Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

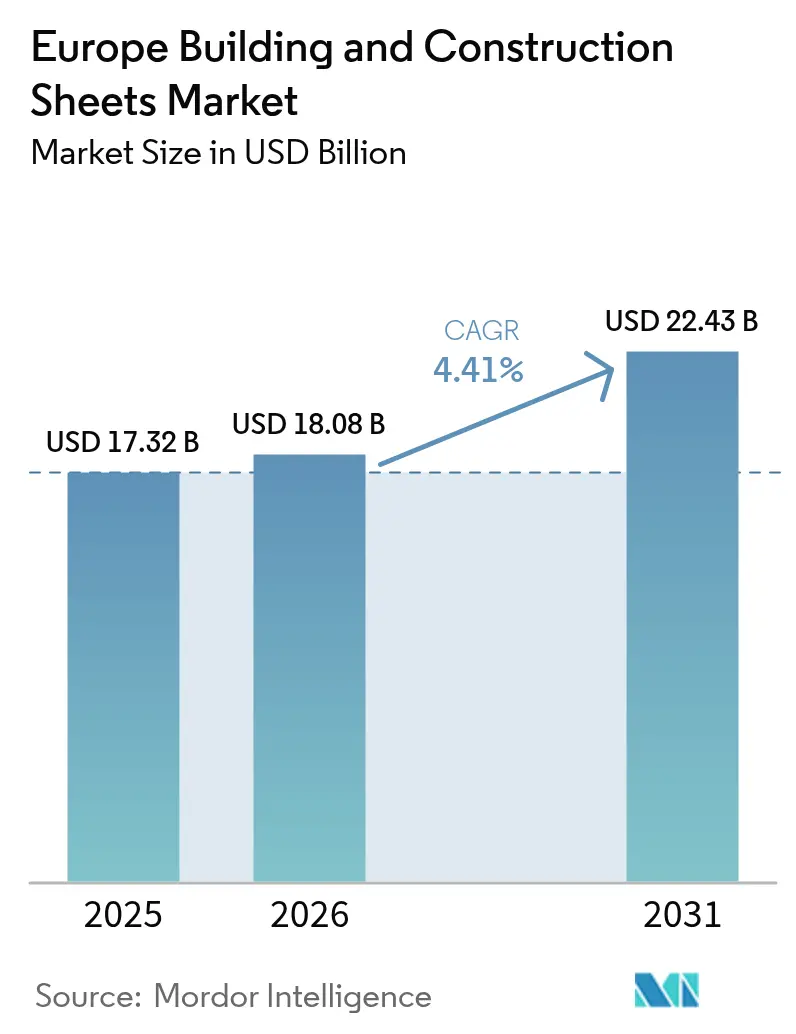

| Base Year Market Size (2025) | USD 17.32 Billion |

| Market Size (2026) | USD 18.08 Billion |

| Market Size (2031) | USD 22.43 Billion |

| Growth Rate (2026 - 2031) | 4.41% CAGR |

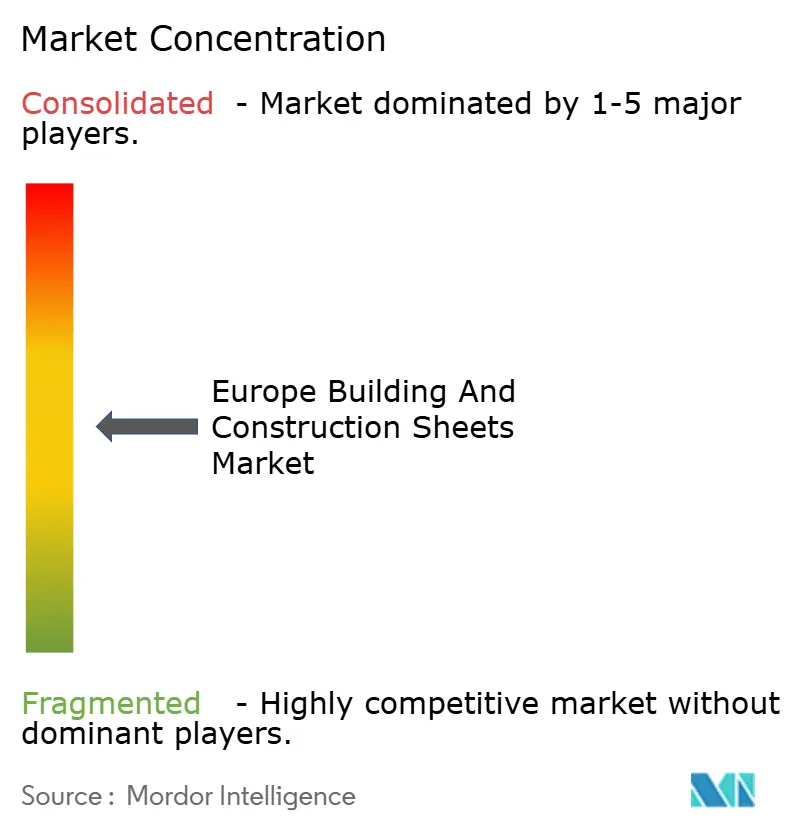

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Building And Construction Sheets Market Analysis by Mordor Intelligence

The Europe Building And Construction Sheets Market size was valued at USD 17.32 billion in 2025 and is estimated to grow from USD 18.08 billion in 2026 to reach USD 22.43 billion by 2031, at a CAGR of 4.41% during the forecast period (2026-2031).

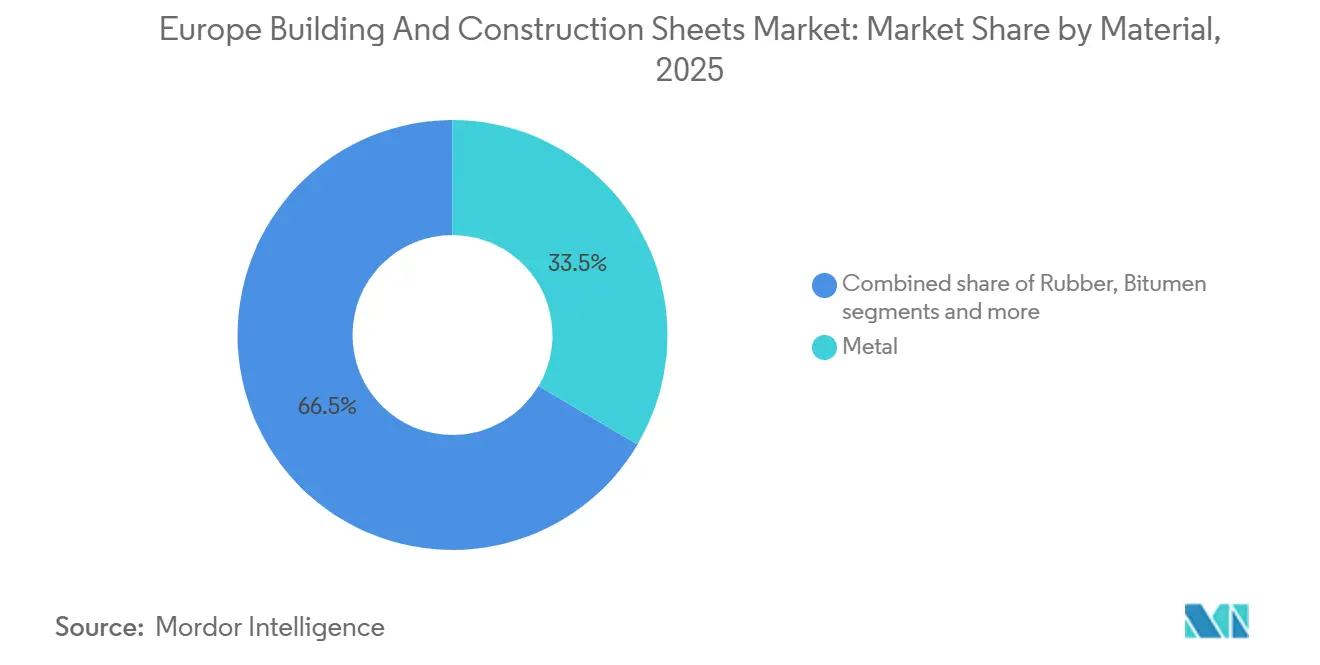

Sustained demand comes from simultaneous retrofits of energy-inefficient buildings and a new wave of industrial facilities that require lightweight, corrosion-resistant cladding. Renovation absorbed 54.8% of regional demand in 2025, yet warehouse and manufacturing projects tied to e-commerce and reshoring are accelerating new-build volumes. Metal sheets held a 33.5% share in 2025, but polymer sheets are advancing fastest because moisture-resistant profiles shorten installation times on complex roofs. Supply-chain volatility in steel and aluminum keeps profit margins tight, pushing suppliers toward composite and polymer offerings with higher value per square foot.

Key Report Takeaways

- By material, metal commanded 33.5% of the Europe building and construction sheets market share in 2025, while polymer sheets are on track for a 5.15% CAGR through 2031.

- By construction type, renovation captured 54.8% of the Europe building and construction sheets market size in 2025, whereas new construction is set to expand at a 4.92% CAGR to 2031.

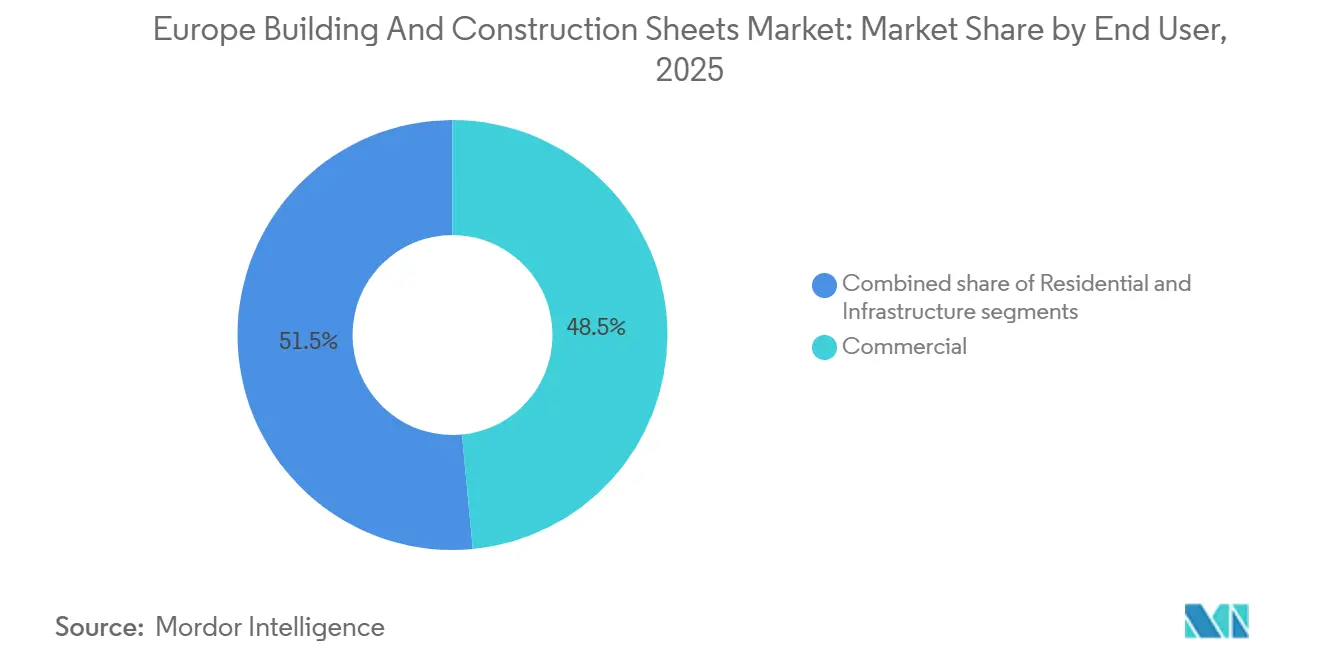

- By end-user, commercial facilities led with 48.5% of the Europe building and construction sheets market in 2025, and infrastructure projects are forecast to record the fastest 5.22% CAGR over 2026-2031.

- By geography, Germany contributed 24.2% of the Europe building and construction sheets market in 2025, while Spain is projected to grow the quickest at a 5.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Building And Construction Sheets Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation and energy-efficiency upgrades are increasing the demand for roofing and cladding sheets | +1.2% | Germany, France, the United Kingdom | Medium term (2-4 years) |

| Growth in industrial and warehouse construction is supporting metal sheet consumption | +1.0% | Germany, Poland, Netherlands | Short term (≤ 2 years) |

| Stricter insulation standards are boosting the use of sandwich panels and composite sheets | +0.9% | EU-wide, rapid in Nordics | Long term (≥ 4 years) |

| Rising adoption of lightweight, corrosion-resistant materials in commercial projects | +0.7% | Spain, Italy, coastal belts | Medium term (2-4 years) |

| Expansion of prefabricated and modular buildings is driving standardized sheet demand | +0.6% | Scandinavia, Germany | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Renovation and Energy-Efficiency Upgrades Increasing Demand for Roofing and Cladding Sheets

More than three-quarters of Europe’s buildings predate 1990, and stricter energy-performance certificates now compel deep retrofits. Germany’s federal subsidy of EUR 14 billion (USD 15.2 billion) in 2025 financed high-performance panels that lift thermal resistance by 30%–40% per project[1]Federal Ministry for Economic Affairs and Climate Action, “Building Renovation Program 2025,” bmwk.de . France’s MaPrimeRénov expansion in 2025 opened similar incentives for small commercial properties. Multi-layer assemblies integrating vapor barriers and weather skins therefore lift the square-meter consumption of sheets. Uptake is swift in dense urban cores where higher property values justify premium products, yet rural upgrades advance more slowly due to budget constraints. Collectively, this renovation cycle adds steady volume to the Europe building and construction sheets market.

Growth in Industrial and Warehouse Construction Supporting Metal Sheet Consumption

Central and eastern Europe added over 5 million m² of new warehouse floor space in 2025, driven by e-commerce fulfillment and reshored manufacturing. Pre-painted steel and aluminum sheets dominate these large roofs because they balance fire safety with fast installation. Tata Steel Europe shipped 12% more construction coil during 1H 2025, crediting distribution-center builds along major freight corridors[2]Tata Steel Europe, “Joint Venture with Modular Builder,” tatasteeleurope.. The cold-storage boom layers on insulated metal panels with polyurethane cores to meet tight temperature tolerances. Permitting delays in some regions temper short-term momentum, but the underlying structural shift toward regionalized logistics continues to enlarge the Europe building and construction sheets market.

Stricter Insulation Standards Boosting Use of Sandwich Panels and Composite Sheets

The January 2025 revision of the Energy Performance of Buildings Directive requires near-zero-energy outcomes, effectively mandating U-values below 0.20 W/m²K for most non-residential envelopes. Single-skin sheets cannot comply, so builders are pivoting to sandwich panels that pair steel or aluminum facings with mineral-wool or polyurethane cores. Kingspan recorded a 15% increase in European insulated-panel volume in 2025, fueled by higher office and retail specifications. However, the panels introduce supply complexity because fabricators must certify both thermal and fire credentials, stretching lead times. Installers also need training to handle thicker, heavier components, creating ancillary service opportunities for suppliers.

Rising Adoption of Lightweight and Corrosion-Resistant Materials in Commercial Projects

Coastal humidity drives accelerated corrosion in southern Europe, and property owners are switching from galvanized steel to aluminum-magnesium alloys or advanced polymer coatings that resist salt attack for 30 years or more. Spain’s tourism rebound means hotels and convention centers increasingly specify standing-seam aluminum roofs to reduce lifetime repaint costs, enlarging the premium segment of the Europe building and construction sheets market. ArcelorMittal Construction responded in 2025 with a steel grade offering enhanced edge protection and a 30-year warranty. TPO and PVC membranes also gain share on low-slope roofs where their high reflectivity supports cooling-energy cuts that help projects secure green-building badges.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in steel and aluminum prices is impacting manufacturers' margins | –0.8% | EU-wide | Short term (≤ 2 years) |

| Environmental regulations are increasing compliance and production costs | –0.5% | Germany, France, the Netherlands | Medium term (2-4 years) |

| Intense price competition among regional sheet manufacturers | –0.4% | Southern & Eastern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Steel and Aluminum Prices Impacting Manufacturer Margins

European hot-rolled-coil prices bounced between EUR 550 and EUR 720 per t in 2025 (USD 600–785), while primary aluminum ranged EUR 2,200–2,600 per t (USD 2,400–2,835) amid energy-price gyrations and trade policy shifts[3]EUROMETAL, “Western European Steel Market Trends 2025,” eurometal.net . Sheet producers quoting projects 60–90 days ahead have limited ability to reprice when inputs spike mid-contract, eroding gross margins by up to 300 basis points. Larger vertically integrated players hedge exposures and diversify into higher-margin composites, widening the gap to mid-sized regional fabricators. Public tenders rarely accept escalation clauses, forcing suppliers either to absorb surges or exit bids, which temporarily restrains growth in the Europe building and construction sheets market.

Environmental Regulations Increasing Compliance and Production Costs

From 2026, the EU Carbon Border Adjustment Mechanism will levy fees on imported steel and aluminum based on embedded CO₂, raising feedstock costs for manufacturers sourcing outside the bloc. Extended producer responsibility laws in Germany and France also require funding for end-of-life collection, adding EUR 5–10 per t (USD 5.45–10.90). Paint chemistries face tighter VOC limits, compelling multicountry requalification cycles lasting 12–18 months. Multinationals amortize testing across broad ranges, but smaller firms confront outsized R&D expense and risk losing listings. These layers of compliance lift operating cost and slow product launches, marginally breaking the Europe building and construction sheets market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Polymer Gains Ground as Metal Retains Core Demand

Metal sheets accounted for 33.5% of the Europe building and construction sheets market share in 2025, benefiting from high structural strength and established supply chains. Polymer sheets are expected to post a 5.15% CAGR, the fastest among materials, as architects value lightweight and moisture resilience for intricate roof geometries. Bitumen membranes remain popular on low-slope residential roofs in southern Europe, yet sustainability scrutiny limits future growth. Rubber membranes serve niche waterproofing roles on green roofs and plaza decks where elasticity is critical.

Kingspan’s 2025 rollout of a polymer-faced insulated panel embedded with photovoltaic laminates shows how hybrid innovations blur category lines. Metal suppliers counter with polymer-film-laminated steel that offers metallic rigidity with enhanced corrosion protection in coastal builds. Fire codes reinforce material divergence: mineral-wool-cored metal panels dominate high-rise and industrial projects demanding Euroclass A1, while polymers thrive in low-rise residential and agricultural structures. This balanced demand underpins long-term stability for the Europe building and construction sheets market size.

By Construction Type: Renovation Still Leads as New-Build Speeds Up

Renovation made up 54.8% of the Europe building and construction sheets market in 2025, reflecting an aging stock and subsidy-driven retrofits. New construction is forecast to grow at 4.92% through 2031 as e-commerce warehouses, light factories, and selected housing rise. Retrofit projects offer quicker approvals and fragmented contractor bases, requiring flexible supply networks and small-batch deliveries of lightweight polymer overlays compatible with existing roofs.

Conversely, large new-build logistics hubs secure bulk contracts for pre-painted steel coils, bringing economies of scale and a predictable offtake. Residential new-build remains muted due to high mortgage costs, though Germany and Scandinavia accelerate modular-housing pilots that favor factory-standard panels. The dual-track dynamics ensure both sub-segments contribute meaningfully to the Europe building and construction sheets market size over the forecast period.

By End-User: Infrastructure Takes Off While Commercial Dominates

Commercial properties held 48.5% of 2025 demand, encompassing offices, retail, hotels, and schools that require aesthetics, insulation, and minimal upkeep. Infrastructure exhibits the fastest 5.22% CAGR as EU rail, bridge, and renewable-energy programs roll out. Residential remains sizeable but slower growing because renovation outweighs new starts.

TEN-T transport nodes and wind-farm service buildings increasingly specify non-corrosive metal panels rated for 30-year exposure, elevating volumes in infrastructure. Commercial projects continue to favor curtain-wall systems with composite sheets for visual impact and thermal control, sustaining a dominant share. Suppliers therefore juggle direct strategic accounts with contractors on megaprojects and distributor networks serving residential reroofing, a balanced approach that supports the Europe building and construction sheets market.

Geography Analysis

Germany contributed 24.2% of regional sheet demand in 2025, thanks to robust industrial output and USD 15.2 billion in federal retrofit subsidies that reward insulated metal and polymer-coated panels compliant with KfW energy classes. Spain is forecast to post the swiftest 5.61% CAGR through 2031 as infrastructure stimulus, coastal tourism, and high-speed-rail extensions lift cladding volumes and favor corrosion-resistant aluminum and TPO membranes. France, the United Kingdom, and Italy jointly represent close to 40% of consumption, yet each displays unique catalysts: expanded MaPrimeRénov grants drive French facade upgrades, cold-storage projects prop up U.K. demand despite post-Brexit frictions, and seismic retrofit funds in Italy increase orders for reinforced fastening systems and thicker gauge metal.

The Rest-of-Europe cluster—Poland, the Netherlands, Belgium, and Scandinavia—delivers varied momentum. Polish logistics hubs absorb large runs of roll-formed steel for warehouses, while Scandinavian modular builders purchase standardized coils that support off-site production lines. The Netherlands and Belgium benefit from renewable-energy projects needing durable panelized enclosures. Suppliers adapt by establishing stocking centers near regional hotspots and by offering multilingual technical support that aligns with divergent building codes, ensuring the Europe building and construction sheets market remains resilient across geographies.

Competitive Landscape

Competition is moderate, with multinationals such as Saint-Gobain, Kingspan, and ArcelorMittal battling more than 200 regional roll-formers and coating specialists. Differentiation pivots on sustainability credentials, lead-time reliability, and integrated digital design tools. Larger firms exploit vertical integration and hedging programs to neutralize metal-price swings and to offer BIM-ready product libraries that speed specification for architects, thereby enlarging their footprint in the Europe building and construction sheets market.

Strategic moves are frequent. Kingspan invested EUR 120 million (USD 126 million) in Polish insulated-panel capacity in February 2026, adding 2 million m² annual output and lowering embodied carbon by 40% through renewable energy. Saint-Gobain’s January 2026 acquisition of a Spanish polymer-sheet producer extends its Iberian reach, while ArcelorMittal’s corrosion-resistant grade addresses harsh Mediterranean climates. Tata Steel Europe’s service-center joint venture with a modular builder delivers just-in-time coils that slash factory downtime.

Automation and M&A accelerate consolidation. Rockwool’s USD 87 million upgrade of its Danish mineral-wool line in September 2025 boosts fire-safe core production, and Sika’s USD 49 million coating acquisition in France widens its low-VOC portfolio. Digital portals such as CertainTeed’s April 2025 BIM specification platform are now standard expectations. Smaller fabricators counter with rapid customization and local relationships but face mounting capex needs to comply with carbon accounting and product transparency, setting the stage for further mergers across the Europe building and construction sheets market.

Europe Building And Construction Sheets Industry Leaders

Saint Gobain

Lyondellbasell

James Hardie Industries plc

Paul Bauder GmbH

Euramax International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Kingspan Group unveiled a EUR 120 million (USD 126 million) expansion of insulated-panel capacity in Poland to serve e-commerce warehouses and cold storage.

- January 2026: Saint-Gobain acquired a Spanish polymer-sheet manufacturer, gaining two plants and a distribution network across Iberia.

- November 2025: ArcelorMittal Construction launched a pre-painted steel with a 30-year edge-corrosion warranty aimed at Mediterranean builds.

- October 2025: Tata Steel Europe partnered with a German modular builder to co-develop factory-optimized sheet profiles and set up a dedicated service center.

Europe Building And Construction Sheets Market Report Scope

By Material

| Bitumen |

| Rubber |

| Metal |

| Polymer |

| Others |

By Construction Type

| New Construction |

| Renovation |

By End-user

| Residential |

| Commercial |

| Infrastructure |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Material | Bitumen |

| Rubber | |

| Metal | |

| Polymer | |

| Others | |

| By Construction Type | New Construction |

| Renovation | |

| By End-user | Residential |

| Commercial | |

| Infrastructure | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe building and construction sheets market in 2031?

The market is forecast to reach USD 22.43 billion by 2031, rising at a 4.41% CAGR from 2026 to 2031.

Which material segment is expanding fastest?

Polymer sheets are projected to grow at a 5.15% CAGR through 2031, benefiting from moisture resistance and ease of installation.

Why is Germany the largest national market?

Germany combines strict energy codes with generous retrofit subsidies, giving it a 24.2% share of regional demand in 2025.

What end-user category will see the quickest growth?

Infrastructure projects are expected to post the fastest 5.22% CAGR as EU rail, bridge, and renewable-energy programs advance.

How are suppliers tackling raw-material price volatility?

Leading firms hedge steel and aluminum costs, diversify into higher-margin composites, and invest in digital ordering tools to maintain margins.

What regulatory change most influences future demand?

The revised Energy Performance of Buildings Directive, effective January 2025, drives adoption of insulated sandwich panels to achieve near-zero-energy standards.

Page last updated on: