EMC Filter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.09 Billion |

| Market Size (2031) | USD 1.42 Billion |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

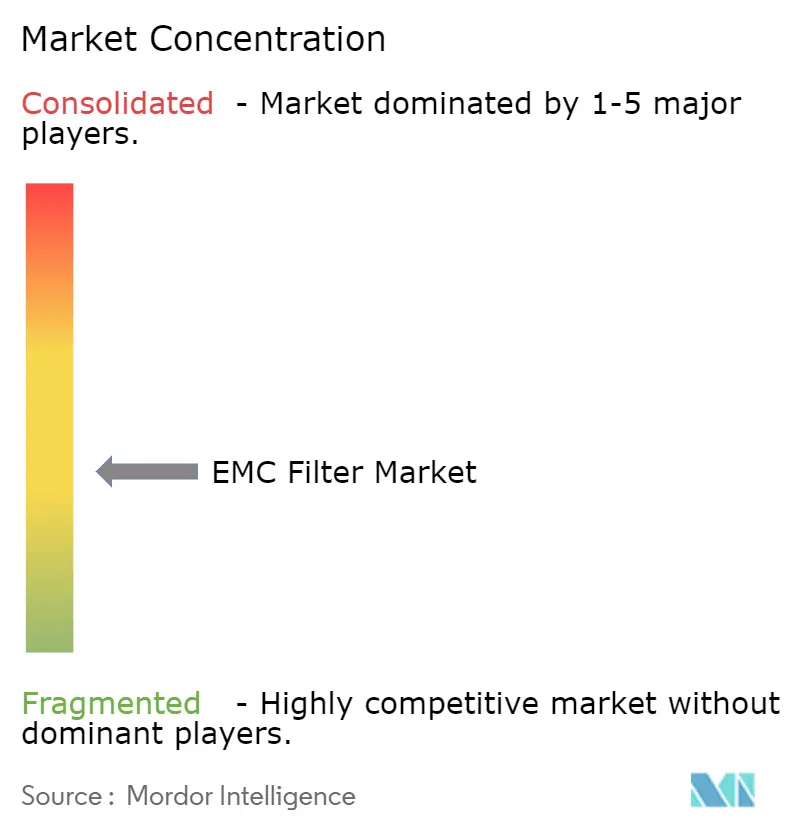

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

EMC Filter Market Analysis by Mordor Intelligence

The EMC filter market size was valued at USD 1.03 billion in 2025 and estimated to grow from USD 1.09 billion in 2026 to reach USD 1.42 billion by 2031, at a CAGR of 5.53% during the forecast period (2026-2031). Sustained demand comes from tougher global electromagnetic-interference regulations, wider use of SiC and GaN power devices in electric-vehicle (EV) chargers, and rapid 5G roll-outs that place board-level noise control at a premium. Asia–Pacific leads current unit shipments thanks to dense electronics production bases, while North American and European spending grows around data-center compliance mandates and grid-modernization programs. The EMC filter market is also buoyed by rising rooftop solar-plus-storage installations in Germany and Japan, by IEC 60601-1-2-driven upgrades in medical imaging, and by heightened three-phase power quality demands in more-electric aircraft.

Key Report Takeaways

- By filter type, single-phase power-line filters held 47.10% of the EMC filter market share in 2025, whereas PCB Filter Arrays are forecast to post a 7.06% CAGR through 2031.

- By phase configuration, single-phase units accounted for 62.70% of revenue in 2025; Three-Phase solutions are set to increase at a 6.55% CAGR to 2031.

- By mounting method, chassis/enclosure products led with a 54.10% revenue share in 2025; however, PCB/Surface-Mount offerings are advancing at an 7.74% CAGR.

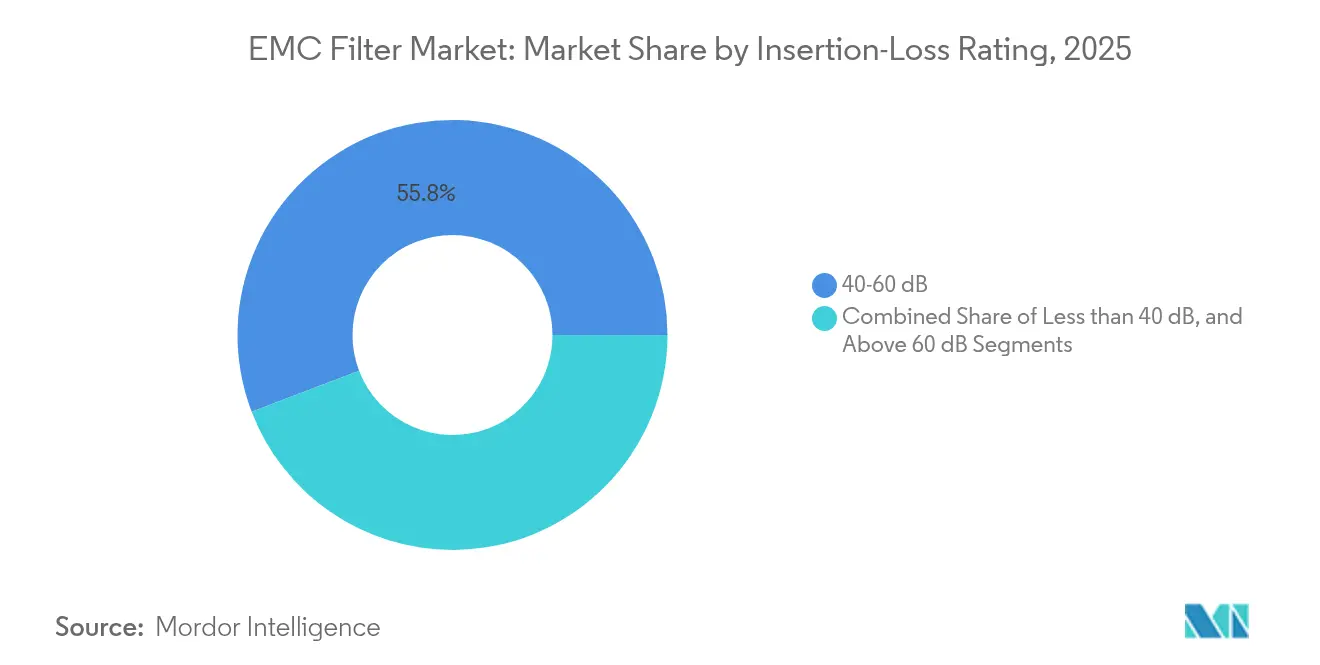

- By insertion-loss class, the 40-60 dB segment held a 55.80% share in 2025, while devices with insertion loss greater than 60 dB are expected to rise at a 5.84% CAGR amid tighter standards.

- By end-user vertical, industrial automation held a 21.60% share in 2025; automotive and EV charging infrastructure are expected to register the fastest 8.75% CAGR from 2025 to 2031.

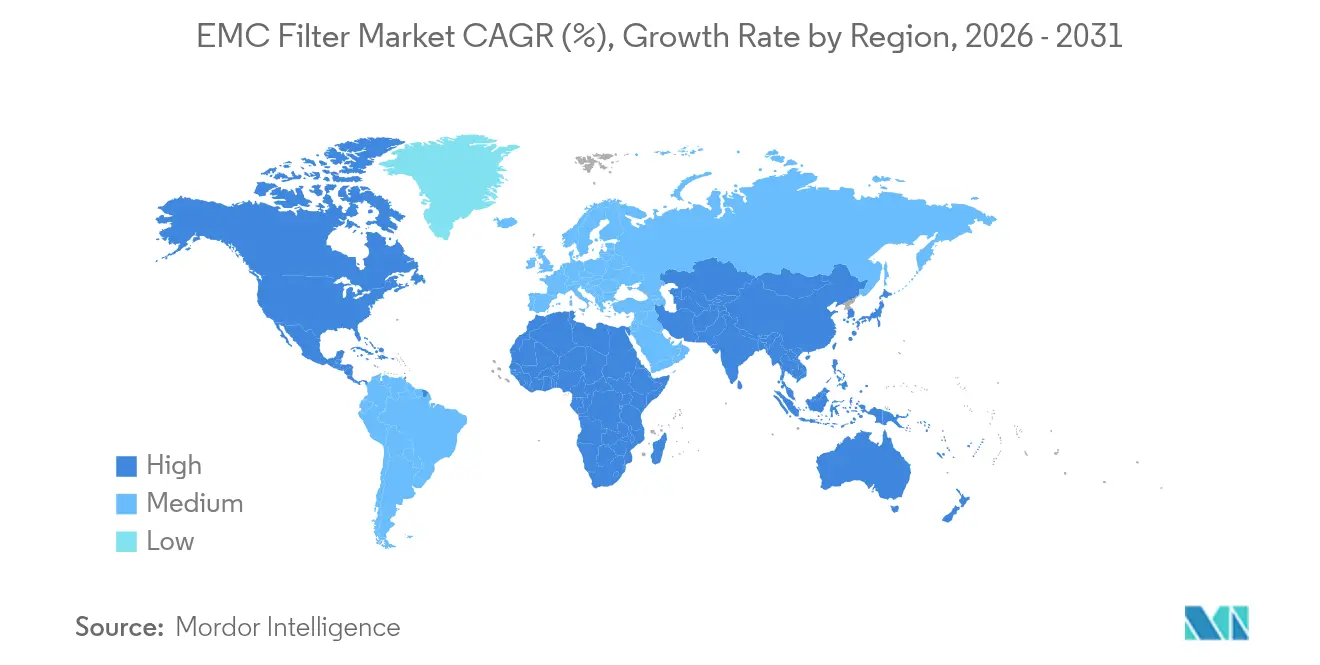

- By geography, the Asia-Pacific region commanded 38.40% of the 2025 revenue, whereas North America is expected to expand the EMC filter market at a 5.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global EMC Filter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of SiC/GaN-based EV Fast-Charger Power Electronics | +1.2% | North America and EU | Medium term (2-4 years) |

| Mandatory CISPR-32/35 Compliance for Hyperscale Data Centres | +0.9% | Global | Short term (≤ 2 years) |

| 5G Macro and Small-Cell Densification in Asia | +0.8% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Rooftop PV + Home Storage Adoption Requiring DC-Side EMI Suppression | +0.6% | Germany, Japan, North America | Long term (≥ 4 years) |

| More-Electric Aircraft 270 VDC Buses Raising Three-Phase Filter Demand | +0.4% | North America and EU | Long term (≥ 4 years) |

| IEC 60601-1-2 4th-Edition Tightening Leakage Specs in Medical Imaging | +0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of SiC/GaN-based EV Fast-Charger Power Electronics

High-power DC chargers now exceed 33 kW while achieving 95% conversion efficiency, yet their MHz-range switching creates complex differential and common-mode noise. Recent IET studies show that optimized LCR branches can cut gate-source oscillation by 41.9 dB, prompting filter makers to pair multi-stage topologies with wide temperature ferrite cores.[1]IET Research Team, “Study on Gate-Source Voltage Oscillation Suppression in SiC MOSFETs Based on LCR Parallel Branch,” IET Research, ietResearch.onlinelibrary.wiley.comCISPR 25 revisions lifting test bands to 400 GHz accelerate specifications across American and European fast-charger programs, ensuring the EMC filter market installs larger capacitance-per-amp packages and semi-custom feed-through designs

Mandatory CISPR-32/35 Compliance for Hyperscale Data Centres

Rack densities topping 100 kW and AI accelerators emitting broadband noise have forced operators to deploy facility-level harmonic filters and board-level common-mode chokes. CISPR 32 Class B demands span 9 kHz-400 GHz, while IEEE 519 still caps voltage distortion at 2.5%. Keysight traces show common-mode-to-differential conversion jeopardizing 100 Gb/s lanes unless insertion loss stays under 1 dB.[2]Keysight Authors, “100 Gb/s System Level Electrical Signaling Impact from EM Modal Artifacts in Hyperscale Networks,” Keysight, keysight.com Consequently, North American data-centre builders award multi-year contracts for 60 dB filters with 2 mΩ max impedance rise, strengthening the EMC filter market outlook.

5G Macro and Small-Cell Densification in Asia

Seventy-five percent of mobile traffic will ride on 5G by 2029, and Asian carriers are deploying dense small-cell grids that pack radios near each other.[3]Ericsson Staff, “Backhaul Capacity Evolution – Ericsson Microwave Outlook,” Ericsson, ericsson.com Boards must integrate common-mode filters able to suppress coupled noise across sub-6 GHz and 26–28 GHz bands while keeping thermal rise below 15 °C. TDK’s latest 10BASE-T1S filter meets Class IV parasitic requirements at one-third prior capacitance, illustrating the shift to ultra-small form factors.[4]TDK Editors, “EMC Components: TDK Offers Common Mode Filter for Automotive Ethernet 10BASE-T1S,” TDK, tdk.com

Rooftop PV + Home Storage Adoption Requiring DC-Side EMI Suppression

Germany and Japan now pair rooftop PV with residential batteries that cycle multiple times per day. Bidirectional converters inject high-frequency noise into DC wiring, which traditional AC filters cannot block. Studies in Electronics journal note up to 20% total harmonic distortion harming nearby communication links. Suppliers therefore design low-leakage DC filters using nanocrystalline toroids to meet utility-grid power-quality codes and support subsidy programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| On-Chip Integration Shrinking TAM for Discrete Filters | -0.7% | Global | Medium term (2-4 years) |

| Miniaturisation-Driven Insertion-Loss Limitations in Wearables | -0.4% | North America and Asia-Pacific | Short term (≤ 2 years) |

| Fragmented Certification (FCC/VCCI/CCC) Slowing Launch Cycles | -0.3% | Global | Short term (≤ 2 years) |

| Ferrite/Nanocrystalline Core Supply Volatility Constraining Output | -0.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

On-Chip Integration Shrinking TAM for Discrete Filters

Semiconductor vendors embed active EMI cancellation that achieves 30 dB attenuation, eliminating bulkier L-C networks. TI’s filter ICs pair DSP algorithms with power stages, reducing parts counts by up to 40% and freeing board space. BAW filters printed at wafer-level now reach −50 dB rejection inside 0.8 mm² footprints. As more designs move to system-in-package, discrete revenue cannibalisation weighs on long-range growth for the EMC filter market.

Miniaturisation-Driven Insertion-Loss Limitations in Wearables

Wearables run low-power radios next to the human body, yet casing size leaves little inductance length. Designers must trade line impedance against attenuation, often capping insertion-loss below 3 dB to preserve battery life. Multi-function stacks-sensors, radios, microfluidics-raise cross-coupled noise, yet SAR limits keep transmit levels low. These constraints restrict high-performance filters, trimming demand for larger discrete parts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Filter Type: Miniaturized Arrays Outpace Legacy Power-Line Designs

Single-Phase Power-Line devices retained a 47.10% EMC filter market share in 2025, equalling USD 0.49 billion of the EMC filter market size. Growth, however, gravitates toward PCB Filter Arrays, whose 7.06% CAGR mirrors OEM moves to consolidate conducted- and radiated-noise mitigation on the board. The segment benefits from low-profile packaging as low as 1 mm height and from pick-and-place compatibility that shortens assembly cycles. Data-Line filters service high-speed ports from 10 Gb/s USB to 100 Gb/s Ethernet, demanding stable impedance up to the fifth harmonic. Feed-Through capacitors hold niches in avionics bulkheads where hermetic sealing offsets higher cost. The EMC filter market remains dynamic as array manufacturers upgrade material systems to handle both ESD pulses and continuous RF energy.

Evolving power topologies push designers to replace chassis-mount L-C bricks with compact multilayer arrays that integrate into the signal path. TDK’s 1.0 × 0.5 × 0.7 mm inductors show that automotive-grade robustness is achievable in sizes once reserved for consumer phones. This shift underpins double-digit unit growth for arrays, whereas classic plug-in filters mature alongside legacy AC drives. Custom LC and Pi networks persist in medical and defense programs that specify unique leakage or environmental limits, so profitability remains healthy even as volumes lag.

By Phase Configuration: Industrial Electrification Fuels Three-Phase Uptake

Single-Phase products produced 62.70% of 2025 revenue but will cede share as factories add variable-frequency drives, pumps, and compressors that require balanced three-phase lines. Three-Phase filters will post a 6.55% CAGR, supported by renewable inverters and 270 VDC aerospace buses. The EMC filter market size for this class is projected to reach USD 0.49 billion by 2031. DC filters remain specialised but meaningful, with EV charging and PV inverters accounting for most demand. Motor-control OEMs specify ≥60 dB common-mode attenuation from 150 kHz-30 MHz to satisfy IEC 61800-3 limits, spurring orders for high-current (≥2500 A) units like Schurter’s FMCC SOL series.

Up-rated switching speeds in SiC drives push resonance issues into the low-MHz range, compelling filter makers to tighten parasitic models and add damping resistors. While Single-Phase lines remain dominant in residential electronics, growth pace slows as saturation sets in. By contrast, energy-transition projects-from offshore wind to electrolyser plants-adopt three-phase layouts that need hybrid common- and differential-mode suppression, thereby driving fresh revenue streams.

By Mounting Method: PCB/SMT Adoption Accelerates

Chassis/Enclosure filters generated 54.10% of 2025 revenue as heavy machinery and UPS cabinets still favor bolt-down modules. Yet PCB/SMT units will expand at an 7.74% CAGR, the highest among mounting classes, as EMS providers automate assembly. DIN-Rail parts serve control panels, especially in EU factories adopting Industry 4.0 retrofits. Feed-Through panel mounts target high-reliability markets that validate hermetic sealing over ten-year service. The EMC filter market sees SMT chokes such as Würth Elektronik’s WE-LF family delivering >40 dB attenuation from 150 kHz-30 MHz while operating from -40 °C to +125 °C .

Component makers now co-design magnetic cores with pick-and-place hardware tolerances, enabling reel-to-reel packaging that aligns with automotive SMT rules. As line widths shrink on six-layer boards, maintaining creepage distances challenges designers; hence low-profile shielded housings grow in use. Chassis filters remain essential where heat and vibration exceed PCB tolerances, yet their share erodes as portable and rack-mount electronics demand compactness.

By Insertion-Loss Rating: Higher Attenuation Gains Traction

Filters rated 40-60 dB at 150 kHz held 55.80% revenue in 2025, but demand is tilting toward >60 dB designs as regulatory bands widen to 400 GHz in some markets. This upper tier will grow 5.84% annually, lifting its slice of the EMC filter market size. Sub-40 dB devices persist in price-sensitive goods like household appliances. Above-60 dB products employ multi-stage topologies with nanocrystalline or amorphous cores to sustain flat impedance. Applied Sciences shows peak-absorption techniques lowering radiated EMI by 41.9 dB on high-speed PWM fans, underscoring how next-generation platforms will need stronger suppression.

Heightened attenuation also surfaces in AI servers where edge inference cards radiate in V-band frequencies. Designers now balance leakage current against noise reduction, driving interest in X-cap combinations and advanced Y capacitors under 100 nF. Growth remains tied to standards bodies that continue to lower emission ceilings

By End-User Vertical: Automotive and Charging Lead Growth

Industrial Automation maintained 21.60% of 2025 revenue; nonetheless, Automotive and EV Charging will outpace all others at a 8.75% CAGR. Power-dense onboard chargers and vehicle Ethernet links need compact common-mode filters meeting AEC-Q200, and TDK’s ACT1210E delivers Class IV parasitic targets to support zonal vehicle architectures. Consumer Electronics stays steady as appliance makers refresh lines under evolving CISPR 14-1-based national rules like China’s GB 4343.1-2024. Telecom and 5G Infrastructure accelerate in tandem with Asian densification. Medical Equipment invests in leakage-controlled filters to pass IEC 60601-1-2 4th-Edition limits, prompting demand for low-displacement current parts in imaging suites.

Renewable Energy installations need bidirectional DC filters that survive ±600 V swings and wide climatic variation. Aerospace and Defense remains premium, valuing hermetic feed-throughs that sustain -55 °C to +125 °C with altitude derating.

Geography Analysis

Asia Pacific captured 38.40% of global revenue in 2025 on the back of China’s electronics export engine, Japan’s robotics leadership, and South Korea’s advanced packaging lines. New Chinese EMC mandates, modeled on CISPR 14-1:2020, turn mandatory after mid-2026 and will reinforce compliance spending. Japan’s PV-plus-storage wave spurs low-leakage DC filters, while South Korean fabs order high-frequency chokes for 2.5D and 3D IC packaging. India’s rare-earth shortfall has already extended EV magnet deliveries by up to six months and raised local filter core costs 5-8%, exposing supply-chain fragility. ASEAN nations attract PCB investments that diversify production away from single-country risk, presenting local assembly openings for the EMC filter market.

North America is the fastest growing geography at 5.92% CAGR. Federal EV-charger incentives and data-center expansions push utilities to demand filters that cut harmonic content to IEEE-519 thresholds. NERC’s 2025 policy review highlights grid-instability risks from clustered hyperscale loads, nudging site developers toward facility-wide 60 dB attenuation plans. Mexico’s maquiladora corridor gains traction for medium-volume filter assembly, benefitting from USMCA rules and proximity to Texan charger OEMs.

Europe retains a balanced outlook. Germany leads rooftop PV adoption, and its HVDC interconnects require three-phase filters with low partial-discharge rates. Nordic wind projects specify corrosion-resistant coatings to handle saline environments. The United Kingdom harmonizes post-Brexit EMC laws with EU rules, preserving market access. France upgrades nuclear control electronics, demanding long-life filters certified to IEC 60721-3-3 class 3C2 humidity. Eastern Europe becomes an alternate ferrite-core milling site, reducing shipping distance to EU plants.

Competitive Landscape

The EMC filter market exhibits moderate concentration. TE Connectivity finalized its Schaffner acquisition in May 2025, forming the broadest portfolio that spans 250 mA PCB beads to 2,500 A three-phase cabinets. TDK and Murata out-innovate rivals through material science; TDK’s glass-tape winding cuts DC resistance by 20%, while Murata scales ceramic multilayer arrays for smart-meter roll-outs. Delta Electronics’ USD 71 million purchase of Alps Alpine’s inductor assets deepens vertical control over metallic powders that underpin high-frequency chokes.

Strategic moves center on application-specific platforms. In automotive, suppliers co-develop Ethernet filters with Tier 1 harness makers to secure design-ins through 2030. Data-center accounts favour suppliers with quick-turn custom brackets that mate with 3-U power shelves. Aerospace bids require DO-160G qualification, where only a few firms possess in-house vibration rigs. Supply-chain volatility in nanocrystalline ribbon prompts dual-sourcing; players with European and Asian slit-core lines win preference. Meanwhile, chip-level integration threatens discrete volumes, prompting incumbents to offer reference-design services ensuring compliance even when passive counts fall.

Emerging disruptors include startups printing polymer inductor coils directly on PCBs, slashing z-height for wearables. Another niche is cryogenic filters for quantum-computing racks, where μΩ impedance and sub-Kelvin thermal conduction demand exotic alloys.

EMC Filter Industry Leaders

TE Connectivity

Schurter Holding AG

Würth Elektronik Group

TDK Corporation

Schaffner Holding AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: TE Connectivity completed the integration of Schaffner Holding AG, expanding its multi-vertical EMC filter catalogue.

- January 2025: China Quality Certification Centre released GB 4343.1-2024 EMC rules for household appliances, aligning with CISPR 14-1:2020 and becoming compulsory after mid-2026.

- October 2024: TDK partnered with NEOM McLaren Formula E to co-engineer high-temperature capacitors for race EV drivetrains

Global EMC Filter Market Report Scope

EMC filters are indispensable components in modern electronic systems, mitigating electromagnetic interference between devices and their power sources. With the constant miniaturization of electronic components and escalating clock frequencies, the demand for effective EMC filtering solutions is increasing across industries. The EMC filter market study comprehensively analyzes trends and demand for these products across various end-user verticals and geographies. Market numbers are derived by accruing EMC filter sales by major market vendors globally.

The EMC filter market is segmented by type (common mode filters, feedthrough filters, filter circuits, other types), by end user (consumer electronics, aerospace and defense, medical, telecom, other end users), and by geography (Americas, Europe and Middle East and Africa, Asia-Pacific). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Power-Line EMI/EMC Filters |

| Data-Line/Signal Filters |

| Feed-Through capacitive Filters |

| PCB Filter Arrays/Circuits |

| Other Filter Type |

| Single-Phase |

| Three-Phase |

| DC |

| Chassis/Enclosure Mount |

| DIN-Rail Mount |

| PCB/Surface-Mount |

| Feed-Through Panel Mount |

| Less than 40 dB |

| 40-60 dB |

| Above 60 dB |

| Consumer Electronics and Appliances |

| Automotive and EV Charging Infrastructure |

| Aerospace and Defence (Avionics, Satellites) |

| Industrial Automation and Drives |

| Telecom and 5G Infrastructure |

| Medical Equipment |

| Renewable Energy (PV, Wind, ESS) |

| Rail and Transportation |

| Other End-User Vertical |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Filter Type | Power-Line EMI/EMC Filters | ||

| Data-Line/Signal Filters | |||

| Feed-Through capacitive Filters | |||

| PCB Filter Arrays/Circuits | |||

| Other Filter Type | |||

| By Phase Configuration | Single-Phase | ||

| Three-Phase | |||

| DC | |||

| By Mounting Method | Chassis/Enclosure Mount | ||

| DIN-Rail Mount | |||

| PCB/Surface-Mount | |||

| Feed-Through Panel Mount | |||

| By Insertion-Loss Rating (at 150 kHz) | Less than 40 dB | ||

| 40-60 dB | |||

| Above 60 dB | |||

| By End-User Vertical | Consumer Electronics and Appliances | ||

| Automotive and EV Charging Infrastructure | |||

| Aerospace and Defence (Avionics, Satellites) | |||

| Industrial Automation and Drives | |||

| Telecom and 5G Infrastructure | |||

| Medical Equipment | |||

| Renewable Energy (PV, Wind, ESS) | |||

| Rail and Transportation | |||

| Other End-User Vertical | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the EMC filter market?

The EMC filter market size stands at USD 1.09 billion in 2026 and is projected to reach USD 1.42 billion by 2031.

Which region grows the fastest through 2031?

North America leads growth with a forecast 5.92% CAGR, propelled by data-center compliance and EV-charging roll-outs.

Why are SiC and GaN devices critical for EMC filter demand?

These wide-bandgap semiconductors switch at high frequencies, generating complex EMI that requires advanced multi-stage filters.

Which end-user segment expands quickest?

Automotive and EV charging infrastructure will advance at a 8.75% CAGR as vehicle electrification accelerates.

How does on-chip EMI filtering affect discrete filter suppliers?

Active EMI suppression embedded in ICs trims discrete component volumes, shaving an estimated 0.7% off the market’s long-term CAGR.

What insertion-loss levels dominate current designs?

Filters providing 40-60 dB attenuation at 150 kHz held 55.80% of 2025 revenue, though demand for >60 dB devices is rising with tougher standards.

Page last updated on: