EMI Shielding Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

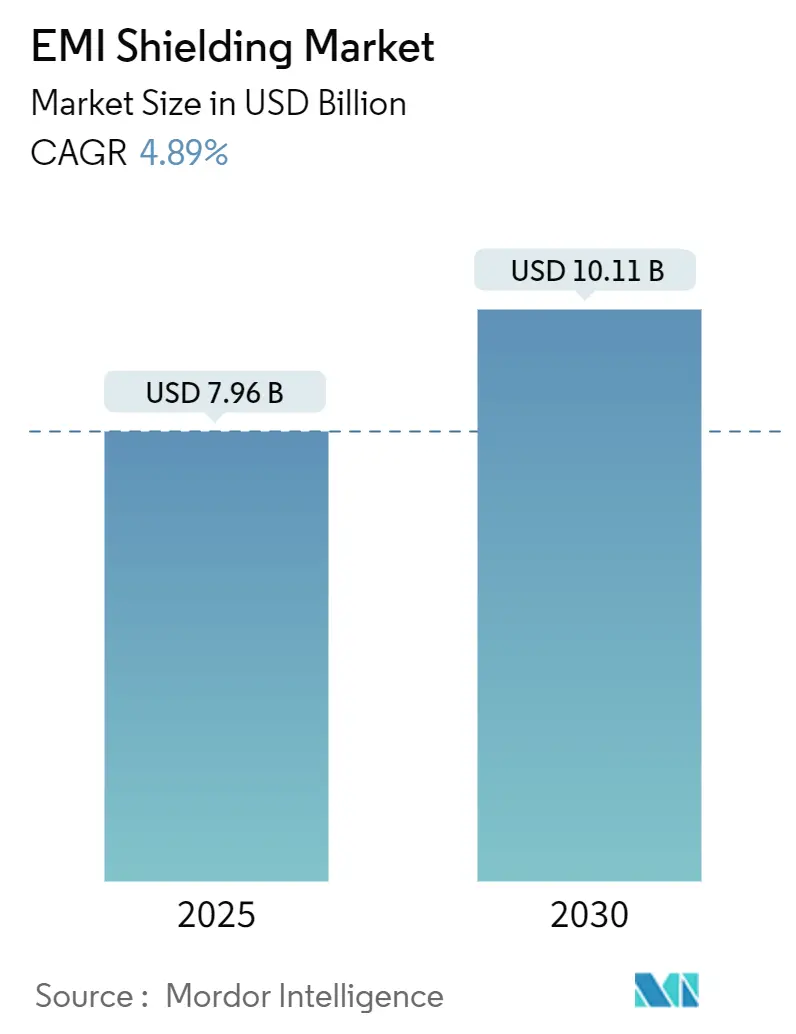

| Market Size (2025) | USD 7.96 Billion |

| Market Size (2030) | USD 10.11 Billion |

| Growth Rate (2025 - 2030) | 4.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

EMI Shielding Market Analysis by Mordor Intelligence

The EMI shielding market size stood at USD 7.96 billion in 2025 and is forecast to reach USD 10.11 billion by 2030, reflecting a 4.89% CAGR over the period. Rising 5G base-station density, rapid electric-vehicle (EV) adoption, and tighter electromagnetic-compatibility (EMC) regulations are expanding design-in opportunities for conductive coatings, polymers, and board-level cans. Regulatory benchmarks such as IEC 60601-1-2 for medical devices and CISPR-25 for automotive electronics continue to elevate performance specifications.[1]International Electrotechnical Commission, “IEC 60601-1-2,” The shift from reflection-dominant to absorption-dominant materials, exemplified by MXene films with 35,000 S/cm conductivity, positions conductive polymers for outsize growth. Asia-Pacific commands nearly half of global revenues on the back of China, Japan, and South Korea’s manufacturing depth, while North America and Europe prioritize high-value aerospace, medical, and EV platforms that demand premium solutions. At the product level, board-level cans align with miniaturization and system-in-package trends, reinforcing their twin roles as today’s volume leader and tomorrow’s growth engine.

Key Report Takeaways

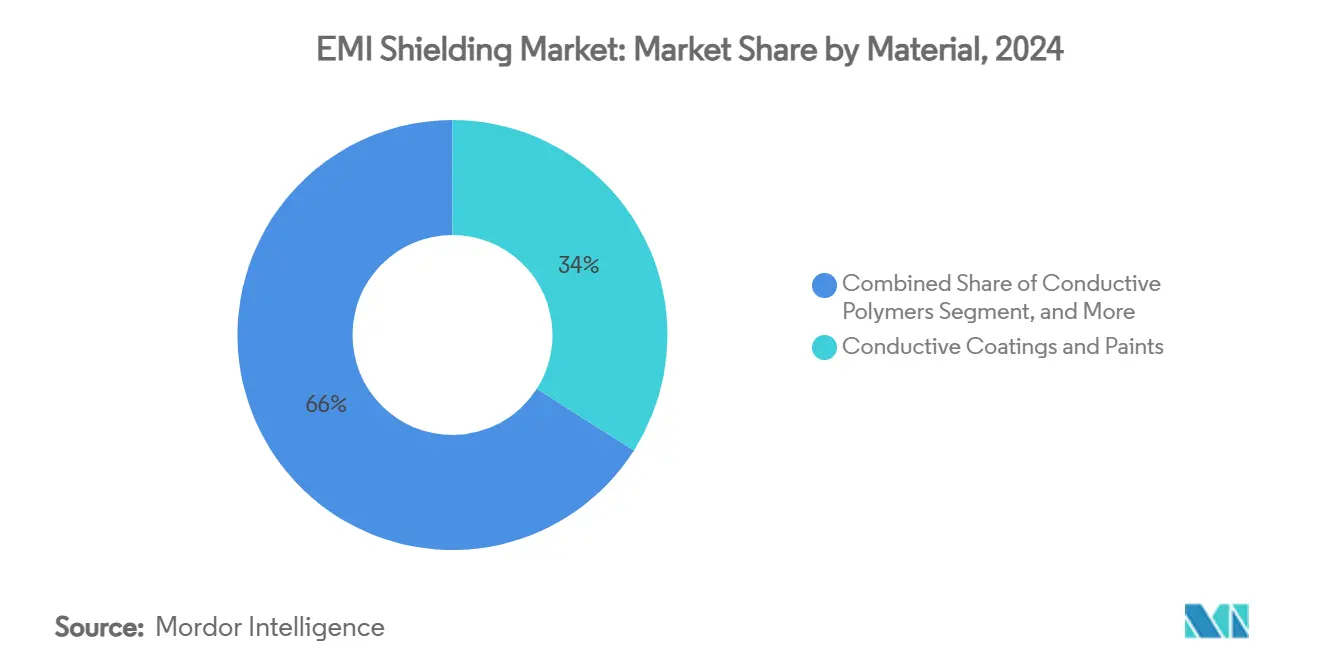

- By material, conductive coatings and paints captured 34.02% revenue share in 2024, while conductive polymers are projected to advance at 7.23% CAGR through 2030.

- By shielding product type, board-level cans accounted for 32.78% share in 2024, and the same category is poised to expand at 6.76% CAGR to 2030.

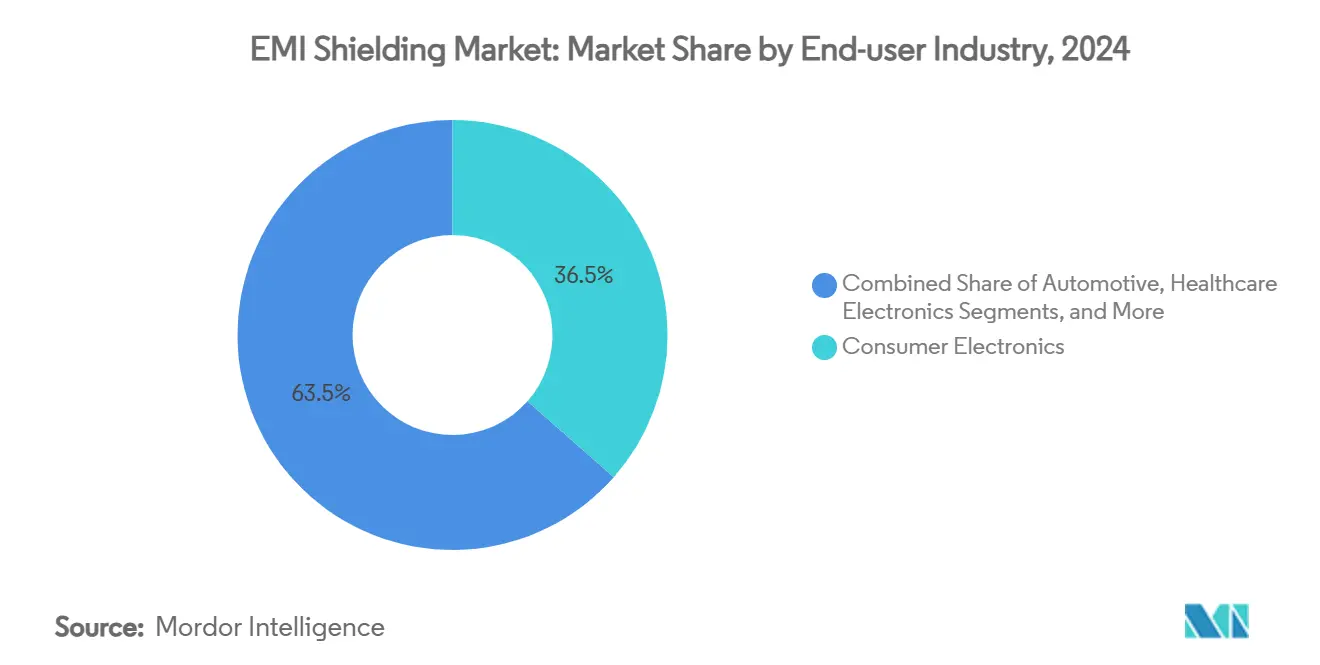

- By end-use industry, consumer electronics held a 36.50% share in 2024, whereas electric vehicles are set to grow at a 5.89% CAGR through 2030.

- By application, PCB-level shielding commanded 41.10% of the EMI shielding market share in 2024 and is progressing at 6.02% CAGR through 2030.

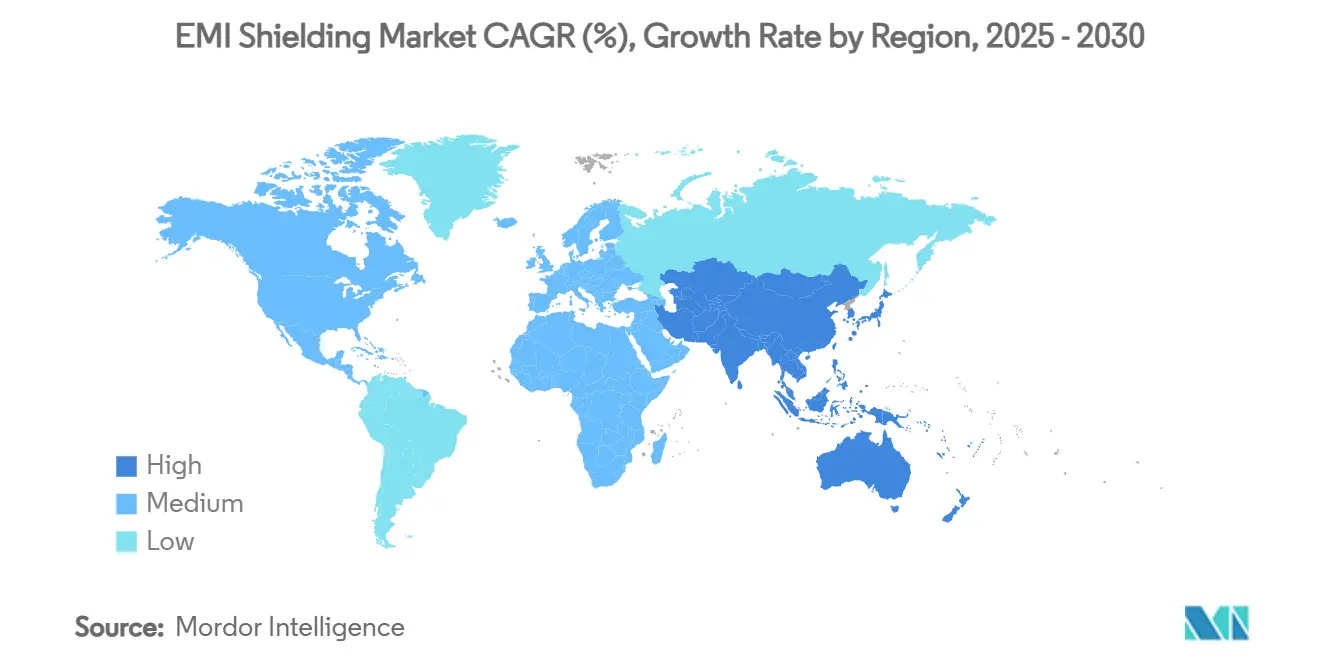

- By geography, Asia-Pacific led with 45.90% contribution in 2024 and is forecast to register a 5.43% CAGR to 2030.

Global EMI Shielding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Miniaturization of consumer electronics and 5G densification | +1.2% | Global with APAC core | Medium term (2–4 years) |

| Rapid EV platform launches requiring lightweight shielding | +0.8% | North America and EU expanding to APAC | Long term (≥ 4 years) |

| Regulatory tightening on EMC compliance | +0.6% | Global; stricter in developed markets | Short term (≤ 2 years) |

| Adoption of ultra-high-frequency radar in ADAS | +0.4% | North America and EU automotive corridors | Medium term (2–4 years) |

| Shift to system-in-package and board-level shielding in IoT | +0.3% | APAC manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Miniaturization of Consumer Electronics and 5G Densification

Compact smartphones, wearables and IoT nodes release electromagnetic energy across multiple bands, intensifying mutual coupling that degrades signal integrity. Millimeter-wave 5G radios above 24 GHz impose shorter wavelengths that penetrate conventional metal cages, prompting designers to migrate toward sub-10 µm polymer films imbued with carbon nanotubes. High-volume handset production magnifies cost sensitivity, so suppliers refine roll-to-roll coating lines to deliver stable 60 dB attenuation at material thicknesses under 25 µm. As every device becomes both emitter and victim, OEMs specify multilayer absorption stacks that damp near-field coupling without compromising antenna tuning. The EMI shielding market therefore benefits from recurring refresh cycles as each smartphone generation raises clock speeds and adds radios.

Rapid EV Platform Launches Requiring Lightweight Shielding

Next-generation 800 V drivetrains generate steep transient edges that radiate over wide spectra, compelling automakers to integrate shielding around inverters, DC-DC converters and battery packs. Lightweight carbon-fiber composites infused with stainless-steel fibers deliver 70 dB effectiveness yet weigh 60% less than aluminum panels. Radar-equipped ADAS modules further elevate requirements because 77–81 GHz sensors must coexist with high-voltage circuits. Frequency-selective enclosures that block broadband noise while passing 5.9 GHz V2X signals are gaining favor, and this technical pivot accelerates material substitution away from traditional brass or copper meshes. As global EV output climbs, the EMI shielding market records incremental unit growth beyond the general automotive uptrend.

Regulatory Tightening on EMC Compliance

Fourth-edition IEC 60601-1-2 embeds risk-management language stipulating that medical equipment must preserve essential performance under defined electromagnetic stress levels. CISPR-25 now includes emissions limits for high-voltage harnesses, forcing automotive Tier-1s to shield HV cables and charger housings. Regulatory harmonization across China, the EU, and the United States permits component vendors to amortize compliance costs over larger volumes, yet simultaneously raises baseline shielding effectiveness to 50–60 dB on many platforms. Certification delays threaten product launches, so OEMs increasingly source pre-qualified materials libraries from their suppliers, solidifying multi-year supply contracts. These dynamics enlarge the addressable EMI shielding market because compliance is now integral to product-reliability narratives.

Adoption of Ultra-High-Frequency Radar in ADAS

Transitioning from 24 GHz to 77 GHz radar improves resolution but shortens wavelength, meaning minor package discontinuities amplify scattering and degrade sensing accuracy. Polymer radomes with ±0.05 mm thickness tolerance ensure phase stability while integrated conductive meshes attenuate out-of-band emissions. Multisensor arrays place 6–12 radar modules per vehicle, multiplying potential interference paths and elevating cumulative shielding demand. Millimeter-scale cavity resonances are mitigated by applying thin ferrite absorbers inside modules, a practice that expands average shielding cost per vehicle. As Level 3 autonomous functions proliferate, the EMI shielding market sees rising content value even if unit demand plateaus.

Restraints Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating raw-material prices of silver, copper, and nickel | –0.7% | Global; higher in cost-sensitive regions | Short term (≤ 2 years) |

| Weight-addition trade-offs in aerospace and space electronics | –0.3% | North America and EU aerospace corridors | Medium term (2–4 years) |

| Limited recycling routes for polymer-based laminates | –0.2% | EU regulatory pressure; global uptake | Long term (≥ 4 years) |

| Emerging chip-level shielding reducing enclosure demand | –0.4% | APAC semiconductor hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuating Raw-Material Prices of Silver, Copper and Nickel

Spot prices for silver and copper rose more than 15% between 2024 and 2025, straining coating formulators that rely on metal flakes for conductivity. Index-linked contracts pass costs downstream, but consumer electronics OEMs resist price escalation, compressing supplier margins. Long lead-times for nickel sulfide concentrate complicate hedging, exposing ferrite producers to valuation swings that disrupt production planning. Developers accelerate polymer-nanotube research to hedge against metal volatility, yet qualification for life-critical medical devices lags price shocks by several quarters. These dislocations temporarily pinch the EMI shielding market growth rate until material substitution matures.

Weight-Addition Trade-offs in Aerospace and Space Electronics

Every additional kilogram on a geostationary satellite can add USD 20,000 to launch expense, prompting avionics designers to weigh shielding benefits against payload penalties. Metallic gaskets deliver excellent low-frequency attenuation but create galvanic corrosion risks under thermal cycling from -55 °C to +125 °C. Composite alternatives reduce mass by 40% yet introduce anisotropy that complicates multi-axis protection, often requiring hybrid lay-ups that offset weight gains. Extensive vibration and outgassing tests prolong development schedules, imposing opportunity costs that discourage new entrants. Consequently, the EMI shielding market faces slower adoption in aerospace despite high per-unit value.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Conductive Polymers Lead Performance Shift

The materials segment reached USD 2.71 billion in 2025, with conductive coatings and paints maintaining a 34.02% slice of the EMI shielding market share, while conductive polymers—though smaller, registered the segment’s fastest 7.23%. Their intrinsic absorption mechanism turns incident energy into trace heat, minimizing secondary EMI reflections inside crowded PCB cavities. Recent graphene-reinforced polyaniline films achieved 90 dB attenuation across 18–40 GHz yet remain pliable at 0.02 mm thickness, expanding deployment in foldable phones and smartwatches. Nanotube loading levels under 5 wt% deliver percolation without embrittling the matrix, addressing wearability concerns in e-textiles. Conversely, metal-filled paints still dominate infrastructure where spray application and cost scaling outweigh weight penalties. Suppliers integrate intumescent additives, enabling single-coat fire and EMI protection for telecom cabinets, thereby broadening tender eligibility under stringent building codes. As eco-labels gain traction, recycled polyethylene blends incorporating stainless-steel fibers achieve credible 50 dB shielding, moving the EMI shielding industry toward circularity.

By Shielding Product Type: Board-Level Cans Retain Dual Leadership

Board-level cans generated USD 2.61 billion in 2025 and supplied 32.78% of overall revenue, while also charting a 6.76% CAGR to 2030, underscoring their resilience in the face of package-integrated alternatives. Smartphones, wearables, and IoT modules adopt multi-compartment lids allowing concurrent LTE, Wi-Fi, GPS, and Bluetooth radios inside a single RF shield without cross-talk, preserving layout density. Automotive customers specify deep-drawn stainless-steel cans for zone controllers that operate from -40 °C to +150 °C, validating durability through 1,000-hour salt-spray tests. Cable and connector shields follow as the next sizeable segment, driven by Category 7 data-center interconnects that require 50 µΩ contact resistance. Vent and window meshes employ 90% open-area aluminum honeycomb, balancing airflow with 85 dB suppression above 1 GHz in 5G base stations. Conformal sputtering, while still emerging, deposits nickel–chromium layers directly on components, reaching 15 dB at 6 GHz and meeting wearables’ thickness budgets. Collectively, these product innovations reinforce the EMI shielding market trajectory.

By End-Use Industry: EVs Propel New Revenue Streams

Consumer electronics contributed USD 2.90 billion in 2025, equal to 36.50% of total spend in the EMI shielding market, but their mid-single-digit growth has ceded headline momentum to electric vehicles growing at a 5.89% CAGR. Each battery electric vehicle integrates upward of 70 electronic control units, quadruple the count of legacy platforms, elevating shielding content per vehicle to USD 60 on average. High-frequency inverter whine necessitates laminated busbars with integrated EMI gaskets to meet CISPR 25 Class 5 thresholds. Telecommunications infrastructure contributes stable double-digit demand as operators densify small cells, with a typical 5G remote radio head requiring 500 g of conductive paint. Medical device makers pursue polymeric shields that withstand ethylene-oxide sterilization, maintaining 40 dB suppression after five cycles. Industrial-automation customers focus on durability against hydraulic-fluid exposure, favoring nickel-plated brass glands that pass IP68 immersion tests. These diversified pulls anchor the EMI shielding market against cyclical swings in any single sector.

By Application: PCB-Level Protection Intensifies

PCB-level shielding absorbed USD 3.27 billion in 2025 and represented 41.10% of the EMI shielding market, advancing at a 6.02% CAGR toward 2030. Higher clock domains and tighter trace spacing accentuate radiation from microstrip edges; hence, designers route sensitive antennas within 3-sided Faraday frames lined by form-in-place gaskets. System-in-package integration embeds copper walls inside the substrate, delivering 20 dB isolation while saving 15% board area compared with discrete lids. Cable assemblies trail with rising adoption of single-pair Ethernet for zonal automotive architectures; foil-plus-braid constructions meet 40 dB at 1 GHz yet remain bendable to 20 mm radius. Device enclosures now combine magnesium frames and conductive spray coats, squeezing 5 g from a typical smartphone mid-plate. Facility-level “quiet rooms” rely on galvanized-steel panels sealed with conductive silicone, blocking 100 dB across 0.1–10 GHz for military installations. The escalating need for multilayer, multi-scale mitigation sustains application diversity inside the EMI shielding market.

Geography Analysis

Asia-Pacific delivered USD 3.65 billion in 2025, representing 45.90% of global revenue, and is tracking a 5.43% CAGR supported by regional electronics exports. China's 5G macro-site roll-outs surpass 3 million units, each requiring up to 1 kg of conductive paint across radome frames and filter housings. Japan funds advanced radar‐on-chip programs that elevate board-level can demand, while South Korea's memory fabs specify low-outgassing gaskets to protect extreme-ultraviolet scanners.

North America follows with USD 1.58 billion, propelled by defense and medical OEMs that impose 70–90 dB targets across 2–18 GHz. The United States' CHIPS Act incentives catalyze domestic package-level shielding R&D, spurring collaboration between semiconductor fabs and materials suppliers. Canada's aerospace cluster in Quebec adopts carbon-fiber composite enclosures that shed 200 g per avionics bay, offering a precedent for European air-framers.

Europe generated USD 1.21 billion, centered on Germany's EV powertrain hubs and France's satellite programs. EU guidelines on recyclability favor thermoplastic-based shields, stimulating German polymer suppliers to pilot closed-loop recovery schemes. With 24 national regulators aligning under RED 2024, a harmonized test regime simplifies cross-border exports, indirectly enlarging addressable revenue for EMI shielding market participants.

Competitive Landscape

The market hosts a cluster of diversified material science leaders complemented by agile specialists targeting high-growth niches. 3M leverages its 25-year semiconductor portfolio to supply ultra-thin copper-nickel films for fan-out wafer-level packages, reinforcing its value in emerging chip-level shielding. Parker-Hannifin's Chomerics unit capitalizes on vertically integrated metallurgy to offer silver-plated aluminum fillers that secure stable conductivity yet cut dielectric weight 30%. DuPont's 2024 acquisition of Laird Performance Materials broadened its suite to include thermally conductive, electrically shielding pads that streamline thermal and EMC co-design.[2]3M News, "3M Joins Consortium to Accelerate Semiconductor Technology," 3m.com

TDK exploits magnetic-material heritage to introduce common-mode filters and chip beads that complement mechanical shields, pursuing a platform approach where passive components and enclosures co-optimize EMC budgets.[3]TDK Corporation, "AI at Electronica 2024," tdk.com SABIC enters through specialty polymers embedding stainless-steel fibers, addressing OEM requests for non-halogenated formulations that pass V-0 flammability ratings while delivering 55 dB attenuation. Additive-manufacturing start-ups print lattice shields customized to board topography, reducing part count for low-volume aerospace runs.

Competitive intensity rises in Asia, where Taiwanese and Chinese vendors scale sputtered-metal lids integrated into substrate manufacturing lines, potentially eroding price premiums enjoyed by Western incumbents. Nevertheless, intellectual-property portfolios around polymer chemistry and absorber formulations provide defensible moats, ensuring differentiated profit pools persist across the EMI shielding market.

EMI Shielding Industry Leaders

-

3M Company

-

Parker-Hannifin Corporation (Chomerics)

-

DuPont de Nemours, Inc.

-

Henkel AG & Co. KGaA

-

PPG Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: 3M joined the US-JOINT Consortium to accelerate semiconductor packaging materials for EMI-sensitive applications.

- November 2024: DuPont showcased Laird Performance Materials solutions at Electronica 2024, emphasizing integrated thermal-EMI management.

- October 2024: TDK unveiled AI-driven EMI mitigation software through start-up Denpaflux at Electronica 2024.

- October 2024: DuPont and Zhen Ding Technology signed a cooperation pact on high-end PCB materials targeting EMI control.

Global EMI Shielding Market Report Scope

| Conductive Coatings and Paints |

| Conductive Polymers |

| EMI Shielding Tapes and Laminates |

| Metal Shielding Sheets and Foams |

| EMI Filters and Ferrites |

| EMI Gaskets and O-Rings |

| Other Materials |

| Board-Level Shielding Cans |

| Cable and Connector Shielding |

| Enclosure and Cabinet Shielding |

| Vent and Window Shielding |

| Other Shielding Product Types |

| Consumer Electronics |

| Automotive (ICE and EV) |

| Telecommunications and IT Infrastructure |

| Aerospace and Defense |

| Healthcare Electronics |

| Industrial Automation and Energy |

| Other End-Use Industries |

| PCB / Board-Level |

| Device Enclosure / Housing |

| Cable Assemblies |

| Architectural and Room Shielding |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Material | Conductive Coatings and Paints | ||

| Conductive Polymers | |||

| EMI Shielding Tapes and Laminates | |||

| Metal Shielding Sheets and Foams | |||

| EMI Filters and Ferrites | |||

| EMI Gaskets and O-Rings | |||

| Other Materials | |||

| By Shielding Product Type | Board-Level Shielding Cans | ||

| Cable and Connector Shielding | |||

| Enclosure and Cabinet Shielding | |||

| Vent and Window Shielding | |||

| Other Shielding Product Types | |||

| By End-Use Industry | Consumer Electronics | ||

| Automotive (ICE and EV) | |||

| Telecommunications and IT Infrastructure | |||

| Aerospace and Defense | |||

| Healthcare Electronics | |||

| Industrial Automation and Energy | |||

| Other End-Use Industries | |||

| By Application | PCB / Board-Level | ||

| Device Enclosure / Housing | |||

| Cable Assemblies | |||

| Architectural and Room Shielding | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the EMI shielding market?

The EMI shielding market size is USD 7.96 billion in 2025 and is projected to reach USD 10.11 billion by 2030.

Which material segment is expanding fastest?

Conductive polymers lead growth at a 7.23% CAGR owing to their absorption-dominant mechanism and lightweight profile.

Why are electric vehicles important for EMI shielding demand?

High-voltage battery packs and multiple radar sensors in EVs elevate electromagnetic emissions, lifting shielding content per vehicle and driving a 5.89% CAGR in the segment.

Which region dominates the EMI shielding market?

Asia-Pacific holds 45.90% revenue share thanks to dense electronics manufacturing bases in China, Japan and South Korea.

How are regulations influencing product design?

Tighter standards like IEC 60601-1-2 and CISPR-25 require higher shielding effectiveness across broader frequency ranges, pushing adoption of advanced materials and board-level solutions.

Page last updated on: