Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 8.86 Billion |

| Market Size (2026) | USD 9.12 Billion |

| Market Size (2031) | USD 10.54 Billion |

| Growth Rate (2026 - 2031) | 2.94% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Printed Signage Market Analysis by Mordor Intelligence

The United States printed signage market size was valued at USD 8.86 billion in 2025 and estimated to grow from USD 9.12 billion in 2026 to reach USD 10.54 billion by 2031, at a CAGR of 2.94% during the forecast period (2026-2031). The market size outlook reflects structural shifts in which static media competes with digital solutions even as infrastructure funding and evolving retail formats bolster demand. Cost-effectiveness in long-duration outdoor applications, federal “Investing in America” branding mandates, and rapid quick-service restaurant (QSR) roll-outs underpin near-term growth. Material innovation-especially recyclable substrates-mitigates regulatory risk, while inkjet’s short-run economics strengthen provider margins. Supply-chain volatility for PVC and aluminum composites, together with widening environmental oversight, poses strategic risks that favor diversified sourcing and sustainable materials.

Key Report Takeaways

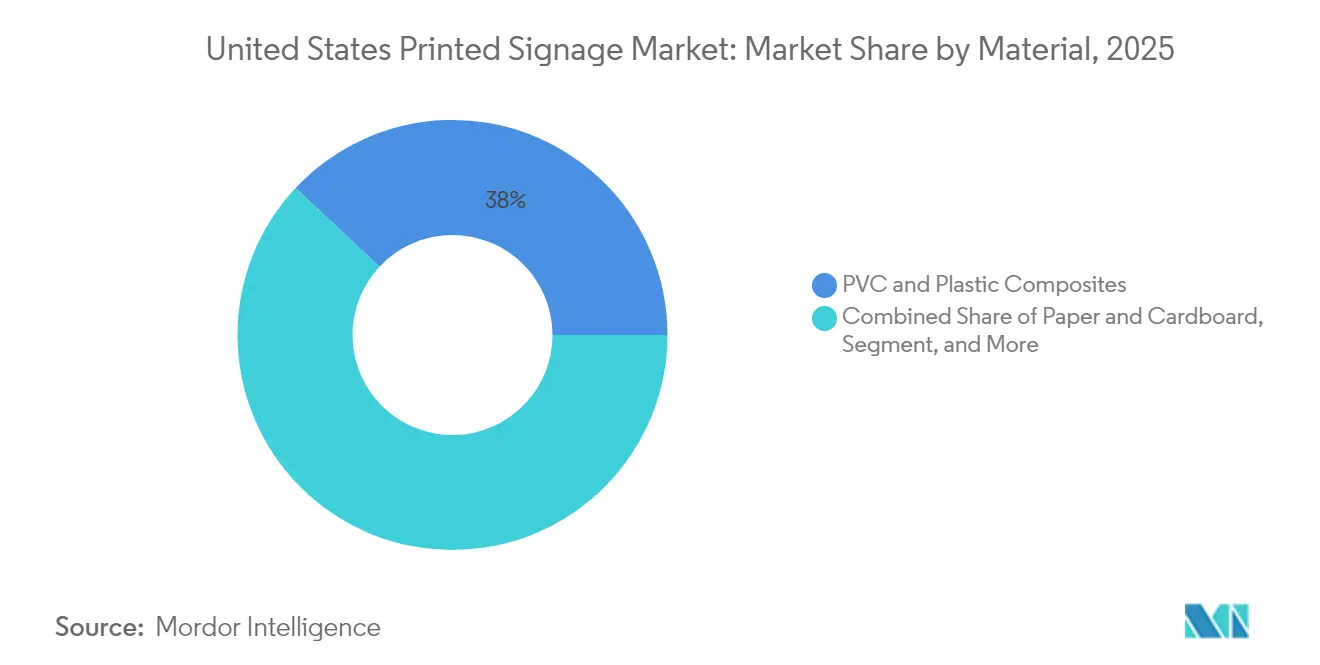

- By material, PVC and plastic composites led with 38.02% of the United States printed signage market share in 2025, while paper and cardboard are set to expand at a 4.18% CAGR through 2031.

- By product, banners, flags, and backdrops accounted for 31.05% of the United States printed signage market size in 2025; backlit displays hold the fastest growth outlook at 3.38% CAGR to 2031.

- By application, outdoor formats dominated with 60.78% of the United States printed signage market share in 2025, whereas indoor signage is projected to rise at a 4.04% CAGR over 2026-2031.

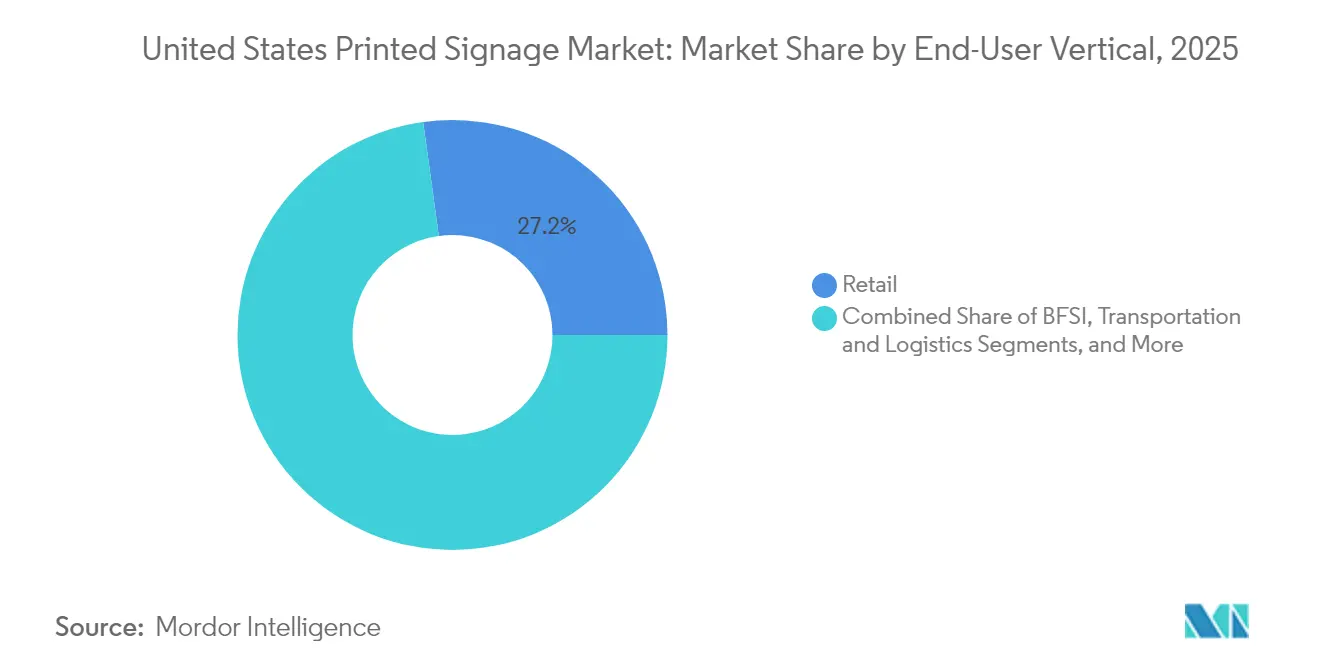

- By end-user vertical, retail commanded 27.18% of the United States printed signage market size in 2025; education and government demand is climbing at a 3.92% CAGR to 2031.

- By printing technology, inkjet systems held 42.05% United States printed signage market share in 2025 and are predicted to advance at a 4.14% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Printed Signage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-effectiveness of printed signage | +0.8% | National, QSR and value-focused retail | Short term (≤ 2 years) |

| Surging demand from quick-service restaurants | +0.6% | Texas, California, Florida corridors | Medium term (2-4 years) |

| Digital short-run printing lowering inventory costs | +0.5% | Nationwide, regional franchises | Medium term (2-4 years) |

| Growing retail pop-up and experiential stores | +0.4% | New York, California, Illinois urban centers | Short term (≤ 2 years) |

| Infrastructure stimulus boosting outdoor advertising | +0.3% | IIJA transportation corridors | Long term (≥ 4 years) |

| Rise of recyclable/biodegradable sign materials | +0.2% | California and Northeast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-Effectiveness Drives Market Resilience Against Digital Alternatives

Printed signage remains the lowest-total-cost option for static outdoor and QSR drive-through menus because it requires no electricity or network infrastructure. Digital displays consume 100–400 watts and impose service costs, whereas printed boards are maintenance-light, an advantage for operators struggling with staffing gaps as 70% of restaurants reported hard-to-fill positions in 2024. Budget-sensitive chains therefore continue to standardize on durable print packages for high-traffic sites. The result is sustained baseline demand that supports the United States printed signage market even as digital alternatives mature.

QSR Expansion Fuels Systematic Signage Demand

U.S. QSR sales surpassed USD 1.1 trillion in 2024, prompting new builds and remodels that each require full signage suites-storefront, menu boards, compliance notices, and temporary promotions. Franchisees favor printed assets for uniform color matching across hundreds of outlets and simpler procurement compared with IT-heavy digital screens. Drive-through lanes, where glare and weather challenge LCD readability, further secure printed formats. These high-volume roll-outs anchor revenue visibility for vendors across the United States printed signage market.

Digital Short-Run Printing Transforms Inventory Economics

Modern inkjet presses eliminate setup plates, allowing economical runs of fewer than 100 units. Retailers capitalize on this agility to refresh seasonal campaigns without locking cash in old inventory. Labels and Labeling reported accelerating converter investment to meet these micro-run needs. [1]Labels & Labeling, “North American Market Navigates Key Challenges,” labelsandlabeling.com Reduced obsolescence risk encourages broader adoption of localized graphics, extending the application scope for the United States printed signage market.

Pop-Up Retail Drives Temporary Signage Innovation

Experiential pop-ups require lightweight, portable signs that install in hours and exit cleanly. Fabric backdrops and foldable frames now dominate these deployments, meeting urban landlords’ no-alteration clauses. Brands value the tactile impact of printed textiles, which complement digital activations without power or data cabling. These agile formats open incremental revenue pools across the United States printed signage market, especially in dense metros where real estate costs favor temporary concepts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advent of digital signage | -0.9% | High-traffic QSR and retail sites | Medium term (2-4 years) |

| Environmental regulations on PVC substrates | -0.4% | California, Northeast, federal path | Long term (≥ 4 years) |

| Supply chain volatility of paper and aluminum composites | -0.3% | Nationwide freight-sensitive zones | Short term (≤ 2 years) |

| Labor shortages in wide-format printing shops | -0.2% | Manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital Signage Adoption Accelerates Across High-Value Applications

Dynamic menu boards and interactive displays now integrate with cloud CMS and AI analytics, allowing price shifts and personalized ads at scale. Large QSR chains and flagship retailers view these capabilities as revenue multipliers, eroding share from static boards. However, infrastructure costs and maintenance requirements still limit penetration, preserving significant addressable volume for the United States printed signage market in cost-centric venues.

Environmental Regulations Target PVC Substrate Usage

The Environmental Protection Agency’s Safer Choice framework and state-level rules restrict vinyl chloride exposure, driving up compliance costs for PVC sheet suppliers. [2]U.S. Environmental Protection Agency, “Safer Choice Standards and Criteria,” epa.gov California’s early bans often set nationwide precedent, prompting multi-state chains to pre-specify recyclable alternatives. While eco-friendly films such as non-PVC polyolefins carry price premiums, early adopters gain procurement preference in government bids, reshaping material demand across the United States printed signage market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: PVC Dominance Faces Sustainability Pressures

PVC and plastic composites captured 38.02% of United States printed signage market share in 2025 owing to superior weather resistance. The segment’s growth is slowing as compliance costs rise, but absolute demand remains high for highway and construction signage tied to IIJA projects. Paper and cardboard’s 4.18% CAGR signals rapid substitution in indoor décor and short-lifecycle retail campaigns, while recyclable rigid boards such as Neenah’s Endura line win institutional contracts.

For premium outdoor installations, metal sheets retain niche appeal, and fabric substrates scale alongside pop-up retail. Emerging biodegradable films position vendors to hedge regulatory risk and safeguard margins. These shifts ensure material diversification within the United States printed signage market as buyers balance cost, durability, and sustainability credentials.

By Product: Banners Lead While Backlit Displays Accelerate

Banners, flags, and backdrops delivered 31.05% of the United States printed signage market size in 2025, sustained by versatility in events, storefronts, and civic campaigns. Their lightweight construction simplifies logistics and installation, keeping unit costs low. Backlit displays, though smaller in volume, will outpace other products at a 3.38% CAGR. Retailers deploy illuminated graphics in windows and transit hubs, seeking premium aesthetics that command consumer attention after dark.

Billboards remain indispensable where zoning impedes digital boards, especially along federally funded corridors that must feature “Investing in America” branding. Point-of-purchase displays preserve impulse-buy lift in supermarkets, blending with QR-code interactivity. Such diversification underscores the resilience of the United States printed signage market against single-product disruption.

By Application Type: Outdoor Leadership Challenged by Indoor Growth

Outdoor installations represented 60.78% United States printed signage market share in 2025 thanks to billboards, construction hoardings, and roadside menus. IIJA roadway upgrades guarantee multi-year project pipelines for reflective and high-durability substrates. Yet indoor formats will expand faster at 4.04% CAGR as experiential retail, pop-ups, and institutional wayfinding programs scale.

Indoor environments allow cheaper materials and design freedom, fostering creative point-of-sale concepts that reinforce omnichannel campaigns. Educational campuses invest in updated wayfinding and compliance graphics during facility renovations, adding volume to the United States printed signage market while aligning with ADA visibility rules.

By End-User Vertical: Retail Dominance Meets Government Growth

Retail generated 27.18% of the United States printed signage market size in 2025 due to constant promotional activity and store refresh cycles. Chains lean on print kits to maintain brand consistency across thousands of outlets. Education and government entities, however, will record the highest CAGR at 3.92% through 2031. Public-sector funding for school modernizations and transit hubs mandates standardized signage packages that meet accessibility, bilingual, and sustainability criteria.

Transportation authorities commissioning new terminals specify tactile and high-contrast signs, widening scope for specialized vendors. BFSI institutions continue to require audited compliance disclosures posted at branch entrances. Collectively, these vertical trends diversify opportunity streams within the United States printed signage market beyond retail dependence.

By Printing Technology: Inkjet Leadership Strengthens

Inkjet systems secured 42.05% United States printed signage market share in 2025 and will grow at a 4.14% CAGR, propelled by improved UV-curable inks that adhere to varied substrates without primers. Shops embracing single-operator workflows and automated finishing mitigate the sector’s projected 1.9 million labor shortfall by 2033.

Screen printing remains cost-effective for very large runs but lacks the variable-data flexibility retailers now expect. Hybrid lines blending inkjet with rotary screen allow printers to harmonize volume and customization, sustaining competitiveness. As technology refresh cycles shorten, capex decisions increasingly dictate market positioning across the United States printed signage market.

Geography Analysis

California leads spending momentum, backed by USD 32.7 billion in IIJA allocations that stipulate consistent “Investing in America” project branding. The state’s aggressive PVC regulation simultaneously spurs demand for premium non-PVC substrates, raising average selling prices.

Texas follows with USD 28 billion in federal infrastructure grants plus private-sector building booms along the I-35 corridor. Retail buildouts for expanding QSR brands and warehouse logistics hubs require high volumes of outdoor directional signs, bolstering regional contributions to the United States printed signage market.

Northeast metros such as New York absorb USD 23.6 billion in federal funds and exhibit sophisticated buyer preferences-favoring recyclable materials and sleek mounting systems compatible with dense streetscapes. Florida’s hospitality sector cycles seasonal signage packages that withstand UV exposure and hurricane-grade winds, anchoring a steady refurbishment revenue stream.

Midwestern manufacturing zones rely on OSHA compliance and facility signage, prioritizing durable yet economical boards. Mountain-West recreation markets demand eco-sensitive designs that blend with natural scenery, further diversifying substrate requirements. These geographic nuances underline the importance of localized production networks within the United States printed signage market.

Competitive Landscape

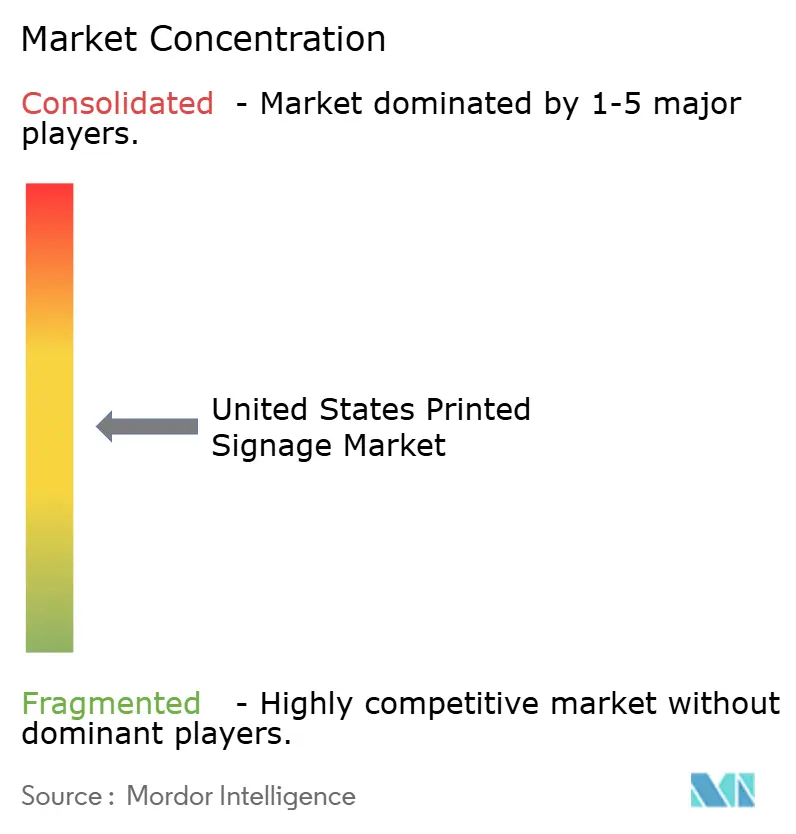

The United States printed signage market remains moderately fragmented as regional providers offer rapid turnarounds unachievable for national chains. Consolidation persists, typified by R.R. Donnelley’s pending Williams Lea acquisition that extends marketing services across 26 countries. Players investing in high-speed inkjet lines and automated finishing offset rising wages and worker shortages.

Sustainability marks a key differentiator: Arlon’s launch of non-PVC DPF V9500 film captures buyers seeking regulatory compliance without sacrificing outdoor longevity. Start-ups leverage web-to-print portals for direct-to-SMB ordering, pressuring incumbents on price transparency. Patent filings on bio-composite boards and AI-driven layout tools suggest continuous innovation cycles that will reshape market shares over the forecast horizon.

While top suppliers collectively control enough capacity to serve national roll-outs, no single firm exceeds a dominant threshold, keeping pricing disciplined yet competitive. Automation, eco-credentialing, and multi-touchpoint service bundles will determine leadership trajectories inside the United States printed signage market.

United States Printed Signage Industry Leaders

Avery Dennison Corporation

3A Composites USA Inc.

Neenah Paper & Packaging LLC

Cimpress plc (Vistaprint)

Kelly Gold & Co. Signs Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: R.R. Donnelley filed trade-secrets litigation against Prisma Graphics, underscoring rising intellectual-property stakes in print services.

- February 2025: Menasha Packaging announced a preprint hub expansion to service signage and packaging clients.

- January 2025: Interstate Advanced Materials promoted recyclable board solutions to meet institutional mandates.

- December 2024: R.R. Donnelley agreed to acquire Williams Lea, broadening tech-enabled business support reach.

United States Printed Signage Market Report Scope

The Printed signage is one of the most widely used forms of signage solutions owing to its cost-effectiveness. It is employed by end-users across various industries to market their products, services by means of Billboards, Backlit Displays, Banners, among others, to attract consumers and expand their knowledge regarding availability and features. The report covers the emerging trends in the United States Printed Signage Market segmented by product, type , and end-user verticals.

By Material

| Paper and Cardboard |

| PVC and Plastic Composites |

| Fabric and Textile |

| Metal Sheets and Foils |

| Wood and Rigid Boards |

By Product

| Billboards |

| Backlit Displays |

| Point-of-Purchase (POP) Displays |

| Banners, Flags and Backdrops |

| Corporate Graphics, Exhibition and Trade-show Materials |

| Transit and Street Furniture |

| Other Products |

By Application Type

| Indoor Printed Signage |

| Outdoor Printed Signage |

By End-user Vertical

| Retail |

| BFSI |

| Transportation and Logistics |

| Sports and Leisure |

| Entertainment and Media |

| Education and Government |

| Other End-User Verticals |

By Printing Technology

| Screen Printing |

| Inkjet Printing |

| Toner-based (Electrophotography) |

| Other Printing Technologies |

| By Material | Paper and Cardboard |

| PVC and Plastic Composites | |

| Fabric and Textile | |

| Metal Sheets and Foils | |

| Wood and Rigid Boards | |

| By Product | Billboards |

| Backlit Displays | |

| Point-of-Purchase (POP) Displays | |

| Banners, Flags and Backdrops | |

| Corporate Graphics, Exhibition and Trade-show Materials | |

| Transit and Street Furniture | |

| Other Products | |

| By Application Type | Indoor Printed Signage |

| Outdoor Printed Signage | |

| By End-user Vertical | Retail |

| BFSI | |

| Transportation and Logistics | |

| Sports and Leisure | |

| Entertainment and Media | |

| Education and Government | |

| Other End-User Verticals | |

| By Printing Technology | Screen Printing |

| Inkjet Printing | |

| Toner-based (Electrophotography) | |

| Other Printing Technologies |

Key Questions Answered in the Report

How large is the United States printed signage market in 2026?

It is valued at USD 9.12 billion and is projected to reach USD 10.54 billion by 2031.

Which product category is growing the fastest?

Backlit displays hold the highest projected CAGR at 3.38% through 2031.

Why does inkjet technology lead U.S. signage production?

Inkjet combines short-run cost efficiency, broad substrate compatibility, and automation features that offset labor shortages.

What regulatory factors influence material choices?

EPA initiatives and state PVC restrictions push buyers toward recyclable and non-PVC substrates.

Which end-user segments show the strongest growth?

Education and government signage demand is expanding at a 3.92% CAGR due to infrastructure modernization programs.

How will infrastructure spending affect future demand?

IIJA requirements for standardized project branding guarantee multi-year volume for outdoor and transit signage.

Page last updated on: