Electromagnetic Compatibility Test Equipment And Testing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

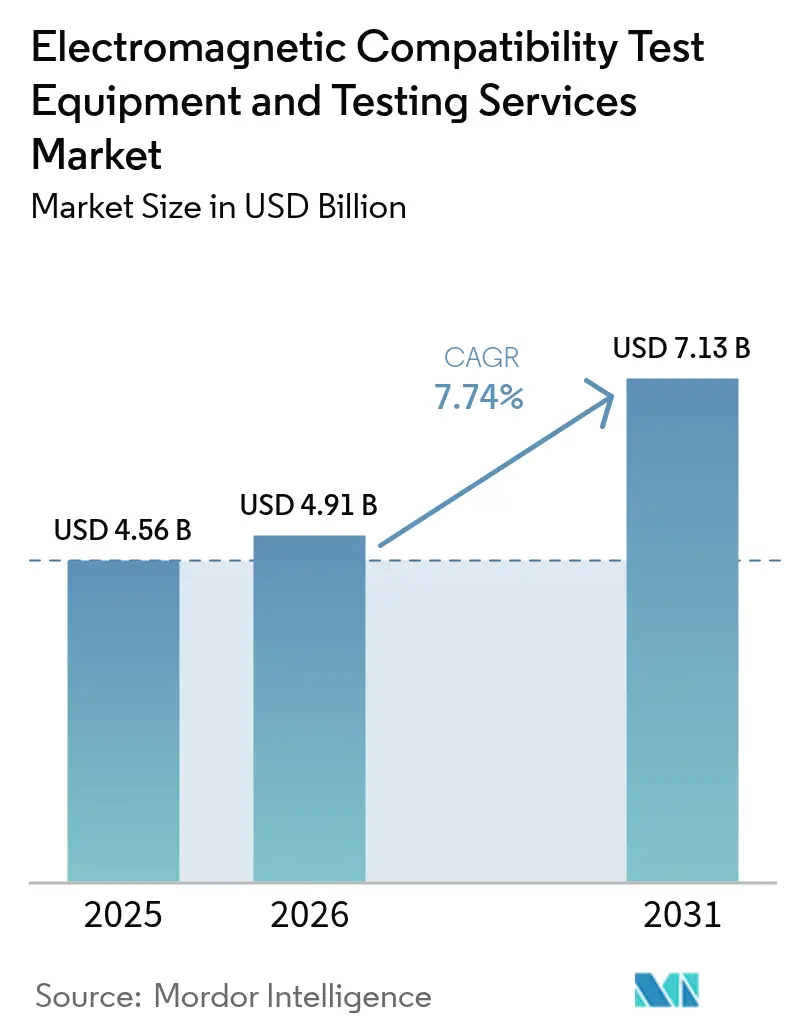

| Market Size (2026) | USD 4.91 Billion |

| Market Size (2031) | USD 7.13 Billion |

| Growth Rate (2026 - 2031) | 7.74% CAGR |

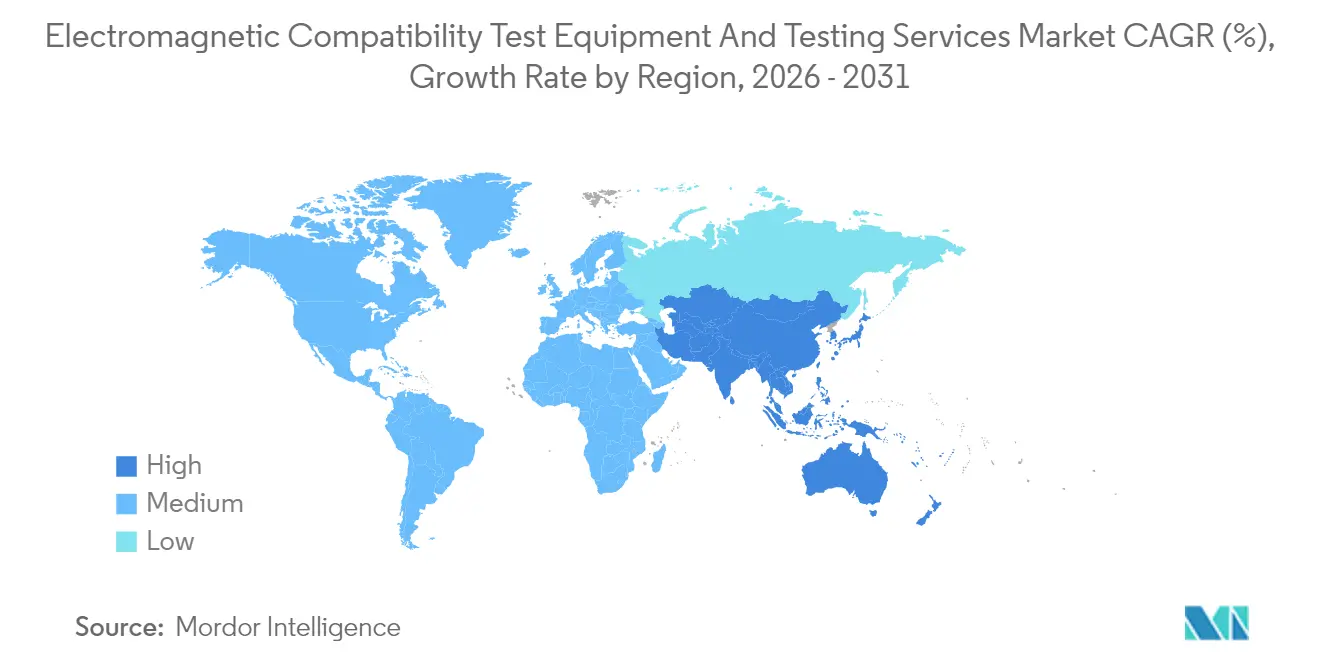

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

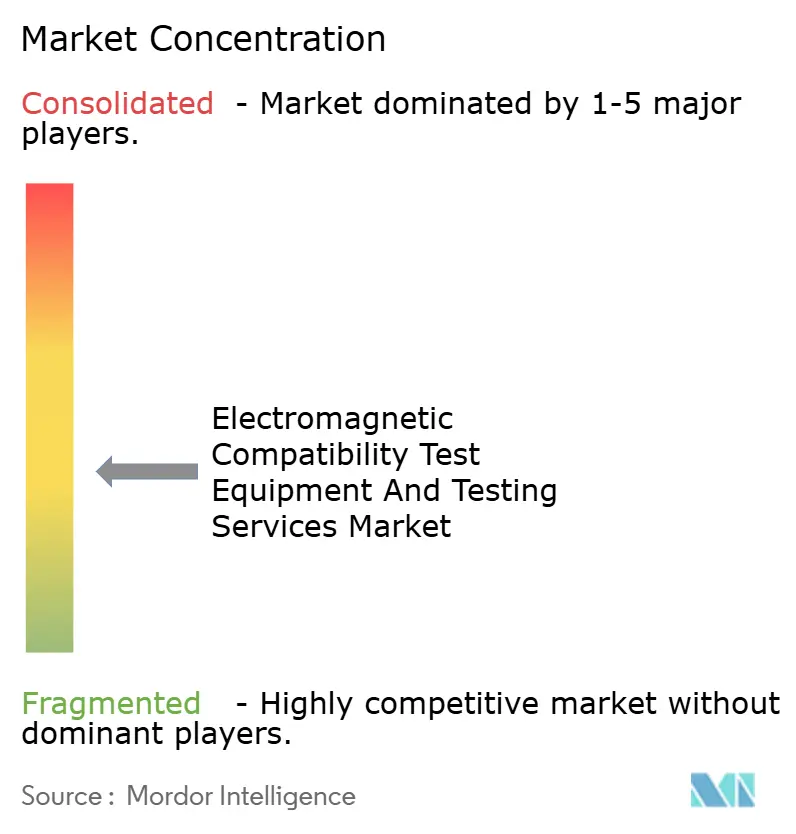

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electromagnetic Compatibility Test Equipment And Testing Services Market Analysis by Mordor Intelligence

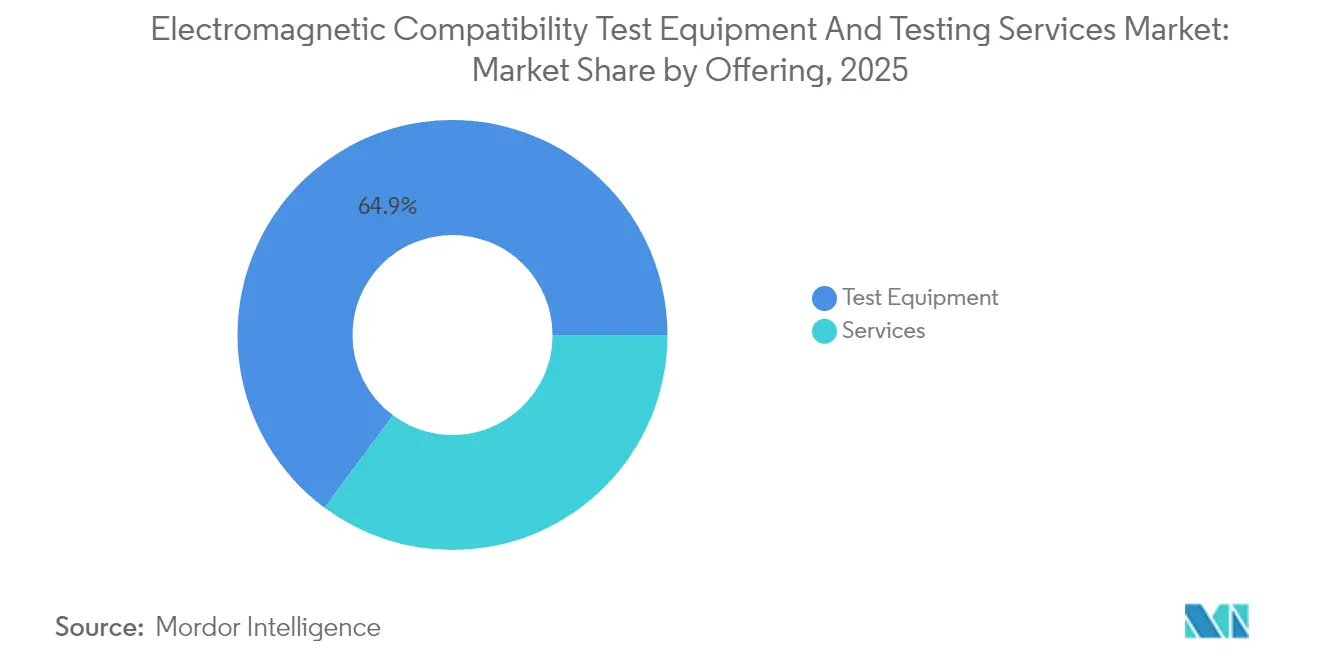

The electromagnetic compatibility test equipment and testing services market size was valued at USD 4.56 billion in 2025 and estimated to grow from USD 4.91 billion in 2026 to reach USD 7.13 billion by 2031, at a CAGR of 7.74% during the forecast period (2026-2031). 5G densification, electric-vehicle mandates and satellite mega-constellations are tightening radiated and conducted emission limits, which lifts test demand across emissions, immunity and on-orbit validation programs. The electromagnetic compatibility test equipment and testing services market continues to draw capital because spectrum analyzers, EMI receivers and reverberation chambers remain compulsory for every new electronic design entering high-volume production. Equipment led 2024 revenue with a 65.55% slice while third-party services accelerate on a pay-per-test model that frees OEM cash for battery and software projects. Asia-Pacific is the fulcrum of laboratory expansion as regulators in China, India and South Korea align domestic GB/T and KS C limits with CISPR and FCC thresholds, which fuels double-digit spending on new 10-meter chambers. Vendors are embedding artificial-intelligence-driven anomaly detection into receivers, but certification bodies are still validating these workflows, which leaves a near-term compliance blind spot.

Key Report Takeaways

- By offering, test equipment captured 64.85% of 2025 revenue while services are forecast to expand at a 9.25% CAGR through 2031.

- By equipment type, spectrum analyzers led with 28.95% of 2025 revenue, whereas EMI receivers are projected to rise at a 10.44% CAGR to 2031.

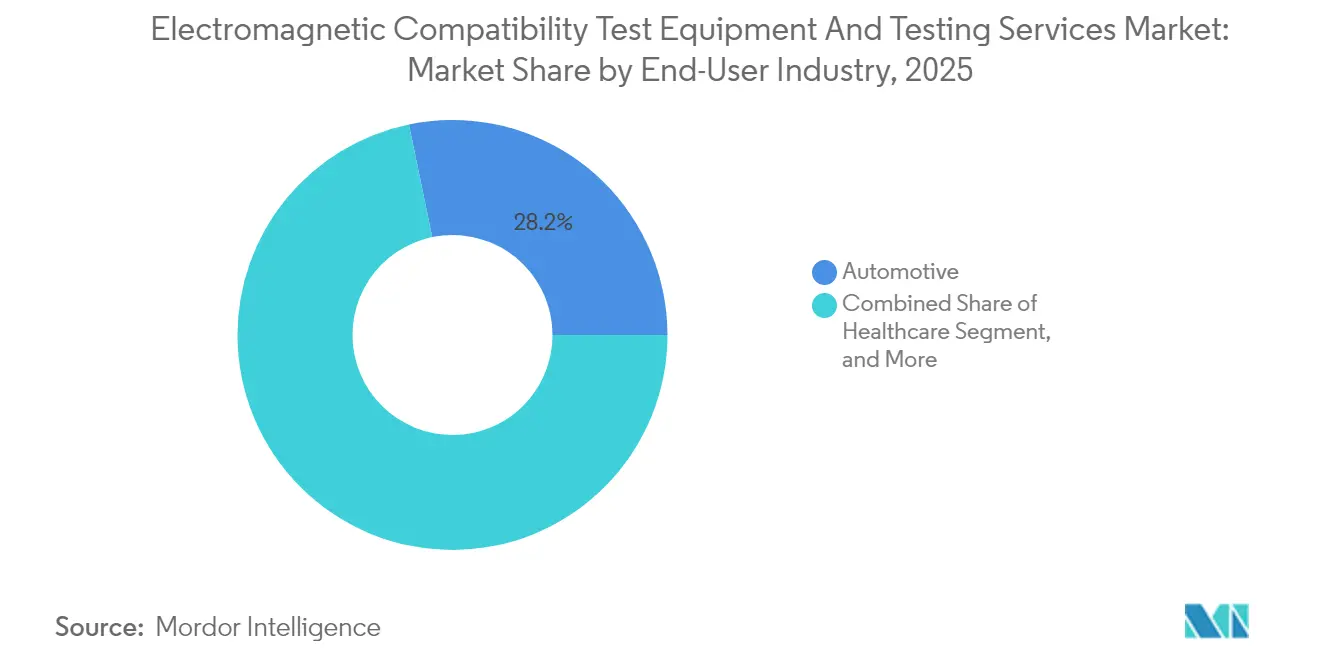

- By end-user, automotive accounted for 28.25% of 2025 spending and healthcare is poised for a 9.67% CAGR through 2031.

- By standard family, CISPR protocols governed 35.90% of 2025 testing while FCC-aligned procedures are projected to grow at 10.54% CAGR to 2031..

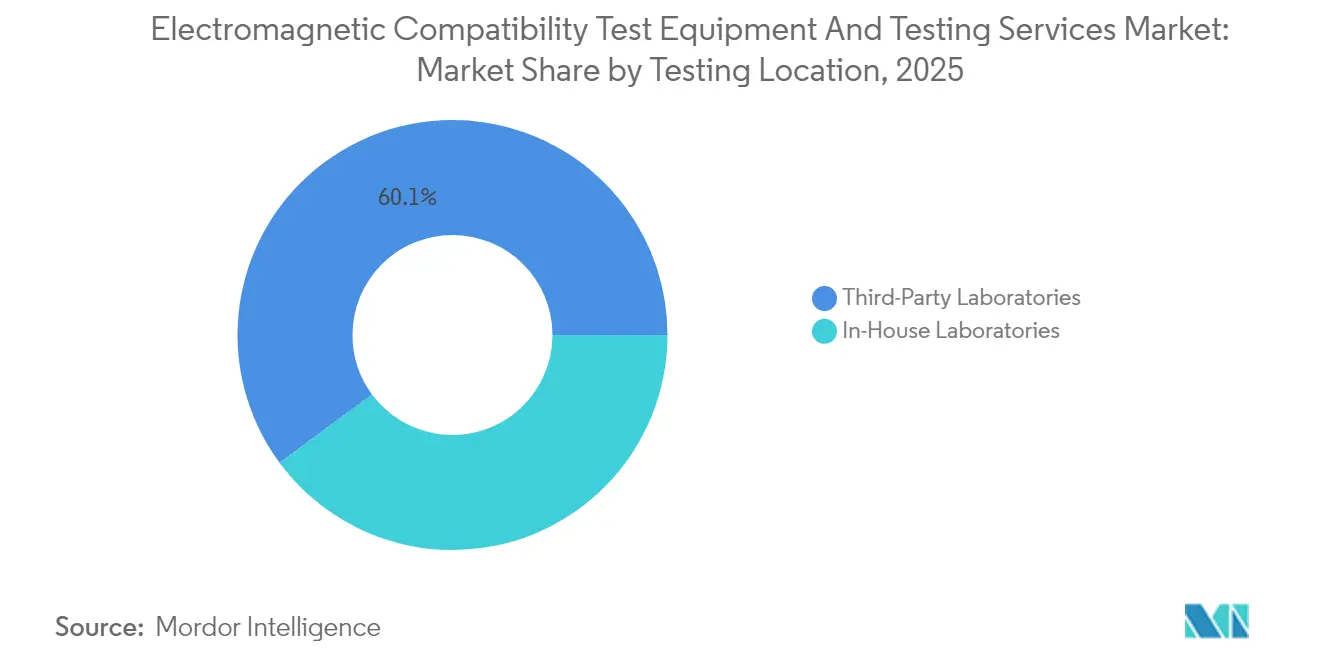

- By testing location, third-party laboratories controlled 60.12% of 2025 revenue and will advance at an 11.55% CAGR to 2031.

- By application, radiated emission dominated with a 45.10% share in 2025 but immunity evaluations are set to increase at 9.06% CAGR to 2031..

- By geography, Asia-Pacific held 40.45% of 2025 revenue and is expected to expand at an 11.21% CAGR, outpacing North America and Europe.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electromagnetic Compatibility Test Equipment And Testing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of 5G Infrastructure Across Emerging Economies | +1.8% | APAC core (India, Indonesia, Vietnam), spill-over to Middle East | Medium term (2-4 years) |

| Rapid Proliferation of IoT-Enabled Devices in Critical Sectors | +1.6% | Global, with early concentration in North America and EU industrial hubs | Short term (≤ 2 years) |

| Stringent Global EMC Regulations for Electric Vehicle Components | +1.5% | Global, led by EU (UNECE R10), China (GB/T), North America (FCC Part 15) | Medium term (2-4 years) |

| Increasing Electromagnetic Complexity in Aerospace Electrification | +1.3% | North America and EU aerospace corridors, expanding to APAC suppliers | Long term (≥ 4 years) |

| Growing Adoption of Wireless Medical Devices in Healthcare | +0.9% | North America and EU, gradual uptake in APAC urban centers | Medium term (2-4 years) |

| Rising Satellite Mega-Constellation Launches Requiring On-Orbit EMC Validation | +0.7% | Global, concentrated in U.S. (SpaceX, Amazon) and EU (OneWeb) launch markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of 5G Infrastructure Across Emerging Economies

Telecom operators in India, Indonesia and Vietnam plan to deploy more than 500,000 new 5G base stations between 2024 and 2026, each of which must undergo IEC 62232 and CISPR 32 emission checks before on-air activation. Dynamic beam-steering antennas with 64- to 128-element arrays require over-the-air testing that doubles chamber usage hours per device, lifting bookings for accredited labs. The International Telecommunication Union tightened adjacent-channel power-ratio thresholds at its 2024 World Radiocommunication Conference, forcing re-measurement of small-cell radios that were certified under earlier, looser limits. Equipment suppliers answered by integrating beamforming analytics into test systems that compress certification cycles from 12 weeks to six weeks. Mutual-recognition pacts signed by the Telecommunications Engineering Centre in India and the Vietnamese Ministry of Information and Communications allow local certificates to be accepted in Europe and the United States, further accelerating demand for regional laboratories.[1]Telecommunications Engineering Centre, “EMC Testing Capacity Expansion Report,” TEC.GOV.IN

Rapid Proliferation of IoT-Enabled Devices in Critical Sectors

Industrial players are swapping wired SCADA nodes for wireless sensors that crowd the 2.4 GHz and 5 GHz ISM bands, increasing electromagnetic risk to legacy programmable controllers.[2]IEEE Standards Association, “IEEE P1528.7 Standard for EMC Test Methods for IoT Devices,” IEEE.ORG The IEEE P1528.7 standard, issued in 2024, prescribes 10 V/m immunity and 2 kV fast-transient resilience, raising test complexity for IIoT gateways. Automotive suppliers add wireless tire-pressure and battery-management sensors that must pass both CISPR 25 emission scans and IEC 61000-4 immunity sweeps, doubling the bill-of-test for each new.. Keysight Technologies reported a 34% year-over-year jump in orders for its UXA signal analyzer optimized for Bluetooth Low Energy and Zigbee traffic, highlighting the pull-through effect on equipment sales. Co-location of functional-safety and EMC chambers is becoming standard practice, which lifts facility investment barriers and tilts share toward large, well-funded service providers

Stringent Global EMC Regulations for Electric Vehicle Components

UNECE Regulation 10 Revision 7, enforced in January 2024, introduces 200 V/m immunity tests and tighter limits above 1 GHz, forcing full-vehicle validations rather than component bench.[3]United Nations Economic Commission for Europe, “UNECE Regulation 10 Revision 7,” UNECE.ORG China elevated the bar further by mandating 20-meter chamber tests for battery-electric passenger cars under GB/T 18655-2024, a shift that channels projects to top-tier laboratories with oversized facilities. The U.S. Federal Communications Commission has proposed extending Part 15 limits to home charging equipment, citing consumer complaints about Wi-Fi disruption near driveways. Bureau Veritas noted that average EV certification timelines rose to 18 months in 2024 because high-voltage inverter filters induce unplanned resonances that require multiple retests. Automakers are fast-tracking active EMI filter designs yet still depend on third-party labs for impartial pass/fail evidence acceptable to regulators worldwide

Increasing Electromagnetic Complexity in Aerospace Electrification

Electric actuators and high-speed power electronics on single-aisle jets concentrate kilowatts of switching noise inside tight equipment bays that also host flight-critical avionics. RTCA DO-160G amendments released in 2024 lifted immunity thresholds for high-intensity radiated fields to 7,200 V/m, which doubles the amplifier power needed for certification. Airbus disclosed that the A320neo family contains more than 40 electric actuators, each requiring stand-alone and system-level testing to prove cumulative emissions remain below cockpit-display susceptibility limits. The European Union Aviation Safety Agency now mandates in-service monitoring of electromagnetic performance in fly-by-wire systems, extending EMC oversight beyond initial type certification. Long queues at European reverberation chambers nine months in 2024 according to ETS-Lindgren are encouraging tier-1 suppliers to pre-book slots two years out, which supports sustained equipment orders

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure for Advanced Millimeter-Wave Test Chambers | -0.8% | Global, acute in emerging markets with limited laboratory infrastructure | Short term (≤ 2 years) |

| Shortage of Skilled RF and EMC Engineers | -0.6% | Global, most severe in North America and EU | Medium term (2-4 years) |

| Lengthy Certification Lead Times Causing Market Entry Delays | -0.5% | Global, with regional variations in accreditation body responsiveness | Short term (≤ 2 years) |

| Uncertainty Around Harmonization of Regional EMC Standards for Autonomous Vehicles | -0.4% | Fragmented across U.S., EU, China, and Japan regulatory zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for Advanced Millimeter-Wave Test Chambers

A 10-meter, 110 GHz-rated fully anechoic chamber costs USD 8 million to USD 12 million and occupies 400 square meters, an outlay that many mid-tier labs cannot finance. Ferrite absorber tiles must remain below –40 dB reflectivity across octave bandwidths and require USD 500,000 to USD 800,000 replacement every decade, lifting the total cost of ownership beyond the purchase price ETS. Lack of subsidized credit in India, Brazil and Indonesia forces OEMs to ship prototypes overseas, adding 8- to 12-week delays and freight costs to each certification cycle. Floor-space constraints in urban tech corridors, where industrial real-estate leases exceed USD 1,000 per square meter annually, further deter local expansion. Consequently, the electromagnetic compatibility test equipment and testing services market sees uneven geographic capacity that limits revenue realization despite robust demand.

Shortage of Skilled RF and EMC Engineers

The IEEE Electromagnetic Compatibility Society reported that 62% of North American labs struggled to hire qualified staff in 2024 and median recruitment cycles stretched to nine months. Salaries for senior EMC engineers climbed 18% in two years, compressing margins at smaller facilities and prompting them to narrow service menus to basic emission scans. Accreditation bodies such as A2LA require documented proficiency tests, but training pipelines lag because universities favor digital signal processing curricula over classical RF measurement. Bureau Veritas stated that a new hire needs 14 months of internal mentoring before leading CISPR 32 projects, which reduces billable hours and stretches payback on new chambers. The talent gap restrains theelectromagnetic compatibility test equipment and testing services market from achieving its full potential CAGR even though demand indicators remain strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain as Outsourcing Accelerates

Services accounted for 35.15% of the electromagnetic compatibility test equipment and testing services market share in 2025, but are forecast to climb at a 9.25% CAGR to 2031 as OEMs prioritize variable testing costs over depreciating assets. Intertek reported a 22% jump in outsourced EMC billing because automotive brands redirected budgets toward battery innovation and autonomous-driving software. The electromagnetic compatibility test equipment and testing services market size allocated to equipment, still dominant at USD 2.96 billion in 2025, is shifting toward lease and software-as-a-service bundles where hardware ownership stays with the vendor.

Services provide a faster path to revenue for laboratories because a single 10-meter chamber can host 15-20 client projects monthly, yielding cash flow earlier than equipment amortization schedules. Asia-Pacific contract labs in Shenzhen and Bengaluru quote 48-hour CISPR 32 scans at prices 30% lower than U.S. peers, pulling multinational handset brands into the region for pre-compliance screening. Equipment suppliers reciprocate by offering cloud-based reporting and remote-witness dashboards that make outsourced testing nearly as transparent as in-house work . The electromagnetic compatibility test equipment and testing services industry, therefore, benefits from synergies between service providers and hardware makers that jointly expand addressable clients without duplicating capital spend.

By Test Equipment Type: EMI Receivers Lead Innovation

Spectrum analyzers held 28.95% of 2025 revenue, yet EMI receivers are projected to record the fastest 10.44% CAGR as regulators tighten quasi-peak detector mandates. The electromagnetic compatibility test equipment and testing services market size tied to EMI receivers is expected to reach USD 1.18 billion by 2031 as test cycles compress from six hours to 90 minutes using real-time, gap-free sweeps. Amplifiers and signal generators each float near 15% share, supported by immunity-test demand that now calls for 30 V/m field strengths under IEC 61000-4-3 updates IEC.CH.

Commoditization looms for accessories such as LISNs and current probes, which Chinese vendors price at USD 1,200 compared with USD 4,500 from established brands, although accreditation bodies scrutinize uncertainty budgets on low-cost gear. Vendors react by embedding artificial-intelligence-driven pre-scan functions that identify emission hotspots on PCB schematics, creating software lock-in that protects margins. Overall, instrument makers that pair hardware leases with subscription analytics stand to capture recurring revenue even as per-unit prices normalize.

By End-User Industry: Healthcare Emerges as Growth Leader

Automotive led spending with 28.25% in 2025 after UNECE Regulation 10 tightened limits for battery-electric drivetrains. Yet healthcare is forecast to grow at 9.67% CAGR because IEC 60601-1-2 fourth edition demands 28 V/m immunity and extends testing up to 2.7 GHz for connected medical devices IEC.CH. The electromagnetic compatibility test equipment and testing services market size earmarked for medical electronics will likely double between 2025 and 2031 as remote patient monitoring proliferates in the United States.

Industrial IoT, consumer electronics, and IT-telecom each hover near 20% share, but lengthening smartphone refresh cycles constrain growth in consumer categories. Aerospace and defense hold around a 12% share, anchored by DO-160 and MIL-STD-461 programs for avionics and radar modules. Renewable energy equipment, especially solar inverters, contributes 8% as utility-scale farms migrate to 1,500 VDC architectures that risk harmonic injection into grid telemetry. Smaller niches such as rail, marine, and quantum computing round out demand, often requiring bespoke test fixtures that command premium billing rates.

By EMC Standards: FCC Protocols Accelerate

CISPR protocols controlled 35.90% of 2025 test hours, while FCC procedures are projected to climb at a 10.54% CAGR as unlicensed 6 GHz devices proliferate under Part 15.247. The electromagnetic compatibility test equipment and testing services market share linked to FCC authorizations will therefore rise faster than its European counterparts through 2031. MIL-STD-461 persists at roughly 18% because defense ministries refresh procurement for avionics and communications.

IEC standards, spanning industrial, medical and renewable energy applications, represent 22% and continue to gain as smart-grid and e-mobility technologies standardize on IEC 61000-6-x immunity benchmarks. Fragmentation across national variants-GB/T in China, KS C in South Korea-still forces OEMs into redundant campaigns, which triples cost and prolongs development schedules by up to six months. Standardization bodies are negotiating reciprocity but detector weighting and uncertainty budgets remain sticking points.

By Testing Location: Third-Party Labs Dominate

Third-party laboratories controlled 60.12% of 2025 revenue and are on course for an 11.55% CAGR thanks to pay-per-use attractiveness. A single 10-meter chamber can serve 20 client projects per month, delivering superior asset utilization compared with in-house sites that may stand idle outside prototype phases. The electromagnetic compatibility test equipment and testing services market size attributable to external labs is forecast to eclipse USD 4.25 billion by 2031.

Remote witnessing via encrypted video feeds reached 65% adoption in 2024 at TÜV SÜD, slashing travel costs and expediting decision-making. OEMs still maintain strategic chambers for confidential prototypes, but rising calibration and accreditation costs of about USD 200,000 annually are nudging mid-tier manufacturers into hybrid strategies that keep a pre-scan booth on-site yet subcontract final certification. Equipment vendors respond by bundling leases with on-site engineering, a model that blurs the line between capital and service revenue.

By Application: Immunity Testing Gains Momentum

Radiated emission tests held a 45.10% share in 2025, reflecting their gatekeeper role for every electronic product. Immunity evaluations, however, are projected to rise at a 9.06% CAGR because IEC 61000-4 updates lift field strengths to 30 V/m and expand upper frequency limits to 6 GHz for industrial equipment. The electromagnetic compatibility test equipment and testing services market size tied to immunity will exceed USD 2.38 billion by 2031 if growth sustains.

Conducted emission checks remain vital in electric-vehicle powertrains, where broadband noise overlaps aircraft and AM radio bands. Regulators contemplate merging emission and immunity sweeps into unified schedules to cut certification cost by 15-20%. Anritsu’s 2024 analyzer now captures both domains simultaneously, reducing overall test time by 25% and demonstrating the productivity leap possible when hardware meets updated standards

Geography Analysis

Asia-Pacific generated 40.45% of electromagnetic compatibility test equipment and testing services market revenue in 2025 and is projected to expand at an 11.21% CAGR to 2031, the fastest among all regions. China’s revised GB/T 18655 rule shifts focus to full-vehicle testing in 20-meter chambers, compelling both domestic and foreign automakers to book local facilities in Shenzhen, Shanghai and Chongqing. India augmented national capacity by 40% in 2024 with three new 10-meter chambers under its Production-Linked Incentive scheme, which aligns export certification with ETSI and FCC requirements. South Korea’s National Radio Research Agency added stricter limits for 79 GHz automotive radar, which has sparked a round of retesting for modules supplied to Hyundai and LG Innotek. Japan introduced EN 50121-aligned immunity for railway signaling in June 2024, thereby integrating domestic rolling stock into European export portfolios. Australia and New Zealand collectively capture 4% of regional spend, led by mining equipment labs validating autonomous haul-truck electronics against high-power radar fields.

North America represented 27.75% of 2025 revenue. The U.S. processed over 12,000 FCC authorizations in 2024, a 16% jump fueled by IoT rollouts and proposed Part 15 limits for home EV chargers FCC.GOV. Canada aligns on Industry Canada limits but retains separate labeling, which forces dual filings for consumer devices. Mexico’s NOM-208 update mandated CISPR 32 compliance for all smart-home appliances, driving cross-border lab utilization in Texas and California. Europe also held 27.55% of revenue; Germany saw a 21% boost in automotive EMC demand across Bavaria and Baden-Württemberg as BMW and Mercedes tapped third-party capacity to clear UNECE Regulation 10 queues. France benefits from Airbus and Thales programs while Italy serves Stellantis suppliers. The United Kingdom created a temporary spike in retesting because post-Brexit UKCA markings replaced CE labels in 2024.

South America and the Middle East and Africa together comprised 4.25% of 2025 revenue yet both regions will post double-digit CAGRs. Brazil’s ANATEL now requires CISPR 32 for every licensed-spectrum IoT device, redirecting budgets to accredited labs in São Paulo and Rio de Janeiro. The United Arab Emirates enforced EMC checks on 5G small cells in February 2024, catalyzing new Dubai laboratories to serve Gulf Cooperation Council markets. Saudi Arabia partnered with TÜV SÜD to open a USD 18 million Riyadh center that addresses regional automotive and telecom certifications. South Africa updated IEC 61000 alignment in March 2024, opening avenues for labs in Johannesburg and Cape Town to test mining-equipment telemetry. Kenya and Nigeria start to emerge as hubs for East and West Africa respectively as mobile-network operators push for 5G coverage.

Competitive Landscape

The electromagnetic compatibility test equipment and testing services market displays moderate concentration: the top 10 players, a mix of equipment vendors and service providers, hold roughly 55% of global revenue. Rohde and Schwarz, Keysight Technologies and Anritsu dominate the instrument space by emphasizing frequency coverage and software integration, while SGS, Bureau Veritas, Intertek, TÜV SÜD and UL LLC lead testing services by accreditation breadth and turnaround. Equipment makers embed AI predictive algorithms that interpret PCB layouts, cutting pre-scan time by 50% once validated under ISO/IEC 17025.

Keysight’s PathWave EMC software generated USD 47 million in subscription revenue in Q3 2024, up 38% year-over-year, signaling a shift from one-off hardware sales to recurring analytics. Service providers consolidate to scale: Element Materials Technology acquired three Southeast Asian facilities in 2024, raising its global lab count to 18 and positioning itself as a one-stop shop for multi-standard automotive programs. Smaller regional labs counter by focusing on emerging segments such as wireless power transfer and terahertz communications, where standard methods are nascent, and clients pay premium rates for custom fixtures.

Hybrid models that combine equipment leasing with on-site engineering support are gaining traction among mid-tier OEMs that need chamber access for six-month windows but lack capital or floor space for permanent builds. Mobile chambers mounted on trailers, recently introduced by DEKRA in Germany, reduce logistics time for automotive tier-1 suppliers during design iterations. AI-driven anomaly detection still awaits regulator endorsement; until then, labs continue to perform time-consuming manual scans, which sustains demand for high-performance receivers even in mature segments.

Electromagnetic Compatibility Test Equipment And Testing Services Industry Leaders

TÜV SÜD AG

ALS Limited

Bureau Veritas SA

SGS SA

Dekra Certification B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Keysight Technologies launched the N9042B UXA X-Series signal analyzer covering up to 110 GHz for automotive radar and 5G mmWave testing.

- September 2024: SGS opened a 15,000-square-meter EMC facility in Pune, India, with two 10-meter chambers and a reverberation room for full-vehicle projects.

- August 2024: Rohde and Schwarz released its cloud-based R&S EMC32 suite, automating limit-line checks and remote chamber control.

- July 2024: Bureau Veritas acquired CETECOM Advanced in Germany for EUR 42 million (USD 45.8 million).

Global Electromagnetic Compatibility Test Equipment And Testing Services Market Report Scope

Electromagnetic compatibility (EMC) testing measures an electrical product’s ability to function satisfactorily in its intended electromagnetic environment without generating intolerable electromagnetic disturbances to anything in that environment.

The Electromagnetic Compatibility Test Equipment And Testing Services Market Report is Segmented by Offering (Test Equipment, Services), Test Equipment Type (EMI Test Receiver, Signal Generator, Amplifiers, Spectrum Analyzer, Other Test Equipment), End-User Industry (Automotive, Consumer Electronics, IT and Telecom, Aerospace and Defense, Healthcare, Renewable Energy, Other End-User Industries), EMC Standards (CISPR, MIL-STD, FCC, IEC, Other Standards), Testing Location (In-House Laboratories, Third-Party Laboratories), Application (Radiated Emission Testing, Conducted Emission Testing, Immunity Testing, Other Applications), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Test Equipment |

| Services |

| EMI Test Receiver |

| Signal Generator |

| Amplifiers |

| Spectrum Analyzer |

| Other Test Equipment |

| Automotive |

| Consumer Electronics |

| IT and Telecom |

| Aerospace and Defense |

| Healthcare |

| Renewable Energy |

| Other End-User Industries |

| CISPR |

| MIL-STD |

| FCC |

| IEC |

| Other EMC Standards |

| In-House Laboratories |

| Third-Party Laboratories |

| Radiated Emission Testing |

| Conducted Emission Testing |

| Immunity Testing |

| Other Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Nigeria | ||

| Rest of Africa | ||

| By Offering | Test Equipment | ||

| Services | |||

| By Test Equipment Type | EMI Test Receiver | ||

| Signal Generator | |||

| Amplifiers | |||

| Spectrum Analyzer | |||

| Other Test Equipment | |||

| By End-User Industry | Automotive | ||

| Consumer Electronics | |||

| IT and Telecom | |||

| Aerospace and Defense | |||

| Healthcare | |||

| Renewable Energy | |||

| Other End-User Industries | |||

| By EMC Standards | CISPR | ||

| MIL-STD | |||

| FCC | |||

| IEC | |||

| Other EMC Standards | |||

| By Testing Location | In-House Laboratories | ||

| Third-Party Laboratories | |||

| By Application | Radiated Emission Testing | ||

| Conducted Emission Testing | |||

| Immunity Testing | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the electromagnetic compatibility test equipment market?

The market is valued at USD 4.91 billion in 2026 and is projected to reach USD 7.13 billion by 2031.

Which region grows the fastest in electromagnetic compatibility testing demand?

Asia-Pacific is forecast to grow at an 11.21% CAGR as China, India and South Korea enforce stricter EMC standards.

Why are EMI receivers gaining momentum over traditional spectrum analyzers?

Regulators now require tighter quasi-peak detection, and modern EMI receivers can finish full-vehicle sweeps in 90 minutes, cutting test time by 75%.

How are 5G deployments influencing EMC testing?

5G base stations with beam-forming antennas need over-the-air emission and immunity checks, effectively doubling chamber hours per station.

What is the main challenge limiting lab capacity expansion?

The shortage of skilled RF and EMC engineers lengthens hiring cycles to nine months and inflates salary budgets, delaying new lab openings.

How does outsourcing influence OEM testing strategies?

Outsourcing to third-party labs shifts fixed equipment costs into variable operating expenses, freeing capital for R&D while accelerating certification turnarounds.

Page last updated on: