Electric Vehicle Telematics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

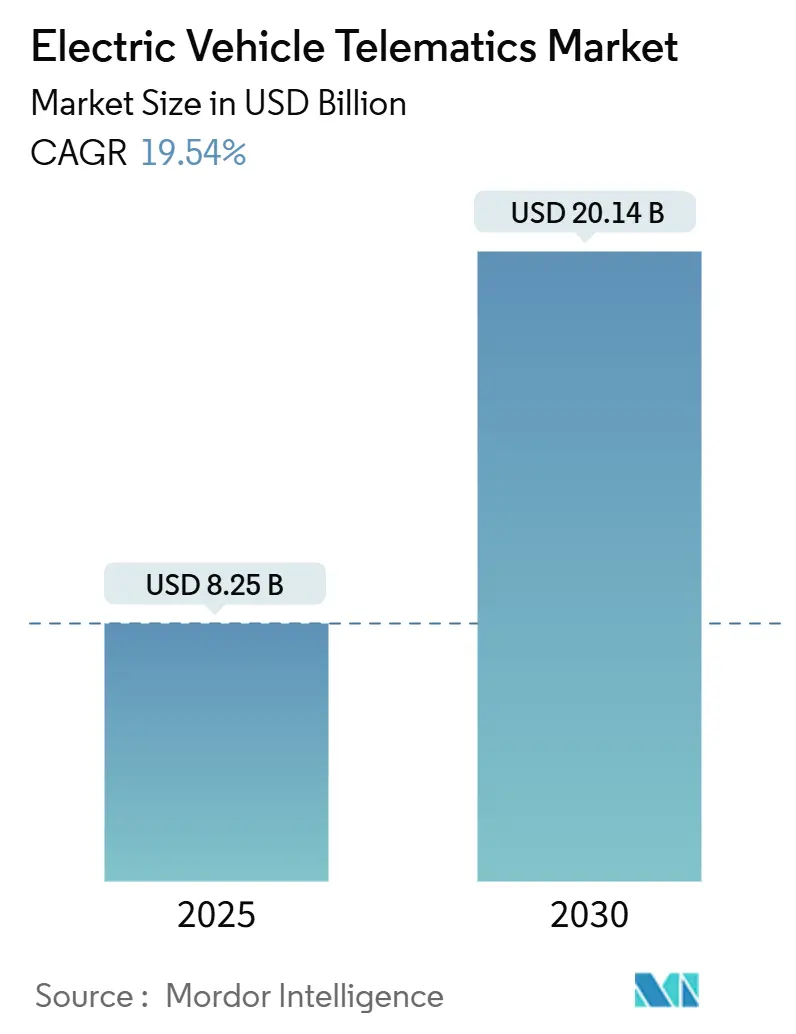

| Market Size (2025) | USD 8.25 Billion |

| Market Size (2030) | USD 20.14 Billion |

| Growth Rate (2025 - 2030) | 19.54% CAGR |

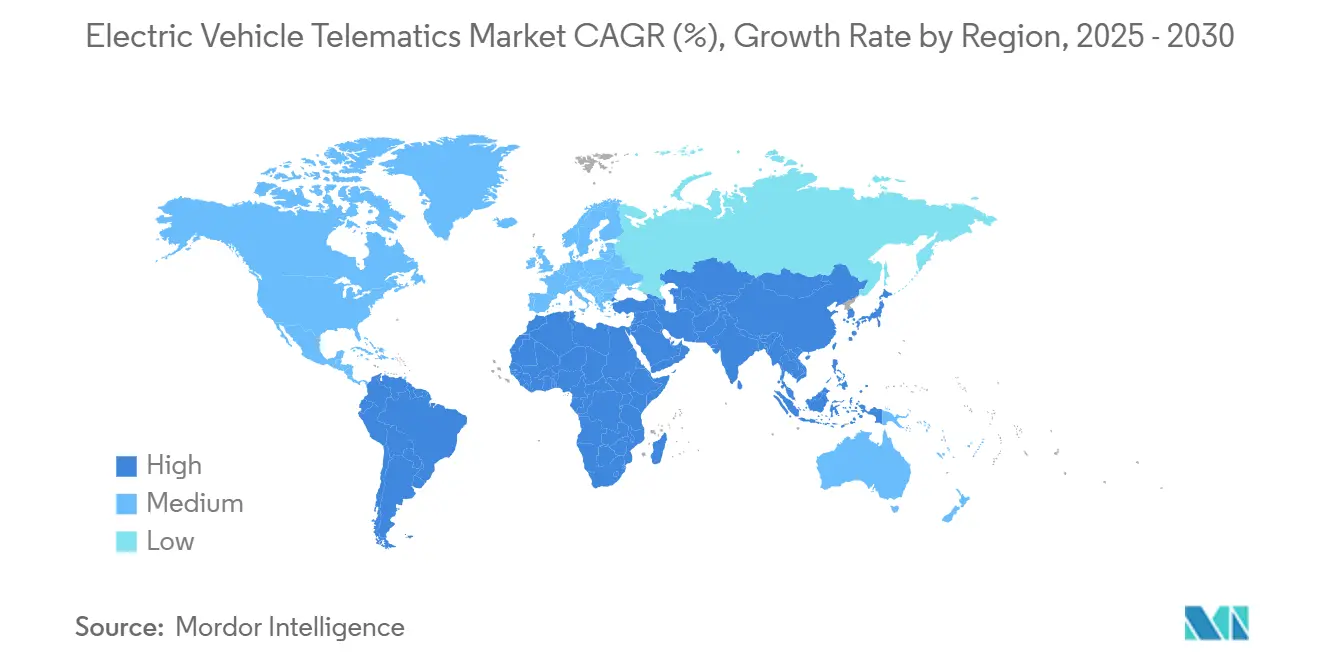

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Electric Vehicle Telematics Market Analysis by Mordor Intelligence

The electric vehicle telematics market size is valued at USD 8.25 billion in 2025 and is projected to reach USD 20.14 billion by 2030, reflecting a robust 19.54% CAGR through the forecast period. Mandatory eCall compliance, rapid 5G TCU cost declines, and artificial-intelligence-based fleet optimization continue to expand addressable demand. Government regulations require 4G/5G-ready emergency-call capability in new electric vehicles across the European Union by 2026–2027, effectively creating a hardware foundation for advanced data-logging and remote diagnostics[1]"EU eCall Regulations Updated to Require 4G/5G Compliant Systems", InterRegs Ltd., interregs.com. Commercial fleet operators accelerate adoption to cut energy costs, while over-the-air (OTA) software monetization enables recurring revenue streams that reshape automaker economics. Competitive intensity remains moderate as traditional suppliers, technology companies, and niche specialists vie to embed edge-ready modules capable of vehicle-to-everything (V2X) communication.

Key Report Takeaways

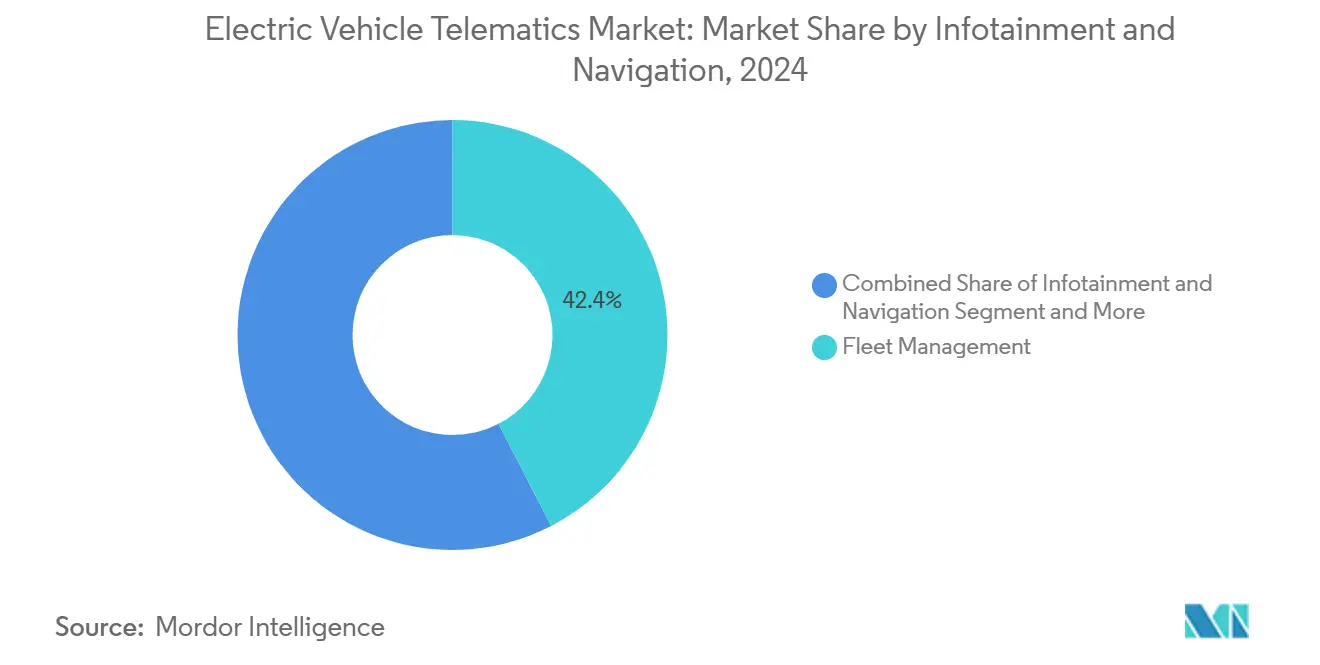

- By service, Fleet Management held 42.41% of the electric vehicle telematics market share in 2024; V2X and OTA Updates are projected to expand at a 24.66% CAGR through 2030.

- By sales channel, OEM-fitted solutions captured 72.54% of the electric vehicle telematics market size in 2024, while the aftermarket channel is forecast to advance at a 20.78% CAGR between 2025 and 2030.

- By connectivity solution, embedded architecture commanded 79.24% share of the electric vehicle telematics market size in 2024; 5G integrated-smartphone solutions will post the fastest 29.88% CAGR to 2030.

- By vehicle type, passenger cars led the electric vehicle telematics market with 69.19% market share in 2024, whereas medium and heavy commercial vehicles are set to grow at a 21.91% CAGR through 2030.

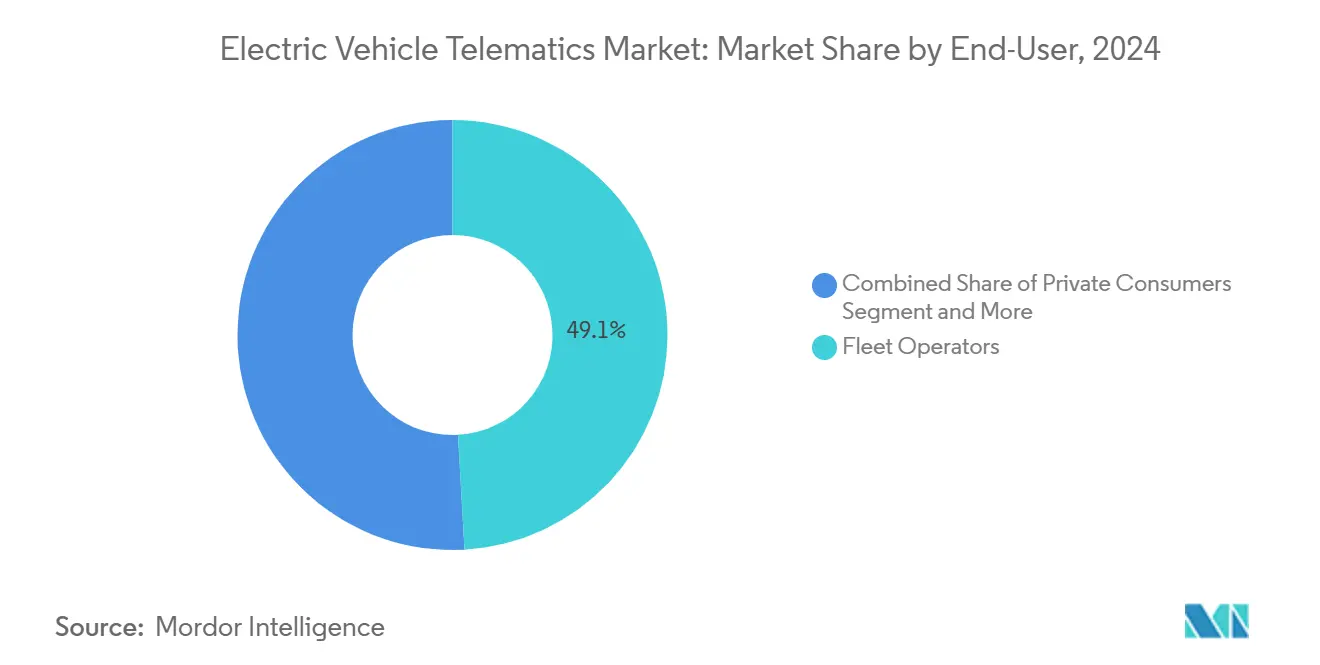

- By end-user, fleet operators accounted for 49.11% of the electric vehicle telematics market share in 2024; car-sharing and mobility providers should experience a 27.63% CAGR to 2030.

- By propulsion type, battery electric vehicles represented 73.66% of the electric vehicle telematics market size in 2024, while fuel cell electric vehicles will record the quickest 27.12% CAGR during the forecast horizon.

- By geography, Asia-Pacific held 43.53% of the electric vehicle telematics market share in 2024, while the Middle-East and Africa region is expected to post the fastest CAGR of 20.06% by 2030.

Global Electric Vehicle Telematics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| eCall and Data-Logging | +4.2% | Europe, North America, APAC core | Medium term (2-4 years) |

| OTA Software Monetization | +3.8% | Global, with early gains in North America, China | Short term (≤ 2 years) |

| Predictive Maintenance | +3.1% | North America, Europe, China | Medium term (2-4 years) |

| Semiconductor Cost Decline | +2.9% | Global | Short term (≤ 2 years) |

| Usage-Based Insurance | +2.4% | Europe, North America | Long term (≥ 4 years) |

| V2G Communication | +2.1% | Europe, California, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Mandates for eCall and Data-Logging in EVs

Mandatory emergency-call compatibility upgrades from 2G/3G to 4G/5G enforce universal telematics hardware in new battery-electric vehicles in the electric vehicle telematics market. The legislation embeds continuous vehicle telemetry capabilities, enabling real-time battery health monitoring and predictive maintenance services. China’s parallel intelligence-connected standards and Japan’s Society 5.0 strategy echo Europe’s approach, sustaining multi-regional tailwinds. Automakers now fast-track partnerships with providers with regulatory credentials, accelerating platform standardization. The compliance window locks in baseline demand and positions telematics vendors for service diversification beyond safety features.

OTA Software Monetization Boosts OEM Recurring Revenue

Over-the-air update ecosystems, pioneered by Tesla, turn vehicles into software platforms sold with subscription up-sell potential in the electric vehicle telematics market. Full-vehicle firmware updates unlock performance enhancements and new features post-sale, raising lifetime customer value. Chinese newcomers such as NIO and XPeng report OTA installation rates exceeding 44% in 2024, underscoring rapid scalability. Subscription-ready architectures justify higher upfront telematics hardware costs and reinforce OEM control of data ownership. The resulting annuity streams diminish hardware margin sensitivity, encouraging broader rollout of embedded modules.

AI-Based Predictive Maintenance for Electric Fleets

Machine-learning algorithms applied to telemetry anticipate component failures, reduce unscheduled downtime, and optimize service intervals in the electric vehicle telematics market. Early pilots demonstrate 15–25% lower maintenance outlays by aligning battery state-of-health with fleet duty cycles. Data-science-centric telematics vendors gain competitive edge through proprietary predictive models. Fleet managers translate savings directly into improved total cost of ownership, reinforcing adoption across high-utilization commercial segments.

Semiconductor Cost Decline Enables Embedded 5G TCUs

Automotive-grade 5G system-on-chip designs now integrate edge processing, reducing bill-of-materials cost and form factor in the electric vehicle telematics market. HARMAN’s 5G-ready TCU platform exemplifies maturity, supporting low-latency V2X and cloud-native services. Mass production in Asia accelerates price compression, letting automakers specify embedded connectivity as standard equipment. Hardware standardization spurs scale economies and unlocks advanced use cases such as edge-hosted artificial-intelligence inferencing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-Security Vulnerabilities | -2.8% | Global, with stricter enforcement in Europe | Short term (≤ 2 years) |

| High Upfront HW Cost | -2.1% | South America, Africa, Southeast Asia | Medium term (2-4 years) |

| Data-Privacy Rules | -1.6% | Europe, California, emerging in APAC | Long term (≥ 4 years) |

| Chipset Supply Constraints | -1.4% | Global, with acute impacts in North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cyber-Security Vulnerabilities and Rising Regulation

High-profile hacks erode consumer confidence and trigger stringent compliance mandates in the electric vehicle telematics market. UNECE WP.29 R155 and R156 now compel end-to-end cybersecurity management systems in all connected vehicles[2]“UN Regulation No. 155 – Cyber Security and Cyber Security Management System,” United Nations Economic Commission for Europe, UNECE.ORG. The ISO/SAE 21434 standard adds further engineering workload. OEMs and suppliers must allocate additional resources to threat detection, patch management, and third-party audits. Smaller vendors face entry barriers owing to security certification costs, while deployment timelines elongate as regulatory reviews intensify.

High Upfront HW Cost in Price-Sensitive Regions

Automotive-grade 5G TCUs remain costly relative to consumer electronics in the electric vehicle telematics market. Emerging markets where electric vehicle adoption hinges on price parity struggle to justify premium embedded modules. Import duties and limited local manufacturing further inflate unit economics. Aftermarket devices provide stop-gap solutions yet lack full integration, hampering advanced use-case activation. Subsidy programs and localized production are required to bridge affordability gaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Fleet Management Optimizes Mixed Deployments

Fleet Management held 42.41% of the electric vehicle telematics market share in 2024. Commercial operators leverage telematics dashboards to orchestrate charging schedules, track battery state-of-health, and monitor driver behavior. The electric vehicle telematics market size for Fleet Management is projected to climb alongside corporate electrification mandates, while energy-cost volatility elevates optimization value. V2X and OTA Updates spearhead expansion at a 24.66% CAGR to 2030, mirroring the transition to software-defined architectures.

Infotainment and Navigation sustain demand among private consumers seeking smartphone-like experiences. Fleet managers quantify savings through lower energy cost per mile and reduced unplanned maintenance. Diagnostics and Prognostics services integrate AI models that predict component wear, extending asset life. Insurance telematics merges carbon-linked policies with usage data, offering tangible premium reductions. Service convergence favors end-to-end platforms capable of harmonizing disparate data streams into a unified control pane.

By Sales Channel: OEM Integration Dominates Factory Fitment

OEM-fitted solutions accounted for 72.54% of the electric vehicle telematics market size 2024 as automakers embedded connectivity at the production line. The embedded approach enables deeper integration with vehicle systems and eliminates compatibility issues that plague aftermarket installations. Aftermarket demand still posts a 20.78% CAGR through 2030, propelled by existing fleet retrofits. The market share of electric vehicle telematics captured by aftermarket providers remains niche yet important for budget-constrained operators.

OEM channel strength reflects strategic acquisitions, such as Continental’s purchase of Motorola’s automotive electronics unit, strengthening the company's position in OEM-fitted telematics solutions. Retrofit kits focus on quick install times and monthly subscription models that lower upfront outlay. Aftermarket solutions remain relevant for commercial fleets seeking to upgrade existing vehicles without replacement costs. Regulatory harmonization could eventually obligate factory-fit telematics even in price-sensitive segments, gradually narrowing the aftermarket scope.

By Connectivity Solution: Embedded Architecture Prevails

Embedded connectivity commanded 79.24% electric vehicle telematics market share in 2024. Automakers prefer eSIM-based modules that guarantee consistent network performance and cradle OTA pipelines. The electric vehicle telematics market size associated with embedded solutions gains from 5G-capable chipsets that enable real-time V2X communication. Integrated-smartphone architectures post the fastest 29.88% CAGR, leveraging consumer device familiarity and app ecosystems.

Telecom operators champion global eSIM provisioning platforms like Deutsche Telekom’s AirOn360® to offer seamless roaming and over-the-air profile swaps. Tethered and Portable solutions serve niche applications where permanent vehicle modification is impractical or cost-prohibitive. The connectivity architecture choice influences telematics service capabilities, with embedded solutions enabling the most comprehensive feature sets but requiring higher upfront investments.

By Vehicle Type: Passenger Cars Lead, Commercial Fleets Accelerate

Passenger Cars held a 69.19% share of the electric vehicle telematics market in 2024, as early adopters demanded remote charging control and connected infotainment. Commercial Medium and Heavy Vehicles registered the swiftest 21.91% CAGR, reflecting quantifiable ROI from uptime optimization. The commercial truck electric vehicle telematics market size will rise as zero-emission zones proliferate in major logistics corridors.

Passenger cars, SUVs, and MPVs demonstrate strong adoption of telematics due to higher average selling prices that can absorb telematics hardware costs. Light Commercial Vehicles bridge consumer and comm ercial applications, with small business operators seeking basic fleet management capabilities at consumer price points. Two-wheelers create emerging data monetization avenues in dense Asian cities. OEM and fleet operator collaboration will shape application priorities, particularly around battery life extension and route planning.

By End-User: Fleet Operators Anchor Demand

Fleet Operators represented 49.11% of the electric vehicle telematics market share in 2024. Telematics enable route optimization, driver coaching, and energy-cost forecasting at scale. Car-Sharing and Mobility Providers will log a 27.63% CAGR through 2030, driven by real-time vehicle availability tracking and automated billing. Private Consumers represent a significant but price-sensitive segment that prioritizes convenience features over comprehensive fleet management capabilities.

Insurance and Leasing Firms increasingly adopt telematics solutions to monitor asset condition and driver behavior for risk assessment and pricing optimization. OEMs partner with telematics specialists to embed fleet management APIs directly into vehicle dashboards, streamlining enterprise connectivity onboarding. The electric vehicle telematics market size in the fleet domain benefits from corporate sustainability targets and total-cost-of-ownership imperatives.

By Propulsion Type: BEVs Dominate, Fuel Cells Advance

Battery Electric Vehicles accounted for 73.66% of the electric vehicle telematics market share in 2024, owing to complex battery monitoring needs. Fuel Cell Electric Vehicles will exhibit a 27.12% CAGR, driven by heavy-duty fleet pilots in logistics hubs. The electric vehicle telematics market size linked to Plug-in Hybrids and Hybrids depends on dual-powertrain optimization software that balances combustion and electric modes.

BEVs benefit from integrated telematics architectures that monitor battery state-of-health, optimize charging schedules, and provide real-time range estimates based on driving conditions. Emerging hydrogen corridors in Europe and California create fresh data requirements around fuel-cell diagnostics and range prediction. Cross-propulsion analytics will grow in importance as mixed fleets become commonplace.

Geography Analysis

Asia-Pacific retained a 43.53% share of the global electric vehicle telematics market in 2024, powered by China’s rapid electrification and intelligent-connected vehicle mandates. The electric vehicle telematics market size in the region rises as public procurement quotas require a significant number of new-energy vehicles, guaranteeing baseline demand for embedded modules. Japan’s 5G coverage milestones and South Korea’s network densification propel advanced V2X pilots. Throttled by supply-chain disruptions, regional OEMs still prioritize factory-integrated TCUs to comply with cybersecurity directives. Commercial fleets leverage dense urban charger networks to pilot predictive maintenance algorithms, further cementing platform adoption.

The Middle East and Africa chart the fastest 20.06% CAGR to 2030. Early adopters in the United Arab Emirates deploy telematics to mitigate extreme-temperature battery degradation, while South Africa’s metropolitan smart-mobility plans bundle telematics with charging-station build-outs. Sparse rural infrastructure amplifies the value of range prediction and real-time charger availability data. Government diversification away from hydrocarbons underpins multi-year incentive schemes that subsidize 5G-ready devices. Start-ups supply ruggedized hardware rated for sand, heat, and vibration, differentiating through hardware resilience.

North America and Europe posted steady growth rates in 2024. Mature regulatory frameworks focus on cyber-security and data-privacy compliance. UNECE R155/R156 adoption in Europe forces suppliers to obtain third-party security certification before launch. U.S. commercial fleets leverage tax credits to justify premium telematics packages that integrate depot-energy management. South America, with Brazil and Chile issuing tax incentives for electric buses and delivery vans. Aftermarket dongles thrive in price-sensitive segments, yet rising fuel-cost volatility nudges operators toward more capable embedded units.

Competitive Landscape

The Electric Vehicle (EV) Telematics Market is moderately fragmented, reflecting a dynamic mix of legacy automotive suppliers, emerging tech firms, and specialized telematics providers competing across different value chain layers. Traditional OEMs increasingly integrate telematics into their platforms, while tech companies bring advanced data analytics and cloud-based services. Tesla stands out with its vertically integrated architecture, enabling seamless over-the-air (OTA) updates that have become industry benchmarks. This capability allows Tesla to rapidly deploy software enhancements, diagnostics, and feature upgrades without physical intervention.

Strategic positioning centers on integrating secure connectivity, edge intelligence, and monetizable data pipelines. Suppliers differentiate by offering turnkey stacks spanning hardware, middleware, cloud analytics, and compliance toolkits. Partnerships flourish: telecom carriers provide eSIM lifecycle management, cyber-security firms supply penetration-testing services, and AI specialists contribute predictive-maintenance algorithms. Vendors capable of harmonizing these disciplines capture wallet share among OEMs transitioning to software-defined vehicles.

Niche opportunities emerge in vehicle-to-grid energy trading, carbon-indexed insurance telematics, and in-cab driver behavior analytics. Chinese chipset makers accelerate cost reduction, challenging incumbent silicon suppliers. Consolidation is likely as mid-tier players seek scale to fund UNECE cyber-security compliance and AI-model training. Market concentration remains in flux as new entrants exploit white spaces while established brands extend portfolios through mergers or joint ventures.

Electric Vehicle Telematics Industry Leaders

-

Continental AG

-

Tesla Inc.

-

Harman International (Samsung)

-

Robert Bosch GmbH

-

Geotab Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Siemens introduces Depot360 in the United States, harnessing vehicle-level telematics to automate home-charging reimbursement.

- January 2025: Samsara and Stellantis launch built-in telematics for commercial electric vehicles, enabling factory-integrated fleet management.

- January 2025: PURE EV unveils X Platform 3.0 with AI-driven controls and real-time connectivity.

Global Electric Vehicle Telematics Market Report Scope

| Infotainment and Navigation |

| Fleet Management |

| Safety and Security |

| Diagnostics and Prognostics |

| Insurance Telematics |

| V2X and OTA Updates |

| OEM-fitted |

| Aftermarket |

| Embedded |

| Integrated-Smartphone |

| Tethered / Portable |

| Two-Wheelers | |

| Passenger Cars | Hatchbacks |

| Sedans | |

| SUVs and MPVs | |

| Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles |

| Private Consumers |

| Fleet Operators |

| Insurance and Leasing Firms |

| Car-Sharing and Mobility Providers |

| Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Service | Infotainment and Navigation | |

| Fleet Management | ||

| Safety and Security | ||

| Diagnostics and Prognostics | ||

| Insurance Telematics | ||

| V2X and OTA Updates | ||

| By Sales Channel Type | OEM-fitted | |

| Aftermarket | ||

| By Connectivity Solution | Embedded | |

| Integrated-Smartphone | ||

| Tethered / Portable | ||

| By Vehicle Type | Two-Wheelers | |

| Passenger Cars | Hatchbacks | |

| Sedans | ||

| SUVs and MPVs | ||

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By End-User | Private Consumers | |

| Fleet Operators | ||

| Insurance and Leasing Firms | ||

| Car-Sharing and Mobility Providers | ||

| By Propulsion Type | Battery Electric Vehicle (BEV) | |

| Hybrid Electric Vehicle (HEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the electric vehicle telematics market in 2030?

The market is forecast to reach USD 20.14 billion by 2030, expanding at a 19.54% CAGR.

Which service segment currently holds the largest share?

Fleet Management services lead with 42.41% share in 2024.

Which connectivity architecture dominates new electric vehicle models?

Embedded solutions commanded 79.24% market share in 2024 owing to factory integration and eSIM provisioning.

Which region will grow the fastest through 2030?

The Middle East and Africa are projected to post the highest 20.06% CAGR.

How do OTA updates benefit automakers financially?

OTA capabilities convert vehicles into subscription platforms, unlocking recurring revenue post-sale while reducing recall costs.

What is the main cyber-security regulation affecting telematics providers in Europe?

UNECE WP.29 Regulation 155 mandates end-to-end cyber-security management systems for all connected vehicles.

Page last updated on: