Passenger Vehicle Telematics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

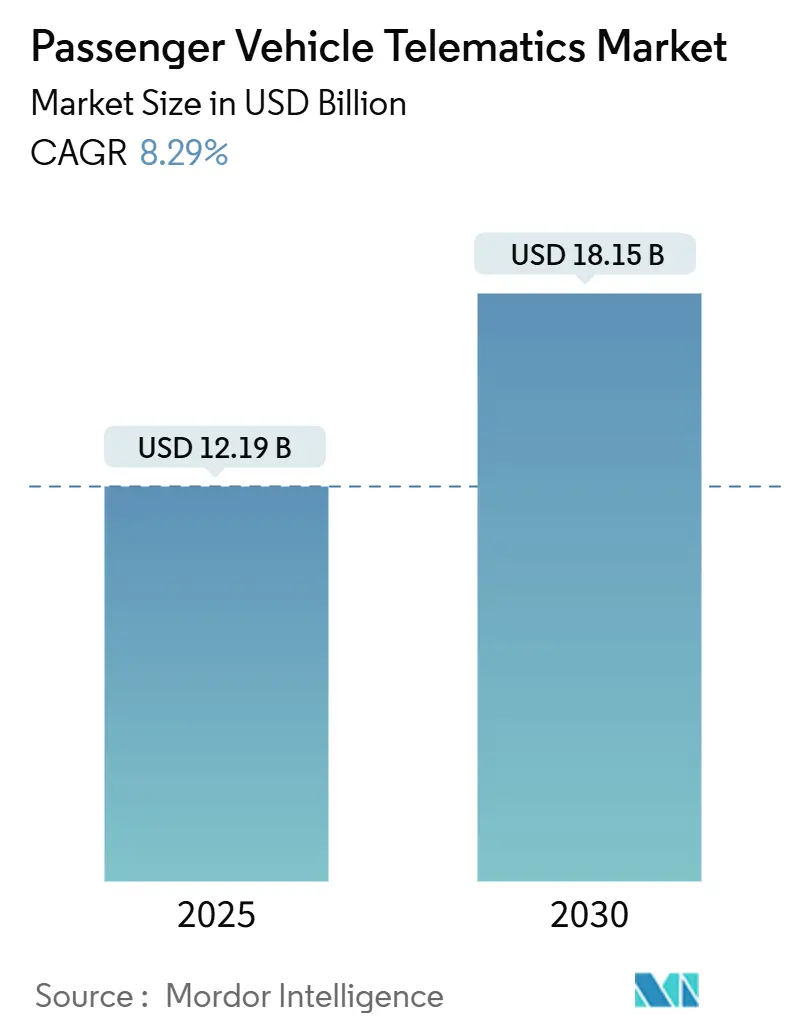

| Market Size (2025) | USD 12.19 Billion |

| Market Size (2030) | USD 18.15 Billion |

| Growth Rate (2025 - 2030) | 8.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Passenger Vehicle Telematics Market Analysis by Mordor Intelligence

The passenger vehicle telematics market size reached USD 12.19 billion in 2025 and is projected to reach USD 18.15 billion by 2030 with an expected CAGR of 8.29% during the forecast period (2025-2030). This outlook reflects the mandatory shift from connectivity-as-convenience to connectivity-as-compliance as regulatory eCall mandates embed telematics deep within vehicle safety architectures. Growth stems from original-equipment-manufacturer (OEM) strategies that transform data streams into recurring revenue through over-the-air (OTA) updates. Increasing fleet-operator demand for cost optimization, rising consumer expectations for connected-infotainment, and accelerating smart-city investments further reinforce expansion across the passenger vehicle telematics market. Fragmented competition and converging hardware–software stacks encourage consolidation, while emerging service niches, such as digital-twin integrations, create new white-space opportunities.

Key Report Takeaways

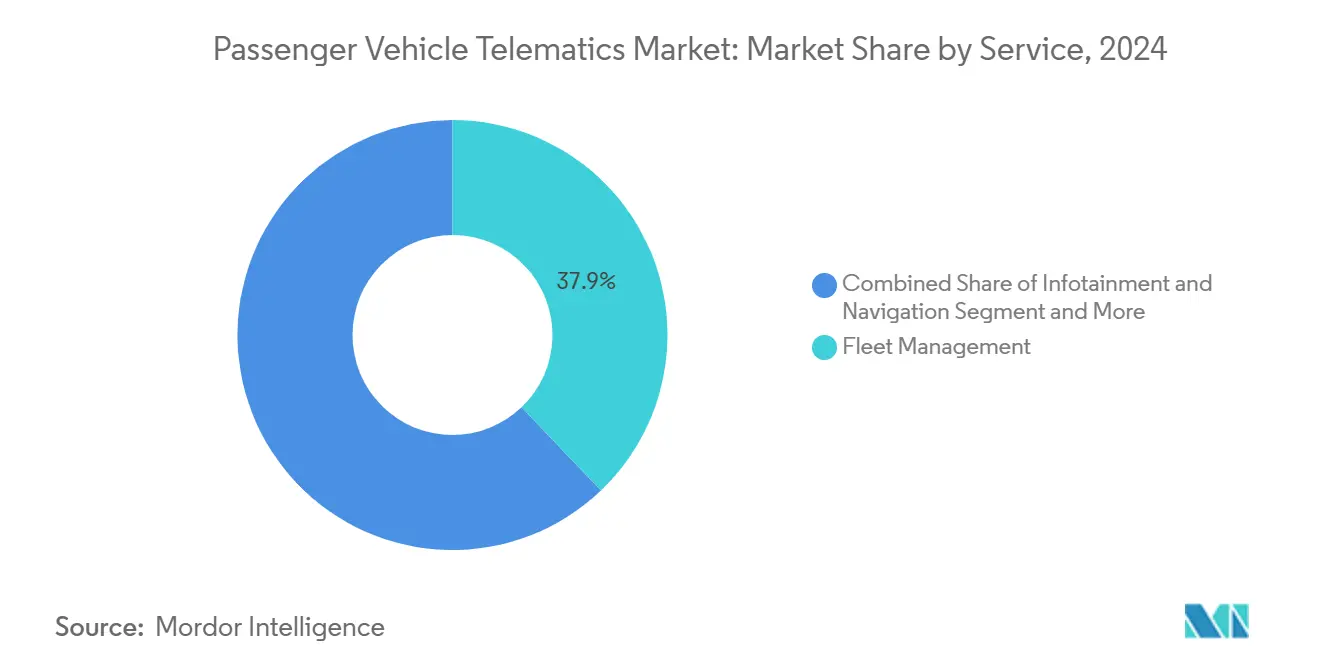

- By service, fleet management led with a 37.87% share in the passenger vehicle telematics market in 2024; insurance telematics is expected to grow at an 11.39% CAGR during the forecast period (2025-2030).

- By sales channel, OEM-fitted solutions dominated the passenger vehicle telematics market with a 75.73% share in 2024, while the aftermarket is forecast to grow at a 10.29% CAGR during the forecast period (2025-2030).

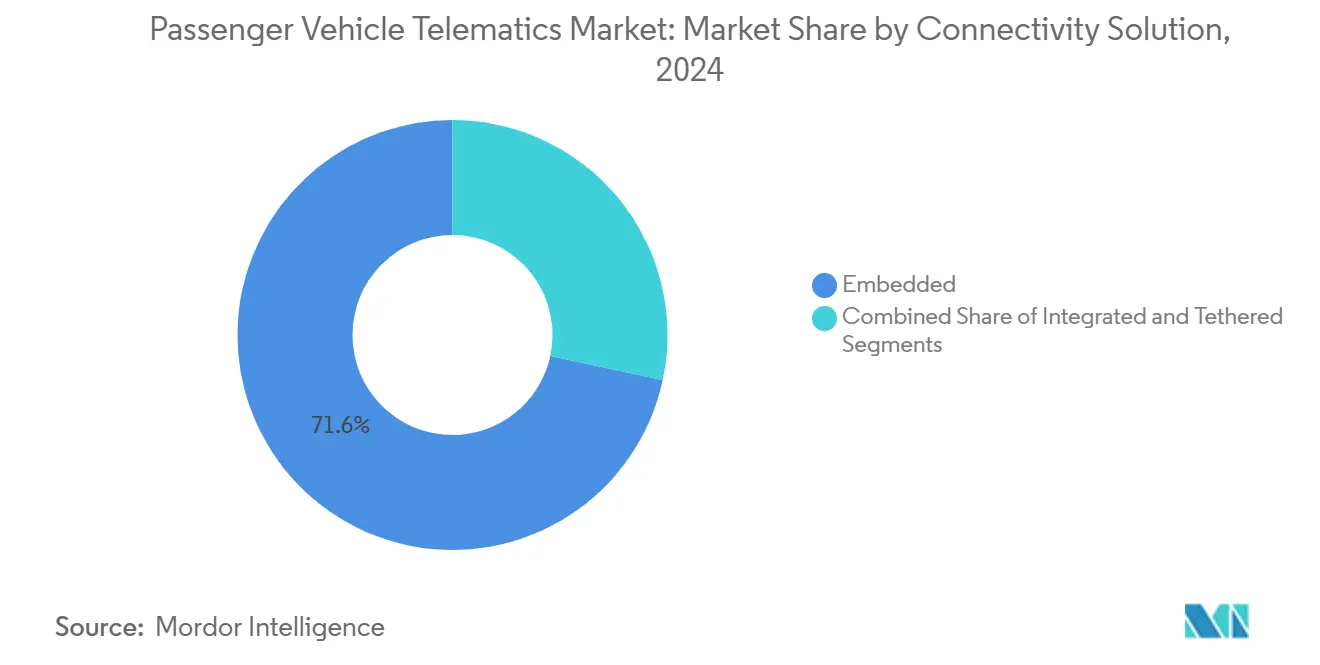

- By connectivity solution, embedded systems commanded a 71.64% share in the passenger vehicle telematics market in 2024, yet integrated smartphone platforms are projected to rise at a 12.68% CAGR during the forecast period (2025-2030).

- By end user, fleet operators accounted for a 41.96% share of the passenger vehicle telematics market in 2024; car-sharing and mobility providers are expected to grow at a 12.49% CAGR during the forecast period (2025-2030).

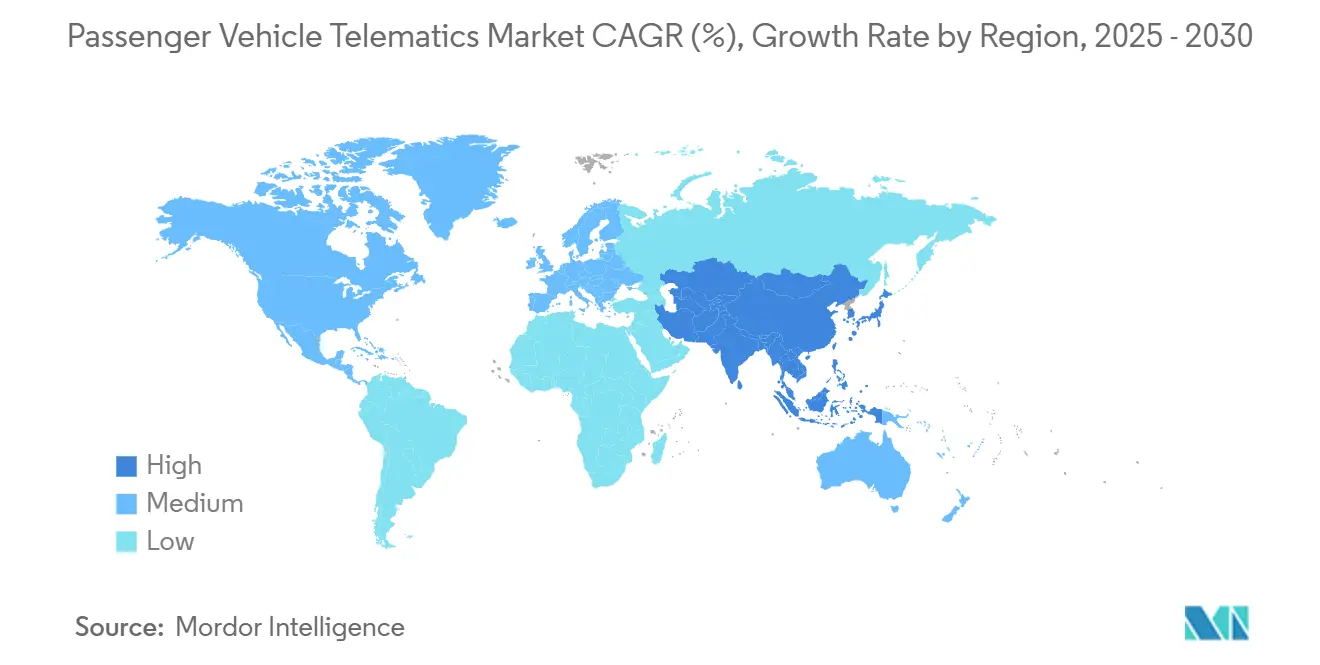

- By geography, North America led the passenger vehicle telematics market share in 2024, capturing 35.82% as the Asia-Pacific is expected to grow at an 8.44% CAGR during the forecast period (2025-2030).

Global Passenger Vehicle Telematics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| eCall Mandates and Safety Compliance | +1.5% | Europe, North America, expanding to APAC | Medium term (2-4 years) |

| Connected-Infotainment Demand | +1.4% | Global, with premium adoption in North America & Europe | Short term (≤ 2 years) |

| Embedded Connectivity and OTA Monetization | +1.2% | Global, led by North America & Europe | Long term (≥ 4 years) |

| Fleet Cost-Optimization | +1.1% | Global, with early adoption in North America | Medium term (2-4 years) |

| Usage-Based-Insurance (UBI) Tie-ins | +0.9% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Digital-Twin Data Integration | +0.7% | APAC core, spill-over to Europe & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory eCall Mandates and Safety Compliance

Mandatory eCall regulations in the European Union require every new passenger vehicle to carry automated emergency-calling functionality, effectively installing a baseline telematics module across all model lines[1]“Revision of the EU General Safety Regulation,” TÜV SÜD, tuv-sud.com. New General Safety Regulation provisions widen the scope to event-data recorders and driver-monitoring systems, compelling OEMs to integrate multi-function telematics platforms rather than isolated systems. Comparable rules in North America reinforce the trend, and Asia-Pacific policymakers are drafting similar requirements, turning telematics from an optional feature into a compliance obligation. As new heavy-vehicle mandates roll out in 2026, technology suppliers are scaling production to meet embedded demand, locking in long-term growth for the passenger vehicle telematics market. Automakers now use unified telematics architectures to streamline certification, shorten validation cycles, and support future OTA upgrades, ensuring that compliance investments also deliver monetization potential.

Connected-Infotainment Demand Surge

Consumer expectations now place seamless digital experiences alongside horsepower and fuel economy when assessing new vehicles. Always-on streaming, real-time navigation, and voice-assistant support require dependable in-vehicle data links, steering automakers toward embedded connectivity that outperforms tethered smartphones in coverage consistency. Integrated app stores and subscription bundles transform dashboards into revenue centers, encouraging continuous software refreshes that extend post-sale customer engagement. As 5G rollout widens bandwidth, OEM-hosted marketplaces for music, video, and cloud-gaming services are multiplying, driving further adoption of embedded modems. Premium brands have already demonstrated higher residual values for models offering robust infotainment ecosystems, incentivizing mainstream manufacturers to follow suit. These dynamics reinforce steady demand for connected services across every segment of the passenger vehicle telematics market.

OEM Push for Embedded Connectivity and OTA Monetization

Transitioning from hardware-centric production to software-defined vehicles lets automakers monetize features throughout ownership lifecycles. OTA upgrades enable paid unlocks of performance modes, advanced driver-assistance functions, and personalized interface themes, converting vehicles into platforms for continuous digital sales. Continental’s 2025 spin-off of its Aumovio software unit signals how Tier-1 suppliers are reorganizing to capture higher-margin recurring revenue from cloud-delivered services[2]“Continental Completes Aumovio Spin-Off,” Continental, continental.com. Centralized data architectures ensure that vehicle telemetry supports predictive maintenance, usage-based insurance partnerships, and data-licensing deals. Automakers that master secure OTA pipelines gain agility in rolling out safety patches and feature enhancements, tightening brand loyalty, and enabling differentiated pricing beyond the showroom. This strategic shift strengthens the structural growth path of the passenger vehicle telematics market.

Fleet Cost-Optimization Needs

Rising fuel prices, driver shortages, and tight delivery windows push commercial operators to lean on data-driven efficiency tools. Modern telematics suites integrate fuel-economy coaching, predictive maintenance, and dynamic routing into a unified dashboard, shrinking the total cost of ownership. Telematics adoption showcases documented fuel savings, leading to swift purchasing decisions due to evident payback periods[3]“ICTS Supply Chain: Connected Vehicles (Proposed Rule),” U.S. Department of Commerce, regulations.gov. Predictive analytics flag engine and component health issues, minimizing breakdown risk and unscheduled downtime. Real-time driver-scorecards foster safer habits, further cutting accident-related expenses and insurance premiums. These tangible returns solidify fleet management as the anchor service within the passenger vehicle telematics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hardware and Connectivity Costs | -1.1% | Asia-Pacific emerging markets, South America, Africa | Short term (≤ 2 years) |

| Cyber-Security Concerns | -0.8% | Global, with stricter enforcement in Europe & North America | Medium term (2-4 years) |

| Fragmented Telematics Software Stacks | -0.6% | Global, particularly affecting aftermarket integration | Long term (≥ 4 years) |

| Smartphone-OS Lifecycle Mismatch | -0.4% | Global, affecting consumer segment adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Hardware and Connectivity Costs in Price-Sensitive Regions

Emerging markets' low average transaction prices push automakers to monitor any uptick in bill-of-materials costs closely. Consumers often zero in on sticker prices, making it challenging to justify the added premium of an embedded telematics module in vehicles. Network fees also trend higher where carrier competition is sparse, inflating the total cost of ownership for buyers. Consequently, OEMs limit connectivity to basic SOS functionality or skip it entirely on entry-level trims, slowing penetration of the passenger vehicle telematics market in these geographies. Retrofit aftermarket units deliver partial relief, yet lack deep vehicle integration, reinforcing a two-tier global adoption pattern.

Cyber-Security and Data-Privacy Concerns

High-profile vehicle-hacking demonstrations and stringent privacy laws raise the stakes for secure data management. In July 2024, the European Union activated Regulation No. 155, obliging OEMs to certify cybersecurity management systems and sustain lifetime monitoring. Across the Atlantic, proposed U.S. rules would bar untrusted suppliers from the connected-vehicle chain, forcing costly supply-base audits. These requirements inflate development budgets and extend launch timelines, particularly for smaller vendors. Consumers likewise hesitate to share driving data without transparent governance, making robust encryption and opt-in controls non-negotiable features.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Commercial Efficiency Spurs Fleet Management Dominance

Fleet management services captured 37.87% of the passenger vehicle telematics market share in 2024, reflecting mature adoption by logistics and corporate fleets seeking measurable returns on fuel, maintenance, and safety benchmarks. The sub-sector’s leadership is underpinned by comprehensive dashboards that merge route optimization, driver coaching, and predictive maintenance into a single interface, yielding fast payback periods. Diagnostics and prognostics packages are increasingly bundled into fleet subscriptions, widening value propositions without incremental hardware. Insurance telematics, though smaller, is projected to grow at an 11.39% CAGR during the forecast period (2025-2030), as pay-how-you-drive underwriting gains regulatory and consumer support. Safety and security services retain a steady foothold, anchored by mandatory eCall compliance across major regions.

Fleet operators also demand integrations with enterprise resource planning and warehouse-management systems, creating new middleware opportunities for telematics vendors. Infotainment and navigation solutions face pressure from smartphone app parity, yet OEMs continue to embed premium content services as future revenue generators. Emerging smart-city and V2X offerings form the “other services” category, positioning suppliers for long-run upside as infrastructure digitization scales. Collectively, this diversified service mix sustains robust expansion for the passenger vehicle telematics market.

By Sales Channel: Factory Fitment Leads, Aftermarket Bridges Affordability

OEM-fitted platforms delivered 75.73% of the passenger vehicle telematics market size in 2024, capitalizing on tighter integration, warranty alignment, and streamlined compliance certification. Factory-installed units provide OEMs with end-to-end data ownership, enabling subscription rollouts and OTA revenue long after vehicle delivery. While development timelines are longer, economies of scale and platform re-use across model lines mitigate costs over successive product cycles. In parallel, the aftermarket channel is set to advance at a 10.29% CAGR during the forecast period (2025-2030), fulfilling demand for older fleets and cost-sensitive consumers who cannot justify new-vehicle purchases.

Aftermarket suppliers differentiate through modular plug-and-play form factors and rapid installation services, making them attractive to commercial operators prioritizing uptime. A significant acquisition highlights the industry's push for greater scale and an expanded range of features. Regional compliance schemes now certify certain retrofit devices, bridging gaps where OEM penetration lags. This dual-channel dynamic ensures that the passenger vehicle telematics market addresses the full vehicle lifecycle, from production line to end-of-life.

By Connectivity Solution: Embedded Strength Meets Smartphone Agility

Embedded modems accounted for 71.64% of the passenger vehicle telematics market in 2024, underlining their centrality to safety mandates, OTA functions, and OEM-controlled user experiences. Secure, always-on links enable high-precision positioning, 5G edge-computing, and seamless integration with advanced driver-assistance systems, reinforcing embedded dominance. Nevertheless, integrated-smartphone solutions are forecast to post a 12.68% CAGR during the forecast period (2025-2030), as consumers value familiar interfaces and regular handset refresh cycles. Automakers seeking low-cost connectivity on entry models view smartphone integration as an interim step toward full telematics adoption.

Premium marques have begun phasing out third-party mirroring to protect data monetization avenues, spotlighting strategic tensions between openness and ecosystem control. Tethered or portable dongles retain relevance for temporary rental fleets and emerging-market buyers but face lifecycle mismatch with fast-evolving mobile operating systems. Hybrid architectures that combine embedded safety domains with smartphone infotainment overlays illustrate the convergence path likely to define future competition in the passenger vehicle telematics market.

By End User: Fleets Drive Volume, Mobility Services Propel Growth

Fleet operators held 41.96% of the passenger vehicle telematics market size in 2024, leveraging integrated telematics to curb fuel outlays, enforce driver-safety programs, and satisfy regulatory reporting. High asset-utilization fleets, such as last-mile delivery, exhibit particularly strong return on investment, ensuring sustained hardware refresh cycles and incremental software sales. Private consumers access telematics primarily through OEM factory fitment, where bundled entertainment and safety packages raise perceived vehicle value. Insurance and leasing firms incorporate telematics to manage residual-value risk, monitor mileage, and refine actuarial models, creating secondary demand for data analytics services.

Car-sharing and broader mobility-as-a-service providers stand out with a 12.49% CAGR during the forecast period (2025-2030), illustrating the sector’s rapid digitalization. Real-time location tracking, usage-based billing, and remote diagnostics form critical infrastructure for efficient fleet turnover and customer satisfaction. Partnerships between telematics suppliers and mobility platforms accelerate feature rollouts such as keyless access and automated customer onboarding. The diverse needs across user types collectively ensure a broad service canvas for the passenger vehicle telematics market.

Geography Analysis

North America preserved its lead with 35.82% market share of the passenger vehicle telematics market in 2024, reflecting early regulatory alignment, ubiquitous 4G and expanding 5G networks, and widespread corporate-fleet digitization. Insurers actively promote usage-based discounts, prompting higher consumer install rates, while federal infrastructure programs back V2X corridor pilots that reference anonymized telemetry feeds. High replacement cycles among commercial fleets catalyze ongoing hardware refreshes, reinforcing regional scale. Yet proposed restrictions on untrusted foreign suppliers could reshape sourcing strategies and marginally elevate deployment costs, injecting mild uncertainty into near-term investment decisions. Despite this, robust capital markets and a sophisticated startup ecosystem ensure the rapid commercialization of next-generation features.

Asia-Pacific is projected to advance at an 8.44% CAGR during the forecast period (2025-2030), buoyed by massive passenger-vehicle volumes, government-backed smart-city programs, and rising middle-class digital expectations. China anchors regional momentum through electric-vehicle mandates and comprehensive connectivity requirements that embed telematics in every new energy model. India’s production-linked incentive schemes and expanding cellular coverage lower barriers for embedded modules, while Southeast Asian mega-cities pilot congestion-pricing systems that rely on vehicle telemetry. Cost sensitivity remains a headwind; nonetheless, localized manufacturing and falling component prices are narrowing the affordability gap. Together, these factors position Asia-Pacific as the principal growth engine of the passenger vehicle telematics market.

Europe continues to record steady uptake, driven by mandatory eCall and forthcoming General Safety Regulation milestones that extend connectivity requirements beyond passenger cars. Advanced driver-monitoring, speed-assistance, and event-data recorder mandates reinforce embedded hardware adoption, benefiting suppliers that can deliver integrated, cyber-secure stacks. Stringent data-protection rules elevate compliance complexity, but simultaneously enhance consumer trust, supporting subscription uptake once privacy assurances are met. OEM collaborations with telecom operators are trialing 5G standalone networks to enable low-latency safety applications and ultra-high-accuracy positioning. As a result, Europe remains a technologically advanced yet regulation-driven pillar of the passenger vehicle telematics market.

Competitive Landscape

The passenger vehicle telematics market is moderately fragmented. Tier-1 suppliers leverage legacy OEM relationships and vertical integration to win long-term platform awards, while cloud-native entrants focus on scalable software and data analytics. Cross-industry alliances are proliferating: semiconductor companies partner with telematics vendors to deliver high-precision positioning chipsets, and telecom operators bundle connectivity with edge-computing services. Acquisitions highlight a trend toward solution-portfolio expansion to address diverse customer requirements.

Strategic differentiation revolves around secure OTA infrastructures, AI-powered predictive analytics, and compliance management toolkits that simplify homologation across multiple jurisdictions. OEMs increasingly favor turnkey partners capable of integrating hardware, middleware, and cloud dashboards to accelerate time-to-market. Vendors strong in cybersecurity can capture a premium share as regulations tighten, especially in Europe and North America. Conversely, companies unable to demonstrate transparent data-governance frameworks risk exclusion from upcoming procurement cycles.

Regional specialization is also shaping competitive dynamics. Asia-Pacific players excel in cost-optimized hardware targeted at emerging markets, while European firms dominate standards-compliant safety modules. North American startups often pioneer SaaS-centric fleet-management portals, which they scale internationally through API-driven partnerships. Over the forecast horizon, partnership agility and regulatory expertise will define winners within the passenger vehicle telematics market.

Passenger Vehicle Telematics Industry Leaders

Continental AG

LG Electronics

Robert Bosch GmbH

Harman International

Denso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Trimble and KT Corporation unveiled a bundled positioning-plus-connectivity service in South Korea to improve telematics accuracy for passenger vehicles.

- May 2025: Hyundai Motor India introduced the Hyundai Vehicle Digital Passport, using telematics and service-record data to create a secure digital identity for every Bluelink-equipped vehicle.

- January 2025: Qualcomm and Trimble deepened their collaboration to integrate centimeter-level positioning into Snapdragon Auto 5G chipsets, which target Level 2+ automated-driving applications.

- January 2025: Samsara broadened its partnership with Stellantis, embedding telematics APIs across additional vehicle platforms to enhance OEM-native connectivity.

Global Passenger Vehicle Telematics Market Report Scope

| Infotainment and Navigation |

| Fleet Management |

| Safety and Security |

| Diagnostics and Prognostics |

| Insurance Telematics |

| Other Services |

| OEM-Fitted |

| Aftermarket |

| Embedded |

| Integrated |

| Tethered / Portable |

| Private Consumers |

| Fleet Operators |

| Insurance and Leasing Firms |

| Car-Sharing and Mobility Providers |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Service | Infotainment and Navigation | |

| Fleet Management | ||

| Safety and Security | ||

| Diagnostics and Prognostics | ||

| Insurance Telematics | ||

| Other Services | ||

| By Sales Channel | OEM-Fitted | |

| Aftermarket | ||

| By Connectivity Solution | Embedded | |

| Integrated | ||

| Tethered / Portable | ||

| By End-User | Private Consumers | |

| Fleet Operators | ||

| Insurance and Leasing Firms | ||

| Car-Sharing and Mobility Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What CAGR is forecast for the passenger vehicle telematics market between 2025 and 2030?

The market is projected to grow at a 8.29% CAGR, increasing from USD 12.19 billion in 2025 to USD 18.15 billion in 2030.

Which service segment currently leads in revenue contribution?

Fleet management services led with 37.87% passenger vehicle telematics market share in 2024, reflecting their strong cost-optimization benefits.

Why are embedded connectivity solutions expected to stay dominant?

Embedded systems integrate seamlessly with safety mandates, support secure OTA functions, and let OEMs monetize data over the vehicle lifecycle.

Which region is anticipated to record the fastest growth to 2030?

Asia-Pacific is forecast to expand at an 8.44% CAGR, driven by large vehicle volumes, government smart-city initiatives, and improving network infrastructure.

How will regulatory mandates shape telematics adoption in Europe?

EU rules such as mandatory eCall and General Safety Regulation requirements enforce embedded telematics in all new vehicles, ensuring consistent demand.

What is the biggest restraint affecting emerging markets?

High hardware and cellular-data costs create adoption barriers in price-sensitive regions, delaying penetration of advanced telematics features.

Page last updated on: