Lactose-Free Milk Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

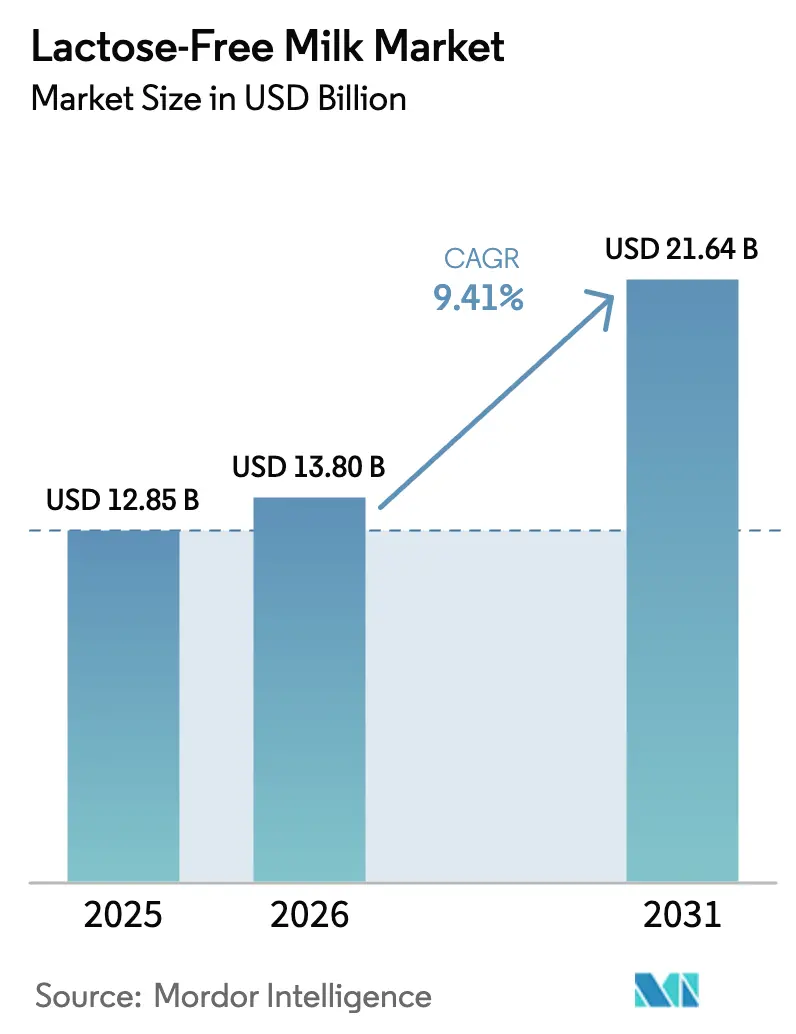

| Market Size (2026) | USD 13.80 Billion |

| Market Size (2031) | USD 21.64 Billion |

| Growth Rate (2026 - 2031) | 9.41% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Lactose-Free Milk Market Analysis by Mordor Intelligence

The Lactose-Free Milk Market size is projected to be USD 12.85 billion in 2025, USD 13.80 billion in 2026, and reach USD 21.64 billion by 2031, growing at a CAGR of 9.41% from 2026 to 2031. The increasing prevalence of lactose intolerance globally continues to drive consistent demand for lactose-free milk products. Additionally, advancements in β-galactosidase processing technology have significantly reduced the sensory differences between lactose-free and conventional milk, encouraging greater consumer adoption. Liquid formats remain the dominant segment due to their compatibility with existing consumption patterns. However, flavored and reduced-fat variants are witnessing rapid growth, fueled by a combination of innovative flavor developments and a growing focus on health-conscious choices. Retailers are increasingly focusing on private-label strategies, which are compressing profit margins. In response, processors are prioritizing investments in areas such as enzyme sourcing, ultra-filtration techniques, and fortified product formulations to maintain their competitive edge and protect value. Simultaneously, competition from plant-based alternatives and emerging precision-fermentation technologies is intensifying, driving the need for enhanced product differentiation and improved supply-chain efficiency.

Key Report Takeaways

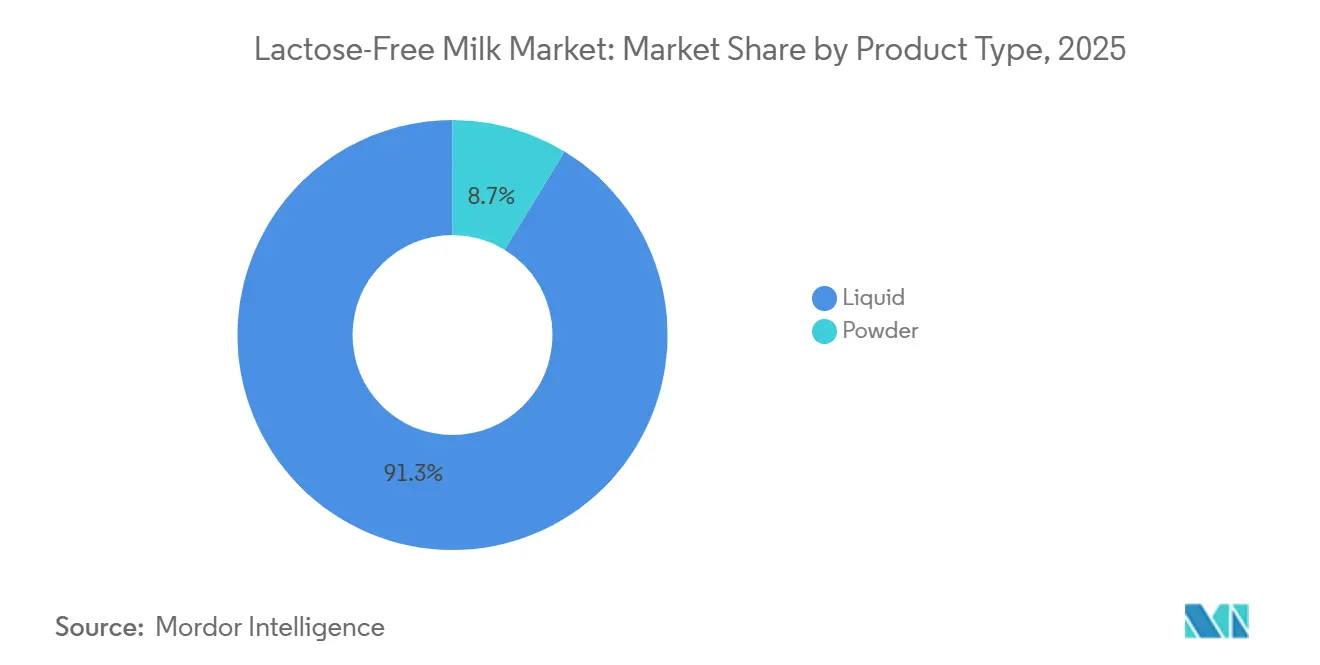

- By product type, liquid milk captured 91.28% revenue share in 2025, while powder is forecast to expand at a 9.73% CAGR to 2031.

- By fat content, whole milk led with a 48.29% share of the lactose-free milk market size in 2025; skimmed and fat-free variants are advancing at a 9.73% CAGR through 2031.

- By category, plain offerings held 75.61% of the lactose-free milk market share in 2025, whereas flavored products are projected to grow at a 10.39% CAGR to 2031.

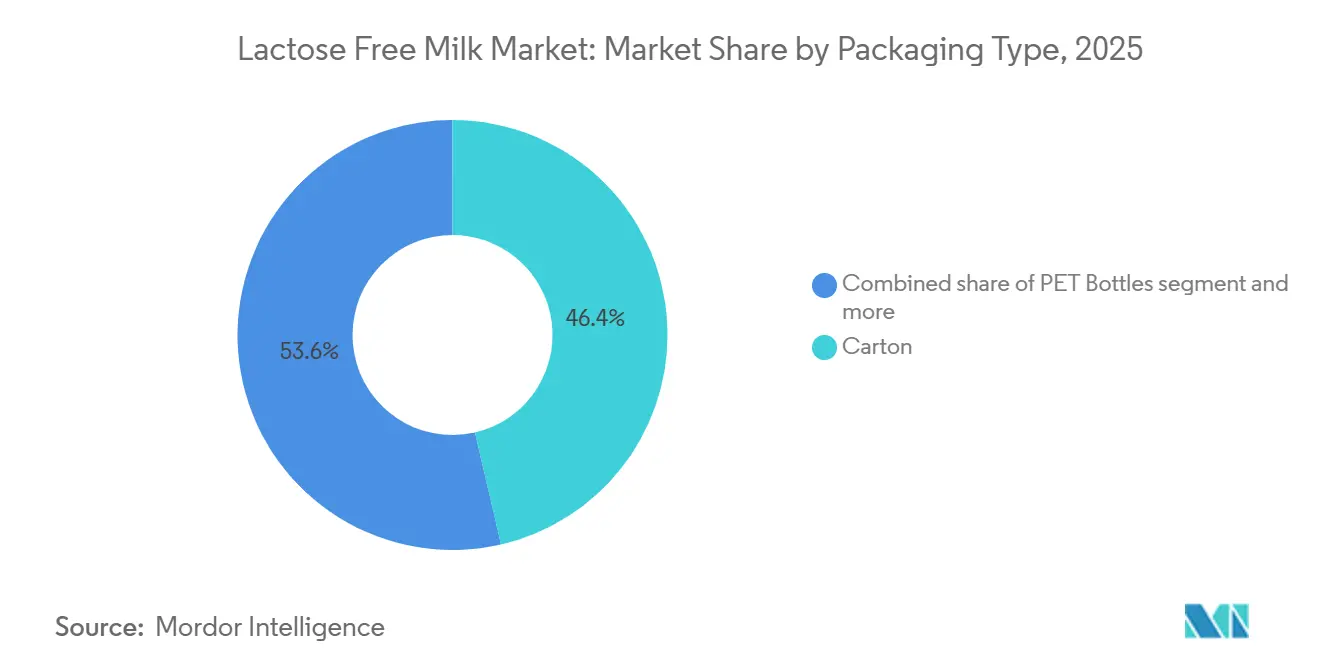

- By packaging type, carton formats commanded 46.38% share in 2025, while PET bottles are growing at a 9.94% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets accounted for 50.24% of 2025 sales; online retail is expanding at a 10.24% CAGR through 2031.

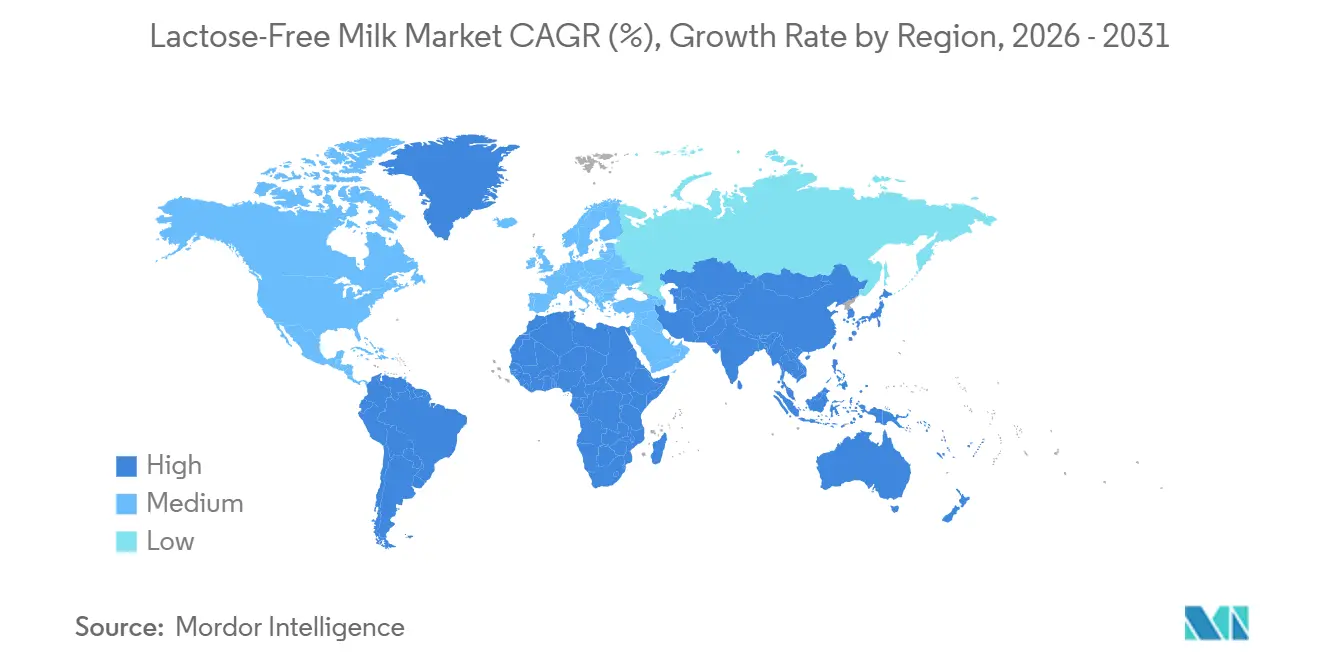

- By geography, North America led with 33.20% revenue share in 2025; Asia-Pacific represents the fastest-growing region, forecast at a 9.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Lactose-Free Milk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of lactose intolerance worldwide | +2.1% | Global, with concentration in Asia-Pacific, Middle East, and Latin America | Long term (≥ 4 years) |

| Growing consumer focus on digestive health and "free-from" claims | +1.8% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Product innovations including flavored, organic, fortified, and reduced-fat variants | +1.5% | North America, Europe, Australia | Medium term (2-4 years) |

| Technological advances in lactose removal improving taste and texture | +1.3% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Adoption by non-intolerant consumers seeking healthier milk alternatives | +1.6% | North America, Europe, affluent urban centers in Asia | Short term (≤ 2 years) |

| Marketing campaigns and education on lactose-free benefits | +0.8% | Global, with emphasis on emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of lactose intolerance worldwide

Globally, lactose malabsorption affects a significant portion of the population, particularly in East Asia, West Africa, Europe, and the Middle East. As of 2024, data from Boston Children's Hospital reveal that 80% of African-Americans and Native Americans experience lactose intolerance, while the rate exceeds 90% among Asian-Americans [1]Source: Boston Children's Hospital, "Lactose Intolerance", childrenshospital.org. Conversely, Americans of Northern European descent report the lowest prevalence of this condition. This genetic characteristic, caused by reduced lactase persistence after weaning, creates a baseline demand for dairy products that traditional options fail to satisfy. In urban areas, increased access to gastroenterology services and hydrogen breath testing has heightened diagnostic awareness, turning previously unrecognized discomfort into a clear demand for lactose-free products. The Middle East demonstrates particularly high rates of lactose intolerance. In China and India, where lactose intolerance is widespread, rapid urbanization and growing dairy consumption have created a unique challenge. Here, the demand for dairy nutrition conflicts with physiological intolerance, a gap effectively addressed by lactose-free alternatives. Additionally, aging populations in developed markets further drive demand for lactose-free products, as lactase production declines with age, even among historically tolerant groups.

Growing consumer focus on digestive health and "free-from" claims

The "free-from" movement, which initially focused on gluten and allergen avoidance, has now expanded to include lactose, as consumers increasingly associate digestive discomfort with overall wellness. For instance, retail sales of lactose-free products in South Korea amounted to USD 57.9 million in 2023, according to Agriculture and Agri-Food Canada [2]Source: Agriculture and Agri-Food Canada, "Market Overview South Korea", agriculture.canada.ca. This group views lactose-free options as a proactive lifestyle choice rather than a response to medical necessity, blurring the distinction between health needs and personal preferences. Gut microbiome research, popularized by direct-to-consumer testing kits and social media wellness influencers, has shifted digestive health from a clinical issue to a mainstream wellness priority. Brands are leveraging this trend by combining lactose-free claims with probiotic fortification, prebiotic fiber, and reduced sugar, creating a "halo effect" that supports premium pricing. The regulatory framework aligns with this trend: Food and Drug Administration guidance under 21 CFR 101.13 permits nutrient content claims when lactose is reduced by 25% or more, providing a compliant pathway for marketing differentiation.

Product innovations including flavored, organic, fortified, and reduced-fat variants

Flavored lactose-free milk is anticipated to grow at a CAGR of 10.39% through 2031, surpassing plain variants. Manufacturers are introducing chocolate, vanilla, and strawberry flavors to attract both children and adults seeking indulgent options. To address the nutritional deficiencies caused by reducing or eliminating conventional dairy, these flavored options are fortified with vitamin D, calcium, and protein. Additionally, reduced-fat and fat-free versions are being reformulated with added protein to ensure they remain satisfying and maintain their mouthfeel, despite the technical challenge of compensating for the creaminess provided by fat. Adapting to changing consumer preferences and rising competition in the dairy sector, the Karnataka Milk Federation (KMF), recognized for its Nandini brand, is expanding its product portfolio. As part of this initiative, KMF launched a range of new products in September 2025, including lactose-free milk, buffalo milk, protein-rich milk, and a new selection of sugar-free sweets and savories.

Technological advances in lactose removal improving taste and texture

β-galactosidase has transformed enzymatic lactose hydrolysis, moving from batch processing to continuous immobilized enzyme reactors. This advancement has reduced processing time from 24 hours to just 4 and significantly lowered enzyme costs. Methods such as covalent bonding to silica supports and entrapment in alginate beads enable enzyme reuse for 50 to 100 cycles, converting lactase from a consumable input into a durable resource. Fairlife and other premium brands are utilizing membrane filtration technologies, including ultrafiltration and nanofiltration, to concentrate protein and remove residual lactose without enzymatic treatment. This approach produces a sweeter, creamier product that appeals to both lactose-intolerant and non-intolerant consumers. To address the sweetness challenge, since glucose and galactose are sweeter than lactose, manufacturers are blending with non-sweet protein isolates and adjusting fat ratios. Ultra-high-temperature (UHT) processing, which extends shelf life to 6 to 9 months without refrigeration, is being increasingly adopted in emerging markets, where cold-chain limitations hinder distribution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher production costs due to specialized processing | -1.2% | Global, particularly impacting emerging markets | Medium term (2-4 years) |

| Intense competition from plant-based alternatives like almond and oat milk | -1.5% | North America, Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| Limited awareness and availability in rural or developing regions | -0.9% | Latin America, Africa, rural Asia | Long term (≥ 4 years) |

| Taste perception issues as lactose breakdown creates a sweeter profile | -0.6% | Global, with higher sensitivity in traditional dairy markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher production costs due to specialized processing

Enzymatic lactose hydrolysis increases processing costs by USD 0.08 to USD 0.15 per liter. These costs include enzyme procurement, extended processing times, and quality assurance tests to ensure residual lactose levels remain below the regulatory threshold of 0.5 grams per 100 grams. Although immobilized enzyme systems can reduce long-term expenses, they require significant capital investments ranging from USD 500,000 to USD 2 million per production line, creating obstacles for small and mid-sized processors. Milk treated enzymatically is more prone to bacterial contamination, necessitating stricter cold-chain requirements compared to conventional milk. These cost pressures are particularly challenging in emerging markets, where consumers are resistant to price increases. In 2024, Kerry Group acquired the NOLA lactase enzyme portfolio for EUR 150 million, reflecting a strategic move to control enzyme supply, mitigate input cost volatility, and protect processing margins.

Intense competition from plant-based alternatives like almond and oat milk

In North America and Europe, sales of plant-based milk alternatives have grown significantly, with oat milk gaining popularity due to its superior taste, barista-friendly frothing properties, and claims of a reduced environmental impact. For example, Americans spent USD 2.8 billion on plant-based milk in 2024, according to the Good Food Institute [3]Source: Good Food Institute, "Retail Sales of Plant-based Food", gfi.org. Almond, soy, and coconut milk variants offer lactose-free options without incurring enzymatic processing costs, creating a competitive pricing advantage in mainstream retail. Dairy processors are responding with hybrid strategies. For instance, Danone acquired the plant-based medical nutrition brand Kate Farms in May 2025, reflecting a strategic effort to diversify its portfolio amid declining dairy consumption. However, the plant-based sector faces its own challenges, including allergen concerns (such as soy and tree nuts), lower protein content in options like almond and oat milk, and 'taste fatigue' as consumers explore various novelty flavors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liquid Dominance Anchored by Retail Convenience

In 2025, the liquid segment, which accounted for a dominant 91.28% share, is expected to maintain its lead through 2031, fueled by advancements in ultra-filtration and precision fermentation. Fairlife's ultra-filtered, lactose-free milk, with 13 grams of protein per serving and no lactose, has secured premium shelf space in North American supermarkets, commanding higher prices than conventional milk. The liquid format aligns with established consumer habits, such as cereal, coffee, and cooking, and its ready-to-use nature eliminates the reconstitution barrier that often limits the adoption of powder formats.

In regions like Asia-Pacific and Latin America, shelf-stable UHT liquid variants are gaining popularity due to ambient distribution, which reduces reliance on cold chains. Powder is forecast to expand at a 9.73% CAGR to 2031. Powder formats serve specific markets like institutional foodservice, infant formula, and emergency relief, where reconstitution is acceptable, and shelf life exceeds 24 months. Industry leaders Nestlé and Fonterra dominate the powder supply chain by leveraging their spray-drying expertise and extensive global distribution networks. The gap between liquid and powder formats is expected to remain significant, as consumer preference for ready-to-drink convenience continues to outweigh the cost and storage benefits of powder in developed markets.

By Fat Content: Skimmed Variants Accelerate Amid Health Repositioning

In 2025, whole milk accounted for a significant 48.29% market share, highlighting its widespread use in cooking, baking, and full-fat coffee. However, as health-conscious consumers increasingly favor low-fat and lactose-free options, skimmed and fat-free variants are growing at a notable 9.73% CAGR, projected through 2031. Semi-skimmed or low-fat milk strikes a balance between indulgence and health, gaining popularity particularly in European markets where fat content of 1.5% to 2% aligns with dietary recommendations. This segmentation by fat content aligns with fortification trends: for example, skimmed lactose-free milk is frequently fortified with vitamins A and D to replace fat-soluble nutrients lost during fat removal, in compliance with Food and Drug Administration standards under 21 CFR 131.110.

Reduced-fat variants are also increasingly fortified with whey protein isolate or milk protein concentrate to enhance satiety. While whole milk maintains a loyal consumer base among children and in culinary applications where fat contributes to texture, the market is shifting towards reduced-fat formats due to growing concerns about obesity and cardiovascular health. Regional preferences vary significantly: Latin America and the Middle East favor whole milk, driven by cultural norms and taste preferences, whereas North America and Europe show a stronger inclination toward reduced-fat options.

By Category: Flavored Variants Capture Indulgent and Pediatric Occasions

Flavored lactose-free milk is anticipated to grow at a CAGR of 10.39% through 2031, surpassing the growth of plain lactose-free milk, which held a 75.61% market share in 2025. Variants such as chocolate, vanilla, and strawberry are gaining popularity for their appeal across various occasions, including children's preferences, post-workout consumption, and adult indulgence. In 2024, Organic Valley launched a chocolate lactose-free milk that combines organic certification with lactose-free claims, targeting parents willing to pay a premium for these combined benefits. However, developing flavored formats presents challenges. The natural sweetness from glucose and galactose, produced during hydrolysis, requires precise balancing with cocoa, vanilla, or fruit flavoring to avoid overly sweet profiles. In a significant technological advancement, Strive introduced its chocolate FREEMILK in October 2024, utilizing Perfect Day's precision-fermentation whey. This innovation eliminates lactose at the molecular level, enabling cleaner and more refined flavor profiles.

Plain lactose-free milk continues to hold a strong position in applications such as cooking, cereals, and coffee, where its neutral taste is a critical factor. Its slower growth rate reflects the maturity of this segment rather than a decline in its importance. The rapid expansion of the flavored segment highlights a significant shift in consumer preferences, with taste innovation emerging as the key growth driver. This trend is further fueled by the increasing interest of non-lactose-intolerant consumers, who are exploring lactose-free options for their taste and perceived health benefits.

By Packaging Type: PET Bottles Gain Ground on Single-Serve and Sustainability

In 2025, carton packaging held a 46.38% market share, utilizing Tetra Pak's aseptic technology and FSC-certified renewable materials. However, PET bottles are experiencing significant growth, with a 9.94% CAGR projected through 2031. This growth is driven by the demand for single-serve convenience, resealability, and compliance with recyclability mandates. Glass bottles, while appealing in premium and organic segments, face scalability challenges due to higher costs and heavier weight. Other formats, such as pouches and bag-in-box, are tailored for institutional and foodservice sectors, where bulk dispensing is a priority. Tetra Pak's connected packaging solutions, which incorporate QR codes for traceability and consumer engagement, are being adopted by companies like Arla and Nestlé to stand out in competitive retail markets.

PET bottles are benefiting from lightweighting advancements that reduce plastic usage by 20% to 30% while maintaining durability. These innovations address sustainability concerns that have traditionally favored carton packaging. The single-serve PET segment, typically ranging from 250 to 500 milliliters, is growing in convenience stores, vending machines, and on-the-go consumption scenarios, appealing to consumers who prioritize portability over cost. Increasing regulatory pressure on plastic waste is driving investments in chemical recycling and bio-based PET. Companies like Danone and Coca-Cola have pledged to achieve 50% recycled content in their PET bottles by 2030. Carton packaging remains advantageous in ambient UHT applications, where its barrier properties protect against light and oxygen, enabling a shelf life of 6 to 9 months without refrigeration.

By Distribution Channel: Online Retail Surges on Subscription and Direct-to-Consumer Models

In 2025, supermarkets and hypermarkets led distribution with a 50.24% share, driven by their strong shelf presence and active promotional efforts. At the same time, online retail channels are projected to grow at a 10.24% CAGR through 2031, highlighting the industry's transition toward subscription models and direct-to-consumer fulfillment. Urban areas, supported by efficient last-mile delivery and advanced cold-chain logistics, exhibit the highest e-commerce penetration. Conversely, rural regions face challenges due to inadequate infrastructure. Convenience stores, which cater to immediate consumption needs, are increasing their lactose-free SKU offerings as consumer awareness rises. Single-serve PET bottles and flavored variants are particularly popular in this segment. Specialty stores, such as health food retailers and organic markets, continue to command premium pricing but are losing market share as mainstream channels expand their assortments.

HoReCa (hotels, restaurants, and catering) channels are incorporating lactose-free milk to meet dietary preferences and enhance their beverage menus. Prominent coffee chains like Starbucks and Costa Coffee now include lactose-free options as standard offerings. The growth of the online channel is further supported by targeted digital advertising and influencer collaborations, which effectively drive product trials among younger, digitally savvy consumers. However, the economics of cold-chain e-commerce remain challenging. High last-mile delivery costs often surpass product margins, prompting businesses to implement minimum order values and encourage subscription commitments to achieve profitability.

Geography Analysis

In 2025, North America accounted for 33.20% of global revenue, supported by established brands such as Fairlife, Lactaid, and Organic Valley. Key drivers included extensive retail penetration and consumer familiarity with lactose-free claims. The United States leads the region, driven by a high prevalence of lactose intolerance and increasing awareness among non-intolerant consumers about digestive health benefits. Canada is experiencing significant growth in its organic and premium segments, while Mexico's market is expanding due to rising disposable incomes and improvements in cold-chain infrastructure. However, intense competition from plant-based alternatives, oat, almond, and soy, is squeezing margins. This competition is pushing dairy processors to focus on fortification, flavor innovation, and sustainability claims to differentiate their offerings. Despite pricing pressures from a mature retail landscape and high private-label penetration, the established base of lactose-free consumers provides a stable revenue foundation, enabling incremental innovations.

Asia-Pacific is projected to grow at a CAGR of 9.51% through 2031, making it the fastest-growing region. This growth is primarily driven by lactose intolerance rates exceeding 90% in countries such as China, Japan, South Korea, and Southeast Asia. China's growing middle class and increasing dairy consumption are creating strong demand, although plant-based alternatives and traditional soy-based beverages remain significant competitors. Japan's aging population and health-conscious consumers are driving demand for premium lactose-free products. Australia and New Zealand benefit from strong domestic dairy production and export-oriented strategies. In India, where lactose intolerance affects around 70% of the population, the market is still developing. Challenges such as low awareness and affordability persist, but urbanization and the expansion of organized retail are gradually unlocking demand.

Europe remains a mature and competitive market, with private-label products accounting for over 40% of sales in key countries like the United Kingdom, Germany, and France. This high penetration is compressing margins for branded products, prompting differentiation through organic certification, fortification, and sustainable packaging. According to industry data, the United Kingdom and Germany lead in per-capita consumption and lactose-free dairy product launches. Sweden and the Netherlands show high awareness and acceptance of lactose-free products, while Southern European countries like Spain and Italy have lower penetration due to cultural preferences for traditional dairy and lower rates of diagnosed lactose intolerance. European Union Regulation 1308/2013, which harmonizes regulations, facilitates cross-border trade but also increases competition as processors from low-cost production regions enter premium markets. In Latin America and the Middle East, rising disposable incomes, urbanization, and growing health awareness are driving market development. However, challenges such as underdeveloped cold-chain infrastructure, price sensitivity, and low awareness are limiting short-term growth. Brazil and Argentina are leading demand in Latin America, while the United Arab Emirates and Saudi Arabia are key markets in the Middle East. Halal certification adds an additional compliance requirement, favoring established multinational players.

Competitive Landscape

The lactose-free milk market is moderately consolidated, with multinational dairy cooperatives such as Arla Foods amba, Fonterra Co-operative Group, and Nestlé S.A. vie for market share alongside regional processors and private-label manufacturers. While scale advantages in enzyme sourcing, cold-chain logistics, and retail distribution pose barriers to entry, niche players carve out their space through organic certification, ultra-filtration technology, and direct-to-consumer models. Fairlife's ultra-filtration technology, which adeptly concentrates protein while eliminating lactose, has secured a premium market position, a feat competitors find challenging to match without significant capital investment. In European markets, private-label products are gaining traction, propelled by retailers' strategies to capture margins and provide value alternatives. Yet, branded players defend their territory through innovation, marketing, and fortification claims that justify their premium pricing.

Key players are not only expanding the production capacity of their existing plants but are also heavily investing in research and development to craft products that resonate with evolving consumer tastes. Moreover, these industry stalwarts are broadening their geographical footprint, tapping into previously unexplored markets, and bolstering distribution capabilities across both offline and online platforms. Simultaneously, local brands specializing in lactose-free dairy products are making their debut in emerging markets. Dominating the landscape are major players like Arla Foods amba, Organic Valley, The Coca-Cola Company, Fonterra Co-operative Group, and Nestlé S.A.

Emerging disruptors, such as precision fermentation startups like Perfect Day, are making waves. Their collaboration with Unilever to debut Breyers lactose-free chocolate frozen dessert in February 2024 showcases a groundbreaking approach: eliminating lactose at the molecular level, sidestepping traditional enzymatic post-processing. Should this technology achieve economic scalability, it holds the potential to challenge conventional dairy processors by slashing processing costs and enhancing shelf stability. Notably, there's a burgeoning demand in flavored, organic, and fortified segments, where consumers are willing to pay a premium. This demand is further buoyed in emerging markets, where both awareness and distribution networks are on the rise. Yet, the landscape isn't without its challenges. Plant-based alternatives from Oatly, Danone, and regional contenders are setting a competitive ceiling, especially among the younger, eco-conscious demographic that perceives dairy as less sustainable. The competitive landscape is further intensified by retailer consolidation, amplifying buying power and compelling processors to shoulder promotional costs to secure shelf space.

Lactose-Free Milk Industry Leaders

-

Arla Foods amba

-

The Coca-Cola Company

-

Organic Valley

-

Nestlé S.A

-

Fonterra Co-operative Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Hiland Dairy has expanded its lactose-free product lineup with the introduction of Fresh Lactose-Free Milk. This new offering provides a tasty, premium choice for those who are lactose intolerant.

- July 2024: Garelick Farms, a brand under Dairy Farmers of America, has launched a fresh lactose-free milk that is easier to digest while providing the same vitamins and nutrients as regular milk.

- May 2024: Brooklyn Creamery introduced India's first high-protein, lactose-free, and fat-free milk. This unflavored and unsweetened high-protein milk integrates effortlessly into any health-conscious lifestyle.

Global Lactose-Free Milk Market Report Scope

Lactose-free milk is regular dairy milk with the lactose sugar broken down into simpler sugars (glucose and galactose) by adding the lactase enzyme. The lactose-free milk market is segmented by product type, fat content, category, packaging type, distribution channels, and geography. By product type, the market is segmented into liquid and powder. By fat content, the market is segmented into whole milk, semi-skimmed/low-fat milk, and skimmed/fat-free milk. By category, the market is segmented into plain and flavored. By packaging type, the market is segmented into PET bottles, glass bottles, cartons, and others. By distribution channel, the market is segmented into HoReCa and retail. The retail segment is further segmented into supermarkets and hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, the Middle East and Africa. The market forecasts are provided in value terms in USD and volume terms liters for all the abovementioned segments.

| Liquid |

| Powder |

| Whole Milk |

| Semi-Skimmed/Low-Fat Milk |

| Skimmed/Fat-Free Milk |

| Plain |

| Flavored |

| PET Bottles |

| Glass Bottles |

| Carton |

| Others |

| HoReCa | |

| Retail | Supermarkets and Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Liquid | |

| Powder | ||

| By Fat Content | Whole Milk | |

| Semi-Skimmed/Low-Fat Milk | ||

| Skimmed/Fat-Free Milk | ||

| By Category | Plain | |

| Flavored | ||

| By Packaging Type | PET Bottles | |

| Glass Bottles | ||

| Carton | ||

| Others | ||

| By Distribution Channel | HoReCa | |

| Retail | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the lactose-free milk market in 2026?

The lactose-free milk market size reached USD 13.80 billion in 2026 and is projected to climb to USD 21.64 billion by 2031.

What CAGR is expected between 2026 and 2031?

The market is forecast to expand at a 9.41% CAGR from 2026 to 2031.

Which region will grow the fastest through 2031?

Asia-Pacific is projected to post the highest regional CAGR at 9.51%, driven by high intolerance prevalence and rising dairy consumption.

Which product segment leads by revenue?

Liquid lactose-free milk accounted for 91.28% of revenue in 2025 due to convenient ready-to-drink formats.

Page last updated on: