Size and Share of Enterprise Resource Planning Market in Schools

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

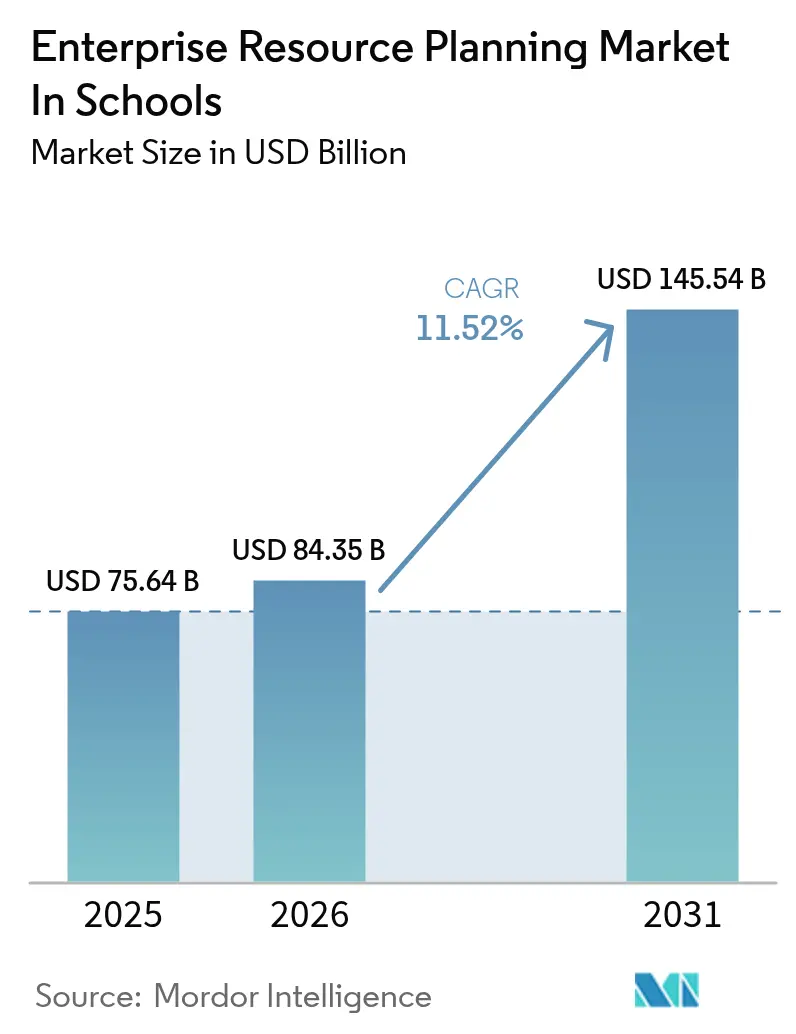

| Market Size (2026) | USD 84.35 Billion |

| Market Size (2031) | USD 145.54 Billion |

| Growth Rate (2026 - 2031) | 11.52% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Enterprise Resource Planning Market in Schools by Mordor Intelligence

The enterprise resource planning market size in schools market size is expected to grow from USD 75.64 billion in 2025 to USD 84.35 billion in 2026 and is forecast to reach USD 145.54 billion by 2031 at 11.52% CAGR over 2026-2031. Mandatory financial-transparency rules, API-based microservices that shorten upgrade cycles, and hybrid learning models that fuse physical and virtual classrooms continue to create tailwinds. Districts replacing spreadsheets with audit-ready ledgers, open architectures that let administrators bolt on new modules, and the desire to track student engagement across every location are reinforcing procurement urgency. Competitive moves by SAP, Oracle, and Microsoft to re-engineer higher-education suites for K-12, alongside pure-play specialists that bundle instruction and administration, are compressing buying cycles as boards weigh end-to-end suites against modular picks. On the demand side, small schools now enter the conversation because SaaS pricing slashes capital outlays, while large districts refresh legacy systems to comply with lease-accounting and data-privacy mandates. Supply-side momentum also reflects cloud-native vendors targeting Africa and Latin America with mobile-first interfaces that work in low-bandwidth settings.

Key Report Takeaways

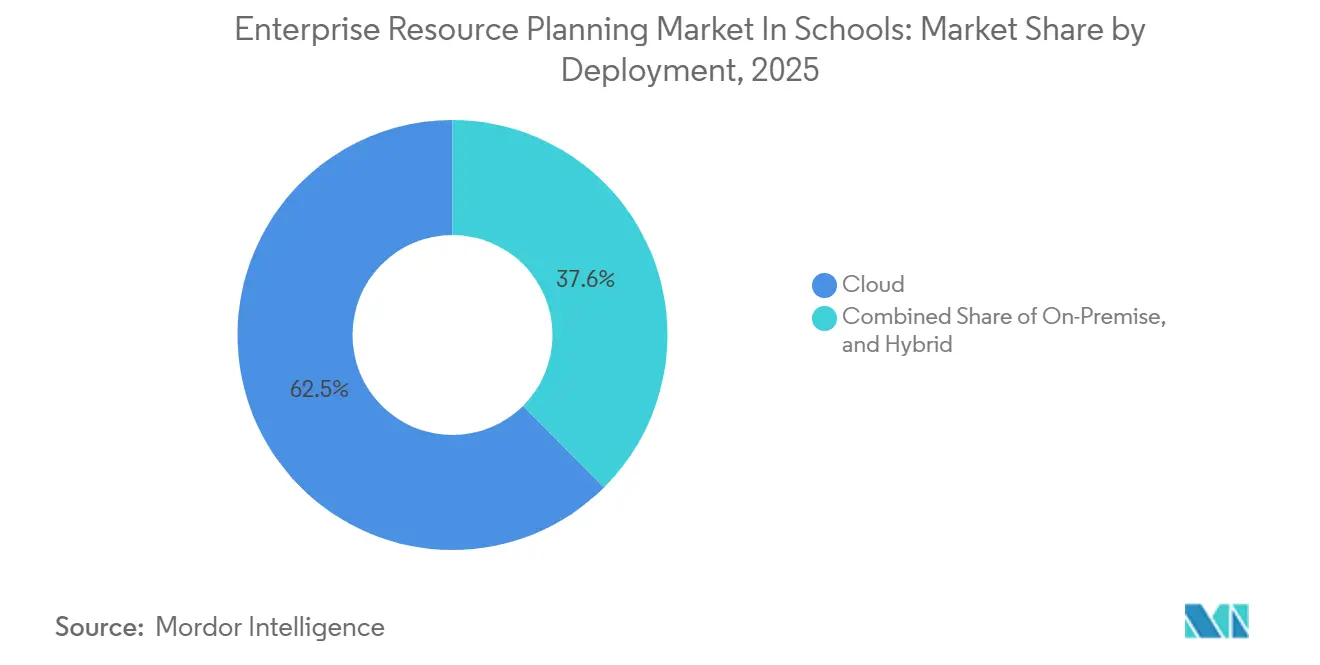

- By deployment, cloud deployment led with a 62.45% Enterprise Resource Planning Market in Schools market share in 2025, while hybrid architectures are advancing at a 15.85% CAGR through 2031.

- By function, administration functions commanded 24.10% of 2025 spending, whereas transportation management is set to grow 15.35% annually to 2031.

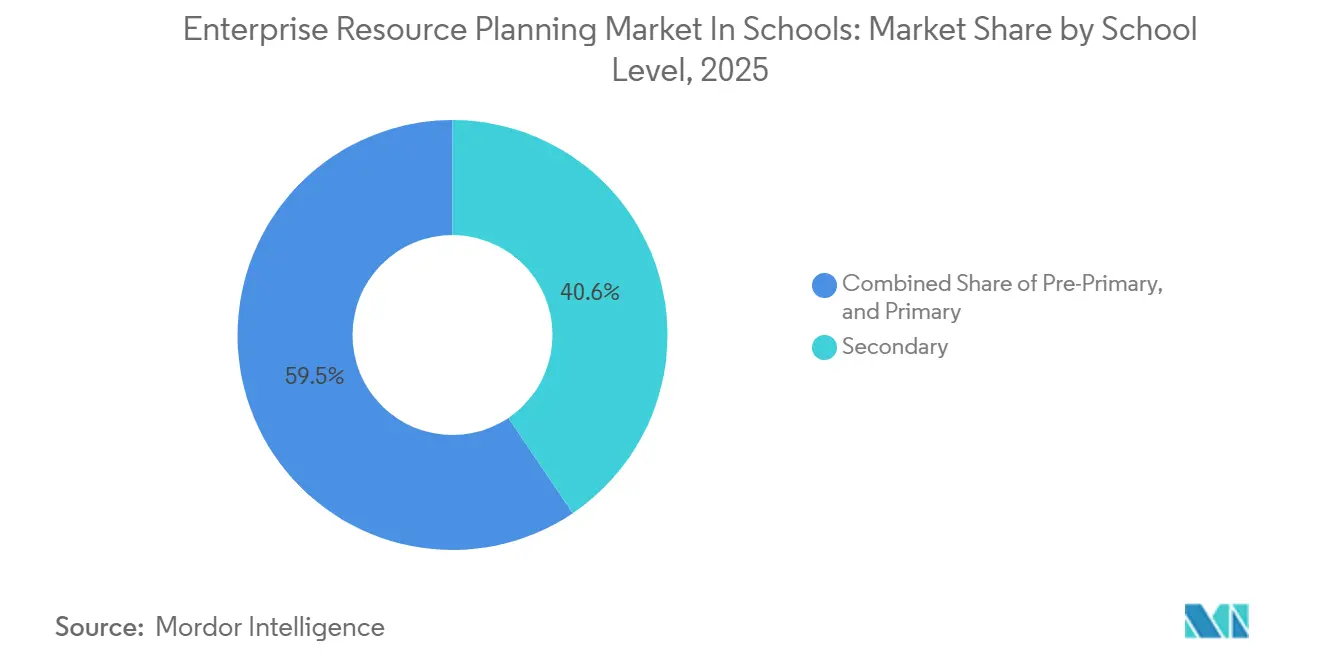

- By school level, Secondary schools held 40.55% of total revenue in 2025, yet pre-primary institutions exhibit the fastest 16.05% CAGR to 2031.

- By institution size, large schools (>2,000 students) captured 37.40% of 2025 revenue, but small schools (<500 students) show a leading 16.90% CAGR.

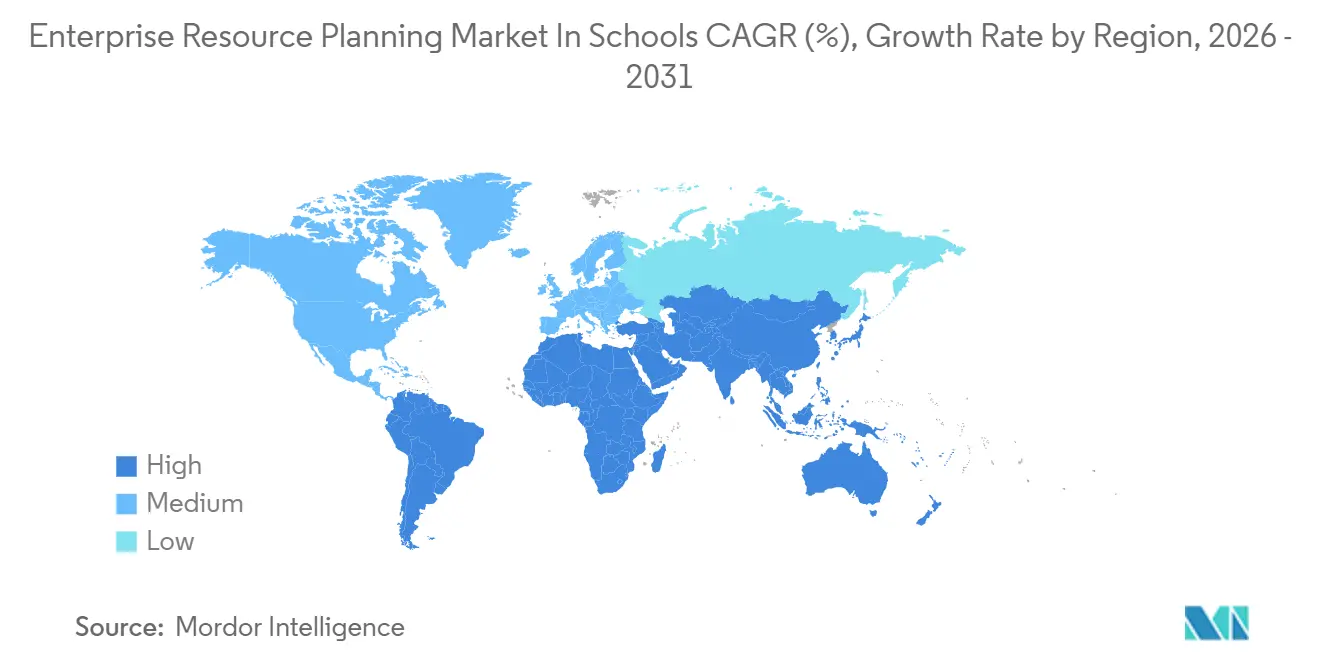

- By geography, North America retained a 33.65% revenue share in 2025, even as Africa posts the highest 16.20% regional CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of Enterprise Resource Planning Market in Schools

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consistent Data Availability | +3.2% | Global, early in North America and Europe | Medium term (2-4 years) |

| Real-Time Data Analytics Adoption | +2.8% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) |

| Increasing Use of Education Software | +2.5% | Global, emphasis in Asia-Pacific and Latin America | Long term (≥ 4 years) |

| Hybrid Learning Models | +2.3% | Global, spill-over from North America to emerging mkts | Medium term (2-4 years) |

| Government Financial-Reporting Mandates | +2.1% | North America, Europe, select Asia-Pacific markets | Short term (≤ 2 years) |

| API-Based Microservices | +1.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consistent Data Availability Across the School Business for Faster Decision Making

Unified data repositories are shrinking decision lead times from weeks to hours, enabling finance committees to shift cash among programs mid-year rather than conduct retrospective audits. Oracle Cloud ERP deployments in U.S. districts during 2024 trimmed budget-revision cycles by 40% once manual reconciliation disappeared.[1]Oracle Corporation, “Cloud ERP for Education,” oracle.com Predictive dashboards embedded in SAP S/4HANA Education flagged overruns before the fiscal quarter ended, letting purchasing teams freeze discretionary spend and avert year-end deficits. Medium and large districts with multiple campuses accrue the greatest gains because cross-site consolidation has historically delayed action.

Real-Time Data Analytics Adoption

Power BI integration with Dynamics 365 turns raw transaction logs into predictive dashboards that expose correlations such as the 30% higher dropout risk for students who miss morning buses, a pattern that pushed several districts to reroute transport and extend cafeteria hours. With analytics moving ERP from compliance ledger to strategic planning engine, boards now run what-if scenarios for opening new grade levels or closing satellite campuses during live sessions. ISO 27001 frameworks, while not mandated, increasingly appear on RFP checklists as parents demand evidence of anonymization in analytics pipelines.

Increasing Use of Education Software in Academics

The line between instructional and administrative workflows is fading. PowerSchool’s 2024 Kinjo acquisition fused lesson plans, quizzes, and gradebooks with finance and HR on a single database, ending nightly sync errors. India’s Digital India program steers grants toward integrated suites, prompting Tata Consultancy Services to launch a bundled ERP that unites classroom, payroll, and procurement for the country’s 1.5 million schools. Although integrated suites elevate switching costs, districts gain assurance that all student interventions appear instantly on transcripts.

Emergence of Hybrid Learning Models Accelerating Integrated ERP Demand

U.S. federal guidance issued in 2024 mandates that instructional minutes count equally whether delivered online or in person, forcing districts to log virtual attendance inside ERP systems for funding eligibility. Infor CloudSuite Education captures video-conference durations and pushes the data to finance modules for precise per-pupil allocation. Adoption peaks in regions with uneven connectivity, where offline tablet entries sync once bandwidth is available, underscoring why hybrid architectures on-premise student records mixed with cloud analytics are no longer transitional but permanent.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Difficulties in Customization | -1.8% | Global, acute in small and rural schools | Medium term (2-4 years) |

| High Initial Implementation Costs | -1.5% | Africa, Latin America, rural Asia-Pacific | Short term (≤ 2 years) |

| Data Privacy and Compliance Concerns | -1.2% | Global, heightened in North America and Europe | Long term (≥ 4 years) |

| Shortage of ERP-Literate Staff | -1.0% | Global, most severe in under-resourced districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Difficulties in Customization According to Business Needs

Off-the-shelf chart-of-accounts templates often clash with existing payroll cycles or local reporting codes. A 2024 Consortium for School Networking study showed 42% of districts halting pilots because required customizations voided support warranties.[2]Consortium for School Networking, “ERP Implementation Survey,” cosn.org Each upgrade risks breaking bespoke code. Tyler Technologies now offers a no-code workflow builder, yet training remains a hurdle for small offices.

High Initial Implementation Costs

GAO analysis revealed mid-sized districts underestimated ERP roll-outs by 35%, largely due to data-cleansing labor and temporary productivity dip during cut-over. In Africa and Latin America, capital constraints pit ERP against roof repairs or teacher hiring. SaaS spreads costs, but fixed fees become inflexible when enrollment shrinks, pressing small schools to justify per-student ERP costs three to five times those of large districts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Hybrid Architectures Gain Traction

Hybrid models represent the fastest-growing deployment option at a 15.85% CAGR, compared with the 62.45% cloud enterprise resource planning market in schools market share recorded in 2025. Hybrid solutions keep sensitive student identifiers on local servers while pushing anonymized data to cloud analytics, satisfying sovereignty laws in Germany and Japan without sacrificing scalability. The United Kingdom now demands data-protection impact assessments before any records move off-premise, pushing districts to store core SIS on-site and shift reporting workloads to the cloud. Microsoft’s Azure Stack for Education allows Dynamics 365 components to run locally while syncing metadata to the cloud, reinforcing the end-state nature of hybrid deployments.

Hybrid ecosystems also lower failure risk; if connectivity drops, onsite transaction processing continues. Infor CloudSuite Education offers encrypted APIs to shuttle finance entries to cloud-based transportation dashboards, illustrating how vendors partition workloads along privacy lines. On-premise installations, still favored by large U.S. districts, face budget scrutiny as server refresh cycles approach, whereas pure-cloud adoption dominates small schools that lack data-center talent.

By Function: Transportation Emerges as Growth Leader

Transportation software is forecast to advance 15.35% yearly through 2031, outpacing all other functions even though administration held a 24.10% enterprise resource planning market in schools market share in 2025. The catalyst lies in GPS-based route optimization, which shows immediate fuel savings and satisfies parent demand for live bus tracking. Tyler Technologies integrates fuel costs directly into GL accounts, letting finance teams calculate per-student transportation expenses and identify routes eligible for consolidation.

Payroll and finance modules, though already widespread, evolve slowly because upgrades deliver marginal gains relative to sunk investments. PowerSchool’s unified Kinjo platform blends lesson plans with purchasing flows so that textbook requisitions align with syllabus timelines. Facilities and food-service modules remain niche but grow when districts link IoT sensors for energy management or cafeteria counts, using ERP analytics to forecast menu demand.

By School Level: Pre-Primary Adoption Accelerates

Pre-primary institutions clock a 16.05% CAGR through 2031 as digital attendance becomes mandatory for subsidy disbursement, while secondary schools commanded 40.55% of 2025 revenue owing to complex timetabling needs. Blackbaud’s early-childhood module logs diaper-changes and nap-time, complying with licensing in 12 states. Parent portals that push real-time updates build loyalty and justify tuition premiums.

Primary schools adopt at moderate speed; their simpler scheduling needs and smaller staff reduce urgency, yet transparency rules still require digital ledgers. Higher secondary institutions add modules that feed exam scores to college-application portals, a selling point for competitive families. GDPR adds impetus across Europe, as deletion requests and consent logging overwhelm spreadsheets.

By Institution Size: Small Schools Narrow the Gap

Small schools under 500 students are growing at a 16.90% CAGR, even though large institutions >2,000 students held a 37.40% enterprise resource planning market in schools market size share in 2025. Focus School Software strips away multi-currency and complex approval chains, letting rural administrators master core functions within days. SaaS tiers charge lower annual fees for storage caps that small offices rarely breach.

Medium schools (500-2,000 students) weigh modular roll-outs, often starting with finance and payroll before adding transportation. Data migration and staff training do not scale down proportionally. Vendors respond with templated chart-of-accounts and guided import tools, yet the learning curve persists when veteran bookkeepers retire.

Geography Analysis

Africa leads global growth with a 16.20% CAGR, propelled by Kenya’s mandate for daily mobile attendance submissions and South African startups bundling ERP with outcome-based education templates. Donor agencies funnel grants contingent on verified digital records, prompting schools to leapfrog desktops and adopt mobile-cloud solutions that work offline and resync later. The region’s procurement cycles favor vendors offering pay-as-you-go models denominated in local currencies, hedging FX risk for rural districts.

North America held a 33.65% enterprise resource planning market in schools market share in 2025, but expansion has plateaued as most districts already run core finance modules. Growth now stems from replacement deals, driven by GASB lease rules and the sunset of on-premise support contracts. Vendors differentiate via migration accelerators that port historical data into cloud-hosted ledgers without extended downtime.

Europe converges on hybrid architectures; the United Kingdom demands data-protection impact assessments, and Germany restricts cross-border backups. France’s national education portal mandates API submissions, pushing schools toward suites with certified connectors. India showers grants on cloud ERP linked to its national portal, while China leans on local-cloud or on-premise deployments, citing data sovereignty. Japan and Australia publish interoperability standards, making open APIs table stakes. Latin America’s urban private schools deploy parent-facing portals to attract middle-class families, whereas public systems adopt modules incrementally as budgets allow. Gulf states bundle ERP with IoT sensors under “smart campus” programs, raising functionality expectations for vendors seeking regional tenders.

Competitive Landscape

The Enterprise Resource Planning for Schools market remains moderately fragmented; the top five vendors, SAP, Oracle, Microsoft, PowerSchool, and Blackbaud, hold roughly 45% combined share. Enterprise giants re-engineer higher-education suites downward, adding K-12-specific modules for transportation and cafeteria management, while specialists expand upward into finance to deliver unified contracts. PowerSchool’s Kinjo purchase exemplifies a bundling strategy, driving single-vendor lock-in and reducing nightly data sync delays.

Open-source challengers such as OpenEduCat and Kuali compete on price and customization, releasing 2024 updates that permit modular cloud or on-premise deployments without breaking support terms. Technology differentiation now revolves around embedded analytics; Microsoft’s Power BI dashboards correlate attendance with meal participation, guiding interventions. SAP embeds predictive cost-overrun alerts, enabling pre-emptive budget freezes.

Regulatory compliance acts as a moat. Vendors boasting ISO 27001 certification and connectors to state portals enter shortlists early, while laggards struggle even at discount pricing. The white space lies in early-childhood centers and small schools, where specialized features and lightweight interfaces trump enterprise breadth. Strategic alliances with telecom operators in Africa and EdTech accelerators in Latin America further broaden reach without heavy in-country sales teams.

Leaders of Enterprise Resource Planning Market in Schools

SAP SE

Oracle Corporation

Microsoft Corporation

Infor Inc.

Ellucian Company L.P.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: PowerSchool completed its Kinjo acquisition, unifying lesson plans, assessment, and transcripts in a single database.

- September 2024: Tyler Technologies signed a USD 12 million ERP contract with 15 Texas districts, including GPS route optimization.

- August 2024: Microsoft launched Azure Stack for Education, enabling hybrid Dynamics 365 deployments that satisfy data-sovereignty laws.

- July 2024: Oracle expanded Cloud ERP for Education with facilities and procurement modules, automating reorder triggers.

Scope of Report on Enterprise Resource Planning Market in Schools

The Enterprise Resource Planning (ERP) Schools Market covers software solutions designed to streamline and centralize key administrative and academic functions within educational institutions. It includes deployment models such as on-premise, cloud, and hybrid, and spans a wide range of functions, including administration, payroll, academics, finance, transportation, and procurement and inventory. The market serves schools across all educational levels, from pre-primary to higher secondary, and across varying institutional sizes.

The Enterprise Resource Planning Market in Schools / Enterprise Resource Planning for Schools Market Report is Segmented by Deployment (On-Premise, Cloud, and Hybrid), Function (Administration, Payroll, Academics, Finance, Transportation, Procurement and Inventory, and Other Functions), School Level (Pre-Primary, Primary, Secondary, and Higher Secondary), Institution Size (Small Schools, Medium Schools, and Large Schools), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| On-Premise |

| Cloud |

| Hybrid |

| Administration |

| Payroll |

| Academics |

| Finance |

| Transportation |

| Procurement and Inventory |

| Other Functions |

| Pre-Primary |

| Primary |

| Secondary |

| Higher Secondary |

| Small Schools (<500 Students) |

| Medium Schools (500-2000 Students) |

| Large Schools (>2000 Students) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

| By Deployment | On-Premise | ||

| Cloud | |||

| Hybrid | |||

| By Function | Administration | ||

| Payroll | |||

| Academics | |||

| Finance | |||

| Transportation | |||

| Procurement and Inventory | |||

| Other Functions | |||

| By School Level | Pre-Primary | ||

| Primary | |||

| Secondary | |||

| Higher Secondary | |||

| By Institution Size | Small Schools (<500 Students) | ||

| Medium Schools (500-2000 Students) | |||

| Large Schools (>2000 Students) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Enterprise Resource Planning for Schools market in 2026?

The market reached USD 84.35 billion in 2026 and is set to grow to USD 145.54 billion by 2031 at an 11.52% CAGR over 2026-2031.

Which segment shows the fastest growth within school ERP deployments?

Hybrid architectures lead with a 15.85% CAGR through 2031 as districts balance data sovereignty with cloud scalability.

What functional module is expanding most quickly?

Transportation management is rising 15.35% per year, driven by GPS route optimization and parent demand for real-time tracking.

Which geographic region offers the highest growth opportunity?

Africa leads with a 16.20% CAGR thanks to mobile-first platforms and donor-funded digital initiatives.

Why are small schools now investing in ERP solutions?

SaaS pricing lowers upfront costs while auditors push for digitized procurement trails, resulting in a 16.90% CAGR for schools under 500 students.

What is driving the shift toward integrated instructional and administrative systems?

Acquisitions like PowerSchool-Kinjo unify lesson plans and finance data, eliminating duplicate entry and raising switching costs for districts.

Page last updated on: