Europe Automotive Telematics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

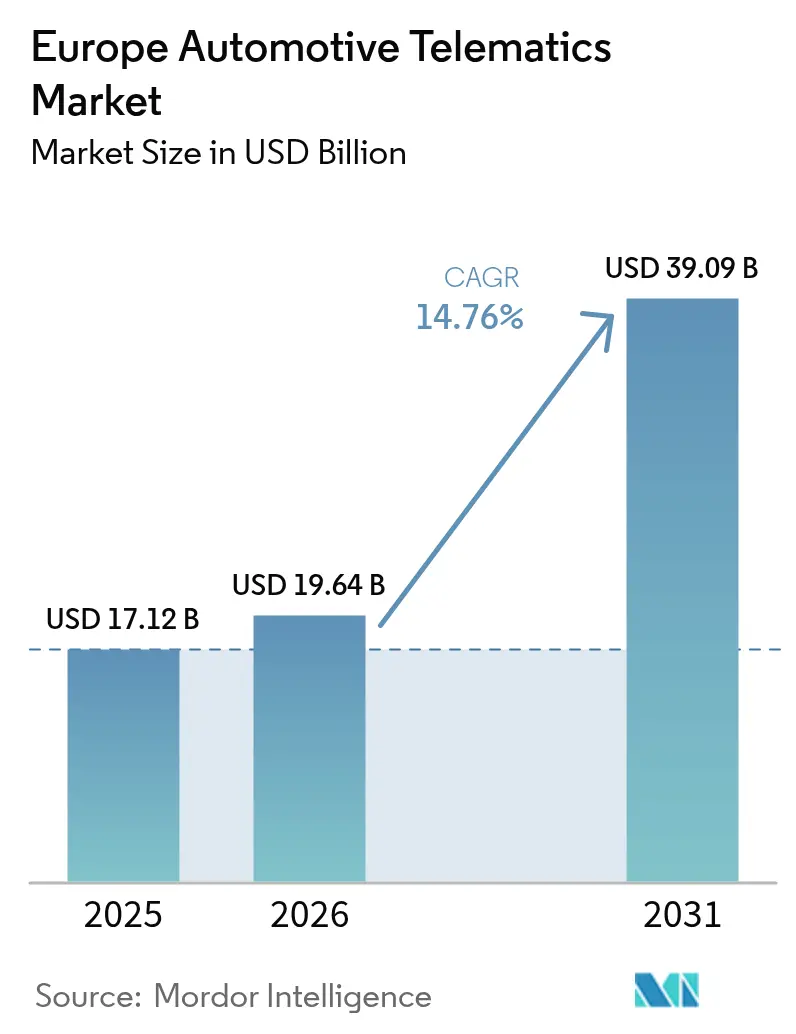

| Base Year Market Size (2025) | USD 17.12 Billion |

| Market Size (2026) | USD 19.64 Billion |

| Market Size (2031) | USD 39.09 Billion |

| Growth Rate (2026 - 2031) | 14.76% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Automotive Telematics Market Analysis by Mordor Intelligence

Europe automotive telematics market size in 2026 is estimated at USD 19.64 billion, growing from 2025 value of USD 17.12 billion with 2031 projections showing USD 39.09 billion, growing at 14.76% CAGR over 2026-2031. Momentum is shifting from connectivity as an optional differentiator to connectivity as a regulatory baseline and a recurring-revenue catalyst. The European Commission’s eCall mandate guarantees factory-fitted modems in new vehicles, turning every car into a data-producing node. Fleet operators are layering telematics into sustainability scorecards as low-emission zones proliferate, while insurers accelerate usage-based pricing that aligns premiums with real-time driving behavior. Germany’s automakers anchor platform scale, yet the United Kingdom is scaling faster thanks to a mature insurance-telematics ecosystem and post-Brexit test-bed flexibility. On the service front, fleet-management modules remain the revenue workhorse, but V2X and over-the-air (OTA) updates are rising sharply as software-defined vehicles become the strategic focus. Competitive intensity is increasing as Tier 1s, telecom carriers, and cloud vendors converge on data monetization opportunities that extend beyond simple asset tracking.

Key Report Takeaways

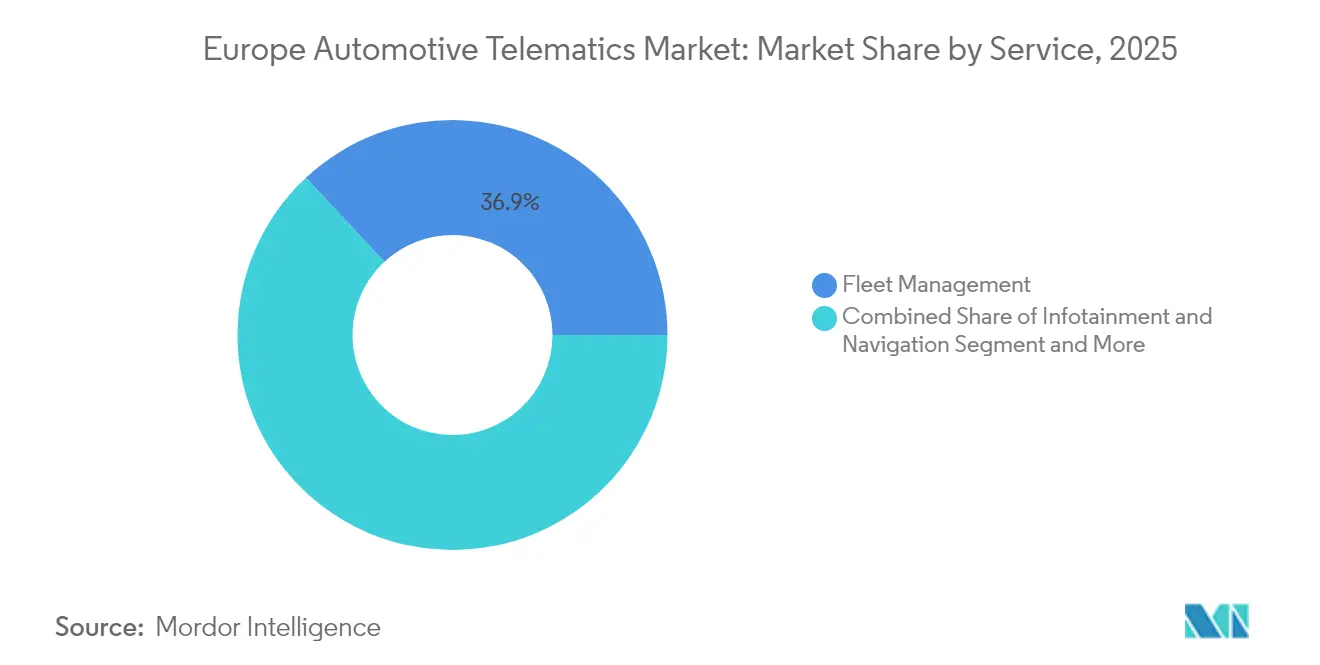

- By service, fleet management held 36.94% of the Europe automotive telematics market share in 2025, while V2X and OTA updates are projected to expand at a 16.95% CAGR through 2031.

- By sales channel, OEM-fitted systems controlled 79.71% share of the Europe automotive telematics market size in 2025; the aftermarket is the fastest-growing channel at 16.48% CAGR.

- By connectivity solution, embedded telematics accounted for 54.05% of the Europe automotive telematics market share in 2025, whereas integrated-smartphone architectures are advancing at a 16.89% CAGR.

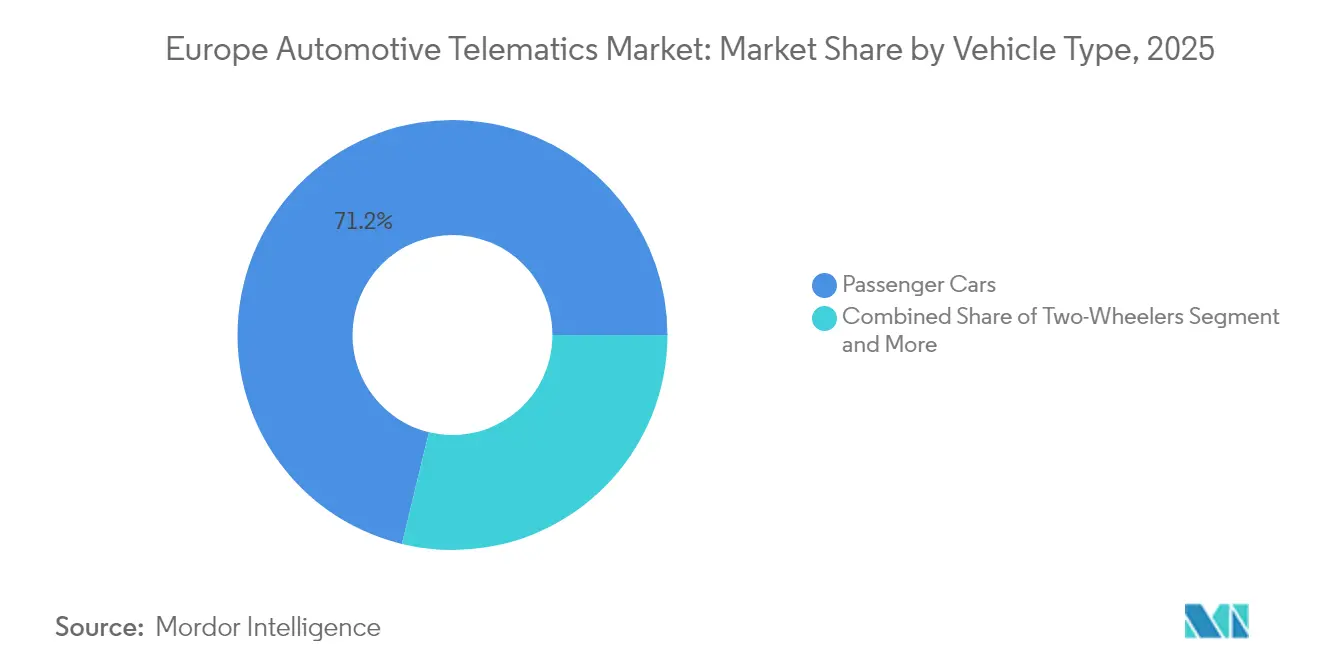

- By vehicle type, passenger cars generated 71.22% of 2025 revenue, but light commercial vehicles are forecast to post a 16.55% CAGR to 2031.

- By end-user, fleet operators commanded 54.16 of % demand in 2025; insurance and leasing firms are the fastest-growing cohort at 17.09% CAGR.

- By country, Germany led with 41.02% revenue share in 2025, while the United Kingdom is projected to grow at 15.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Automotive Telematics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet-Management Digitization Wave | +2.8% | Germany, France, United Kingdom, Benelux, Poland | Medium term (2-4 years) |

| 5G and V2X Rollout Across Europe | +2.4% | Germany, France, United Kingdom, Nordic region | Long term (≥ 4 years) |

| EU eCall and Safety-Mandate Tailwinds | +2.1% | EU27, United Kingdom, Norway, Switzerland | Short term (≤ 2 years) |

| OEM Push for Software-Defined Revenue | +2.3% | Germany, France, United Kingdom, Sweden | Medium term (2-4 years) |

| Infotainment and Navigation Demand Surge | +1.9% | Germany, United Kingdom, France, Italy, Spain | Medium term (2-4 years) |

| ESG-Linked CO₂ Reporting Requirements | +1.6% | EU27, United Kingdom city low-emission zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fleet-Management Digitization Wave

European fleets are increasingly adopting telematics for route optimization, driver scorecarding, and predictive maintenance. These efforts aim to combat fuel theft, minimize downtime, and enhance customer satisfaction. Deployments reveal that predictive maintenance can significantly reduce unplanned stoppages. Additionally, geofencing streamlines proof-of-delivery workflows, helping to accelerate invoicing cycles and improve operational efficiency. A recent survey from a prominent fleet-management platform highlighted that a substantial portion of European fleet managers intend to broaden their telematics usage in the near future. Their motivations include addressing stricter emission regulations and achieving better visibility into the return on investment for electric vehicles. The trend of platform consolidation is becoming more evident, as demonstrated by a technology vendor acquiring a mobility unit to integrate hardware, connectivity, and software into a single contract. This approach simplifies integration processes and significantly reduces the total cost of ownership for fleet buyers, making it a more attractive option for businesses.

5G and V2X Rollout Across Europe

The Connecting Europe Facility has allocated significant funding to equip thousands of kilometers of highways with roadside units. This effort is designed to enable cooperative adaptive cruise control and platooning, which can lead to notable reductions in truck fuel consumption. Key corridors, such as Germany's autobahn and France's A10, are at the forefront of C-V2X implementation. Original Equipment Manufacturers are proactively embedding advanced chipsets from Qualcomm and NXP into upcoming vehicle models to align with anticipated regulatory requirements. In addition to improving safety, the integration of 5G technology, with its low latency capabilities, supports innovative applications like remote-driven shuttle pilots and dynamic speed-limit broadcasts. These advancements further reinforce the rationale for sustained investments in infrastructure development.

OEM Push for Software-Defined Revenue

Automakers are transitioning from one-off feature bundling toward recurring software subscriptions delivered through OTA pipelines. Premium brands already monetize incremental horsepower, advanced parking, and remote climate control as annual or monthly services [1]"eSync announces Arm as eSync Alliance Charter Member" eSync Alliance, esyncalliance.org. This strategy hinges on a secure, bi-directional telematics channel that supports entitlement management, billing, and rapid feature activation. Early deployments suggest predictive maintenance can reduce warranty claims, and recurring digital revenue provides a margin buffer as hardware profits erode in an electrifying market.

EU eCall and Safety-Mandate Tailwinds

The European Union requires all new passenger cars and light commercial vehicles to be equipped with an automatic emergency call module. This regulation has resulted in a significant portion of new vehicles being equipped with the system[2]“eCall Implementation Report 2024,”, European Commission, ec.europa.eu. The hardware that supports eCall also serves as the foundation for advanced services, including stolen-vehicle recovery, remote diagnostics, and subscription-based navigation. As consumers increasingly embrace constant connectivity, they have become more willing to share data, enabling insurers and fleet managers to access real-time driving telemetry. The regulation has further influenced advanced driver-assistance systems, as components such as GNSS receivers and crash sensors from eCall are now utilized across various digital features. After Brexit, the United Kingdom implemented a similar mandate, ensuring regulatory consistency across major European markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR Compliance Cost Inflation | -1.2% | EU27, United Kingdom, EEA | Short term (≤ 2 years) |

| 2G/3G Sunset Retrofit Burden | -1.1% | Germany, Netherlands, United Kingdom, Nordic region | Short term (≤ 2 years) |

| High Embedded-Hardware BOM in Small Cars | -0.9% | Southern and Eastern Europe | Medium term (2-4 years) |

| Fragmented OEM Data Schemas | -0.7% | Pan-European mixed-brand fleet operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GDPR Compliance Cost Inflation

Telematics providers are required to incorporate consent dashboards, implement encryption during data storage and transmission, and maintain extensive audit logs for an extended period, as mandated by the General Data Protection Regulation (GDPR). These legal and technical requirements significantly increase program costs, creating challenges for smaller aftermarket players that often lack the resources or dedicated teams to ensure compliance. Additionally, GDPR complicates and lengthens the commercialization process, as privacy-impact assessments must be conducted before launching any new analytic or monetization initiative. Companies that achieve recognized certifications, such as ISO 27001, and implement real-time consent management systems can appeal to enterprise fleets that prioritize risk mitigation. However, these firms face higher operational costs, which may drive cost-conscious customers to opt for alternatives with less stringent compliance measures.

2G/3G Sunset Retrofit Burden

Mobile network operators across Europe are discontinuing older 2G and 3G bands, rendering legacy telematics units non-functional. A significant number of commercial vehicles require hardware replacements, with costs varying depending on the unit and installation requirements. Smaller fleet operators often delay these upgrades, prioritizing them only when equipment fails inspections or compliance deadlines become unavoidable. The disposal of outdated telematics systems further exacerbates e-waste concerns, adding environmental compliance challenges to an already expensive and resource-intensive retrofit process.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Performance Anchors and Software Upside

Fleet management accounted for 36.94% of 2025 service revenue and remains the backbone of the Europe automotive telematics market. The value proposition is concrete: real-time tracking reduces fuel theft, driver coaching prevents accidents, and route optimization shortens delivery windows, collectively enhancing fleet productivity and customer satisfaction. Diagnostics and prognostics are next in line, enabling fleets to transition from reactive to condition-based maintenance, thereby reducing downtime. Safety and security modules benefit from the eCall installed base, yet margins compress as the features become standard.

V2X and OTA services, although smaller today, are the fastest-growing categories, with a 16.95% CAGR. OTA updates enable automakers to introduce new features and security patches throughout a vehicle’s life, thereby reducing recall costs and generating recurring revenue. V2X enables cooperative driving and intersection warnings, positioning vehicles as nodes within a larger transportation network. Insurance telematics growth is concentrated in high-penetration markets such as the UK and Italy, where usage-based policies reward safe driving with lower premiums. As services evolve, the Europe automotive telematics market size for OTA modules is expected to surpass that of legacy safety features, underscoring a shift in platform from tracking to continuous software delivery.

By Sales Channel Type: Factory Control and Retrofit Agility

OEM-installed telematics represented 79.71% of total 2025 deployments, driven by regulatory mandates and automakers’ need to control data footprints. Factory systems integrate deeply with the CAN bus, enabling remote diagnostics and secure OTA firmware updates. This tight integration also safeguards data ownership, a prerequisite for subscription-based service models.

The aftermarket is expanding at 16.48% CAGR, addressing fleets with pre-2018 vehicles and appealing to cost-sensitive consumers who seek insurance discounts without buying new cars. Plug-and-play OBD-II dongles and hard-wired trackers cost roughly one-third of OEM solutions and can be upgraded more quickly. With the phase-out of 2G/3G networks, many legacy aftermarket devices are becoming obsolete, leading to a growing preference for 4G/5G-compatible units. Over time, the market is expected to reach a balance, with original equipment manufacturers dominating a significant share while the aftermarket segment continues to cater to retrofit needs. This trend underscores the interplay between regulatory requirements and the demand for adaptable solutions within the European automotive telematics market.

By Connectivity Solution: Embedded Reliability Meets Smartphone Economics

Embedded telematics held 54.05% share in 2025, favored for independence from driver smartphones and for deeper system integration that enables remote immobilization and secure OTA patches. The European automotive telematics market share for embedded units also benefits from looming cybersecurity certification proposals that will likely favor hardware-root-of-trust architectures.a

Integrated-smartphone approaches are gaining at a 16.89% CAGR as budget models and emerging-market variants offload navigation and voice-assistant workloads to consumer devices, saving EUR 100-200 per car in compute and antenna costs. Hybrid designs are emerging, in which core telematics remains embedded while infotainment applications mirror from smartphones, creating a blended stack that balances OEM control with consumer familiarity. Tethered solutions serve niche use cases, including rental, ride-sharing, and teen-driver monitoring, but face usage friction and limited functionality. As 5G networks mature, embedded and smartphone strategies will co-exist. Still, embedded hardware is likely to remain the backbone for mission-critical safety and regulatory compliance in the European automotive telematics market.

By Vehicle Type: Passenger-Car Volume and LCV Momentum

Passenger cars dominated the market, accounting for 71.22% of the revenue in 2025. Strong growth in vehicle registrations, along with a significant adoption of infotainment subscriptions, drives this trend. Buyers prioritize navigation and safety features, making sport utility and multi-purpose vehicles the most popular choices for family travel. On the other hand, urban commuters, who are more cost-conscious, prefer hatchbacks and sedans. These vehicle types often rely on smartphone mirroring solutions as a cost-effective alternative to subscription-based services.

Light commercial vehicles (LCVs) are growing at the fastest rate, with a 16.55% CAGR, driven by e-commerce growth and last-mile delivery operators that require real-time routing and geofenced proof of delivery. Heavy trucks, although fewer in number, command higher per-unit spending due to tachograph mandates and fuel-optimization returns. Two-wheelers remain under 10% penetration, yet insurer initiatives in Italy and France suggest a latent market for usage-based products that reward safe riding. The accelerating adoption of LCVs will continue to pull overall growth in the European automotive telematics market size as parcel volumes rise and urban logistics tighten delivery windows.

By End-User: Operational Scale and Risk-Pricing Innovation

Fleet operators contributed 54.16% of 2025 demand, leveraging enterprise telematics to integrate warehouse management, just-in-time inventory, and multi-modal load balancing. Large logistics groups utilize predictive diagnostics to minimize downtime and enhance asset utilization in an environment of driver shortages and volatile fuel prices.

Insurance and leasing firms are the growth leaders, with a 17.09% CAGR, driven by usage-based underwriting that aligns risk with actual driving data rather than demographic averages. European insurers report 15%-20% lower claim frequency among telematics policyholders, justifying premium discounts that attract younger and urban drivers. Private consumers generate lower revenue per vehicle due to subscription attrition when free trials expire. Yet, mobility providers—such as car-sharing and ride-pool fleets—cannot operate without telematics that enable keyless entry and per-minute billing. Regulatory initiatives to establish a Mobility Data Space could standardize access to anonymized data, amplifying network effects and sustaining high-growth end-user segments within the European automotive telematics market.

Geography Analysis

Germany’s scale advantage in production and supplier ecosystems underpins its 41.02% share of the European automotive telematics market. Volkswagen's Cariad platform, developed in-house, is designed to unify data across its various brands within a specific timeframe. This initiative aims to create a streamlined channel for over-the-air (OTA) updates and in-car payment systems, enhancing operational efficiency and user experience. BMW has reported significant growth in its software and services revenue, driven by the increasing adoption of its ConnectedDrive subscriptions, which continue to gain momentum in the market. Meanwhile, Daimler Truck's Fleetboard connects a substantial number of vehicles, integrating telematics with proprietary safety systems to provide comprehensive and vertically integrated fleet management solutions.

The United Kingdom is advancing at 15.42% CAGR, propelled by a mature insurance-telematics ecosystem and a regulatory sandbox that accelerates connected and autonomous vehicle trials. Admiral Group’s LittleBox program monitors a significant number of vehicles, providing substantial premium reductions to encourage safe driving habits. The expansion of London’s Ultra Low Emission Zone has heightened the need for real-time emissions tracking. This development has driven increased demand for retrofit telematics solutions, particularly among urban delivery and service fleets aiming to comply with stricter emission standards.

France, Italy, and Spain collectively bolster growth through emission-zone enforcement and insurer innovation. Stellantis offers a unified telematics cockpit for its extensive commercial-vehicle range, and Generali’s flexible-use policies resonate with low-mileage urban motorists. Spain’s courier leaders deploy telematics to navigate pedestrianized city centers, while Italy pioneers motorcycle telematics to curb elevated accident rates. Eastern Europe is catching up as EU funds support 5G corridors, positioning Poland as a logistics hub that demands real-time proof-of-delivery feeds. Russia’s adoption remains subdued, but local giants such as Yandex are building home-grown platforms to partially offset import constraints.

Competitive Landscape

Moderate competitive concentration characterizes the market: the leading suppliers—Continental, Bosch, TomTom, Geotab, and Verizon Connect—command a significant share of the revenue. Tier 1 suppliers are capitalizing on their hardware presence, bundling telematics with ADAS sensors, which further strengthens their relationships with OEMs. Geotab, a pure-play platform, has distinguished itself with its advanced cloud analytics, which aggregate data from mixed-brand fleets. This capability has enabled them to secure contracts with major players in the automotive industry. Meanwhile, telecom giants like Vodafone Automotive and Orange Business Services are leveraging their network ownership to offer bundled connectivity and telematics solutions on a large scale. At the same time, cloud hyperscalers are gaining traction with their turnkey data lakes, aligning with the evolving strategies of software-defined vehicles.

Continental's CAEdge platform is at the forefront of edge computing innovation, enabling the local processing of sensor fusion, which significantly reduces cloud expenses and minimizes latency [3]“CAEdge Platform Launch,”, Continental AG, continental-press.com. To address data residency requirements and enhance service speed, Verizon Connect has established a data center in Europe, catering to the needs of regional clients.

The focus of differentiation is shifting from hardware to advanced software algorithms. These algorithms drive innovations such as digital twins, predict component failures, and create secure data marketplaces. Providers with recognized certifications and clear compliance with data protection regulations are not only securing enterprise and government contracts but are also building a strong regulatory advantage. Emerging opportunities are evident in areas such as two-wheeler insurance telematics and car-sharing fleets. These sectors, which demand precise billing and automated damage detection, present significant growth potential for agile providers capable of scaling quickly and outperforming established competitors.

Europe Automotive Telematics Industry Leaders

-

Robert Bosch GmbH

-

Continental AG

-

Vodafone Automotive

-

TomTom International BV.

-

Octo Group S.p.A

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Polestar has unveiled Fleet Telematics, a cutting-edge service designed to oversee and enhance electric vehicle fleets. This service offers real-time data and actionable insights, ensuring smooth integration without the need for extra hardware or installation costs. In collaboration with partners Echoes, Geotab, and High Mobility, Polestar Fleet Telematics empowers fleet operators with real-time vehicle data and usage analytics to boost efficiency.

- June 2025: In a strategic move, Targa Telematics has partnered with Volvo Cars to utilize data from Volvo vehicles across Europe. This collaboration enables Targa Telematics to directly integrate data streams from various Volvo models into its platform. The partnership aims to develop innovative connected mobility services by leveraging insights such as distance traveled, fuel consumption, GPS coordinates, electric vehicle data, and remote functionalities like locking and unlocking. All these advancements are implemented while ensuring full compliance with privacy and safety regulations.

Europe Automotive Telematics Market Report Scope

The scope includes segmentation by Service (infotainment and navigation, fleet management, safety and security, diagnostics and prognostics, insurance telematics, and v2x and OTA updates), sales channel type (OEM-fitted and aftermarket), connectivity solution (embedded, integrated-smartphone, and tethered/portable), vehicle type (two-wheelers, passenger cars, LCVs, and MCVs and HCVs), end-user (private consumers, fleet operators, insurance and leasing firms, car-sharing and mobility providers). The analysis also covers country-level segmentation, including Germany, the United Kingdom, France, Italy, Spain, Russia, and the Rest of Europe. Market size and growth forecasts are presented by value in USD.

| Infotainment and Navigation |

| Fleet Management |

| Safety and Security |

| Diagnostics and Prognostics |

| Insurance Telematics |

| V2X and OTA Updates |

| OEM-fitted |

| Aftermarket |

| Embedded |

| Integrated-smartphone |

| Tethered / Portable |

| Two-Wheelers | |

| Passenger Cars | Hatchbacks |

| Sedans | |

| Sports Utility Vehicles | |

| Multi Puropse Vehicles | |

| Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles |

| Private Consumers |

| Fleet Operators |

| Insurance and Leasing Firms |

| Car-Sharing and Mobility Providers |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| Rest of Europe |

| By Service | Infotainment and Navigation | |

| Fleet Management | ||

| Safety and Security | ||

| Diagnostics and Prognostics | ||

| Insurance Telematics | ||

| V2X and OTA Updates | ||

| By Sales Channel Type | OEM-fitted | |

| Aftermarket | ||

| By Connectivity Solution | Embedded | |

| Integrated-smartphone | ||

| Tethered / Portable | ||

| By Vehicle Type | Two-Wheelers | |

| Passenger Cars | Hatchbacks | |

| Sedans | ||

| Sports Utility Vehicles | ||

| Multi Puropse Vehicles | ||

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By End-User | Private Consumers | |

| Fleet Operators | ||

| Insurance and Leasing Firms | ||

| Car-Sharing and Mobility Providers | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How fast is the Europe automotive telematics market expected to grow to 2031?

It is projected to expand at a 14.76% CAGR, rising from USD 17.12 billion in 2025 to USD 39.09 billion by 2031.

Which country currently generates the highest telematics revenue in Europe?

Germany leads with 41.02% of 2025 regional revenue, driven by large OEM platforms and dense Tier 1 supplier networks.

Why are light commercial vehicles adopting telematics so quickly?

Last-mile delivery growth demands real-time routing and proof-of-delivery functions, propelling LCV telematics at a 16.55% CAGR.

What is driving the surge in OTA update services?

Automakers view OTA updates as the backbone of software-defined revenues, enabling continuous feature delivery without dealership visits.

Page last updated on: