Drone Simulation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

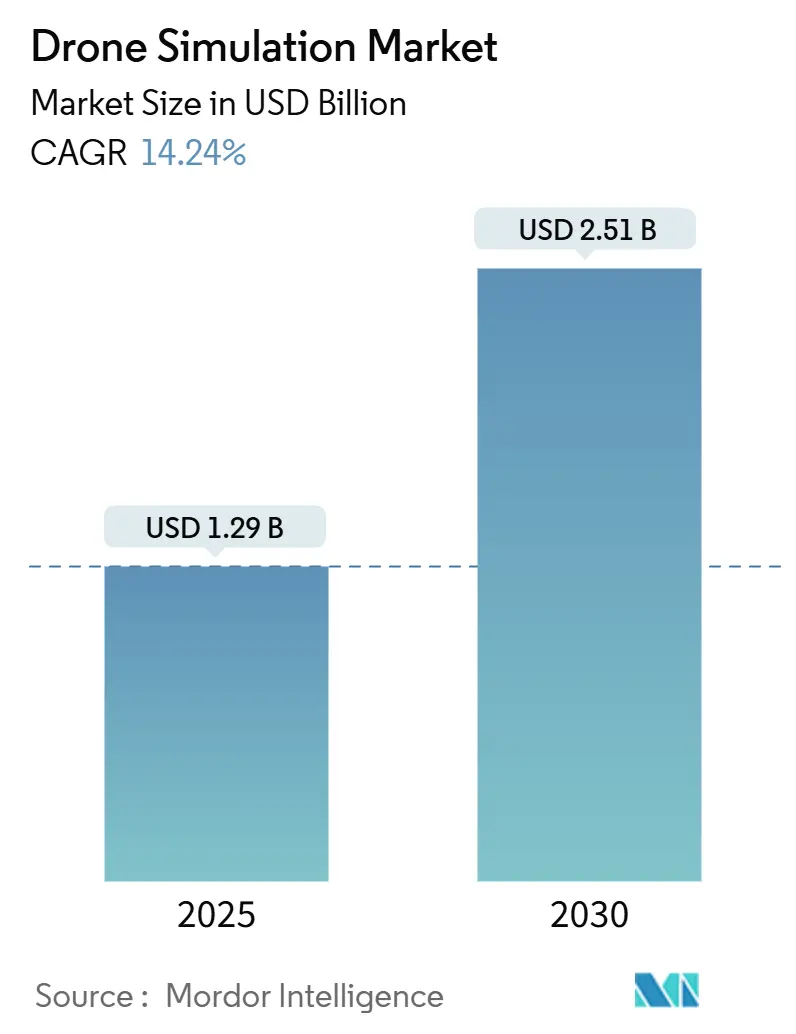

| Market Size (2025) | USD 1.29 Billion |

| Market Size (2030) | USD 2.51 Billion |

| Growth Rate (2025 - 2030) | 14.24% CAGR |

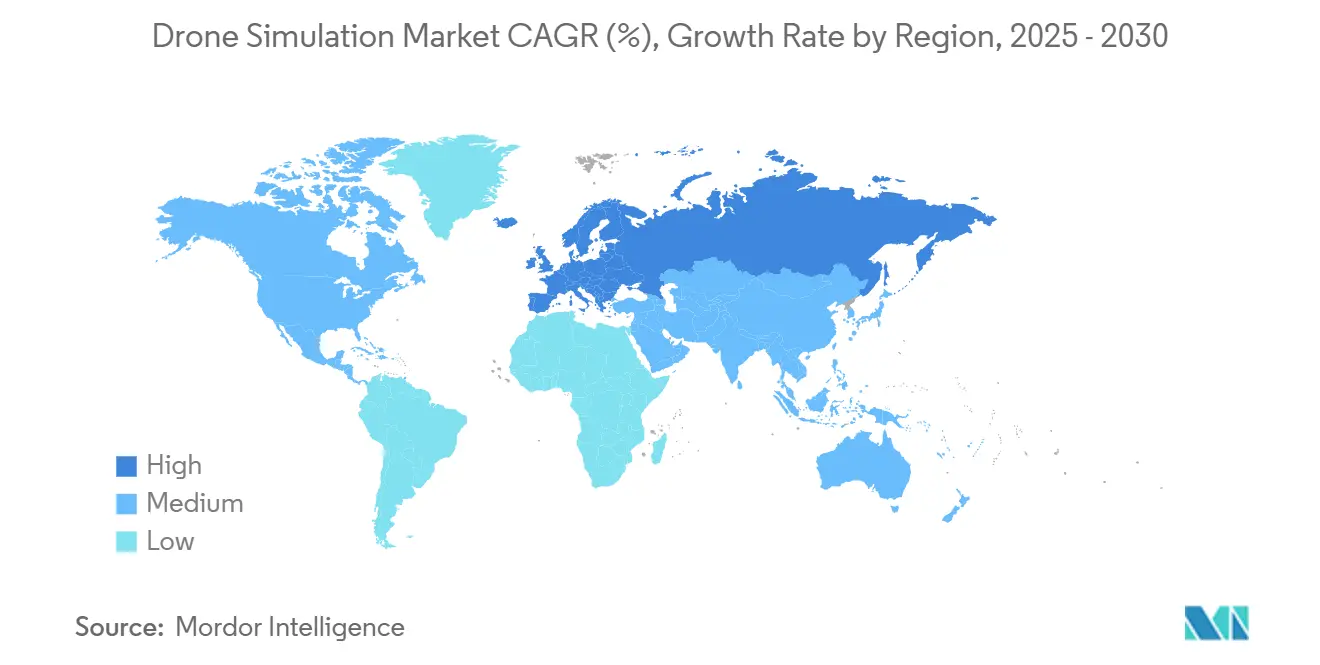

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drone Simulation Market Analysis by Mordor Intelligence

The drone simulation market size stood at USD 1.29 billion in 2025 and is projected to reach USD 2.51 billion by 2030, advancing at a 14.24% CAGR. Mandatory pilot-in-command certification, expanding regulatory sandboxes, and insurer-driven simulator scoring collectively accelerate spending on high-fidelity training ecosystems. Firms invest in physics-rich engines, multi-sensor scenario generation, and distributed GPU compute to satisfy Beyond Visual Line of Sight (BVLOS) requirements and autonomous-flight competencies. Supply-chain shortfalls for premium GPUs spur cloud migration, while photorealistic AI content tools lower scenario-creation costs. Vendors differentiate by vertically integrating hardware, software, and services, rather than competing on price. Growth opportunities also arise from digital-twin convergence, where industrial operators validate maintenance, inspection, and emergency-response workflows in synthetic environments.

Key Report Takeaways

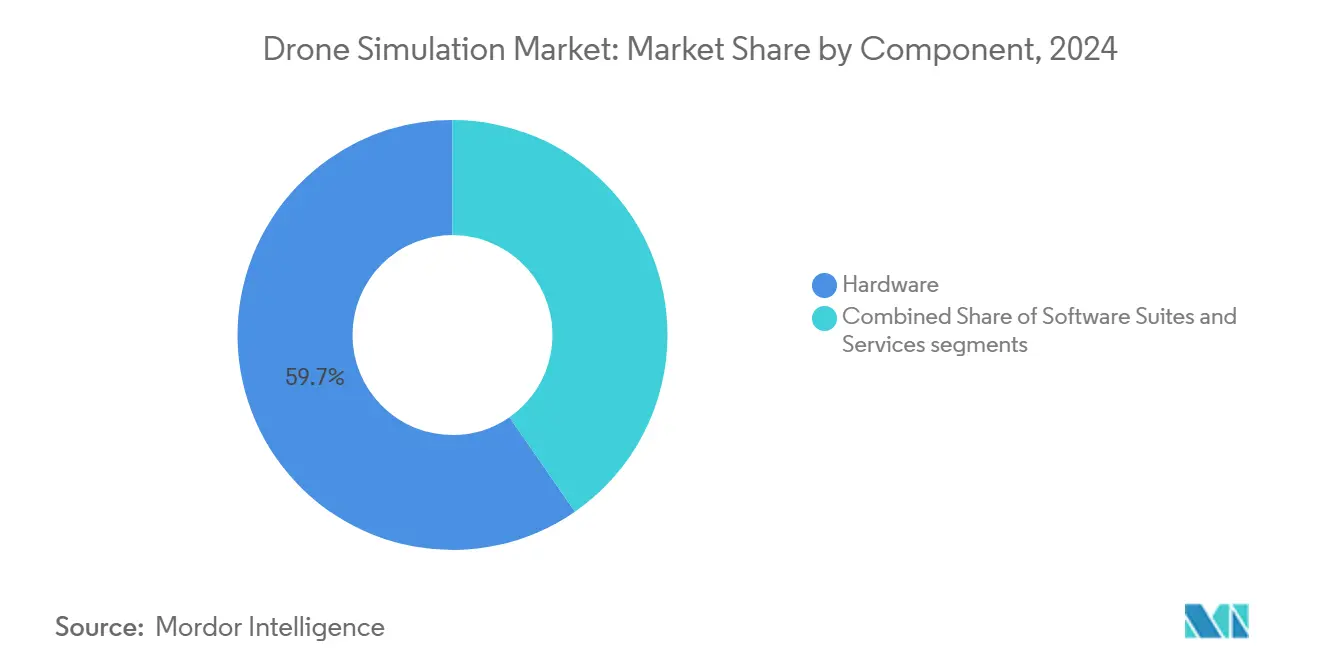

- By component, hardware captured 59.65% of the drone simulation market share in 2024, whereas software is forecasted to expand at a 15.28% CAGR to 2030.

- By platform type, fixed-wing simulators led with 49.89% revenue share in 2024; hybrid/eVTOL simulators are projected to advance at 14.9% CAGR through 2030.

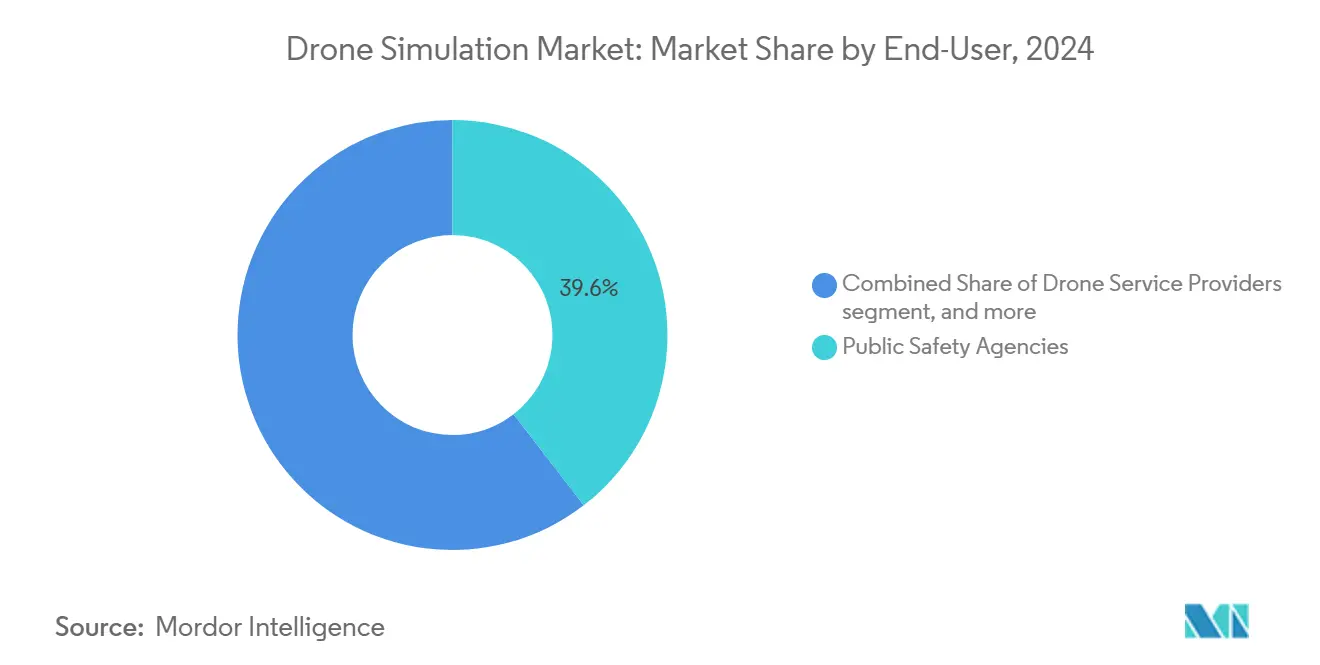

- By end-user, public safety agencies accounted for 39.55% of the drone simulation market in 2024, while e-commerce logistics is the fastest-growing segment, with a 15.83% CAGR.

- By deployment mode, on-premise systems held a 68.51% share in 2024; cloud deployments are expected to rise at a 16.93% CAGR during the forecast period.

- By geography, North America dominated with a 41.31% share in 2024, whereas Europe is set to post the highest regional CAGR of 14.82% to 2030.

Global Drone Simulation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory pilot-in-command certification for commercial UAVs | +3.20% | Global with early adoption in North America and Europe | Medium term (2-4 years) |

| Expansion of last-mile drone delivery sandboxes | +2.80% | North America, Europe, APAC core | Short term (≤ 2 years) |

| Integration of drone digital twins into industrial IoT platforms | +2.10% | Global industrial hubs | Long term (≥ 4 years) |

| Insurance underwriters requiring simulator-based risk scoring | +1.90% | North America and EU | Medium term (2-4 years) |

| AI-driven photorealistic scenario generation | +2.40% | Global tech hubs | Short term (≤ 2 years) |

| Cloud-native simulation platforms lowering entry barriers | +1.80% | Regions with robust cloud infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mandatory Pilot-in-Command Certification for Commercial UAVs

Global regulators now mandate simulator-logged hours before BVLOS or autonomous operations receive approval. The FAA’s revisions to Part 107 and EASA’s Specific Training Scenario (STS) framework require scenario-based proficiency demonstrations, including emergency procedures, multi-aircraft coordination, and adverse-weather decision-making.[1]European Union Aviation Safety Agency, “Drones – Unmanned Aircraft Systems,” EASA, easa.europa.eu National authorities in Canada, Australia, and Singapore are drafting similar rules. As certification gates tighten, operators queue for accredited platforms, spurring procurement cycles among training schools, public-safety agencies, and enterprise drone programs. The continuous update of standardized curricula locks in recurring software-licensing revenue and drives demand for modular hardware that instructors can reseat across aircraft classes.

Expansion of Last-Mile Drone-Delivery Sandboxes

Governments leverage sandbox models to accelerate proof-of-concept deployments while managing public-safety risk. Hong Kong approved 38 low-altitude pilot projects in March 2025, spanning rescue, logistics, and inspection tasks.[2]Hong Kong Special Administrative Region Government, “Regulatory Sandbox Pilot Projects to Foster Low-Altitude Economy,” info.gov.hk The US BEYOND initiative and the UK CAA’s open-lane corridors follow similar logic, granting BVLOS waivers only after virtual flight-path validation. Operators must rehearse dense-traffic contingencies and lost-link protocols inside synthetic environments, driving sales of multi-drone orchestration modules and unified traffic-management (UTM) plugins. Rising parcel volumes and single pilot to many aircraft ratios further heighten simulation throughput needs.

Integration of Drone Digital Twins into Industrial IoT Platforms

Asset-intensive industries couple drone telemetry with plant sensors to build digital twins that forecast equipment wear, schedule maintenance, and test emergency responses. Platforms from Duality AI and other industrial IoT vendors embed physics-based engines capable of simulating rotor downwash on flare stacks, enabling hazardous-area inspections without halting production. The convergence requires APIs that feed real-time operational data into simulation loops, creating demand for open-standard middleware and edge-compute accelerators.

Insurance Underwriters Requiring Simulator-Based Risk Scoring

Insurers led by i3 Underwriting now condition hull and liability coverage on simulator-generated proficiency reports that benchmark pilot response times and adherence to geo-fence alerts. Underwriters integrate scenario-outcome scores into actuarial models, forcing commercial operators to maintain minimum training hours on approved platforms. As loss-ratio data accumulates, insurance-discount tiers reward clients for continuous simulation, incentivizing subscription renewals and feeding a feedback loop reinforcing platform stickiness.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of harmonized global training standards | -1.60% | Global cross-border operations | Long term (≥ 4 years) |

| High licensing fees for high-resolution urban terrain data | -1.20% | Urban-dense developed regions | Medium term (2-4 years) |

| GPU supply constraints for large-ccale cloud simulation | -1.80% | North America and Europe | Short term (≤ 2 years) |

| Cybersecurity risks in SaaS-based simulation environments | -1.40% | Defense and government sectors worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Harmonized Global Training Standards

ICAO works toward global frameworks, yet divergent national interpretations persist, forcing multinational operators to retrain crews for each jurisdiction.[3]International Civil Aviation Organization, “Unmanned Aircraft Systems (UAS),” icao.int European pilots converting national licenses to EASA certificates confront lengthy paperwork, while Asia-Pacific markets still refine BVLOS rules. Fragmented requirements inflate compliance costs and complicate software certification pathways, delaying cross-border fleet expansion and thereby tempering the growth of the drone simulation market.

High Licensing Fees for High-Resolution Urban Terrain Data

Urban-delivery and first-responder scenarios demand sub-25 cm resolution 3-D meshes. Providers like Getmapping charge annual fees exceeding USD 50,000 for full-city coverage. Small simulation vendors struggle to absorb these costs, narrowing geographic libraries and limiting location-specific training. Price pressure also deters new entrants, constraining competition and slowing content diversification needed for the drone simulation market to fulfill diverse regulatory test cases.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Faces Software Disruption

Hardware accounted for 59.65% of the drone simulation market size 2024 as immersive cockpits, premium GPUs, and haptic flight controls remained essential for defense-grade fidelity. GPU shortages, however, cap hardware unit growth and intensify total-cost-of-ownership scrutiny. Software suites, growing at 15.28% CAGR, harness cloud elasticity to render complex aerodynamics without local silicon. Vendors embed no-code scenario editors, open-API integrations, and pay-as-you-go billing, shifting purchasing power toward fleet managers rather than IT procurement desks.

Software-centric models unlock recurring revenue streams through content subscriptions and compliance updates, eroding the up-front hardware margin moat. Edge-rendering pipelines ingest streaming sensor feeds to synchronize digital twins with real plants, deepening enterprise lock-in. As supply-chain strains persist, buyers pivot to software-first stacks that can run on commodity thin clients, propelling the software segment’s influence on the drone simulation market.

By Platform Type: Fixed-Wing Leadership Challenged by Hybrid Innovation

Fixed-wing simulators held 49.89% of the drone simulation market share in 2024, favored for long-range cargo, survey, and agricultural missions requiring sophisticated aerodynamic modeling. High-aspect-ratio wing behavior under mountain wave turbulence necessitates robust physics engines that incumbents such as ANSYS supply. Yet hybrid/eVTOL platforms, expanding at 14.9% CAGR, attract urban-mobility investors seeking to optimize transition regimes between hover and forward flight.

Hybrid training curricula demand scenarios covering rooftop vertiport congestion, power-module redundancy, and noise abatement—a richer domain than classical fixed-wing syllabi. Vendors respond with variable-geometry models and multi-domain control-law editors. Multirotor simulators remain popular for entry-level SKUs, but revenue momentum shifts toward hybrid due to higher-value enterprise licenses, reinforcing competitive stakes within the drone simulation market.

By End-User: Public Safety Leads While E-Commerce Accelerates

Public safety agencies commanded 39.55% of the drone simulation market in 2024. Fire, police, and search-and-rescue teams practice night operations, wildfire overflights, and coordinated manned-unmanned response in secure simulators. Grants and homeland security funds continue to subsidize turnkey packages. Conversely, e-commerce logistics shows the quickest trajectory with a 15.83% CAGR, spurred by retailers’ promises of 15-minute delivery windows and regulators’ willingness to issue sandbox waivers after simulator-backed risk assessments.

Industrial and energy verticals adopt at stable rates for asset-inspection rehearsal. Academic institutions expand enrollment in remote-pilot courses, fueling service revenue for tailored curricula. The widening canvas of applications incentivizes vendors to bundle scenario libraries across use cases, nurturing cross-sell opportunities throughout the drone simulation market.

By Deployment Mode: Cloud Migration Accelerates Despite On-Premise Dominance

On-premise deployments retained a 68.51% share in 2024 as defense ministries and critical infrastructure operators prioritized data sovereignty. Latency-sensitive haptic feedback and classified flight profiles still reside in secure facilities. Nonetheless, cloud installations rose at a 16.93% CAGR as encryption standards, zero-trust architectures, and region-locked data centers satisfy corporate risk officers.

As exemplified by FlytBase AI-R, Edge-compute frameworks split workloads, keeping sensor-classified packets local while streaming atmospheric models from cloud clusters. Cost-per-flight-hour analysis favors cloud scaling for commercial fleets subject to seasonality. As GPU capacity gradually unfreezes, hybrid deployment paradigms accelerate the conversion pipeline, aligning with broader enterprise SaaS adoption trends and propelling the drone simulation market.

Geography Analysis

North America captured 41.31% of the drone simulation market in 2024, underpinned by the FAA’s BEYOND program, DIU procurement, and mature venture funding ecosystems. Defense primes integrate simulators into broader live-virtual-constructive ranges. At the same time, tech majors refine open-source engines that feed academic and commercial R&D. US insurers spearhead simulator-linked underwriting, further entrenching domestic demand.

Europe is forecasted to record a 14.82% CAGR through 2030 as EASA’s harmonized Specific Training Scenarios give operators clearer certification roadmaps. National aviation bodies expedite BVLOS corridors for medical deliveries in France, Germany, and the Nordics, driving purchases of platform-agnostic training suites. EU research grants finance AI-generated weather micro-models to support urban-air-mobility safety cases, creating spillover benefits for simulation vendors.

Asia-Pacific advances on surging drone adoption in China, Japan, and India. Hong Kong’s 38-project sandbox demonstrates governmental commitment, while India’s Make-in-India incentives spawn domestic simulator providers allied with local OEMs. Japan’s ministries fund tsunami-response training modules, and Australia’s civil aviation regulator pilots cross-border proficiency recognition. Collectively, these initiatives cultivate a diversified growth stream for the drone simulation market across the region.

Competitive Landscape

The drone simulation market remains moderately fragmented as aerospace incumbents, defense integrators, cloud hyperscalers, and nimble startups vie for end-to-end control of the simulation stack. ANSYS and CAE leverage decades-deep physics and certification know-how to secure high-fidelity defense and airline contracts.[4]CAE Inc., “Civil Aviation Training Solutions,” cae.com Technology giants contribute open-source engines that accelerate experimentation but monetize through cloud consumption.

Startups differentiate with AI-generated content pipelines and pay-as-you-grow SaaS models. Recent acquisitions—Shield AI buying Sentient Vision Systems and Red Cat absorbing FlightWave—signal a consolidation wave aimed at bundling perception, autonomy, and training. Partnerships abound: Zen Technologies teams with AVT Simulation to penetrate US defense channels, and Draganfly aligns with Volatus to co-develop offshore inspection simulators.

Competitive strategy favors vertical integration spanning physics cores, scenario libraries, learning-management dashboards, and accreditation toolkits. Price discounting remains muted; buyers value regulatory compliance and content breadth over low upfront costs. Vendors invest in developer-friendly SDKs and marketplace ecosystems to foster third-party module creation, reinforcing platform stickiness and expanding the total accessible drone simulation market.

Drone Simulation Industry Leaders

SZ DJI Technology Co., Ltd.

ANSYS, Inc

CAE Inc.

AirSim (Microsoft Corporation)

Simlat Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Ansys, part of Synopsys, and NVIDIA established a licensing agreement to integrate and support Omniverse technology within Ansys simulation solutions. Integrating NVIDIA Omniverse™ enables Ansys to provide customers with direct access to Omniverse technologies and libraries, initially focusing on computational fluid dynamics (CFD) and autonomous solutions.

- August 2025: Ukraine developed the Ukrainian Flight Drone Simulator (UFDS), the first specialized training software for FPV drone operators. The simulator includes training modules for interceptors and kinetic counter-drone systems, including VARTA DroneHunter.

Global Drone Simulation Market Report Scope

| Software Suites |

| Hardware |

| Services |

| Multirotor Drone Simulators |

| Fixed-Wing Drone Simulators |

| Hybrid and eVTOL Simulators |

| Drone Service Providers |

| Industrial and Energy Enterprises |

| E-commerce and Logistics Firms |

| Public Safety Agencies |

| Academic and Training Institutions |

| On-Premise |

| Cloud-Based |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Israel |

| Saudi Arabia | ||

| UAE | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Software Suites | ||

| Hardware | |||

| Services | |||

| By Platform Type | Multirotor Drone Simulators | ||

| Fixed-Wing Drone Simulators | |||

| Hybrid and eVTOL Simulators | |||

| By End-User | Drone Service Providers | ||

| Industrial and Energy Enterprises | |||

| E-commerce and Logistics Firms | |||

| Public Safety Agencies | |||

| Academic and Training Institutions | |||

| By Deployment Mode | On-Premise | ||

| Cloud-Based | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Israel | |

| Saudi Arabia | |||

| UAE | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the drone simulation market?

It was valued at USD 1.29 billion in 2025 and is set to reach USD 2.51 billion by 2030, advancing at a 14.24% CAGR.

Which segment is growing fastest within drone simulators?

Software suites, boosted by cloud delivery, are advancing at a 15.28% CAGR.

Why are insurers interested in simulation data?

Underwriters use simulator-derived proficiency scores to calibrate premiums and reduce loss ratios.

Which region is projected to post the highest growth?

Europe, benefiting from EASA’s harmonized rules, is forecasted to grow at 14.82% CAGR.

How do AI tools impact simulation content?

Generative AI cuts scenario-creation time, enabling photorealistic environments that improve pilot readiness.

What deployment mode is gaining traction beyond defense?

Cloud-based platforms, supported by enhanced encryption and hybrid edge designs, show the fastest uptake.

Page last updated on: