Electrical And Electronic Test Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

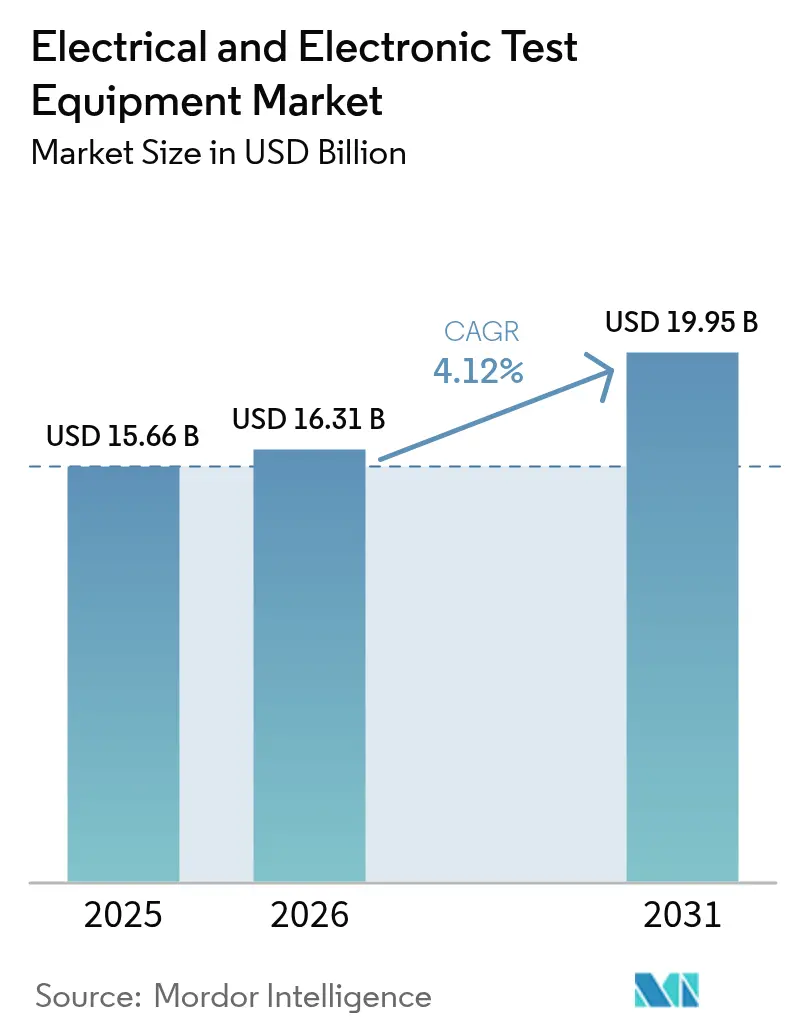

| Market Size (2026) | USD 16.31 Billion |

| Market Size (2031) | USD 19.95 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

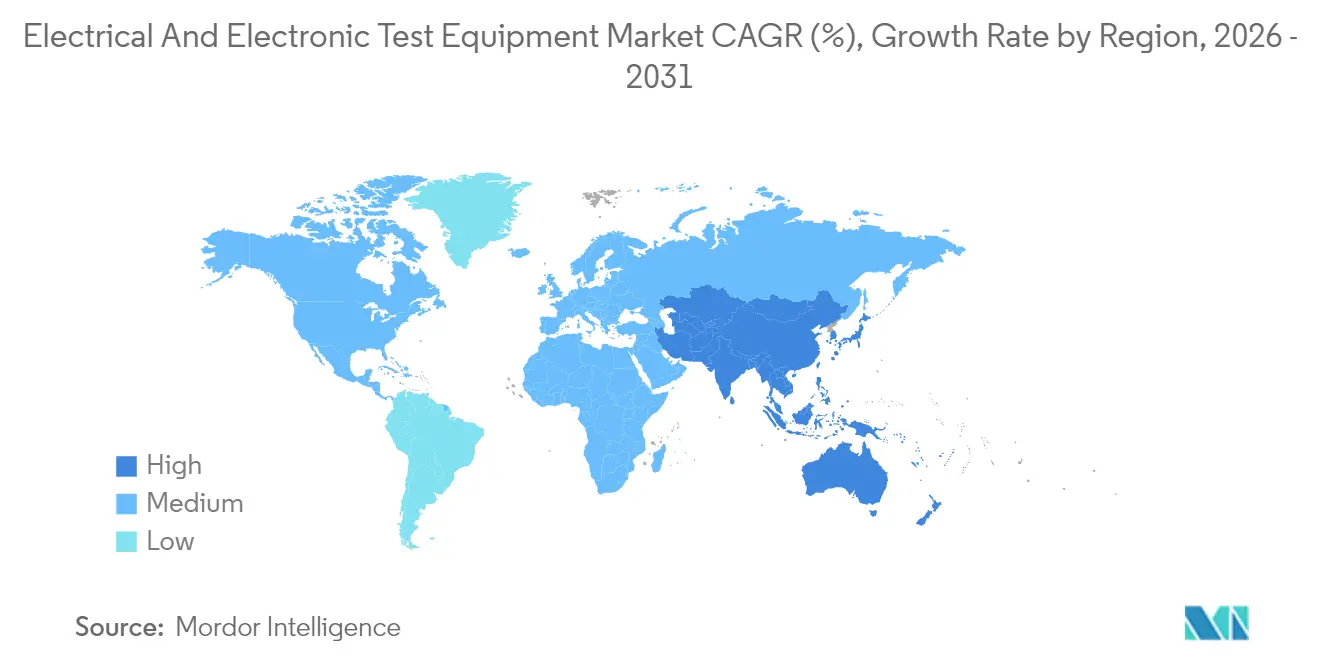

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrical And Electronic Test Equipment Market Analysis by Mordor Intelligence

The electrical and electronic test equipment market size is expected to grow from USD 15.66 billion in 2025 to USD 16.31 billion in 2026 and is forecast to reach USD 19.95 billion by 2031 at 4.12% CAGR over 2026-2031. This steady rise mirrors the growing complexity of telecommunications, automotive electrification, advanced semiconductor production and tightening IoT security rules. Demand grows as 5G millimeter-wave rollouts, 800 V electric-vehicle platforms and 3 nm chip architectures stretch legacy measurement limits. Adoption of AI-assisted automation, software-defined instruments and modular PXI systems is widening access to sophisticated capabilities while helping users mitigate supply-chain delays and component cost inflation. At the same time, competitive pressure from cost-focused Asian vendors is reshaping procurement strategies, and rental models are gaining traction among customers facing large capital outlays. These parallel trends maintain forward momentum for the electrical and electronic test equipment market despite periodic headwinds from component shortages and geopolitical disruptions.

Key Report Takeaways

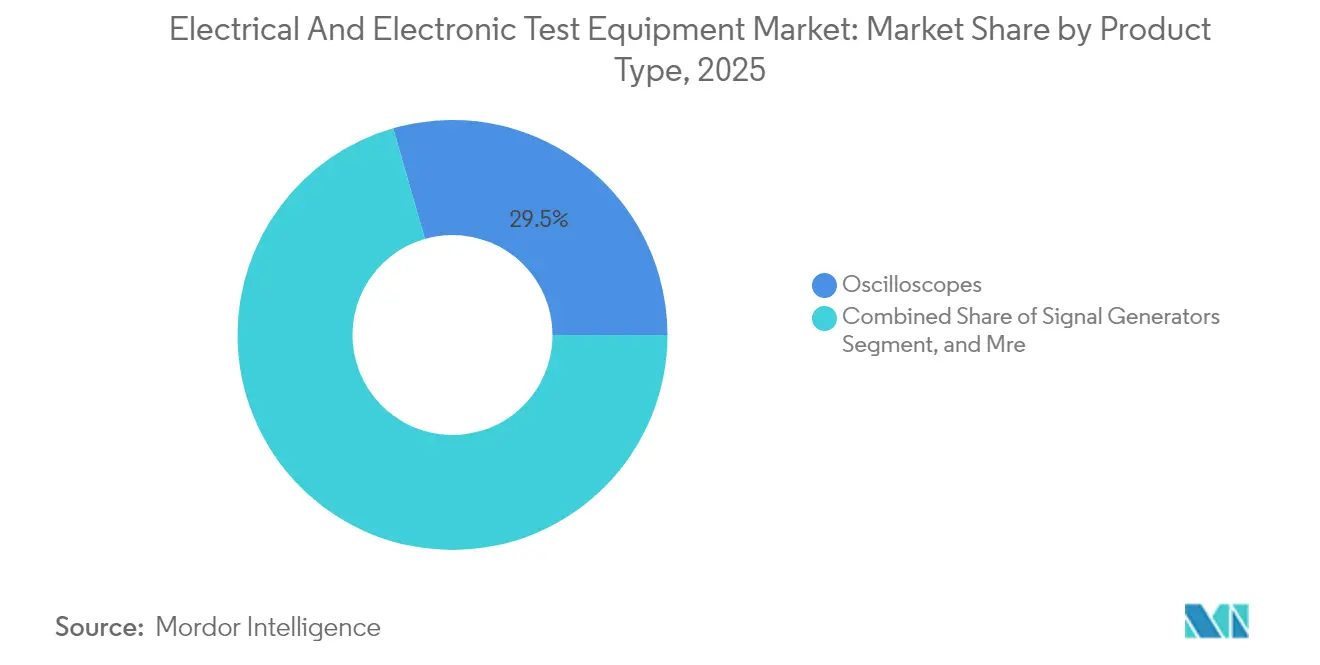

- By product type, oscilloscopes led with 29.45% of the electrical and electronic test equipment market share in 2025, whereas RF and microwave gear is projected to grow the fastest at a 4.63% CAGR to 2031.

- By form factor, benchtop platforms held 47.12% share of the electrical and electronic test equipment market size in 2025, while PXI systems show the highest projected CAGR at 5.02% through 2031.

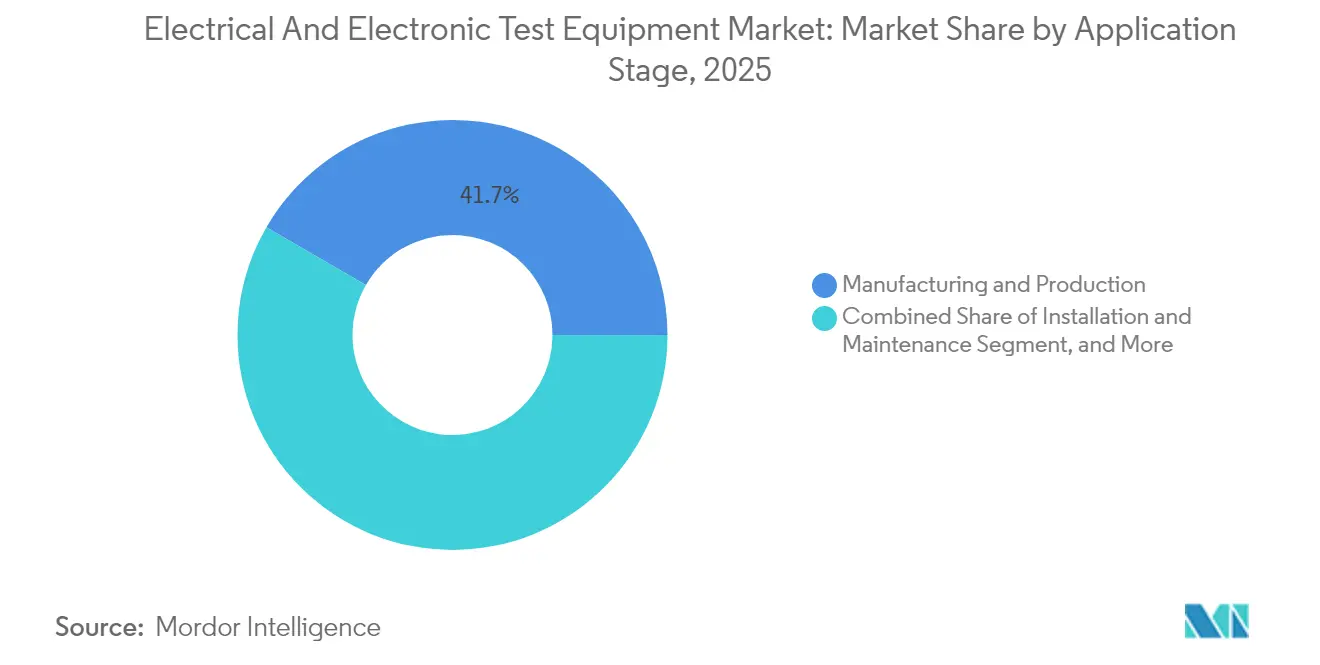

- By application stage, manufacturing and production captured 41.65% share of the electrical and electronic test equipment market size in 2025; certification and compliance testing is advancing at a 4.91% CAGR over 2026-2031.

- By end-user industry, communications and networking commanded 32.24% share in 2025 in the electrical and electronic test equipment market, but automotive and electric-vehicle applications record the highest forecast CAGR at 4.79% to 2031.

- By geography, Asia Pacific led with 39.68% revenue share in 2025 of the electrical and electronic test equipment market, whereas Asia-Pacific is forecast to post a 5.22% CAGR and become the fastest-growing region by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electrical And Electronic Test Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G and Advanced Wireless Deployment Wave | +1.2% | Global, with early gains in North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Advanced-Node Semiconductor Complexity | +0.9% | Global, concentrated in Taiwan, South Korea, United States | Long term (≥ 4 years) |

| EV and Power-Electronics Test Needs | +0.8% | Global, with acceleration in Europe, China, North America | Medium term (2-4 years) |

| AI/ML-Assisted Automated Testing | +0.6% | North America and EU, spill-over to APAC core | Long term (≥ 4 years) |

| Ultra-Wide-Bandgap Device Characterization | +0.4% | North America, Europe, Japan | Long term (≥ 4 years) |

| IoT Cyber-Security Compliance Mandates | +0.3% | Global, with regulatory leadership in EU, UK | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

5G and Advanced Wireless Deployment Wave

Global 5G infrastructure expansion is driving unprecedented demand for millimeter-wave and sub-6 GHz analyzers, generators and over-the-air chambers. Operators need to validate beamforming, carrier aggregation and satellite backhaul performance across increasingly crowded spectrum allocations.[1]Rohde & Schwarz, “ATS800R Compact Antenna Test Range,” rohde-schwarz.com Equipment must now simulate Doppler effects, GNSS timing and non-terrestrial network latency, tasks that conventional terrestrial RF sets cannot handle. Vendors are launching compact CATR ranges that shrink required floor space while retaining quiet-zone fidelity, a key need for consumer-device makers. Demand also flows from private-network deployments in manufacturing plants and logistics hubs, where spectral coexistence and ultra-reliability place fresh verification burdens on test labs. These factors collectively sustain momentum for the electrical and electronic test equipment market as wireless standards evolve toward 5G-Advanced and early 6G research.

Advanced-Node Semiconductor Complexity

Fabricating 3 nm and finer nodes multiplies test vectors as chipmakers adopt multi-die packaging and chiplet architectures. Industry association SEMI forecasts USD 6.7 billion in semiconductor test-equipment sales for 2024, with a 30.3% lift expected in 2025 as device complexity rises.[2]SEMI, “Global Semiconductor Equipment Sales Forecast,” semi.org Teradyne and partners now probe both sides of silicon-photonics wafers in one pass, slashing cycle times for co-packaged optics. High-bandwidth memory stacks, AI accelerators and on-package transceivers require tight thermal control and multi-gigabit interface coverage, pushing legacy ATE beyond its limits. Probe-card vendors FormFactor and Technoprobe have gained strategic investment from Advantest to secure next-gen contactor supply. The rising capital spend underpins long-term growth for the electrical and electronic test equipment market by widening addressable workloads.

EV and Power-Electronics Test Needs

Electric-vehicle adoption accelerates demand for bidirectional sources and regenerative loads that handle 800 V architectures, silicon-carbide inverters, and grid-tied chargers. National Instruments offers scalable systems up to 2.4 MW with 95% energy efficiency for battery-pack and powertrain validation.[3]National Instruments, “High-Power EV Test Platforms,” ni.com Tektronix highlights probing challenges at 100 kHz switching frequencies, where parasitics distort loss measurements. Vehicle-to-grid integration and wireless transfer introduce compliance checkpoints for EMC, safety, and grid codes, widening the test envelope. Chroma ATE covers the full EV chain from battery emulators to propulsion dynos, illustrating the breadth of opportunities for the electrical and electronic test equipment market. Growth remains robust as automakers scale volume production of electrified platforms worldwide.

AI/ML-Assisted Automated Testing

Machine-learning algorithms are turning instruments into predictive systems that cut cycle times and flag anomalies before yield losses occur. Vendors embed AI routines that auto-calibrate setups, optimize test sequences and schedule proactive maintenance, extending asset life while lowering total cost of ownership. Software-defined architectures pool data from oscilloscopes, sources and analyzers to feed neural networks that learn optimal parameter windows. Early adopters report double-digit test-time reductions, a persuasive benefit as factories chase higher throughput for high-mix electronics. The shift requires robust compute back-ends and secure data pipelines, prompting alliances between instrument makers and cloud-AI providers. These developments elevate the electrical and electronic test equipment market by adding software value streams atop traditional hardware revenues.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost and Shift to Rentals | -0.7% | Global, with acute impact in cost-sensitive markets | Short term (≤ 2 years) |

| Low-Cost Asian Vendor Price Pressure | -0.5% | Global, with concentration in price-sensitive segments | Medium term (2-4 years) |

| Precision-Component Supply Shortages | -0.3% | Global, with severe impact in North America and Europe | Short term (≤ 2 years) |

| Right-to-Repair Curtailing Proprietary Protocols | -0.2% | North America and EU, regulatory spill-over to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost and Shift to Rentals

Flagship 5G or semiconductor ATE platforms can exceed USD 1 million apiece, straining capex budgets. Customers increasingly choose rental or subscription models; Electro Rent maintains USD 1.2 billion of inventory to meet these needs. The U.S. Equipment Leasing and Finance Association projects that 54% of equipment acquisitions will be financed in 2024 and expects Equipment-as-a-Service to grow 50% CAGR through 2030. While recurring revenue benefits vendors long term, near-term hardware sales flatten, tempering overall expansion of the electrical and electronic test equipment market.

Low-Cost Asian Vendor Price Pressure

Brands such as GW Instek and Rigol Technologies offer oscilloscopes, spectrum analyzers and DC supplies at price points well below incumbent rivals, leveraging high-volume component sourcing and localized production. With component obsolescence cycles now as short as two years, agile redesign and fast tool changeovers give emerging suppliers a foothold. This pressure erodes average selling prices in entry-level segments, subtly diluting revenue growth for the electrical and electronic test equipment market even as unit demand holds firm.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: RF Equipment Drives Innovation

The electrical and electronic test equipment market size for oscilloscopes stood at USD 4.61 billion in 2025, translating to a dominant 29.45% slice of total revenue. Oscilloscopes remain indispensable across R&D, validation, and troubleshooting, yet bandwidth ceilings and protocol-decode depth are now differentiators as designs push beyond 70 GHz. RF and microwave instruments are expanding at a 4.63% CAGR thanks to 5G non-terrestrial networks, satellite IoT, and automotive radar. Spectrum analyzers with real-time triggers and signal generators capable of 2 GHz modulation bandwidth are moving from lab to field use. Portable vector-network analyzers such as the 40 GHz USB-powered VNA400 are proof that miniaturization no longer compromises performance.

Semiconductor ATE faces cyclical buying tied to fab expansions but benefits from chiplet architectures that raise pin counts and drive multisite test. Environmental-stress chambers and electrical-safety testers are getting a lift from stricter IEC and UL updates, especially in battery-powered consumer devices. Optical-electrical convergence is spawning hybrid testers that measure insertion loss, eye diagrams, and RF impairments in a single workflow, meeting data-center demand for co-packaged optics. Overall, product diversification underpins revenue stability for the electrical and electronic test equipment market despite pockets of volatility.

By Form Factor: Modular Systems Gain Momentum

Benchtop platforms deliver benchmark accuracy, intuitive front panels and robust input protection, securing 47.12% of 2025 revenue. They dominate early-stage design and university labs, where flexibility outranks rack density. Modular PXI systems, however, are climbing fastest with a 5.02% CAGR as users favor synchronized, software-defined channels for parallel test. The electrical and electronic test equipment market size attributed to PXI setups is forecast to exceed USD 5.18 billion by 2031 as factories digitize quality stations and shorten changeover cycles.

NI counts more than 600 PXI modules under its brand and 1,500 across the broader ecosystem, giving engineers a Lego-like palette of RF, mixed-signal, and power cards. ADLINK extends reach into mass-production lines with PXI-based parametric testers that rival proprietary rack systems on throughput. Handheld analyzers fill gap-filling tasks in field service, renewable-energy farms, and telecom tower audits, now featuring cloud dashboards for instant report generation. This convergence of form factors sustains healthy competition inside the electrical and electronic test equipment market.

By Application Stage: Compliance Testing Accelerates

Manufacturing and production stations represented 41.65% of 2025 spending, supported by rising automation and inline analytics that curb rework costs. Certification and compliance test outpaces other stages at a projected 4.91% CAGR, a result of new cybersecurity clauses in EU radio regulations and evolving EMC limits for high-power chargers. Test houses broaden scope beyond traditional electrical parameters to include code analysis and over-the-air performance, increasing equipment turnover.

Design and R&D remains the creativity engine for the electrical and electronic test equipment market, accounting for roughly one quarter of annual sales. Toolchains that link simulation with live measurement, sometimes called “model-based test”, deliver tighter design loops and spur upgrades to higher-bandwidth scopes and logic analyzers. Installation and maintenance demand is rebounding with 5G small-cell densification and solar-farm scale-out, fueling purchases of compact spectrum scopes, I-V curve tracers and fiber inspection probes.

By End-User Industry: Automotive Transformation Leads

Communications networks still top the buyer list with 32.24% of expenditures in 2025, covering macro-base-station rollout, data-center backbone upgrades and satellite ground-segment expansion. Yet automotive and electric-vehicle makers will post a 4.79% CAGR through 2031, reflecting rising sensor fusion, EV drivetrain validation and embedded cybersecurity audits. The electrical and electronic test equipment market finds new ground in battery test rigs, LiDAR calibration benches and functional safety verification across zonal architectures.

Semiconductor foundries and outsourced assembly-test providers remain heavy investors as AI accelerators, high-bandwidth memory and advanced packaging raise defect-detection benchmarks. Aerospace and defense budgets are climbing for electronic-warfare, phased-array radar and space-payload test. Industrial automation and smart-grid upgrades require power analyzers and protocol gateways able to coexist with legacy SCADA fields, spreading demand beyond electronics OEMs into process-industry players.

Geography Analysis

North America generated significant share on the back of defense R&D, fab expansions in Arizona and 5G C-band build-outs. Federal incentives and accredited calibration labs sustain a mature ecosystem that values traceability and rapid service. Canadian telecom carriers and electric-vehicle startups add incremental demand for compliance services.

Asia-Pacific is on track for a 5.22% CAGR and will likely approach parity with North America by 2031. China’s push for indigenous semiconductors, Taiwan’s leadership in advanced nodes and South Korean investments in memory assist volume growth. Southeast Asian nations provide a manufacturing off-load valve, creating greenfield opportunities for mid-range oscilloscopes and PXI racks. Indian telcos embracing Open RAN and Japanese automakers validating solid-state batteries add diverse revenue streams to the electrical and electronic test equipment market.

Europe shows moderate but stable growth as automotive electrification, renewable-energy targets, and digital-sovereignty initiatives keep capex flowing. Germany and France host significant calibration and rental operations, while Nordic nations pioneer 5G advanced field trials. Eastern European EMS providers attract near-shoring contracts, bolstering demand for entry-level but network-connected instruments. South America and the Middle East and Africa remain nascent yet promising, with mining automation, utility-scale solar, and airport upgrades enabling first-time installations of modular test benches.

Competitive Landscape

The electrical and electronic test equipment industry features moderate consolidation, with top vendors expanding portfolios through acquisition and partnerships. Keysight’s USD 1.46 billion purchase of Spirent broadens its automated cloud and SD-WAN test-suite reach. Anritsu’s plan to acquire DEWETRON adds high-precision power analysis for EV propulsion systems. These moves exemplify a shift toward end-to-end platforms that blend hardware, software and managed services, creating switching costs that lock in customers.

Smaller specialists thrive in niches such as quantum-computer qubit readout, high-speed coherent optics and EMC rental fleets. Partnerships like Teradyne’s team-up with Infineon on wide-bandgap power devices illustrate how OEMs and equipment makers co-innovate when single-party solutions fall short. Cost-competitive challengers from Taiwan and mainland China keep entry-level price points low, encouraging incumbents to migrate value toward analytics and AI-powered automation.

Service infrastructure is another battleground; calibration chain Trescal added 15 facilities across five continents during 2024. Vendors now bundle remote-monitor dashboards, predictive-maintenance alerts and cloud-based firmware updates, turning instrumentation into connected assets. Compliance with ISO 17025, ANSI Z540.3 and IEC-60529 remains a barrier to new entrants, favoring incumbents with accredited, multi-country labs.

Electrical And Electronic Test Equipment Industry Leaders

Fortive Corporation

Keysight Technologies Inc.

Rohde & Schwarz GmbH & Co. KG

National Instruments Corporation

Anritsu Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Anritsu agreed to acquire DEWETRON to expand precision power-measurement solutions for EV and renewable-energy applications.

- March 2025: Teradyne launched the first production-ready double-sided wafer probe test cell for silicon photonics in partnership with ficonTEC.

- February 2025: Teradyne and Infineon formed a power-semiconductor test partnership and transferred 80 Infineon ATE engineers to Teradyne.

- January 2025: Advantest invested in FormFactor and Technoprobe, acquiring minority stakes to secure probe-card supply for advanced nodes

Global Electrical And Electronic Test Equipment Market Report Scope

Electrical and electronic test equipment includes a wide range of tools and instruments used to measure, diagnose, test, and troubleshoot electrical and electronic systems and devices. They are used to measure electrical parameters such as voltage, current, resistance, capacitance, and frequency.

The electrical and electronic test equipment market is segmented by type (semiconductor automatic test equipment (ATE), radio frequency (RF) test equipment, digital test equipment, electrical and environmental test, and data acquisition (DAQ)), end-user industry (communications, semiconductors and computing, aerospace and defense, consumer electronics, electric vehicles (EVS), and other end-user industries), and geography (North America, Europe, Asia-Pacific, Latin America, and the Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Oscilloscopes |

| Spectrum and Network Analyzers |

| Signal Generators |

| Semiconductor Automatic Test Equipment (ATE) |

| RF and Microwave Test Equipment |

| Data Acquisition (DAQ) Systems |

| Electrical and Environmental Safety Test |

| Benchtop |

| Portable / Hand-held |

| Modular / PXI / PC-based |

| Design and R&D |

| Manufacturing and Production |

| Installation and Maintenance |

| Certification and Compliance |

| Communications and Networking |

| Semiconductors and Computing |

| Automotive and Electric Vehicles |

| Aerospace and Defense |

| Consumer Electronics and Appliances |

| Industrial and Energy |

| Healthcare and Life Sciences |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product Type | Oscilloscopes | ||

| Spectrum and Network Analyzers | |||

| Signal Generators | |||

| Semiconductor Automatic Test Equipment (ATE) | |||

| RF and Microwave Test Equipment | |||

| Data Acquisition (DAQ) Systems | |||

| Electrical and Environmental Safety Test | |||

| By Form Factor | Benchtop | ||

| Portable / Hand-held | |||

| Modular / PXI / PC-based | |||

| By Application Stage | Design and R&D | ||

| Manufacturing and Production | |||

| Installation and Maintenance | |||

| Certification and Compliance | |||

| By End-user Industry | Communications and Networking | ||

| Semiconductors and Computing | |||

| Automotive and Electric Vehicles | |||

| Aerospace and Defense | |||

| Consumer Electronics and Appliances | |||

| Industrial and Energy | |||

| Healthcare and Life Sciences | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the electrical and electronic test equipment market in 2026?

The electrical and electronic test equipment market size stands at USD 16.31 billion in 2026.

What is the expected growth rate through 2031?

The market is forecast to expand at a 4.12% CAGR, reaching USD 19.95 billion by 2031.

Which product segment shows the fastest growth?

RF and microwave test equipment is projected to grow at 4.63% CAGR through 2031 due to 5G, satellite and radar demand.

Why is Asia-Pacific considered the growth engine?

Manufacturing capacity expansions, regional semiconductor investments and supportive government initiatives together drive a 5.22% CAGR in Asia-Pacific.

How are rental models affecting equipment vendors?

Rising rental and subscription adoption smooths long-term revenues but can dampen near-term hardware sales, trimming approximately 0.7% from forecast CAGR.

Page last updated on: