Embossing And Foil Stamping Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.39 Billion |

| Market Size (2030) | USD 7.51 Billion |

| Growth Rate (2025 - 2030) | 6.86% CAGR |

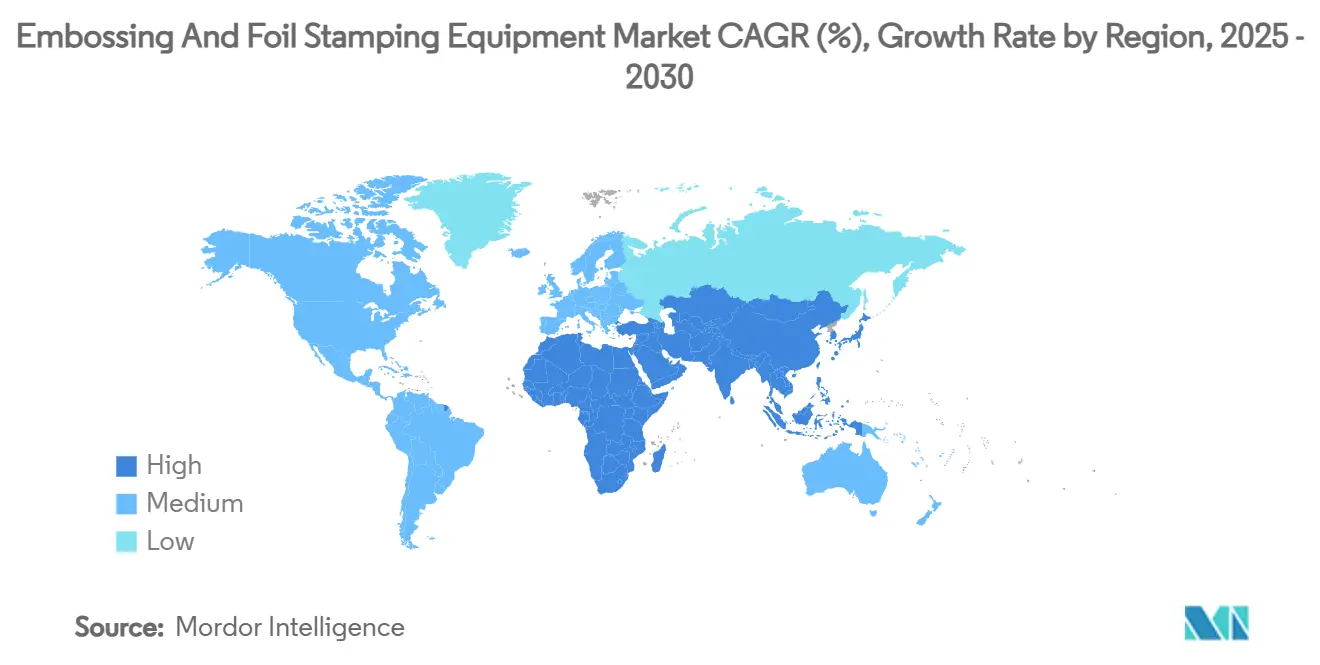

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

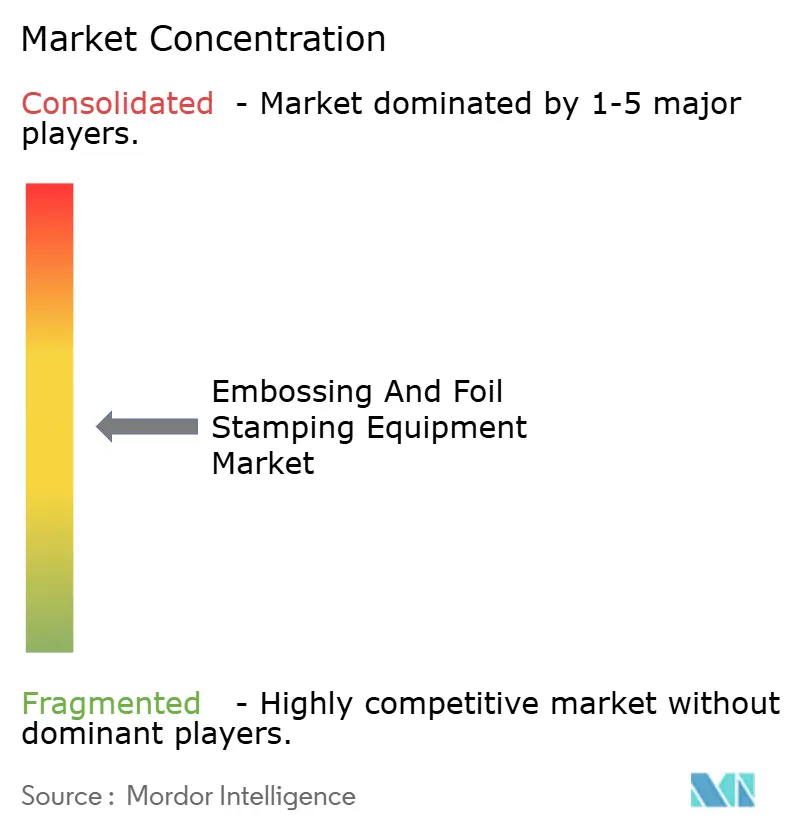

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Embossing And Foil Stamping Equipment Market Analysis by Mordor Intelligence

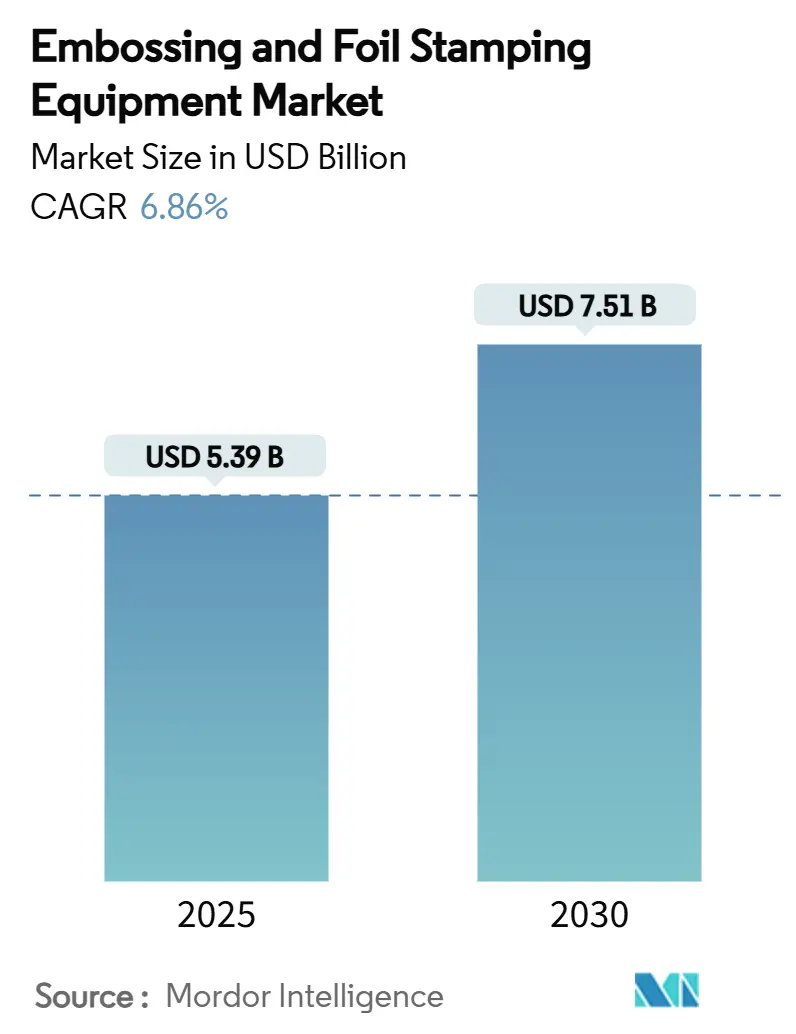

The Embossing And Foil Stamping Equipment Market size is estimated at USD 5.39 billion in 2025, and is expected to reach USD 7.51 billion by 2030, at a CAGR of 6.86% during the forecast period (2025-2030).

Demand accelerates as brand owners turn to premium finishing for shelf appeal, while anti-counterfeiting rules expand security applications. Hot-foil systems keep a broad installed base in high-volume packaging, yet digital embellishment platforms gain ground where short runs and variable data matter. Equipment vendors push modular automation to offset labor shortages and to align with sustainability mandates that favor cold-foil processes. Rapid adoption in Asia-Pacific underpins global volume as regional governments back advanced manufacturing to lift economic output.

Key Report Takeaways

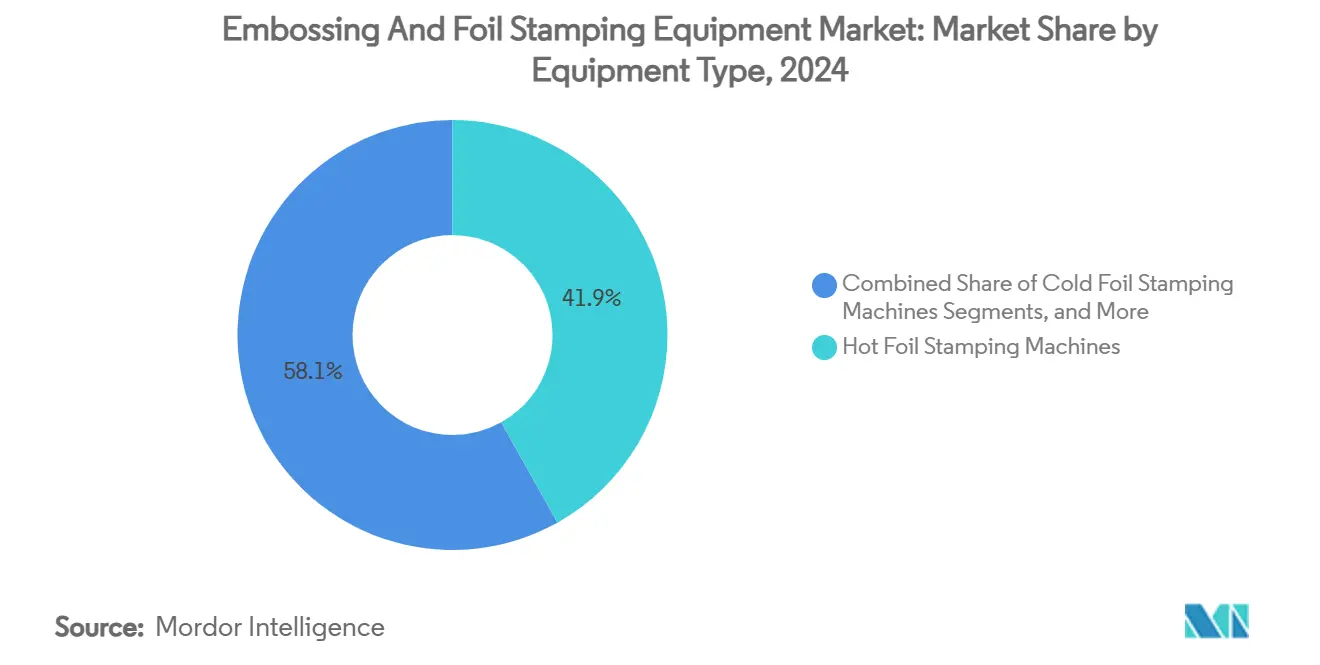

- By equipment type, hot-foil stamping machines led with 41.89% of the embossing and foil stamping equipment market share in 2024.

- By operation mode, the fully automatic category records the highest forecast CAGR at 8.21% to 2030.

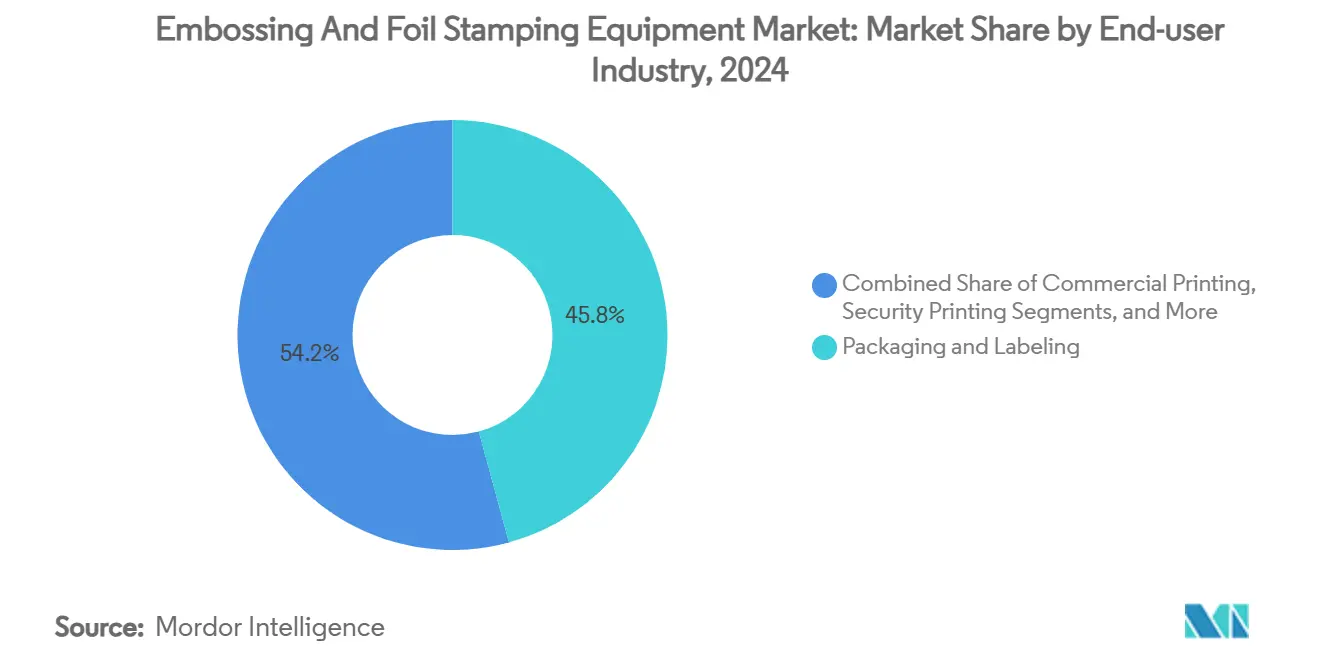

- By end-user industry, packaging and labeling accounted for 45.76% of the embossing and foil stamping equipment market size in 2024.

- By geography, Asia-Pacific commanded 37.18% of the embossing and foil stamping equipment market in 2024.

Global Embossing And Foil Stamping Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in premium packaging demand | 1.8% | Global, with concentration in North America & EU luxury markets | Medium term (2-4 years) |

| Growth of craft–e-commerce personalization | 1.2% | North America & EU core, expanding to APAC urban centers | Short term (≤ 2 years) |

| Sustainable cold-foil process adoption | 0.9% | EU regulatory-driven, spreading to North America & APAC | Long term (≥ 4 years) |

| Expansion of digital inline embellishment | 1.4% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| APAC printing & packaging capacity boom | 1.1% | APAC core, with spill-over effects to Middle East & Africa | Short term (≤ 2 years) |

| Anti-counterfeit holographic security uptake | 0.7% | Global, with priority in pharmaceutical & luxury goods markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium packaging demand surge

Greater use of luxury finishing has shifted procurement toward integrated systems that combine embossing, hot-foil and cold-foil in one pass. Heidelberg reports more than 50% of total turnover now tied to packaging solutions as the global packaging market expanded 60% in the past decade[1]Heidelberger Druckmaschinen AG, “Annual Report 2025,” heidelberg.com. Brands outside the luxury tier adopt similar embellishment to win shelf differentiation, extending growth beyond traditional high-price categories. Paper-based formats accelerate the trend, since converters need versatile lines able to treat coated board, recycled fiber and specialty papers without quality loss. Vendors respond with wide-substrate platforms and faster changeover tooling.

Craft-e-commerce personalization growth

Online sellers of craft and promotional items generate short-run jobs that favor semi-automatic and digital systems. Manufacturing sales of CAD 71.9 billion in March 2025, with an 11.9% rise in furniture and related products, illustrate how small-batch producers upgrade finishing lines[2]Statistics Canada, “Monthly Survey of Manufacturing, March 2025,” statcan.gc.ca. Digital foil stamping equipment, supported by 8.13% CAGR, addresses the need for variable names, color swaps and same-day dispatch. As unboxing videos shape consumer expectations, mainstream brands mimic the craft aesthetic with highly personalized secondary packaging, reinforcing demand for quick-setup embellishment machinery.

Sustainable cold-foil process uptake

Circular-economy policies within the EU push converters toward cold-foil because it eliminates heat, lowers energy draw and simplifies metallic separation during recycling. The bloc’s advanced manufacturing sector climbed from 1,900 firms in 2009 to 4,500 in 2023, showing a fertile base to adopt greener lines[3]European Commission Joint Research Centre, “Advanced Manufacturing in Europe 2024,” ec.europa.eu. North American and Asian converters follow, driven by brand pledges to cut carbon intensity. Equipment makers invest in chilled-cure adhesives, LED curing stations and waste-foil collection modules to align with these rules while preserving gloss levels demanded by cosmetics and premium spirits clients.

Digital inline embellishment expansion

Pairing digital print engines with inline foil and emboss stations reduces handling steps, saves pressroom floor space and shortens lead time. Heidelberg’s cooperation with Canon on sheetfed inkjet printing illustrates how suppliers converge to offer turnkey lines that push jobs straight from pre-press to packed cartons[4]Heidelberger Druckmaschinen AG, “Annual Report 2025,” heidelberg.com. Short-run packaging sees strong gains because cost overhead per version falls. Smart sensors and analytic dashboards inside inline platforms let operators tweak nip pressure or foil nip speed in real time, cutting waste and boosting consistency.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of automated systems | -1.3% | Global, with particular impact on emerging markets | Medium term (2-4 years) |

| Metallic-foil recyclability concerns | -0.8% | EU regulatory focus, expanding to North America and APAC | Long term (≥ 4 years) |

| Shortage of skilled die-making operators | -0.6% | Developed markets with aging workforce | Long term (≥ 4 years) |

| Competition from digital spot-UV and varnish | -0.9% | Global, with faster adoption in commercial printing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High capital cost of automated systems

The up-front price of a fully automatic embossing line can be triple that of manual gear, discouraging upgrades in smaller converters. Bobst noted a 24% fall in printing and converting order entries in H1 2024 as clients postponed investment amid macro uncertainty[5]Bobst Group SA, “Half-Year Report 2024,” bobst.com. Tiered finance packages and equipment-as-a-service models are emerging, yet adoption lags behind other capital goods. Vendors now design modular frames that let buyers bolt on automatic feeders, stackers or inspection cameras over time, easing cash-flow barriers.

Metallic-foil recyclability concerns

Regulators scrutinize the end-of-life impact of laminated substrates. Although cold-foil improves fiber recovery, legislators in the EU are drafting stricter disposal rules that could add compliance costs. Brand owners therefore weigh spot-UV, varnish or digital effects that use less metal. Suppliers compete by launching ultrathin foil gauges and water-based release coats to reassure eco-certification bodies. These technical tweaks slow but do not stop demand, as luxury sectors still view genuine metallic sheen as irreplaceable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Digital platforms accelerate while hot-foil keeps core volume

Hot-foil stamping machines retained 41.89% share of the embossing and foil stamping equipment market in 2024, underpinned by reliability in high-speed folding-carton lines. The segment’s installed base supports consistent consumables supply and trained operators. Digital foil stamping units, helped by cloud-based job management and rapid plate-free changeovers, post an 8.13% CAGR and continue to outpace legacy gear. Cold-foil modules appeal to converters that need recyclability assurances; embossing presses serve both luxury cartons and security documents. Combination lines that merge foil, emboss and die-cut functions enhance floor-space efficiency and answer converter calls for single-pass workflows.

Growing customization and substrate-mix requirements steer investment toward configurable systems. DuPont’s USD 70 million 2023 electronics and industrial expansion signals broader manufacturing shifts that favor integrated machinery capable of switching between rigid and flexible materials. Equipment makers differentiate through servo-driven registration, adaptive heat-management and AI-based make-ready tools. Overall, the embossing and foil stamping equipment market size tied to digital and hybrid platforms is projected to widen its slice as converters standardize on data-rich production planning.

By Operation Mode: Automation delivers productivity gains

Semi-automatic lines captured 35.73% of embossing and foil stamping equipment market revenue in 2024 by balancing labor flexibility and unit cost. They fit converters handling multiple SKUs with moderate run lengths. Fully automatic machines, supported by an 8.21% CAGR, draw demand wherever high throughput or 24 hour shifts are common. Japan’s 222,770 manufacturing establishments and aging workforce have catalyzed adoption of lights-out finishing cells that minimize operator fatigue. Manual presses persist in boutique shops that prize tactile craft or where runs stay below break-even thresholds for automation.

Predictive-maintenance dashboards and closed-loop quality cameras now ship as standard on high-end automatic presses, shrinking downtime. Robotics handle blank sheet loading and finished pile stacking to cut ergonomic strain. Modular design lets converters add auto-foil reel changers or dual-press stations later, aligning capital spend with order book growth. Consequently, the embossing and foil stamping equipment market experiences a gradual but steady tilt toward fully automatic configurations.

By End-user Industry: Security drives incremental revenue

Packaging and labeling activities represented 45.76% of the embossing and foil stamping equipment market size in 2024, as brand marketing relies on premium cues to lift sell-through rates. Anti-counterfeiting programs in pharmaceuticals, luxury goods and government documents push security printing to an 8.05% CAGR, the fastest among application groups. Komori’s integrated report places heavy emphasis on security press know-how, validating the revenue potential of overt and covert foil features.

Commercial print retains value in invitations, business reports and covers that benefit from tactile embellishment. Craft and promotional merchandise apply foil and emboss in small batches for e-commerce clients, sustaining niche demand for quick-change platforms. Growth converges where security and aesthetic functions overlap, prompting machine builders to incorporate holographic foil indexers and micro-emboss modules capable of producing complex layered textures in one pass.

Geography Analysis

Asia-Pacific anchored 37.18% of global embossing and foil stamping equipment market revenue in 2024 and is projected to rise at a 7.92% CAGR through 2030. China supplies large-scale packaging volumes, while Japan contributes process innovation that raises regional equipment standards. India’s Production-Linked Incentive scheme and National Manufacturing Policy target a 25% GDP manufacturing share by 2025, stimulating local converters to modernize. South Korea and Southeast Asian nations increase demand across electronics and personal-care packaging that needs consistent metallic accents.

North America and Europe show mature replacement cycles yet advance technologically. The Federal Reserve’s printing and related support index hit 83.2061 in May 2025, illustrating a stable base for capital refreshes that improve productivity. European converters adopt cold-foil and energy-efficient dryers to meet aggressive climate targets. The EU’s advanced manufacturing sector, centered in Germany, Spain, France and Italy, climbed to 4,500 firms in 2023, broadening the buyer pool for next-generation embellishment lines.

Middle East and Africa, alongside South America, present emerging opportunities. Saudi Arabia and the UAE diversify away from hydrocarbons and set up large fast-moving consumer goods plants that need localized packaging supply. Brazil and Argentina spearhead South American adoption as regional consumer goods brands upscale presentation. Suppliers tailor propositions by pairing cost-effective mid-range machines with upgrade paths to full automation, recognizing budget constraints in developing economies.

Competitive Landscape

The embossing and foil stamping equipment market shows moderate concentration, with heritage players such as Bobst, Heidelberg, Koenig and Bauer and Komori leveraging extensive service networks. Bobst recorded CHF 828.2 million H1 2024 sales, though incoming orders dipped as converters delayed large projects. Heidelberg secures more than half of revenue from packaging, boosted by its Canon alliance that extends digital print reach. Koenig and Bauer achieved EUR 1,274.4 million revenue in 2024, maintaining a EUR 1,039.8 million order backlog that underwrites future press deliveries.

Competition intensifies as digital spot-UV and varnish systems provide alternative decoration routes. Vendors respond with hybrid presses capable of switching from foil to varnish in minutes, protecting share in commercial print. Patent filings climb in micro-emboss patterning and low-energy adhesive chemistry, highlighting a shift toward sustainability and security. New entrants focus on holographic module retrofits that integrate into existing offset lines, while established groups market subscription-based maintenance to lock in recurring revenue.

White-space lies in software that links pre-press, press and post-press data, giving converters real-time costing and carbon-footprint dashboards. Suppliers capable of offering open-architecture platforms stand to win multi-site deals as global brand owners harmonize finishing specifications across continents.

Embossing And Foil Stamping Equipment Industry Leaders

BOBST

Heidelberg (MK Masterwork)

Komori Corporation

Gietz AG

Brandtjen & Kluge LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Heidelberg projected FY 2025/26 sales of EUR 2,350 million with up to 8% EBITDA margin on the back of robust packaging demand and China Print order flow.

- February 2025: Koenig and Bauer posted operating EBIT of EUR 46.5 million for Q4 2024 on revenue of EUR 1,274.4 million, maintaining record backlog to support 2025 guidance.

- January 2025: Heidelberg opened its 175th anniversary year with a growth roadmap that seeks EUR 300 million extra sales by 2029 through packaging and digital print expansion.

- January 2025: Komori released its Integrated Report 2024, detailing anti-counterfeiting technology progress and long-term security press focus.

- November 2024: DuPont announced 4% net-sales growth to USD 3.2 billion in Q3 2024, citing semiconductor recovery and a USD 70 million capex program in electronics and industrial lines

Global Embossing And Foil Stamping Equipment Market Report Scope

| Hot Foil Stamping Machines |

| Cold Foil Stamping Machines |

| Digital Foil Stamping Machines |

| Embossing Presses |

| Combination Foil-Emboss Systems |

| Manual |

| Semi-automatic |

| Fully Automatic |

| Packaging and Labeling |

| Commercial Printing |

| Security Printing |

| Textile and Leather Goods |

| Craft and Promotional Items |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Equipment Type | Hot Foil Stamping Machines | ||

| Cold Foil Stamping Machines | |||

| Digital Foil Stamping Machines | |||

| Embossing Presses | |||

| Combination Foil-Emboss Systems | |||

| By Operation Mode | Manual | ||

| Semi-automatic | |||

| Fully Automatic | |||

| By End-user Industry | Packaging and Labeling | ||

| Commercial Printing | |||

| Security Printing | |||

| Textile and Leather Goods | |||

| Craft and Promotional Items | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the embossing and foil stamping equipment market?

The embossing and foil stamping equipment market size is USD 5.39 billion in 2025.

Which segment shows the fastest growth?

Digital foil stamping machines record the fastest growth at an 8.13% CAGR through 2030.

Why is Asia-Pacific the leading region?

Asia-Pacific benefits from large-scale manufacturing expansion and supportive government schemes that spur equipment investment, giving it 37.18% share in 2024.

How are sustainability trends influencing equipment design?

Converters are selecting cold-foil systems and energy-efficient modules that support recyclability and lower carbon footprints, driving suppliers to integrate greener technology.

What restrains wider adoption of fully automatic presses?

High capital costs remain the chief barrier, especially for small and medium converters, although modular upgrades and financing models aim to ease entry.

Page last updated on: