Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

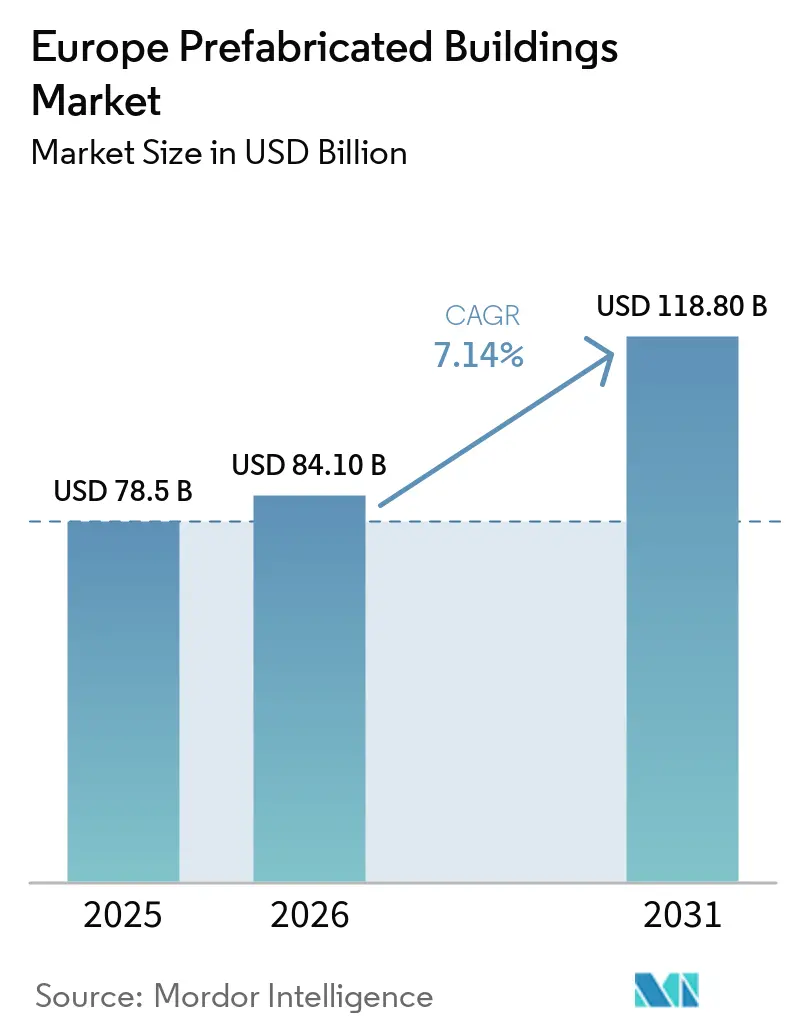

| Base Year Market Size (2025) | USD 78.5 Billion |

| Market Size (2026) | USD 84.10 Billion |

| Market Size (2031) | USD 118.80 Billion |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Prefabricated Buildings Market Analysis by Mordor Intelligence

The Europe prefabricated buildings market size is projected to be USD 78.5 Billion in 2025, USD 84.10 billion in 2026, and reach USD 118.8 billion by 2031, growing at a CAGR of 7.14% from 2026 to 2031[1]European Commission, “Communication on Affordable and Sustainable Housing,” ec.europa.eu. Demand is accelerating as the EU Green Deal renovation-wave mandates push owners to upgrade 35 million structures this decade, while the Carbon Border Adjustment Mechanism (CBAM) raises the delivered cost of non-EU steel and cement, reinforcing local supply chains. A chronic regional labor deficit, 2.3 million open positions in 2025, makes factory assembly attractive because automation compensates for scarce tradespeople. Digital product passports embedded in modules simplify compliance with new lifecycle, carbon reporting rules, and procurement policy across Germany, the Netherlands, and the Nordics increasingly reward timber and hybrid systems that cut embodied emissions by up to 60%.

Key Report Takeaways

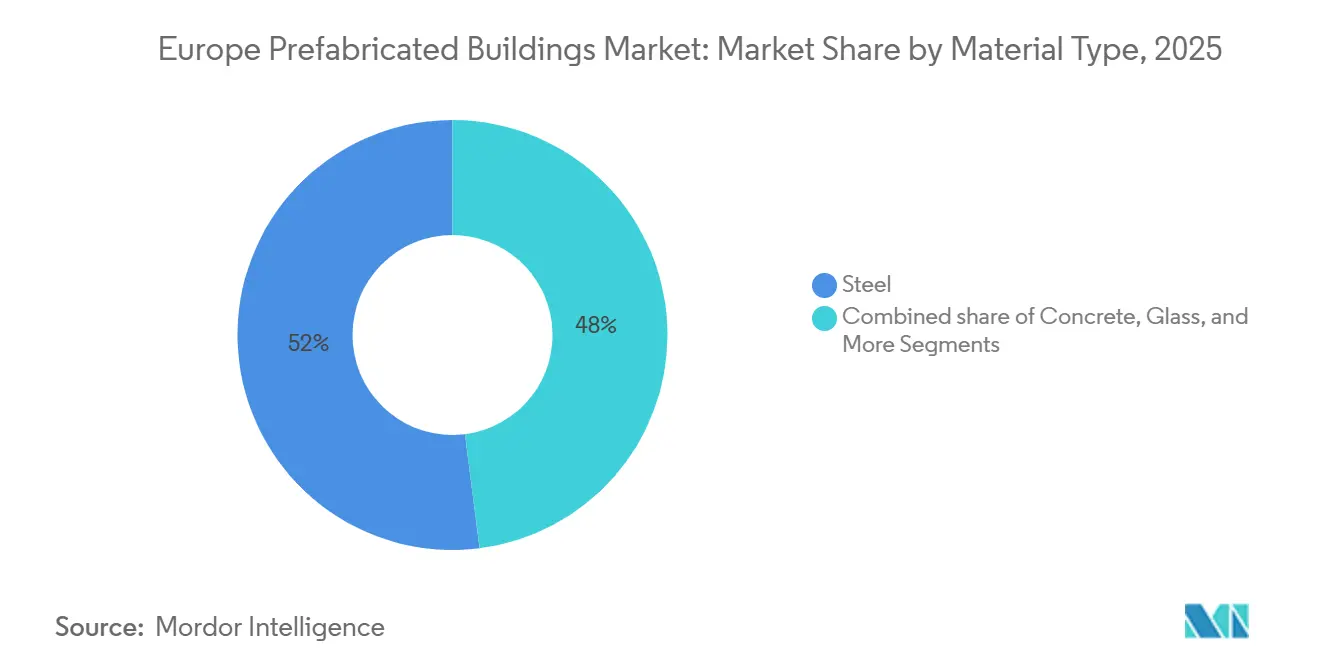

- By material type, metal led with 52% of the Europe prefabricated buildings market share in 2025, while timber is forecast to register a 9.4% CAGR through 2031.

- By application, residential captured 58% of the Europe prefabricated buildings market size in 2025; the “others” segment is projected to expand at an 8.7% CAGR between 2026-2031.

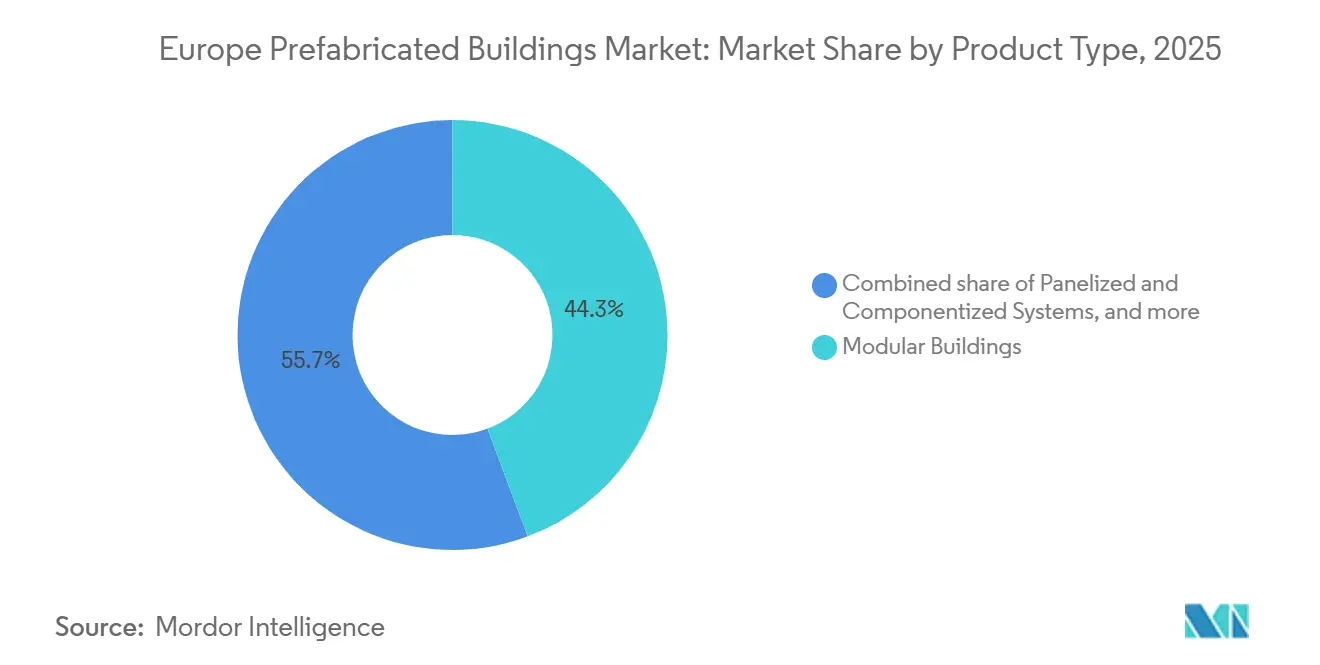

- By product type, modular buildings accounted for 44.3% revenue in 2025, whereas panelised systems are advancing at a 9.9% CAGR to 2031.

- By geography, Germany commanded 35% of regional revenue in 2025, while the Netherlands is expected to register the fastest pace at a 9.2% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Prefabricated Buildings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Affordable-housing gap spurring volumetric residential modules | +2.1% | EU-27, focus on Germany, Spain, Netherlands | Long term (≥ 4 years) |

| EU Green Deal renovation-wave mandates favoring off-site upgrades | +1.8% | EU-27, strongest in Germany, France, Netherlands | Medium term (2–4 years) |

| Persistent skilled-labor shortages across Western Europe | +1.5% | Germany, UK, France, Benelux | Long term (≥ 4 years) |

| Corporate net-zero commitments boosting low-carbon prefab demand | +1.2% | Western Europe, spreading to Southern Europe | Medium term (2–4 years) |

| CBAM cost-shield incentivising EU-made modular steel frames | +0.9% | EU-27, particularly Germany, France, Italy | Short term (≤ 2 years) |

| On-site robotic / 3D-print hybridisation enabling just-in-time modules | +0.7% | Netherlands, Germany, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Green Deal Renovation-Wave Mandates Favoring Off-Site Upgrades

The 2024 update of the Energy Performance of Buildings Directive obliges member states to double annual renovation rates, translating to 35 million units that need new façades, HVAC pods, or roof cassettes by 2030[2]European Parliament, “Energy Performance of Buildings Directive,” europarl.europa.eu. Factory-made envelopes shrink on-site disruption to days, a decisive benefit for occupied properties. Digital renovation passports now award higher tender scores to components that arrive with embedded lifecycle-carbon data. France’s RE2020 rule and Germany’s revised Building Energy Act tighten carbon and renewable-heat quotas, pushing developers toward pre-tested timber and heat-pump modules. As a result, public buyers increasingly specify prefabricated packages to meet both speed and climate targets.

Affordable-Housing Gap Spurring Volumetric Residential Modules

The EU faces a 5.8 million-unit housing shortage and earmarks USD 165 billion annually to close it by 2035. Volumetric modules cut site programs by up to half and slash labor needs by 40%, enabling cities to fast-track social-housing backlogs. The Netherlands now reserves a fifth of zoning permits for modular schemes that deliver keys within 12 months of land release. Spain channels USD 4.9 billion into modular social projects integrating solar roofs and grey-water loops. Berlin’s 1,548-unit Landsberger Allee complex shows that high-density infill can rely on stacked modules without compromising urban form.

Corporate Net-Zero Commitments Boosting Low-Carbon Prefab Demand

More than 2,100 European firms have Science Based Targets, locking in net-zero deadlines that shift procurement toward low-embodied-carbon buildings. Timber-framed retrofits for Vonovia’s multifamily assets removed 70% of construction-phase emissions, while Stora Enso’s CLT headquarters stores 6,000 t CO₂. Companies also want plug-and-play renewable systems: Paf’s glulam office ships with 742 rooftop panels wired at the factory. Suppliers able to certify cradle-to-gate footprints win preference in corporate campus tenders across the Nordics, Germany, and the UK.

Persistent Skilled-Labor Shortages Across Western Europe

FIEC records a 2.3 million worker gap that widened by 400,000 roles between 2021-2025. Vacancy lengths exceed 120 days in Germany, and apprenticeship output trails retirements across the region. Factory assembly mitigates the crunch: productivity studies show modular lines deliver 25-30% more output per employee than traditional sites. UK and French policy now funds off-site upskilling centers, and contractors pivot to robotics that weld, paint, or fit services within controlled environments, insulating delivery schedules from labor volatility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile timber & steel prices eroding cost predictability | -1.3% | EU-27, acute in Nordics and Southern steel importers | Short term (≤ 2 years) |

| Cross-border permitting fragmentation within EU / EEA | -0.8% | Germany-France corridor, Nordics-Baltics | Medium term (2–4 years) |

| Pending EU Construction Products Regulation overhaul delaying certifications | -0.6% | EU-27 manufacturers of novel modules | Short term (≤ 2 years) |

| Digital-factory cybersecurity vulnerabilities raising insurer premiums | -0.4% | Germany, UK, Netherlands | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatile Timber & Steel Prices Eroding Cost Predictability

Hot-rolled coil swung between USD 600-930 per tonne in 2024-2025 as energy markets gyrated and Chinese exports surged[3]European Steel Association, “Market Reports Q4 2024 & Q2 2025,” eurofer.eu. Softwood indices moved 35% year-on-year because bark-beetle infestations trimmed supply and mass-timber demand spike. Such turbulence upends fixed-price contracts: a 20% timber jump can add USD 545,000 to a 100-unit scheme, wiping out margins for SMEs. Without hedging instruments, manufacturers either delay quoting or surcharge clients, dampening tender activity and eroding the growth outlook.

Cross-Border Permitting Fragmentation Within EU / EEA

Even after the 2026 CPR revision, nations keep bespoke fire, acoustic, and seismic rules. A module cleared for Germany’s F30 fire class often needs extra coatings to satisfy France’s stricter M1, adding USD 2,200-5,400 per unit and months of paperwork. Sweden’s prescriptive code clashes with Estonia’s performance framework, forcing dual product lines. The promised Digital Building Logbook will harmonize data by 2028, but today’s patchwork still fragments scale economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Timber Outpaces Metals on Carbon Credentials

Metal retained 52% of the Europe prefabricated buildings market share in 2025 as steel modules dominate temporary schools, site hubs, and healthcare annexes. Yet timber is set to expand at a 9.4% CAGR, the fastest among materials, propelled by EU Taxonomy incentives and eight-story mass-timber breakthroughs that remove concrete cores. Stora Enso’s 7,600 m³ CLT headquarters locks 6,000 t CO₂, signaling acceptance for sizable corporate assets.

Growing timber adoption is reshaping supply networks. TIMBERHAUS pilots circular CLT using hardwood off-cuts, easing pressure on softwood flows. Metsä Wood’s 2026 LVL modules for the Dutch market cut haulage emissions by leveraging local spruce. Denmark’s DGNB-Platinum Marmormolen tower shows fire-safe timber can rise 36 m in dense districts. As CBAM elevates steel costs, carbon-priced tenders tilt toward engineered wood, narrowing metal’s lead within the Europe prefabricated buildings market.

By Application: Residential Commands Majority While Social Infrastructure Accelerates

Residential held 58% of the Europe prefabricated buildings market size in 2025, reflecting an acute shortage of affordable homes. The “others” category, healthcare, education, light industrial, is forecast to grow quickest at 8.7% CAGR through 2031, driven by modular hospitals and schools that can open within nine months. Berlin’s 1,548-unit volumetric complex underscores scale viability, whereas Paf’s solar-clad office proves commercial buyers value energy-positive modules.

Cost-of-living pressures keep municipalities searching for faster build methods: factory economies shave 15-25% off per-unit costs and reduce finance charges tied to shorter schedules. Spain’s USD 4.9 billion housing plan funds modular pilots with rooftop PV and grey-water kits. Meanwhile, flexible work patterns push corporates toward reconfigurable interiors, sustaining non-residential demand within the Europe prefabricated buildings market.

By Product Type: Panelised Systems Gain on Transport Savings

Modular buildings captured 44.3% revenue in 2025, yet panelised and componentised systems are the pacesetters, expanding at 9.9% CAGR thanks to 30-40% lower shipping costs and easy integration with on-site robotics. SISMO’s ETA-certified panels fabricate bespoke layouts without retooling, and Peab doubles output at two Scandinavian plants to meet panel demand.

Volumetric remains unbeatable for prisons, student blocks, and disaster relief where speed and minimal site labor matter; Algeco’s 611-cell UK prison contract proves the point. Still, cramped urban sites favor flat-packs that slide through regular road freight without escorts. Hybrid models, bathroom pods plus panelised walls, balance speed and logistics, and are emerging as a sweet spot in the Europe prefabricated buildings market.

Geography Analysis

Germany controlled 35% of 2025 revenue, aided by a USD 15.9 billion (EUR 14.5 billion) federal housing fund and Länder codes that reward timber and steel modules for rapid occupancy. The Netherlands is the fastest climber at 9.2% CAGR to 2031; its 2024 Housing Pact earmarks 100,000 homes per year and explicitly champions industrialized construction, trimming delivery times below 12 months. Nordic nations contribute 18% of volume, leveraging mature timber supply and municipal carbon budgets that steer specifications to CLT and glulam.

The United Kingdom, outside the EU rulebook, still relies heavily on temporary modular classrooms and clinics, with Algeco locking in USD 101 million (£80 million) of Scottish frameworks in 2025. France, Spain, and Italy share 22% but grow more slowly because disparate permits hinder cross-regional players. France’s RE2020 carbon caps nevertheless propel timber hybrids, while Spain’s seismic-prone zones begin trialing steel-lightweight modules for rapid post-quake rehousing.

Central and Eastern Europe, Poland, Czechia, Baltics, are emerging export hubs. MOD21’s net-zero-electricity Polish factory won USD 44 million orders within eight months, and Estonia’s Harmet ships 3,600 modules yearly to Scandinavia. Lower labor costs and proximity to Nordic forests position the sub-region as a manufacturing back office for the wider Europe prefabricated buildings market.

Competitive Landscape

Modulaire Group dominates rental and semi-permanent niches, expanding its UK Carnaby facility to 60,000 m² and winning USD 101 million in government work. Goldbeck’s 2026 entry into UK residential via the Oak House partnership with Prime plc shows German giants exporting know-how. Skanska pilots “flying factories” that cut costs 28% by situating pop-up workshops near sites, signaling a shift toward distributed manufacturing.

Disruptors exploit digital tooling. Leko Labs’ parametric engine converts customer sketches into fabrication files within hours, shrinking design lead times. KLEUSBERG’s five KUKA robots weld 2,000 m of frames weekly, paring headcount and cycle time. Timber specialists Baufritz and CREE target premium segments where buyers prize embodied-carbon disclosure and architectural flair over lowest cost.

Competitive intensity is rising as CBAM erodes cheap import advantages. Players differentiate on carbon transparency, automation depth, and lifecycle services such as module take-back or refurbishment. The European Technical Assessment pathway offers market access for novel systems, yet a 12-18 month queue forces innovators to plan product launches early. Consolidation pressure is likely as mid-sized firms seek scale to fund certification, R&D, and cybersecurity upgrades.

Europe Prefabricated Buildings Industry Leaders

Skanska AB

Modulaire Group (Algeco Scotsman)

Lindbäcks Bygg

Portakabin Ltd

Huf Haus

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Goldbeck and Prime plc broke ground on the 79-unit Oak House key-worker scheme in Dorchester, the firm’s first UK residential venture.

- February 2026: Metsä Wood launched LVL modules tailored to Dutch housing, cutting haulage distance and lead times.

- August 2025: Modulaire Group refinanced USD 2.1 billion (EUR 1.9 billion) of debt to 2031 and announced a new CEO as ERP roll-out continued.

- June 2025: Laing O’Rourke and KONE revealed a lift module that installs in 26 minutes, replacing a 32-week on-site process.

Europe Prefabricated Buildings Market Report Scope

By Material Type

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Others |

By Product Type

| Modular Buildings |

| Panelised & Componentised Systems |

| Other Prefab Types |

By Country

| Germany |

| United Kingdom |

| France |

| Spain |

| Italy |

| Netherlands |

| Sweden |

| Denmark |

| Norway |

| Rest of Europe |

| By Material Type | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application | Residential |

| Commercial | |

| Others | |

| By Product Type | Modular Buildings |

| Panelised & Componentised Systems | |

| Other Prefab Types | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Sweden | |

| Denmark | |

| Norway | |

| Rest of Europe |

Key Questions Answered in the Report

What is the forecast value of the Europe prefabricated buildings market by 2031?

The market is projected to reach USD 118.8 billion by 2031, reflecting a 7.14% CAGR between 2026 and 2031.

How large will Europe’s prefabricated buildings sector be by 2031?

The Europe prefabricated buildings market size is projected to reach USD 118.8 billion by 2031, expanding at a 7.14% CAGR from 2026.

Which material leads the adoption curve today?

Metal modules dominate with 52% share in 2025, though engineered timber is the fastest-growing material at 9.4% CAGR.

Why are governments turning to modular housing?

Factory-built apartments cut build times up to 50% and reduce labor needs 40%, helping close the EU’s 5.8 million-unit housing deficit.

How does CBAM influence supply chains?

The carbon levy lifts import costs for steel frames by roughly 15-20%, steering procurement toward EU-made modular systems.

Which country shows the quickest growth outlook?

The Netherlands leads with a forecast 9.2% CAGR through 2031, driven by a national pact targeting 100,000 industrialized homes annually.

Page last updated on: