Drone Battery Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

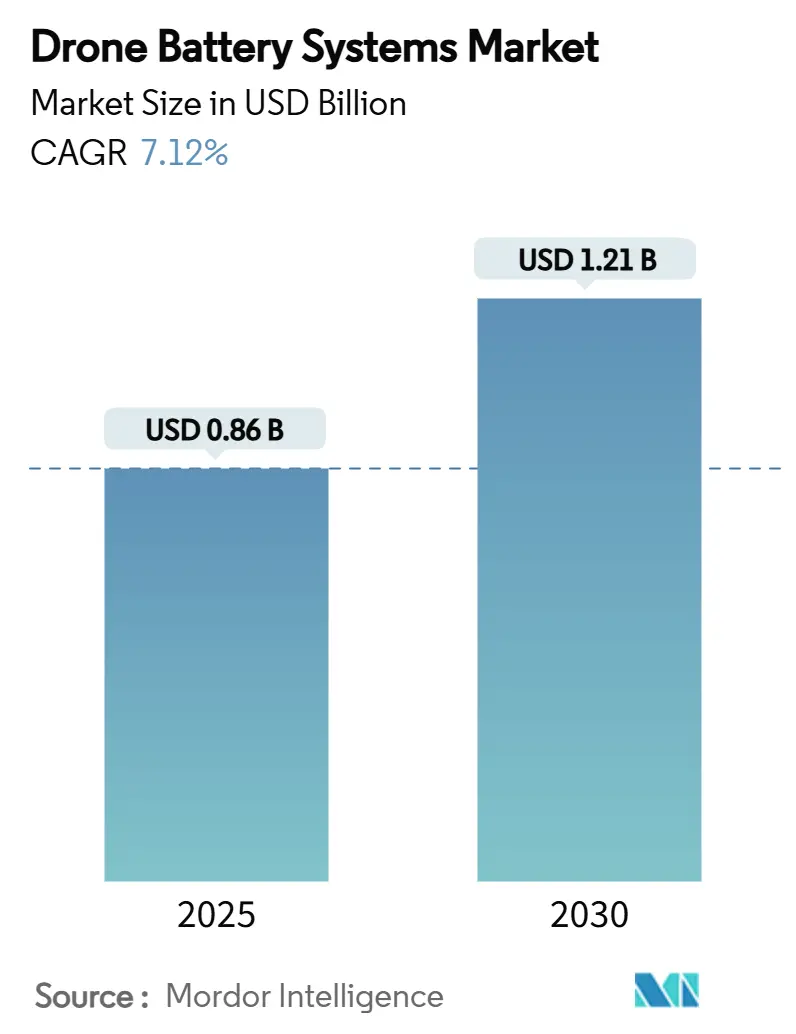

| Market Size (2025) | USD 0.86 Billion |

| Market Size (2030) | USD 1.21 Billion |

| Growth Rate (2025 - 2030) | 7.12% CAGR |

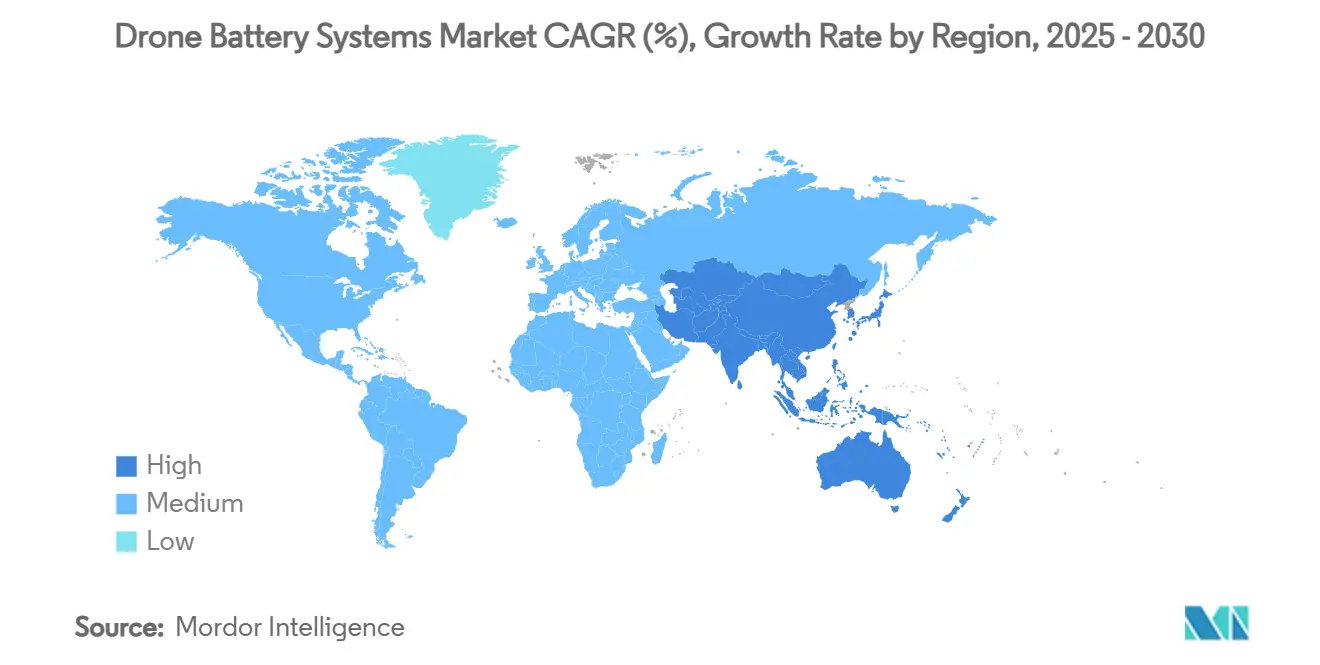

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

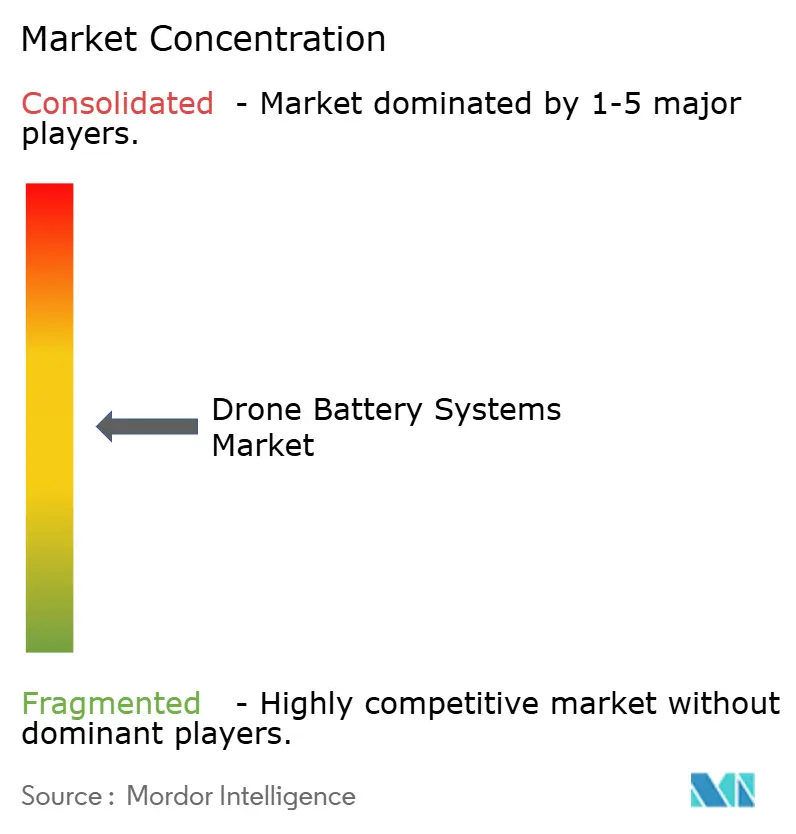

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drone Battery Systems Market Analysis by Mordor Intelligence

The drone battery systems market size is USD 0.86 billion in 2025 and is forecasted to reach USD 1.21 billion by 2030, reflecting a 7.12% CAGR. This advance stems from commercial operators demanding higher-energy solutions that support routine beyond-visual-line-of-sight (BVLOS) missions, which extend flight times two-to-three-fold over legacy designs. Component miniaturization, silicon-anode breakthroughs, and vertical integration across Asian supply chains accelerate cost declines per watt-hour, widening adoption across imaging, agriculture, and logistics applications. Regulatory clarity in North America and Europe, combined with national postal projects in Asia-Pacific, pushes operators toward intelligent battery management systems that lower lifetime operating costs while meeting stricter airworthiness rules. Meanwhile, venture funding in lithium-sulfur (Li-S) and solid-state start-ups sharpens the competitive race to supply next-generation packs offering 450–500 Wh/kg gravimetric density.

Key Report Takeaways

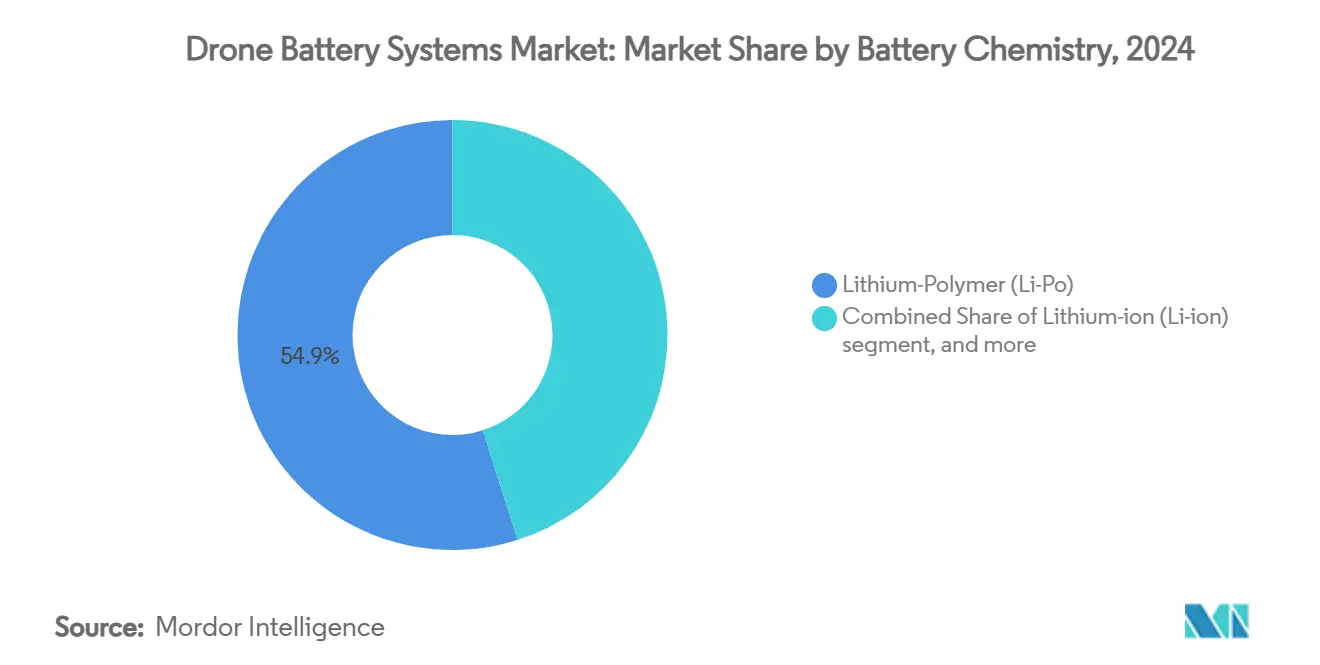

- By battery chemistry, lithium-polymer commanded 54.91% of the drone battery systems market share in 2024, while lithium-sulfur is projected to expand at a 9.41% CAGR through 2030.

- By capacity range, 3,001 to 10,000 mAh packs held 43.65% share of the drone battery systems market size in 2024; packs above 20,000 mAh are advancing at a 7.32% CAGR to 2030.

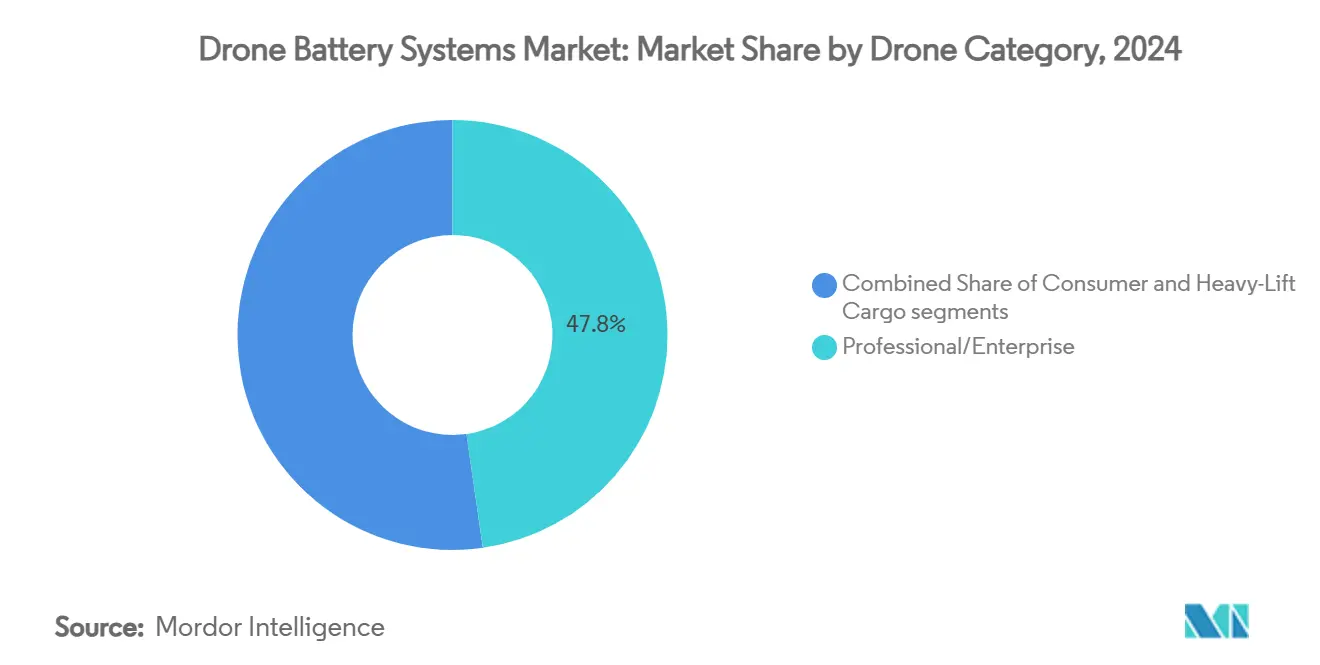

- By drone category, the professional and enterprise segment accounted for 47.76% of 2024 revenue, whereas heavy-lift cargo drones recorded the fastest 10.45% CAGR through 2030.

- By application, aerial imaging captured 40.45% of the current demand; logistics and last-mile delivery lead growth at a 10.37% CAGR until 2030.

- By geography, North America retained a 33.93% share in 2024, while Asia-Pacific is climbing at an 11.67% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Drone Battery Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling cost per watt-hour of high-energy lithium-ion cells | +1.20% | Global with APAC manufacturing advantages | Medium term (2-4 years) |

| Growing adoption of beyond-visual-line-of-sight (BVLOS) missions that require more than double the usual endurance | +1.80% | North America and EU regulatory leadership | Short term (≤ 2 years) |

| National postal fleets scaling e-commerce drone delivery | +1.50% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Rapid take-up of heavy-lift cargo drones that integrate hybrid fuel-cell powertrains | +1.10% | Global logistics hubs | Long term (≥ 4 years) |

| Surging investment in silicon-anode and lithium-sulfur battery start-ups | +0.90% | North America and EU innovation clusters | Long term (≥ 4 years) |

| Rising demand for quick-swap battery stations that maximise commercial drone fleet uptime | +0.70% | APAC manufacturing regions, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Falling Cost per Watt-Hour of High-Energy Lithium-Ion Cells

Cell prices continue to retreat because Chinese cathode producers standardize NMC 811 formulations that deliver 350 Wh/kg at scale.[1]Grepow, “20000 mAh Semi-Solid State High Energy Density Battery,” grepow.com Vertical integration from raw ore to finished pack trims logistics overhead, allowing professional operators to shave 15–20% off battery operating budgets. Mass production of 21,700 cylindrical formats offers higher packing efficiency, raising flight time without structural redesigns. As the cost per watt-hour sinks, fleet owners increasingly adopt redundancy-focused dual-battery architectures that enhance safety while extending mission duration.

Growing Adoption of BVLOS Missions Requiring Extended Endurance

EASA’s risk-based framework now greenlights regional BVLOS corridors, pushing commercial operators to specify batteries capable of 2+ hour sorties.[2]European Union Aviation Safety Agency, “EASA launches third release of Innovative Air Mobility Hub,” easa.europa.eu Agricultural enterprises covering 500-acre fields demand packs exceeding 20,000 mAh, and inspection firms embrace modular hot-swap units that minimize downtime in remote areas. Software-defined power management algorithms dynamically balance current draw, protecting cell health during prolonged hover or climb phases. The regulatory momentum is mirrored in the United States, where FAA exemptions for linear infrastructure inspection encourage larger-capacity packs.

National Postal Fleets Scaling E-Commerce Drone Delivery

Postal services in China, South Korea, and Singapore deploy fleets for dense urban parcels, prioritizing batteries that achieve 1,500+ charge cycles with consistent winter-weather performance. Automated sorting hubs integrate robotic battery swap stations, cutting turnaround time to under three minutes and boosting fleet utilization. Weight-optimized battery casings using carbon-fiber composites, free payload capacity for heavier packages, and enhancing economic viability. North American parcel operators track these developments and form joint ventures with pack suppliers to secure priority allocations.

Rapid Take-Up of Heavy-Lift Cargo Drones with Hybrid Powertrains

Fuel-cell–battery hybrids such as H3 Dynamics’ modules enable 200 kg payloads, with batteries supplying peak power during take-off and landing while hydrogen maintains cruise.[3]FuelCellsWorks News Desk, “H3 Dynamics to supply fuel cells for cargo VTOL,” fuelcellsworks.com The success of these demonstrators motivates battery makers to refine high-current discharge chemistries that complement fuel stacks. CATL’s condensed batteries reaching 500 Wh/kg hint at all-electric heavy-lift variants for routes under 300 km. Logistics providers value the simpler maintenance profile of battery-dominant systems, channeling R&D funding toward thermal management solutions for high-amp draws.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PFAS restrictions tightening on fluorinated electrolytes | -0.80% | EU leadership, expanding to North America | Short term (≤ 2 years) |

| Lithium-price volatility hitting pack makers’ margins | -1.10% | Global supply chain impact | Medium term (2-4 years) |

| Airport U-space rules capping battery weight classes | -0.60% | EU and North America aviation hubs | Short term (≤ 2 years) |

| Recycling logistics lag for small-format drone packs | -0.40% | Global with pressure in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PFAS Restrictions Tightening on Fluorinated Electrolytes

The EU’s proposed ban on per- and polyfluoroalkyl substances compels manufacturers to replace fluorinated salts and binders, adding 8–12% to near-term production costs. Test laboratories must verify thermal-runaway behavior under the revised UN-38.3 transport rules, lengthening certification cycles and delaying product launches by as much as nine months. Smaller cell assemblers face higher capital needs for pilot-scale solvent-recovery lines, and some risk of market exit if they cannot fund reformulation programs. North American regulators are weighing parallel limits, prompting global suppliers to pre-qualify non-fluorinated chemistries to keep cross-border sales uninterrupted. Early adopters that lock in long-term contracts for fluorine-free electrolytes may gain pricing leverage once the rules enter force in 2027.

Lithium-Price Volatility Hitting Pack Makers’ Margins

Spot prices for battery-grade lithium carbonate whipsawed between USD 9,000–12,000 per ton in early 2025, squeezing assemblers locked into fixed-price deals. Producers hedge exposure by signing recycling partnerships that recover 70–80% of lithium content, yet collection networks for spent drone packs remain nascent and fragmented. Price swings push some OEMs to dual-source chemistries, mixing lithium-polymer with emerging sodium-ion options to stabilize costs. Larger cell makers stockpile six-month inventories when prices dip, a tactic smaller firms cannot afford, widening competitive gaps. Futures-linked supply agreements are gaining favor, but their success depends on reliable recycling inflows that can buffer spot-market shocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: Lithium-Sulfur Emergence Challenges Polymer Dominance

Lithium-polymer (Li-Po) held 54.91% of the drone battery systems market share in 2024 because of well-established production lines and proven safety profiles. The segment’s incremental advances in energy density, now near 300 Wh/kg, sustain demand for professional-grade drones. Lithium-sulfur, projected to post a 9.41% CAGR, appeals to operators targeting 500 Wh/kg without rare-metal cathodes; early flight tests show three-hour sortie capability, signaling commercial readiness. Silicon-anode lithium-ion bridges current and next-generation offerings by delivering 20–30% energy gains while using existing assembly equipment. Fuel-cell hybrids serve niche heavy-lift missions where instant high-torque output pairs with hydrogen for cruise endurance.

Fleet owners value chemistry diversification to hedge raw-material risks. OEMs increasingly design powertrains that are agnostic to cell type, enabling seamless upgrades as new chemistries mature. This modularity reduces obsolescence concerns, a decisive factor in multiyear procurement cycles for the drone battery systems industry.

By Capacity Range: High-Capacity Systems Drive Extended Mission Profiles

Packs in the 3,001 to 10,000 mAh bracket represented 43.65% of 2024 shipments, balancing flight endurance with manageable recharge times for survey and imaging tasks. Modules above 20,000 mAh are set to grow at 7.32% CAGR as BVLOS regulation spreads, supporting corridor inspections and pipeline monitoring. Sub-3,000 mAh batteries cater to consumer drones where portability trumps duration, while 10,001 to 20,000 mAh models fill mid-range roles in precision agriculture.

Intelligent thermal control and active balancing unlock higher usable depth-of-discharge in large packs, extending cycle life. Operators deploying centralized swap stations note a 12% reduction in downtime when using standardized high-capacity formats, confirming the economic case.

By Drone Category: Heavy-Lift Segment Accelerates Despite Professional Dominance

Professional drones captured 47.76% revenue in 2024 thanks to diversified enterprise use cases. Heavy-lift cargo platforms, forecasted for a 10.45% CAGR, capitalize on automated freight and offshore resupply, each demanding exceptional energy reserves. Consumer drones remain stable, providing volume that sustains scale economies for cell producers.

Regulators increasingly require redundant energy paths on heavy-lift craft, often leading to dual-chemistry solutions—lithium-polymer for bursts and lithium-sulfur for cruise—thereby boosting per-airframe battery value. Component suppliers focusing on interoperability across categories are best placed to capture incremental demand in the drone battery systems market.

By Application: Logistics Growth Challenges Imaging Dominance

Aerial imaging retained a 40.45% share in 2024 through bread-and-butter roles in mapping, cinematography, and inspection. Logistics, advancing at 10.37% CAGR, benefits from reduced last-mile delivery costs and consistent regulatory progress on urban flight corridors. Precision agriculture continues steady expansion as farmers deploy multispectral sensors to optimize inputs, while emergency response uses specialized packs tolerant to temperature extremes.

Battery vendors differentiate via application-specific firmware that modulates discharge curves to prolong hover time during imaging or to supply rapid thrust changes for parcel delivery. Such tailored solutions underpin higher margins than commodity packs, reinforcing strategic R&D investment across the drone battery systems industry.

Geography Analysis

North America controlled 33.93% of sales in 2024, underpinned by robust commercial adoption and clear FAA guidelines that certify BVLOS waivers for infrastructure inspection. Domestic cell innovators such as Amprius collaborate with drone OEMs to field 400 Wh/kg silicon-anode packs, further anchoring regional leadership. Canada leverages its widespread resources sector to pilot long-range inspection flights, while Mexican logistics firms experiment with rural parcel corridors.

Asia-Pacific is projected to register the fastest 11.67% CAGR through 2030. China expects 3.7 million active drones by 2029, spurring enormous demand for intelligent batteries and localized recycling capacity.[4]ZIYAN UAS, “Global UAV market trends,” ziyanuas.com Japanese integrators deploy automation to offset labor shortages, adopting smart-pack grids that signal state-of-health in real time. India’s agri-tech initiatives subsidize drone purchases, encouraging domestic battery assemblers to standardize 6S-rated packs compatible with rugged field conditions.

Europe balances regulatory thought leadership with manufacturer agility. EASA’s frameworks for urban air mobility push pack makers toward higher safety margins, including mandatory over-temperature shutdown protocols. Germany and France prioritize industrial applications, while Nordic operators pioneer cold-weather electrolyte blends. The EU’s forthcoming battery passport scheme prompts detailed lifecycle tracking, accelerating investment in second-life and recycling ventures across the drone battery systems market.

Competitive Landscape

The marketplace exhibits moderate fragmentation; the top five suppliers account for an estimated 55–60% combined share, yielding ample room for niche specialists. DJI continues to bundle proprietary Smart Batteries with its aircraft, leveraging firmware locks that favor in-house chemistry. Grepow scales semi-solid production to 20 GWh annually, enabling OEM custom packs at sub-USD 120 kWh cost levels. Amprius secures long-term deals to supply 450 Wh/kg cells for premium enterprise platforms, signaling a shift toward co-development models.

Emerging entrants tackle technical white spaces. Factorial Energy supplies Avidrone with the first commercial solid-state cells, offering improved thermal abuse tolerance critical for autonomous operations.[5]DroneLife, “Factorial Energy ships solid-state batteries,” dronelife.com Lyten’s lithium-sulfur line reaches three-hour endurance in mid-size multi-rotors, marking a tangible leap over conventional packs. Power-as-a-service models gain traction as operators trade upfront capex for subscription-linked energy bundles that guarantee uptime and scheduled recycling.

Strategic maneuvers include vertical integration, joint R&D, and regional manufacturing expansion. CATL’s aviation unit breaks ground on a 5-GWh facility dedicated to high-energy semi-solid cells for export-controlled markets. At the same time, US firms collaborate with government grants to localize critical mineral supply chains. Collectively, these moves edge the drone battery systems market toward higher concentration without eliminating innovation pathways.

Drone Battery Systems Industry Leaders

SZ DJI Technology Co., Ltd.

Shenzhen Grepow Battery Co., Ltd.

RRC power solutions GmbH

Amprius Technologies, Inc.

EaglePicher Technologies, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: H3 Dynamics and XSun commenced co-development of a solar-hydrogen-electric tribrid drone targeting 12-hour missions.

- May 2025: Lyten unveiled US-manufactured Li-S packs, enabling three-hour flights and focusing on serving the UAV and satellite sectors.

- March 2025: Re/cell launched recycled-lithium battery blocks for 12-48 Ah drone systems.

- February 2025: Amprius Technologies, a developer of aircraft batteries, received a USD 15 million order for SiCore lithium-ion (Li-ion) battery cells from a yet-to-be-named drone manufacturer. The company anticipates starting deliveries in the latter half of 2025.

Global Drone Battery Systems Market Report Scope

| Lithium-Polymer (Li-Po) |

| Lithium-ion (Li-ion) |

| Lithium High-Voltage (LiHV) |

| Lithium-Sulfur (Li-S) |

| Fuel-Cell/Hybrid Battery Systems |

| Less than 3,000 mAh |

| 3,001 to 10,000 mAh |

| 10,001 to 20,000 mAh |

| Greater than 20,000 mAh |

| Consumer (Less than 2 kg) |

| Professional/Enterprise (2 to 25 kg) |

| Heavy-Lift Cargo (Greater than 25 kg) |

| Aerial Imaging and Survey |

| Precision Agriculture |

| Logistics and Last-Mile Delivery |

| Emergency Response |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Turkey | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Battery Chemistry | Lithium-Polymer (Li-Po) | ||

| Lithium-ion (Li-ion) | |||

| Lithium High-Voltage (LiHV) | |||

| Lithium-Sulfur (Li-S) | |||

| Fuel-Cell/Hybrid Battery Systems | |||

| By Capacity Range | Less than 3,000 mAh | ||

| 3,001 to 10,000 mAh | |||

| 10,001 to 20,000 mAh | |||

| Greater than 20,000 mAh | |||

| By Drone Category | Consumer (Less than 2 kg) | ||

| Professional/Enterprise (2 to 25 kg) | |||

| Heavy-Lift Cargo (Greater than 25 kg) | |||

| By Application | Aerial Imaging and Survey | ||

| Precision Agriculture | |||

| Logistics and Last-Mile Delivery | |||

| Emergency Response | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Turkey | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the drone battery systems market in 2025 and its growth outlook to 2030?

Revenue stands at USD 0.86 billion in 2025 and is projected to expand at an 7.12% CAGR, reaching about USD 1.21 billion by 2030.

Which battery chemistry is gaining momentum among commercial operators?

Lithium-sulfur (Li-S) packs post the fastest 9.41% CAGR as energy density advantages of up to 500 Wh/kg appeal to long-range missions.

Why is Asia-Pacific considered the fastest-growing geography?

China’s plan for 3.7 million active drones by 2029 and supportive government policies drive an 11.67% regional CAGR through 2030.

How do automated battery swap stations improve fleet economics?

Robotic docks exchange packs in under 90 seconds, boosting drone utilization by about 25% and cutting daily labor expenses.

What revenue share did professional and enterprise drones capture in 2024?

Professional and enterprise platforms accounted for 47.76% of 2024 sales.

Which regulatory shift is lifting demand for extended-endurance battery packs?

BVLOS approvals in North America and Europe require 2 hour-plus flight capability, pushing operators toward higher-capacity modules.

How are lithium price swings affecting battery suppliers?

Fluctuations between USD 9,000–12,000 per ton tighten margins, leading assemblers to hedge with recycling deals and diversify chemistries.

Page last updated on: