Dyestuff For Cotton Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

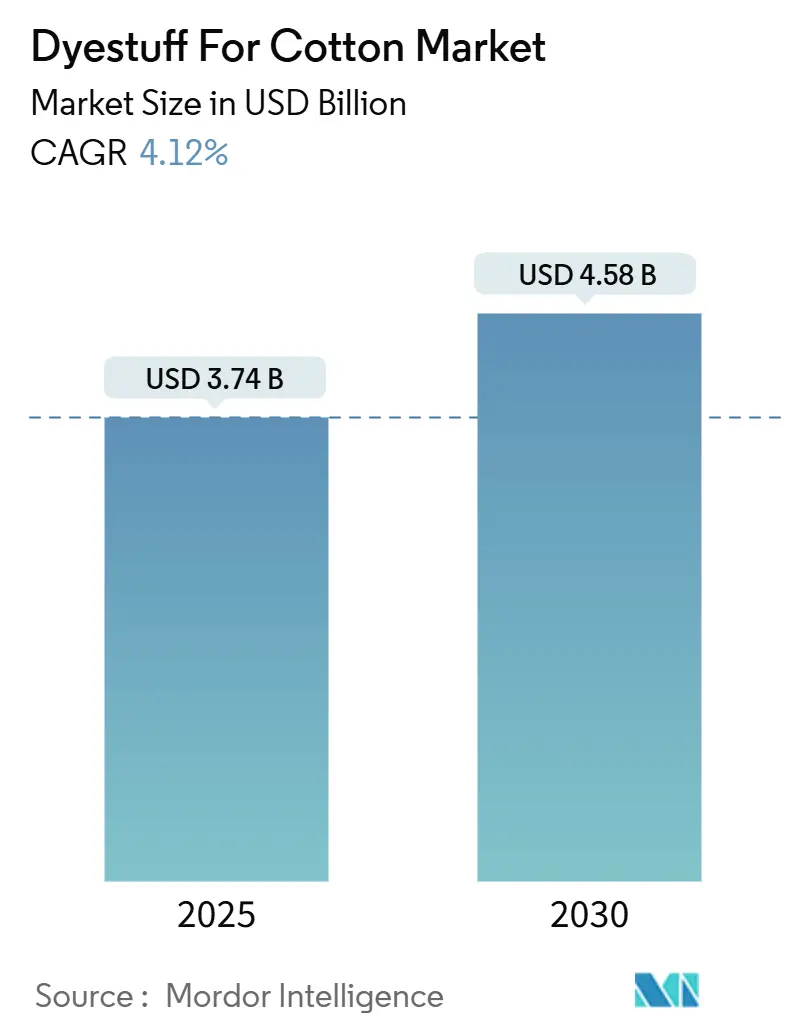

| Market Size (2025) | USD 3.74 Billion |

| Market Size (2030) | USD 4.58 Billion |

| Growth Rate (2025 - 2030) | 4.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dyestuff For Cotton Market Analysis by Mordor Intelligence

The Dyestuff For Cotton Market size is estimated at USD 3.74 billion in 2025, and is expected to reach USD 4.58 billion by 2030, at a CAGR of 4.12% during the forecast period (2025-2030). The outlook is underpinned by steady apparel demand, accelerated adoption of salt-free reactive dyeing, and rising penetration in medical and protective technical textiles. High-wash-fastness reactive chemistries, digital printing growth, and government-backed green textile parks are reshaping the competitive field while opening premium niches for performance-enhanced shades. Mid-stream players are integrating upstream to secure intermediates, and downstream brands are shifting toward suppliers that can certify zero-liquid-discharge production in line with global stewardship programs.

Key Report Takeaways

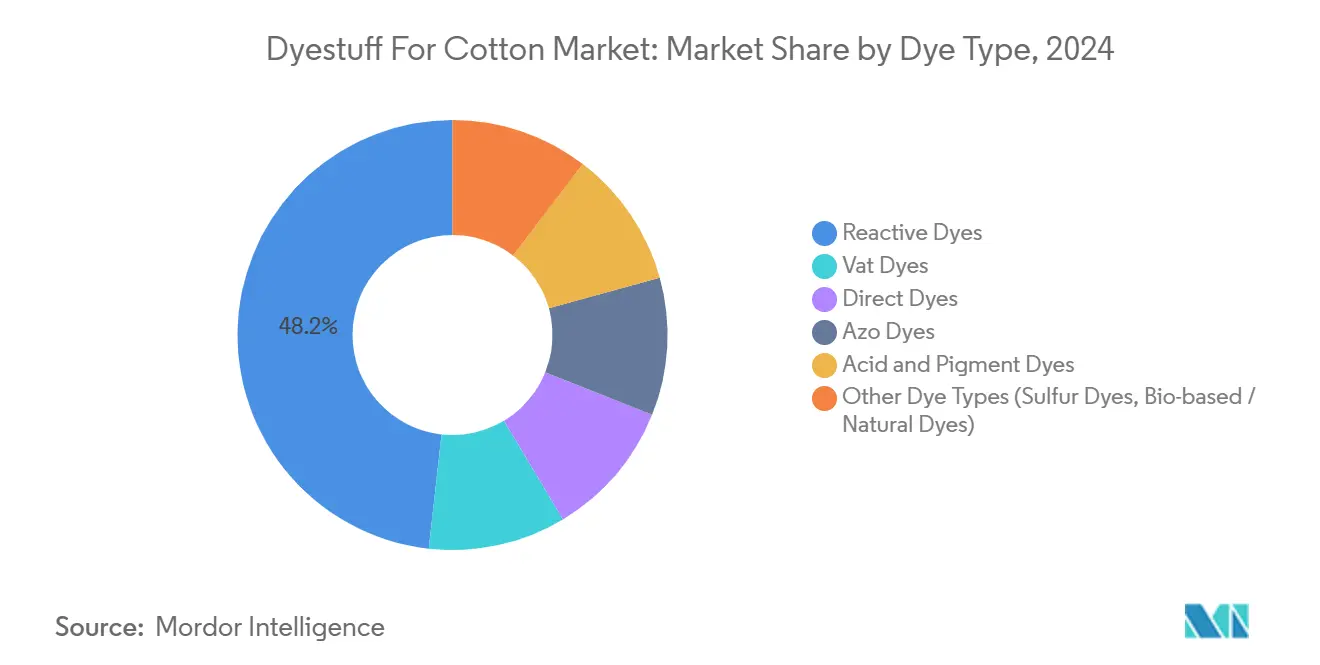

- By dye type, reactive dyes held 48.23% of the cotton dyestuff market share in 2024, and other dye types led by bio-based alternatives are projected to expand at a 4.67% CAGR through 2030.

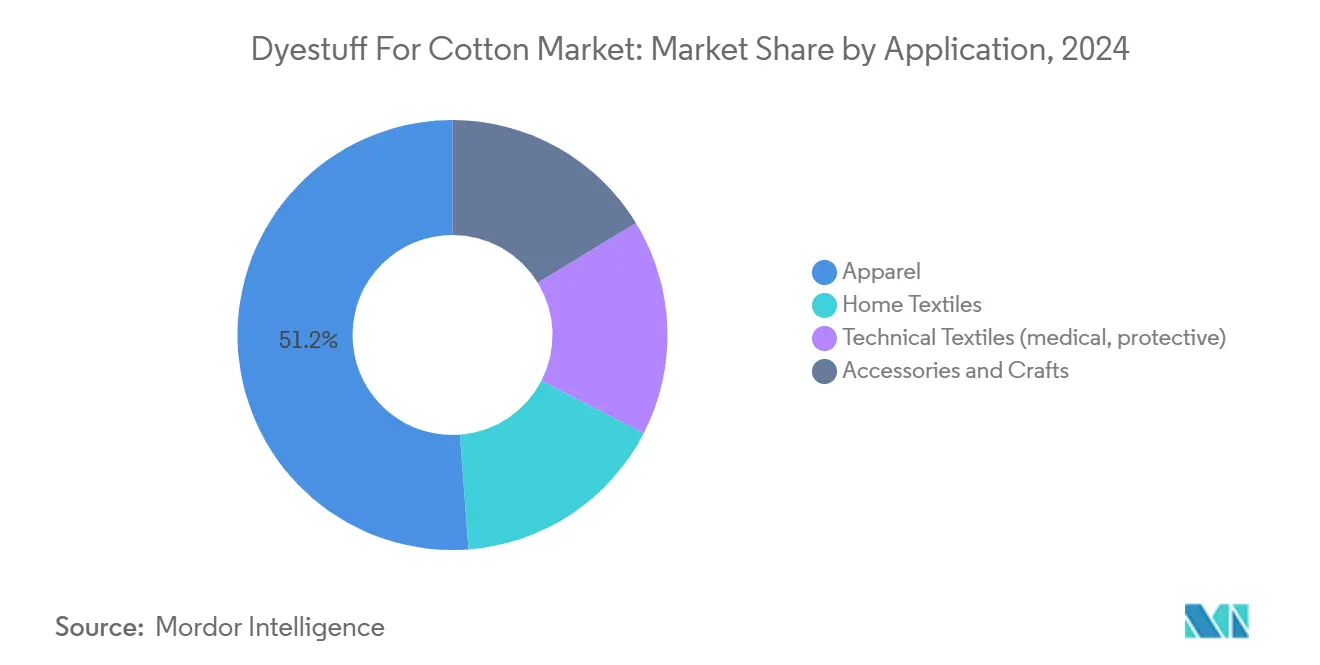

- By application, apparel accounted for 51.18% of the cotton dyestuff market size in 2024, while technical textiles recorded the fastest growth at 4.82% CAGR to 2030.

- By the dyeing process, exhaust/batch operations captured 51.87% revenue share in 2024, whereas digital printing advances at a 4.98% CAGR between 2025-2030.

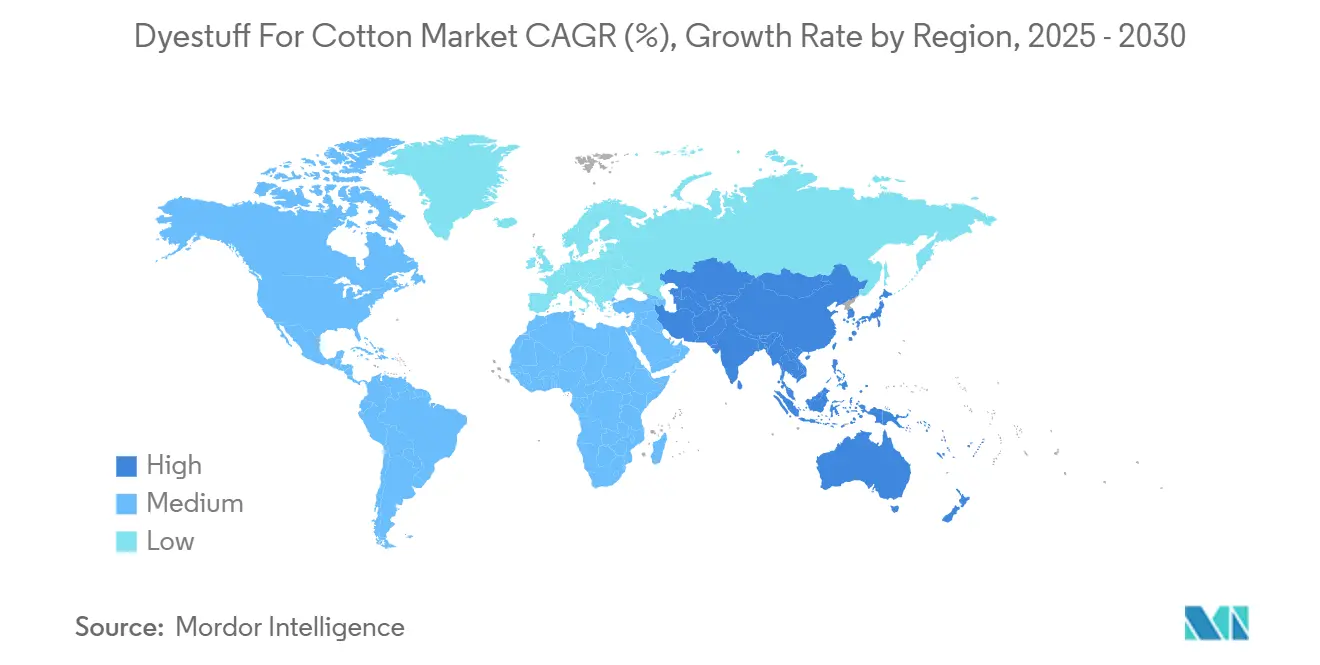

- By geography, Asia-Pacific claimed 46.72% revenue share in 2024 and is set to lead with a 4.81% CAGR during the forecast window.

Global Dyestuff For Cotton Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for cotton apparel and home textiles | +1.2% | Global, with a concentration in Asia-Pacific and Europe | Medium term (2-4 years) |

| Expansion of textile manufacturing hubs in developing economies | +0.9% | Asia-Pacific core, spill-over to South America and MEA | Long term (≥ 4 years) |

| Rapid shift toward high-wash-fastness reactive dyes | +0.8% | Global, led by North America and Europe quality standards | Short term (≤ 2 years) |

| Government incentives for green textile parks | +0.6% | Asia-Pacific, particularly India and China | Medium term (2-4 years) |

| Deployment of salt-free reactive dyeing systems | +0.5% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Cotton Apparel and Home-Textiles

Global consumers are prioritizing natural fiber comfort, pushing retailers to secure durable, sustainably dyed cotton ranges. In Europe, 86% of shoppers rank sustainability as a leading purchase factor, with millennials and Gen Z steering the shift toward organic cotton goods[1]CBI Market Intelligence, “Which trends offer opportunities or pose threats on the European home decoration and home textiles market?,” cbi.eu. Record Brazilian cotton exports also improve raw-fiber availability for regional dyestuff producers, shortening supply chains and allowing quicker fashion-cycle response. Home-textile categories such as ready-made curtains rose to EUR 1.9 billion in 2021, a trend that sustains bulk demand for eco-certified shades in bedding, upholstery, and decorative fabrics. Post-pandemic wellness spending extends product lifecycles, so buyers request wash-fast and antimicrobial coloration to assure prolonged household hygiene. Regional dyestuff distributors that offer rapid color-matching earn an advantage in a market where shorter design releases are becoming the norm.

Expansion of Textile Manufacturing Hubs in Developing Economies

New mills in India, Vietnam, and parts of Africa capitalize on labor cost competitiveness while installing automated dyeing units that demand consistent, higher-purity dyestuff. Maharashtra approved 18 mini parks backed by INR 1,800 crores, each with shared effluent treatment to streamline compliance. Vietnam’s Binh Dinh expansion by an Israeli group adds 15.9 million m² of annual knit capacity and locks in local dye supply contracts. Clustering shortens lead times from greige fabric to finished garment, prompting dyestuff makers to commission regional warehouses that curb freight costs and enhance delivery reliability. Water-scarce Xinjiang, where over 60% of China’s cotton grows, is trialing concentrated liquor-ratio technologies to slash freshwater use during coloration

Rapid Shift Toward High-Wash-Fastness Reactive Dyes

Retailers face scrutiny on color degradation after multiple laundering cycles, especially for uniforms and hospital linens that must endure industrial washing. Covalent bonding between reactive dyes and cotton hydroxyl groups maintains brilliance and reduces re-dyeing needs, a performance edge validated in comparative trials on ramie and cotton substrates. DyStar’s Cadira Reactive platform saves 40% chemicals while complying with global fastness norms, proving large-scale viability. High-wash-fastness grades now penetrate technical textiles, where repeated sterilization demands exceptional color lock without fiber damage. Vinyl sulfone–monochlorotriazine dual-anchor molecules provide extra attachment sites, extending the dye–fiber union beyond 50 industrial cycles and reinforcing premium price positioning.

Deployment of Salt-Free Reactive Dyeing Systems

Reactive dyeing traditionally discharges up to 100 g/L salt, raising treatment costs and intensifying ZDHC scrutiny. CHPTAC cationization eliminates electrolyte need by imparting positive charges on cotton, improving exhaustion rates without compromising shade depth. TNA protocols drive 99% COD and 97% TDS reductions against conventional salt/alkali baths. Nike’s waterless pilot plant cut energy 60% and set a commercial precedent for mass-scale electrolyte-free lines. Early adopters gain lower wastewater surcharges and stronger branding credentials, a compelling incentive amid consumer pressure for measurable impact metrics.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Waste-water pollution and ZDHC compliance costs | -0.8% | Global, with stricter enforcement in North America and Europe | Short term (≤ 2 years) |

| Volatility in dye-intermediate prices (H-acid, vinyl sulfone) | -0.6% | Global, with supply concentration in Asia-Pacific | Medium term (2-4 years) |

| Competition from dye-free colorization of regenerated cellulose | -0.3% | Europe and North America, early adoption markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Waste-Water Pollution and ZDHC Compliance Costs

The ZDHC Manufacturing Restricted Substances List caps aniline, arylamines, and metals at parts-per-million thresholds, prompting formulators to re-engineer shade cards and finance new analytics. The US EPA is assessing PFAS in textile effluent, a signal that cotton dyestuff recipes containing fluorinated auxiliaries may soon face tighter curbs. European dyers navigate a mosaic of member-state water standards, forcing multinational groups to align operations with the strictest benchmarks to maintain seamless brand certification. Reverse-osmosis and MBR systems add USD 90/m³ to processing costs, a material burden for commodity fabric converters that already operate on thin margins. The capital outlay pushes some players toward relocation, fragmenting global supply nodes.

Competition from Dye-Free Colorization of Regenerated Cellulose

Emerging extrusion technologies impregnate pigment at the spinning stage, eliminating dye baths for lyocell or modal fibers. Brands exploring cradle-to-cradle certification view dope-dye schemes as a straightforward route toward zero-effluent targets. Although cotton retains a natural fiber halo and comfort benefits, regenerated cellulose now offers pastel colorways without post-dyeing water use, a proposition that can draw away volume from preciously dyed cotton lines in niche athleisure or lingerie segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dye Type: Reactive Grades Set the Baseline for Performance Needs

Reactive grades accounted for a 48.23% cotton dyestuff market share in 2024. Covalent fixation provides a delta-E color shift under 1 after 20 consumer washes, reinforcing their status as the default chemistry for mass-market tees and pajamas. The cotton dyestuff market size tied to reactive dyes is projected to expand alongside integrated continuous lines that leverage automated dosing to minimize shade variance. Emerging “other dye types” amalgamate sulfur, natural, and bio-derived options and post a 4.67% CAGR to 2030, reflecting both regulatory tailwinds and brand storytelling opportunities. Consumers perceive plant-based colorants such as oolong tea stem extracts as safer and more skin-friendly[2]MDPI Editorial Office, “Eco-Friendly Dyeing and Functional Finishing of Organic Cotton Using Optimized Oolong Tea Stems,” mdpi.com.

Vat dyes remain pertinent for workwear that faces prolonged ultraviolet exposure, though they cede share to high-light-fastness reactive hybrids tuned for open-end yarn. Direct dyes linger in budget segments, while azo restrictions in the EU accelerate their displacement even in price-sensitive zones.

By Dyeing Process: Digital Printing Redraws the Production Map

Exhaust systems retain a 51.87% share given entrenched vat capacity and compatibility with varied fabric counts, yet their fluid consumption footprint creates regulatory headwinds. Digital printing is the fastest riser at 4.98% CAGR as design-to-shelf cycles compress and brands embrace on-demand micro-drops. Carboxylate-modified reactive inks eliminate alkaline pre-soaks, curbing water and energy demand while sidestepping fabric fibrillation risks. The cotton dyestuff market share for digital formulations sees steady new entrants from ink majors repositioning away from solvent systems toward water-based offerings.

Continuous dyeing retains favour for denim and sheeting lines where homogenous shade build and high throughput justify capital costs. Semi-continuous pad-batch bridges small-run flexibility and medium-volume economics, though it loses momentum to direct-to-fabric printers as machine speeds climb past 200 m²/h. Gujarat’s new Optima plant was commissioned specifically to support toluene-free, ketone-free inks for this segment

By Application: Technical Textiles Capture Premium Growth Momentum

Apparel generated 51.18% of the 2024 value, but growth slows as fashion chains rationalize SKU counts and switch to seasonless assortments. Conversely, technical textiles log the highest 4.82% CAGR to 2030, buoyed by hospital disposables, military uniforms, and personal protective equipment requiring proven antimicrobial, flame-retardant, or UV-absorbent functions. The cotton dyestuff market size in technical textiles benefits directly from higher price realization, as buyers accept a 10-15% pigment premium to meet stringent safety norms. Medical fabrics finished with lignin nanoparticle dispersions block Staphylococcus aureus replication while retarding oxidative degradation, extending single-use drape longevity.

Accessories and crafts preserve a niche reliant on color constancy and small-batch artisanal appeal. Here, regional micro-blenders thrive by offering bespoke pantone matches on 48-hour lead times, distinguishing themselves from multinationals optimized for container-scale logistics. The broader diversification away from single-end-use dependence mitigates seasonality risk for dyestuff vendors and underpins long-term revenue stability.

Geography Analysis

Asia-Pacific dominated with 46.72% revenue in 2024 and is forecast at a 4.81% CAGR through 2030. The cotton dyestuff market size in India is primed for double-digit expansion as the PM MITRA parks roll out shared zero-liquid-discharge hubs backed by INR 18,500 crores commitments. China’s Xinjiang pivot toward concentrated dye baths reduces freshwater withdrawals, a response to an arid climate and regulatory guardrails.

North America targets technical and protective fabrics that yield higher unit margins. Archroma invested USD 750,000 in South Carolina to localize sophisticated shades for defense and work-wear clients. Subsidies for reshoring critical PPE supply chains sustain demand for low-formaldehyde, high-fastness dyes certified under US performance standards. Europe continues to punch above its weight due to 86% consumer enthusiasm for sustainability credentials, pushing dyers to certify cradle-to-cradle loops.

South America gains strategic prominence as Brazil’s record 3.7 million-ton cotton harvest elevates local spinning utilization and trims freight distance between farm and mill. Lower feedstock transit translates into 6-8% logistical savings, part of which flows to dyestuff purchases. Middle East and Africa experience gradual uptake, led by Egypt’s long-staple cotton heritage and nascent Ethiopian industrial parks courting Asian investors. Infrastructure gaps and water scarcity remain obstacles, yet pilot zero-liquid-discharge projects point toward accelerated modernization once policy incentives align.

Competitive Landscape

Market structure is moderately fragmented. DyStar enhances vertical grip by co-locating intermediate synthesis units near its Indonesian and Chinese formulation hubs, buffering price volatility associated with H-acid. Atul Ltd extends downstream into garment pre-treatment chemicals, promoting bundled supply contracts that lock in color consistency across full processing chains. Smaller niche players focus on low-minimum-order custom shades for couture and craft, building loyalty through speed and flexibility rather than price.

Dyestuff For Cotton Industry Leaders

Archroma

Atul Ltd.

DyStar Singapore Pte Ltd

Kiri Industries Ltd.

lonsen, inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Sudarshan Chemical Industries Limited, through its wholly owned subsidiary Sudarshan Europe B.V., completed the acquisition of Germany-based Heubach Group, adding an extensive inorganic pigment portfolio.

- February 2023: Archroma finalized the acquisition of the Textile Effects division of Huntsman Corporation, integrating dyes, chemicals, and sustainability services to support global textile customers.

Global Dyestuff For Cotton Market Report Scope

| Reactive Dyes |

| Vat Dyes |

| Direct Dyes |

| Azo Dyes |

| Acid and Pigment Dyes |

| Other Dye Types (Sulfur Dyes, Bio-based / Natural Dyes) |

| Exhaust / Batch Dyeing |

| Continuous Dyeing |

| Semi-continuous (Pad-Batch) |

| Digital / Ink-jet Printing |

| Apparel |

| Home Textiles |

| Technical Textiles (medical, protective) |

| Accessories and Crafts |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Dye Type | Reactive Dyes | |

| Vat Dyes | ||

| Direct Dyes | ||

| Azo Dyes | ||

| Acid and Pigment Dyes | ||

| Other Dye Types (Sulfur Dyes, Bio-based / Natural Dyes) | ||

| By Dyeing Process | Exhaust / Batch Dyeing | |

| Continuous Dyeing | ||

| Semi-continuous (Pad-Batch) | ||

| Digital / Ink-jet Printing | ||

| By Application | Apparel | |

| Home Textiles | ||

| Technical Textiles (medical, protective) | ||

| Accessories and Crafts | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is global spending on cotton dyestuff in 2025?

It stands at USD 3.74 billion and is on track for a 4.12% CAGR to 2030.

Which dye type dominates commercial cotton coloration?

Reactive dyes hold 48.23% of 2024 revenue thanks to superior wash-fastness and broad machinery compatibility.

Why is Asia-Pacific critical for suppliers?

The region contributes 46.72% of 2024 demand and enjoys integrated cotton, dye, and textile clusters plus generous green-park incentives.

What application offers the fastest revenue growth?

Technical textiles lead with a 4.82% CAGR through 2030, driven by medical and protective fabric orders.

How are brands reducing dyehouse environmental impact?

They adopt salt-free reactive systems, digital printing, and zero-liquid-discharge parks to lower water, salt, and effluent loads.

Page last updated on: