Open Source Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

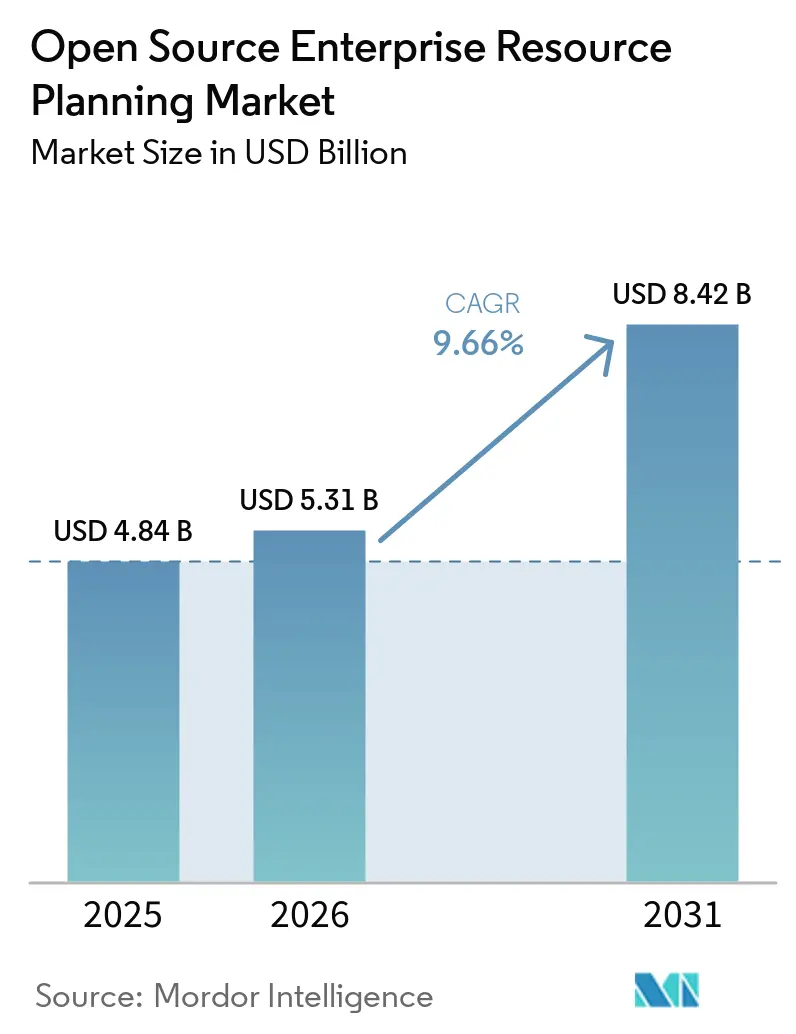

| Market Size (2026) | USD 5.31 Billion |

| Market Size (2031) | USD 8.42 Billion |

| Growth Rate (2026 - 2031) | 9.66% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

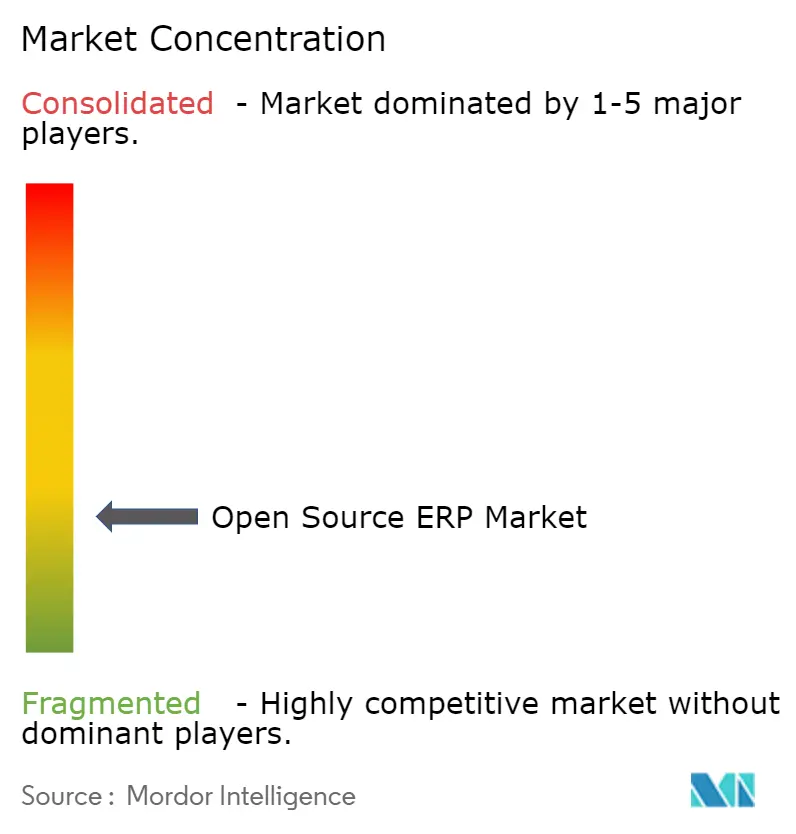

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Open Source Enterprise Resource Planning Market Analysis by Mordor Intelligence

The open source enterprise resource planning market size in 2026 is estimated at USD 5.31 billion, up from USD 4.84 billion in 2025, with 2031 projections showing USD 8.42 billion, growing at a 9.66% CAGR over 2026-2031. Enterprises are shifting from proprietary to community-driven stacks to secure vendor independence, simplify composable architecture, and expand low-code customization. Cloud deployment is the leading growth catalyst, as small and medium enterprises prefer capital-light rollouts that preserve cash flow. Services revenue is rising faster than software because organizations need integration support to connect open architectures with legacy systems. Artificial intelligence modules embedded in leading platforms now automate journal entries, forecast cash flow, and draft purchase orders, raising buyer expectations for real-time insights. Geographic momentum is strongest in the Asia-Pacific region, where government programs and a large small-business base accelerate digital modernization.

Key Report Takeaways

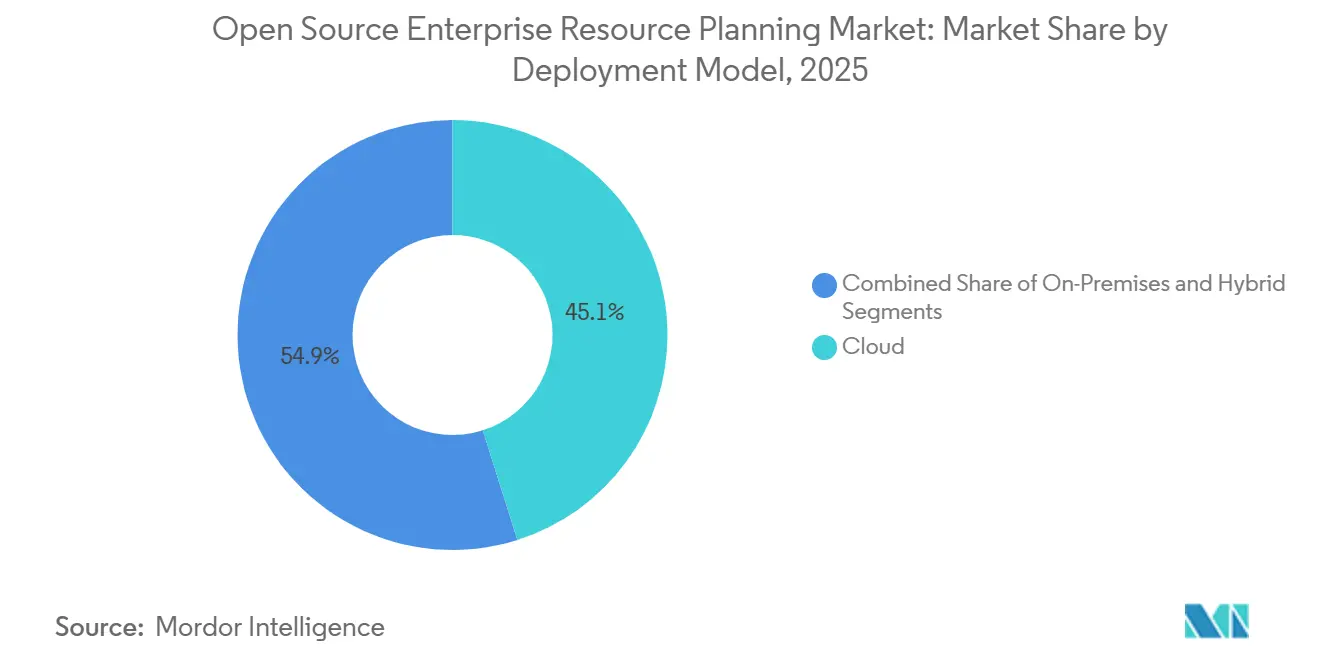

- By deployment model, cloud configurations captured 45.12% of the open source enterprise resource planning market share in 2025; hybrid and pure cloud implementations are forecast to expand at a 10.05% CAGR through 2031.

- By component, software accounted for 58.62% of the open-source ERP market in 2025, while services are projected to grow at a 9.74% CAGR through 2031.

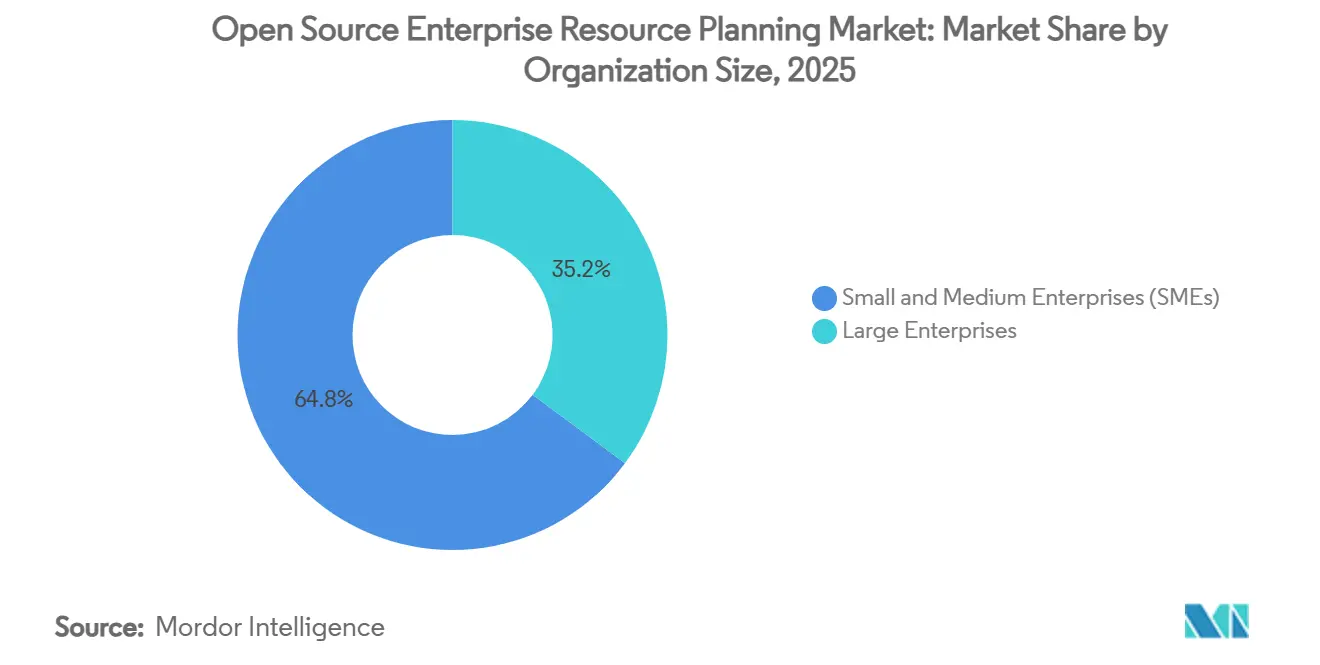

- By organization size, small and medium-sized enterprises accounted for 64.83% of the market share in 2025 and are projected to grow at a 9.79% CAGR through 2031.

- By end-use industry, manufacturing led with 26.74% of the share in 2025, whereas retail and e-commerce are projected to grow at a 11.09% CAGR through 2031.

- By geography, North America accounted for 36.40% of the market share in 2025; however, the Asia-Pacific region is recording the highest growth, with a 10.55% CAGR projected through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Open Source Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of Cloud Deployment Models Among SMEs | +2.1% | Global, concentrated in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Lower Total Cost of Ownership Compared to Proprietary ERP | +1.8% | Asia-Pacific, Latin America, Africa | Long term (≥4 years) |

| Rapid Digital Transformation Initiatives in Manufacturing Sector | +1.5% | Germany, United States, China, Japan, South Korea | Medium term (2-4 years) |

| Growing Preference for AI-Ready Open Source Stacks for Composable ERP | +1.3% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Government Import Substitution Policies Boosting Open Source Uptake | +0.9% | Russia, Brazil, Argentina, Bolivia | Short term (≤2 years) |

| Integration of Low-Code Platforms Accelerating Custom Module Development | +1.2% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Cloud Deployment Models Among SMEs

Cloud-hosted solutions are replacing on-premises installations because subscription-based infrastructure eliminates the need for servers and enables pay-as-you-grow pricing. Smaller firms value remote access to finance, inventory, and customer data, especially when teams are distributed across regions. Hybrid rollouts provide a bridge strategy by keeping sensitive ledgers on-premises while shifting procurement or CRM to public cloud, satisfying GDPR or similar residency rules while reducing hardware costs. Improved multi-tenant isolation now meets most security guidelines, encouraging even cautious sectors such as professional services to migrate. Overall, cloud growth accounts for more than one-fifth of the incremental revenue expected in the open source enterprise resource planning market.

Lower Total Cost of Ownership Compared to Proprietary ERP

Community editions eliminate license fees and reduce five-year ownership costs by 30-50%. Savings are decisive for firms with thin margins in retail, textiles, and light manufacturing. Expenses reappear if in-house talent is scarce, because external consultants can absorb 15-20% of first-year budgets for upgrades and security. Even so, proprietary suites impose change-order fees that can surpass initial contracts, whereas open code allows iterative changes without vendor approval. In price-sensitive regions such as Indonesia and Kenya, these factors tilt purchase decisions toward open-source ERP, widening the addressable market by thousands of new installations each year.[1]National Association of Software and Service Companies, “Digital Transformation in Indian MSMEs,” nasscom.in

Rapid Digital Transformation Initiatives in Manufacturing Sector

Industry 4.0 programs weave sensor data into planning modules to automate replenishment, quality checks, and maintenance. Modern plants demand an ERP that ingests real-time machine metrics and triggers procurement when stock falls below thresholds. Modular plugin architectures found in open stacks let manufacturers bolt predictive algorithms onto core finance without rewriting entire systems. Discrete segments such as consumer electronics and auto components are early beneficiaries, where just-in-time scheduling needs sub-hourly updates to shop-floor commands. As connected lines expand, manufacturers view market solutions as the least restrictive path to integrate operational technology with enterprise planning.

Growing Preference for AI-Ready Open Source Stacks for Composable ERP

Buyers now expect native connectors for large language models that automate invoice reconciliation, cash forecasting, and report summaries. Odoo’s 2024 release shipped a generative module that drafts purchase orders from plain-language inputs, while ERPNext added conversational queries for financial dashboards. Packaged business capabilities break monolithic suites into swappable components, so firms can refresh compliance or payroll modules without touching core GL. Pharmaceuticals and banking favor this approach to quickly meet evolving regulations. The result is accelerated release cycles that continue to enlarge the market as enterprises embrace composable designs.[2]Odoo, “Odoo Raises €500 Million at €5 Billion Valuation,” Company Press Release, odoo.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Availability of Enterprise-Grade Support Services | -1.4% | Africa, Middle East, smaller Asia-Pacific markets | Medium term (2-4 years) |

| Persistent Security and Compliance Concerns Around Community Versions | -1.1% | North America, Europe, BFSI, healthcare, government | Long term (≥4 years) |

| Shortage of Skilled Contributors to Maintain Critical Modules | -0.8% | North America, Western Europe, specific Asia-Pacific hubs | Long term (≥4 years) |

| Rising Fragmentation of Project Forks Creating Upgrade Complexity | -0.6% | Global multi-instance deployments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Availability of Enterprise-Grade Support Services

Many African and Middle Eastern enterprises hesitate to deploy community platforms because local integrators lack 24-hour support and certified consultants. Financial services firms in Kenya and Nigeria report that downtime penalties outweigh license savings, driving partial retention of proprietary suites. Several vendors are expanding managed hosting and premium SLA packages, yet coverage gaps persist in tier-2 cities. Partnerships between global providers and regional resellers are gradually closing the service deficit. Until a broader bench of experts exists, this restraint will subtract more than a single percentage point from overall CAGR.[3]Corteza, “Release Announcement: Low-Code Platform for Composable ERP,” cortezaproject.org

Persistent Security and Compliance Concerns Around Community Versions

CISA advisories in 2024 highlighted SQL injection and cross-site scripting flaws in widely used modules, intensifying scrutiny in healthcare and banking. Although patches often ship within days, risk teams perceive community QA processes as ad hoc. Compliance audits for HIPAA, PCI-DSS, or data localization require verifiable hardening standards that some community-built solutions do not document. Large enterprises mitigate risk by layering intrusion detection and external code scans, which add cost and complexity. As long as high-severity vulnerabilities persist, security concerns will constrain the open source enterprise resource planning market in regulated verticals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud Dominance Reshapes Infrastructure Strategies

Cloud captured 45.12% of the open-source ERP market share in 2025 and will expand the fastest, with a 10.05% CAGR. Edge computing nodes on factory floors now sync with cloud analytics to limit latency on production lines. Subscription hosting removes the need for server procurement and maintenance, freeing capital for customer acquisition or R&D. Hybrid strategies position sensitive ledgers or product formulas on-premises while moving procurement or CRM off-site, easing compliance with data sovereignty statutes. This phased approach minimizes downtime and enables gradual skills transfer, making the cloud the cornerstone of future spending in the open source enterprise resource planning market.

SMEs are the primary adopters because they can spin up sandboxes within hours and pay only for the resources they consume. Managed hosting providers bundle automatic backups, encryption, and patching, lowering administrative overhead. In transportation and logistics, cloud ERP integrates telematics data to improve dispatch planning and fuel optimization. Defense contractors and pharmaceutical labs still prefer on-premises instances for intellectual property protection, but pilots of secure tenant isolation models are underway. As certifications mature, the cloud’s appeal will broaden to sectors once considered off-limits, maintaining momentum for this segment.

By Component: Services Surge as Integration Complexity Escalates

Software modules accounted for 58.62% of revenue in 2025, as vendors monetize proprietary localizations, payroll, and tax extensions. Yet services will grow at 9.74% CAGR through 2031, reflecting labor required to knit ERP engines into payment gateways, data lakes, and IoT feeds. Organizations that lacked Python or Java experts now hire integrators for upgrades, custom reports, and security audits. A typical five-year total cost of ownership shows services consuming up to 70% of spending once community licenses erase software fees. Training and change management further expand service budgets as users navigate multiple composable applications rather than a single monolith.

Premium support contracts that guarantee response times under four hours are gaining popularity, especially in retail, where downtime means lost sales. Migration services convert proprietary customizations into open plug-ins, mitigating vendor lock-in. As composable architecture accelerates module churn, demand for ongoing integration retainer agreements will continue to rise, adding sustained revenue streams for consulting partners. The interplay between software and services, therefore, anchors long-term value capture across the open-source ERP market.

By Organization Size: SMEs Drive Adoption While Enterprises Hesitate

SMEs controlled 64.83% of market value in 2025 and are projected to post a 9.79% CAGR. Their lean IT teams choose community editions that provide core finance, inventory, and sales in a single package, with no license charges. India’s 31.6 million small businesses showcase this effect; local ERP implementers bundle managed hosting at monthly rates aligned with seasonal cash flow. Large enterprises, weighed down by historic proprietary investments, test open source ERP in regional subsidiaries before green-lighting global rollouts. Early success stories in Latin American retail chains demonstrate that corporate policy can shift once local pilots prove stable.

The open-source ERP industry has low entry barriers, enabling micro-firms to digitize invoices, payroll, and tax in days. Meanwhile, conglomerates explore incremental adoption by carving out non-critical assets, such as joint ventures or greenfield plants. Enterprise-grade audits, SSO integration, and worldwide support SLAs remain requirements for corporate endorsement. As commercial vendors expand these capabilities, more Fortune 500 firms are expected to join the open source enterprise resource planning market by decade-end.

By End-Use Industry: Retail Acceleration Outpaces Manufacturing Maturity

Manufacturing accounted for 26.74% of revenue in 2025, after decades of reliance on material requirements planning. However, retail and e-commerce will record the fastest 11.09% CAGR through 2031, as omnichannel operators need unified inventory and customer data across webstores and physical outlets. Open interfaces allow plug-ins to Shopify or regional payment gateways, accelerating time-to-value. Warehouses deploy barcode scanning that posts real-time inventory counts back to ERP, preventing stockouts. In fashion, rapid style cycles demand configurable product variants, which open stacks deliver via dynamic item attributes.

Healthcare, education, and public agencies adopt open source to stretch limited budgets. Hospitals run procurement and HR modules while preserving certified electronic medical records separately. Universities integrate tuition billing, dorm assignments, and alum donations into a single codebase without per-student charges. Banking adoption remains cautious, confined to general ledger or expense reconciliation that does not touch core transaction processing. These shifts collectively reinforce vertical diversity in the open-source ERP market.

Geography Analysis

Asia-Pacific has the fastest trajectory, advancing at a 10.55% CAGR, driven by India’s MSME digitization funds and China’s push to retire spreadsheet accounting in factories. Subsidies in South Korea’s Smart Manufacturing program reimburse up to 50% of ERP deployment costs, spurring pilot projects among component suppliers. In Southeast Asia, Vietnam and Indonesia leverage local integrators to customize open-source modules for multilingual tax filings, speeding up rollouts for exporters. North America holds 36.40% share, supported by mature SaaS ecosystems and abundant solution partners. Growth is steady as mid-market firms finish migrations from legacy on-premises systems. U.S. manufacturers use open-source stacks to connect machine monitoring with finance, while Canadian retailers leverage omnichannel capabilities to harmonize online and in-store inventory. Venture capital continues to back commercial vendors based in the region, underscoring confidence in the open source ERP market.

Europe shows bifurcated momentum. Germany and France advance through Industry 4.0 grants that favor domestic software. Eastern Europe and Russia grow faster because import-substitution policies channel state budgets toward domestic production.[4]Plattform Industrie 4.0, “International Cooperation with France,” plattform-i40.de Russia’s program funded 12 Industrial Competence Centers in 2024 to guide migrations away from foreign vendors, reducing licensing outflows. Meanwhile, Scandinavian nations are adopting open-source ERP in the public sector to improve transparency and reduce procurement costs.

Latin America rides regulatory catalysts. Brazil’s mandatory electronic invoicing requires companies to upgrade their ERPs to support real-time tax reporting. Argentina and Bolivia follow similar mandates, creating a rising tide for compliant open stacks. The region’s cloud infrastructure expansion reduces latency, encouraging more firms to shift workloads off-site. Africa is earlier in the curve, but promising. TradeMark Africa reports that over half a million firms already employ sophisticated digital tools. Programs in Kenya and Nigeria provide grants and training to accelerate adoption, ensuring future contributions to the open source enterprise resource planning market.

Competitive Landscape

The market remains fragmented. No single vendor exceeds a double-digit share because community projects and commercial hybrids coexist. Odoo’s November 2024 funding of EUR 500 million (USD 565 million) ranked among the largest software investments that year, signaling investor faith in the freemium plus premium model. ERPNext positions itself on rapid deployment and clean code, appealing to smaller firms in emerging markets. Axelor and iDempiere cultivate niche vertical modules, such as auto parts supply chain or process manufacturing, differentiating by domain depth rather than breadth.

Artificial intelligence is the new battleground. Odoo’s AI Tools Suite suggests GL account classifications, while Corteza’s low-code designers let business analysts assemble workflows without scripting. Tailor Platform pushes visual process mapping, lowering dependence on scarce developers. Integration marketplaces define ecosystem strength; vendors host hundreds of plug-ins for tax, KYC, CRM, and IoT connectors. Localization remains another wedge. Latin American startups embed regional payroll and e-invoicing rules that global players overlook, winning deals on compliance readiness.

System integrators gain strategic significance as enterprises assemble composable ERP from multiple projects. Their recurring revenue stems from API orchestration, data lake synchronization, and security hardening. White-space persists in healthcare, where ERP must exchange HL7 or FHIR messages with electronic health records. Similarly, BFSI modernization and government budgeting present untapped niches. These dynamics sustain vibrant competition and propel continuous innovation throughout the open source ERP market.

Open Source Enterprise Resource Planning Industry Leaders

Odoo SA

Frappe Technologies Private Limited

Axelor SAS

Dolibarr Foundation

Tryton Foundation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Retail and e-commerce operators increased adoption of open source ERP with native omnichannel tools that unify online and in-store inventory, underpinning the segment’s 11.26% CAGR projection.

- May 2025: Enterprises deepened the shift to composable, API-first ERP frameworks, using low-code builders to attach best-of-breed modules without large development teams.

- March 2025: Cloud ERP uptake surged across Asia-Pacific as India’s 31.6 million MSMEs adopted subscription deployments to avoid hardware spending, reinforcing the region’s 10.71% CAGR outlook through 2030.

- January 2025: Odoo SA broadened its AI automation suite by adding advanced natural language tools that generate journal entries and forecast cash flow, supporting the platform’s 65.49% SME user base.

Global Open Source Enterprise Resource Planning Market Report Scope

The Open Source ERP market encompasses software solutions and services that enable organizations to manage core business processes such as finance, supply chain, human resources, and customer relations through customizable, open-source platforms

The Open Source ERP Market Report is Segmented by Deployment Model (Cloud, and On-Premises, Hybrid), Component (Software, and Services), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-Use Industry (Manufacturing, Retail and E-Commerce, Healthcare, Banking, Financial Services and Insurance (BFSI), Information Technology and Telecom, Education, Government and Public Sector, and Other End-Use Industry), and Geography(North America, South America, Europe, Asia-Pacifc, and Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premises |

| Hybrid |

| Software |

| Services |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Manufacturing |

| Retail and E-Commerce |

| Healthcare |

| Banking, Financial Services and Insurance (BFSI) |

| Information Technology and Telecom |

| Education |

| Government and Public Sector |

| Other End-Use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Model | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Component | Software | ||

| Services | |||

| By Organization Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By End-Use Industry | Manufacturing | ||

| Retail and E-Commerce | |||

| Healthcare | |||

| Banking, Financial Services and Insurance (BFSI) | |||

| Information Technology and Telecom | |||

| Education | |||

| Government and Public Sector | |||

| Other End-Use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the open source enterprise resource planning market?

The open source enterprise resource planning market size is USD 5.31 billion in 2026.

How fast is the open source ERP market expected to grow?

It is projected to expand at a 9.66% CAGR to reach USD 8.42 billion by 2031.

Which deployment model is expanding the quickest?

Cloud configurations are growing at 10.05% CAGR through 2031, led by SME adoption.

Why are SMEs leading adoption of open source enterprise resource planning solutions?

SMEs value lower total cost of ownership and capital-light cloud rollouts, giving them 64.83% revenue share in 2025.

Which industry segment shows the fastest growth?

Retail and e-commerce is advancing at an 11.09% CAGR due to omnichannel inventory needs.

Which region holds the strongest future growth potential?

Asia-Pacific is forecast to expand at 10.55% CAGR, supported by digitization programs in India and China.

Page last updated on: