Size and Share of Passive Electronic Components Market in Aerospace And Defense Industry

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

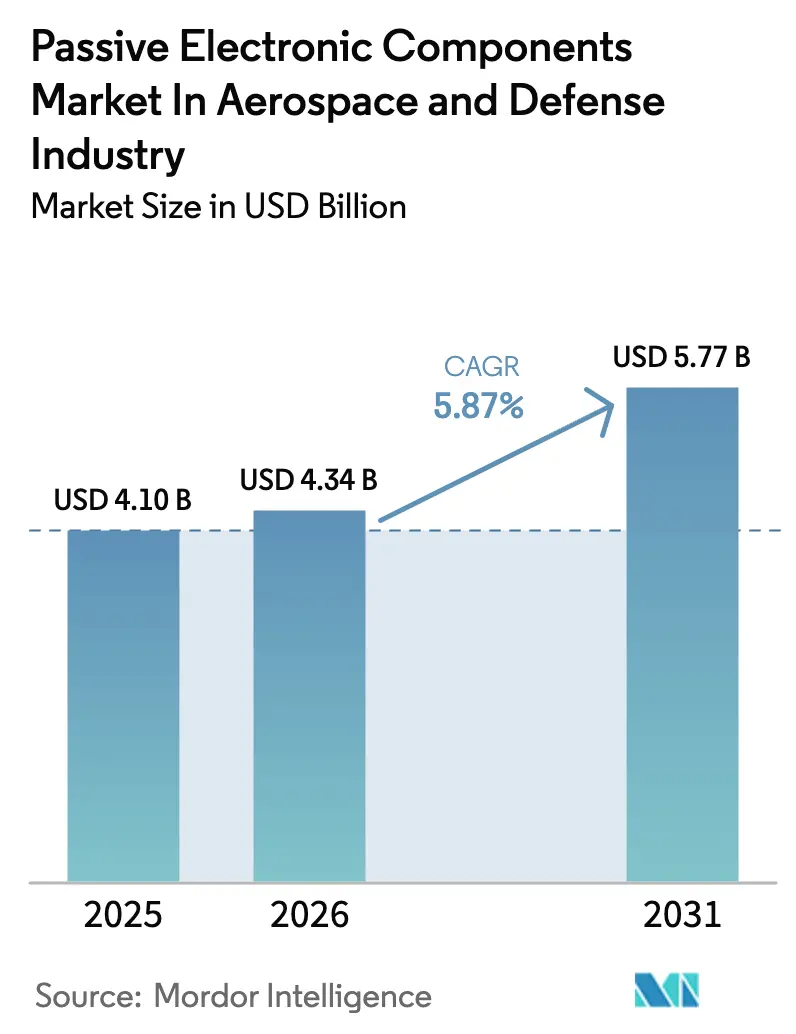

| Market Size (2026) | USD 4.34 Billion |

| Market Size (2031) | USD 5.77 Billion |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

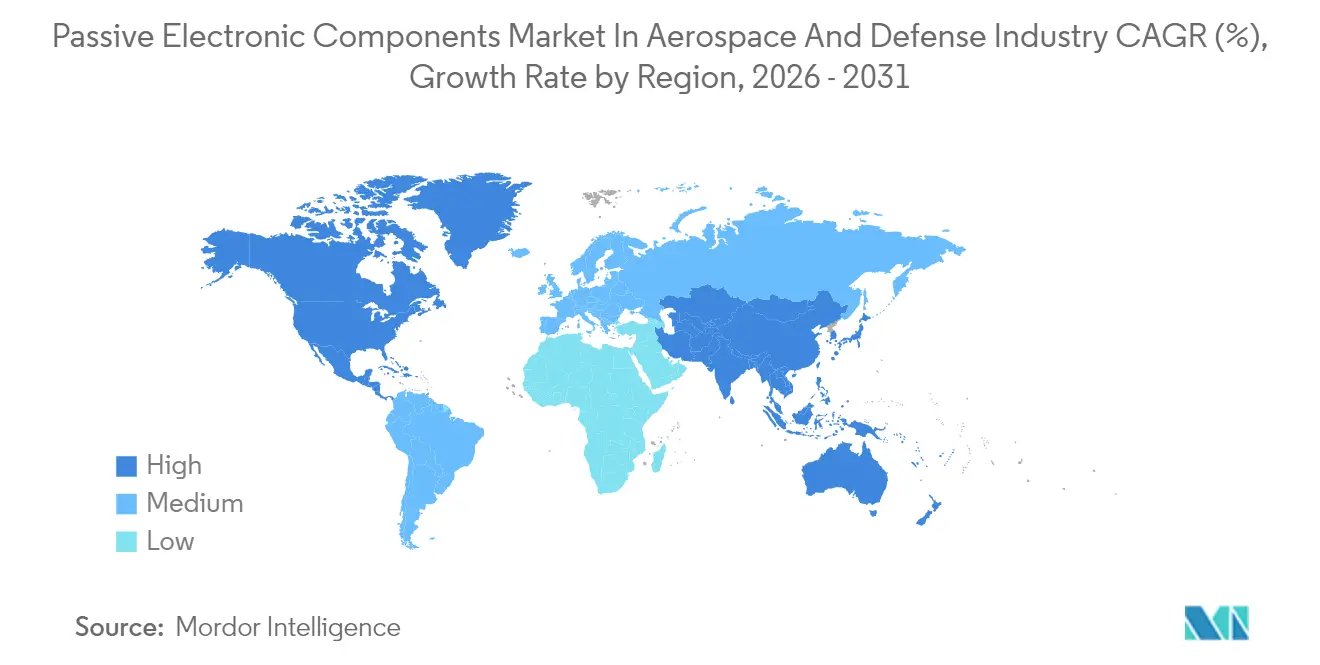

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Passive Electronic Components Market in Aerospace And Defense Industry by Mordor Intelligence

The passive electronic components market size in the aerospace and defense industry was valued at USD 4.1 billion in 2025 and estimated to grow from USD 4.34 billion in 2026 to reach USD 5.77 billion by 2031, at a CAGR of 5.87% during the forecast period (2026-2031). Continued electrification of aircraft, modernization of military electronics, and resilient demand for space-borne platforms anchor this growth trajectory. Commercial aviation’s recovery has revived fixed-wing production lines, while next-generation unmanned systems and Low Earth Orbit (LEO) satellites add fresh demand signals. Component suppliers that hold recognized aerospace certifications and vertically integrated supply chains have exercised pricing power in tight markets. Regional expansion of manufacturing footprints and strategic inventory buffers has emerged as a key hedging tactic against critical material shortages and geopolitical friction. The passive electronic components market continues to benefit from design transitions toward higher voltage, lighter weight, and thermally robust architectures that traditional mechanical subsystems cannot match.

Key Report Takeaways

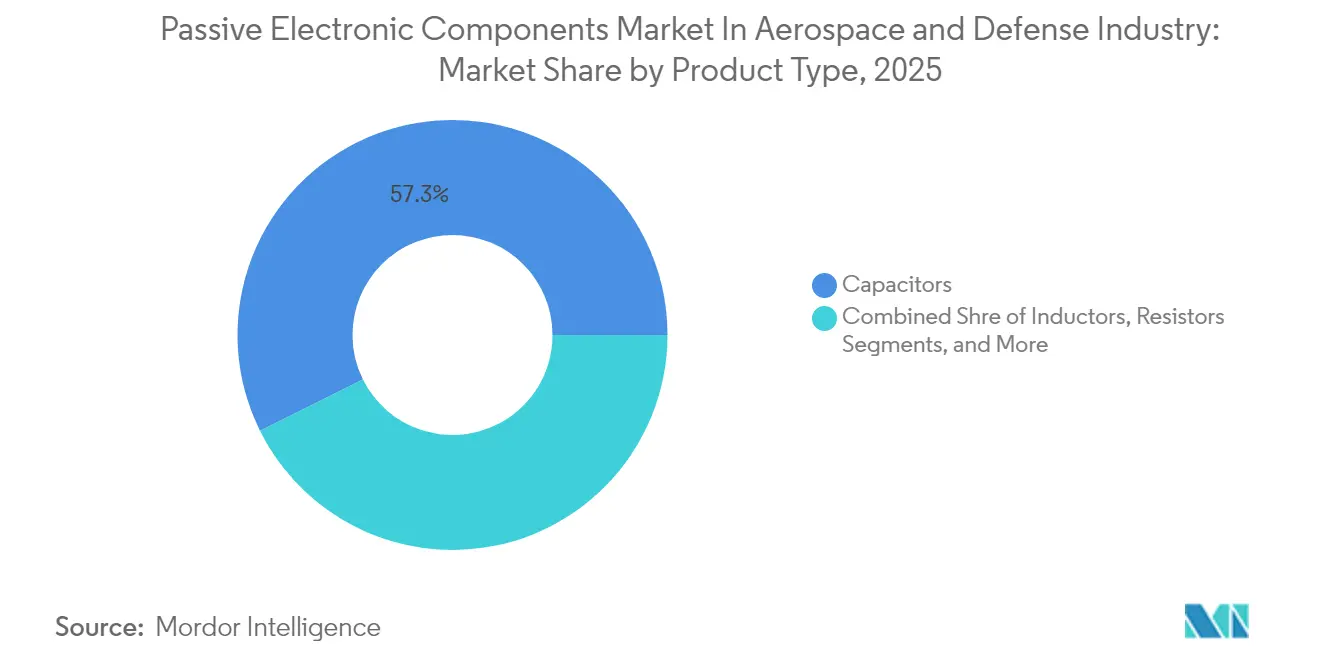

- By product type, capacitors led with 57.34% revenue share in 2025; the same segment is forecast to expand at an 7.68% CAGR through 2031.

- By platform, fixed-wing aircraft accounted for 31.62% of the market share in 2025, while unmanned aerial vehicles are projected to post the fastest 7.55% CAGR to 2031.

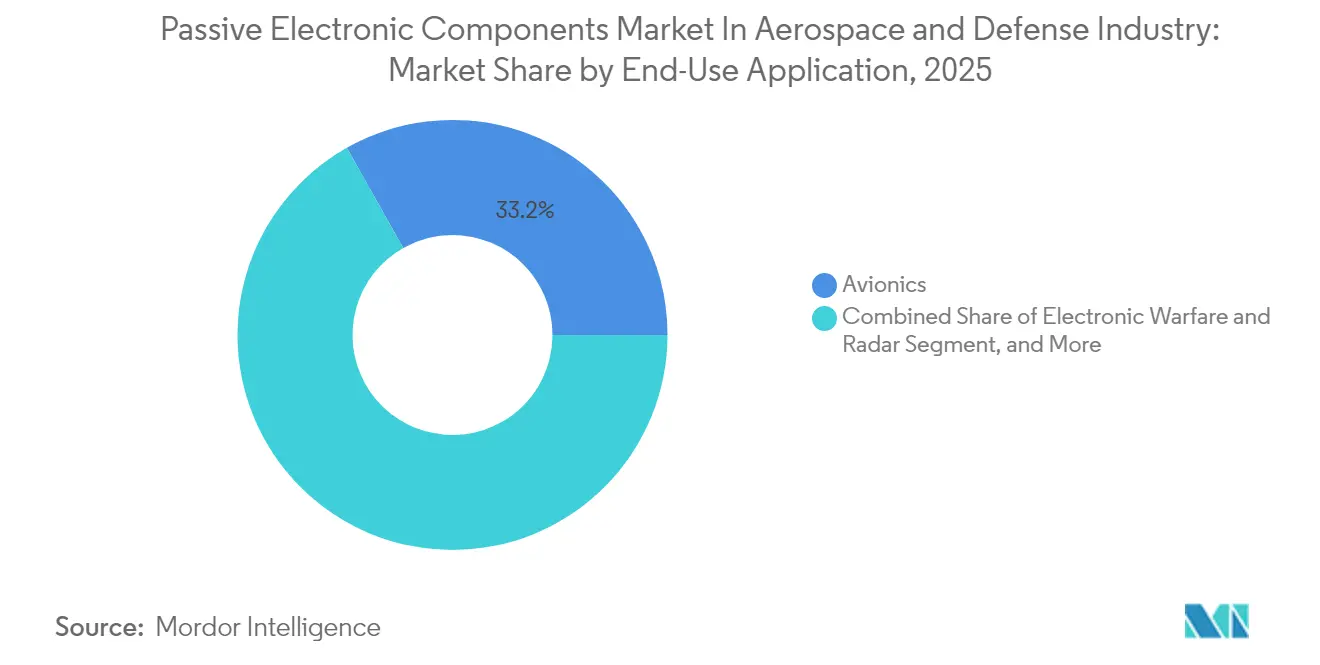

- By application, avionics captured a 33.18% share in 2025, while electronic warfare systems are advancing at a 7.41% CAGR through 2031.

- By geography, North America held 33.05% of 2025 revenue, whereas Asia-Pacific is set to grow at an 7.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of Passive Electronic Components Market in Aerospace And Defense Industry

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| More-electric aircraft architectures | +1.8% | Global; North America and Europe lead | Medium term (2-4 years) |

| Defense electronics modernization budgets | +1.5% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Expansion of LEO satellite constellations | +1.2% | Global, North America, and Asia-Pacific core | Short term (≤ 2 years) |

| Shift to wide-bandgap (GaN/SiC) power electronics | +0.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Additive manufacturing of custom RF passives | +0.6% | North America, Europe | Long term (≥ 4 years) |

| NATO STANAG-4736 RoHS-like mandates | +0.4% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of More-Electric Aircraft Architectures

Airframe primes are replacing hydraulics and pneumatics with electrically driven subsystems, a shift that intensifies power densities and thermal loads across next-generation platforms. Collins Aerospace has field-tested megawatt-class distribution prototypes under the Clean Aviation SWITCH program, validating component operation at unprecedented electrical stress levels.[1]South China Morning Post, “China’s Critical Minerals Dominance Threatens US Military Supply Chain,” scmp.comSilicon carbide-based power stages developed by GE Aerospace deliver roughly 3 × higher power density and 3% efficiency gains versus legacy silicon devices, prompting matching advances in capacitors, resistors, and magnetic components. Airbus and Toshiba have partnered on superconducting 2 MW propulsion concepts, signaling future demand for cryogenic-compatible passives. As voltage ratings rise toward the kV class, dielectric materials with low loss tangents and minimal parasitic inductance gain strategic importance. Suppliers with in-house ceramic formulation and proprietary foil technologies position themselves to capture emerging design slots across commercial and military aircraft builds.

Rising Defense Electronics Modernization Budgets

The U.S. Army earmarked USD 8.6 billion in FY 2025 for communications and electronics procurement, a budget line that indirectly scales passive component volumes across radio, sensor, and fire-control subsystems. Similar investment patterns in Europe focus on radar upgrades and counter-drone electronic warfare suites. BAE Systems received contracts exceeding USD 440 million to modernize Bradley A4 vehicles with digitized electronics, driving demand for high-reliability passives that meet MIL-PRF and DO-160 qualifications.[2]BAE Systems, “Bradley A4 Modernization Contract Award,” baesystems.com Defense primes are layering artificial intelligence into signal-processing chains, prompting tighter voltage tolerances and wider operating temperature windows for supporting capacitors and inductors. Program schedules often outlast commercial product life cycles, so vendors with long-term supply agreements and obsolescence management services maintain an edge. As open-systems architectures proliferate, interchangeability requirements elevate the importance of footprint-compatible passive devices qualified to multiple standards.

Expansion of LEO Satellite Constellations

Mega-constellation operators have accelerated order placements for space-qualified RF and microwave hardware. Filtronic’s E-band amplifiers shipped to the Starlink program underscore the volume potential for millimeter-wave passives that can withstand radiation, thermal cycling, and outgassing constraints. ASTM E595 drives component material selections by capping condensable volatile matter to 0.10%, a threshold that favors polymer film capacitors with low residual solvents. CubeSat integrators demand miniature inductors and resistors that combine high Q factor with lightweight packaging. National space agencies in Asia-Pacific are channeling procurement budgets toward indigenous component ecosystems, a development that opens licensing opportunities for Western IP holders. Qualification costs remain high, but steady launch cadences justify dedicated production lines optimized for flux-free soldering, vacuum bake-outs, and serialized lot traceability.

Shift to Wide-Bandgap (GaN/SiC) Power Electronics

Onsemi committed USD 2 billion to expand European silicon carbide wafer capacity, validating long-term demand for wide-bandgap devices that switch at megahertz frequencies. Passive networks surrounding these fast switches must exhibit low parasitic values and high thermal endurance as junction temperatures near 200 °C. Qorvo’s 750 V SiC JFETs with 4 mΩ RDS(on) bracket the current envelope, compelling matching advances in snubber capacitors and high-frequency ferrites. Aerospace engineers seek inductors with cobalt-based amorphous cores that maintain permeability at high temperatures. Packaging innovations such as lead-frame molding and direct-bond-copper substrates improve thermal paths while preserving board real estate, reinforcing cross-disciplinary collaboration between passive suppliers and power semiconductor vendors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in tantalum and palladium prices | -0.8% | Global; Asia-Pacific most affected | Short term (≤ 2 years) |

| Geopolitical supply-chain disruptions | -1.2% | Global; North America and Europe most affected | Medium term (2-4 years) |

| Qualification bottlenecks for 3-D-printed passives | -0.4% | North America, Europe | Long term (≥ 4 years) |

| Stricter CubeSat out-gassing limits on polymer films | -0.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Tantalum and Palladium Prices

Tantalum and palladium supply remains concentrated in a handful of mining nations, exposing aerospace supply chains to price spikes and export restrictions. The U.S. Government Accountability Office reported that the Department of Defense relies on imports for 100% of its tantalum needs, amplifying vulnerability for mission-critical capacitors.[3]Government Accountability Office, “Critical Materials: Action Needed to Implement Requirements That Reduce Supply Chain Risks,” gao.gov Spot market surges compress margins for component makers that must honor fixed-price contracts awarded years earlier. Alternate dielectrics such as niobium oxide and high-voltage multilayer ceramic variants are under evaluation, yet qualification timelines delay their broad rollout. Manufacturers have responded by stockpiling strategic reserves and establishing dual-sourcing frameworks across continents. Financial hedging products provide partial relief but cannot mitigate delivery risk when export bans take effect with minimal notice.

Geopolitical Supply-Chain Disruptions

The U.S.–China Economic and Security Review Commission notes that nearly 90% of global rare-earth processing capacity resides in China, a single-country exposure that unbalances competitive dynamics. Recent export-license requirements on gallium and germanium extend control levers that directly affect semiconductor substrates used in millimeter-wave passives. Supply diversification initiatives outlined in the CHIPS Act have triggered ground-breaking ceremonies for new facilities, yet the GAO estimates that a decade of capital investment is required before meaningful domestic refining capacity comes online. European aerospace primes are redistributing procurement volumes to trusted foundries in Singapore and Malaysia, but logistics complexity and increased working capital accompany this pivot. Defense programs with long planning horizons incorporate escalation clauses to account for rapid tariff changes and material embargoes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Capacitors Support High-Density Power Needs

Capacitors held a 57.34% share of the passive electronic components market in 2025 and are on track for an 7.68% CAGR, reflecting their central role in energy storage, power conditioning, and electromagnetic interference suppression. Tantalum and high-capacitance multilayer ceramics help satisfy hold-up times dictated by MIL-STD-704F, ensuring avionics remain powered during generator transients. This product class benefits from megawatt-class voltage rails introduced in more-electric aircraft, where film designs with polypropylene or fluorinated dielectrics deliver low dissipation factors at elevated temperatures. Inductors and resistors follow with mature demand curves but still post mid-single-digit growth as RF front-ends migrate toward higher frequencies. Miniaturization efforts push component footprints below 0402 sizes while maintaining reliability under wide temperature swings.

The passive electronic components market demands tighter tolerance and higher voltage ratings, prompting investments in thin-film deposition, photo-lithography, and autonomous optical inspection. Suppliers that vertically integrate powdered metal atomization and ceramic tape casting gain supply assurance during raw-material shortages. Meanwhile, interest in embedded passives fabricated directly into printed circuit boards offers weight savings for satellites and UAVs. Adoption hinges on IPC-6012 qualification cycles and the ability to meet rework requirements during board assembly. Addressing both ends of the spectrum, vendors now offer hybrid capacitor modules that combine film and ceramic elements to optimize ripple handling and volumetric efficiency.

By Platform: UAV Growth Supersedes Traditional Airframes

Fixed-wing aircraft delivered 31.62% revenue share in 2025, underpinned by single-aisle jet production rates yet constrained by long replacement cycles. Ongoing cockpit digitization and predictive maintenance systems fuel incremental passive content, but growth remains moderate. Rotary-wing airframes, missiles, and satellite buses each present specialized thermal or shock environments that translate into premium pricing tiers for radiation-tolerant or high-G-rated passives.

Unmanned aerial vehicles, by contrast, lead segment growth at a 7.55% CAGR. Defense ministries see persistent surveillance and precision strike capabilities as force multipliers, pushing active procurement programs. Commercial drones for cargo delivery, agriculture, and inspection adopt sensor-rich payloads needing high-frequency capacitors and lightweight inductors. The passive electronic components market gains from shorter design cycles in the UAV domain, allowing newer dielectrics and board-embedded passives to move from concept to flight in under 24 months. Regulatory harmonization among civil aviation authorities further accelerates the deployment of beyond-visual-line-of-sight systems, expanding addressable volumes for qualified component suppliers.

By End-Use Application: Electronic Warfare Accelerates Component Innovation

Avionics represented 33.18% of revenue in 2025, reflecting mandatory passive-content baselines for flight control, navigation, and display systems. Reliability metrics such as FIT rates below 0.1 per million hours sustain the need for conservative derating practices and redundant architectures. Power distribution assemblies capitalized on electrification trends, integrating high-energy density capacitors that can tolerate ripple currents exceeding 100 A.

Electronic warfare and radar installations offer the fastest-growing application track at 7.41% CAGR. These systems operate across ultra-wide frequency bands, driving demand for broadband filters and low-loss substrates. Passive networks must sustain peak pulsed power while maintaining phase linearity to prevent signal distortion. The passive electronic components market size allocated to thermal management also increases as gallium nitride amplifiers generate heat fluxes surpassing 5 W /cm². Advanced materials such as aluminum nitride substrates assist in dissipating localized hotspots, preserving the mean time between critical failure targets.

Geography Analysis

North America commanded a 33.05% share of the passive electronic components market in 2025, buoyed by strong defense budgets and a mature commercial aerospace supply chain. Government programs funded under the CHIPS and Science Act target domestic processing of gallium and rare earths, yet the GAO cautions that meaningful capacity will not arrive before 2030. Leading primes such as Boeing, Lockheed Martin, and Raytheon emphasize supplier resilience, awarding multiyear agreements to component makers that maintain redundant North American manufacturing sites. Policy incentives encourage the reshoring of wafer-level capacitor fabrication, though high capital intensity slows greenfield progress. Export compliance regimes, including ITAR and DFARS cybersecurity clauses, introduce administrative overhead, favoring incumbents versed in defense contracting.

Asia-Pacific is forecast to log the highest 7.86% CAGR through 2031, propelled by rising aircraft fleet counts and indigenous defense projects. China, Japan, South Korea, and India invest heavily in LEO and GEO satellite constellations, multiplying demand for radiation-hardened passives. Electronics manufacturing clusters across Southeast Asia provide cost-competitive assembly for multilayer ceramic capacitors and wire-wound inductors. However, the region’s structural reliance on imported cobalt, tantalum, and palladium exposes pricing to external shocks. OEMs respond by expanding local research and development centers to customize designs for regional airworthiness regulations. Strategic stockpiling and material substitution programs mitigate near-term exposure to geopolitical supply disruptions.

Europe maintains solid participation in the passive electronic components market thanks to advanced civil aerospace programs and defense modernization across NATO members. Environmental legislation accelerates the replacement of legacy chemistries with RoHS-compliant alternatives, fostering innovation in lead-free solder alloys and halogen-free laminates. Collaborative frameworks under the Clean Aviation Joint Undertaking allow shared risk on electrification demonstrators. Satellite prime contractors in France, Germany, and the United Kingdom contractually mandate European content for space-grade passives, safeguarding local supply chains. While the Middle East and Africa show nascent volumes, sovereign defense procurement packages increasingly stipulate technology-transfer clauses, presenting long-term opportunities for qualified suppliers willing to invest in local assembly and test operations.

Competitive Landscape

The passive electronic components market exhibits moderate fragmentation, with the top five vendors. TDK Corporation, Murata Manufacturing, and Vishay Intertechnology leverage vertically integrated ceramic and film capabilities, aligning product roadmaps with avionics and power system trends. Murata has completed 13 acquisitions since 2020, including a January 2025 investment in Sensoride that extends sensing expertise into navigation and condition-monitoring applications. Vishay focuses on long-lifecycle franchises, maintaining die banks and historical tooling that de-risk obsolescence for defense primes.

Strategic consolidation reshapes mid-tier suppliers. Teledyne closed a USD 57.3 million deal for Micropac Industries in December 2024, widening its catalog of high-reliability optoelectronics and hermetic packaging.[4]B. Riley Financial, “All Flex Acquisition Announcement,” brileyfin.com In January 2025, Micross acquired Integra Technologies, forming the largest U.S. outsourced semiconductor assembly and test provider dedicated to high-reliability markets. Private equity stakes in defense electronics inject capital for capacity expansion yet draw scrutiny over long-term security of supply.

Technology partnerships complement mergers. The 3D Systems-Airbus collaboration qualified additive manufactured RF antenna components for the OneSat platform, reducing mass by 50% compared with machined aluminum. CAES and SWISSto12 launched joint development of Monolithic Microwave Integrated Circuit (MMIC) packaging optimized for Ka-band communications. Vendors increasingly publish material data packages to accelerate customer qualification, fostering ecosystem transparency.

Leaders of Passive Electronic Components Market in Aerospace And Defense Industry

TDK Corporation

Vishay Intertechnology Inc.

KYOCERA AVX Components Corp.

KEMET Corporation (Yageo)

Panasonic Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Pasternack and PMI signed a private-label agreement to broaden RF and microwave distribution reach.

- February 2025: ICAPE Group acquired Kingfisher PCB and formed a U.K. PCB Business Unit to support European aerospace clients.

- January 2025: Murata Manufacturing acquired a stake in Sensoride, deepening its sensor technology portfolio.

- January 2025: Micross acquired Integra Technologies, creating the largest U.S. high-reliability microelectronics OSAT provider.

Scope of Report on Passive Electronic Components Market in Aerospace And Defense Industry

The market is defined by the revenue generated from the sale of passive electronic components in the aerospace and defense industry globally.

The passive electronic components market in the aerospace and defense industry is segmented by type (capacitors, inductors, resistors), application (aerospace, defense), and geography (North America, Europe, Asia Pacific, Latin America, Middle East, and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Capacitors |

| Inductors |

| Resistors |

| Other Passive Component Product Types (Transformers, Crystals) |

| Fixed-wing Aircraft |

| Rotary-wing Aircraft |

| Unmanned Aerial Vehicles (UAVs) |

| Spacecraft and Satellites |

| Missiles and Guided Weapons |

| Avionics |

| Communications and Navigation |

| Power Distribution and Conditioning |

| Electronic Warfare and Radar |

| Thermal Management |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Capacitors | ||

| Inductors | |||

| Resistors | |||

| Other Passive Component Product Types (Transformers, Crystals) | |||

| By Platform | Fixed-wing Aircraft | ||

| Rotary-wing Aircraft | |||

| Unmanned Aerial Vehicles (UAVs) | |||

| Spacecraft and Satellites | |||

| Missiles and Guided Weapons | |||

| By End-Use Application | Avionics | ||

| Communications and Navigation | |||

| Power Distribution and Conditioning | |||

| Electronic Warfare and Radar | |||

| Thermal Management | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the passive electronic components market in aerospace and defense for 2026?

The market stands at USD 4.34 billion in 2026 and is forecast to reach USD 5.77 billion by 2031.

Which product category leads revenue?

Capacitors dominate with a 57.34% share in 2025 and are also the fastest-growing segment at 7.68% CAGR.

What region is expanding the fastest?

Asia-Pacific is projected to record an 7.86% CAGR through 2031, driven by rising aircraft production and defense spending.

Which platform segment shows the highest growth?

Unmanned aerial vehicles are expected to grow at a 7.55% CAGR, outpacing fixed-wing and rotary-wing airframes.

What is the biggest restraint on future growth?

Geopolitical supply-chain disruptions, including export controls on critical minerals, impose the greatest downward pressure on CAGR.

How competitive is the supplier landscape?

The market is moderately concentrated, with the top five vendors holding about 45% of revenue and an overall competition score of 5.

Page last updated on: