Electromagnetic Interference (EMI) Shielding Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

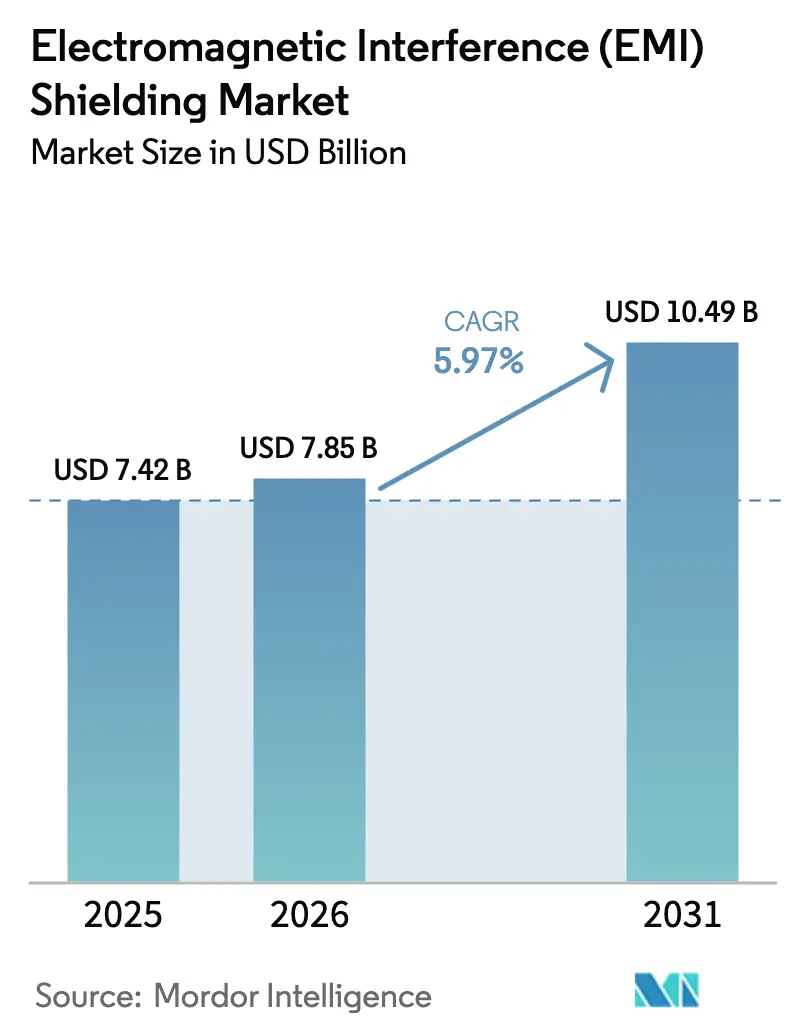

| Market Size (2026) | USD 7.85 Billion |

| Market Size (2031) | USD 10.49 Billion |

| Growth Rate (2026 - 2031) | 5.97% CAGR |

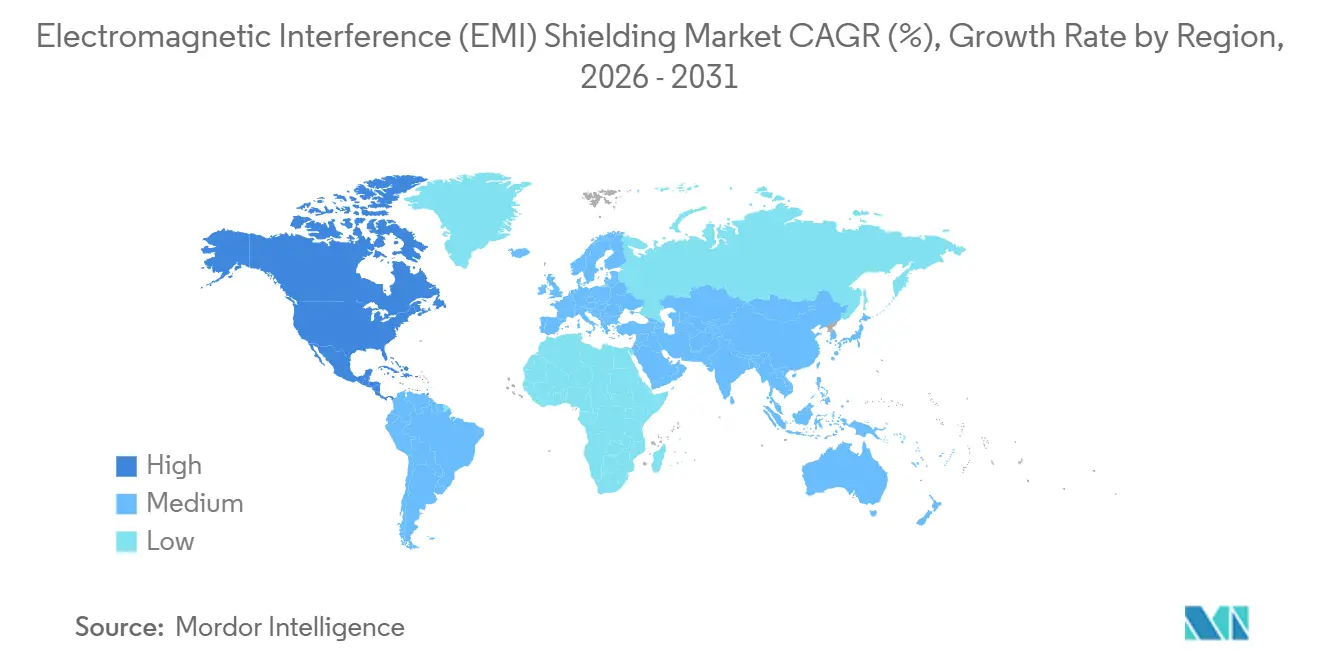

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

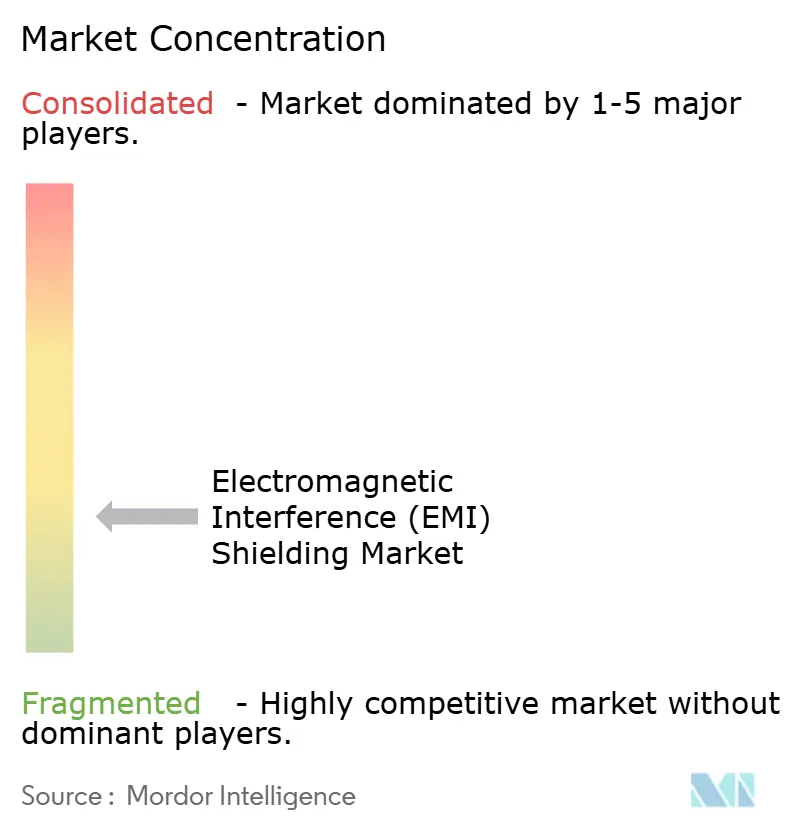

| Market Concentration | Low |

Major Players-shielding-market/electromagnetic-interference-(emi)-shielding-market-1753429347798-major-players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electromagnetic Interference (EMI) Shielding Market Analysis by Mordor Intelligence

The Electromagnetic Interference Shielding Market size was valued at USD 7.42 billion in 2025 and is estimated to grow from USD 7.85 billion in 2026 to reach USD 10.49 billion by 2031, at a CAGR of 5.97% during the forecast period (2026-2031). Performance-critical deployments in AI data centers, 5G base stations, and electric-vehicle powertrains are replacing compliance-only purchases as signal-integrity stakes rise. Asia-Pacific led with 41.40% revenue in 2025, owing to smartphone and EV battery hubs, while North America is projected to expand fastest at 6.55% CAGR on hyperscale data-center buildouts that need RF-shielded liquid-cooled racks. Conductive coatings held a 32.70% material share in 2025, yet lighter conductive polymers are set to grow at 6.12% CAGR as designers favor corrosion resistance in foldable phones and wearables. Gasket shielding captured 53.00% of 2025 method revenue and remains essential for automotive door modules that must survive 100,000 open-close cycles without losing less than 1 Ω contact resistance. The 1-6 GHz band still dominates at 62.00%, but sub-THz demand is rising at 6.11% CAGR as satellite constellations and millimeter-wave small cells proliferate.

Key Report Takeaways

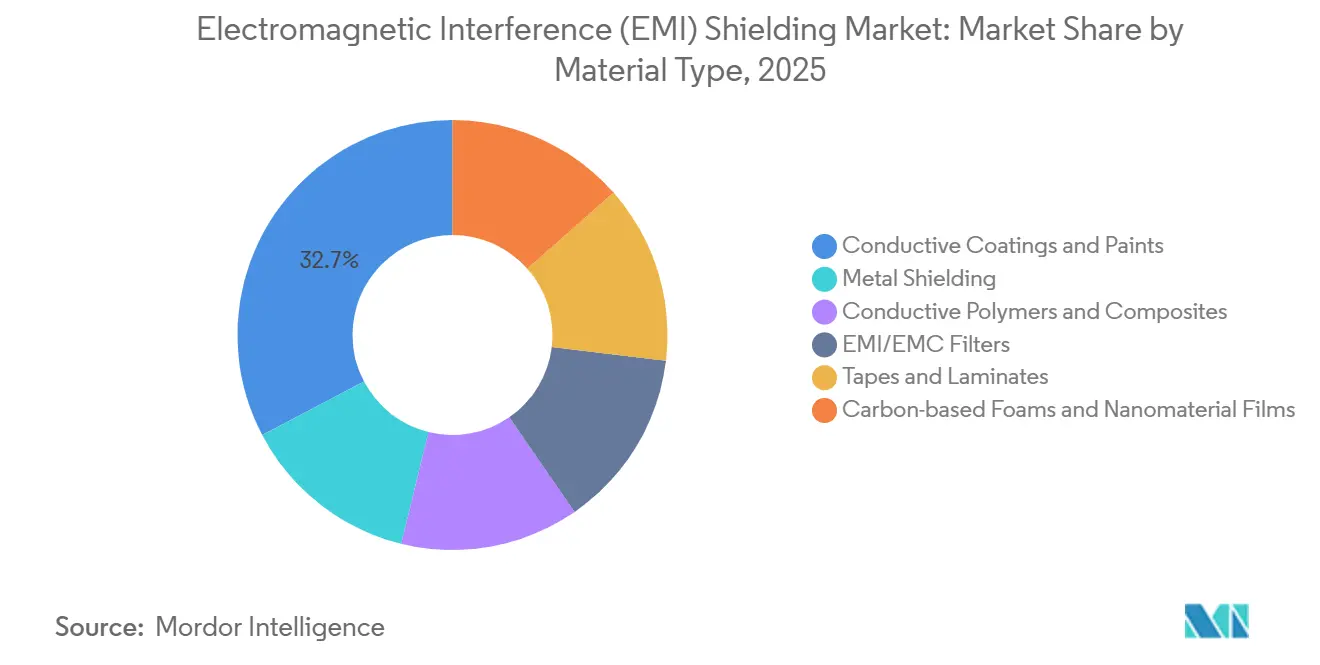

- By material type, conductive coatings and paints led with 32.70% revenue share in 2025, and the share of conductive polymers and composites is poised to increase with a CAGR of 6.12% during the forecast period (2026-2031).

- By shielding method, gasket shielding captured 53.15% of the electromagnetic interference shielding market share in 2025, and this share is expected to increase with a CAGR of 6.23% during the forecast period (2026-2031).

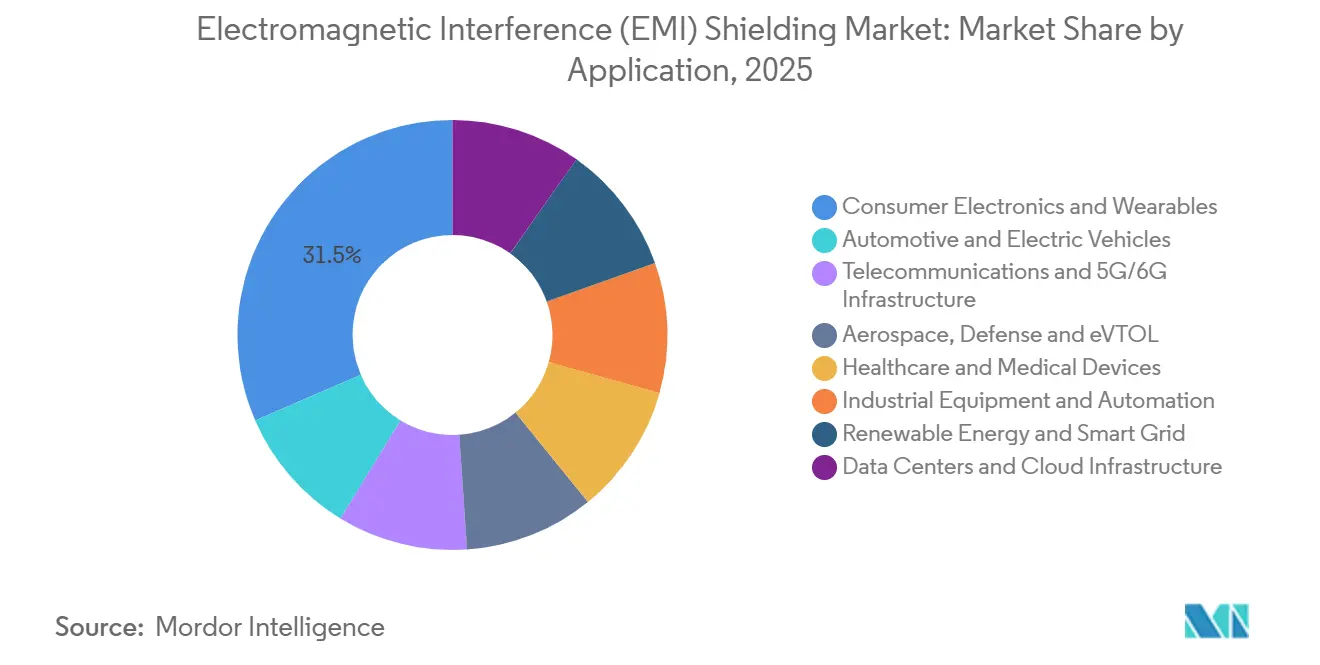

- By application, consumer electronics and wearables accounted for 31.50% of the electromagnetic interference shielding market size in 2025, while data centers and cloud infrastructure are expected to record the fastest 6.32% CAGR to 2031.

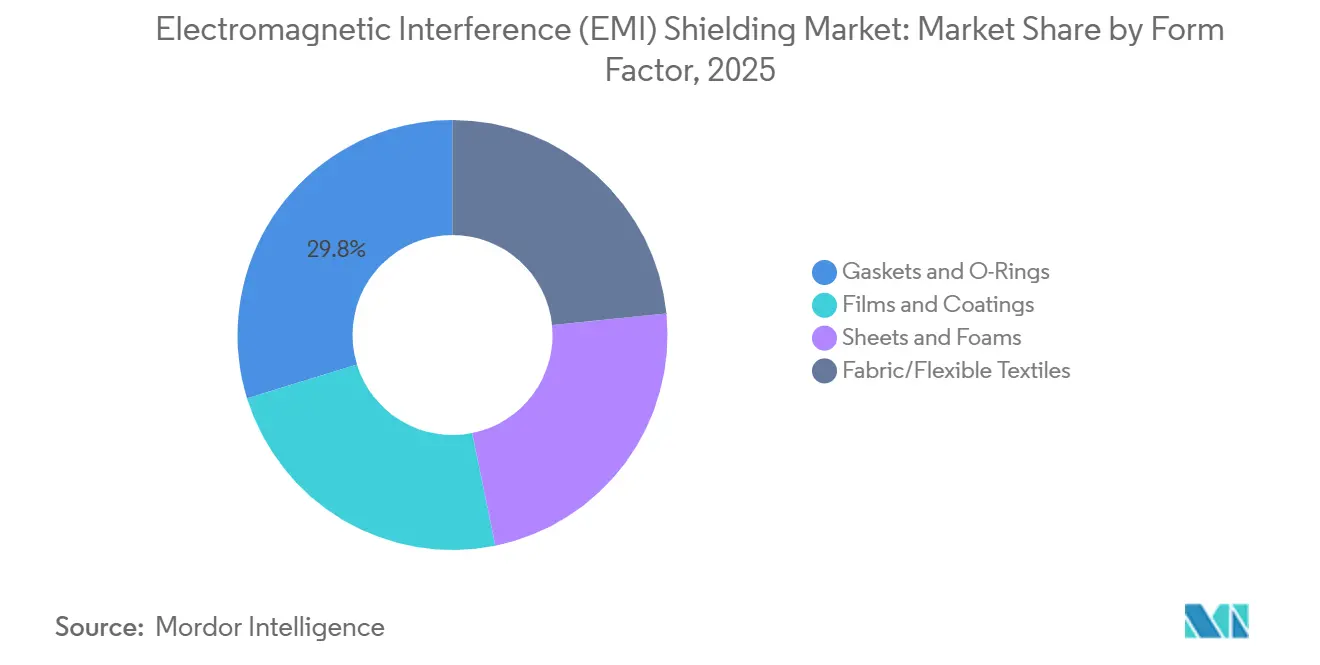

- By form factor, gaskets and O-rings had the share of 29.77% in 2025 and films and coatings' share is poised to grow with a CAGR of 6.41% during the forecast period (2026-2031).

- By geography, Asia-Pacific held 41.40% of the electromagnetic interference shielding market share in 2025 and North America is advancing at a 6.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electromagnetic Interference (EMI) Shielding Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging adoption of consumer electronics and wearables | +1.8% | Global, with APAC core and spill-over to North America & Europe | Medium term (2-4 years) |

| Rapid 5G/mm-Wave infrastructure rollout | +1.6% | North America, Europe, APAC (China, South Korea, Japan) | Short term (≤ 2 years) |

| Stricter global EMC regulations in auto, medical and aero sectors | +1.2% | Europe (automotive), North America (medical, aerospace), APAC (automotive) | Long term (≥ 4 years) |

| Vertical-specific satellite constellations driving on-board shielding demand | +0.5% | Global, with concentration in North America launch hubs | Medium term (2-4 years) |

| Chiplet and SiP compartment-level shielding in advanced packaging | +0.9% | APAC (Taiwan, South Korea), North America (design hubs) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Adoption of Consumer Electronics and Wearables

Smartphones, smartwatches, and earbuds are shrinking, so engineers now specify shielding layers thinner than 10 μm that still deliver over 60 dB attenuation from 2.4-6 GHz. MXene-based fabrics achieve 42 dB in a single layer and 69 dB in triple stacks while enduring more than 500 bends, making them ideal for curved wearable surfaces. Foldable-phone hinges flex over 200,000 times; silver-nanowire inks keep 31,000 S/cm conductivity even under 50% strain, preventing RF leakage paths. As transparent, stretchable, and washable films mature, suppliers with roll-to-roll coating lines will outpace traditional metal-can vendors.

Rapid 5G/mm-Wave Infrastructure Rollout

Millimeter-wave base stations at 26 GHz and 39 GHz need board-level shields rated above 80 dB because low-loss polytetrafluoroethylene (PTFE) and liquid-crystal-polymer substrates amplify radiated emissions. Federal Communications Commission (FCC) Part 15 and European Telecommunications Standards Institute (ETSI) EN 301 489 tightened in 2024, so OEMs (Original Equipment Manufacturers) now buy molded assemblies that combine thermal vias and EMI gaskets, cutting production steps. North American small-cell counts are on track to top 1 million by 2028, and data-center operators near Washington D.C. already retrofit racks with 60-80 dB panels after graphics processing unit (GPU) memory-error incidents[1]FCC, “Part 15 Radio Frequency Devices,” fcc.gov.

Stricter Global EMC Regulations in Auto, Medical and Aero Sectors

CISPR 12 Edition 7.0 and UNECE R10 Revision 7 raised vehicle emission and immunity limits in 2025. Automakers now demand conductive-elastomer gaskets that hold compression-set below 10% after 168 hours at 125°C; performance fabric-over-foam parts cannot match[2]United Nations, “UNECE R10 Revision 7,” unece.org. Medical devices must meet IEC 60601-1-2 Edition 5.0, while MIL-STD-461G drives aerospace demand for cable shields able to cut induced currents from 200 kA lightning strikes to about 1 A.

Chiplet and SiP Compartment-Level Shielding in Advanced Packaging

As chiplet designs spread, crosstalk rises. Laser-patterned molded-package walls give more than 70 dB isolation between RF and baseband in 5G modules without post-sputter steps, but the epoxy walls need less than 0.1 Ω·cm resistivity and matched thermal expansion to stay bonded across 1,000 thermal cycles. Electrospray-printed silver films deliver 60 dB at 25 μm thickness with 90% material yield, cutting per-package cost by about 40%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced shielding materials and processes | -0.9% | Global, with acute pressure in cost-sensitive consumer segments | Medium term (2-4 years) |

| Form-factor constraints in ultra-compact and foldable devices | -0.4% | APAC (consumer electronics hubs), North America (wearables) | Short term (≤ 2 years) |

| Copper-price volatility elevating BOM risk in large-volume programs | -0.7% | Global, with heightened exposure in automotive and telecom infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Shielding Materials and Processes

Nanomaterial films can exceed USD 200 per kg, ten times the price of nickel-coated carbon fibers. Vacuum sputtering tools cost above USD 500,000 and run 30-60 minute cycles, while ultrasonic coaters have lower capital needs, at roughly USD 50,000, but add ink-formulation complexity. Certification adds 15-20% to development budgets, so small firms without in-house Electromagnetic Compatibility (EMC) labs face delayed launches.

Copper-Price Volatility Elevating BOM Risk

London Metal Exchange copper neared USD 11,735 per ton late in 2025; every USD 2,000 swing lifts gasket bills of material by up to 10% for auto and telecom volumes. United States tariffs on semi-finished copper and scant domestic smelting intensify sourcing risk. Aluminum or polymer substitutes either need thicker sections or lack durability, making real-time hedging and closed-loop recycling vital for margin stability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Conductive Polymers Gain as Corrosion and Weight Drive Substitution

Conductive coatings and paints controlled 32.70% of revenue in 2025, sustained by their compatibility with spray, brush, and dip-coating processes that integrate seamlessly into existing production lines without capital-intensive tooling changes. Metal shielding still dominates high-robustness roles such as avionics bays that need more than 80 dB attenuation.

Conductive polymers and composites will grow at 6.12% CAGR to 2031, attract designers seeking corrosion immunity in marine and outdoor telecom enclosures; polyaniline/nickel-ferrite composites achieved 78.07 dB shielding effectiveness in K-band with absorption-dominant mechanisms and Green Index above 1.0, signaling environmental advantages over hexavalent-chromate surface treatments banned under EU REACH. Hybrid TPU composites now post 312 S/cm conductivity, so suppliers offering multi-material portfolios can cross-sell within shrinking vendor lists.

By Shielding Method: Gasket Dominance Reflects Automotive and Telecom Enclosure Cycles

Gasket Shielding held 53.15% method share in 2025 and will grow at 6.23% CAGR during the forecast period (2026-2031), propelled by automotive OEMs specifying conductive-elastomer and fabric-over-foam gaskets that maintain less than 1 Ω contact resistance across 100,000 door-open cycles and withstand underhood temperatures reaching 125°C. Board-Level Shielding captures smartphone and IoT-module demand, yet this segment faces margin pressure as module vendors shift to molded shielding integrated during substrate fabrication.

Conformal Coating serves cost-sensitive consumer applications, set-top boxes, and smart speakers, where spray-applied silver or nickel paints deliver 30-50 dB attenuation sufficient for FCC Part 15 Class B compliance without tooling investment. Cable Shielding and Enclosure and Vent Shielding address infrastructure markets: data-center operators installing liquid-cooled AI racks require RF-shielded ventilation panels with honeycomb mesh that attenuates 60-80 dB at 1-6 GHz while sustaining airflow above 200 CFM to prevent thermal throttling.

By Application: Data Centers Surge as AI Workloads Impose Zero-Error Tolerance

Consumer electronics generated 31.50% of 2025 sales, yet replacement cycles are lengthening. Data centers and cloud infrastructure are forecast to post the fastest 6.32% CAGR during the forecast period (2026-2031); a 2024 incident in a Northern Virginia server farm showed GPU memory errors tied to 5G edge nodes, spurring retrofits with 80 dB rack panels. Automotive EMC labs grew to USD 1.83 billion in 2024 and head toward USD 3.11 billion by 2031 as battery inverters spew broadband noise.

Healthcare and Medical Devices, Industrial Equipment and Automation, Renewable Energy and Smart Grid round out the application portfolio, each imposing sector-specific standards, IEC 60601 for medical, IEC 61326 for in-vitro diagnostics, and IEC 61000 for industrial, which fragments supplier go-to-market strategies and rewards domain expertise over scale.

By Form Factor: Films and Coatings Accelerate on Wearable and Flexible-Display Adoption

Gaskets and O-rings owned 29.77% revenue in 2025, driven by automotive door seals and telecom-enclosure closures requiring repeatable compression and environmental sealing alongside EMI attenuation. Films and Coatings, forecast at 6.41% CAGR, capture wearable and flexible-display demand; Panasonic's March 2026 launch of FineX transparent conductive film, featuring ultra-fine copper mesh with optical-clear-adhesive backing, targets industrial HMIs and touch screens where more than 90% optical transmissivity and less than 1 Ω/sq sheet resistance enable EMI shielding without compromising display clarity.

The form-factor segmentation's trajectory toward thinner, lighter, and more conformable solutions aligns with miniaturization trends, and suppliers that master roll-to-roll coating and laser patterning will gain cost and lead-time advantages over traditional stamping and die-cutting operations.

Geography Analysis

Asia-Pacific commanded 41.40% of revenue in 2025, anchored by China's electronics-manufacturing base, where Shenzhen and Dongguan clusters assemble over 60% of global smartphones and wearables, and India's expanding EV cell-production capacity, which is attracting battery-management-system shielding demand. Japan logged about USD 900 million on advanced ferrite cores for 2-6 GHz modules. South Korea’s 5G leadership and Samsung investments uplift chiplet shielding, while Singapore and Jakarta data centers spike vent-panel demand.

North America, forecast to grow fastest at 6.55% CAGR through 2031, benefits from hyperscale data-center expansion and 5G infrastructure investment; Northern Virginia alone accounted for over 30% of regional EMI-shielding ventilation-panel consumption in 2025 as operators co-locate GPU clusters and edge nodes within the same facilities.

Europe held a significant share in 2025, driven by Germany's automotive and industrial base and stringent EU REACH regulations that accelerate the substitution of hexavalent-chromate coatings with conductive polymers. France's aerospace and defense sectors demand lightning-strike-certified cable shields and MIL-STD-461G enclosures, while the United Kingdom's 5G rollout and smart-grid investments support telecom and industrial-automation segments. South America and Middle East and Africa remain emerging markets, with Brazil's aerospace clusters and UAE's smart-city projects providing niche opportunities, yet limited local manufacturing and reliance on imports constrain growth relative to established regions.

Competitive Landscape

The Electromagnetic Interference (EMI) Shielding market is fragmented. MXene and graphene startups promise 70 dB at 1 μm, thinning form factors for foldables. Regional specialists such as Holland Shielding and Huarui Honeycomb dominate vent panels near car and telecom plants. Defense and medical buyers still demand AS9100D or ISO 13485 plus MIL-STD-461G reports, carving the market into high-reliability and commercial tiers.

Electromagnetic Interference (EMI) Shielding Industry Leaders

3M

DuPont

Henkel AG & Co. KGaA

Parker-Hannifin Corporation

PPG Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: At Productronica 2025, the premier global trade fair for electronics development and manufacturing, Henkel AG & Co. KGaA unveiled a diverse range of innovations and launched its new electromagnetic interference (EMI) shielding film that delivers superior EMI noise management for increasingly complex automotive electronics.

- February 2025: Tech Etch unveiled its newest addition to the metal shielding lineup: the 2100 Series EMI Shielding Tape. Designed to tackle contemporary electromagnetic interference issues.

Global Electromagnetic Interference (EMI) Shielding Market Report Scope

Electromagnetic Interference (EMI) shielding reduces or blocks unwanted electromagnetic radiation by creating a barrier with conductive or magnetic materials, protecting sensitive electronics from malfunction or data loss. It works by reflecting or absorbing radio waves/electromagnetic energy, commonly utilizing metals like copper, nickel, and aluminum or advanced composites.

The Electromagnetic Interference (EMI) Shielding market is segmented by material type, shielding method, frequency range, application, form factor, and geography. By material type, the market is segmented into conductive coatings and paints, metal shielding, conductive polymers and composites, EMI/EMC filters, tapes and laminates, and carbon-based foams and nanomaterial films. By the shielding method, the market is segmented into conformal coating, gasket shielding, board-level shielding, cable shielding, and enclosure and vent shielding. By frequency range, the market is segmented into less than 1 GHz, 1-6 GHz, 6-40 GHz (mmWave), and more than 40 GHz (sub-THz). By application, the market is segmented into consumer electronics and wearables, automotive and electric vehicles, telecommunications and 5G/6G infrastructure, aerospace, defense and eVTOL, healthcare and medical devices, industrial equipment and automation, renewable energy and smart grid, and data centers and cloud infrastructure. By form factor, the market is segmented into films and coatings, gaskets and o-rings, sheets and foams, and fabric/flexible textiles. The report also covers the market size and forecasts for electromagnetic interference (EMI) shielding in 19 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Conductive Coatings and Paints |

| Metal Shielding |

| Conductive Polymers and Composites |

| EMI/EMC Filters |

| Tapes and Laminates |

| Carbon-based Foams and Nanomaterial Films |

| Conformal Coating |

| Gasket Shielding |

| Board-Level Shielding |

| Cable Shielding |

| Enclosure and Vent Shielding |

| Consumer Electronics and Wearables |

| Automotive and Electric Vehicles |

| Telecommunications and 5G/6G Infrastructure |

| Aerospace, Defense and eVTOL |

| Healthcare and Medical Devices |

| Industrial Equipment and Automation |

| Renewable Energy and Smart Grid |

| Data Centers and Cloud Infrastructure |

| Films and Coatings |

| Gaskets and O-Rings |

| Sheets and Foams |

| Fabric/Flexible Textiles |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| China | |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | South Africa |

| United Arab Emirates | |

| Rest of Middle-East and Africa |

| By Material Type | Conductive Coatings and Paints | |

| Metal Shielding | ||

| Conductive Polymers and Composites | ||

| EMI/EMC Filters | ||

| Tapes and Laminates | ||

| Carbon-based Foams and Nanomaterial Films | ||

| By Shielding Method | Conformal Coating | |

| Gasket Shielding | ||

| Board-Level Shielding | ||

| Cable Shielding | ||

| Enclosure and Vent Shielding | ||

| By Application | Consumer Electronics and Wearables | |

| Automotive and Electric Vehicles | ||

| Telecommunications and 5G/6G Infrastructure | ||

| Aerospace, Defense and eVTOL | ||

| Healthcare and Medical Devices | ||

| Industrial Equipment and Automation | ||

| Renewable Energy and Smart Grid | ||

| Data Centers and Cloud Infrastructure | ||

| By Form Factor | Films and Coatings | |

| Gaskets and O-Rings | ||

| Sheets and Foams | ||

| Fabric/Flexible Textiles | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| China | ||

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | South Africa | |

| United Arab Emirates | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Electromagnetic Interference (EMI) Shielding market in 2031?

Electromagnetic Interference (EMI) Shielding market is forecast to reach USD 10.49 billion by 2031 at a 5.97% CAGR from 2026.

Which region is expected to grow the fastest?

North America is projected to post the highest growth, expanding at 6.55% CAGR through 2031.

Which segment will record the quickest growth?

Data centers and cloud infrastructure are forecast to advance at 6.32% CAGR during the forecast period (2026-2031) to GPU-dense racks that require high-grade shielding.

Why are conductive polymers gaining popularity?

They cut weight, resist corrosion, and meet new REACH rules while delivering up to 78 dB shielding effectiveness.

Page last updated on: