Market Overview

| Study Period | 2020 - 2031 |

|---|---|

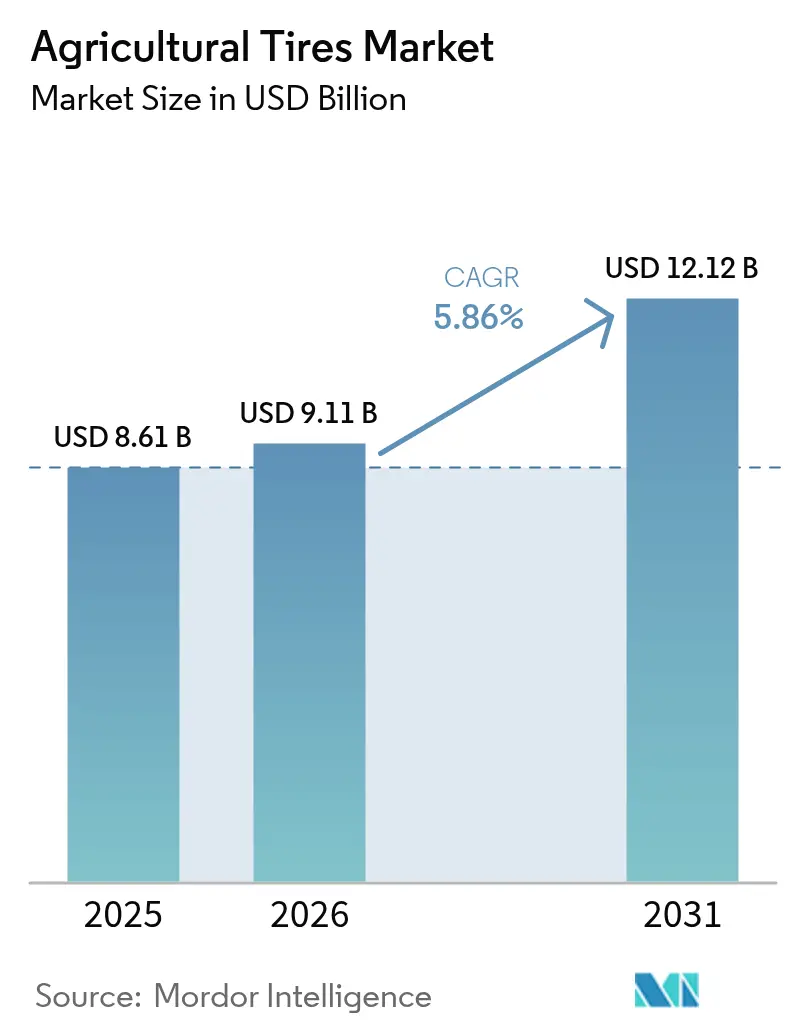

| Market Size (2026) | USD 9.11 Billion |

| Market Size (2031) | USD 12.12 Billion |

| Growth Rate (2026 - 2031) | 5.86% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Agricultural Tires Market Analysis by Mordor Intelligence

The agricultural tires market size is expected to grow from USD 8.61 billion in 2025 to USD 9.11 billion in 2026 and is forecast to reach USD 12.12 billion by 2031 at a 5.86% CAGR over 2026-2031. Demand is expanding as mechanization deepens in Asia and Latin America, conflict-zone reconstruction fuels fresh equipment orders, and low-compaction tire technologies migrate from premium farms to mainstream fleets. The agricultural tire market is also adopting smart-tire features, such as embedded sensors and Central Tire Inflation Systems, reinforcing the link between precision agriculture and tire specifications. Competitive intensity remains moderate because global brands still face credible regional challengers, while sustainability pressures push every player to rethink raw-material sourcing and end-of-life solutions. Long-term prospects hinge on balancing raw-material cost swings with farmers’ need to control soil health and fuel consumption.

Key Report Takeaways

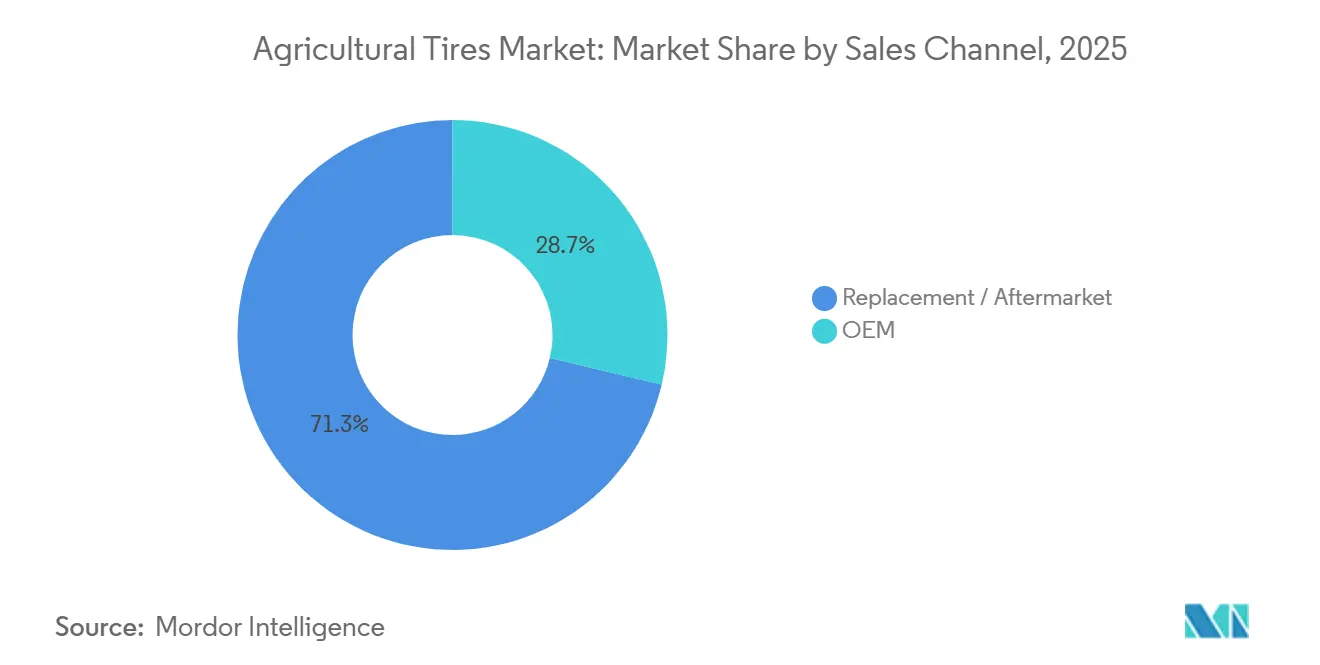

- By sales channel, the replacement/aftermarket segment held 71.29% of the agricultural tires market share in 2025, while the OEM channel is set to post the fastest CAGR at 5.97% through 2031.

- By application, tractors led the agricultural tires market with a 56.73% share in 2025, and sprayers are advancing at a 6.03% CAGR through 2031.

- By tire construction, radial products accounted for 53.22% of the agricultural tires market size in 2025, yet IF/VF radials are pacing ahead at a 6.07% CAGR.

- By rim size, 20-to-30-inch rims commanded 45.51% of the agricultural tires market size in 2025, whereas rims above 40 inches are expanding at a 6.12% CAGR.

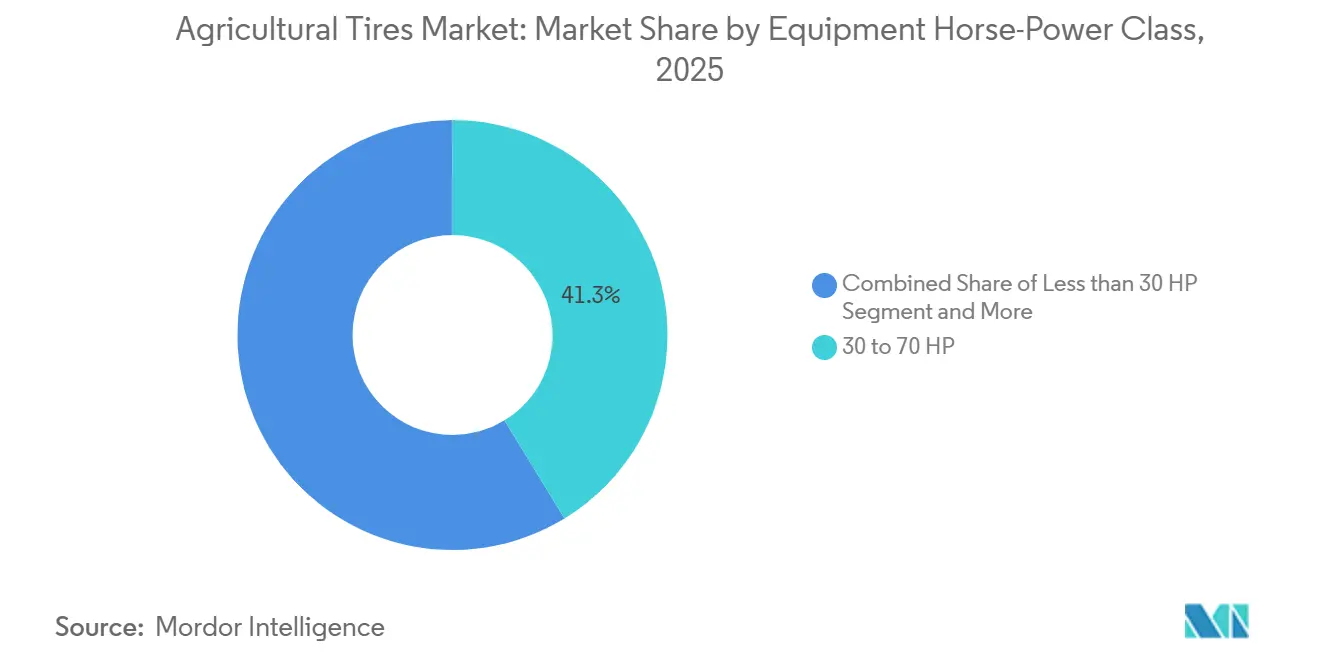

- By equipment horsepower, the 30-to-70-HP class accounted for 41.28% of the agricultural tire market revenue in 2025, but machines above 150 HP are forecast to grow at 6.17%.

- By inflation-technology compatibility, standard tires dominated with 81.26% share in 2025; CTIS-ready and smart tires are growing fastest at 6.23% CAGR.

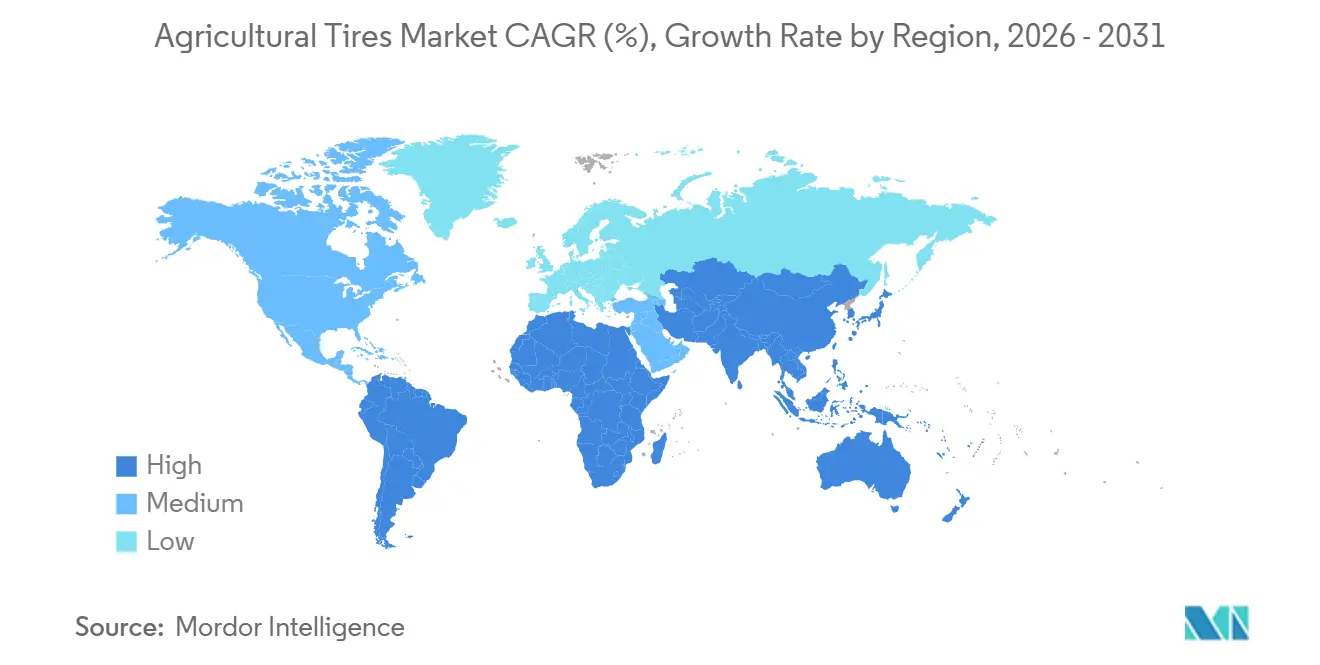

- By geography, Asia-Pacific held the largest share of the agricultural tire market at 37.83% in 2025, while South America is the fastest-growing region, with a 6.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Agricultural Tires Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-Ukraine Reconstruction | +1.2% | Europe, with spillover to North America and Asia-Pacific suppliers | Short term (≤ 2 years) |

| Rapid Mechanization and Fleet Renewal | +1.1% | Asia-Pacific core (India, China), Latin America (Brazil, Argentina), MEA | Medium term (2-4 years) |

| Shift from Bias to Radial Tires | +1.0% | Global, with early adoption in North America and Western Europe | Medium term (2-4 years) |

| CTIS Adoption | +0.9% | North America, Western Europe, Australia; emerging in Brazil and India | Long term (≥ 4 years) |

| Surging Replacement Demand | +0.8% | Global, with concentration in North America, Europe, and India | Short term (≤ 2 years) |

| Growing Global Population | +0.7% | Global, with emphasis on Asia-Pacific, Sub-Saharan Africa, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU-Ukraine Reconstruction Demand Spike

The World Bank’s ARISE facility has channelled USD 700 million into farm machinery recovery, aimed at reaching over 90,000 farmers and accelerating orders for high-horsepower tractors that ship with premium radials[1]"Ukraine Agriculture Recovery Inclusive Support Emergency (ARISE) Project (P180732)", World Bank, worldbank.org. Suppliers are reallocating European plant capacity toward IF/VF sizes as cleared acreage returns to grain, sunflower, and rapeseed. Dealers report that tires are among the first consumables replaced when equipment is rebuilt after being destroyed, pushing OEM backlogs higher. Logistics corridors reopened as damaged rail lines were restored, shortening delivery cycles for finished tires and raw materials. The spike is expected to taper after 2027 as the replacement wave normalizes.

Mechanization Momentum in Emerging Economies

Brazilian tractor output is projected to rise after government credit lines revived capital spending on large planters and sprayers. In India, subsidy tweaks and a good monsoon are lifting sentiment, although penetration remains below half of arable land. Chinese cooperatives are pooling plots to justify investments in 100-plus-HP tractors that need larger-diameter radials. Fleet renewal also drives demand, as tractors bought during the 2010-2015 surge are now due for their first tire change. As mechanization progresses, the agricultural tires market benefits from a structural rise in average rim size and load index.

Shift From Bias to Radial / IF-VF Tires

Farmers who switch from bias to radial report smoother rides and fuel savings, while those adopting IF/VF gain extra flotation at lower inflation. Field trials published by Michelin showed significant improvements, with VF tires reducing soil compaction. OEMs have begun factory-fitting IF/VF on premium tractors, making such specifications standard on machines above 200 HP. Price gaps between standard radials and entry-level VF options are narrowing as mid-tier brands launch hybrid constructions. This transition underpins the value growth of the agricultural tires market even when unit volumes plateau.

Real-Time Tire-Pressure and CTIS Adoption

John Deere integrates CTIS interfaces on many 9-series tractors, letting growers deflate for field work then reinflate for road transport without leaving the cab. Early adopters report up to 30% less slip in moist soils and measurable fuel savings. Telematics bundles now stream tire pressure to cloud dashboards, enabling predictive maintenance and automated alerts. Although the upfront cost remains significant, payback periods are compressing as fuel prices remain high and downtime tolerance on large farms declines. Retrofit kits are entering the aftermarket, widening the addressable base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost Volatility | -0.5% | Global, with acute impact in Asia-Pacific production hubs (Thailand, Indonesia, India) | Short term (≤ 2 years) |

| Fluctuating Commodity Prices | -0.4% | Global, with concentration in North America (corn, soybeans) and South America (soybeans, coffee) | Medium term (2-4 years) |

| Supplier Exits Limiting Choice | -0.3% | Europe (Continental exit), with spillover to global OEM supply chains | Short term (≤ 2 years) |

| Rubber-Leaf Disease | -0.2% | Southeast Asia (Thailand, Indonesia, Vietnam, Malaysia), with global supply-chain ripple effects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Natural-Rubber and Petrochemical Cost Swings

Plant disease outbreaks in Thailand and Indonesia cut latex yields, while crude-oil fluctuations lifted synthetic rubber and carbon-black costs. Mid-tier tire makers, lacking sophisticated hedging, pushed through multiple price increases, which some cash-constrained farmers deferred by extending tire life. Natural rubber prices fluctuated annually between 13,550 and 17,400 CNY (USD 1,960-2,516.91) per ton in 2025[2]"Natural Rubber Prices Fluctuated Downward in 2025, Bottom Support Exists in 2026 with a Slight Shift Upward in Price Focus", ECHEMI, echemi.com. Larger manufacturers accelerated sustainable-rubber pilot programs to lower exposure, but commercialization will take time. The restraint is cyclical yet recurs often enough to influence contracting strategies and inventory buffers throughout the agricultural tires market.

Commodity-Price Volatility Affecting Farm Income

Crop prices slipped from 2023 peaks, compressing cash flows and causing growers to postpone non-essential tire purchases. Equipment sales in North America showed double-digit declines in high-horsepower tractor registrations during 2024, directly softening OEM tire call-offs. When margins tighten, growers opt for retreading or running tires longer, shifting mix toward premium, longer-life products, but reducing unit throughput. As monetary policy eases and inventories rebalance, replacement cycles should return to historical averages after 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sales Channel: Aftermarket Dominance Drives Steady Growth

Replacement/Aftermarket tires dominate the agricultural tires market, with a commanding 71.29% share in 2025, reflecting the long operational life of farm equipment and the frequent tire wear cycles under heavy field use. Farmers typically prioritize maintenance to avoid downtime during peak planting and harvest seasons, which drives consistent replacement demand. The aftermarket segment also benefits from expanding rural distribution networks and increasing availability of multi-brand tire options across emerging markets.

Additionally, fluctuations in crop cycles and terrain conditions create steady pull-through demand for new tires, reinforcing the segment’s leadership within the global agricultural tires market. Meanwhile, the OEM channel represents the fastest-growing segment, expanding at a 5.97% CAGR through 2031 as new tractor and harvester sales rise in mechanizing economies. Growth in large-horsepower machinery and precision farming equipment further accelerates OEM tire demand, particularly for advanced tire technologies aligned with new equipment specifications.

By Application: Tractors Lead While Sprayers Accelerate

Tractor tires hold the largest share at 56.73% in 2025, affirming their critical role as the backbone of agricultural machinery worldwide. Tractors require multiple tire configurations for tasks ranging from soil preparation to hauling, making them the single most significant contributor to overall agricultural tire demand. The segment benefits from continuous fleet modernization, growing mechanization in Asia and Africa, and the increasing adoption of high‑traction radial and IF/VF technologies for improved fuel efficiency.

Sprayers form the fastest-growing application segment, expanding at a 6.03% CAGR as precision agriculture intensifies. Modern sprayers require specialized tires with low soil compaction and high flotation, creating demand for advanced radial and VF tires that protect crop yields and enhance field productivity. Harvesters require the largest casings to carry heavy grain tanks through soft soils, leading to premium average selling prices. Implementers such as trailers and telehandlers add incremental demand, especially in mixed farming zones where livestock or materials handling broaden tire-use scenarios. Overall, the application mix gradually tilts the agricultural tires market toward specialized patterns and higher value per unit.

By Tire Construction: Radial Dominance With IF/VF Innovation

Radial tires lead the market with a 53.22% share in 2025, showcasing their strong adoption as farmers prioritize productivity, fuel savings, and better soil protection. Radial agricultural tires offer enhanced tread life, improved ride comfort, and lower rolling resistance, making them the preferred choice for both tractors and high‑horsepower equipment. Their ability to support wider footprints and lower inflation pressures aligns well with the global shift toward precision farming.

As sustainability becomes a priority, radial tires continue gaining traction due to their lower fuel consumption and improved field efficiency. In contrast, IF/VF radial tires are the fastest-expanding construction type, growing at a 6.07% CAGR, owing to their superior load-carrying capacity and ability to operate at lower pressures. These tires support reduced soil compaction, an increasingly important metric in modern farming, making them the premium choice for advanced machinery and large commercial farms.

By Rim-Size: Mid-Range Leadership With Large-Size Growth

The 20 to 30‑inch rim-size category accounts for the largest share in 2025 at 45.51%, aligning with tire dimensions commonly used on mid-sized tractors, loaders, and agricultural trailers. This size range offers a balance of durability, versatility, and traction, making it a staple across small- and medium-sized agricultural operations worldwide. Farmers prefer this category for its affordability, wide availability, and compatibility with diverse terrain conditions. The segment continues to benefit from intense replacement cycles, especially in markets where mid-range tractors dominate fleet populations.

At the same time, the segment above 150 HP is the fastest-growing, expanding at a 6.17% CAGR as large-scale commercial farms adopt high-horsepower machinery to increase productivity. These machines require premium radial and VF tires designed for heavy loads, extended field hours, and advanced traction performance. Farmers operating large-scale farms increasingly rely on these high-horsepower machines to meet the growing demand for agricultural output. The adoption of such equipment not only enhances efficiency but also reduces operational downtime, making it a critical investment for commercial farming operations. As a result, the demand for durable, high-performance tires in this segment is expected to rise steadily, reflecting the evolving needs of modern agriculture.

By Equipment Horse-Power Class: Mid-Range Dominance with High-Power Growth

The 30 to 70 HP equipment class leads the agricultural tire market with a 41.28% share in 2025, supported by the widespread use of mid-sized tractors on small- to medium-sized farms. This horsepower range dominates in India, China, Southeast Asia, and parts of Europe, where versatile utility tractors form the backbone of farming operations. These tractors require frequent tire replacement due to multitasking across cultivation, hauling, and spraying. The segment’s stability reflects the global trend toward mechanization among smallholder farmers, which is contributing significantly to the agricultural tire market's size.

At the same time, the segment above 150 HP is the fastest-growing, expanding at a 6.17% CAGR as large-scale commercial farms adopt high-horsepower machinery to increase productivity. These machines require premium radial and VF tires designed for heavy loads, extended field hours, and advanced traction performance. Farmers operating these high-powered machines are increasingly prioritizing durability and efficiency, as these tires must withstand the demands of modern farming practices. The adoption of such equipment is particularly evident in regions with large-scale farming operations, such as North America and parts of Europe, where maximizing yield and minimizing downtime are critical to profitability.

By Inflation-Technology Compatibility: Standard Tires Lead with Smart Technology Growth

Standard agricultural tires dominate with an 81.26% share in 2025, driven by their affordability, wide availability, and compatibility with the majority of global farm equipment. Farmers in emerging markets continue to prefer standard tires due to cost considerations and familiarity with use. Despite technological advancements, standard tires remain the primary choice for traditional tractors, trailers, and implements where precision inflation systems are not essential. Their strong presence reinforces the stable, price-sensitive nature of agricultural tire demand worldwide.

However, CTIS-ready and smart tires represent the fastest-growing segment, expanding at a 6.23% CAGR as farms adopt CTIS and telematics for real-time pressure monitoring. These advanced tires are transforming the way farmers manage their equipment, offering significant benefits such as reduced soil compaction, improved traction, and optimized fuel efficiency. By enabling farmers to adjust tire pressure based on field conditions, CTIS-ready tires help protect valuable arable land while enhancing productivity. Additionally, integrating telematics and IoT technologies allows predictive maintenance, reducing downtime and operational costs.

Geography Analysis

Asia-Pacific leads the agricultural tires market, capturing 37.83% of revenue share in 2025, driven by a vast fleet that is still modernizing. Government incentives in India and China encourage tractor ownership beyond traditional cereal belts, while Southeast Asian plantations mechanize to offset labor shortages. Farmers in the region often choose bias or basic radials due to price sensitivity, yet awareness of soil compaction is rising as double-cropping intensifies. Local manufacturers meet entry-level needs, but premium brands grow share where high-value horticulture justifies IF/VF investments.

North America and Europe together represent a mature yet sizable slice of the agricultural tire market. Replacement cycles dominate because mechanization is already universal. Farmers here experiment early with CTIS and smart-tire analytics, making these regions incubators for next-gen features. However, cyclical dips in commodity prices or subsidy reforms quickly filter into OEM production schedules, making demand somewhat erratic. Reconstruction in Eastern Europe adds a transient spike as contaminated fields re-enter cultivation, drawing new machinery with premium tire packages into service.

South America records the fastest growth rate of 6.21% to 2031, propelled by Brazil’s soy and corn expansion across the Cerrado and Argentina’s push for scale to hedge export volatility. Credit programs enable upgrades to larger tractors and high-capacity sprayers, thus increasing demand for wider rims and advanced tread patterns. The Middle East and Africa remain smaller in absolute value but offer a long runway. Government-backed food security projects, irrigated desert farming, and donor-funded mechanization schemes slowly raise baseline demand. Distribution challenges and harsh climates put a premium on puncture resistance and heat-tolerant compounds. Over time, as credit access widens, a leapfrog effect could move many buyers straight from bias to smart radials, contributing incremental share to the agricultural tires market.

Competitive Landscape

The agricultural tire industry is moderately concentrated. Bridgestone, Michelin, Goodyear, and Nokian maintain global reach, while BKT, Titan International, and Trelleborg anchor strong regional franchises. Continental’s April 2025 withdrawal opened doors for mid-tier entrants, especially in Europe, and signalled that capital intensity and automotive priorities can reshape participation. Suppliers are investing in proprietary carcass architectures, recycled-rubber blends, and digital diagnostics to differentiate beyond tread depth.

Strategic moves continue. Titan International acquired Carlstar to boost rapid-delivery coverage, a service trait that resonates with dealers facing unpredictable planting windows. Michelin unveiled an automated manufacturing cell that shortens design-to-market time for customized VF sizes. Alliance Tire Group celebrated one million Agri Star II units sold and quickly extended the line to row-crop formats, proving that niche designs can achieve scale. Meanwhile, Brazilian distribution tie-ups by Trelleborg and new influencer-led marketing by Maxam illustrate fresh approaches to reach growers overwhelmed by digital channels.

Technology is the main battleground. Embedded RFID tags improve traceability and warranty service, while data-rich tires feed agronomic algorithms that are now integral to mixed-brand machinery fleets. Sustainability claims also shape positioning, with several incumbents committing to certified natural-rubber sourcing and circular schemes that collect worn casings for retreading or material recovery. The agricultural tires market thus rewards players who can combine manufacturing prowess with ecosystem partnerships.

Agricultural Tires Industry Leaders

-

Michelin

-

Bridgestone Corporation (Firestone)

-

Titan International Inc. (Goodyear Tires)

-

BKT Tires

-

Continental AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Trelleborg Tires took the stage at Agritechnica 2025, rolling out the TM200 Progressive Traction. Tailored for niche farming needs, this tire melds VF and Progressive Traction technologies, promising 15% more traction, 26% enhanced stability, and a 10% extended lifespan, making it ideal for the meticulous tasks in vineyards and orchards.

- November 2025: Linglong Tire, hailing from China, made its Agritechnica debut, showcasing the Spring Ultra Flex model. Sized at VF 900/60 R32, this combines harvester tire boasts a low-profile tread pattern, expertly crafted to evenly distribute heavy loads.

- October 2025: Bridgestone unveiled its inaugural agro-industrial tire, the VH-IND, engineered for superior traction across diverse surfaces and enhanced load capacity.

- March 2025: Apollo expanded its Vredestein Traxion range for CLAAS tractors, adding sizes optimized for the ARION series to enhance traction and durability.

Global Agricultural Tires Market Report Scope

An agricultural tire is a specialized tire designed for use in farm machinery and equipment, such as tractors, combines, and harvesters. These tires are built to withstand the unique demands of agricultural applications, providing traction, stability, and flotation on various terrains. They are designed with deep treads, reinforced sidewalls, and strong carcasses to handle heavy loads, reduce soil compaction, and improve overall performance in farming operations.

The agricultural tire market is segmented by sales channel, application, tire construction, rim size, equipment horsepower class, inflation-technology compatibility, and geography. By sales channel, the market is segmented into OEM and Replacement/Aftermarket. By application, the market is segmented into Tractors, Combine Harvesters, Sprayers, Trailers, Loaders & Telehandlers, and Other Implements. By tire construction, the market is segmented into Bias, Radial, and IF/VF Radial. By rim size, the market is segmented into Less than 20 inches, 20 to 30 inches, 30 to 40 inches, and More than 40 inches. By equipment horsepower class, the market is segmented into Less than 30 HP, 30 to 70 HP, 71 to 150 HP, and More than 150 HP. By inflation-technology compatibility, the market is segmented into Standard Tires and CTIS-Ready/Smart Tires. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

By Sales Channel

| OEM |

| Replacement / Aftermarket |

By Application

| Tractors |

| Combine Harvesters |

| Sprayers |

| Trailers |

| Loaders & Telehandlers |

| Other Implements |

By Tire Construction

| Bias |

| Radial |

| IF / VF Radial |

By Rim-Size

| Less than 20 inch |

| 20 to 30 inch |

| 30 to 40 inch |

| More than 40 inch |

By Equipment Horse-Power Class

| Less than 30 HP |

| 30 to 70 HP |

| 71 to 150 HP |

| More than 150 HP |

By Inflation-Technology Compatibility

| Standard Tires |

| CTIS-Ready / Smart Tires |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Sales Channel | OEM | |

| Replacement / Aftermarket | ||

| By Application | Tractors | |

| Combine Harvesters | ||

| Sprayers | ||

| Trailers | ||

| Loaders & Telehandlers | ||

| Other Implements | ||

| By Tire Construction | Bias | |

| Radial | ||

| IF / VF Radial | ||

| By Rim-Size | Less than 20 inch | |

| 20 to 30 inch | ||

| 30 to 40 inch | ||

| More than 40 inch | ||

| By Equipment Horse-Power Class | Less than 30 HP | |

| 30 to 70 HP | ||

| 71 to 150 HP | ||

| More than 150 HP | ||

| By Inflation-Technology Compatibility | Standard Tires | |

| CTIS-Ready / Smart Tires | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the agricultural tires market today and where is it heading by 2031?

It is valued at USD 9.11 billion in 2026 and is projected to reach USD 12.12 billion by 2031, growing at a 5.86% annually.

Which equipment type drives the most tire demand?

Tractors led the volume share because every mechanized farm has at least one, whereas sprayers currently log the quickest growth.

Why are IF/VF radials attracting attention?

They carry the same load at lower pressure, cutting soil compaction and sometimes lifting yields, benefits proven in field trials.

What factors limit faster adoption of smart tires?

Upfront cost for CTIS hardware, the need for onboard air compressors, and limited integration with older tractors remain key hurdles.

How volatile are raw-material costs for tire makers?

Natural-rubber supply still swings with disease outbreaks and weather, while synthetic rubber tracks crude-oil prices, periodically squeezing margins.

Page last updated on: