Europe Residential Construction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

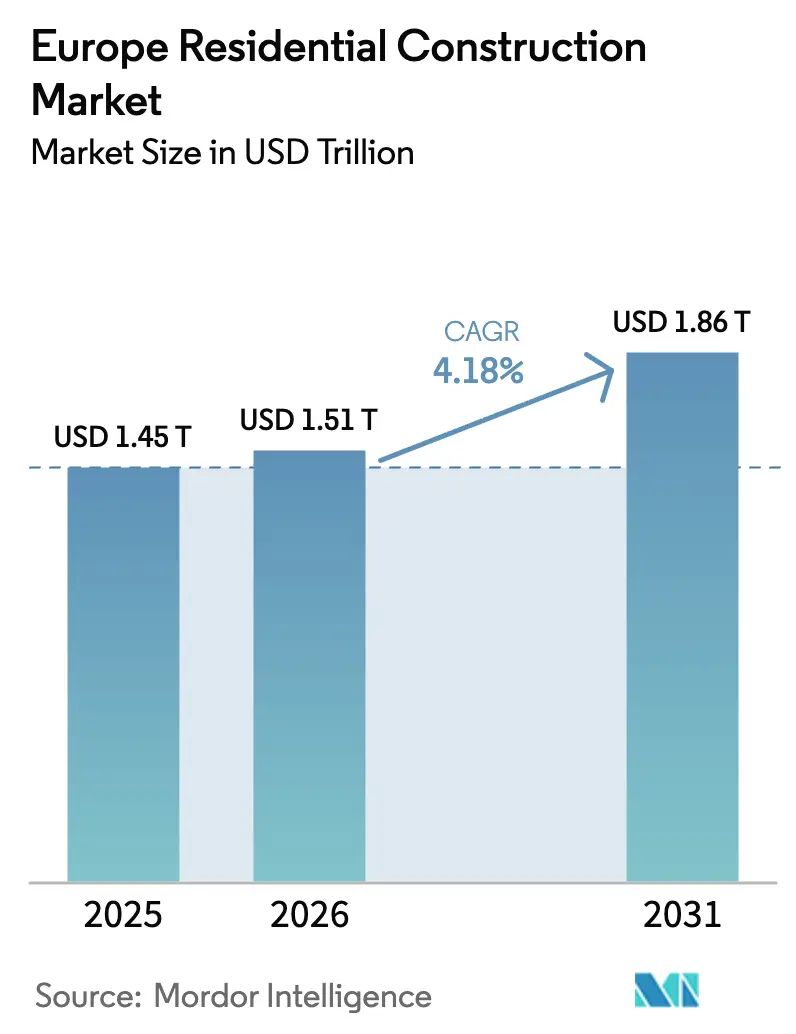

| Base Year Market Size (2025) | USD 1.45 Trillion |

| Market Size (2026) | USD 1.51 Trillion |

| Market Size (2031) | USD 1.86 Trillion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

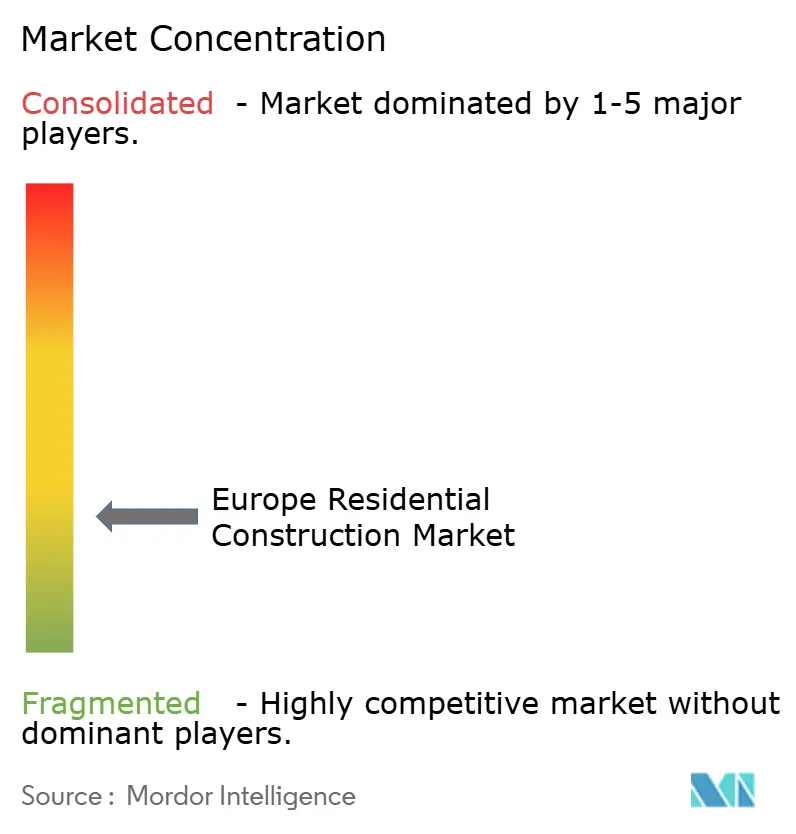

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Residential Construction Market Analysis by Mordor Intelligence

The Europe residential construction market size is projected to be USD 1,457.5 billion in 2025, USD 1,518.42 billion in 2026, and reach USD 1,863.43 billion by 2031, growing at a CAGR of 4.18% from 2026 to 2031. Activity is shifting toward retrofit programs that harvest USD 165 billion in renovation grants and tax incentives, helping contractors pivot from new-build volume to energy-upgrade work. Institutional build-to-rent investors deployed USD 30.8 billion across core markets in 2025, tightening yields and accelerating multi-family project starts. Material inflation of 18-22% during 2024-2025 spurred widespread adoption of digital procurement platforms that hedge timber and steel price swings. At the same time, green-bond issuance climbed to USD 15.73 billion in 2025, lowering borrowing costs for developers that align with EU Taxonomy carbon thresholds.

Key Report Takeaways

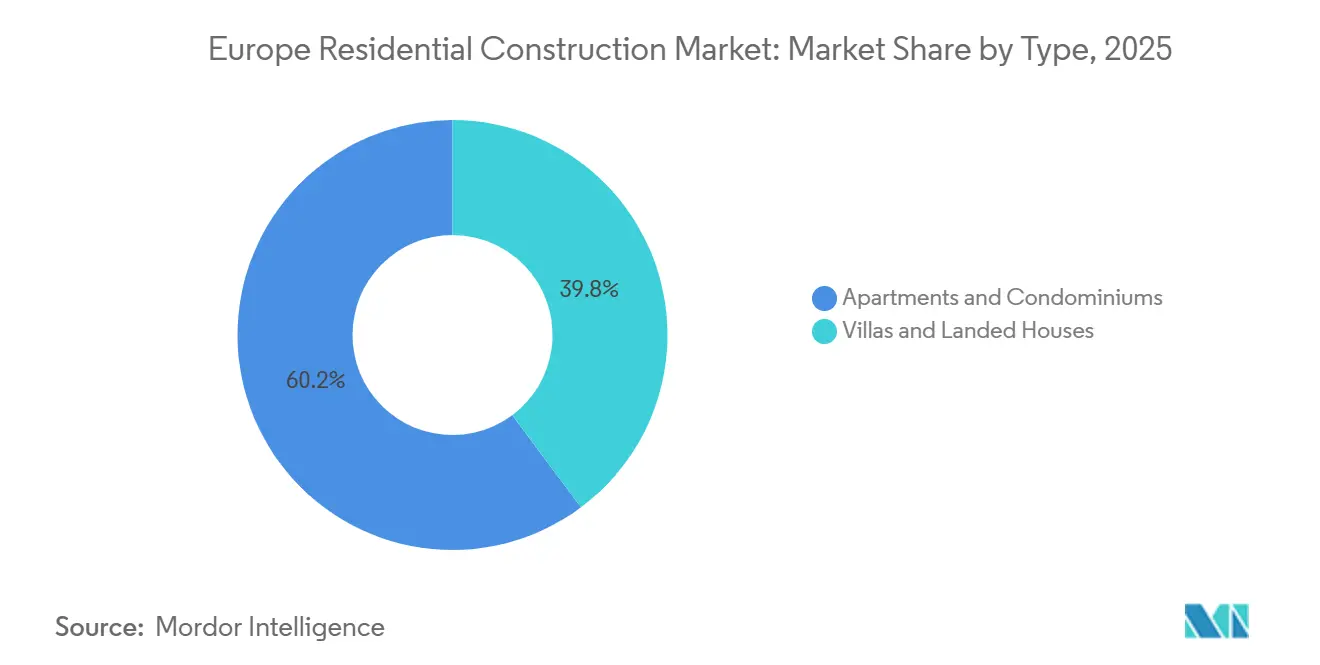

- By type, apartments and condominiums captured 60.2% of the Europe residential construction market share in 2025, while villas and landed houses trailed as financing and land-use curbs slowed detached-home starts.

- By construction type, renovation and refurbishment commanded 54.1% of the Europe residential construction market size in 2025, whereas new construction is projected to post the fastest 7.21% CAGR through 2031.

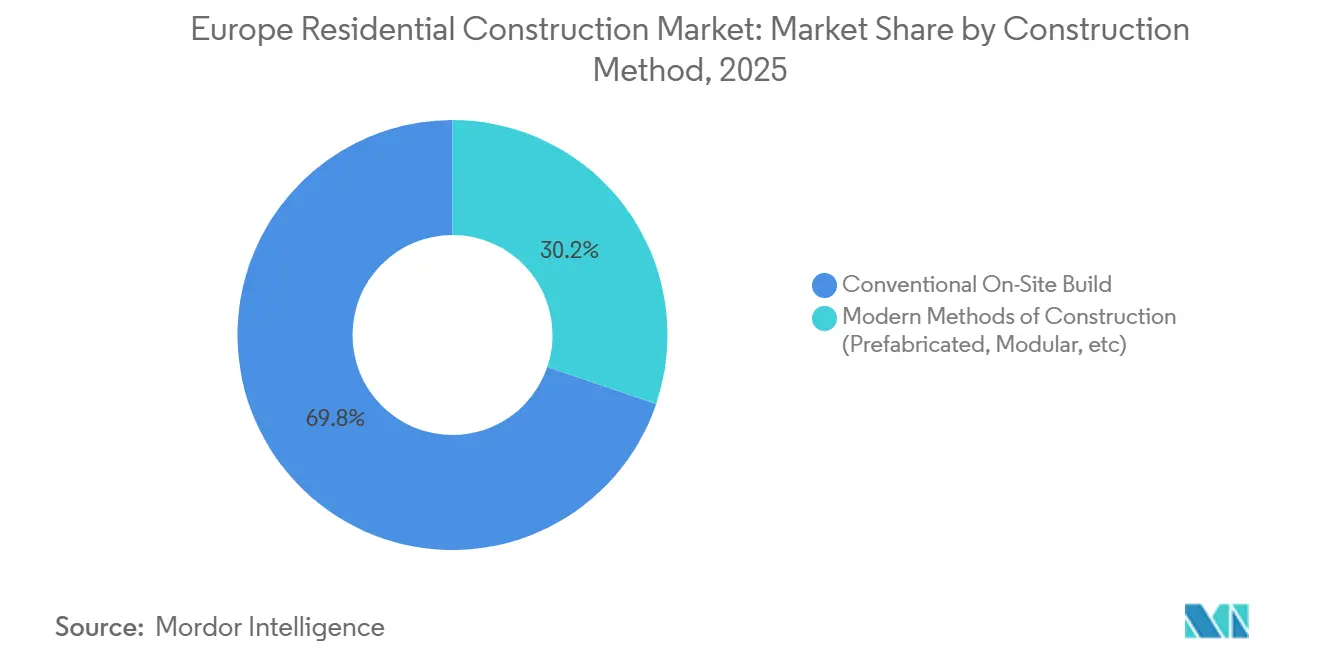

- By construction method, conventional on-site retained a 69.8% share in 2025, yet modern methods of construction are forecast to expand at a 7.45% CAGR to 2031.

- By investment source, private capital led with 79.9% of spending in 2025, but public outlays are set to grow at an 8.1% CAGR on the back of affordable-housing mandates.

- By geography, Germany held 17.5% of regional value in 2025, whereas Poland is expected to grow fastest at a 6.5% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Residential Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Renovation Wave grants & tax-credits accelerating deep-retrofits | +1.2% | Germany, France, Italy, Spain, Netherlands | Medium term (2-4 years) |

| Persistent urban housing-supply gap stimulating multi-family starts | +0.9% | Germany, UK, France, Poland, Spain | Long term (≥ 4 years) |

| Institutional build-to-rent capital inflows from pension & PE funds | +0.8% | Germany, UK, Netherlands, France | Medium term (2-4 years) |

| Affordable-housing & first-time-buyer stimulus packages | +0.6% | UK, Spain, Poland, Netherlands | Short term (≤ 2 years) |

| Green-bond & EU-taxonomy aligned financing lowering cost of capital | +0.5% | Germany, France, Netherlands, Sweden | Long term (≥ 4 years) |

| Ukraine-related refugee inflows spiking demand for rapid-build dwellings | +0.4% | Poland, Germany, Czech Republic, Romania | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU Renovation Wave Grants & Tax-Credits Accelerating Deep-Retrofits

EUR 165 billion (USD 165 billion) earmarked for residential renovations between 2021 and 2026 is reshaping order books as retrofit work rose to 54.1% of total value in 2025. Germany alone processed over 420,000 retrofit-grant applications worth USD 10.1 billion in 2025. Contractors now face a talent bottleneck that is pushing wage premiums for certified specialists 15-20% above conventional trades. In response, firms embrace modular façade panels that cut on-site labor hours and speed certification timelines. These dynamics position retrofit specialists to outpace traditional builders through 2031.

Persistent urban housing-supply gap stimulating multi-family starts

Europe’s top 50 metros faced a 2.1 million-unit shortfall in Q4-2025, boosting apartment approvals that already held 60.2% share. Berlin, Paris, and Amsterdam each cleared more than 15,000 units, luring pension capital with rental yields near 4% . The UK’s 2025 zoning reform aims to unlock 370,000 additional homes annually, although local opposition remains a drag. Developers securing forward-funding from build-to-rent operators de-risk exposure to mortgage volatility. Multi-family growth at a 6.11% CAGR therefore remains central to the Europe residential construction market outlook.

Institutional build-to-rent capital inflows from pension & PE funds

Pension and private-equity sponsors placed USD 30.8 billion in European build-to-rent assets during 2025, up 22% year on year. Yields compressed to 3.8-4.2% on stabilized stock, steering contractors toward forward-funded models that trade near-term sales for long-term management income. Vonovia earmarked USD 2.31 billion for 8,500 energy-positive units across three countries. Skanska’s USD 0.68 billion joint venture with APG underlines how institutional balance sheets now shape project formats. This capital influx is a durable growth lever for the Europe residential construction market.

Affordable-housing & first-time-buyer stimulus packages

Targeted subsidies are energizing lower-income segments. France’s MaPrimeRénov disbursed USD 5.6 billion in 2025, focusing on low-income retrofits. Poland’s National Housing Program provided USD 5.3 billion for starter homes, while the UK promotes shared-ownership schemes to bridge rising mortgage rates. These incentives compress developer payback periods, especially for modular schemes that qualify for faster grant release. With stimulus framed around social value, public-private consortia gain transaction priority through 2028.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ECB rate-hike cycle tightening mortgage & project finance | –0.9% | Germany, France, Italy, Spain, Netherlands | Medium term (2-4 years) |

| Construction-material cost inflation & supply-chain volatility | –0.7% | Germany, UK, France, Spain, Poland | Short term (≤ 2 years) |

| Municipal NIMBY opposition constraining high-density approvals | –0.4% | UK, Germany, France, Netherlands | Long term (≥ 4 years) |

| Embodied-carbon caps delaying permits for concrete-heavy designs | –0.3% | Germany, France, Netherlands, Sweden | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ECB rate-hike cycle tightening mortgage & project finance

The European Central Bank’s 3% deposit rate held firm into 2026, lifting prime mortgages to 3.8-4.5% across major economies. Loan approvals in the UK and Germany fell 9-12% during 2025, dampening for-sale housing demand. Construction debt for speculative multi-family schemes priced at 5.2-6.0%, forcing developers to inject more equity or pivot to forward-funded agreements. Elevated finance costs slow starts and temper the CAGR of the Europe residential construction market through 2028.

Construction-Material Cost Inflation & Supply-Chain Volatility

Input prices for cement, steel, and timber jumped 18-22% between Q1-2024 and Q4-2025, slicing 3-5 percentage points from developer margins on fixed-price contracts. Germany saw concrete costs rise 19% year on year, while Poland grappled with a 27% spike in rebar. Contractors countered by switching to cross-laminated timber, which picked up eight market-share points in 2025. Long-term supply agreements with sawmills now shift price risk upstream but restrict flexibility for smaller builders. Unless commodities cool, material inflation will continue to weigh on the Europe residential construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Apartments Dominate Amid Urbanization

Apartments and condominiums held 60.2% of the Europe residential construction market share in 2025, reflecting their alignment with dense land strategies and institutional capital appetite. Rental yields above 4% in Berlin, Amsterdam, and Warsaw underpinned robust forward-funding deals that secured construction pipelines. The segment is forecast to advance at a 6.11% CAGR through 2031, far outpacing villas as tight zoning and carbon caps favor multi-family density.

Developers are ramping modular apartment production to cut delivery times by 30%, evident in Skanska’s BoKlok system rolled out across Poland and the Czech Republic. Larger schemes now integrate shared coworking lounges and bicycle parking to mirror post-pandemic tenant preferences. Although detached housing retains appeal in Spain’s coastal provinces and Poland’s second-tier cities, credit tightening and land-scarcity constraints leave it trailing. Consequently, apartments will continue to anchor demand, reinforcing the long-term trajectory of the Europe residential construction market.

By Construction Type: Retrofit Leads, New Build Accelerates

Renovation and refurbishment accounted for 54.1% of the Europe residential construction market size in 2025 after grant disbursements peaked under the Renovation Wave program. Germany alone directed USD 10.1 billion toward façade insulation, heat-pump retrofits, and rooftop solar, while France supported 620,000 projects via MaPrimeRénov. Energy-service companies are expanding turnkey contracts that guarantee post-work savings, carving new niches within an already-fragmented field.

New construction, while smaller at 45.9%, is forecast to post the fastest 7.21% CAGR to 2031 as Poland, Spain, and other cohesion-fund beneficiaries tackle structural housing shortages. Poland’s USD 13.2 billion National Recovery Plan alone targets 180,000 units by 2026. Developers who combine retrofit expertise with greenfield capacity can diversify cash flows and tap both EU grants and private capital, fortifying their position in the Europe residential construction industry.

By Construction Method: MMC Gains Momentum

Conventional on-site techniques retained 69.8% share in 2025, yet modern methods of construction are scaling rapidly, supported by evidence that modular builds cut on-site labor hours 40-50% and shorten schedules by 30%[1]UK Government, “MMC Productivity Study,” gov.uk . Germany approved 28,000 modular units for refugee accommodation in 2025, highlighting the speed advantage of MMC.

Major contractors have responded with factory investments and strategic alliances. Skanska’s tie-up with Lindbäcks Bygg delivered 1,200 volumetric apartments in Sweden during 2025, achieving a 25% carbon reduction against concrete frames. Vinci Construction’s timber-panel pilot in Lyon and Toulouse produced 340 units with 35% quicker assembly. With a 7.45% CAGR forecast, MMC stands out as the fastest-growing method and a key pillar of the Europe residential construction market outlook.

By Investment Source: Public Spending Surges

Private capital dominated at 79.9% of funding in 2025, led by pension money chasing ESG-screened rental portfolios, yet sovereign programs are scaling up. Germany allocated USD 20.4 billion for social-housing build and retrofit, while France’s Action Logement committed USD 6.82 billion to affordable-unit pipelines.

Public-private partnerships now bundle public land, grants, and developer know-how. Homes England’s 8,400-unit framework with Berkeley Group exemplifies the model, shaving 30-40% from land acquisition costs and stabilizing revenue streams. With an 8.1% CAGR projected, public finance will grow faster than any other source, cushioning the Europe residential construction industry against private-market cyclicality.

Geography Analysis

Germany commanded 17.5% of the Europe residential construction market in 2025, underpinned by USD 10.1 billion in retrofit subsidies, strong build-to-rent pipelines, and an estimated 700,000-unit supply gap. However, embodied-carbon rules delayed 12,000 permits, nudging developers toward timber-hybrid designs that lengthen pre-construction phases. Institutional landlords such as Vonovia invested USD 2.31 billion in new projects, indicating confidence despite regulatory friction[2]Vonovia SE, “Annual Report 2025,” vonovia.com.

Poland is the forecast growth leader with a 6.5% CAGR to 2031, propelled by USD 13.2 billion in cohesion funding and 8% wage growth that lifts mortgage eligibility. Warsaw, Krakow, and Gdansk together drew 240,000 new residents in 2025, amplifying demand for both rental and ownership stock. Modular providers captured emergency orders for refugee housing, then parlayed factory throughput into affordable-housing tenders that will mature by 2028.

The United Kingdom, France, Spain, Italy, and the Netherlands together accounted for 48% of regional value in 2025. The UK’s planning reform promises 370,000 annual starts but progress varies by council, while mortgage rates around 4.5% temper first-time-buyer volumes. France deployed USD 12.4 billion across MaPrimeRénov and Action Logement, driving a surge in urban retrofits. Spain’s USD 9.6 billion investment program focuses on 40,000 rental apartments in Madrid and Barcelona, supported by rising lifestyle migration. Italy’s Superbonus tax credits underwrite USD 6.71 billion in retrofit spend despite fiscal cuts, and the Netherlands wrestles with nitrogen caps that limit land releases, capping growth near 3.2% annually. The Nordics and Baltics close out the landscape with modular, energy-positive pilots that provide a test bed for next-generation timber and heat-pump solutions.

Competitive Landscape

Large-scale multi-family projects attract pan-European contractors such as Vinci, Bouygues, STRABAG, and Skanska, which differentiate through balance-sheet capacity, lifecycle-carbon tracking, and factory-built capabilities. In contrast, single-family and small-retrofit markets stay dominated by local builders that leverage neighborhood relationships but lack scale for green-bond certification.

Strategy has pivoted to capital-light, forward-funded models that offload demand risk to institutions or public agencies. Skanska’s USD 0.68 billion joint venture with APG secures both construction revenue and multi-year asset-management fees[3]Skanska AB, “Net-Zero Apartment JV,” skanska.com. Vinci’s USD 0.462 billion contract with AXA Investment Managers to deliver 1,800 energy-positive apartments in Lyon and Grenoble highlights how insurers fund low-carbon stock for long-duration yields.

Technology adoption is advancing rapidly. Digital-twin platforms now monitor embodied carbon in real time, while AI-driven procurement engines hedge volatile input prices. Swedish modular specialist Lindbäcks Bygg and German timber-hybrid expert Brüninghoff exploit niche know-how to win turnkey contracts under EU Taxonomy criteria. With consolidation accelerating around carbon compliance and MMC capacity, firms that master lifecycle accounting, off-site production, and institutional partnerships are set to gain share in the Europe residential construction market.

Europe Residential Construction Industry Leaders

Skanska AB

Vinci SA

Bouygues SA

Eiffage SA

Barratt Developments plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Vinci Construction secured a USD 0.462 billion forward-funded contract for 1,800 energy-positive apartments in Lyon and Grenoble, targeting completion in 2027.

- January 2026: Skanska and APG Asset Management launched a USD 0.68 billion joint venture to develop 3,200 net-zero apartments across Stockholm, Copenhagen, and Warsaw.

- December 2025: Taylor Wimpey acquired a 140-hectare Birmingham land bank for USD 110.5 million, planning 2,400 mixed-tenure units by 2029.

- November 2025: Bouygues Immobilier issued a USD 0.66 billion green bond priced 35 basis points below conventional debt for 4,200 net-zero apartments.

Europe Residential Construction Market Report Scope

Residential construction is a process that involves the expansion, renovation, or construction of a new home or spaces intended to be occupied for residential purposes. In the residential construction market, buildings are constructed and sold to customers.

Europe's Residential Construction Market is segmented by property type (single-family and multi-family), construction type (new construction and renovation), and country (Germany, United Kingdom, France, Italy, and the rest of Europe).

The Europe Residential Construction Market report offers the market sizes and forecasts in value (USD) for all the above segments

| Apartments and Condominiums |

| Villas & Landed Houses |

| New Construction |

| Renovation & Refurbishment |

| Conventional On-Site |

| Modern Methods of Construction |

| Public |

| Private |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Poland |

| Rest of Europe |

| By Type | Apartments and Condominiums |

| Villas & Landed Houses | |

| By Construction Type | New Construction |

| Renovation & Refurbishment | |

| By Construction Method | Conventional On-Site |

| Modern Methods of Construction | |

| By Investment Source | Public |

| Private | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe residential construction market today?

It was valued at USD 1,457.5 billion in 2025 and is projected to reach USD 1,863.43 billion by 2031.

Which segment holds the biggest share of activity?

Apartments and condominiums led with 60.2% of total value in 2025.

What growth rate is expected for modern methods of construction?

MMC is forecast to register a 7.45% CAGR between 2026 and 2031.

Why is Poland the fastest-growing national market?

EU cohesion funding, rapid urbanization, and wage growth drive a 6.5% CAGR through 2031.

How are green bonds influencing project finance?

Taxonomy-aligned green bonds priced 35 basis points below conventional debt, trimming weighted-average capital costs by up to 50 basis points in 2025.

Page last updated on: