2 years) |

| Rapid anti-drone and precision-munition deployment post-Ukraine conflict | +0.80% | Germany, Poland, Baltic states, Nordic countries | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in European Defense-Electronics Modernization Programmes

Defense spending climbed across the continent in 2025 as Germany, France, and the United Kingdom each met or exceeded the NATO 2% of GDP threshold. Procurement budgets now earmark avionics, radar, and electronic-warfare upgrades as top priorities, accelerating the qualification of AS9100-certified capacitors, resistors, and filters suited for extended temperature and radiation exposure.[1]European Commission, "European Defence Fund," defence-industry-space.ec.europa.eu National content clauses stipulating that at least half of electronic components be sourced inside the European Union are steering prime contractors toward regional vendors, shortening design-win cycles, and lifting the average selling price for high-reliability passives.

Demand Spike from Small-Sat and Launch-Service Build-Up in the United Kingdom, France and Germany

The commercial and institutional small-satellite backlog exploded after OneWeb began its second-generation constellation while Arianespace secured long-term launch contracts valued at EUR 2.1 billion (USD 2.37 billion) in 2025.[2]Arianespace, "Arianespace Contracts and Launch Services," arianespace.com Each spacecraft embeds upwards of 12,000 multilayer ceramic capacitors, 600 precision resistors, and scores of inductors, pushing annual component demand well above historical averages. Government grants to NewSpace launch startups are amplifying the pull for European-made inductors and transformers that bypass United States International Traffic in Arms Regulations.

More-Electric-Aircraft Architectures Driving High-Temperature Passives

Commercial transports such as the Airbus A320neo now route roughly 1.5 MW of electric power, up from near-zero a decade ago, forcing designers to specify film capacitors and thick-film resistors that remain stable at temperatures up to 200 °C.[3]IEEE Xplore, "High-Temperature Passive Components for More-Electric Aircraft," ieeexplore.ieee.org Similar requirements are appearing on hybrid-electric demonstrators funded under the Clean Aviation Joint Undertaking, where silicon-carbide and gallium-nitride inverters operate above 600 V DC and demand ceramic capacitors with single-digit milliohm equivalent series resistance.

EU-Backed GaN Power R&D Catalyzing Advanced Passives Integration

Horizon Europe consortia such as ALL2GaN and GaN4AP collectively received EUR 47 million (USD 53 million) during 2024-2025 to mature 650-V and 1,200-V gallium-nitride modules. The high switch-frequency capability of GaN devices slashes filter and inductor size by up to 60% but also tightens ripple-current and dielectric-loss specifications for input and output capacitors. Early field deployment on Airbus auxiliary-power-unit starters demonstrated inverter efficiencies of 98.5%, validating the commercial case for low-loss ceramic and film dielectrics.[4]Infineon Technologies, "CoolGaN Power Platform," infineon.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Geopolitical volatility of tantalum and ferrite supply | -0.60% | Europe-wide, acute in Germany, France, United Kingdom | Short term (≤ 2 years) |

| Cost burden of REACH-compliant lead-free redesigns | -0.50% | Europe-wide, particularly Germany, France, Italy | Medium term (2-4 years) |

| Limited EU ceramic-capacitor fab capacity lengthening lead times | -0.40% | Europe-wide, concentrated in Germany, Czech Republic | Short term (≤ 2 years) |

| Integration of SiP solutions reducing discrete passive counts | -0.30% | Europe-wide, led by France, United Kingdom | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Geopolitical Volatility of Tantalum and Ferrite Supply

Export restrictions introduced by the Democratic Republic of the Congo and Rwanda in early 2025 lifted tantalum spot prices by 42% within nine months, squeezing margins for capacitor manufacturers and triggering redesign activity toward polymer-aluminium options where feasible. Simultaneously, China’s ferrite quota reduced European ferrite-powder availability by 18%, compelling inductor suppliers to evaluate larger powdered-iron or air-core alternatives that occupy more board area and dissipate extra heat.

Cost Burden of REACH-Compliant Lead-Free Redesigns

Although aerospace platforms historically enjoyed exemptions from lead-free mandates, the 2024 European Chemicals Agency review recommended phasing them out by 2030. Switching to tin-silver-copper solder raises peak reflow temperatures from 220 °C to 245 °C, degrading capacitance stability by up to 8% in class-II multilayer ceramic parts and requiring fresh DO-160G thermal-shock validation. Qualification budgets ranging from EUR 150,000 to EUR 300,000 (USD 169,000-338,000) per component family deter smaller firms and strengthen the incumbency advantage of suppliers with existing in-house reliability laboratories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: RF and Microwave Filters Elevate Growth Trajectory

RF and microwave filters are on track to post a 7.11% CAGR through 2031, outpacing the Europe passive electronic components in aerospace and defense market average as active electronically scanned array radar proliferates. The segment’s upside is anchored in gallium-nitride power amplifiers that switch at multi-megahertz frequencies and therefore require low-loss filtering to mitigate harmonic distortion. Capacitors retained a dominant 41.32% share in 2025 thanks to their ubiquitous presence in decoupling and back-up power circuits, though discrete unit volumes are plateauing as system-in-package integration advances.

Inductors and transformers maintain indispensable roles in switch-mode power supplies for flight-control computers, while niche devices such as varistors and thermistors handle transient suppression and temperature compensation. Thales’s Ground Master 200 radar alone employs more than 2,400 surface-mount RF capacitors per array face, underscoring the component intensity inherent in phased-array architectures. The Europe passive electronic components in aerospace and defense market size for RF filters is forecast to rise to USD 0.27 billion by 2031, reflecting both price and volume expansion.

By Material: Ceramic Substrates Consolidate Leadership

Ceramic substrates carried 36.91% share in 2025 and will keep leadership as gallium-nitride-ready formulations rated above 200 °C gain adoption. These multilayer ceramic capacitors deliver lower equivalent series resistance than polymer or aluminium electrolytic alternatives, unlocking 40% mass reduction in inverter modules for hybrid-electric demonstrators. Tantalum remains essential for high-density back-up power circuits, but intense price volatility is steering designers toward polymer-aluminium technology when board space allows.

Film capacitors made with polypropylene or polyphenylene-sulfide dielectrics underpin snubber and DC-link circuits inside actuation drives and radar transmitters, whereas ferrite materials enable inductors and transformers in switching regulators below 10 MHz. The Europe passive electronic components in aerospace and defense market share for ceramic materials is projected to widen modestly as additional capacity comes online in Austria and the Czech Republic, shaving average lead times to near 16 weeks by 2027.

By Platform: Unmanned Aerial Vehicles Outpace Legacy Airframes

Unmanned aerial vehicles are forecast to expand at a 6.88% CAGR, reflecting accelerated defense procurement of tactical reconnaissance drones, loitering munitions, and rotary-wing uncrewed systems after the Ukraine conflict reshaped battlefield intelligence requirements. Each medium-altitude long-endurance airframe contains roughly 5,000 multilayer ceramic capacitors, 1,400 resistors, and 300 inductors across flight-control, navigation, and secure-data-link subsystems.

Military fixed-wing aircraft kept a sizable 28.47% share in 2025 as Eurofighter Typhoon and Dassault Rafale avionics entered major retrofit phases, embedding more than 10,000 passives per jet. Rotorcraft and commercial transports contribute steady pull, while the missile and precision-munition niche, though smaller in absolute value, commands premium pricing because components must withstand launch acceleration up to 15,000 g and extreme thermal shock.

By End-User: OEM Production Lines Drive Volume

OEM production lines captured 52.18% revenue in 2025 and will remain the largest outlet because initial assembly embeds most passives. Line-replaceable units ordered by Airbus, Leonardo, Dassault, and Saab often fix part numbers for 20+ years, guaranteeing volume stability but imposing rigorous AS9100 and IATF 16949 compliance. Maintenance, repair, and overhaul demand remains steady for aging fleets such as the Tornado, yet its CAGR is capped at 5.1% as European budgets pivot toward new-build programs.

Offset requirements further fortify OEM-centric demand: Poland’s FA-50 avionics contract obliges 50% European Union content, prompting Thales to dual-source capacitors from AVX Czech Republic and WIMA Germany rather than low-cost Asian vendors. MRO shops, faced with shorter planning horizons, rely on distributors and carry negligible sway over future product roadmaps.

Geography Analysis

Germany held a commanding 23.73% of the Europe passive electronic components in aerospace and defense market in 2025, anchored by Airbus aircraft final assembly, Hensoldt radar production, and MTU Aero Engines power electronics. More than 400 million passives flowed annually into German facilities, and the nation’s co-leadership role in the Future Combat Air System imposes a 50% European content clause that heavily favours domestic capacitor and resistor suppliers.

Spain is projected to advance at a 6.91% CAGR as Airbus boosts A400M output in Seville from 12 airframes in 2025 to at least 18 in 2026, each airlifter integrating nearly 10,000 passives across flight-control and mission-computer chains. The program’s supply-chain strategy requires 60% European Union content, accelerating qualification of local ceramic-capacitor vendors.

France combines Dassault Rafale assembly, Thales avionics, and Safran engine-control production to consume roughly 320 million passives in 2025. Ongoing Rafale F4 electronic-warfare upgrades and Scorpion armoured-vehicle deployments sustain appetite for rugged film capacitors and thick-film resistors capable of surviving electromagnetic pulses.

The United Kingdom contributes sizable demand through BAE Systems Typhoon manufacturing and Rolls-Royce engine-control units, yet Brexit-induced customs latency added an average 8 days to 2025 lead times. Italy’s Leonardo helicopter lines follow, whereas the rest of Europe, led by Poland and Sweden, accounts for 18% share. Poland’s defense expenditure rose to 4.7% of GDP, spurring orders for tactical drones that require European-sourced passives to satisfy 60% domestic-content clauses.

Competitive Landscape

The top five players, KEMET, TDK, Vishay, Murata, and AVX, collectively held approximately 48% of the Europe passive electronic components in aerospace and defense market in 2025, with no single firm exceeding 12% share. Multi-decade qualification approvals from Airbus, Leonardo, Thales, and BAE Systems create steep barriers for new entrants, as DO-160G and MIL-PRF-55365 testing cycles span 18 to 36 months. European specialists such as Exxelia, WIMA, and TT Electronics differentiate through localized engineering support, faster prototyping, and willingness to customize low-volume, high-reliability variants, capturing 15% to 20% of niche segments such as space-qualified tantalum capacitors and pulse-rated film devices.

Technology deployment focuses on material innovation: TDK's CeraLink capacitors, featuring a lead-free relaxor ferroelectric dielectric rated for 300 V and 150 °C, entered Airbus A320neo auxiliary-power-unit starters in 2024. Vishay expanded its thin-film resistor portfolio in 2025 to include 0.01% tolerance variants for fly-by-wire current sensing, while Murata disclosed silicon-capacitor prototypes that deliver 10 times higher capacitance density and intrinsic radiation tolerance exceeding 1 megarad.

Offset and localization mandates favour suppliers with European fabrication footprints: AVX expanded its Czech Republic facility in 2025, and Panasonic acquired a tantalum-capacitor line in Pardubice to serve defense contracts stipulating 50% domestic content by value. White-space opportunities exist in gallium-nitride-compatible RF capacitors, high-temperature ceramic formulations for more-electric-aircraft inverters, and radiation-hardened inductors for satellite constellations, segments where performance specifications exceed legacy product capabilities and justify premium pricing.

Europe Passive Electronic Components In Aerospace And Defense Industry Leaders

-

KEMET Corporation (Yageo Group)

-

Panasonic Corporation

-

TDK Corporation

-

Vishay Intertechnology Inc.

-

AVX Corporation (Kyocera Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Exxelia introduced the CF/CFS Series pulse capacitors featuring integrated bleed resistors for defense and launch systems.

- April 2025: The European Commission launched the EUR 150 billion SAFE joint arms-procurement program mandating 65% EU-origin components.

- March 2025: Germany unveiled a dual investment strategy coupling unlimited defense spending with a EUR 500 billion infrastructure fund.

- March 2025: The European Commission proposed a EUR 150 billion loan facility to boost joint defense procurements.

- February 2025: Exxelia launched high-performance silvered-mica capacitors for RF and aerospace applications.

Europe Passive Electronic Components In Aerospace And Defense Market Report Scope

The Europe Passive Electronic Components in Aerospace and Defense Market Report is Segmented by Type (Capacitors, Resistors, Inductors, Transformers, RF and Microwave Filters, Others), Material (Ceramic, Tantalum, Aluminum Electrolytic, Film, Ferrite, Carbon Composition and Thick Film), Platform (Commercial Fixed-Wing Aircraft, Military Fixed-Wing Aircraft, Rotorcraft, UAVs, Missiles and Precision Munitions, Spacecraft and Satellites), End-User (OEM Production Lines, MRO), and Geography (Germany, France, United Kingdom, Italy, Spain, Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

| Capacitors |

| Resistors |

| Inductors |

| Transformers |

| RF and Microwave Filters |

| Others Type |

| Ceramic |

| Tantalum |

| Aluminum Electrolytic |

| Film |

| Ferrite |

| Carbon Composition and Thick Film |

| Commercial Fixed-Wing Aircraft |

| Military Fixed-Wing Aircraft |

| Rotorcraft |

| Unmanned Aerial Vehicles (UAVs) |

| Missiles and Precision Munitions |

| Spacecraft and Satellites |

| OEM Production Lines |

| Maintenance, Repair and Overhaul (MRO) |

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Rest of Europe |

| By Type | Capacitors |

| Resistors | |

| Inductors | |

| Transformers | |

| RF and Microwave Filters | |

| Others Type | |

| By Material | Ceramic |

| Tantalum | |

| Aluminum Electrolytic | |

| Film | |

| Ferrite | |

| Carbon Composition and Thick Film | |

| By Platform | Commercial Fixed-Wing Aircraft |

| Military Fixed-Wing Aircraft | |

| Rotorcraft | |

| Unmanned Aerial Vehicles (UAVs) | |

| Missiles and Precision Munitions | |

| Spacecraft and Satellites | |

| By End-User | OEM Production Lines |

| Maintenance, Repair and Overhaul (MRO) | |

| By Country | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe passive electronic components in aerospace and defense market by 2031?

The Europe passive electronic components in aerospace and defense market size is forecast to reach USD 1.46 billion by 2031, expanding at a 6.41% CAGR from 2026.

Which material segment dominates the Europe passive electronic components in aerospace and defense market?

Ceramic substrates commanded 36.91% share in 2025 and are advancing at a 6.97% CAGR, driven by gallium-nitride-ready formulations for high-temperature inverters and radar modules.

Why are unmanned aerial vehicles growing faster than other platforms?

Unmanned aerial vehicles are expanding at a 6.88% CAGR as European defense ministries procure tactical reconnaissance drones and loitering munitions following the Ukraine conflict.

What role do offset and localization mandates play?

Offset clauses requiring 40% to 60% European Union content favor suppliers with regional fabrication, accelerating qualification cycles and elevating pricing power for compliant vendors.

Which country leads the regional market?

Germany held 23.73% share in 2025, anchored by Airbus, Hensoldt, and MTU Aero Engines, yet Spain is forecast to grow fastest at a 6.91% CAGR as A400M output rises.

How does supply-chain volatility affect the market?

Geopolitical restrictions on tantalum and ferrite supply triggered price spikes of 42% in 2025, compelling redesigns toward polymer-aluminum capacitors and powdered-iron inductors where feasible.

Page last updated on: