Bleached Linter Cellulose Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.54 Billion |

| Market Size (2031) | USD 1.91 Billion |

| Growth Rate (2026 - 2031) | 4.36% CAGR |

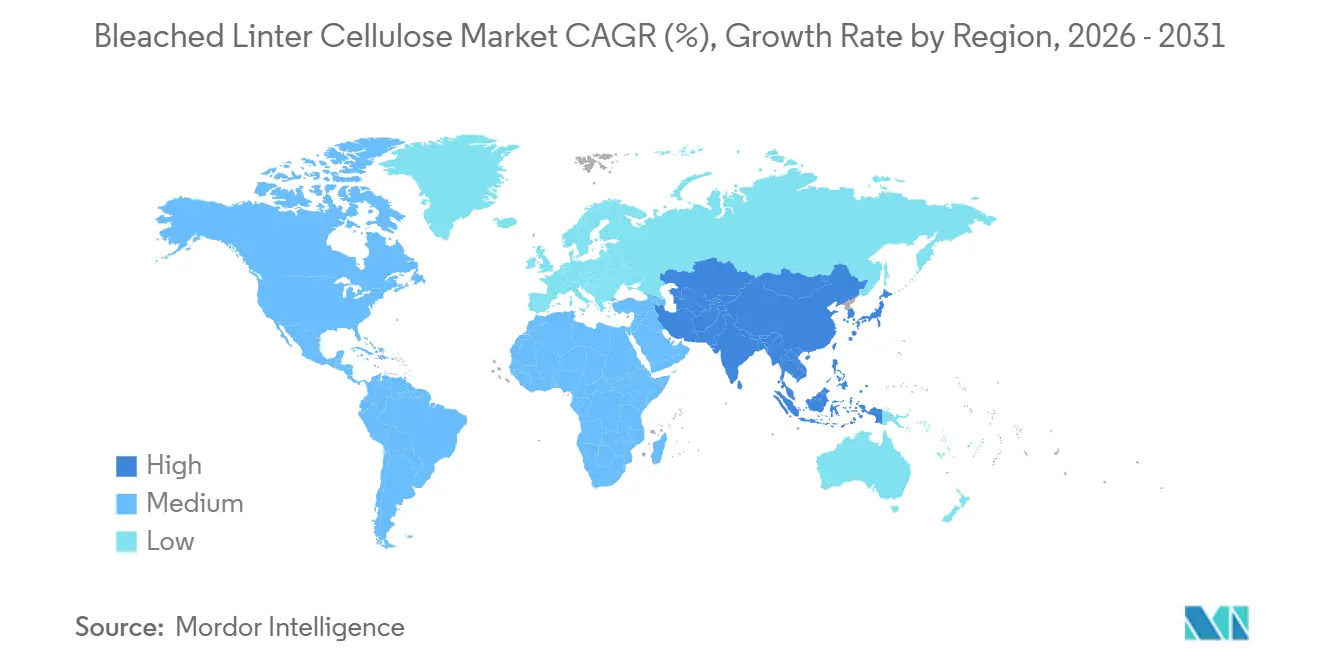

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

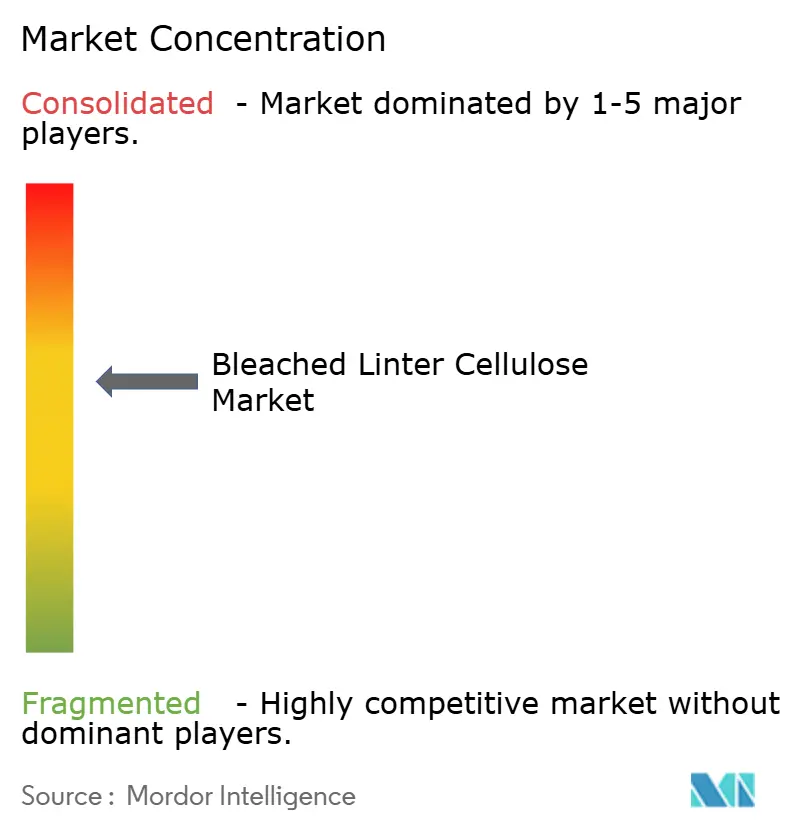

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bleached Linter Cellulose Market Analysis by Mordor Intelligence

The Bleached Linter Cellulose Market size is projected to be USD 1.48 billion in 2025, USD 1.54 billion in 2026, and reach USD 1.91 billion by 2031, growing at a CAGR of 4.36% from 2026 to 2031. In the short term, increased demand for pharma-grade microcrystalline cellulose and battery-separator films has enabled producers to achieve higher price premiums, even as commodity grades remain stagnant. Integrated viscose manufacturers are expanding linter-based capacities to address an oversupply of wood pulp and to meet stricter sulfur-recovery targets that support closed-loop bleaching sequences. On the regulatory side, the European Commission's decision to lower AOX and COD discharge ceilings has raised operational costs for mills unable to retrofit with oxygen-delignification systems. In the Asia-Pacific region, which already contributes to over two-fifths of the market's revenue, subsidy programs in China and India incentivizing bio-based packaging inputs enhance the material's appeal. However, competitive pressures persist, as low-cost eucalyptus dissolving pulp from ASEAN is reducing linter prices in the commodity viscose market, prompting Western suppliers to focus on high-certification niches.

Key Report Takeaways

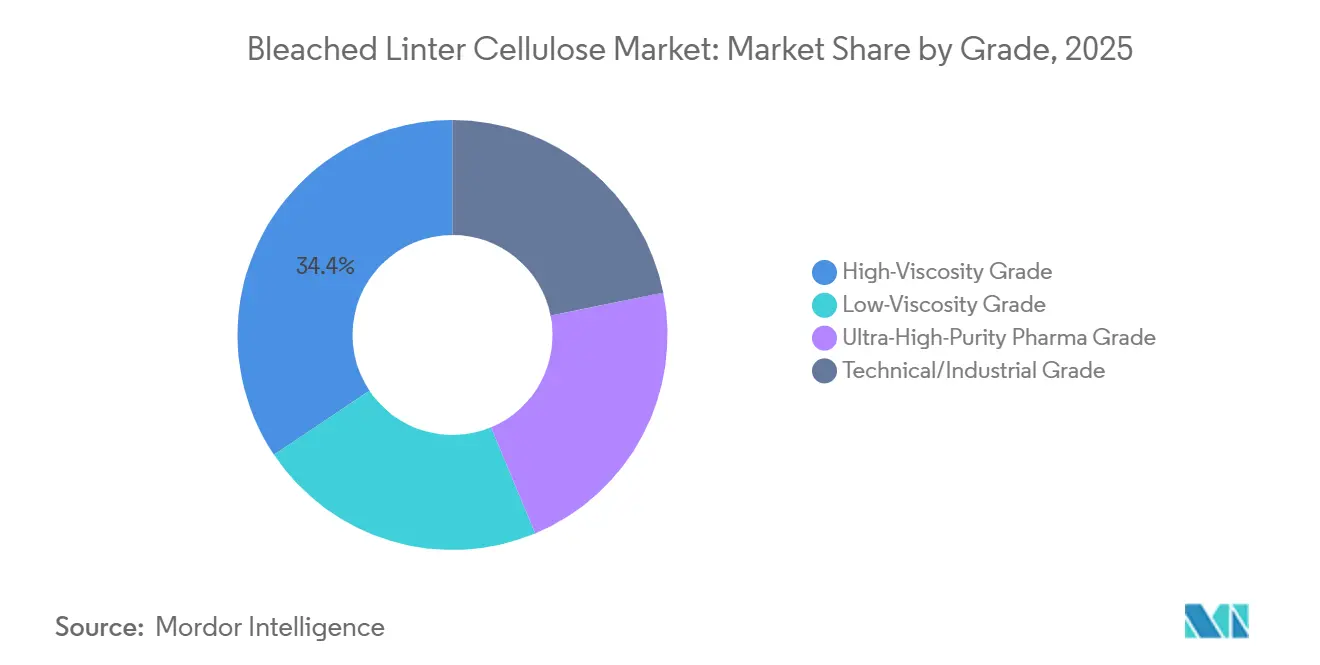

- By grade, High-Viscosity Grade led with 34.41% revenue share in 2025, while Ultra-High-Purity Pharma Grade is advancing at a 4.59% CAGR from 2026 to 2031.

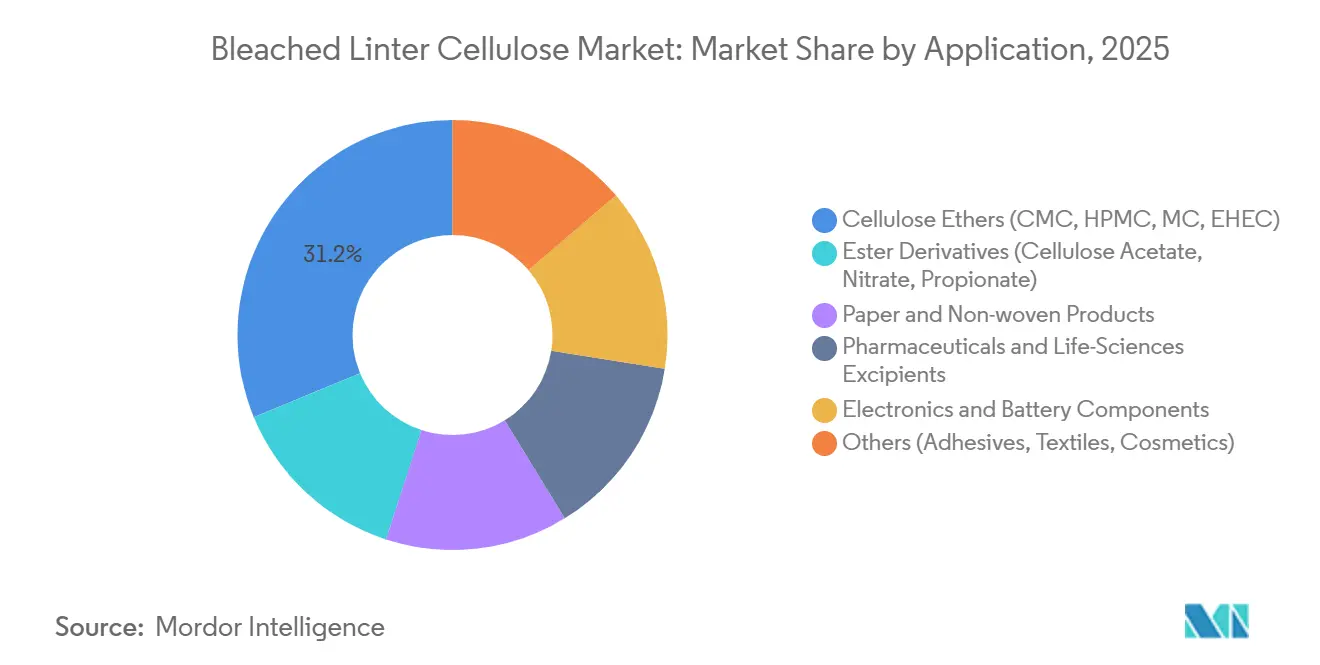

- By application, Cellulose Ethers held 31.24% of the bleached linter cellulose market share in 2025; Electronics and Battery Components exhibit the fastest 5.11% CAGR from 2026 to 2031.

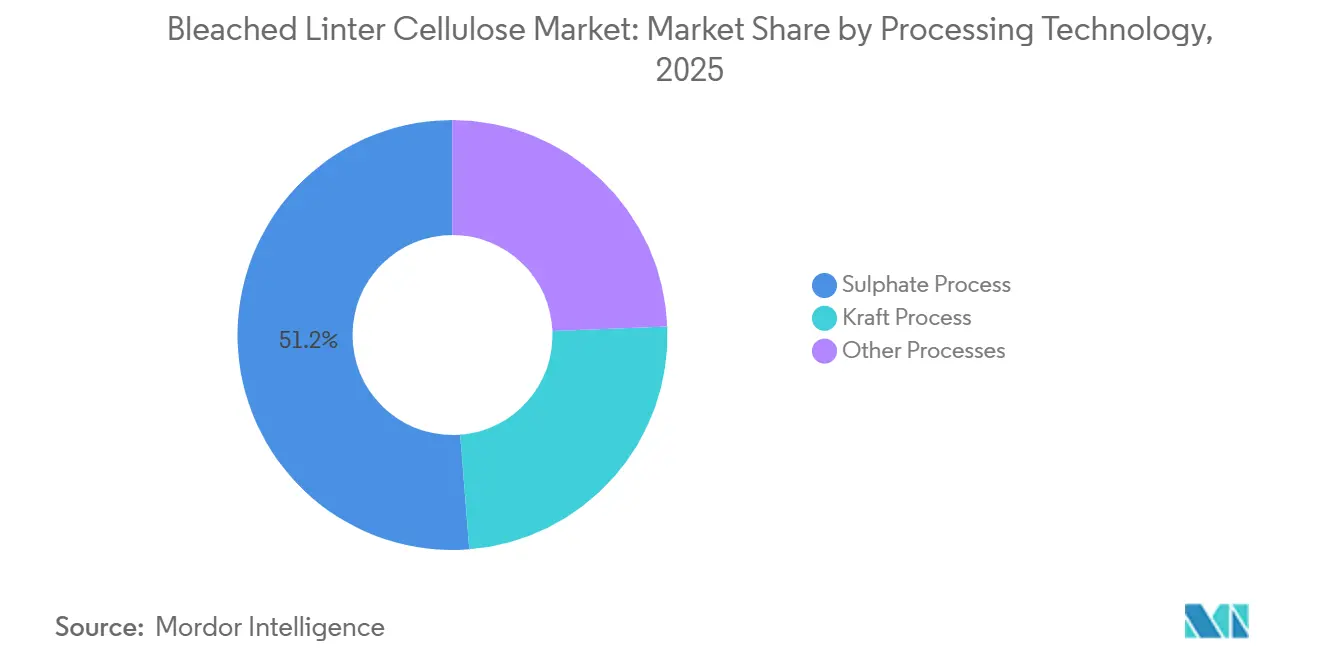

- By processing technology, the Sulphate Process captured 51.25% share of the bleached linter cellulose market size in 2025; the Kraft Process expanded at a 4.92% CAGR from 2026 to 2031.

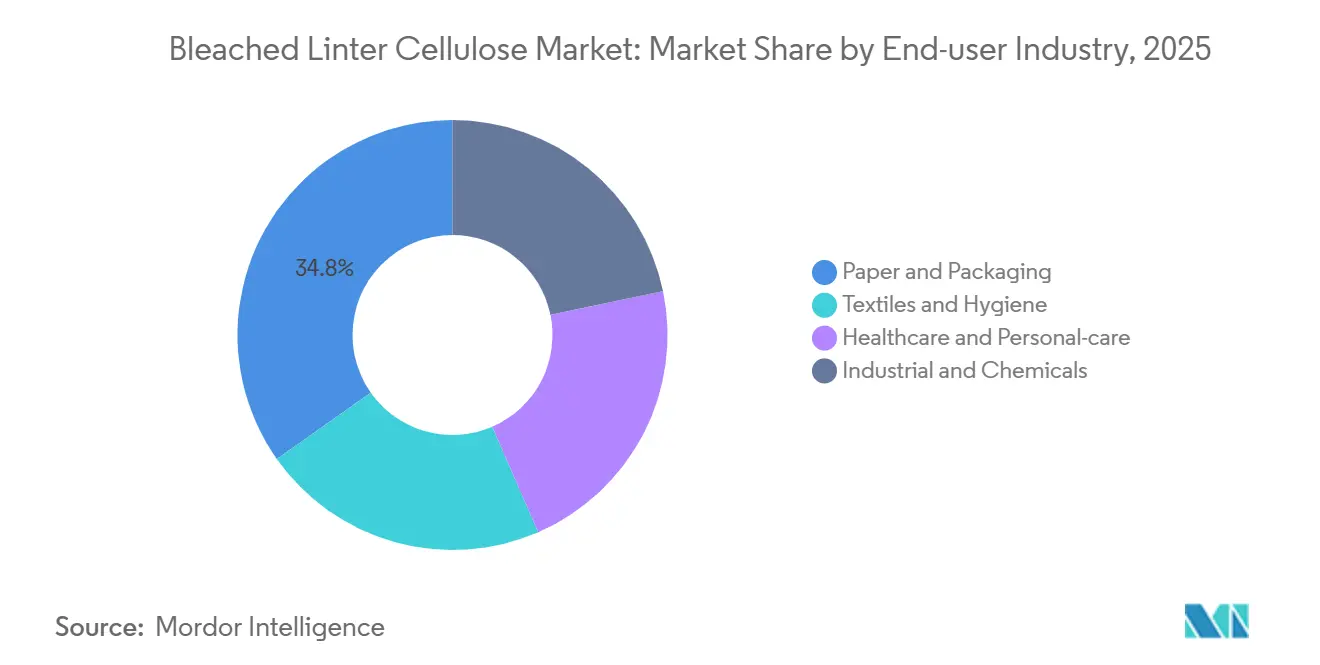

- By end-user industry, Paper and Packaging accounted for 34.78% share in 2025, whereas Healthcare and Personal-care are growing at a 4.66% CAGR from 2026 to 2031.

- By geography, Asia-Pacific commanded 41.78% of 2025 revenues and is projected to post a 4.93% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bleached Linter Cellulose Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong demand from specialty paper and non-woven producers | +0.8% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Capacity shift of viscose players toward cotton-linter pulp | +1.1% | Asia-Pacific core, spillover to Europe | Long term (≥4 years) |

| Surge in pharma-grade MCC for continuous-manufacturing tablets | +0.9% | North America & EU, emerging in India | Medium term (2-4 years) |

| Battery-separator films using linter-derived cellulose acetate | +0.7% | Asia-Pacific (China, Japan, South Korea), North America | Long term (≥4 years) |

| Tax incentives for bio-based packaging (China, India, EU) | +0.6% | China, India, EU-27 | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Strong Demand from Specialty Paper and Non-Woven Producers

Specialty papers, utilizing linter fibers of 10-15 mm length, achieve improved tensile strength and opacity compared to wood-pulp alternatives. This development enables mills to eliminate one calendering pass, resulting in energy savings of up to 18%. Non-woven fabric producers are increasingly adopting cellulose over polypropylene in hygiene products, driven by consumer preferences for biodegradable materials. This transition aligns with the projected growth of the global non-woven market, valued at USD 20.6 billion in 2025, with a growth rate of 6.7%. Georgia-Pacific's 2024 modernization in Alabama, which allows flexibility between paper-pulp bales and fluff-pulp rolls, reflects efforts by integrated mills to manage raw-material risks effectively. Alpha-cellulose content above 95% supports archival brightness and stability in medical wipes, maintaining a 15-20% price premium over wood pulp in niche paper grades. However, this premium reduces in commodity non-wovens, where cost efficiency takes precedence over performance improvements.

Capacity Shift of Viscose Players Toward Cotton-Linter Pulp

In 2025, an oversupply in China led to a 12% drop in staple-fiber prices, reducing margins for commodity viscose. In response, major producers shifted their focus to linter feedstock, which supports premium Lyocell and specialty viscose outputs. Sateri initiated a 35,000-ton line that processes post-consumer textile waste in combination with certified pulp. This move aligns with EU mandates targeting 25% recycled content by 2030. Grasim's 110,000-ton Lyocell program utilizes the purity of cotton linter, achieving solvent-recovery efficiency above 99% and eliminating sulfur emissions. Lenzing is directing investments toward compliance, aiming to use stricter EU regulations as a competitive advantage rather than focusing on volume. Meanwhile, Indonesian and Vietnamese wood-pulp dissolving lines, priced between USD 650-700 per ton, continue to attract orders for low-grade viscose. This trend has segmented the bleached linter cellulose market into certification-driven high-value niches and a price-sensitive commodity tier.

Surge in Pharma-Grade MCC for Continuous-Manufacturing Tablets

In 2024, the U.S. FDA issued guidance on continuous manufacturing, driving demand for MCC with specifications requiring moisture content below 3.5% and heavy metals under 10 ppm. Linter-derived materials are the only ones consistently meeting these criteria. Additionally, EXCiPACT certification has become a requirement for most tenders in Europe. With only twelve global suppliers holding this certification, supply constraints have contributed to maintaining premium prices. In March 2025, Daicel introduced BELLOCEA BS7, a product designed to meet the sub-30 second breakup target for orally disintegrating tablets, offering improved performance compared to traditional wood-pulp MCC. Hydrothermal treatments, such as A-ConCrystal, refine particle-size distributions to 3 µm. However, limited licensing continues to protect these advantages for incumbents until at least 2028. Emerging markets continue to adopt wood-pulp MCC to reduce costs, resulting in a two-speed global demand scenario.

Tax Incentives for Bio-Based Packaging

China, India, and the EU are offering corporate income tax rebates and accelerated depreciation to encourage investments that replace fossil-based polymers with bio-based fibers in packaging. This policy is driving regional converters to adopt cellulose ethers from linter pulp as rheology modifiers in polylactic acid blends to align with compostability standards. These measures are increasing short-term volumes while creating challenges for converters relying solely on lower-cost wood-pulp derivatives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile cottonseed prices and supply shocks | -1.2% | Global, acute in North America, China (Texas, Xinjiang) | Short term (≤2 years) |

| Tightening EU AOX and COD discharge limits | -0.7% | Europe, spillover to export-oriented mills in Asia | Medium term (2-4 years) |

| Low-cost wood-based dissolving pulp competition (ASEAN) | -0.9% | ASEAN core, competitive pressure in India, China | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile Cotton-Seed Prices and Supply Shocks

In early 2025, cottonseed prices rose by 22% year-on-year, driven by a 17% reduction in U.S. acreage as farmers shifted to higher-return crops like soybeans and corn. This change removed 120,000 tons from the potential linter supply[1]USDA, “Prospective Plantings 2025,” usda.gov. Additionally, a 9% decline in Xinjiang's output in 2024 further limited supply. By Q1 2025, Chinese spot linter prices reached CNY 8,200 per ton (approximately USD 1,150), creating challenges for processors without long-term offtake contracts. Since linter accounts for only 8-10% of the cottonseed's mass, the supply remains unresponsive to changes in linter demand, contributing to price fluctuations. Borregaard's trade petition in October 2025 highlighted perceived subsidies that provided Chinese mills with a 15-18% cost advantage, reflecting how raw-material policies influence market constraints.

Tightening EU AOX and COD Discharge Limits

In 2024, the BAT update reduced AOX limits to 0.25 kg and COD to 20 kg per air-dried ton[2]European Commission, “BAT Reference Document for Pulp Production 2024,” europa.eu . This change has required mills to implement oxygen-delignification and closed-loop bleaching, with costs that may exceed EUR 40 million per line. Sappi’s Somerset conversion, with a USD 170 million investment, achieved an AOX of 0.18 kg, but operating costs increased by 8%. Producers of EU Ecolabel tissue now require an AOX of less than 0.15 kg per ton. Non-compliance with this standard results in linter pulp being excluded from premium contracts. As a result, three small mills in Italy and Spain have ceased operations. Additionally, Asian exporters targeting the European market now need to secure ISO 14001 audits, which increase their landed costs by 4 to 6%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Pharma Purity Commands Premium Despite Volume Lag

Ultra-high-purity pharma pulp, supported by the growth of the bleached linter cellulose market, recorded a 4.59% CAGR. However, high-viscosity pulp, due to its versatile role in producing CMC, HPMC, and EHEC, accounted for 34.41% of the bleached linter cellulose market in 2025. Companies such as Grasim, Daicel, and Borregaard are focusing on EXCiPACT accreditation within this segment, which facilitates the batch genealogy required for continuous-manufacturing lines. Commodity technical grades are experiencing a 25-30% price reduction due to competition from ASEAN dissolving pulp, which is impacting margins. In contrast, specialty product launches, such as BELLOCEA BS7, demonstrate how suppliers are targeting specific applications to maintain pricing power. Additionally, certifications like ISO 9001 and ISO 14001 have become standard requirements for pharma tenders in Europe and the United States.

From an operational perspective, capacity trends are shifting. In Q4 2025, Rayonier increased specialty-cellulose prices by 18% year-on-year, citing limited EXCiPACT-certified supply, while commodity grades experienced a 6% decline. The broad applicability of high-viscosity pulp supports strong volumes, but it remains vulnerable to synthetic polymer substitution in cost-sensitive construction markets. Low-viscosity variants, associated with propellant and lacquer demand, continue to serve niche applications influenced by fluctuations in defense cycles.

By Application: Battery Components Surge as Ethers Plateau

In the bleached linter cellulose market, cellulose ethers accounted for 31.24% of the 2025 revenue and are expected to remain stable. Electronics and battery components are projected to grow at a CAGR of 5.11% through 2031. Separator films, designed for thermal shutdowns above 160 °C, highlight the safety benefits of linter-derived acetate. Ethers such as CMC and HPMC have a strong presence in the construction and food sectors, but are now facing competition from synthetic polymers. Ester derivatives are utilized in cigarette filters, defense propellants, and coatings, with each application requiring specific purity profiles. Pharmaceutical excipients, which make up 40-45% of tablet binders, are anticipated to grow annually at a moderate rate, supported by the increasing demand for orally disintegrating dosage forms among aging populations.

Nouryon’s FinnFix PB MAX, introduced in February 2026, reflects an industry shift toward 100% bio-based formulations, with certifications like ISCC Plus being used for carbon accounting. The "Others" category includes adhesives, cosmetics, and textiles. Within this category, cosmetics show potential for growth as cellulose replaces microplastic beads. The market is segmented into high-growth, low-volume niches and maturing, high-volume categories.

By Processing Technology: Kraft Gains on Emission Compliance

In the bleached linter cellulose market, the sulphate route accounted for 51.25% of the 2025 output. However, as the Kraft route is projected to grow at a 4.92% CAGR through 2031, the sulphate route is expected to lose its share. The ZDHC's aspirational target of achieving a 98% sulfur recovery is directing new investments toward Kraft systems, which are recognized for their efficient chemical recovery. Sateri's six viscose mills face a significant challenge, as each needs to invest between USD 25-30 million to retrofit recovery boilers. This investment level is difficult for smaller sulphate mills to achieve. Meanwhile, Kraft's sodium-sulphate byproduct is gaining interest among detergent manufacturers, helping to offset rising caustic-soda costs. For example, Georgia-Pacific's USD 800 million project on the Alabama River reflects a modern Kraft design, achieving a 40% reduction in particulates and a 25% cut in water usage. On a different note, while organosolv and ionic-liquid pilots are being explored, their global output remains limited to under 5,000 tons due to solvent costs exceeding USD 3,000 per ton.

EU's BAT standards are enhancing Kraft's competitive position by setting AOX thresholds that older sulphate lines find challenging to meet without oxygen-delignification. In contrast, Asian mills, which operate under more lenient regulations, are maintaining sulphate line operations at 70-80% capacity. This operational approach allows them to lead in domestic sales pricing, creating a distinct two-tier cost structure in the market.

By End-User Industry: Healthcare Outpaces Legacy Paper Demand

In 2025, the bleached linter cellulose market recorded a 34.78% share for the paper and packaging segment. However, the healthcare and personal care segments are expected to grow at a 4.66% CAGR through 2031. In North America and Europe, the demand for linter supply is increasing due to tighter specifications required for continuous-manufacturing tablet lines. Specialty papers, such as banknotes, utilize linter’s tensile strength, although overall print demand is declining as economies transition to digitization. In textiles, premium Lyocell and modal fibers are experiencing growth, while commodity viscose is losing market share to polyester. Industrial applications in construction and mining remain dependent on infrastructure spending. Nouryon is planning to expand its EHEC capacity in Southeast Asia to enhance localized supply.

The FDA's approval of MCC in orally disintegrating tablets is driving growth in healthcare volumes. At the same time, specialty packaging for food and medicine is maintaining demand for virgin fibers, countering competition from recycled alternatives. The market performance of cellulose ethers will depend on their sustainability credentials and cost, as they compete with lower-cost synthetic rheology modifiers.

Geography Analysis

In the bleached linter cellulose market, Asia-Pacific, which accounted for 41.78% of 2025 revenue, is expected to grow at a 4.93% CAGR through 2031. In China, a January 2026 notice issued by nine ministries allocates subsidies to bio-based fibers, increasing the demand for linter-derived cellulose ethers in PLA blends. Chinese viscose-staple-fiber plants operated at 78% capacity in Q1 2025, while buyers paid an 18% premium for pharma MCC to secure supply. In Japan and South Korea, the focus remains on high-value tablets and battery separators. Daicel’s BELLOCEA BS7, aimed at ODT segments, is projected to grow annually by 8-9%. In the ASEAN region, Indonesia and Vietnam are increasing the supply of commodity viscose using inexpensive eucalyptus pulp, whereas Thailand and Malaysia rely on imports of linter-based MCC for their pharmaceutical plants. In India, import dependence for ultra-high-purity grades continues, but Grasim’s 55,000-tonne Phase 1 Lyocell unit, planned for mid-2027, may address this issue.

In North America, reduced cotton acreage is limiting linter supply. Georgia-Pacific’s expansion into softwood fluff-pulp is creating competition with linter in hygiene products, reducing margins for unlabeled grades. Borregaard's trade petition reflects domestic suppliers pursuing regulatory measures to maintain pricing. In the United States, continuous-manufacturing contract producers, responsible for nearly two-thirds of tablet volume, require EXCiPACT-certified linter inputs, which strengthens their bargaining position.

In Europe, revised BAT standards resulted in the closure of three mills, reducing local supply. Germany and the Nordic regions continue to operate specialty-cellulose facilities that are integrated into tissue and pharmaceutical supply chains. The EU's Packaging and Packaging Waste Regulation, finalized in 2024, sets a target of 65% recycled content in paper packaging by 2030. This regulation reduces demand for virgin-fiber commodities but excludes food-contact and medical applications, where linter remains significant. Lenzing is investing EUR 100 million in emission compliance, with the expectation that the EU's carbon-border adjustment will improve competitiveness against Asian imports. In South America, Brazil's Bracell is competing with linter in dissolving-pulp applications, while the Middle East and Africa continue to import pharma MCC due to limited domestic cotton production.

Competitive Landscape

The bleached linter cellulose market is moderately consolidated in nature. The top five players, Sateri Holdings Ltd, Daicel Corporation, Rayonier Advanced Materials, Lenzing AG, and Borregaard ASA, collectively account for approximately 45-50% of the specialty-cellulose output. In comparison, over 20 regional mills compete in the commodity pulp segment. Western suppliers maintain their market position through certifications such as EXCiPACT, PEFC, and the EU Ecolabel. On the other hand, Asian companies are focusing on vertical integration, covering processes from cotton ginning to viscose spinning, to achieve economies of scale. Borregaard's petition in October 2025 and Rayonier's 18% increase in specialty-cellulose prices illustrate how regulation and contracting help sustain premium pricing. Grasim's investment in Lyocell production and Sateri's development of a recycled-viscose line reflect a strategic focus on differentiated grades rather than increasing volume output.

Technological innovation is becoming a critical factor in competition. Daicel's A-ConCrystal technology optimizes MCC particle size to 3 µm, catering to continuous-manufacturing lines. Nouryon's solvent-free EHEC and ISCC-Plus certified CMC enhance sustainability credentials in consumer chemicals. Georgia-Pacific's upgrade at its Alabama facility incorporates high-efficiency recovery boilers, reducing particulate emissions by 40% and water usage by 25%. This development increases competitive pressure on mills that are behind in meeting emission standards. ZDHC's sulfur-recovery targets serve as a trade barrier, with retrofitting costs estimated at USD 25-30 million per line, driving consolidation among financially robust players. Opportunities exist in battery separators and EXCiPACT-certified pharma MCC segments, which offer premium spreads but face constraints due to limited qualified capacity.

Bleached Linter Cellulose Industry Leaders

Lenzing AG

Borregaard AS

RYAM

Sateri Holdings Ltd

Daicel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sateri launched commercial-scale viscose fiber produced from recycled post-consumer textile waste on a 35,000-tonne-per-annum production line, using dissolving pulp from Swedish cooperative Södra blended with certified cellulose pulp, marking a strategic move toward circularity in viscose production

- October 2025: Borregaard ASA filed a U.S. trade petition alleging that Chinese specialty-cellulose producers receive subsidized cotton-linter feedstock through state-owned reserves, creating a 15-18% cost advantage and requesting tariff remedies to restore competitive parity for Western mills

Global Bleached Linter Cellulose Market Report Scope

Bleached linter cellulose (BLC) is a high-purity cellulose product derived from the short, fluffy fibers left on cottonseeds after ginning. It is chemically treated to remove impurities, creating a bright white, highly absorbent pulp used in specialty paper, textiles, and chemical derivatives

The market is segmented by grade, application, processing technology, end-user industry, and geography. By grade, the market is segmented into high-viscosity grade, low-viscosity grade, ultra-high-purity pharma grade, and technical/industrial grade. By application, the market is segmented into cellulose ethers (including CMC, HPMC, MC, and EHEC), ester derivatives (including cellulose acetate, nitrate, and propionate), paper and non-woven products, pharmaceuticals and life-sciences excipients, electronics and battery components, and other applications (including adhesives, textiles, and cosmetics). By processing technology, the market is segmented into the sulphate process, the kraft process, and other processes. By end-user industry, the market is segmented into paper and packaging, textiles and hygiene, healthcare and personal care, and industrial and chemicals. The report also covers the market size and forecasts for Bleached Linter Cellulose in 17 countries across the world. For each segemnt market sizing and forecasts are provided in terms of value (USD).

| High-Viscosity Grade |

| Low-Viscosity Grade |

| Ultra-High-Purity Pharma Grade |

| Technical/Industrial Grade |

| Cellulose Ethers (CMC, HPMC, MC, EHEC) |

| Ester Derivatives (Cellulose Acetate, Nitrate, Propionate) |

| Paper and Non-woven Products |

| Pharmaceuticals and Life-Sciences Excipients |

| Electronics and Battery Components |

| Others (Adhesives, Textiles, Cosmetics) |

| Sulphate Process |

| Kraft Process |

| Other Processes |

| Paper and Packaging |

| Textiles and Hygiene |

| Healthcare and Personal-care |

| Industrial and Chemicals |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | High-Viscosity Grade | |

| Low-Viscosity Grade | ||

| Ultra-High-Purity Pharma Grade | ||

| Technical/Industrial Grade | ||

| By Application | Cellulose Ethers (CMC, HPMC, MC, EHEC) | |

| Ester Derivatives (Cellulose Acetate, Nitrate, Propionate) | ||

| Paper and Non-woven Products | ||

| Pharmaceuticals and Life-Sciences Excipients | ||

| Electronics and Battery Components | ||

| Others (Adhesives, Textiles, Cosmetics) | ||

| By Processing Technology | Sulphate Process | |

| Kraft Process | ||

| Other Processes | ||

| By End-User Industry | Paper and Packaging | |

| Textiles and Hygiene | ||

| Healthcare and Personal-care | ||

| Industrial and Chemicals | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

Which regions lead demand for bleached linter cellulose?

Asia-Pacific holds 41.78 % of revenue and is set to expand at 4.93 % CAGR to 2031, driven by Chinese and Indian bio-based packaging incentives.

What grades are growing fastest?

Ultra-high-purity pharma pulp shows the strongest 4.59 % CAGR as continuous-manufacturing tablet lines require narrow particle-size MCC.

How is technology shaping production economics?

Kraft processing is gaining share because its higher sulfur-recovery rate meets ZDHC and EU BAT limits, offsetting costs with sodium-sulfate byproduct sales.

Why is battery-separator demand important?

Cellulose-acetate separators deliver thermal shutdown above 160 °C, commanding premiums that support a 5.11 % CAGR in electronics and battery components.

What is the main supply-side risk?

Cottonseed price swings, amplified by droughts in Texas and Xinjiang, can cut linter availability and depress margins for non-integrated processors.

What is the current market size of bleached linter cellulose market?

The Bleached Linter Cellulose Market size is projected to be USD 1.48 billion in 2025, USD 1.54 billion in 2026, and reach USD 1.91 billion by 2031, growing at a CAGR of 4.36% from 2026 to 2031.

Page last updated on: