Eastern Europe Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

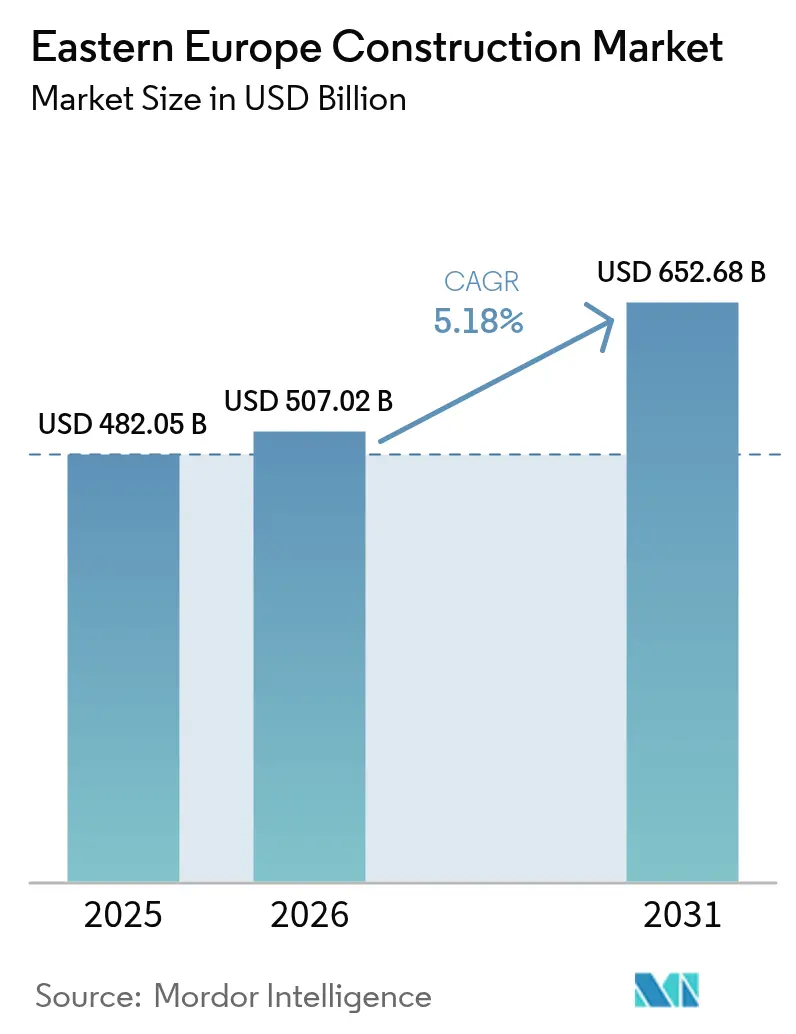

| Base Year Market Size (2025) | USD 482.05 Billion |

| Market Size (2026) | USD 507.02 Billion |

| Market Size (2031) | USD 652.68 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

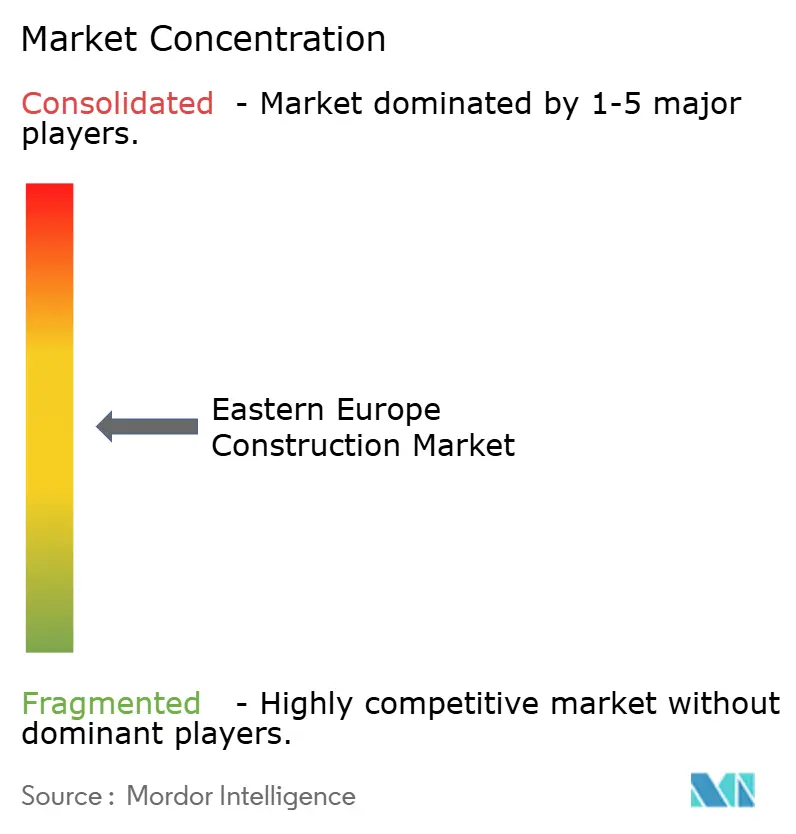

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Eastern Europe Construction Market Analysis by Mordor Intelligence

The Eastern Europe Construction Market size is expected to grow from USD 482.05 billion in 2025 to USD 507.02 billion in 2026 and is forecast to reach USD 652.68 billion by 2031 at 5.18% CAGR over 2026-2031. Current growth reflects the convergence of post-war reconstruction, accelerated European Union infrastructure modernization, and a sweeping renewable-energy build-out that is diverting sizeable capital toward transport, energy, and digital networks. Infrastructure remains the anchor segment, public programs continue to dominate financing, and Ukraine’s rebuilding efforts are drawing unprecedented flows of foreign direct investment. Private capital is returning on the back of gradually improving interest-rate conditions, while supply-chain constraints in cement and steel are nudging the industry toward vertical integration. Modern construction methods are beginning to shake up on-site traditions, driven by labor scarcity, building information modeling (BIM) mandates, and stricter carbon-reduction rules.

Key Report Takeaways

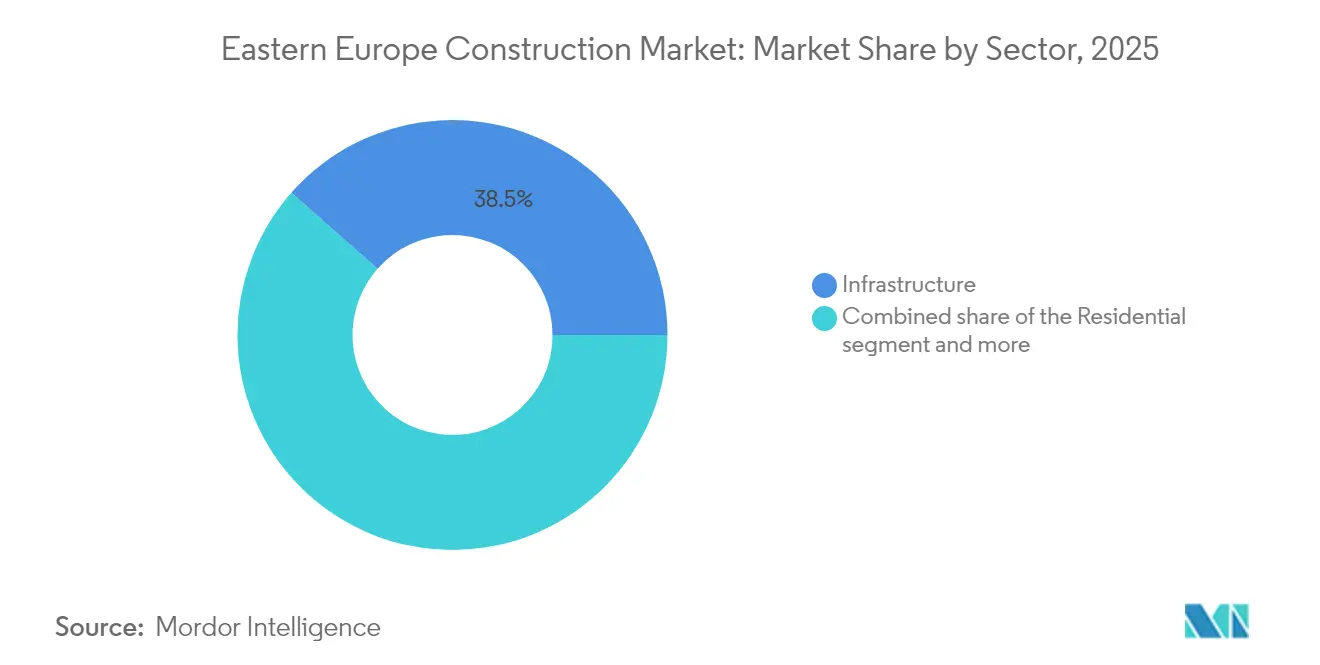

- By Sector, Infrastructure led with a 38.49% share of the Eastern Europe construction market in 2025, while the same segment is forecast to post the fastest 7.28% CAGR through 2031.

- By Construction type, New construction accounted for 60.85% of the Eastern Europe construction market size in 2025, whereas renovation activity is advancing at a 6.15% CAGR on aging asset upgrades.

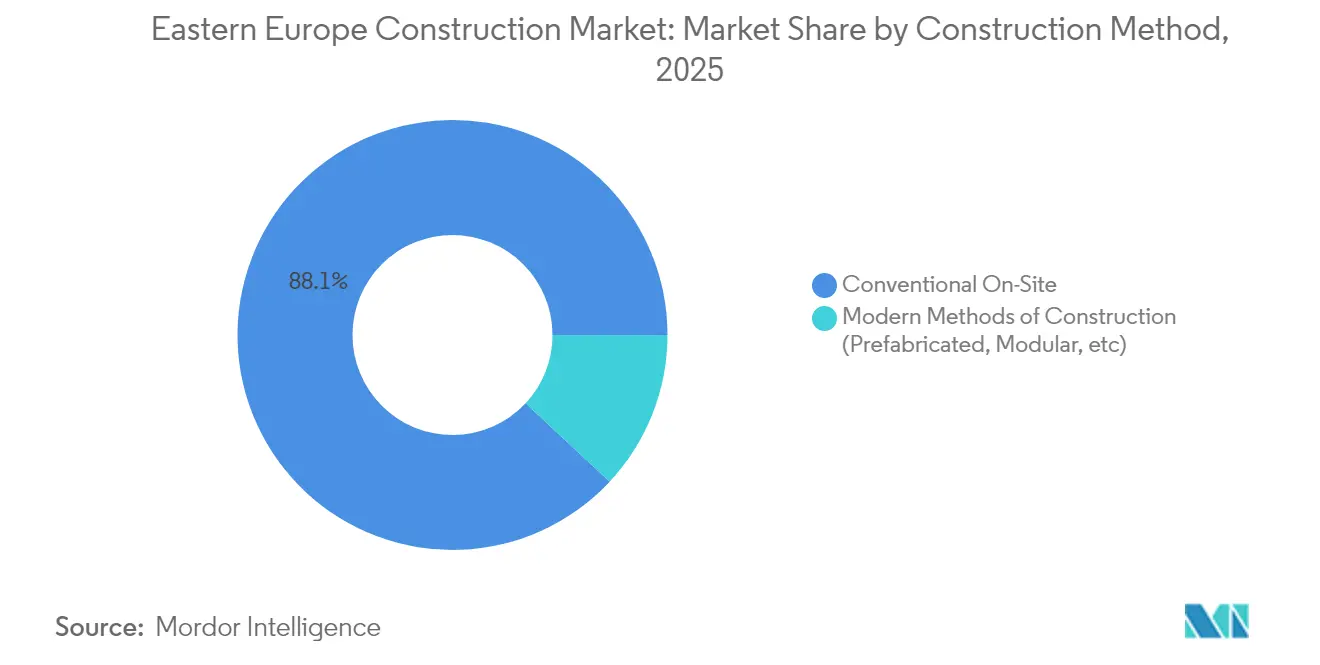

- By Construction Method, Conventional on-site building retained 88.05% of Eastern Europe construction market share in 2025; prefabricated and modular solutions are gaining momentum at a 8.65% CAGR to 2031.

- By Investment source, Public funding controlled 54.10% of 2025 spending, yet privately financed projects are pacing the field with a 7.45% CAGR through 2031 as investors re-enter reconstruction and renewables.

- By geography, Romania contributed 21.20% of 2025 regional revenue, whereas Ukraine is projected to log the quickest 6.78% CAGR on the back of multibillion-dollar recovery programs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Eastern Europe Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in EU-funded infrastructure programs | +1.8% | EU cohesion economies | Medium term (2-4 years) |

| Rapid build-out of renewable-energy assets | +1.5% | Romania, Hungary, Poland | Medium term (2-4 years) |

| Return of foreign direct investment into post-war Ukraine reconstruction | +1.2% | Ukraine and neighbors | Long term (≥ 4 years) |

| Demand spike for affordable multifamily housing in urban corridors | +0.9% | Bucharest, Warsaw, Budapest, Prague | Short term (≤ 2 years) |

| Digital-twin & BIM mandates in public procurement | +0.6% | Latvia, Poland, Czech Republic | Medium term (2-4 years) |

| Pre-fabricated timber modules to meet green-build quotas | +0.5% | Germany, Poland, Czech Republic | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in EU-Funded Infrastructure Programs

EU cohesion countries have been awarded EUR 25.8 billion (USD 28.1 billion) for 2021-2027 under the Connecting Europe Facility, unleashing large packages for rail, road, energy, and digital corridors. Hungary’s MAV rail upgrade alone combines EUR 1.0 billion (USD 1.1 billion) of European Investment Bank funding with national co-financing, underscoring the catalytic role of blended public capital. The 2024 CEF Transport call introduced an extra EUR 2.5 billion (USD 2.7 billion) and opened eligibility to Ukraine and Moldova, broadening the addressable project pipeline. Compliance with EU procurement law and environmental standards is incentivizing contractors to upgrade digital processes. Taken together, these measures anchor a multi-year backlog that is expected to keep civil-engineering order books full through the medium term[1]Adina Vălean, “Connecting Europe Facility 2024 Transport Call Launches,” European Climate, Infrastructure and Environment Executive Agency, cinea.europa.eu.

Rapid Build-Out of Renewable-Energy Assets

Eastern Europe’s energy transition is catalyzing construction demand across generation, transmission, and storage. The Green Energy Corridor that links Azerbaijan, Georgia, Hungary, and Romania represents a EUR 10 billion (USD 10.9 billion) opportunity to build 1,100 km of high-capacity lines capable of carrying 4 GW of clean power. Hungary has earmarked EUR 52.5 million (USD 57.2 million) to upgrade its network so it can triple solar capacity by 2030, requiring new substations and automation. In Romania, a 400 MW wind farm at Peștera II attracted EUR 30 million (USD 32.7 million) of EIB money, while the USD 93 million Pecineaga project is under construction. Ukrainian-owned DTEK is rolling out a 5 GW portfolio across four EU markets, channeling nearly USD 163 million into early-stage wind and solar parks. These investments are fast-tracking grid reinforcement, foundation works, and component installation across the region[2]Valdis Dombrovskis, “European Commission Approves €52.5 Million for Hungarian Grid Upgrade,” European Commission, ec.europa.eu.

Return of Foreign Direct Investment into Post-War Ukraine Reconstruction

The EU has endorsed EUR 50 billion (USD 54.4 billion) for Ukraine’s recovery, while total rebuilding needs are estimated at EUR 451 billion (USD 491.6 billion). Multinationals are positioning early: CRH has funneled USD 500 million into Ukraine since 1999, including USD 80 million after the 2022 invasion, and has taken over Dyckerhoff Cement Ukraine to secure cement supply. The Ukraine FIRST facility is offering technical aid for priority assets ranging from power grids to social housing. Domestic cement output stabilized at 7.97 million t in 2024, and exports multiplied to 1.7 million t, illustrating quick supply adaptation. FDI momentum is therefore lifting building-materials demand and bringing forward tender activity for critical infrastructure[3]Andriy Kostin, “Ukraine Facility for Infrastructure Reconstruction Technical Brief,” European Investment Bank, eib.org.

Demand Spike for Affordable Multifamily Housing in Urban Corridors

Household formation and shrinking unit sizes are pushing cities to accelerate apartment delivery. Cluj-Napoca’s housing stock expanded 12% from 2011-2018, with peri-urban districts absorbing the bulk of new supply as commuting infrastructure improved. Developers such as Kesz Group broke ground on the USD 54.5 million Corallis Apartments in Bucharest in 2024, a five-tower scheme scheduled for completion in 2027. Persistent affordability gaps and thin social-housing pipelines create a robust demand floor. Consequently, urban-residential work is likely to retain its share despite financing headwinds.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High interest-rate environment squeezing developer liquidity | -1.1% | Region-wide | Short term (≤ 2 years) |

| Acute skilled-labor shortages driving wage inflation | -0.8% | Czech Republic, Moldova, Poland | Medium term (2-4 years) |

| Chronic permitting delays tied to anti-corruption reforms | -0.6% | Romania, Poland, Czech Republic | Medium term (2-4 years) |

| Cross-border supply-chain chokepoints for cement & rebar | -0.4% | Poland-Ukraine frontier | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Interest-Rate Environment Squeezing Developer Liquidity

Policy rates have toggled between 4.5% and 8.1% since 2023, eroding debt-coverage ratios and scuttling some speculative schemes. The European Central Bank has since started trimming key rates, narrowing commercial-property yield spreads, and partially reviving deal flow. Private lenders have returned selectively to Central and Eastern Europe after a decade-long lull, but underwriting remains conservative. Developers, therefore, face a period of tight capital, likely to temper growth over the next two years.

Acute Skilled-Labor Shortages Driving Wage Inflation

Two-thirds of Czech construction firms reported unfilled positions in 2024, and Moldovan companies flagged shortages at 30%, up from 16% in 2021. Deloitte’s 2025 Central Europe real-estate survey ranks labor costs and availability ahead of financing as the sector’s most pressing challenge. Governments are tackling the gap through reskilling initiatives and relaxed visa regimes; Hungary and Greece have lightened entry rules for seasonal construction workers. Romania’s removal of wage tax breaks for site workers risks further cost escalation. Unless migration inflows offset domestic deficits, rising pay may compress contractor margins through the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure as Both Anchor and Accelerator

Infrastructure contributed 38.49% to 2025 revenue and is projected to rise at a 7.28% CAGR, the fastest among all sectors, thereby defining the growth vector of the Eastern Europe construction market size. Mega-rail projects such as Hungary’s EUR 2.162 billion (USD 2.4 billion) modernization and Romania’s cross-country motorway extensions are moving in lockstep with power-grid upgrades like the USD 10.9 billion Green Energy Corridor. Energy-infrastructure work is further supported by Hungary’s USD 57.2 million network upgrades aimed at tripling solar capacity by 2030.

Residential activity is mixed: urban apartment demand remains strong, as highlighted by Bucharest’s USD 54.5 million Corallis project, yet high rates and elevated land prices constrain mortgage affordability. Commercial work is pivoting toward low-carbon office retrofits, exemplified by Skanska’s timber-frame tower in Prague, while industrial and logistics builds benefit from near-shoring and e-commerce growth despite site-permitting frictions.

By Construction Type: Renovation Accelerates Under Efficiency Mandates

New builds maintained 60.85% of 2025 revenue, cementing their role as the largest slice of the Eastern Europe construction market share. However, renovation works are gathering pace at a 6.15% CAGR as Soviet-era assets undergo energy-efficiency retrofits to meet European performance standards. Ukraine offers a unique blend, where demining and partial rebuilding of utilities are prerequisites for full-scale new construction.

EU funding increasingly rewards deep-renovation projects, easing the financing of façade insulation, HVAC upgrades, and smart-meter installation. Space scarcity in city cores and permitting complexities further tilt economics toward adaptive reuse, particularly among commercial landlords needing to hit carbon-budget checkpoints.

By Construction Method: Prefabrication Edges Into the Mainstream

Conventional on-site techniques still controlled 88.05% of 2025 turnover, but modern methods are growing at a 8.65% CAGR, eroding the traditional dominance of the Eastern Europe construction market. Poland’s prefabricated share, at 6.5%, signals early traction compared with Germany’s 11%, while BIM mandates are compressing learning curves for modular workflows.

Latvia’s 2025 BIM requirement, combined with rising timber-module adoption, is expected to steer public tenders toward integrated off-site solutions. Prefabrication also mitigates skilled-labor shortages and accelerates deployment timelines, reinforcing its economic case across the region.

By Investment Source: Public Funds Hold the Majority, but Private Capital Gains Steam

Public budgets delivered 54.10% of 2025 spend, courtesy of EU cohesion envelopes and multilateral loans. The Connecting Europe Facility’s EUR 25.8 billion (USD 28.1 billion) allocation and Ukraine’s EUR 50 billion (USD 54.4 billion) recovery package underline the scale of taxpayer-backed financing.

Private outlays are picking up at a 7.45% CAGR, buoyed by sector-specific plays such as DTEK’s 5 GW renewables rollout and CRH’s cement-plant acquisitions. European Central Bank rate cuts and tightening green-asset supply are further tipping investors toward development pipelines, signaling a more balanced funding mix by the decade’s end.

Geography Analysis

Romania led regional revenue with a 21.20% share in 2025, leveraging its bridge position between Western Europe and the Black Sea. Ongoing works on the A3 motorway (USD 92.7 million) and the USD 93 million Pecineaga wind farm underscore the breadth of transport and energy pipelines. However, 2024 output dipped 4% after seven years of rapid gains as labor-tax relief expired and material inflation persisted.

Ukraine is poised for the fastest 6.78% CAGR through 2031, anchored by multilateral packages and a domestic cement industry that stabilized at 7.97 million t in 2024. Two new kiln lines are planned in Kryvy Rih and Ivano-Frankivsk, and the Ukraine FIRST facility is marshaling technical assistance for roads, hospitals, and energy hubs.

Secondary markets such as Hungary, Croatia, and Bulgaria benefit from EU cohesion funds and cross-border interconnectors. Hungary’s USD 1.1 billion rail overhaul and USD 57.2 million grid upgrade illustrate a pipeline rich in both civil-engineering and power-system opportunities. The second 400 kV Greece-Bulgaria link is already under construction, and the Green Energy Corridor adds a further USD 10.9 billion of grid work. Poland is emerging as a digital-procurement frontrunner, with BIM tenders and modular demand showing above-average growth potential.

Competitive Landscape

Eastern Europe’s construction arena is moderately fragmented, mixing global heavyweights with agile local specialists. Infrastructure megaprojects generally favor multinationals such as STRABAG, Skanska, and PORR, whose balance sheets and engineering depth satisfy complex-project criteria. Residential and commercial niches, by contrast, often award contracts to regional firms that can navigate municipal codes and client networks.

Strategic consolidation picked up in 2024 when Hungary’s Duna Aszfalt Zrt. Acquired 100% of Mota-Engil Central Europe, later re-branded Duna Polska, thereby enlarging its mining and road-building footprint. On the materials side, CRH’s purchase of Dyckerhoff Cement Ukraine secures local clinker supply and boosts vertical-integration leverage ahead of large-scale reconstruction.

Digital capabilities are emerging as a key differentiator. Contractors fluent in BIM and modular workflows tend to outscore rivals on public tender assessments in Latvia and Poland. Renewables represent a fresh battleground, with specialized EPC firms chasing DTEK’s 5 GW roll-out and grid-reinforcement contracts tied to the Green Energy Corridor. Supply-chain integration, particularly in cement and steel, offers scope for margin defense amid input-price volatility.

Eastern Europe Construction Industry Leaders

Strabag

Skanska

PORR

Budimex

Metinvest

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Romania obtained EUR 30 million (USD 32.7 million) from the European Investment Bank for the 400 MW Peștera II wind farm; construction started in 2025.

- February 2025: The EU granted EUR 15.4 million (USD 16.8 million) toward the 400 kV Bălți–Suceava line that will bolster Moldova–Romania interconnection; total project cost stands at EUR 77 million (USD 83.9 million).

- September 2024: Duna Aszfalt Zrt. bought 100% of Mota-Engil Central Europe S.A., renaming it Duna Polska S.A. to fortify its Central European presence.

- September 2024: CRH Ukraine BV finalized the acquisition of a 99.9775% stake in Dyckerhoff Cement Ukraine, adding two cement plants to its asset base and lifting cumulative investment in the country to USD 500 million.

Eastern Europe Construction Market Report Scope

The Eastern Europe construction market covers the growing construction projects in different sectors, like commercial construction, residential construction, industrial construction, infrastructure (transportation construction), and energy and utility construction and by Geography Romania, Hungary, Croatia, Ukraine, Bulgaria and Rest of Eastern Europe. Along with the scope of the report also it analyses the key players and the competitive landscape in the Eastern Europe Construction Market.

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

| New Construction |

| Renovation |

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

| Public |

| Private |

| Romania |

| Hungary |

| Croatia |

| Ukraine |

| Bulgaria |

| Rest of Eastern Europe |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Romania | |

| Hungary | ||

| Croatia | ||

| Ukraine | ||

| Bulgaria | ||

| Rest of Eastern Europe | ||

Key Questions Answered in the Report

What is the 2026 value of the Eastern Europe construction market?

The market was valued at USD 507.02 billion in 2026.

How fast is Eastern European construction expected to grow through 2031?

It is forecast to expand at a 5.18% CAGR, reaching USD 652.68 billion.

Which sector holds the biggest slice of regional spending?

Infrastructure leads with 38.49% of 2025 revenue.

Which country is growing the fastest?

Ukraine is projected to register a 6.78% CAGR through 2031.

What share does public funding hold in 2025?

Public sources accounted for 54.10% of spending.

How large is the prefabricated and modular opportunity?

Modern methods are expanding at a 8.65% CAGR, outpacing traditional on-site techniques.

Page last updated on: