Electrical Test Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 17.31 Billion |

| Market Size (2031) | USD 23.15 Billion |

| Growth Rate (2026 - 2031) | 5.99% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

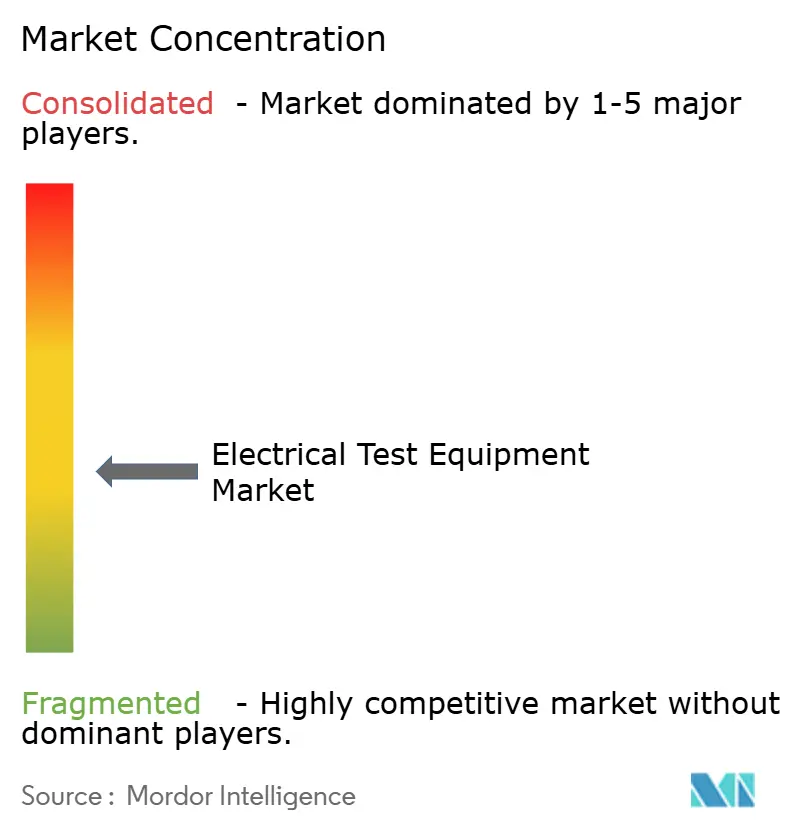

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electrical Test Equipment Market Analysis by Mordor Intelligence

The electrical test equipment market size was USD 17.31 billion in 2026 and is projected to reach USD 23.15 billion by 2031, registering a 5.99% CAGR. Across the electrical test equipment market, portable instruments, regenerative loads, and connected analyzers remain the growth engines as utilities, manufacturers, and service providers modernize field workflows and digitize laboratories. Demand concentrates in battery-energy-storage commissioning, semiconductor fabrication, and 5G network roll-outs, all of which require high-bandwidth, safety-compliant instruments that shorten validation cycles. Vendors capable of combining hardware accuracy with cloud analytics, cybersecurity controls, and energy-recovery features increasingly shape competitive strategy, while regulatory mandates such as IEC 61010-1 Edition 4.0 and IEC 62443 amplify replacement cycles. Pricing pressure persists at the lower end of the electrical test equipment market as Chinese suppliers undercut premium brands, yet mid- and high-performance tiers defend margins by layering software subscriptions and calibration services.

Key Report Takeaways

- By equipment mobility, portable instruments commanded 61.73% of the electrical test equipment market share in 2025, and the category is forecast to expand at a 7.12% CAGR through 2031.

- By product category, multimeters and clamp meters led with 28.74% of the electrical test equipment market size in 2025, while electronic loads post the fastest 6.33% CAGR to 2031.

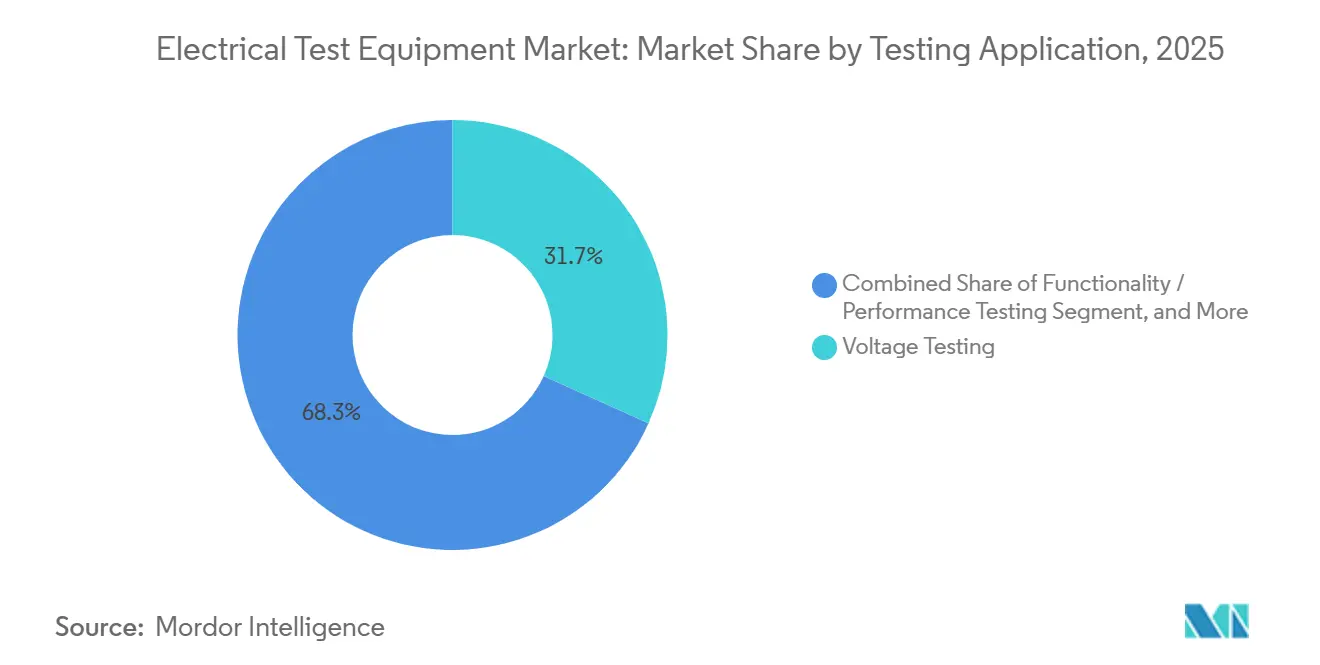

- By testing application, voltage testing held 31.74% share in 2025 of the electrical test equipment market, whereas preventive maintenance and condition monitoring are projected to register a 6.66% CAGR to 2031.

- By industry application, energy and power captured 41.82% revenue share in 2025 of the electrical test equipment market, while automotive and e-mobility is the quickest-growing vertical at a 6.77% CAGR through 2031.

- By geography, North America retained 38.73% share in 2025 of the electrical test equipment market, but Asia-Pacific is poised for the highest 6.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electrical Test Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter global electrical-safety regulations | +1.2% | Global, with early enforcement in EU and North America | Medium term (2-4 years) |

| Expansion of renewable-energy installations | +1.5% | Global, concentrated in APAC, North America, and Europe | Long term (≥ 4 years) |

| Proliferation of 5G and high-speed networks | +1.1% | Global, led by APAC and North America | Medium term (2-4 years) |

| Rising EV adoption and battery-test demand | +1.3% | Global, with highest growth in APAC and Europe | Long term (≥ 4 years) |

| Predictive-maintenance-as-a-service uptake | +0.6% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Demand for energy-regenerative loads | +0.4% | Global, early adoption in automotive and energy sectors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stricter Global Electrical-Safety Regulations

Regulators worldwide are increasing insulation-coordination thresholds and incorporating cybersecurity checks into electrical safety protocols, compelling both manufacturers and end-users to update their instrument fleets. IEC 61010-1 Edition 4.0, effective January 2024, increased clearance and creepage distances for equipment above 1 000 V, leading vendors to redesign enclosures and customers to recalibrate installed bases.[1]International Electrotechnical Commission, “IEC 61010-1 Edition 4.0 Safety Requirements,” IEC.ch In the United States, UL 9540A now mandates multi-level thermal-runaway validation for battery-energy storage systems, resulting in a threefold increase in tester utilization rates during certification. The European Union amended the Low Voltage Directive to require IEC 62443 component security attestations, tying dielectric tests to cybersecurity audits. Replacement demand is acute in data-center and pharmaceutical facilities where downtime penalties outweigh instrument cost. Consequently, portable safety analyzers with ruggedized housings and secure firmware record double-digit shipment growth.

Expansion of Renewable-Energy Installations

Utility-scale solar, wind, and co-located battery assets multiply grid-edge test points that need harmonic, power-quality, and insulation verification. The U.S. Department of Energy’s Grid Resilience and Innovation Partnerships program earmarked USD 3.46 billion for transmission upgrades that specify analyzers able to capture sub-cycle voltage sags through the 50th harmonic.[2]U.S. Department of Energy, “Grid Resilience and Innovation Partnerships Program,” Energy.gov North Sea offshore wind farms deploy 525 kV HVDC links, requiring insulation testers such as Megger’s IDAX 350 for on-board converter-station cables. China’s GB/T 36547-2024 forces every grid-storage site above 10 MWh to complete standardized performance tests, boosting bids for domestic regenerative loads. These policies drive sustained investment in high-voltage, high-precision portable instruments across the electrical test equipment market.

Proliferation of 5G and High-Speed Networks

3GPP Release 18 pushes test frequencies to 71 GHz, outpacing legacy protocol analyzers. Keysight’s UXM 5G Wireless Test Platform combines over-the-air and conducted modes in one chassis, cutting radio-validation rack space in half.[3]Keysight Technologies, “Company Overview and Product Portfolio,” Keysight.com Open RAN architectures fragment suppliers, prompting operators to acquire interoperability test suites, as evidenced by Viavi’s 31% jump in O-RAN license sales during 2024. Fiber backhaul expansion shifts optical time-domain reflectometers from labs to field kits, and shortages of certified fiber technicians increase demand for simplified, automated instruments. Together, these factors continue to lift the electrical test equipment market in telecom verticals.

Rising EV Adoption and Battery-Test Demand

Fast-charging above 350 kW and the advent of solid-state chemistries intensify validation workloads in automotive labs. ISO/SAE 12906:2024 mandates cycle-life testing across -40 °C to +50 °C ambient conditions, which require combined thermal chambers and high-current cyclers. Chroma’s Model 17040 regenerative tester recovers up to 90% discharge energy, saving large battery lines USD 120 000 annually in electricity costs. China’s revised GB/T 31467-2023 adds fast-charge durability clauses, driving domestic orders for Itech and Rigol systems. These pressures sustain the fastest CAGR contribution within the electrical test equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition cost of instruments | -0.8% | Global, acute in emerging markets | Medium term (2-4 years) |

| Rapid technology-driven obsolescence | -0.6% | Global, especially in high-frequency and digital domains | Short term (≤ 2 years) |

| Shortage of skilled metrology technicians | -0.4% | North America and Europe, emerging in APAC | Long term (≥ 4 years) |

| Cyber-security risks in connected devices | -0.3% | Global, critical in regulated industries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Acquisition Cost of Instruments

Ten-gigahertz oscilloscopes priced above USD 100 000 remain out of reach for many regional labs, slowing modernization in Southeast Asia and South America. Vendors experiment with lower-spec models such as Tektronix’s MSO 2 Series at USD 1 200, yet 200 MHz bandwidth confines usage to consumer-electronics repair. Operating leases now constitute 34% of PXI orders at Emerson Test and Measurement, transferring obsolescence risk from buyers to suppliers. Nevertheless, tariffs like India’s 20% basic customs duty still inflate landed cost on premium analyzers. Budget constraints therefore lengthen mixed-fleet lifecycles, limiting near-term electrical test equipment market upgrades.

Rapid Technology-Driven Obsolescence

Millimeter-wave adoption, software-defined radios, and evolving cybersecurity baselines shorten effective product life. Customers hesitate to purchase when a new protocol or frequency band could arrive within two years, dampening capital-spending cycles. Mid-power signal generators introduced pre-2024 already lack Release 18 capabilities, compelling owner labs to weigh retrofit boards against full replacement. Subscription-based firmware updates mitigate some risk but do not solve inherent analog-front-end limitations. Consequently, obsolescence concerns shave growth potential off the electrical test equipment market, especially in bandwidth-driven categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Mobility: Portable Instruments Extend Field Reach

Portable assets represented 61.73% of the electrical test equipment market share in 2025. The segment is projected to deliver a 7.12% CAGR through 2031, as utilities, contractors, and renewable-energy installers prefer battery-powered devices that eliminate the need for de-energizing circuits during commissioning. Fluke’s 4.2 kg Norma 6000 power analyzer exemplifies laboratory-grade precision on the job site, while Rohde and Schwarz’s eight-hour handheld oscilloscope gains traction in automotive service bays. Stationary gear maintains relevance in semiconductor fabs where environmental control is paramount, but ruggedized housings and IEC 61010-1 drop-test compliance broaden portable use cases.

The portable wave drives accessory ecosystem includes wireless probes, cloud dashboards, and edge-AISafety features that integrate seamlessly with enterprise asset-management software. As a result, procurement frameworks are increasingly assessing total connectivity and cybersecurity, rather than raw accuracy. With average selling prices falling 8% in 2024 due to Chinese competition, premium brands are bundling calibration vouchers and firmware unlock codes to protect their margins, thereby sustaining differentiation in the electrical test equipment market.

By Product Category: Electronic Loads Outpace Legacy Staples

Multimeters and clamp meters delivered 28.74% of 2025 revenue but face price erosion from low-cost entrants. Conversely, regenerative electronic loads, though smaller in absolute terms, are projected to register a 6.33% CAGR, the fastest among all categories. EA Elektro-Automatik’s 96% energy-recovery models helped one European battery lab cut annual consumption by 1.2 GWh annually. Oscilloscopes polarize, with sub-USD 2 000 instruments winning education and repair markets and USD 50 000 mixed-signal editions anchoring aerospace programs.

Power analyzers see renewed demand as silicon-carbide drives penetrate HVAC and industrial automation, while safety testers commoditize as users stretch calibration to 18-month intervals. Battery-specific testers surge in demand for EVs and grid storage, and software-defined waveform generators based on PXI or FPGA platforms replace aging analog units. These shifts illustrate how efficiency, modularity, and software extensibility shape purchasing in the electrical test equipment market.

By Testing Application: Predictive Analytics Gain Momentum

Voltage verification remained the baseline at 31.74% share in 2025, yet preventive maintenance and condition monitoring are forecast to expand at 6.66% CAGR as plants seek data-driven uptime. Edge-enabled power-quality recorders that transmit only exception events reduce bandwidth by up to 85%, a decisive factor for oil-and-gas facilities. Automated test equipment in semiconductor lines sustains high volumes, processing more than 10 000 devices per hour.

In renewable-energy commissioning, IEEE 1547.1 certified analyzers speed site acceptance, while compliance testing in automotive and medical devices leans on turnkey service bundles that combine hardware with calibration certificates. Extended warranties and three-year calibration guarantees lower total cost of ownership, furthering adoption. Together, these dynamics reinforce the analytics-first mindset permeating the electrical test equipment market.

By Industry Application: Mobility Electrification Leads Growth

Energy and power still captured the largest slice at 41.82% in 2025 due to grid-scale storage and inverter validation. However, automotive and e-mobility are projected to chart a 6.77% CAGR through 2031, reflecting fast-charge, solid-state, and battery-management-system test needs. Regenerative cyclers enable throughput gains, while impedance spectroscopy across micro-hertz bands characterizes lithium-metal interfaces.

Aerospace and defense retain premium margins given MIL-STD qualification, and manufacturing automation uses power analyzers to debug variable-frequency drives. Consumer electronics tests commoditize, and intrinsics-safe instruments dominate oil-and-gas maintenance. Telecommunication tower upgrades demand handheld spectrum and vector analyzers, and academic labs leverage discounted leasing programs. Collectively, these verticals dictate the investment cadence inside the electrical test equipment market.

Geography Analysis

North America held 38.73% of global revenue in 2025, underpinned by USD 3.46 billion in federal transmission upgrades and expanding EV battery labs in Michigan and California. Canada’s 47% surge in grid-scale storage deployments and Mexico’s USD 1 billion EV plant conversion sustain additional momentum.

Europe’s accelerated energy transition propels investment in power-quality and insulation-diagnostic tools. Germany’s offshore wind expansion, the United Kingdom’s USD 4.3 billion substation upgrades, and France’s nuclear life-extension projects together elevate demand for high-voltage test gear. The European Union’s Battery Regulation reinforces traceable energy-consumption metering, compelling purchase of calibrated analyzers.

Asia-Pacific is forecast to post the strongest 6.65% CAGR to 2031, driven by Taiwan’s USD 65 billion semiconductor capex, South Korea’s memory-chip fab, and China’s storage-testing mandate favoring local suppliers. India’s INR 29.8 billion incentive payouts attract additional electronics factories that procure multimeters and power analyzers, while Japan’s solid-state battery pilots and ASEAN manufacturing relocations amplify regional purchasing. Emerging markets in South America, the Middle East and Africa lag in absolute volumes but register robust project pipelines that require portable safety testers and grid-code analyzers, broadening the electrical test equipment market footprint.

Competitive Landscape

The top five vendors, Keysight Technologies, Rohde and Schwarz, Tektronix, Fluke Corporation, and Emerson Test and Measurement, collectively accounted for about half of 2024 revenue, signaling moderate concentration. Keysight’s USD 1.5 billion acquisition of Spirent’s network-test arm consolidated 5G protocol validation and deepened its software moat. Rohde and Schwarz safeguards gross margins through vertical integration, while Fluke’s high-volume multimeters face price compression from Rigol, Mastech, and UNI-T entrants.

White-space opportunities surface in regenerative electronic loads where EA Elektro-Automatik and NH Research innovate but lack global service coverage, and in cybersecurity-hardened instruments compliant with IEC 62443 where few products exist. Keysight’s PathWave cloud suite exemplifies the pivot toward subscription ecosystems that lock in customers and generate recurring revenue streams.

Chinese challengers such as Itech captured 12% of domestic battery-tester sales by undercutting incumbents by up to 40%, though reliability concerns persist for Tier-1 automotive programs. Partnerships, localized manufacturing, and turnkey calibration packages remain decisive levers as the electrical test equipment market evolves toward software-defined, service-centric models.

Electrical Test Equipment Industry Leaders

Keysight Technologies, Inc.

Rohde and Schwarz GmbH and Co. KG

Tektronix, Inc.

Fluke Corporation

National Instruments Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Keysight Technologies formed a partnership with TSMC to co-develop test solutions for 2 nm nodes at the Arizona fab scheduled for 2026 production.

- November 2025: Rohde and Schwarz launched the RTP oscilloscope family with 16 GHz bandwidth targeting automotive radar and 5G millimeter-wave projects.

- October 2025: Fluke Corporation introduced the 1770 Series three-phase power-quality analyzer featuring IEC 62443-4-2 compliant firmware.

- September 2025: Chroma ATE secured a USD 47 million order from a European automaker for regenerative battery testers supporting solid-state validation.

Global Electrical Test Equipment Market Report Scope

The Electrical Test Equipment Market Report is Segmented by Equipment Mobility (Stationary, Portable), Product Category (Oscilloscopes, Multimeters, Power Analyzers, Safety Testers, Battery Testers, Electronic Loads, Signal Generators, Network Analyzers, Data Acquisition Systems), Testing Application (Voltage, Performance, Commissioning, Maintenance, Compliance, Calibration), Industry Application (Energy, Aerospace, Manufacturing, Automotive, Telecom, Healthcare), and Geography. Market Forecasts are in Value (USD).

| Stationary |

| Portable |

| Oscilloscopes |

| Multimeters and Clamp Meters |

| Power Analyzers |

| Electrical Safety Testers |

| Battery Testing Equipment |

| High-Voltage Testers |

| Electronic Loads |

| Signal and Function Generators |

| Network and Protocol Analyzers |

| Data Acquisition Systems |

| Voltage Testing |

| Functionality / Performance Testing |

| Installation and Commissioning Testing |

| Preventive Maintenance and Condition Monitoring |

| Compliance and Certification Testing |

| Quality Assurance and Lab Calibration |

| Energy and Power |

| Aerospace and Defense |

| Manufacturing and Industrial Automation |

| Consumer Electronics |

| Oil and Gas |

| Automotive and E-Mobility |

| Telecommunications and IT Infrastructure |

| Healthcare and Medical Devices |

| Research and Academics |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Equipment Mobility | Stationary | ||

| Portable | |||

| By Product Category | Oscilloscopes | ||

| Multimeters and Clamp Meters | |||

| Power Analyzers | |||

| Electrical Safety Testers | |||

| Battery Testing Equipment | |||

| High-Voltage Testers | |||

| Electronic Loads | |||

| Signal and Function Generators | |||

| Network and Protocol Analyzers | |||

| Data Acquisition Systems | |||

| By Testing Application | Voltage Testing | ||

| Functionality / Performance Testing | |||

| Installation and Commissioning Testing | |||

| Preventive Maintenance and Condition Monitoring | |||

| Compliance and Certification Testing | |||

| Quality Assurance and Lab Calibration | |||

| By Industry Application | Energy and Power | ||

| Aerospace and Defense | |||

| Manufacturing and Industrial Automation | |||

| Consumer Electronics | |||

| Oil and Gas | |||

| Automotive and E-Mobility | |||

| Telecommunications and IT Infrastructure | |||

| Healthcare and Medical Devices | |||

| Research and Academics | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the electrical test equipment market size today and its forecast value in 2031?

The market stood at USD 17.31 billion in 2026 and is projected to reach USD 23.15 billion by 2031 on a 5.99% CAGR trajectory.

Which product category is growing the fastest among test instruments?

Regenerative electronic loads lead growth, posting a 6.33% CAGR as battery-validation labs recapture up to 90% of discharge energy and cut utility costs.

Why are portable instruments prioritized in new procurement plans?

They already hold 61.73% share and will grow at 7.12% CAGR because field crews can complete commissioning without de-energizing assets or hauling units to a lab.

How do recent safety regulations affect capital budgets for test gear?

IEC 61010-1 Edition 4.0 and UL 9540A mandate redesigned housings and longer battery-storage fire tests, triggering accelerated replacement cycles and higher compliance spending.

Which geography is expected to deliver the highest growth through 2031?

Asia-Pacific is forecast to expand at a 6.65% CAGR due to semiconductor fab builds, EV battery plants, and government incentive schemes.

Page last updated on: