Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

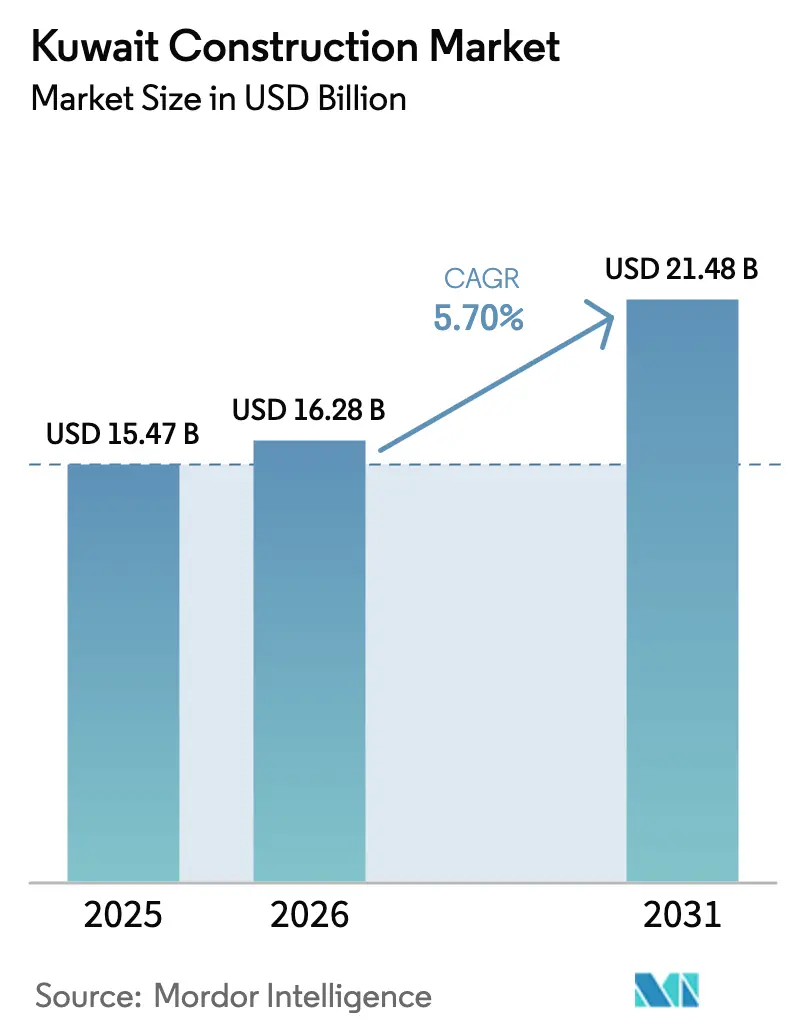

| Base Year Market Size (2025) | USD 15.47 Billion |

| Market Size (2026) | USD 16.28 Billion |

| Market Size (2031) | USD 21.48 Billion |

| Growth Rate (2026 - 2031) | 5.70% CAGR |

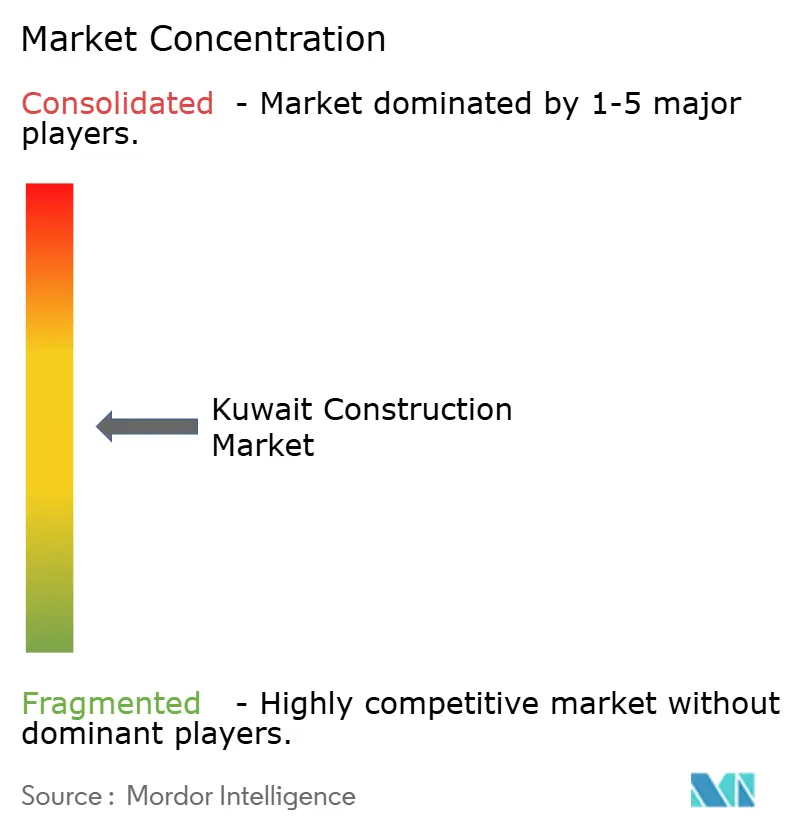

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kuwait Construction Market Analysis by Mordor Intelligence

The Kuwait Construction Market size is projected to expand from USD 15.47 billion in 2025 and USD 16.28 billion in 2026 to USD 21.48 billion by 2031, registering a CAGR of 5.70% between 2026 to 2031.

Robust public spending on Vision 2035 flagships, rising foreign direct investment, and an accelerating shift toward modular building methods are sustaining momentum despite tighter fiscal ceilings. Parliamentary suspension in May 2024 unblocked contract awards worth USD 1.9 billion during 2025, quadrupling 2024 levels and signaling a decisive move from planning to execution[1]MEED Editorial Team, “Kuwait Awards USD 1.9 Billion in 2025 Contracts". Residential activity dominates as the social-housing backlog reached 105,000 applications in 2025, driving a 6.93% CAGR that outpaces all other segments and underpinning aggressive mandates for 30% modular or 3D-printed components in public-housing starts. Private participation is climbing at 6.73% CAGR on the back of Kuwait Investment Authority co-investment platforms that have attracted more than USD 10 billion for mixed-use megaprojects such as Silk City and South Saad Al-Abdullah. Even so, conventional on-site techniques remain prevalent, capturing 93.23% of 2025 spending, while modern methods expand briskly at 7.93% CAGR under Ministry of Public Works mandates for factory-assembled components.

Key Report Takeaways

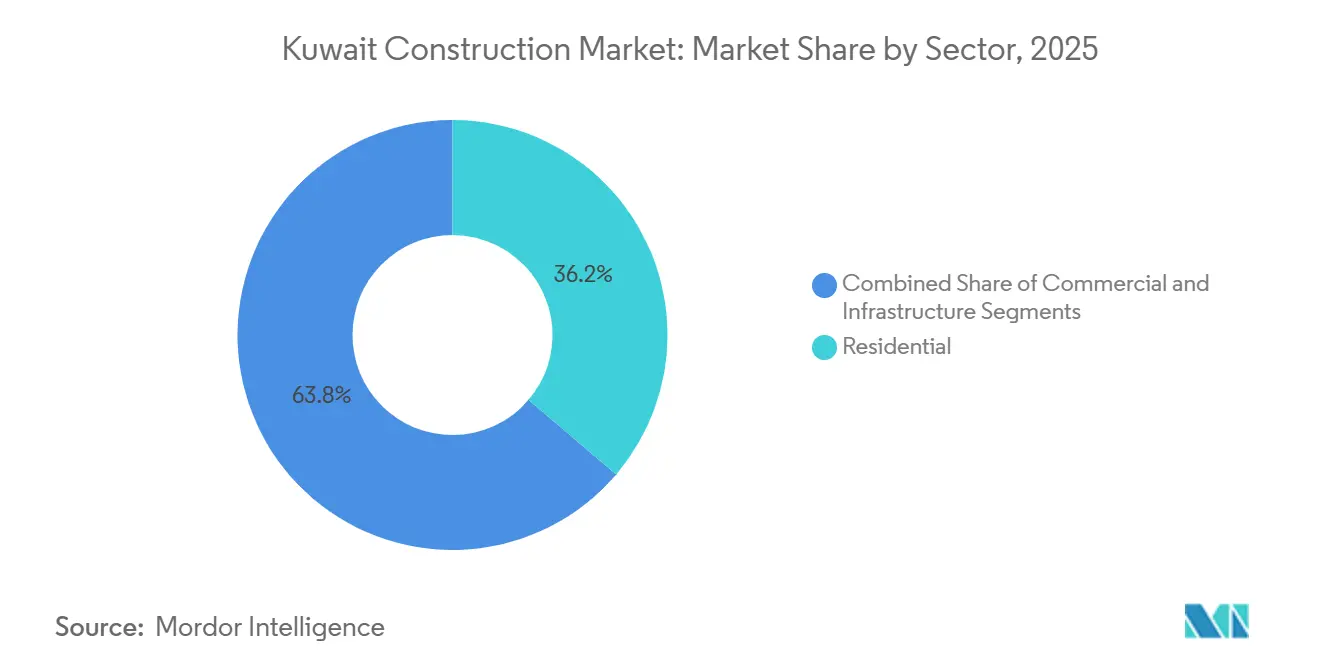

- By sector, residential led with 36.23% of the Kuwait construction market share in 2025 and is advancing at a 6.93% CAGR through 2031.

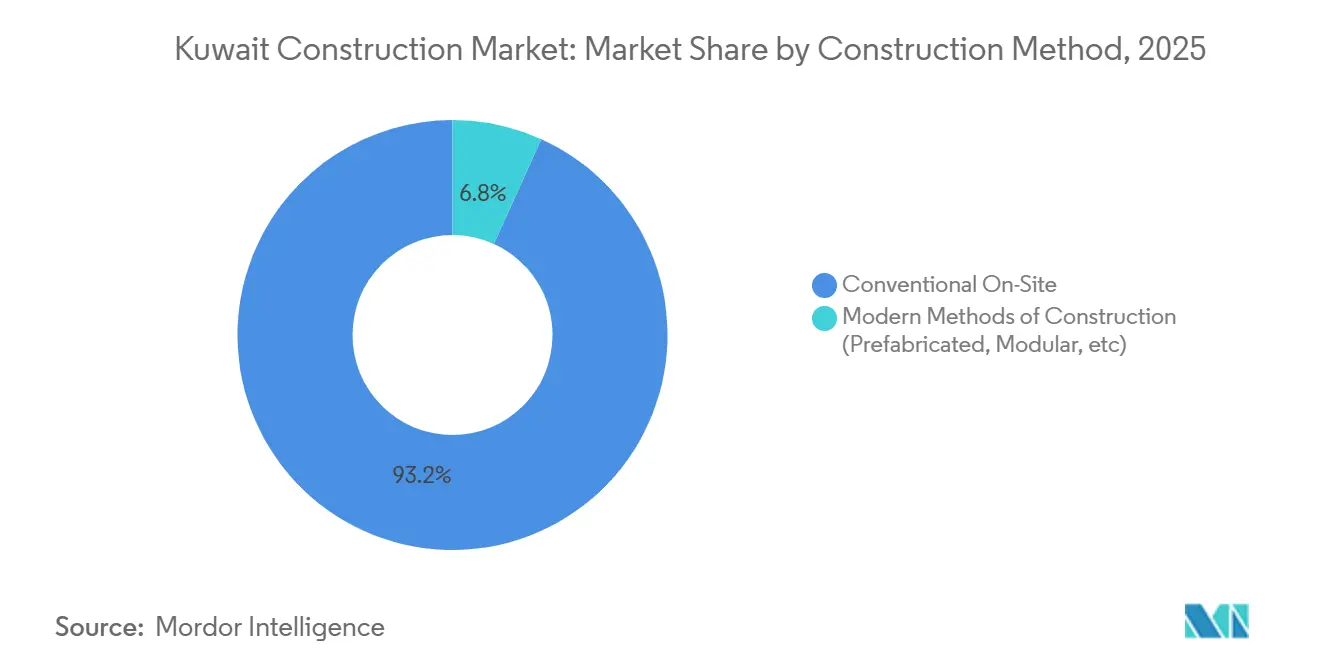

- By construction method, conventional on-site techniques held 93.23% of the Kuwait construction market size in 2025, while modular methods are expanding at a 7.93% CAGR through 2031.

- By investment source, public spending accounted for 72.23% of 2025 outlays, yet private investment is recording the highest projected 6.73% CAGR through 2031.

- By governorate, Kuwait City commanded 37.23% of the 2025 value, whereas the Rest of Kuwait is growing fastest at 7.13% CAGR to 2031.

- Combined Group Contracting, KCPC, MAK, Hyundai E&C, and JGC together controlled under 40% of 2025 contract values, underscoring a moderately concentrated landscape.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Kuwait Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision 2035 megaprojects entering full construction phase | +1.8% | Kuwait City, Jahra, Al-Zour | Medium term (2-4 years) |

| Sovereign wealth fund co-investment unlocking >USD 10 billion FDI | +1.2% | Silk City, South Saad Al-Abdullah | Long term (≥ 4 years) |

| Modular & 3D-printed housing program acceleration | +1.1% | Jahra, Farwaniya, Mutlaa | Medium term (2–4 years) |

| 2025 Sustainable Building Code boosting retrofits | +0.9% | Kuwait City, Hawalli | Short term (≤ 2 years) |

| 5G-enabled smart-city mandates | +0.7% | Silk City, South Saad Al-Abdullah | Long term (≥ 4 years) |

| Blue/green hydrogen & CCUS scale-up in Al-Zour | +0.6% | Al Ahmadi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Implementation of Kuwait Vision 2035 Megaprojects Entering Full Construction Phase

Vision 2035 moved decisively from blueprint to building after parliament’s May 2024 suspension lifted a 13-year legislative gridlock, triggering USD 1.9 billion in contract awards during 2025 and compressing procurement cycles for Silk City, South Saad Al-Abdullah and the Mubarak Al-Kabeer Port expansion. Oil revenue averaging USD 78 per barrel in early 2026 provides fiscal headroom, while 300 active projects worth USD 115 billion signal sustained opportunity even though fewer than 60% have reached financial close. Concentrated activity in Kuwait City, Jahra and Al-Zour is reshaping regional labor markets, pushing non-oil GDP growth to 3.3% in 2026. Contractors now face aggressive delivery windows that favor firms with robust project-management and cash-flow capacity.

Sovereign Wealth Fund–Backed Infrastructure Co-Investment Platform Unlocking Over USD 10 Billion FDI from 2025

Kuwait Investment Authority’s pivot toward domestic infrastructure co-investment channels foreign capital into joint ventures that grant 30%–40% equity in exchange for design and operational expertise. Phase 1 infrastructure in Silk City is already in service, and Phase 2 residential towers are breaking ground in late 2026. South Saad Al-Abdullah mirrors the model with China Gezhouba leading a USD 4 billion smart-city build. Performance-based contracts penalize schedule drift, a break from Kuwait’s traditional cost-plus norm, and real-estate sales surged 28% year-on-year in H1 2025 on confidence in megaproject timelines.

Acceleration of Modular & 3D-Printed Housing Programs to Clear 92,000-Unit Backlog

Social-housing applications could reach 197,000 by 2035, prompting mandates that at least 30% of units use modular or 3D-printed elements by 2028. The 3,345-unit Jahra pilot trims on-site labor by 40% and halves the build time to 18 months. With three more cities tendering 40,000 modular units, supply-chain investments in automated welding and local assembly plants are scaling rapidly.

Mandatory 2025 Update to Kuwait Sustainable Building Code Spurring Energy-Efficient Retrofits

The 2025 code revision forces every commercial building above 5,000 m² to slash energy intensity 25% by December 2027 or face escalating fines, instantly converting 18 million m² of legacy stock into retrofit targets[2]Kuwait EPA Directorate, “Sustainable Building Code 2025 Revision". Prescriptive measures such as double-glazed façades and solar-ready rooftops are favoring contractors with building-management and grid-integration skill sets, while quarterly inspections from January 2026 compress delivery schedules. Early compliant landlords are capturing 12%–18% rent premiums.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-labor shortages under 2024 Kuwaitization quotas | −0.8% | Kuwait City, Al-Zour | Short term (≤ 2 years) |

| Volatile steel & cement costs amid EU CBAM/export levies | −0.6% | National | Medium term (2-4 years) |

| Fiscal-consolidation law capping capital spending | −0.5% | Public projects nationwide | Short term (≤ 2 years) |

| Water-scarcity compliance raising onsite costs | −0.4% | Greenfield sites | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Skilled-Labor Shortages Intensified by Kuwaitization Quotas

Non-nationals still hold 78.7% of jobs, yet public contracts must now staff 70%–98% Kuwaiti nationals, shrinking the experienced workforce for site supervision, BIM coordination and CCUS engineering[3]International Labour Organization Statistics Dept., “Kuwait Labor Force Q1 2024". Wage inflation of 18%–25% since 2023 is eroding margins on fixed-price deals, while vocational programs lag industry needs by up to two years.

Volatile Steel & Cement Costs Amid EU CBAM and Regional Levies

EU CBAM surcharges and Saudi cement export duties lifted landed costs 12%–18% and cut inbound volumes 22% in H1 2025, straining contracts signed prior to policy shifts. Smaller firms face liquidity pressure as they renegotiate price-escalation clauses or absorb losses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Residential Leads Kuwait’s Supply-Gap Agenda

Residential accounted for 36.23% of the Kuwait construction market size in 2025 and is growing at a 6.93% CAGR to 2031, propelled by an expanding social-housing queue and mandates for modular delivery that reduce build cycles to 18 months[4]Kuwait EPA Directorate, “Sustainable Building Code 2025 Revision". Apartments represent roughly 65% of unit starts, reflecting land scarcity and high urban plot prices, while villa construction concentrates in Jahra and South Sabah Al-Ahmad, where land grants lower entry costs. Early modular adopters, often joint ventures with foreign fabricators, are positioned to capture outsized Kuwait construction market share as tenders scale.

The commercial segment lags in both share and growth but underpins Vision 2035 diversification. Office buildings tilt toward energy-retrofit upgrades that satisfy the 2025 code, and industrial–logistics facilities flourish in Silk City’s free zone and Al-Zour’s petrochemical cluster. Retail footprints are downsizing amid e-commerce penetration above 30%, reallocating capital toward experiential formats.

By Construction Type: New Builds Dominate, Retrofits Rise

New construction claimed 80.23% of the 2025 value as Silk City, South Saad Al-Abdullah, and Mubarak Al-Kabeer Port entered heavy civil phases. Although front-loaded capital skews cash-flow profiles, elevated oil prices offer a cushion for accelerated tendering, supporting continued strength in the Kuwait construction market.

Retrofit spending, 19.77% in 2025, matches new-build growth at 6.93% CAGR thanks to the energy-certificate mandate. Around 18 million m² of legacy stock in Kuwait City and Hawalli must upgrade façades, HVAC, and controls to avoid escalating fines, creating steady workstreams and premium lease gains.

By Construction Method: Conventional Prevails, Modular Accelerates

Conventional on-site practices still hold 93.23% of 2025 spend, yet modular techniques expand at 7.93% CAGR under Ministry of Public Works targets for 30% prefabrication in social housing. The Kuwait construction market size attached to modular bids is poised to jump once ISO 19208-aligned standards debut in Q3 2026, streamlining approvals. Supply-chain investments, automated welding lines, and local assembly yards are narrowing tolerance gaps and boosting local content.

By Investment Source: Private Capital Accelerates

Public entities funded 72.23% of the 2025 value, but private capital is rising at a 6.73% CAGR as sovereign wealth co-investment mandates pull global developers into joint ventures. The Kuwait construction industry, meanwhile, adjusts to longer payment cycles and stricter debt ceilings that favor well-capitalized firms capable of bridging cash-flow gaps.

Geography Analysis

Kuwait City’s retrofit-led growth revolves around an 18 million m² backlog of aging stock now subject to 25% energy-reduction mandates. High-rise apartments dominate new urban supply as USD 3,250-per-m² land costs constrain villas. Silk City, while administratively within the capital, operates as a self-contained megaproject with a USD 130 billion envelope incorporating a 36-km causeway and five man-made islands.

Al Ahmadi’s industrial focus features ACWA Power’s USD 3.3 billion IWPP and blue/green hydrogen pilots that demand specialist EPC skills. Logistics bottlenecks water trucking at KD 8 per m³, and limited worker accommodation inflates costs 10%–15% over Kuwait City benchmarks. Hawalli supplies dense retrofit opportunities, whereas Farwaniya benefits from airport-adjacent logistics growth and mid-market housing spillover.

Rest-of-Kuwait governorates are decentralization winners. Jahra hosts the 3,345-unit modular pilot and tenders for 40,000 additional social-housing units. South Saad Al-Abdullah’s USD 4 billion smart-city plan, Mutlaa City’s USD 2 billion infrastructure, and a USD 1.2 billion Jahra wastewater upgrade will collectively reshape labor distribution and utilities demand through 2031.

Competitive Landscape

The top five contractors secured below 40% of 2025 awards, confirming moderate concentration that leaves room for mid-tier specialists. Local firms dominate civil works but increasingly outsource digital and MEP scopes to global EPCs. Workforce Kuwaitization raises costs and spurs investment in training, yet graduation rates remain under 40%, prolonging skilled-labor gaps.

Modular construction and energy retrofits are emerging white spaces. Only 32% of surveyed contractors have completed modular pilots, yet mandates for 30% prefabrication in public housing will quickly scale demand. Early movers with ISO 19208-aligned processes and digital-twin capabilities are positioned to earn premium margins. Technology integration, 5G networks, BIM-driven sequencing, and carbon-capture readiness offer differentiation as smart-city and hydrogen clusters proliferate.

International majors such as ACWA Power, Technip Energies, JGC, and Fluor capture high-complexity EPC scopes. Joint ventures combining local client access with foreign engineering depth are now standard on megaproject pursuits, evidenced by the VINCI–Van Oord bid for Mubarak Al-Kabeer Port and KCPC’s partnership with China Gezhouba at South Saad Al-Abdullah.

Kuwait Construction Industry Leaders

Combined Group Contracting Co.

Kuwait Company for Process Plant Construction & Contracting (KCPC)

Mushrif Trading & Contracting Co.

Mohammed Abdulmohsin Al-Kharafi & Sons (MAK)

Hyundai Engineering & Construction Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Bechtel won USD 1.2 billion FEED and PM services for a green-hydrogen plant in Al-Zour.

- October 2025: VINCI and Van Oord formed a JV to bid the USD 9 billion Mubarak Al-Kabeer Port expansion.

- September 2025: Petrofac landed a USD 4 billion contract for the Lower Fars heavy-oil project.

- June 2025: Larsen & Toubro won up to USD 720 million for a 300 km gas pipeline to northern hubs

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study views the Kuwait construction market as the yearly value of on-site labor, materials, and professional services required to build, expand, or refurbish residential, commercial, industrial, and civil infrastructure projects across the country. Planned, budgeted, or under-execution projects recorded in official registers are counted once physical spending starts.

Scope Exclusion: work linked to offshore oil and gas platforms, owner-built informal housing, and temporary site facilities is left outside this boundary.

Segmentation Overview

- By Sector

- Residential

- Apartments/Condominiums

- Villas/Landed Houses

- Commercial

- Office

- Retail

- Industrial and Logistics

- Others

- Infrastructure

- Transportation Infrastructure (Roadways, Railways, Airways, others)

- Energy & Utilities

- Others

- Residential

- By Construction Type

- New Construction

- Renovation

- By Construction Method

- Conventional On-Site

- Modern Methods of Construction (Prefabricated, Modular, etc.)

- By Investment Source

- Public

- Private

- By Governorate

- Kuwait City

- Al Ahmadi

- Hawalli

- Farwaniya

- Rest of Kuwait

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted structured calls with project developers, EPC contractors, quantity surveyors, building officials, and sector consultants spread across Kuwait City, Al Ahmadi, and Farwaniya. Interviews validated average project lead times, typical cost breakups, and the realistic conversion of the announced KWD 3.9 billion airport and metro phases into yearly spend.

Desk Research

Our team opened the model with government information such as the Central Statistical Bureau's national accounts, Ministry of Finance capital spending annexes, Kuwait Authority for Partnership Projects' pipeline, and Public Authority for Housing Welfare handover data. We layered these with project registers from MEED Projects, building permit bulletins, GCC Contractors Association briefs, and construction material price indices published by the Kuwait Chamber of Commerce. Subscription tools from D&B Hoovers, Dow Jones Factiva, and Volza supplied company revenue splits, tender notices, and shipment clues that helped us reconcile import-heavy material cost lines. The sources cited above are illustrative; many other public and paid references informed data checks and narrative clarity.

Market-Sizing and Forecasting

We reconstructed annual output through a top-down roll-up of historical gross fixed capital formation, segregated by construction-specific budget lines, and then filtered through project stage weights. Results were cross-checked with sampled contractor revenue pools and average selling price multiplied by bagged cement sales to adjust totals. Key variables feeding the model include awarded project value, building permit approvals, cement dispatches, government capital expenditure, Brent crude price (proxy for fiscal headroom), and population-driven housing demand. A multivariate regression linked those drivers with past spending patterns before projecting them to 2030 under base, optimistic, and delay scenarios.

Data Validation and Update Cycle

Outputs undergo variance checks versus material price trends and project progress milestones. Senior reviewers challenge anomalies, and records are refreshed each year, with mid-cycle updates when megaproject timelines shift materially.

Why Our Kuwait Construction Baseline Commands Confidence

Published estimates often differ because firms pick varying scopes, exchange rates, and project slippage assumptions.

Key gap drivers for this market include whether renovation spend is included, how stalled PPP projects are discounted, inflation treatment on multi-year contracts, and the month chosen for dinar to dollar conversion. Mordor's disciplined approach aligns scope with actual on-site expenditure, applies progress-weighted discounting to announced projects, and updates currency at the average annual rate, yielding a dependable baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.40 B (2025) | Mordor Intelligence | - |

| USD 8.90 B (2024) | Regional Consultancy A | Omits public infrastructure outlays and uses 2022 exchange rate |

| USD 14.33 B (2025) | Trade Journal B | Counts contract awards without slippage adjustment and assumes 7.6 percent CAGR |

In sum, the side-by-side view shows that when scope breadth, progress weighting, and currency logic are harmonized, our figure stays centered and reproducible, giving decision-makers a stable starting point for strategy and risk analysis.

Key Questions Answered in the Report

What is the current value of the Kuwait construction market?

It is valued at USD 16.28 billion in 2026 with a forecast to reach USD 21.48 billion by 2031.

How fast is the sector expected to grow?

The market is projected to expand at a 5.7% CAGR between 2026 and 2031.

Which segment leads spending today?

Residential construction leads with 36.23% of 2025 value, fueled by social-housing demand.

Where is construction activity growing quickest geographically?

The Rest of Kuwait is advancing at a 7.13% CAGR through 2031, led by governorates outside Kuwait City such as Jahra.

How concentrated is contractor competition?

The top five players control under 40% of contract awards, indicating moderate concentration and room for new entrants.

Page last updated on: