Advanced Tires Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

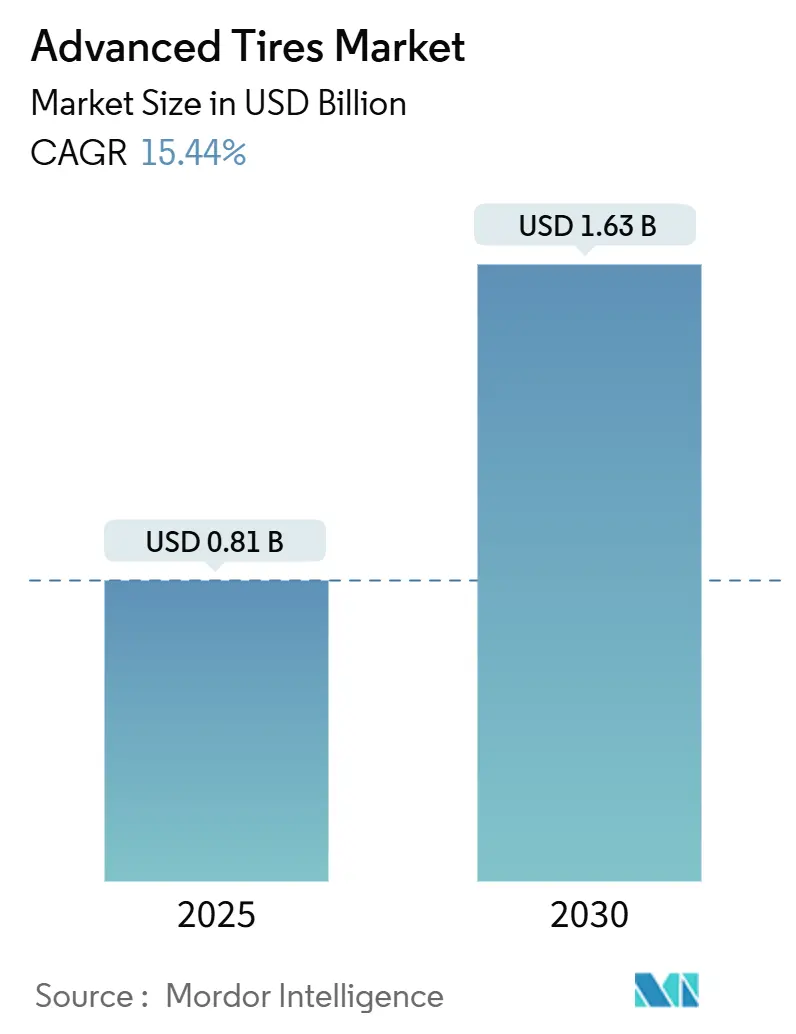

| Market Size (2025) | USD 0.81 Billion |

| Market Size (2030) | USD 1.63 Billion |

| Growth Rate (2025 - 2030) | 15.44% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Tires Market Analysis by Mordor Intelligence

The Advanced Tires Market size is estimated at USD 0.81 billion in 2025, and is expected to reach USD 1.63 billion by 2030, at a CAGR of 15.44% during the forecast period (2025-2030). The doubling in value captures how electric-vehicle proliferation, IoT penetration, and autonomous-driving development turn formerly passive rubber components into data-rich, performance-critical vehicle subsystems. Demand concentrates on torque-resilient compounds, embedded-chip architectures, and self-inflating mechanisms that mitigate maintenance downtime. Market momentum is further reinforced by sustainability regulations such as California’s 6PPD ban, which accelerates bio-based chemical innovation. Competitive intensity is moderate as legacy tire majors defend share against sensor, software, and materials specialists. Yet, collaboration outpaces confrontation because OEM integration now rewards partners that blend mechanical engineering with digital analytics.

Key Report Takeaways

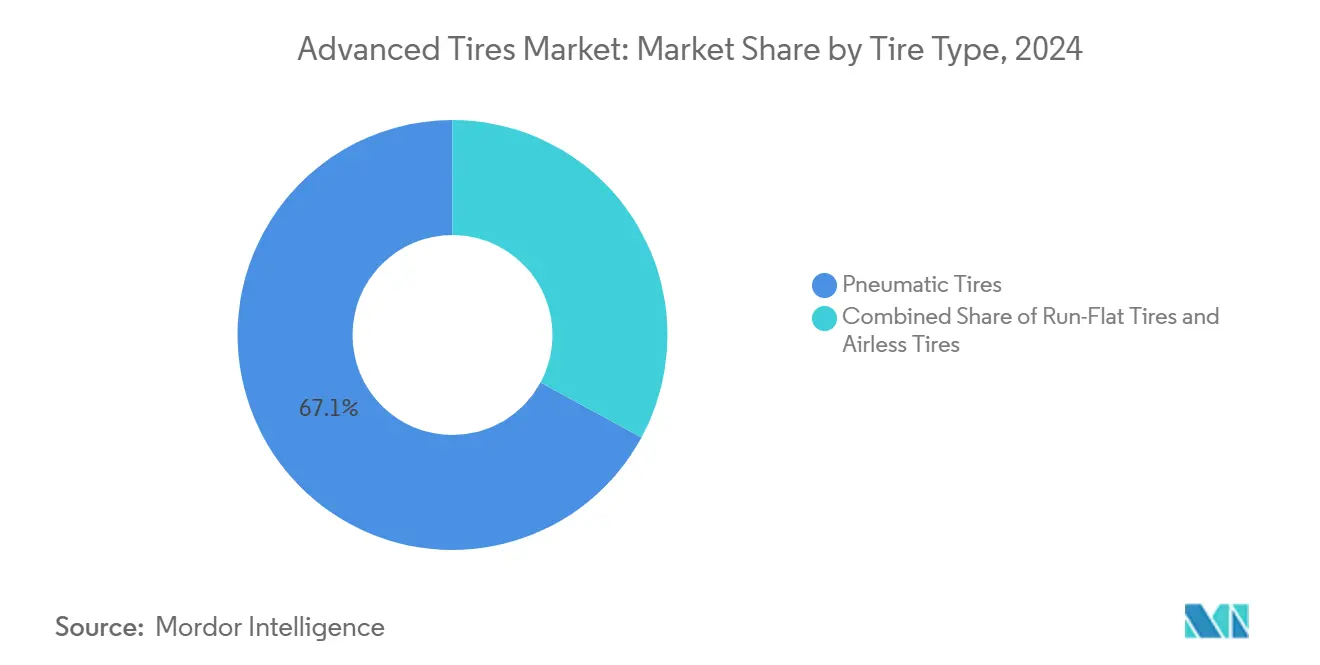

- By tire construction, pneumatic products accounted for 67.13% of the advanced tires market size in 2024, and airless formats are growing at a 15.48% CAGR between 2025 and 2030.

- By technology, chip-embedded smart tires commanded 44.54% of the advanced tires market size in 2024; self-inflating systems are forecast to expand at a 15.51% CAGR to 2030.

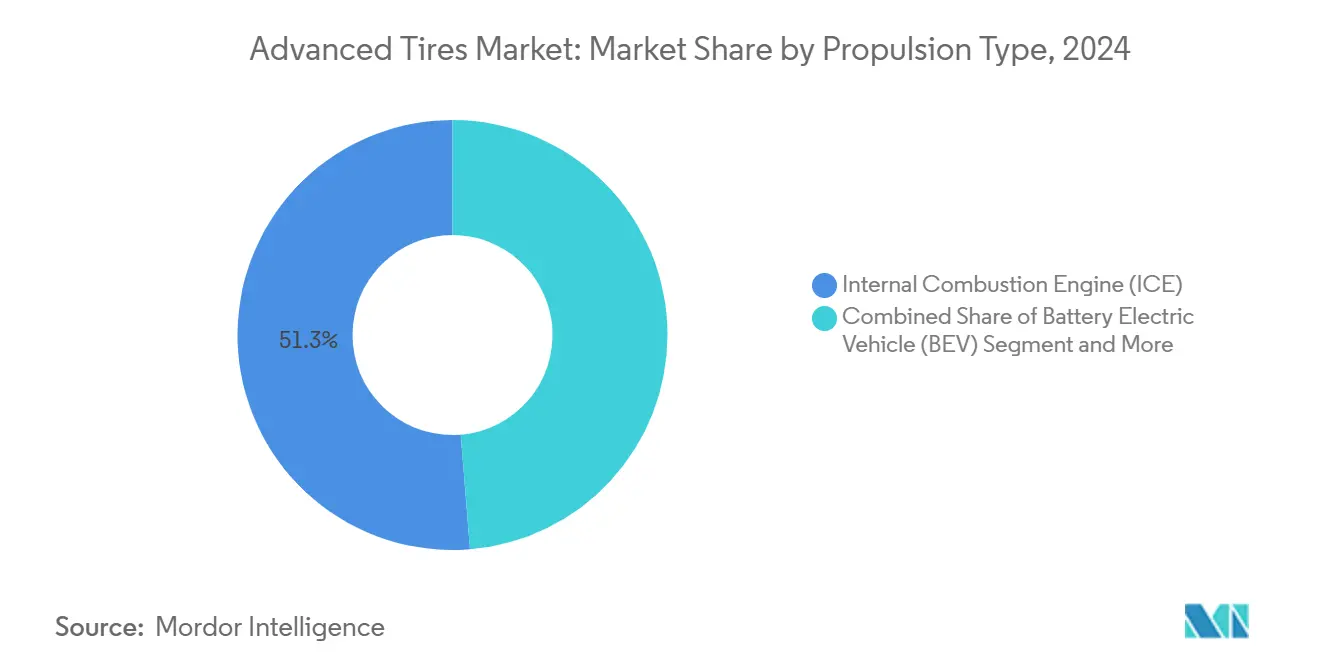

- By propulsion type, internal combustion engines held 51.26% of the advanced tires market share in 2024, while battery electric vehicles are projected to advance at a 15.55% CAGR through 2030.

- By sales channel, the aftermarket controlled 73.42% of the advanced tires market size in 2024, whereas OEM fitments are poised for the quickest expansion at 15.45% CAGR by 2030.

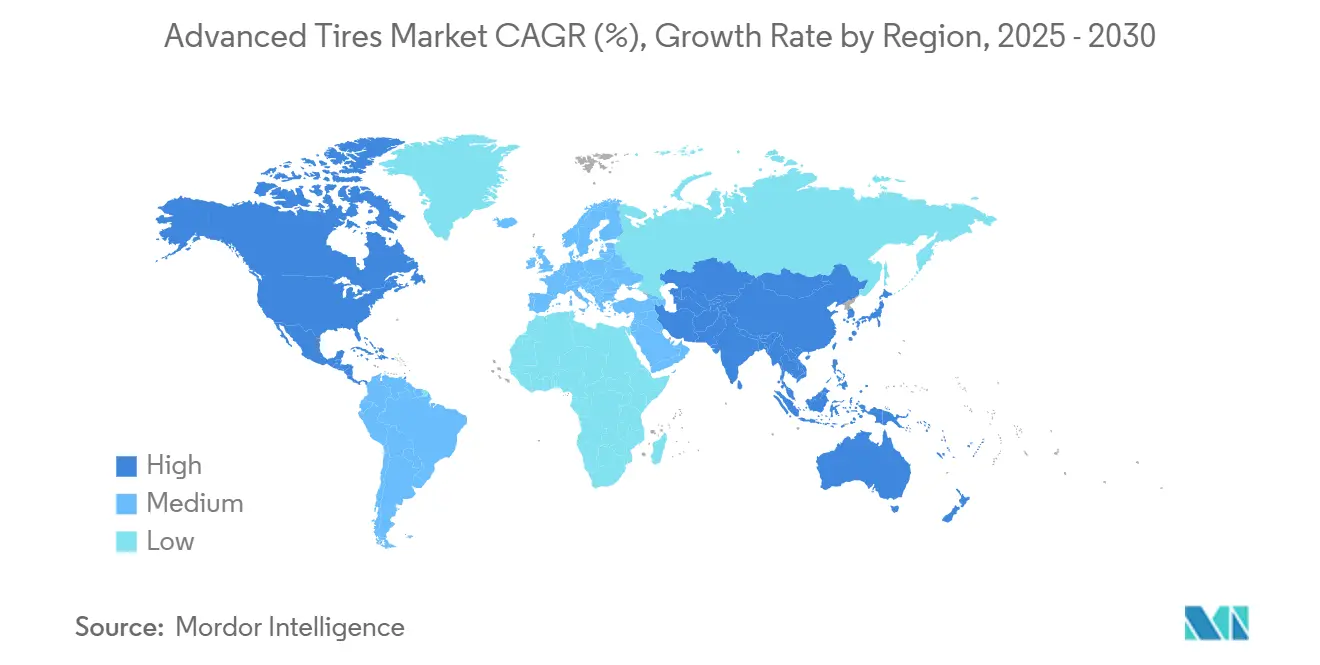

- By region, Asia Pacific led with 37.88% share of the advanced tires market size in 2024 and is set to post the fastest 15.49% CAGR to 2030.

Market Trends and Insights

Drivers Impact Analysis of Advanced Tires Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise of Electric & Connected Vehicles | +4.2% | Global, with Asia Pacific and North America leading | Medium term (2-4 years) |

| OEM Push for Smart Connected Tires | +3.8% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Industry 4.0 Automated Tire Plants Lower Costs | +2.3% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Regulatory Fuel-Economy Mandates | +2.1% | North America and EU primarily | Long term (≥ 4 years) |

| California 6PPD Regulation | +1.9% | North America, spillover to global markets | Medium term (2-4 years) |

| Fleet Subscription & Service Models | +1.1% | North America and EU, expanding to Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise of Electric & Connected Vehicles

Electric traction adds mass, instant torque, and low cabin noise, so tires now use high-load carcasses, silica-rich compounds, and acoustic foams that can trim rolling resistance by one-fifth and cabin noise by 2 dB[1]“Elect Tire Technology,” Pirelli SpA, pirelli.com . Continental’s EV-Ready line integrates noise-absorbing polyurethane strips and optimized tread geometry, securing OEM nominations on 2025 model-year SUVs[2]“Smart Tires for Electric Mobility,” Continental AG, continental.com . EV-specific SKUs also command price premiums of one-fourth, lifting revenue per unit for manufacturers. Data streams from chip-enabled casings feed range-prediction algorithms in battery-management systems. The collab between electric platforms and intelligent tires positions suppliers with EV portfolios for outsized growth as global BEV deliveries increase in 2025.

OEM Push for Smart Connected Tires

Level-3 autonomy prototypes require real-time friction and temperature data to refine braking envelopes, driving OEM mandates for embedded-sensor casings at the program-kickoff stage. Chip-embedded designs already occupy more than two-fifths of technology revenue. Continental’s joint development contracts with two European automakers illustrate how tire and vehicle ECUs now co-develop communication protocols. Predictive maintenance models reduce fleet downtime and shrink warranty costs. The OEM-channel CAGR reflects how factory fitment of connected tires will outpace retrofit installations. As proprietary data ecosystems mature, OEMs prefer tier-one tire suppliers that can guarantee cybersecurity compliance and over-the-air firmware updates.

Industry 4.0 Automated Tire Plants Lower Costs

Cobot bead-assembly cells, machine-vision tread inspection, and digital twins push first-pass yield above four-fifths, cutting scrap and energy usage. Bridgestone’s Hiroshima facility reports a one-fifth labor reduction and cycle-time gain post-automation. As capital amortizes, unit costs converge faster toward conventional tires, easing the cost restraint. Enhanced process data also informs real-time compound adjustments that elevate uniformity, directly supporting autonomous-vehicle ride comfort targets.

Regulatory Fuel-Economy Mandates

The EU’s post-2025 CO2 rules compel passenger cars to trim fleet emissions by two-fifths from 2021 baselines, and low-rolling-resistance tires contribute up to 4 g/km of that requirement. Silica-enriched tread recipes and narrow-section designs shed minimal energy loss, equivalent to two years of powertrain efficiency gains. Labeling schemes like Europe’s Grade A rating now influence two-fifths of consumer purchase decisions. U.S. CAFE updates mirror this trajectory, prompting North American tire plants to retool for low-hysteresis compounds. Manufacturers investing early in material science secure price premiums and regulatory credits while easing OEM compliance costs.

Restraints Impact Analysis of Advanced Tires Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost | -2.7% | Global, particularly affecting emerging markets | Short term (≤ 2 years) |

| Specialty Material Supply Volatility | -1.9% | Global, with higher impact in import-dependent regions | Short term (≤ 2 years) |

| Durability and Reliability Concerns for New Designs | -1.8% | Global, with higher impact in commercial applications | Medium term (2-4 years) |

| Data Ownership and Cybersecurity Risks | -1.4% | Global, concentrated in developed markets with connected vehicles | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost & Limited Economies of Scale

Smart casings with multilayer sensor arrays retail at USD 240 versus USD 155 for comparable premium pneumatic models, narrowing addressable demand in price-sensitive geographies. Production volumes decrease per SKU, keeping material and calibration overheads high. Freight operators in Latin America and Southeast Asia postpone adoption until the total cost of ownership modeling proves tangible savings. Suppliers are piloting built-in-USA credits and modular sensor cartridges that reduce incremental cost per tire by one-tenth to unlock volume. Scale is anticipated once three global OEM programs transition from validation to series production during 2026-2027.

Durability & Reliability Concerns for New Designs

Embedded electronics add potential failure points; field tests show moisture ingress causing 3% sensor dropout after 24 months in heavy-duty cycles. Airless prototypes still grapple with heat build-up at sustained highway speeds, limiting initial launches to last-mile fleets. Fleet operators demand assurance parity with conventional casings’ 160,000 km warranty coverage. Service technicians also require new calibration equipment, increasing downtime during early rollouts. As ISO 21750 finalizes interoperability criteria, component vendors aim to halve sensor housing thickness, improve flex-fatigue life, and address warranty hesitations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Advanced Tires Market Segment Analysis

By Tire Type:

Pneumatic Dominance Faces Airless DisruptionPneumatic tires captured 67.13% share of the advanced tires market in 2024, benefitting from global manufacturing scale and a mature replacement ecosystem. Airless architectures, however, exhibit the strongest 15.48% CAGR, reflecting Michelin’s UPTIS pilots with General Motors and Bridgestone’s logistics-fleet deployments. Pneumatics continue to evolve via self-sealing linings and run-flat inserts that stretch product relevance even as puncture-proof alternatives mature. In contrast, airless ribs, spoke lattices, and additively manufactured structures aim to cut downtime and disposal waste, positioning the format well for autonomous robo-taxi fleets.

The advanced tires market shows bifurcation: premium passenger cars still favor comfort-oriented pneumatics, whereas warehouse, last-mile, and military fleets test air-free concepts. Scaling challenges include retooling mounting equipment and achieving vibration damping comparable with inflated casings. Regulators are drafting endurance test protocols to certify airless models for highway use by 2026. As producers refine polyurethane elastomers to dissipate heat, adoption barriers fall, and airless tires could erode pneumatic dominance in high-utilization segments where puncture risk imposes hidden costs.

By Technology:

Smart Integration Leads Innovation WaveChip-embedded designs controlled 44.54% share of the advanced tires market in 2024, underscoring how connectivity now defines competitive advantage for the advanced tires market. Self-inflating casings headline growth at 15.51% CAGR, leveraging peristaltic pumps that replenish pressure using rotational energy. The advanced tires market share for multi-chamber formats remains modest but attractive for defense and mining, where redundancy trumps cost. Self-sealing compounds insert polyisobutylene layers that plug 5-mm punctures within seconds, protecting passenger vehicles from roadside hazards.

Platform convergence is evident in Michelin’s VISION concept, which marries airless lattices with printable tread modules and integrated RFID. Component standardization around ISO 21750 permits sensors from Melexis or Murata to interface across brands, reducing R&D duplication. As carmakers mandate over-the-air update capability, tire firmware joins vehicle ECU patch cycles, embedding suppliers deeper into OEM software supply chains. Over time, the combination of self-inflation, chip telemetry, and adaptive compounds is expected to lift average selling price while lowering lifetime operating cost for fleets.

By Propulsion Type:

Electric Transition Reshapes RequirementsInternal combustion vehicles retained a 51.26% share of the advanced tires market in 2024, but battery electric vehicles generated the quickest 15.55% CAGR, reshaping compound, contour, and noise requirements. As global EV registrations accelerate, the advanced tires market size for BEV fitments will double by 2030. Rolling-resistance coefficients drop to 6.2 kg/t in flagship EV tires versus 7.8 kg/t for comparable ICE models, extending range by roughly 7 km per charge. Acoustic foams trim cavity resonance, reducing in-cabin noise by up to 2 dB and meeting luxury-EV expectations.

Hybrids and plug-in hybrids bridge the technology gap, demanding casings that withstand combustion-engine heat cycles and EV torque spikes. Fuel-cell platforms constitute a niche share but require ultra-low rolling resistance to maximize the hydrogen economy. As battery chemistries advance, tire load ratings must stretch further, prompting bead-area reinforcement and lightweight cord fabrics. Suppliers that align compound development with OEM electrification roadmaps secure preferred-vendor status and design-in royalties.

By Sales Channel:

OEM Integration AcceleratesThe aftermarket commanded a 73.42% share of the advanced tires market in 2024 because existing global vehicle stock relies on replacement purchases. OEM sales, though smaller, will register a 15.45% CAGR as new-vehicle platforms specify smart tire SKUs at launch. Long design cycles and validation testing bake suppliers into five-year production runs, ensuring volume predictability. The advanced tires market share shift toward OEMs also means higher technical barriers: automotive cybersecurity audits, PPAP documentation, and functional-safety compliance add costs that smaller aftermarket players struggle to bear.

Subscription-based “tire-as-a-service” bundles blur channel boundaries by pairing casings with telemetry dashboards and scheduled replacement logistics. OEM finance arms increasingly package these services into leasing contracts, monetizing data streams while locking in captive parts revenue. Meanwhile, regional tire dealers evolve into sensor-calibration hubs, capturing service income and reinforcing aftermarket resilience.

Geography Analysis

APAC Advanced Tires Market

Asia Pacific contributed a 37.88% share of the advanced tires market in 2024, spearheaded by China’s exports in the first eight months of the year. A regional CAGR of 15.49% through 2030 benefits from dense BEV adoption, smart-factory deployments, and supportive government R&D grants. Japan sustains a technology leadership halo via Sumitomo’s ACTIVE TREAD polymer, which adapts viscoelasticity to road micro-textures and extends wear life by minimal volume. South Korea’s Hankook invests in iFlex airless concepts for delivery robots and micro-mobility fleets.

North America Advanced Tires Market

North America emphasizes fleet uptime and regulatory compliance. California’s 6PPD prohibition forces chemical reformulation, creating North American-centric eco-label launches by 2026. Goodyear’s expansion of its Napanee plant will raise EV-tire output by a vast number annually, aligning local supply with U.S. EV production targets. Canadian waste-management fleets pilot Revvo’s AI-driven tire analytics, illustrating how data services generate cross-border collaboration.

Europe Advanced Tires Market

Europe intertwines sustainability with digital innovation. EU tire-label revisions now display snow-handle icons and QR-linked performance databases, spurring informed consumer choices. OEMs such as Volvo Trucks specify connected tire modules across regional heavy-duty lines to maximize uptime and CO2-credit earnings. Circular-economy legislation pushes reclaimed carbon black adoption, and pilot plants in the Netherlands scale pyrolysis output for compound reintegration.

Competitive Landscape

Competition is moderately concentrated, with the top five suppliers, Bridgestone, Michelin, Continental, Goodyear, and Pirelli, commanding roughly three-fifths of global revenue. Legacy incumbents leverage century-old distribution channels, high-volume molding lines, and joint development agreements with automakers. Michelin’s collaboration with General Motors on UPTIS has reached on-road piloting across Michigan shuttle fleets, funneling test data into design validation loops[3]“UPTIS Airless Tire Road Tests,” Michelin Group, michelin.com .

Technology entrants inject specialized capabilities. Revvo Technologies licenses edge AI algorithms that predict anomalous vibration signatures 300 km before a blowout, securing contracts with U.S. logistics firms. Melexis supplies 6-axis MEMS accelerometers rated 180 °C, and they are now qualified in two European OEM tire programs. Partnerships outweigh outright acquisitions; Continental co-develops sensor packaging with Siemens for Industry 4.0 plants, while Bridgestone’s minority stake in Kodiak Robotics explores tire feedback loops for autonomous freight.

Cost-leadership strategies coexist with differentiation plays. Chinese producers scale low-rolling-resistance pneumatics at sub-USD 90 wholesale prices, challenging premium brands in emerging markets. In response, Western majors prune non-core assets—exemplified by Goodyear’s divestiture of its off-the-road business to Yokohama—to redeploy capital toward connected-tire ecosystems. Patent filings 2024 indicate intensifying R&D competition in recyclable elastomers and energy-harvesting tread inserts that could power next-generation sensors independently.

Advanced Tires Industry Leaders

Michelin

Continental AG

Pirelli

The Goodyear Tire & Rubber Company

Bridgestone Corporation

- *Disclaimer: Major Players sorted in no particular order

Advanced Tires Market Companies Covered in this Report

- Bridgestone Corporation

- Michelin

- Continental AG

- The Goodyear Tire & Rubber Company

- Pirelli & C. S.p.A.

- Sumitomo Rubber Industries Ltd.

- Yokohama Rubber Co. Ltd.

- Hankook Tire & Technology Co Ltd.

- Nokian Tyres Plc

- Toyo Tire Corporation

- CEAT Ltd.

- Kumho Tire

- Cooper Tire & Rubber Company

- Apollo Tyres Ltd.

- JK Tyre & Industries Ltd.

- Giti Tire

- ZC Rubber

- Maxxis International

- Sailun Group Co Ltd.

- Revvo Technologies Inc.

Recent Industry Developments in Advanced Tires Market

- February 2025: Goodyear completed the sale of its off-the-road tire business to Yokohama Rubber for USD 905 million, reallocating resources toward advanced passenger and commercial technologies.

- December 2024: CEAT acquired the Camso brand from Michelin for USD 225 million, widening its presence in specialty agricultural and industrial tires.

- August 2024: Goodyear announced a CAD 575 million investment in its Napanee, Ontario, plant to scale electric-vehicle tire capacity.

Global Advanced Tires Market Report Scope

Segmentation Overview

| Pneumatic Tires |

| Run-Flat Tires |

| Airless Tires |

| Self-Inflating Tires |

| Chip-Embedded Smart Tires |

| Multi-Chambered Tires |

| All-in-One Tires |

| Self-Sealing Tires |

| Internal Combustion Engine |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Tire Type | Pneumatic Tires | |

| Run-Flat Tires | ||

| Airless Tires | ||

| By Technology | Self-Inflating Tires | |

| Chip-Embedded Smart Tires | ||

| Multi-Chambered Tires | ||

| All-in-One Tires | ||

| Self-Sealing Tires | ||

| By Propulsion Type | Internal Combustion Engine | |

| Battery Electric Vehicle (BEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is the advanced tires market expected to grow through 2030?

The market is projected to expand at a 15.44% CAGR, doubling from USD 0.81 billion in 2025 to USD 1.63 billion by 2030.

Why are electric vehicles reshaping tire specifications?

BEVs add weight and instant torque, so tires need low-rolling-resistance compounds, higher load ratings, and acoustic dampening to extend range and cut cabin noise.

Which technology segment is growing the quickest?

Self-inflating systems show the fastest 15.51% CAGR because they automatically maintain pressure, improving safety and fuel efficiency.

What share do airless tires hold today?

Pneumatics dominate, but airless designs, while smaller, are advancing at 15.48% CAGR as pilots with logistics and OEM partners scale.

Which region leads demand for advanced tires?

Asia Pacific commands 37.88% revenue and the highest 15.49% CAGR, driven by robust EV production and smart-factory investments.

How are tire makers addressing new sustainability regulations?

Companies are reformulating compounds without 6PPD, adopting bio-based materials, and investing in circular-economy recycling plants to meet tightening global standards.

Page last updated on: