Textile Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

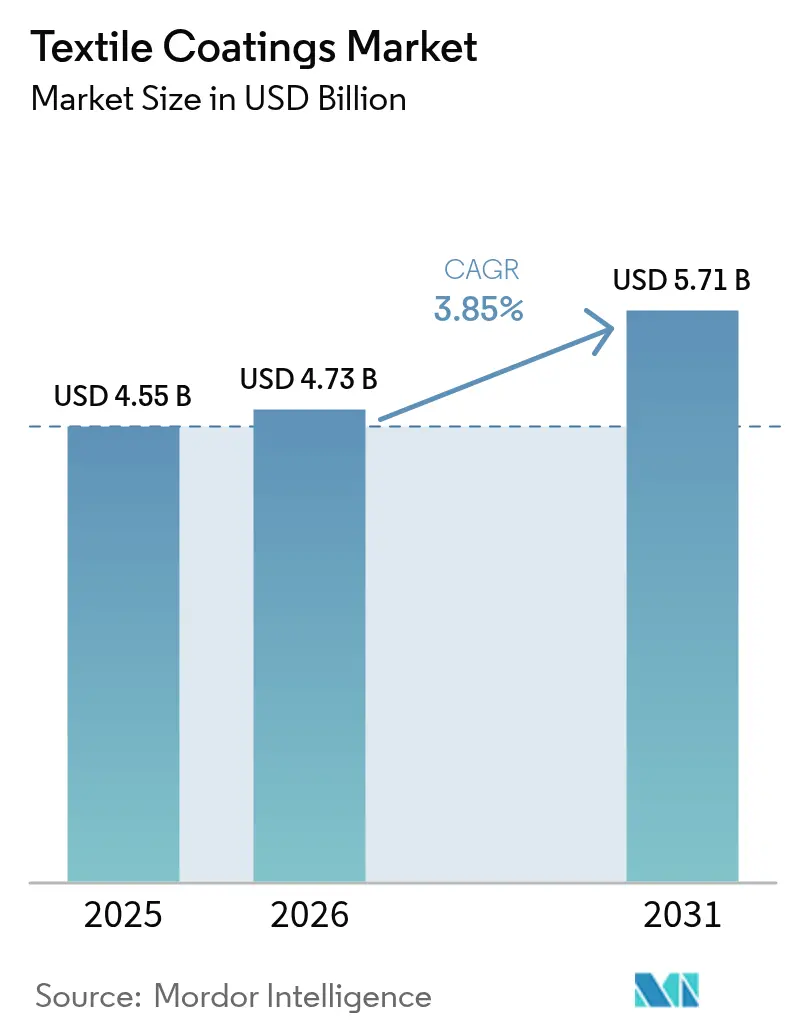

| Market Size (2026) | USD 4.73 Billion |

| Market Size (2031) | USD 5.71 Billion |

| Growth Rate (2026 - 2031) | 3.85% CAGR |

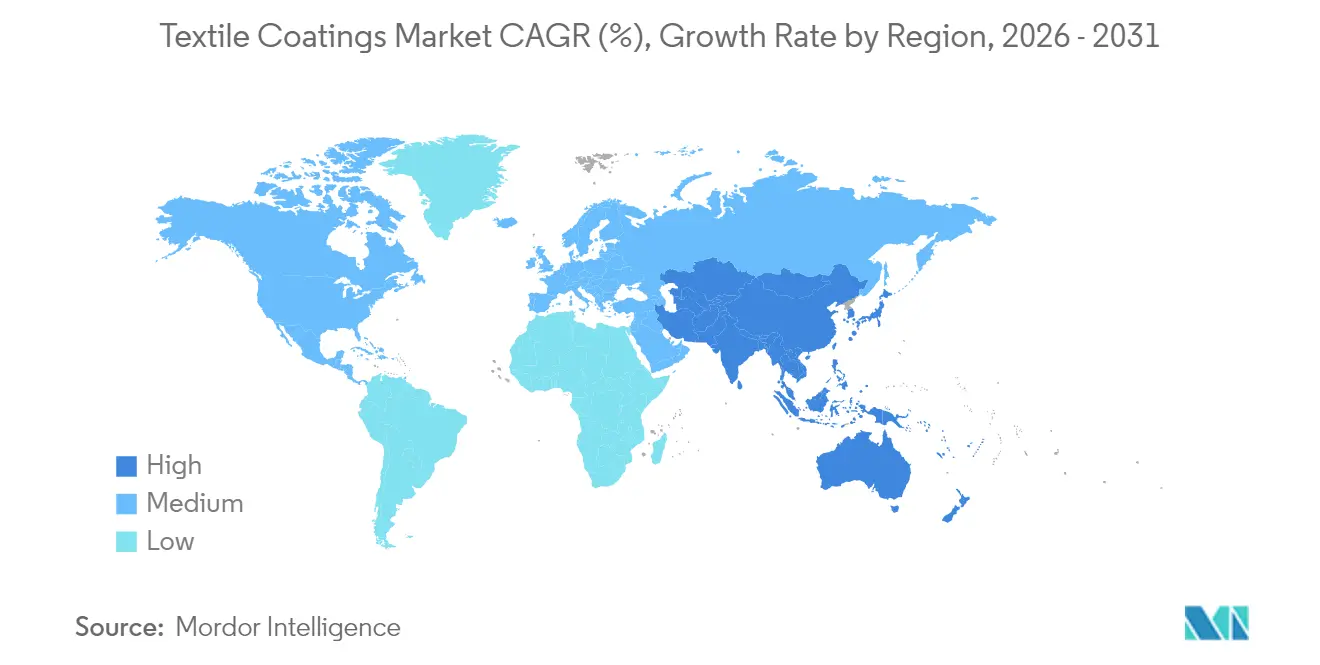

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

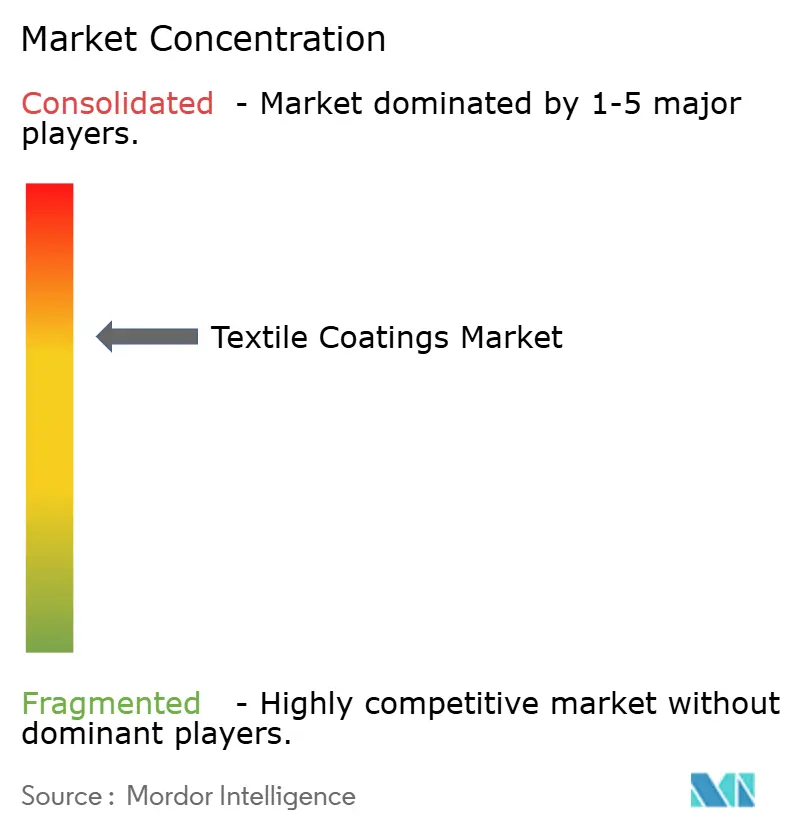

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Textile Coatings Market Analysis by Mordor Intelligence

Textile Coatings Market size in 2026 is estimated at USD 4.73 billion, growing from 2025 value of USD 4.55 billion with 2031 projections showing USD 5.71 billion, growing at 3.85% CAGR over 2026-2031. Accelerated migration toward waterborne and solvent-free polymer systems sits at the center of this shift, as manufacturers seek lower VOC profiles without compromising durability or aesthetics. Asia-Pacific retains cost-leadership advantages and absorbs a majority of new capacity, while North America and Europe propel high-performance chemistry and regulatory frameworks that influence global formulation choices. Medical, automotive, and infrastructure segments are reframing performance benchmarks around antimicrobial, weather-resistant, and flame-retardant properties, prompting suppliers to diversify away from legacy PFAS chemistries. Investments in silicone-based emulsions, plasma surface treatment, and digital application lines reveal a competitive field willing to trade volume for specialty performance and margin resilience. Against this backdrop, the textile coatings market continues to balance cost, compliance, and customization pressures that collectively shape technology road maps through 2030.

Key Report Takeaways

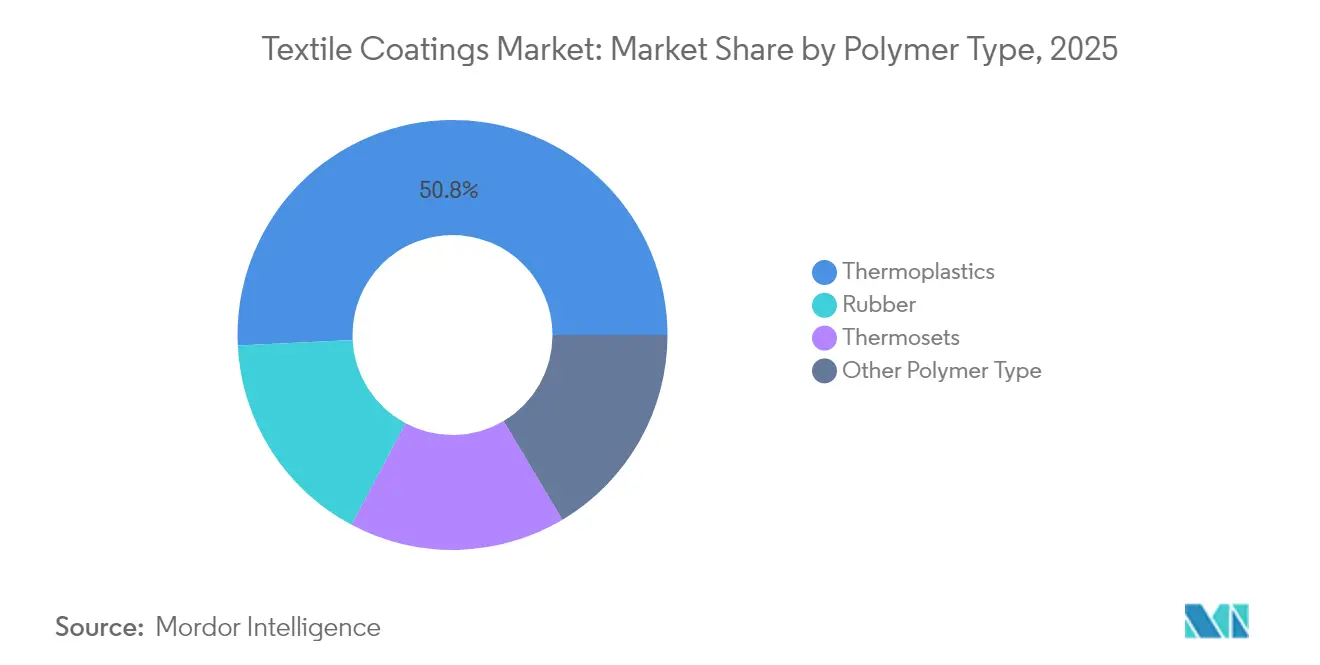

- By polymer type, thermoplastics dominated with 50.78% textile coatings market share in 2025, and are projected to grow at 6.22% CAGR through 2031.

- By fabric type, woven fabrics captured 44.92% of textile coatings market share in 2025 and are advancing at a 5.88% CAGR.

- By functionality, waterproof and breathable finishes commanded 30.12% of the textile coatings market size in 2025, yet antimicrobial and antiviral coatings register the highest 6.63% CAGR.

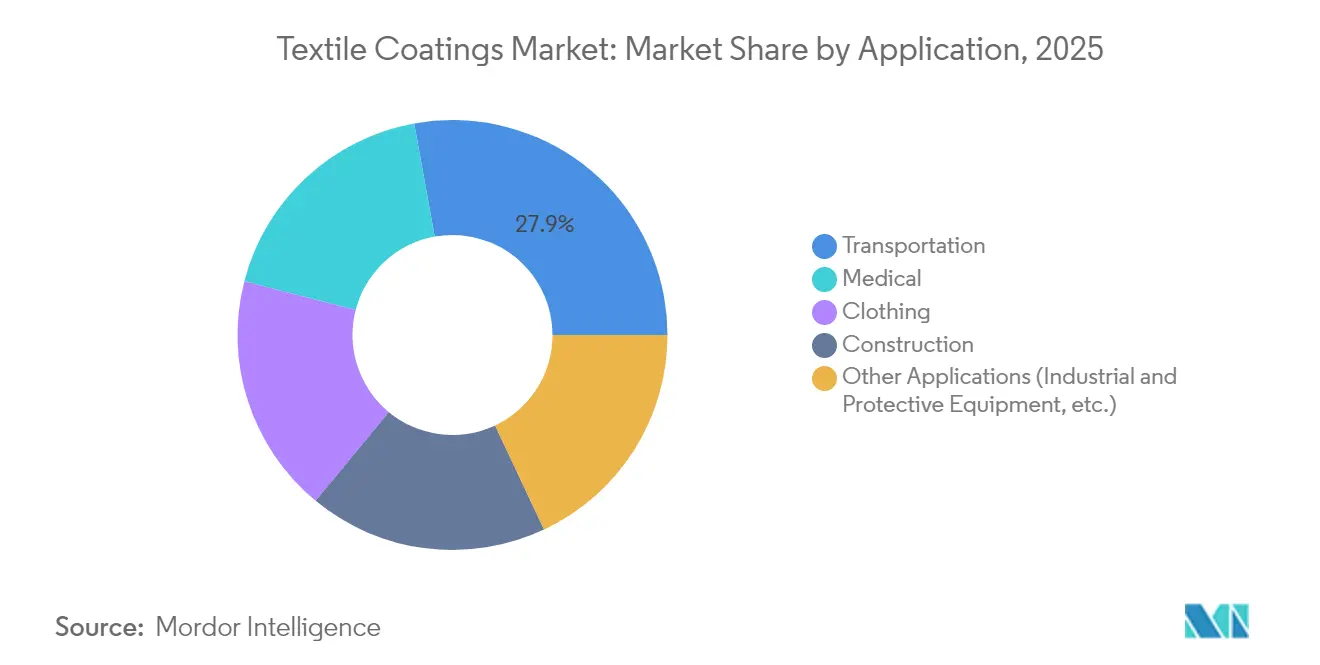

- By application, transportation held 27.85% of the textile coatings market size in 2025, whereas medical textiles represent the fastest growth trajectory at a 6.03% CAGR to 2031.

- By geography, Asia-Pacific led with 52.74% of textile coatings market share in 2025; the region is forecast to expand at a 5.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Textile Coatings Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing standards for protective textiles | +0.8% | Global, with emphasis on North America & EU | Medium term (2-4 years) |

| Growing demand in automotive & transportation upholstery | +1.1% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Rising need for durable & weather-resistant fabrics in construction & infrastructure | +0.7% | Global, concentrated in emerging markets | Long term (≥ 4 years) |

| Shift toward waterborne & solvent free polymers complying with VOC regulations | +0.9% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Emergence of antimicrobial & antiviral nano-coatings in healthcare textiles | +0.6% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Standards for Protective Textiles

Global regulators are tightening performance and safety benchmarks, prompting manufacturers to develop flame-resistant, chemical-resistant, and moisture-barrier solutions that eliminate PFAS while meeting updated norms such as NFPA 1971-2018. Milliken introduced non-PFAS alternatives that surpass earlier durability thresholds, stimulating competitive innovation and accelerating test-lab investments among rivals. European suppliers extend the focus to bio-based chemistries to align with Green Deal ambitions, and demand extends from firefighting ensembles to industrial workwear, broadening commercial potential for compliant chemistries within the textile coatings market.

Growing Demand in Automotive and Transportation Upholstery

Lightweighting agendas and premium cabin expectations in electric and autonomous vehicles translate into coatings that deliver abrasion resistance, thermal management, and antimicrobial properties all in one layer. Health concerns about legacy flame retardants reported in mainstream media spur reformulations toward safer alternatives, steering procurement toward platforms that satisfy both OEM sustainability goals and stringent interior-air-quality metrics. Asian converters leverage cost and scale advantages to win upholstery contracts, reinforcing Asia-Pacific’s role as demand and supply nucleus for the textile coatings market.

Rising Need for Durable and Weather-Resistant Fabrics in Construction and Infrastructure

Public- and private-sector infrastructure programs across emerging economies rely on coated roofing membranes, awnings, and geosynthetics to achieve longevity under harsh climate cycles. ExxonMobil and Freudenberg are commercializing UV-stable, recycled-content systems that withstand prolonged solar and moisture exposure, positioning the textile coatings market as a subtle yet critical component of resilient construction value chains.

Shift Toward Waterborne and Solvent-Free Polymers Complying With VOC Regulations

The latest EPA aerosol-coating amendments and California’s May 2025 limits sharpen industry attention on VOC ceilings, reinforcing corporate road maps aimed at waterborne polyurethane and silicone dispersions. Covestro’s INSQIN range demonstrates how low-VOC systems can outperform solvent-borne predecessors in flexibility and weathering, while Asian exporters adopt similar chemistries to maintain market access to stringent jurisdictions [1]Covestro AG, “INSQIN® Waterborne PU for Textiles,” covestro.com. The collective transition underpins mid-term growth in specialty elastomers within the textile coatings market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating prices of key raw polymers | -0.7% | Global, with acute impact in APAC | Short term (≤ 2 years) |

| High capital cost of coating machinery & lines | -0.5% | Emerging markets, particularly in South America & MEA | Medium term (2-4 years) |

| Competition from plasma & other dry finishing alternatives | -0.3% | Developed markets with advanced manufacturing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuating Prices of Key Raw Polymers

Polyvinyl alcohol, cotton, and oil-derived synthetics exhibit recurrent price swings that distort planning cycles and erode margins among coaters heavily exposed to spot markets. Polyvinyl alcohol price declines in early 2025, yet synthetic fiber costs climbed 10-15% on oil volatility, producing a mixed input-cost picture that forces cautious inventory management and long-term supply contracts. Such volatility introduces near-term earnings uncertainty in the textile coatings market.

High Capital Cost of Coating Machinery and Lines

Transitioning to waterborne systems necessitates advanced drying, exhaust, and automation setups that can cost USD 10 million or more for an integrated line, placing formidable entry barriers before smaller regional players. INVISTA’s USD 23 million CAD recommissioning of HMD assets illustrates the scale of cash outlay required to sustain competitiveness. Financing constraints in emerging regions decelerate capacity additions and potentially cap regional supply growth within the textile coatings market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PolymerType: Thermoplastics Command Both Scale and Growth

Thermoplastic polymers dominate the segment with 50.78% of textile coatings market share in 2025, reflecting their balance of cost efficiency, mechanical strength, and recyclability. Demand concentrates in automotive upholstery, protective apparel, and flexible construction membranes where abrasion resistance and dimensional stability are mandatory. End-users favor thermoplastics for compatibility with waterborne and solvent-free coating chemistries that align with tightening VOC limits. Lightweight electric-vehicle interiors and modular infrastructure projects further elevate volume requirements. These combined drivers anchor thermoplastics as the preferred substrate for high-performance coatings across major consumption regions.

Thermoplastic polymers will also deliver the fastest 6.22% CAGR through 2031, underscoring their dual leadership in both scale and momentum within the textile coatings market size. Competitive materials such as natural, cellulose-based, and thermoset fibers trail in growth because they struggle to match the processing speed, thermal tolerance, and recyclability advantages of thermoplastics. Incremental innovations in copolymer blends and surface treatments continue to raise the performance ceiling without sacrificing environmental compliance. As downstream brands expand circular-economy commitments, the prospect of re-melting and re-processing coated thermoplastic fabric reinforces long-term attractiveness. Consequently, capital expenditure in new coating lines increasingly targets thermoplastic-friendly configurations to secure capacity for the segment’s sustained expansion.

By Fabric Type: Woven Fabrics Maintain Dual Dominance

Woven substrates achieved 44.92% textile coatings market share in 2025 and pair that dominance with a 5.88% CAGR, reflective of their inherent tensile strength, dimensional stability, and superior coating anchorage. Automotive, architectural, and safety segments, which cannot compromise on structural integrity, prefer woven constructions for long-term performance. Non-woven advancements begin gaining traction in medical disposables and filtration media, aided by engineered porosity that improves coating penetration and functional uniformity.

Knitted fabrics occupy niches demanding stretch and drape, yet adhesion and shape-retention limits constrain penetration in large technical applications. Hybrid multilayer fabrics combining woven stability with knitted comfort emerge in sports and medical braces, indicating that substrate innovation remains a critical lever for differentiation within the textile coatings market.

By Functionality: Antimicrobial Surge Challenges Waterproof Leadership

Waterproof and breathable finishes kept the largest 30.12% share in 2025, fueled by outdoor apparel, tents, and roofing. Segment incumbency is now challenged by antimicrobial and antiviral chemistries growing at 6.63% CAGR, catalyzed by infection-control priorities across public, commercial, and residential environments. Copper, silver, and quaternary ammonium platforms are integrated through pad-dry-cure, plasma, and digital-print methods, achieving commercial-laundry durability benchmarks that once hindered market acceptance.

Regulatory initiatives banning PFAS push R&D toward silicone-based and bio-based water-repellent options that maintain water column ratings while avoiding persistent chemicals. Dual-function coatings that offer moisture management and antimicrobial performance in a single layer underscore the march toward multifunctionality that reduces processing steps and material layering.

By Application: Transportation Leadership Challenged by Medical Growth

Transportation applications held 27.85% of the textile coatings market size in 2025 due to robust automotive OEM and replacement demand for seat covers, door trims, and cargo interiors requiring abrasion and stain resistance. Lightweight electric-vehicle architectures intensify material substitution toward coated fabrics that combine reinforcement and aesthetics with weight savings. Simultaneously, medical textiles experience the highest 6.03% CAGR thanks to post-pandemic awareness around antimicrobial protection in hospital bedding, gowns, and barrier fabrics. Nanoparticle-enabled coatings capable of 99.999% pathogen reduction draw procurement interest from large healthcare networks, accelerating adoption.

Cross-segment technology transfer is becoming commonplace. Plasma-treated antibacterial surfaces originally developed for surgical environments now migrate into high-touch public transport interiors, merging application domains and broadening addressable volume. Construction, industrial safety, and apparel continue to contribute materially to volume, yet their growth rates trail the lead pair given mature adoption curves and slower innovation cycles.

Geography Analysis

Asia-Pacific accounted for 52.74% of global revenue in 2025, cementing its influence on price formation and supply allocation across the textile coatings market. China shipped USD 301 billion in textiles and garments in 2024, of which USD 142 billion stemmed from textiles, underscoring capacity depth even amid diversification moves toward Vietnam, India, and Bangladesh. Indian policy tools such as the Production Linked Incentive program and PM MITRA parks seek to elevate national production value to USD 350 billion by 2030, encouraging domestic formulators to embrace water-based chemistries early and embed them in new capacity. Bangladesh and Vietnam cement footholds via competitive labor costs and trade agreements, but the imposition of US tariffs on certain categories could reorder sourcing strategies and push local suppliers toward greater functional differentiation.

North America remains a technology-centric region, channeling regulatory fervor into commercial opportunities for PFAS-free, low-VOC systems. California and New York enact some of the world’s most stringent textile chemical bans effective January 2025, prompting early-mover advantage for firms already equipped to supply compliant portfolios . Lubrizol’s USD 20 million acrylic-emulsion expansion in Gastonia supports demand clusters in home textiles and technical performance fabrics for automotive interiors, reinforcing the region’s tilt toward value-added niches. Canada’s integration with US vehicle production sustains cross-border demand, though exposure to raw-material price cycles forces constant recalibration of sourcing strategies.

Europe sustains leadership in sustainable chemistry and advanced processing. German, French, and Nordic innovators push waterborne polyurethane and bio-polymer frontiers while investing in plasma and digital-application lines that dramatically cut water and energy inputs. Acquisitions such as Freudenberg’s EUR 100 million takeover of Heytex assets expand technical-textile portfolios and signal ongoing consolidation. EU circular-economy legislation accelerates interest in recyclable coatings and closed-loop infrastructures, positioning the textile coatings market as both beneficiary and enabler of regional climate objectives.

Competitive Landscape

Competition in the textile coatings market remains moderately consolidated. Regional players focus on agility and local differentiation. Technological advancements, such as atmospheric-plasma lines, digital-spray heads, and low-temperature silicone crosslinkers, enable firms to secure premium contracts with ESG-focused OEMs and PFAS-free brands. Bio-chemical start-ups developing sugar-based monomers threaten petroleum-based incumbents if cost parity is achieved. Pricing varies by region and polymer, with PVC and nitrile dominating commoditized segments, while silicone and nanocomposites offer specialty opportunities. Strategic collaborations on closed-loop recycling align with waste reduction goals. Ultimately, sustainable functionality, production efficiency, and responsive supply chains determine success in this competitive market.

Textile Coatings Industry Leaders

Covestro AG

Solvay

Archroma

Arkema

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2023: Covestro AG launched Impranil CQ DLU, a bio-based textile coating dispersion with 34% plant-derived carbon content, offering the same properties as its petroleum-based counterpart. With 55% solids content, it enables sustainable one-for-one replacement. The "CQ" label signifies at least 25% alternative raw materials, aligning with growing sustainability demands.

- February 2023: Archroma, finalized its acquisition of Huntsman Corp's textile effects business. The company restructured into two divisions: Archroma textile effects and Archroma paper, packaging, and coatings, aligning its operations to target specific end markets effectively.

Global Textile Coatings Market Report Scope

The textile coatings market report includes:

| Thermoplastics | Polyvinyl Chloride (PVC) |

| Polyurethane (PU) | |

| Acrylic | |

| Others | |

| Thermosets | |

| Rubber | Natural Rubber |

| Styrene butadiene Rubber | |

| Others | |

| Other Polymer Types |

| Woven |

| Knitted |

| Non-woven |

| Waterproof and Breathable |

| Flame-retardant |

| Anti-microbial and Anti-viral |

| UV and IR Resistant |

| Clothing |

| Transportation |

| Medical |

| Construction |

| Other Applications (Industrial and Protective Equipment, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Polymer Type | Thermoplastics | Polyvinyl Chloride (PVC) |

| Polyurethane (PU) | ||

| Acrylic | ||

| Others | ||

| Thermosets | ||

| Rubber | Natural Rubber | |

| Styrene butadiene Rubber | ||

| Others | ||

| Other Polymer Types | ||

| By Fabric Type | Woven | |

| Knitted | ||

| Non-woven | ||

| By Functionality | Waterproof and Breathable | |

| Flame-retardant | ||

| Anti-microbial and Anti-viral | ||

| UV and IR Resistant | ||

| By Application | Clothing | |

| Transportation | ||

| Medical | ||

| Construction | ||

| Other Applications (Industrial and Protective Equipment, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the textile coatings market?

The textile coatings market is valued at USD 4.73 billion in 2026 and is on track to reach USD 5.71 billion by 2031 at a 3.85% CAGR.

Which region leads the textile coatings market?

Asia-Pacific leads with 52.74% share in 2025 and is forecast to grow at 5.86% CAGR through 2031, buoyed by large-scale manufacturing and export capacity.

Which application segment is growing fastest?

Medical textiles record the highest 6.03% CAGR because hospitals and healthcare brands are prioritizing antimicrobial and antiviral functionality.

How are regulations influencing product development?

Tightening VOC and PFAS restrictions in North America and Europe accelerate adoption of waterborne and solvent-free systems, reshaping R&D pipelines worldwide.

Page last updated on: