Combat Helicopter Simulation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

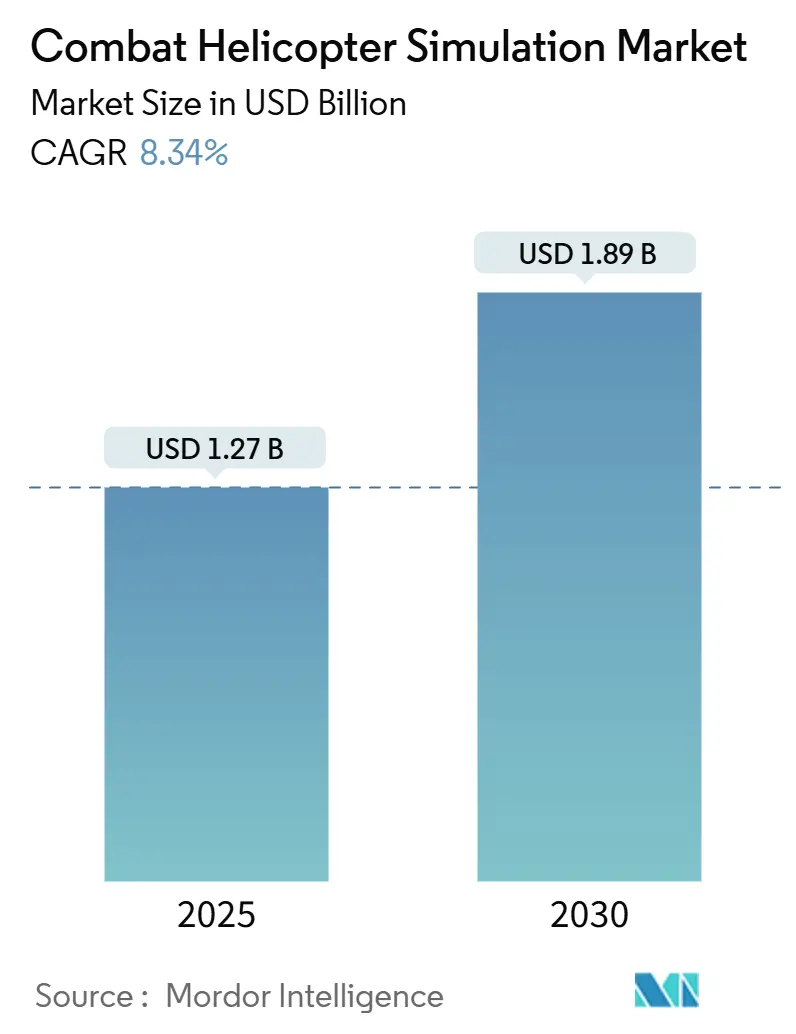

| Market Size (2025) | USD 1.27 Billion |

| Market Size (2030) | USD 1.89 Billion |

| Growth Rate (2025 - 2030) | 8.34% CAGR |

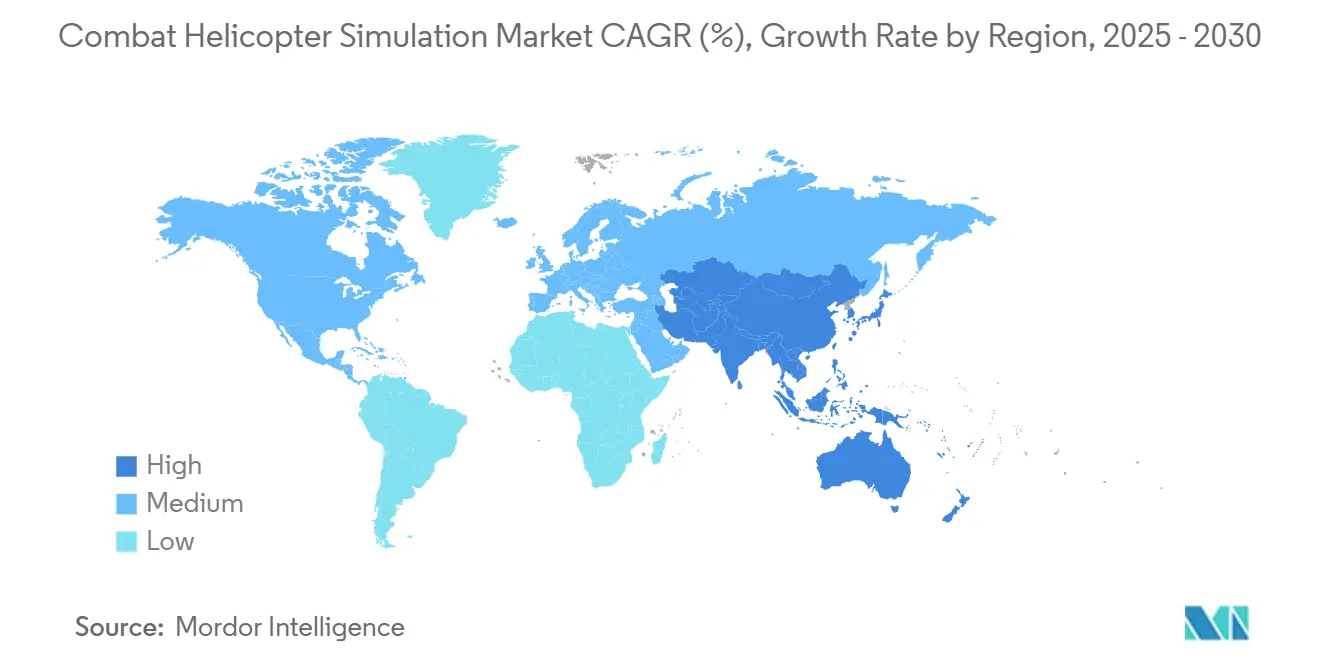

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Combat Helicopter Simulation Market Analysis by Mordor Intelligence

The combat helicopter simulation market reached USD 1.27 billion in 2025 and is forecasted to expand to USD 1.89 billion by 2030, translating into an 8.34% CAGR. Defense ministries are scaling synthetic training to curb live-flight costs, improve safety, and accelerate throughput. At the same time, vendors integrate virtual reality, artificial intelligence, and modular containerized devices to deliver training at the point of need. Continuous fleet modernization and an acute global pilot shortage prompt armed forces to procure high-fidelity simulators replicating new avionics suites and mission systems. Vendors with long-duration service contracts and forward-deployed training solutions enjoy defensible positions as customers prioritize availability, lifecycle support, and rapid technology refresh. As Asia-Pacific militaries modernize rotary-wing fleets and invest in indigenous training infrastructure, regional demand is outpacing the global average, encouraging suppliers to form joint ventures, offer offset arrangements, and localize maintenance capabilities.

Key Report Takeaways

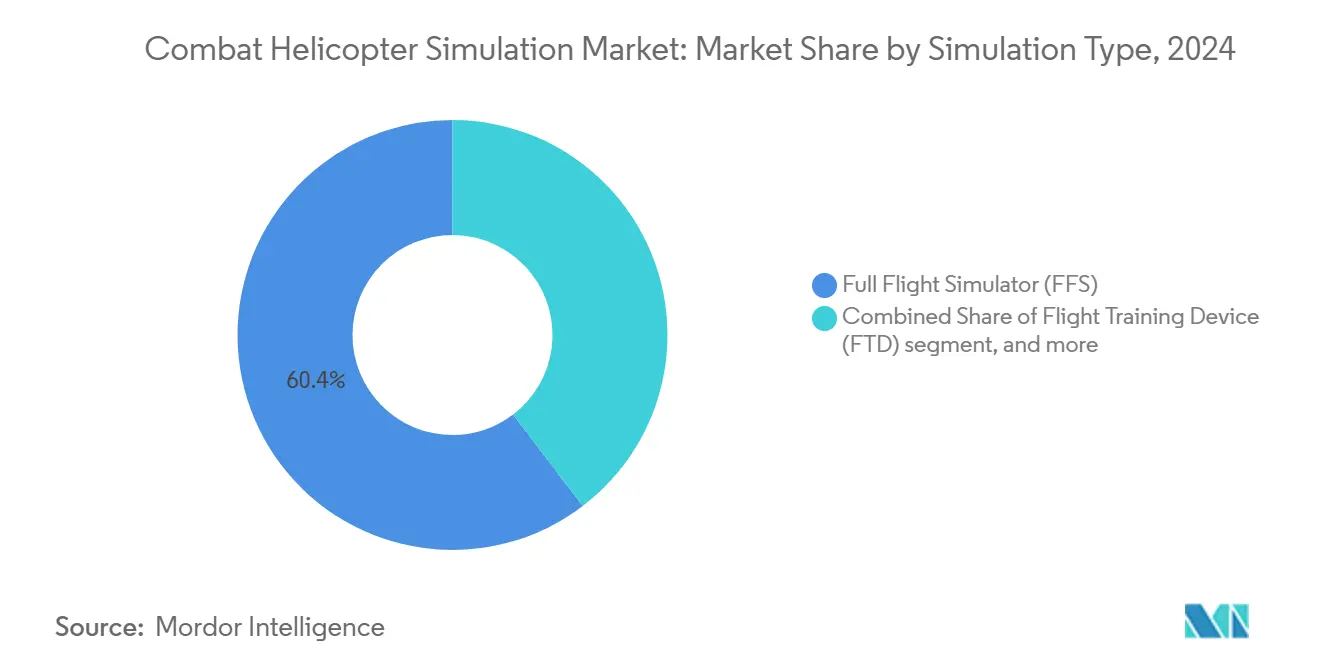

- By simulation type, full flight simulators (FFS) led with 60.36% revenue share in 2024, while VR/mixed-reality trainers registered the fastest 12.45% CAGR through 2030.

- By component, services accounted for 42.48% of the combat helicopter simulation market size in 2024, and software is projected to grow at a 10.80% CAGR to 2030.

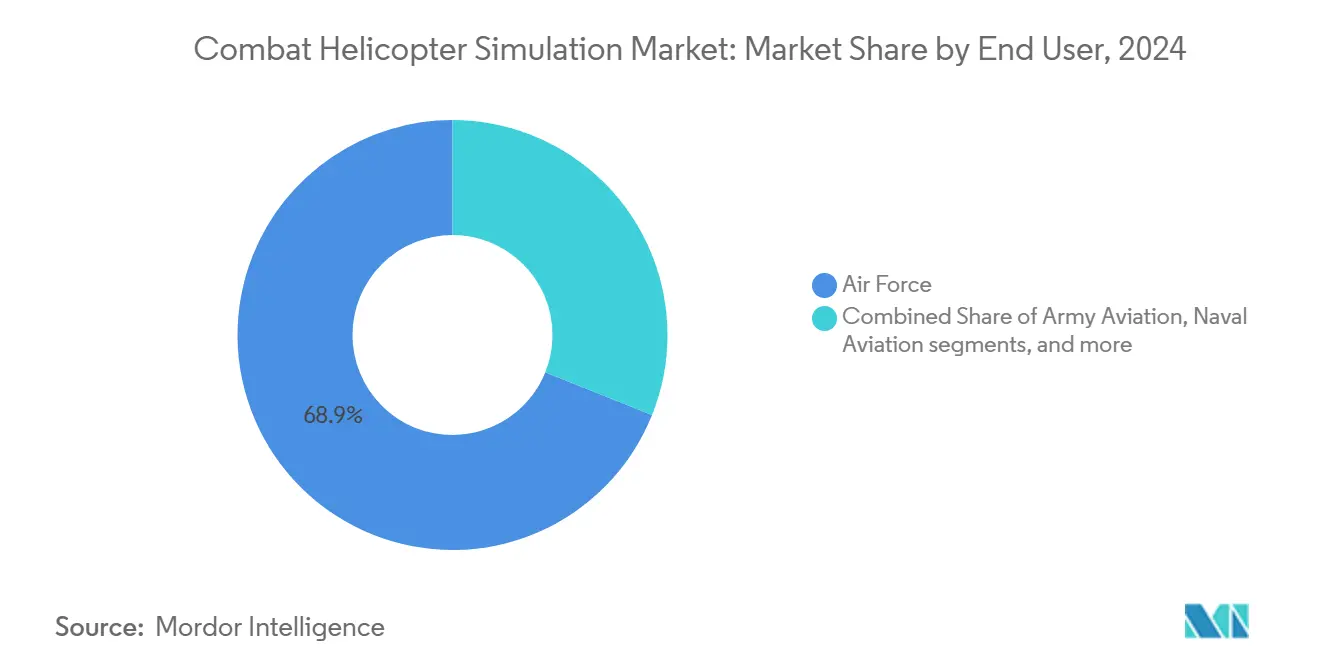

- By end user, air force applications commanded 68.93% of the combat helicopter simulation market share in 2024; naval aviation is advancing at an 11.68% CAGR to 2030.

- By training solution, products held 56.71% share of the combat helicopter simulation market size in 2024, whereas services are expanding at a 9.45% CAGR through 2030.

- Geographically, North America captured 38.27% of revenue in 2024, and Asia-Pacific is forecast to register an 8.48% CAGR between 2025 and 2030.

Global Combat Helicopter Simulation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising defense spending on rotary-wing pilot readiness | +1.80% | North America, Asia-Pacific | Medium term (2-4 years) |

| Cost-effective training need reducing live-flight hours and risk | +1.50% | North America, Europe | Short term (≤ 2 years) |

| Rapid adoption of immersive VR/AR and mixed-reality trainers | +1.40% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Fleet-modernization-driven demand for updated simulation data-packs | +1.20% | Global | Long term (≥ 4 years) |

| AI-driven adaptive scenario generation for personalized mission rehearsal | +1.10% | North America, Europe | Medium term (2-4 years) |

| Containerized forward-deployed simulators trimming infrastructure cost | +0.90% | Global (expeditionary forces) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Defense Spending on Rotary-Wing Pilot Readiness

Military budgets continue to rise as governments respond to evolving security threats and personnel shortfalls. The US Army extended its Advanced Helicopter Flight Training Support contract to 2030 to train about 900 student aviators yearly on CH-47F, UH-60M, and AH-64E variants.[1]CAE, “Advanced Helicopter Flight Training Support Extension,” asdnews.com Comparable procurements are visible in India and the Philippines, where Seahawk and Black Hawk simulators have been ordered to accelerate indigenous pilot pipelines. Japan’s FY 2025 defense plan earmarks additional funds for AH-64E conversion training, signaling that Asia-Pacific outlays are expanding beyond initial procurement toward sustained simulator operations. Long-duration service contracts lock in predictable spending on instructor cadres, software support, and spare parts, giving suppliers a clear growth runway. As multi-year appropriations become the norm, vendors gain better visibility on upgrade cycles and can align R&D roadmaps with customer funding profiles.

Cost-Effective Training Need Reducing Live-Flight Hours and Risk

Flight hour costs for attack and utility helicopters routinely exceed USD 10,000, making simulators an attractive alternative for emergency procedures, NVG operations, and complex mission rehearsal. Lockheed Martin’s containerized CH-53K trainer delivers motion-cueing, visual, and networking capability inside a shipping container that can be air-lifted to forward bases, saving infrastructure spending and preserving operational aircraft for missions. US Air Force “Pilot Training Next” initiatives further validate desktop and VR devices that run commercial hardware, yet still meet curriculum outcomes.[2]Lockheed Martin, “Containerized CH-53K Training Device,” lockheedmartin.com Cost modeling by program analysts shows containerized devices can cut facility investment by 30-40% and decrease per-sortie fuel burn by shifting up to 60% of syllabus events into synthetic environments. Reduced mishap exposure also keeps insurance premiums and maintenance reserves in check, an increasingly important metric for budget oversight offices. Despite capital constraints, these tangible savings strengthen the economic case for expanding simulator fleets.

Rapid Adoption of Immersive VR/AR and Mixed-Reality Trainers

Virtual-reality systems now meet regulatory credit standards. Leonardo’s VxR became the first VR-based helicopter trainer to achieve FAA FTD Level 7 qualification, opening the door for creditable type-rating and recurrent training on immersive devices. Loft Dynamics earned a corresponding FAA approval for its H125 trainer, demonstrating that compact head-mounted displays and electric-actuated cockpits can replicate maneuver cues without full-motion platforms. TRU Simulation’s VERIS platform cuts floor space by 80% and training cost by more than 50%, giving procurement officers an immediate return on investment. Defense Innovation Unit delivered more than 200 mixed-reality stations to Air Education and Training Command, underscoring institutional confidence in head-mounted solutions. As EASA and other regulators align with FAA precedents, the addressable market for creditable VR devices will broaden across NATO and partner nations.

Fleet-Modernization-Driven Demand for Updated Simulation Data-Packs

Rotorcraft upgrades, such as the T901 engine retrofitted into UH-60M fleets, alter performance envelopes and require corresponding simulator re-tuning. Likewise, autonomy kits like MATRIX introduce new flight regimes that pilots must master in synthetic environments before deploying on real aircraft. CAE now offers subscription-based data-pack services that deliver quarterly updates to flight models, avionics logic, and threat libraries, ensuring continuous alignment with fleet software baselines. Customers adopting incremental block upgrades—for example, the AH-64E Version 6 roadmap—prefer simulators with rapid reconfiguration capability to avoid training gaps during aircraft retrofit periods. These modernization cycles generate recurring revenue for database updates, instructor cross-qualification, and hardware modifications, often exceeding the value of the original device sale over a 20-year life span. Because many rotary-wing platforms will remain in service beyond 2040, continual upgrade demand locks in a stable aftermarket for suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition and life-cycle costs of Level-D devices | -1.20% | Global (smaller militaries) | Short term (≤ 2 years) |

| Shortage of qualified simulator instructors and maintainers | -0.80% | Asia-Pacific, Global | Medium term (2-4 years) |

| Motion/cyber-sickness limiting long VR sessions | -0.60% | Global | Short term (≤ 2 years) |

| Cyber-security exposure of networked/cloud simulators | -0.50% | Global (classified networks) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Life-Cycle Costs of Level-D Devices

A single Level-D combat helicopter simulator can require capital outlays near USD 40 million and generate operating costs surpassing USD 1,000 per hour, limiting adoption among smaller forces. Motion system upkeep, proprietary avionics interfaces, and software sustainment drive total cost of ownership even after initial procurement. These economics push buyers toward fixed-base or VR devices for early-stage training, reserving Level-D exposure for critical envelope points and mission rehearsal.

Shortage of Qualified Simulator Instructors and Maintainers

Experienced military aviators with instructional credentials remain in short supply, particularly across emerging Asia-Pacific hubs, where new training centers are coming online faster than workforce pipelines can respond. Technical maintainers also require platform-specific certifications to service hydraulic motion bases, image generators, and networking stacks. Armed forces rely on OEM-supplied personnel when organic staffing is unavailable, increasing operating expense and stretching deployment timelines.[3]Government Accountability Office, “Aircraft Simulator Training Contract Management,” gao.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Simulation Type: VR Growth Accelerates, Full Flight Simulators Retain Primacy

FFS holds 60.36% of the combat helicopter simulation market share in 2024 due to unrivaled fidelity, integrated motion cues, and mandatory use for weapons employment and emergency maneuvers. They remain indispensable for aircraft like AH-64E and CH-53K, which require six-axis motion and out-the-window cueing. VR/mixed-reality trainers post the fastest 12.45% CAGR as head-mounted solutions earn regulatory credit and slash facility footprint. The US Air Force fielded 225 mixed-reality systems across four bases to expand training throughput without constructing new buildings.[4]DVIDS, “DIU Immersive Training Device Delivery,” dvidshub.net Macro-economic pressure to optimize budgets pushes entry-level and currency events into headset devices, yet motion platforms still dominate complex mission rehearsal, ensuring balanced demand across both categories.

Second-generation mixed-reality architecture merges dome visuals with headset-based sensor emulation, enabling gunnery, sling-load, and degraded-visual-environment scenarios within a single device. Commercial game engines cut scenario-development cycles, while containerized units support distributed operations. As certification bodies widen Part 60 and EASA CS-FSTD-H guidance to encompass immersive devices, hybrid fleets that pair motion simulators for advanced tasks with VR suites for initial training will become standard.

By Component: Service Dominance Meets Software Upswing

Services generated 42.48% of revenue in 2024, underscoring the importance of turnkey instructor cadres, lifecycle maintenance, and syllabus management. CAE’s US Army contract extension through 2030 covers instructor pilots, maintenance evaluators, and curriculum updates, locking in multiyear cash flows. Software expands at a 10.8% CAGR on the back of AI-enabled grading engines, cloud-based learning management, and cybersecurity utilities. FlightSafety’s FlightSmart captures more than 4,000 telemetry points per second to automate debriefing and personalize remediation. Hardware demand stabilizes as VR headsets and compact motion bases reduce metal content per device, yet periodic refresh cycles for image generators and motion actuators protect baseline sales.

Lifecycle service bundles now include avionics block updates, threat library refresh, and remote health monitoring that predicts mean-time-between-failure, enhancing device availability and deepening vendor lock-in.

By End User: Air Forces Dominate, Naval Aviation Outpaces Growth

Air Force organizations accounted for 68.93% of 2024 revenue, driven by multi-mission twin-engine fleets and high trainee throughput. Programs like the US Army’s annual expansion to graduate 900 aviators require simultaneous procurement of simulators, classroom systems, and instructor services. Continued upgrades to AH-64E, UH-60M, and CH-47F avionics blocks will keep the demand for the combat helicopter simulation market size elevated for Air Force training detachments through the decade. Decision-makers also favor networked Full Mission Simulators that can link with fixed-wing assets for joint all-domain exercises, a factor that sustains capital investment despite rising VR uptake. Naval aviation grows at an 11.68% CAGR, fueled by shipboard H-60R modernization and emphasis on anti-submarine warfare in the Indo-Pacific. The SH-60R syllabus integrates dipping sonar, data-link tactics, and deck-landing procedures that only high-fidelity simulators can replicate. Fleet Commands additionally require specialized motion cues to practice degraded-visual-environment landings on moving decks, a niche only a handful of suppliers can support. OEM-run centers and Army Aviation maintain a significant share for maintenance test-pilot training and customer demonstration flights, reinforcing a diverse end-user mix that underpins steady aftermarket revenue for data-pack refresh and instructor currency programs.

By Training Solution: Capital Sales Lead, “Training-as-a-Service” Gains Momentum

Products contributed 56.71% of 2024 revenue as customers purchased new devices to replace obsolescent hardware and equip emerging helicopter variants. Services grow at a 9.45% CAGR through 2030, reflecting a shift toward availability-based models where vendors guarantee throughput under performance metrics. Long-term support contracts bundle instructor cadres, software updates, and proactive maintenance, creating predictable cash flows while relieving operators of staffing burdens. Containerized trainers further drive service adoption because OEM crews travel with devices, allowing users to pay a daily rate rather than front-load capital expenditure. The same model extends to cloud-hosted AI debrief tools that bill per student, tightening the link between payment and training outcomes. Performance-based logistics clauses reward suppliers for exceeding simulator-uptime thresholds, pushing them to invest in remote health-monitoring sensors and predictive analytics. As militaries adopt zero-trust cybersecurity mandates, service providers also assume responsibility for accreditation and patch management, deepening customer reliance on outsourced expertise.

Geography Analysis

North America retained a 38.27% revenue share in 2024, benefiting from sustained procurement lines and mature simulator infrastructure at Fort Novosel, Hurlburt Field, and Marine Corps Air Stations. The CH-53K containerized trainer network exemplifies forward-deployed high-fidelity devices that align with expeditionary doctrine.

Europe upholds a sizeable installed base supported by domestic OEMs such as Leonardo and Airbus Helicopters. The Royal Netherlands Air Force commissioned AH-64E simulators in early 2024, and Germany upgraded Sea King MK41 devices to extend service life. NATO interoperability programs pool mission databases and encourage common certification standards, reducing per-unit cost for new acquisitions.

Asia-Pacific posts the fastest 8.48% CAGR as India, Japan, South Korea, the Philippines, and Australia modernize rotorcraft fleets. CAE will deliver Seahawk simulators to the Indian Navy, marking deeper regional localization. Australia’s MRH-90 replacement and Japan’s UH-X induction signal future simulator orders as indigenous training pipelines expand. Regional buyers often negotiate offset packages for local assembly and instructor development, deepening OEM footprints.

The Middle East and Africa show steady demand linked to UH-60M and AH-64E refresh cycles, while Latin America attracts sporadic procurement aligned with US Foreign Military Financing and counter-narcotics initiatives. Despite smaller volume, both regions seek rugged, low-maintenance devices that withstand austere conditions.

Competitive Landscape

The combat helicopter simulation market exhibits high concentration. CAE Inc., Lockheed Martin Corporation, Thales Group, and RTX Corporation collectively deliver more than a significant share of global motion and fixed-base systems. CAE’s multidecade Army contract underscores the power of long-term service relationships. Lockheed Martin differentiates through containerized high-fidelity trainers that align with expeditionary force design. TRU Simulation’s VERIS mixed-reality platform cuts floor space by 80% and training cost by more than 50%, appealing to budget-constrained customers.

Emerging disruptors on the VR front include Loft Dynamics and Leonardo, each securing FAA credits that validate headset-based devices. FlightSafety partners with IBM to embed AI analytics, converting big data insights into adaptive learning. Its competitive strategy centers on rapid scenario generation, secure networking, and lifecycle-service wraps that capture continuous revenue.

Combat Helicopter Simulation Industry Leaders

CAE Inc.

Thales Group

Lockheed Martin Corporation

Indra Sistemas, S.A.

RTX Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: CAE secured a USD 180 million extension to provide Advanced Helicopter Flight Training Support for the US Army through 2030.

- January 2025: Leonardo’s VxR VR trainer achieved FAA FTD Level 7 qualification, making it the first immersive helicopter device to achieve this standard.

- September 2024: CAE Inc. won a contract to supply Seahawk simulators to the Indian Navy.

- July 2024: Loft Dynamics’ H125 VR trainer became the US's first FAA-qualified immersive helicopter device.

Global Combat Helicopter Simulation Market Report Scope

| Full Flight Simulator (FFS) |

| Flight Training Device (FTD) |

| VR/Mixed-Reality Trainer |

| Hardware |

| Software |

| Services |

| Air Force |

| Army Aviation |

| Naval Aviation |

| Defense OEMs and Integrators |

| Products |

| Services |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Simulation Type | Full Flight Simulator (FFS) | ||

| Flight Training Device (FTD) | |||

| VR/Mixed-Reality Trainer | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By End User | Air Force | ||

| Army Aviation | |||

| Naval Aviation | |||

| Defense OEMs and Integrators | |||

| By Training Solution | Products | ||

| Services | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2025 size of the combat helicopter simulation space and where will it stand by 2030?

It is valued at USD 1.27 billion in 2025 and is forecasted to reach USD 1.89 billion by 2030, reflecting an 8.34% CAGR.

Which simulator category holds the largest revenue share right now?

Full Flight Simulators (FFS) command 60.36% of 2024 revenues.

Which geographic region is expanding quickest through 2030?

Asia-Pacific is projected to advance at an 8.48% CAGR, outpacing all other regions.

Why are defense forces accelerating the use of VR trainers?

Head-mounted VR systems cut training cost, lower facility needs, and now carry FAA/EASA credit for loggable hours.

Which end-user segment is showing the fastest growth?

Naval Aviation is slated to grow at an 11.68% CAGR to 2030 on rising shipboard helicopter demand.

What key technology is improving personalized pilot instruction?

AI-driven adaptive scenario engines analyze thousands of data points in real time to tailor missions to each aviator’s skill gaps.

Page last updated on: