Nylon 6 Filament Yarn Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 25.88 Billion |

| Market Size (2031) | USD 35.03 Billion |

| Growth Rate (2026 - 2031) | 6.24% CAGR |

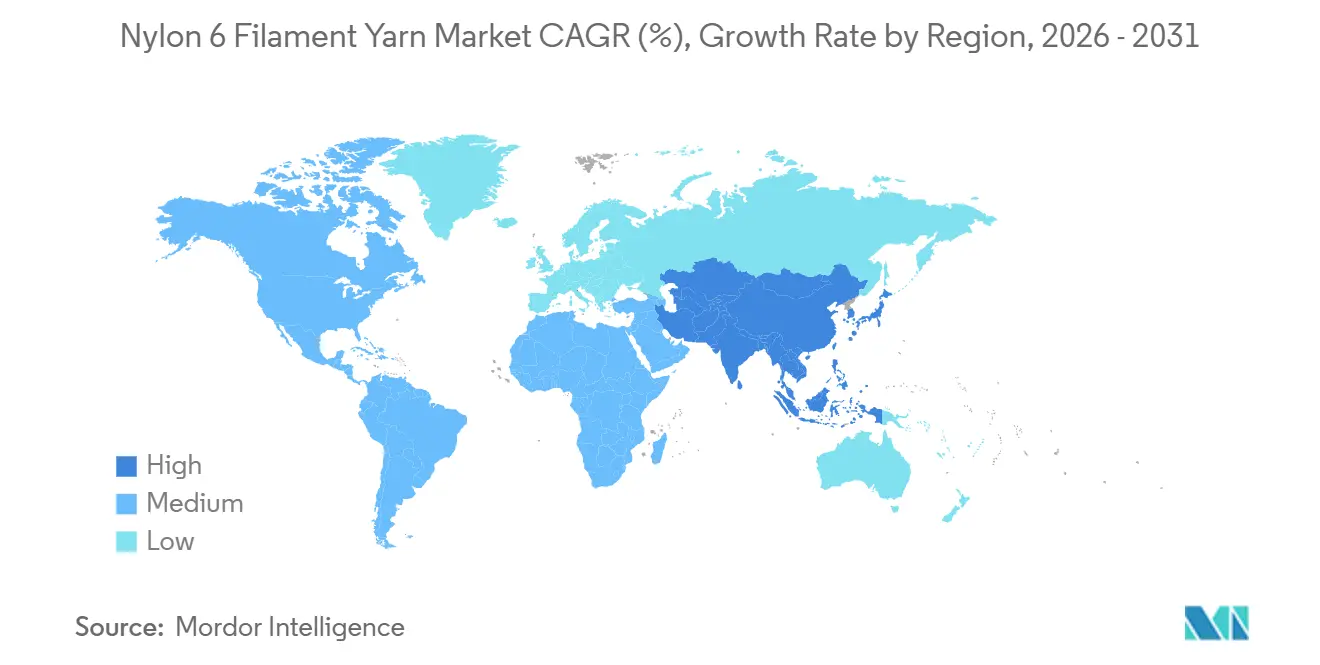

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

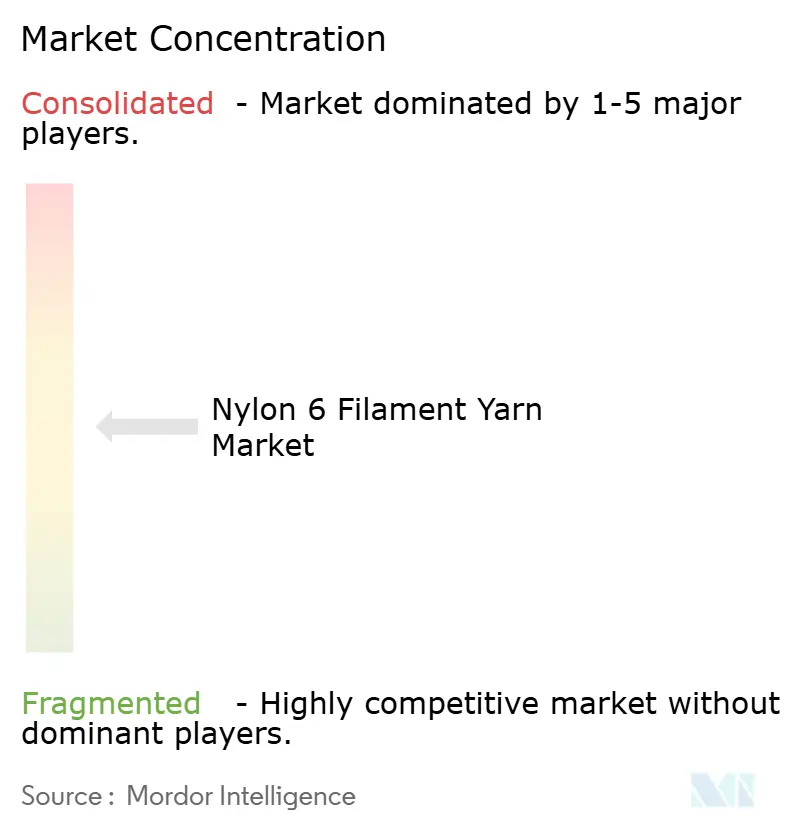

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nylon 6 Filament Yarn Market Analysis by Mordor Intelligence

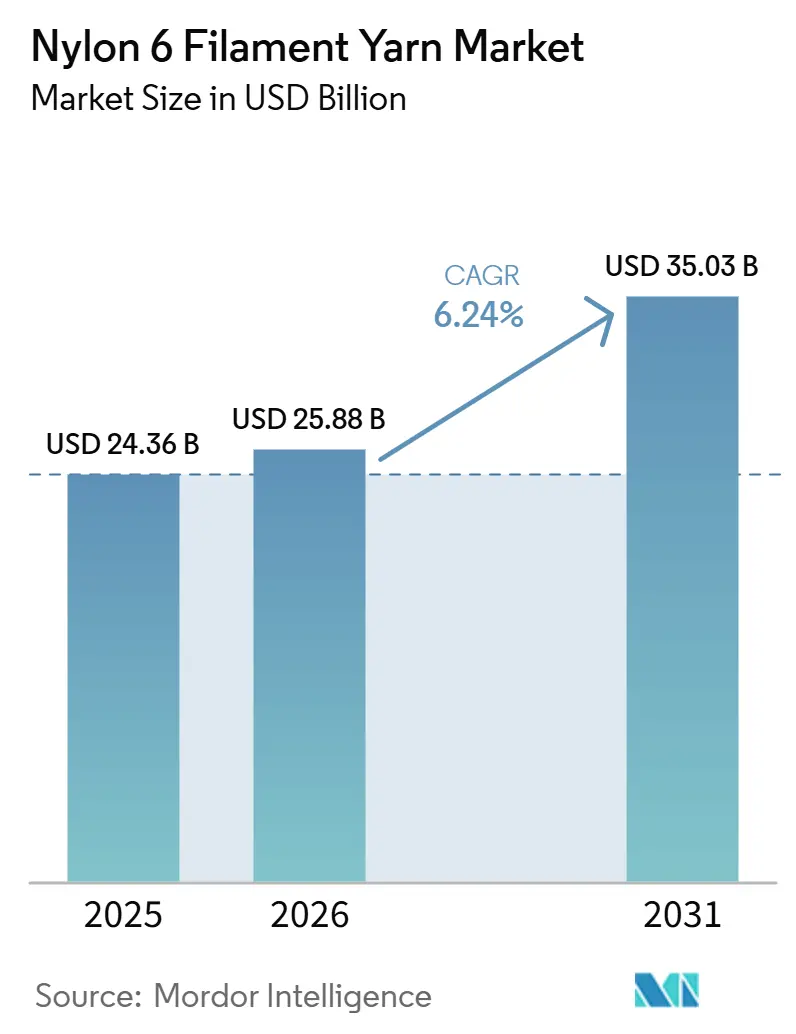

The Nylon 6 Filament Yarn Market size was valued at USD 24.36 billion in 2025 and is estimated to grow from USD 25.88 billion in 2026 to reach USD 35.03 billion by 2031, at a CAGR of 6.24% during the forecast period (2026-2031). Accelerating demand for high-tenacity, dye-receptive grades across airbags, filtration, and premium outdoor fabrics is shifting volume away from commodity textiles toward higher-margin technical segments. Asia-Pacific leads global consumption, supported by integrated caprolactam-to-filament complexes in China and fast-growing tire-cord clusters in Vietnam, while Europe pivots to low-carbon, chemically recycled variants to comply with CBAM tariffs. Digital procurement platforms are compressing distributor margins and enabling just-in-time inventory for small converters, and vertically integrated producers preserve profitability by internalizing caprolactam cost volatility. Despite these tailwinds, substitution by lower-cost polyester, carbon-pricing in energy-intensive polymerization, and limited depolymerization capacity for chemical recycling remain structural headwinds.

Key Report Takeaways

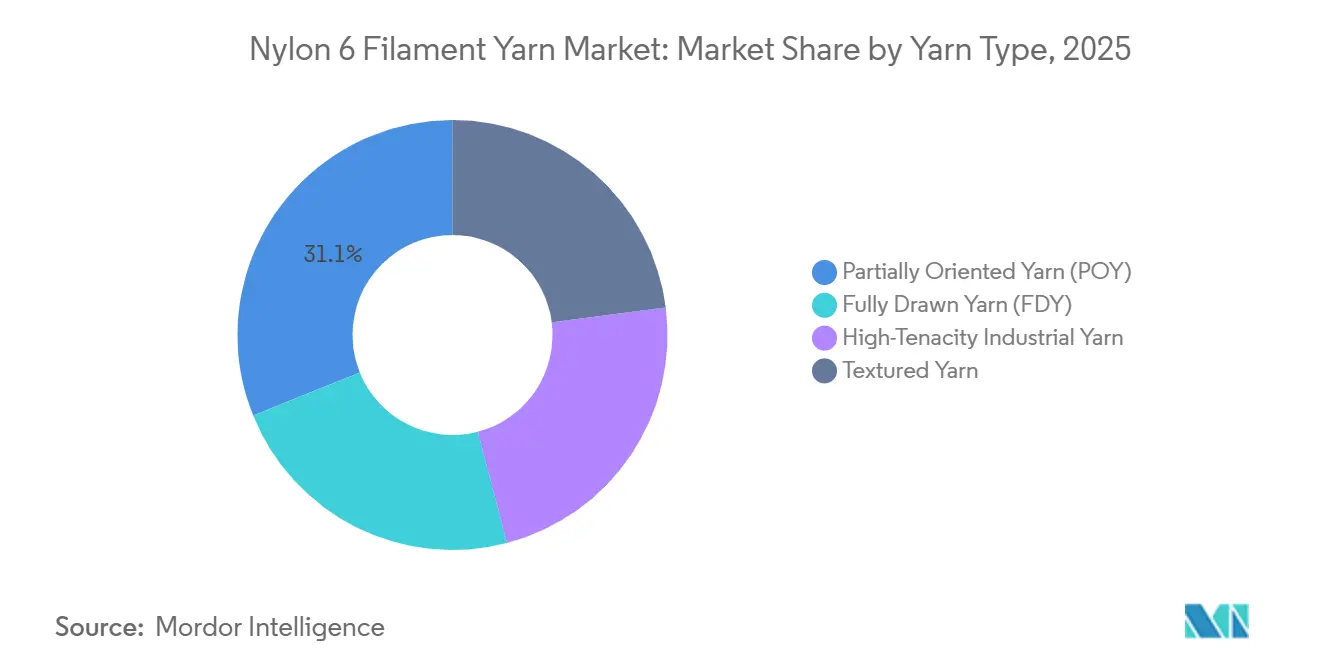

- By yarn type, Partially Oriented Yarn held 31.11% of the Nylon 6 Filament Yarn market share in 2025 and is forecast to expand at a 6.31% CAGR from 2026 to 2031.

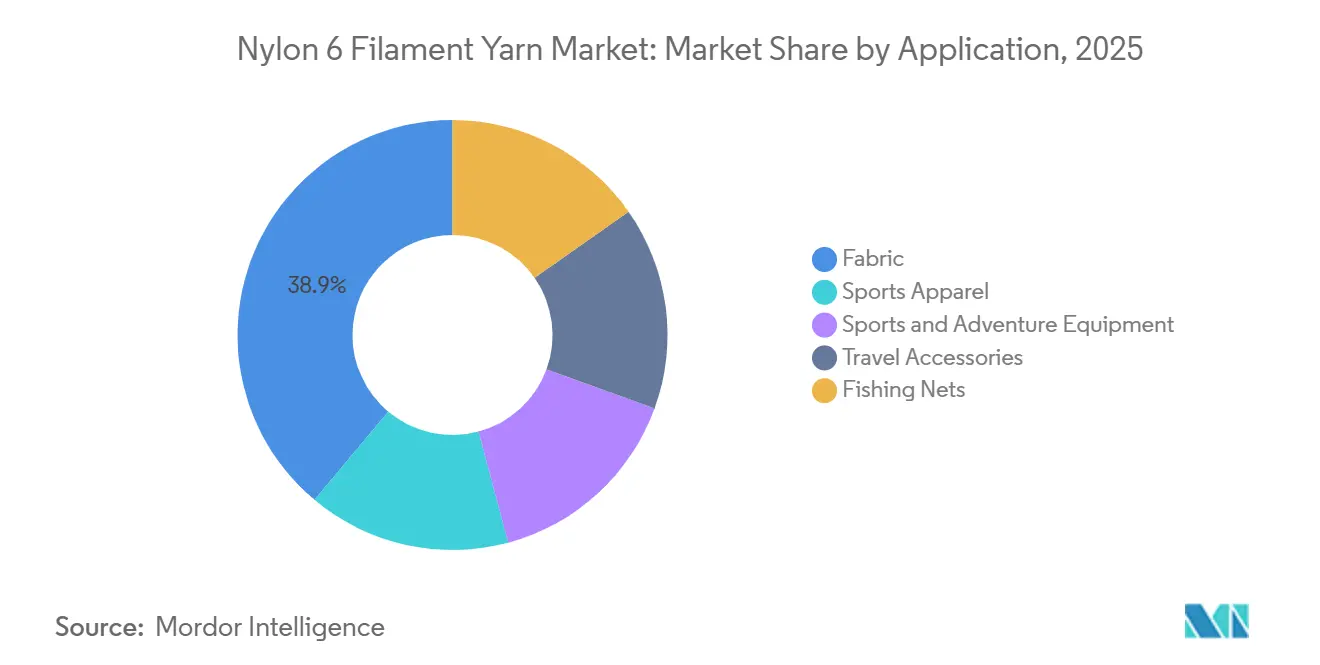

- By application, Fabric led with 38.89% revenue share in 2025, whereas Sports and Adventure Equipment is poised for the fastest growth at a 6.45% CAGR from 2026 to 2031.

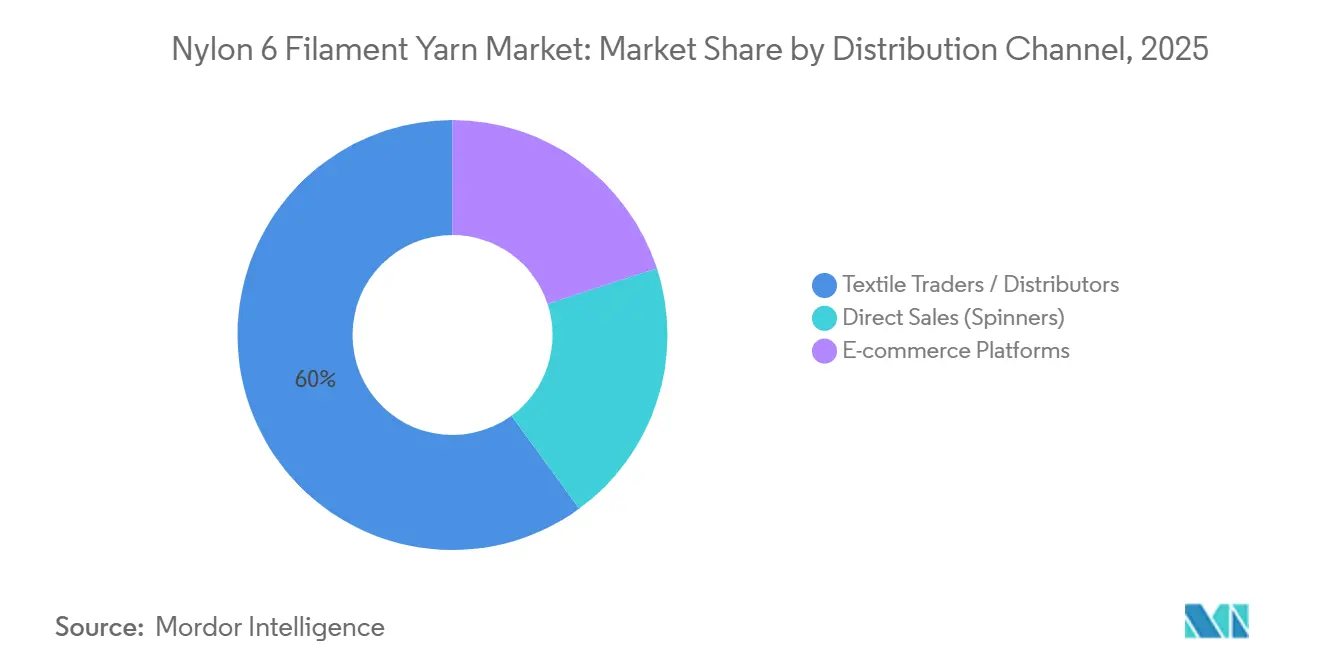

- By distribution channel, Textile Traders/Distributors controlled 60.04% of current volume in 2025, while E-commerce Platforms are projected to grow the quickest at 6.89% CAGR from 2026 to 2031.

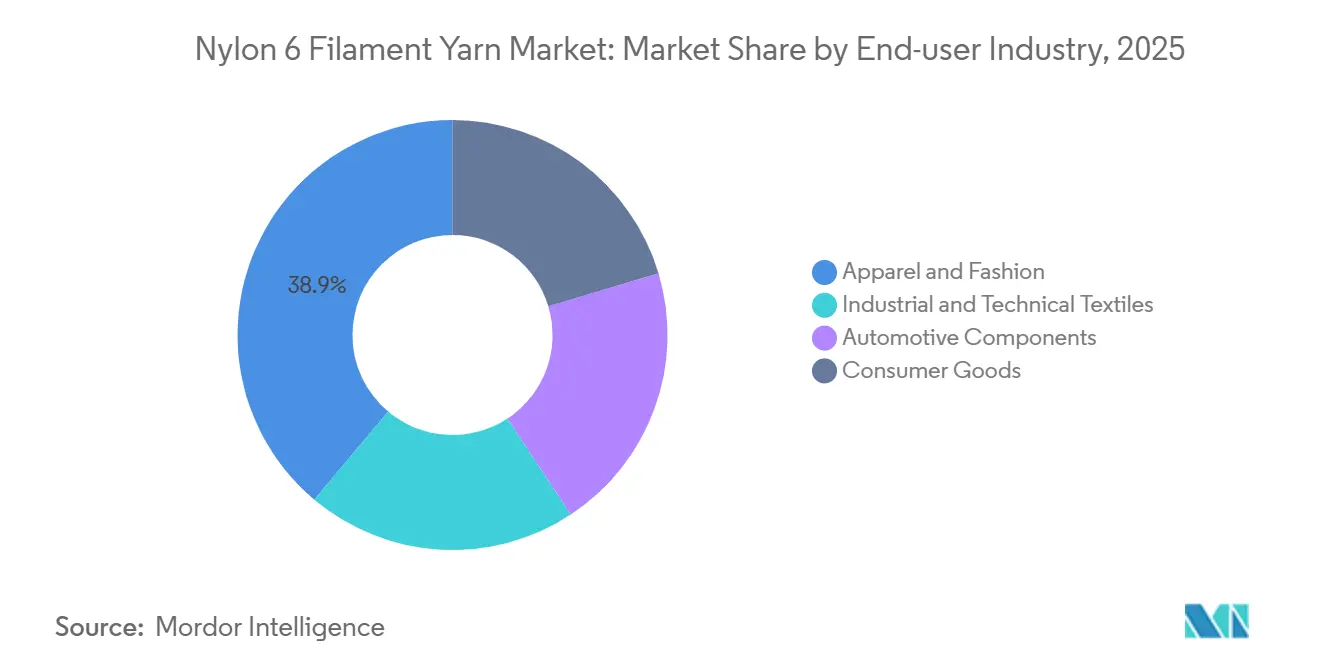

- By end-user industry, Apparel and Fashion accounted for 38.89% share of the Nylon 6 Filament Yarn market size in 2025, and Consumer Goods is expected to advance at a 6.91% CAGR from 2026 to 2031.

- By geography, Asia-Pacific captured 51.12% of global revenue in 2025 and is anticipated to register the highest regional CAGR of 6.36% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Nylon 6 Filament Yarn Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of technical textiles (safety, filtration, airbags) | +1.8% | Global, with concentration in North America, Europe, and China automotive hubs | Medium term (2-4 years) |

| Rapid growth in Asian urban bike-sharing and e-scooter bags | +0.9% | Asia-Pacific (China, India, Southeast Asia) | Short term (≤ 2 years) |

| Fishing and aquaculture net modernization programs | +0.7% | Global, with priority in Europe, Japan, and coastal developing markets | Medium term (2-4 years) |

| Low-denier micro-filament adoption in premium outdoor gear | +1.1% | North America, Europe, Japan | Long term (≥ 4 years) |

| Corporate circularity targets driving recycled Nylon 6 procurement | +1.5% | Global, led by North America and Europe brand commitments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Technical Textiles

Automakers are choosing high-tenacity Nylon 6 filaments over Nylon 6,6 in certain airbag fabrics. This decision is driven by the need to balance slightly lower strength with faster polymerization cycles and reduced material costs. In Thailand, Toyobo and Indorama's facility, producing 11,000 tons per year of airbag yarn, is reducing lead times for OEMs across Southeast Asia. AdvanSix's resins, with low melt viscosity, are reducing injection-molding cycles by up to 40% for under-hood components, aligning with the lightweighting requirements of electric vehicles. Nylon 6 monofilament, valued for its abrasion resistance, is being specified for industrial filtration media during repeated back-wash cycles, meeting ISO 11057 standards. Additionally, updates from OSHA 1926 now recommend UV-stabilized Nylon 6 for safety netting[1] OSHA, “Fall Protection in Construction,” osha.gov. Growth is focused around automotive hubs in the U.S., Germany, and China, where proximity to engineering centers supports specification-driven adoption.

Rapid Growth in Asian Urban Bike-Sharing and E-Scooter Bags

Across China, India, and Southeast Asia, municipal micro-mobility programs are increasingly adopting lightweight 210-420 denier fabrics. These fabrics, which can withstand over 500 wash cycles, are primarily using solution-dyed Nylon 6 filament. Operators such as Meituan and Hello are driving demand for UV-resistant grades to ensure compatibility with digital printing for branding purposes. In response, converters in China's Yangtze River Delta have set up dedicated weaving lines. In India, the Bureau of Indian Standards IS 15061 is encouraging the use of flame-retardant blends, particularly for battery enclosures[2]Bureau of Indian Standards, “IS 15061 Flame-Retardant Requirements,” bis.gov.in . Furthermore, supply contracts, typically lasting 12-18 months, are enabling mid-denier POY producers to maintain a steady off-take.

Fishing and Aquaculture Net Modernization Programs

Norway's 2025 rule requiring traceable and take-back-eligible nets is driving the adoption of ECONYL regenerated nylon 6. Aquafil stated that ECONYL contributed 54% of its 2024 revenue, with a target of 60% in 2025, supported by subsidies from the EU Maritime and Fisheries Fund. In Japan, a JPY 12 billion grant scheme is funding the production of high-strength, low-diameter nets with a tenacity exceeding 8.5 g/denier. Additionally, programs in Chile and Vietnam are collecting end-of-life gear for depolymerization, which is helping to stabilize the supply of recycled caprolactam.

Low-Denier Micro-Filament Adoption in Premium Outdoor Gear

Mountain Hardwear used high-speed drawing technology to reduce the weight of its tents by 35% through the adoption of a 7-denier face fabric, while ensuring that tear strength was not compromised. Patagonia, with the objective of achieving 92% recycled nylon in its Spring 2025 product line, made pre-purchases of recycled and bio-based filament, even agreeing to pay a 30-50% premium. The performance standards established by ASTM D5034 and ISO 105-B02 have limited the applicability of commodity POY, thereby increasing the demand for fully drawn and UV-stabilized yarns. In the case of sub-10 denier filament, commercial yields continue to remain below 75%, which sustains price premiums and restricts adoption primarily to high-end brands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-competitive polyester and polypropylene substitutions | -1.2% | Global, with acute pressure in South Asia and Latin America commodity textile markets | Short term (≤ 2 years) |

| Carbon-pricing and decarbonization CAPEX for high-temperature polymerization | -0.9% | Europe, North America, and regions subject to CBAM import tariffs | Medium term (2-4 years) |

| Equipment bottlenecks for chemical recycling feedstock | -0.6% | Global, with infrastructure gaps most severe in Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-Competitive Polyester and Polypropylene Substitutions

Polyester, which now matches Nylon 6 in moisture-wicking capabilities, achieves this at a cost that is 15 to 20 percent lower. This cost difference is creating challenges for Nylon in retaining its share within the mid-tier activewear market. In India, a year-on-year decline of 18 percent in Nylon monofilament imports in 2024 indicates increasing competition from Polypropylene. Due to its lower density, Polypropylene is gradually replacing Nylon 6 in applications such as geotextiles and brush bristles. Additionally, while recycled polyester has achieved cost parity with its non-recycled counterpart, the higher cost of recycled Nylon 6, which is 30 to 50 percent more expensive, acts as a significant restraint. This price disparity is limiting its adoption primarily to premium market segments.

Carbon-Pricing and Decarbonization CAPEX

Since 2024, the EU's cap-and-trade system (EU ETS) and the Carbon Border Adjustment Mechanism (CBAM) have increased caprolactam prices by USD 160-215 per ton. This price rise has contributed to plant closures by companies such as DOMO and BASF. Furthermore, retrofitting for N2O abatement has introduced significant costs, requiring an investment of USD 15-25 million for every 100 kilotons production line. This has resulted in an increase in operational expenses by 3-5%. At the same time, Chinese suppliers, including Hengyi, have begun exporting low-carbon caprolactam produced in renewable-powered complexes. These exports are priced competitively, creating challenges for the remaining European capacity, even after adjustments under CBAM are considered.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Yarn Type: POY Retains Volume Leadership

Partially oriented yarn accounted for 31.11% of the Nylon 6 filament yarn market in 2025, benefiting from flexibility in downstream texturing. The segment is expected to rise at a 6.31% CAGR as hosiery and stretch fabrics demand controlled bulk and crimp. Fully drawn yarn is gaining traction in integrated Chinese mills feeding air-jet looms, trimming energy use 12-18% versus POY-texturing routes. High-tenacity grades serve tire cord and airbag fabrics where greater than 8.5 g/denier strength is mandatory.

Chinese producers are allocating fresh capacity toward FDY and high-tenacity lines to capture rising technical-textile demand, while Taiwanese mills specialize in sub-10 denier micro-filament for premium outdoor brands. Automation and Industry 4.0 controls now allow real-time monitoring of draw ratio and shrinkage, reducing off-grade waste by 5-7%. However, the Nylon 6 filament yarn market size for POY still dwarfs other yarns, reflecting the entrenched infrastructure of independent texturizers across Asia.

By Application: Sports and Adventure Equipment Accelerates

In 2025, fabric applications accounted for 38.89% of the market share. However, their growth has been limited due to the increasing substitution of polyester. The sports and adventure equipment segment is anticipated to grow at a compound annual growth rate (CAGR) of 6.45%. This growth is attributed to the abrasion resistance of nylon, which justifies a price premium of 25-40% over polyester in applications such as ultralight tents, backpacks, and harnesses. The fishing nets segment, which operates within a regulated niche, is progressively specifying recycled content to comply with sustainability mandates established by the European Union and Japan.

The demand for 7-15 denier fabrics, commissioned by premium brands, is increasing as these fabrics meet the ASTM D5034 ≥40 N tear strength standard. This trend is driving the need for fully drawn and UV-stabilized yarns. In parallel, the travel accessories segment is adopting solution-dyed 420-840 denier filaments. These filaments enable mass-customized digital prints and reduce lead times by 30-40%. The market size for Nylon 6 filament yarn associated with sports and adventure gear remains relatively small but is experiencing growth. Additionally, this segment offers higher margins compared to commodity fabrics.

By Distribution Channel: E-Commerce Gains Momentum

In 2025, traditional textile traders commanded a dominant 60.04% of the market share, leveraging strategies like offering 8-12 week credit and logistics aggregation. Meanwhile, marketplace platforms, YarnLIVE being a notable example, are witnessing a robust growth at a 6.89% CAGR. These platforms are not only posting live caprolactam-indexed prices but are also integrating third-party freight services. This has enabled medium-sized converters in India and Southeast Asia to optimize their operations, effectively shortening their working-capital cycles and transferring inventory risks back to spinners.

Large converters, on the other hand, opt for direct purchasing through multi-year contracts. While this approach stabilizes their volume, it comes at the cost of reduced flexibility. Integrated suppliers, by leveraging digital channels to capture distributor margins, can boost their EBITDA by 1-2 percentage points, even after accounting for platform fees. The Nylon 6 filament yarn market thus showcases a two-pronged approach: major mills engage in relationship-driven bulk deals, while smaller knitters and weavers lean towards algorithmic spot buying.

By End-User Industry: Consumer Goods Lead CAGR

In 2025, apparel and fashion accounted for 38.89% of demand, but growth trends are diverging. While fast fashion is pivoting towards recycled polyester, premium activewear is opting for traceable Nylon 6. The consumer goods sector, encompassing 3D-printed components, electronics housings, and home textiles, is set to lead with a robust 6.91% CAGR. This is largely due to Nylon 6's 220 °C melt point, which facilitates quicker injection cycles and energy efficiency. Meanwhile, industrial textiles are expanding in tandem with vehicle production, bolstered by the establishment of new airbag yarn facilities in Thailand.

Automotive OEMs are increasingly turning to AdvanSix’s low-viscosity resins for battery-enclosure components, signaling a broader industry shift towards engineering plastics. Furthermore, regulations in North America and Europe that advocate for design-for-disassembly are giving Nylon 6 an edge over more challenging-to-recycle blends. This trend is poised to boost the market share of Nylon 6 filament yarn in durable goods, with projections extending through 2031.

Geography Analysis

In 2025, Asia-Pacific accounted for 51.12% of the global volume and is projected to grow at a compound annual growth rate (CAGR) of 6.36%. China's integrated hubs in Jiangsu and Zhejiang offer conversion costs that are 15-20% lower compared to other regions. Additionally, Vietnam and Thailand are emerging as key destinations for Chinese firms seeking tariff-free access to Western tire markets. In India, efforts are underway to upgrade the Surat and Tirupur spinning clusters; however, the country continues to rely on imports to meet its demand for specialty yarns.

North America faces challenges due to a caprolactam deficit, which arose after the closures of BASF and Fibrant facilities. This has increased the region's dependence on imports. Domestic production of high-tenacity yarns, which are essential for airbags and defense applications, remains stable due to International Traffic in Arms Regulations (ITAR) restrictions. However, the sourcing of fashion-grade filaments is shifting toward Asia, facilitated by Canadian and Mexican converters operating under the United States-Mexico-Canada Agreement (USMCA) rules. In Europe, the market is divided between premium circular yarns, such as Aquafil's ECONYL, and a declining commodity production segment that is burdened by Emissions Trading System (ETS) costs. Furthermore, Turkey's safeguard duties are influencing the redirection of Asian exports.

In South America, the market is experiencing modest growth, primarily driven by Brazil's automotive sector and an increasing demand for activewear. However, the region remains dependent on Asian suppliers for specialty filaments. In the Middle East and Africa, early-stage projects in Saudi Arabia are leveraging the availability of low-cost gas feedstocks. Despite this advantage, the region faces obstacles such as a shortage of skilled labor and inefficiencies in the supply chain, which are limiting the scalability of these projects. Consequently, the Nylon 6 filament yarn market continues to be concentrated in Asia, while Europe and North America focus on developing niches that emphasize sustainability and traceability.

Competitive Landscape

The Nylon 6 filament yarn market exhibits a moderate level of consolidation. Key players in the market include Toray Industries Inc., Nan Ya Plastics Corp., Yiwu Huading Nylon, JCT Ltd., and Indorama Ventures PCL. Indorama Ventures and Toray utilize backward-integrated caprolactam to safeguard their margins against fluctuations in feedstock prices. A shift towards low-carbon production is becoming a significant competitive factor. For instance, Hengyi exports renewable-powered caprolactam that complies with CBAM regulations, while Aquafil has expanded its depolymerization capabilities to produce ECONYL yarn. This yarn is offered at a 10 to 15 percent premium, with consistent availability maintained.

Technological advancements are influencing the competitive landscape across different regions. Mills in Japan and Taiwan have developed high-speed drawing lines capable of producing sub-10 denier micro-filaments with yields exceeding 80 percent. This level of technological capability has not yet been widely achieved by manufacturers in China. Additionally, the rise of digital marketplaces is transforming traditional distributor relationships. These platforms are pushing spinners to adopt transparent pricing models and real-time logistics solutions. Smaller, non-integrated companies in various regions are responding to cost pressures by focusing on specialized niches such as solution-dyed, recycled, or low-denier products. Some are exiting the market entirely due to these challenges. Strategic partnerships are also shaping the market. For example, Patagonia has partnered with Aquafil to secure recycled material supplies. These collaborations highlight the increasing importance of brand offtake commitments in securing funding for next-generation feedstock production facilities.

Nylon 6 Filament Yarn Industry Leaders

Toray Industries Inc.

JCT Ltd.

Yiwu Huading Nylon Co., Ltd

NAN YA PLASTICS CORPORATION

Indorama Ventures Public Company Limited.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Norway enforced traceability and take-back mandates for all new commercial fishing nets, favoring regenerated Nylon 6.

- December 2024: Huading Nylon announced a 200 kt PA6 filament project with renewable power and N2O abatement for CBAM-ready exports.

Global Nylon 6 Filament Yarn Market Report Scope

Nylon 6 filament yarn is a strong, synthetic, continuous fiber produced by melt-spinning polyamide 6, which is derived from caprolactam. It is characterized by high tensile strength, excellent dyeability, high elasticity, and abrasion resistance. Used widely in textiles and industry, it differs from spun yarn by consisting of long, smooth, continuous strands.

The market is segmented by yarn type, application, distribution channel, and end-user industry. By yarn type, the market is segmented into partially oriented yarn (POY), fully drawn yarn (FDY), high-tenacity industrial yarn, and textured yarn. By application, the market is segmented into fabric, sports apparel, sports and adventure equipment, travel accessories, and fishing nets. By distribution channel, the market is segmented into textile traders/distributors, direct sales (spinners), and e-commerce platforms. By end-user industry, the market is segmented into apparel and fashion, industrial and technical textiles, automotive components, and consumer goods. The report also covers the market size and forecasts for nylon 6 filament yarn in 21 countries across the world. For each segemnt market sizing and forecasts are provided in terms of value (USD).

| Partially Oriented Yarn (POY) |

| Fully Drawn Yarn (FDY) |

| High-Tenacity Industrial Yarn |

| Textured Yarn |

| Fabric |

| Sports Apparel |

| Sports and Adventure Equipment |

| Travel Accessories |

| Fishing Nets |

| Textile Traders / Distributors |

| Direct Sales (Spinners) |

| E-commerce Platforms |

| Apparel and Fashion |

| Industrial and Technical Textiles |

| Automotive Components |

| Consumer Goods |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Vietnam | |

| Malaysia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Yarn Type | Partially Oriented Yarn (POY) | |

| Fully Drawn Yarn (FDY) | ||

| High-Tenacity Industrial Yarn | ||

| Textured Yarn | ||

| By Application | Fabric | |

| Sports Apparel | ||

| Sports and Adventure Equipment | ||

| Travel Accessories | ||

| Fishing Nets | ||

| By Distribution Channel | Textile Traders / Distributors | |

| Direct Sales (Spinners) | ||

| E-commerce Platforms | ||

| By End-user Industry | Apparel and Fashion | |

| Industrial and Technical Textiles | ||

| Automotive Components | ||

| Consumer Goods | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Vietnam | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Nylon 6 filament yarn market by 2031?

The market is forecast to reach USD 35.03 billion by 2031 growing from USD 25.88 billion in 2026 with a projected CAGR of 6.24% from 2026 to 2031.

Which region will grow fastest to 2031?

Asia-Pacific, expanding at an estimated 6.36% CAGR due to integrated Chinese and Southeast Asian capacity additions.

Which application segment shows the highest CAGR?

Sports and adventure equipment is predicted to register a 6.45% CAGR through 2031.

Why are e-commerce platforms important for yarn procurement?

They provide real-time pricing, reduce working-capital cycles, and are growing at a 6.89% CAGR, eroding traditional distributor share.

Page last updated on: