Driveline Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

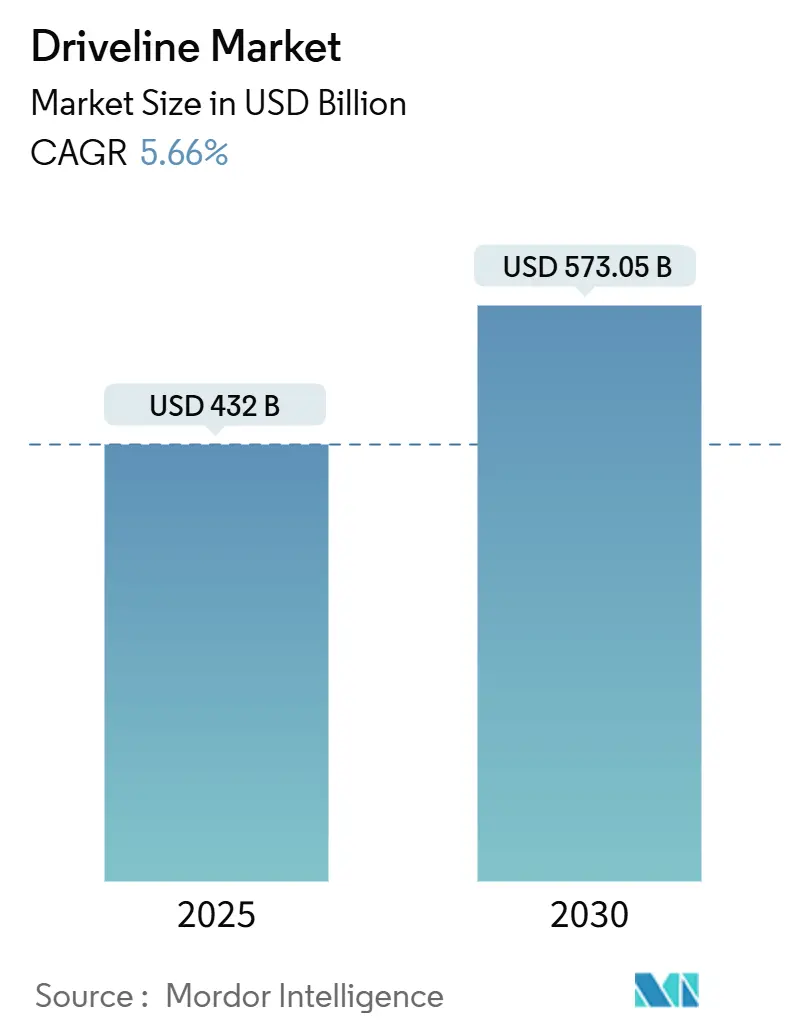

| Market Size (2025) | USD 432 Billion |

| Market Size (2030) | USD 573.05 Billion |

| Growth Rate (2025 - 2030) | 5.66% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

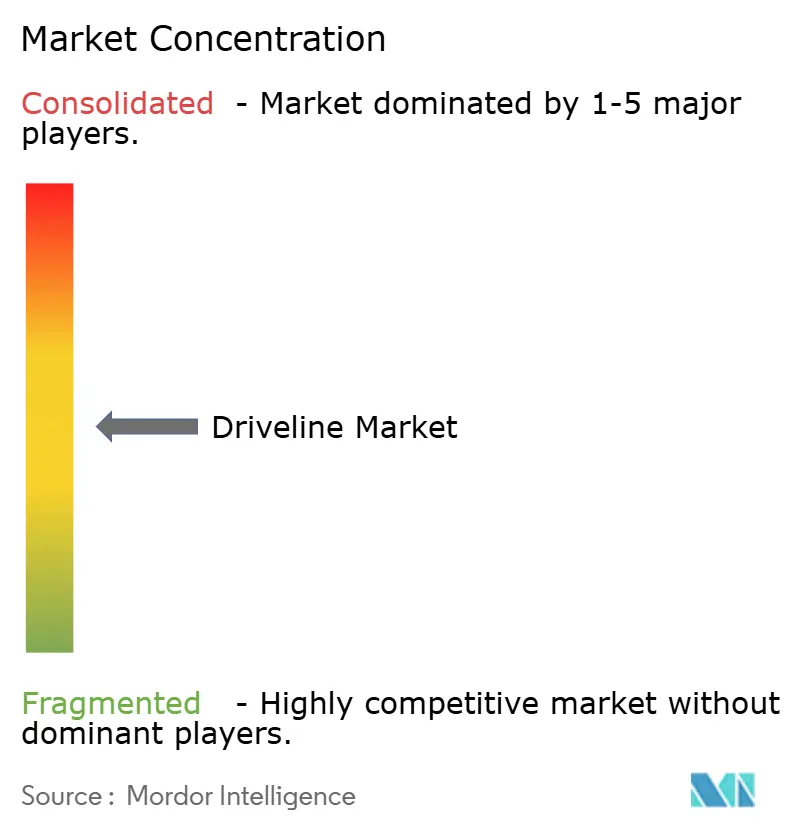

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Driveline Market Analysis by Mordor Intelligence

The driveline market size stands at USD 432 billion in 2025 and is projected to reach USD 573.05 billion by 2030, advancing at a 5.66% CAGR. Continued internal-combustion production in emerging economies and accelerating electrification in developed regions keep the driveline market on a solid expansion path. Strong demand for front-wheel drive architectures in cost-sensitive cars coexists with rapid all-wheel drive uptake in SUVs, while e-axles reshape system integration economics. Asia-Pacific leads volume growth on the back of China’s scale advantages and India’s capacity additions, whereas North America maintains value leadership in high-torque applications. Lightweight materials, modular e-axle platforms, and over-the-air software calibration together underpin the next wave of driveline market innovation.

Key Report Takeaways

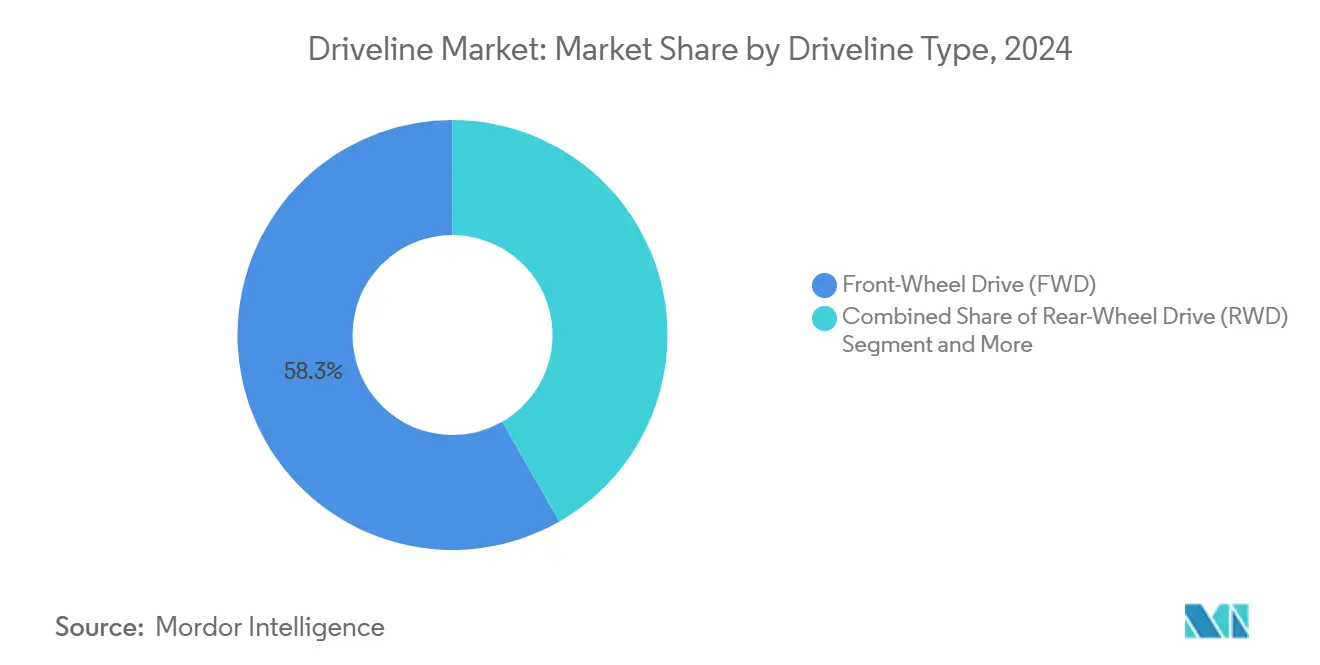

- By driveline type, front-wheel drive commanded 58.27% of driveline market share in 2024; all-wheel drive is forecast to expand at a 12.38% CAGR through 2030.

- By vehicle type, passenger cars captured 67.84% of the driveline market size in 2024, while light commercial vehicles are set to grow at a 15.46% CAGR between 2025 and 2030.

- By propulsion system, internal-combustion drivetrains held 71.12% share of the driveline market size in 2024, and electric systems are advancing at an 18.59% CAGR to 2030.

- By transmission, automatic units accounted for a 55.68% share of the driveline market size in 2024; dual-clutch transmissions are projected to post a 14.92% CAGR through 2030.

- By component, drive shafts led with 33.87% of driveline market share in 2024, whereas e-axles are poised for a 19.74% CAGR up to 2030.

- By material, steel retained 72.43% of the driveline market size in 2024; carbon-fiber components are expected to rise at a 22.51% CAGR during the same period.

- By distribution channel, OEM integration held 82.96% share of the driveline market size in 2024, while aftermarket revenues are projected to grow at a 13.08% CAGR to 2030.

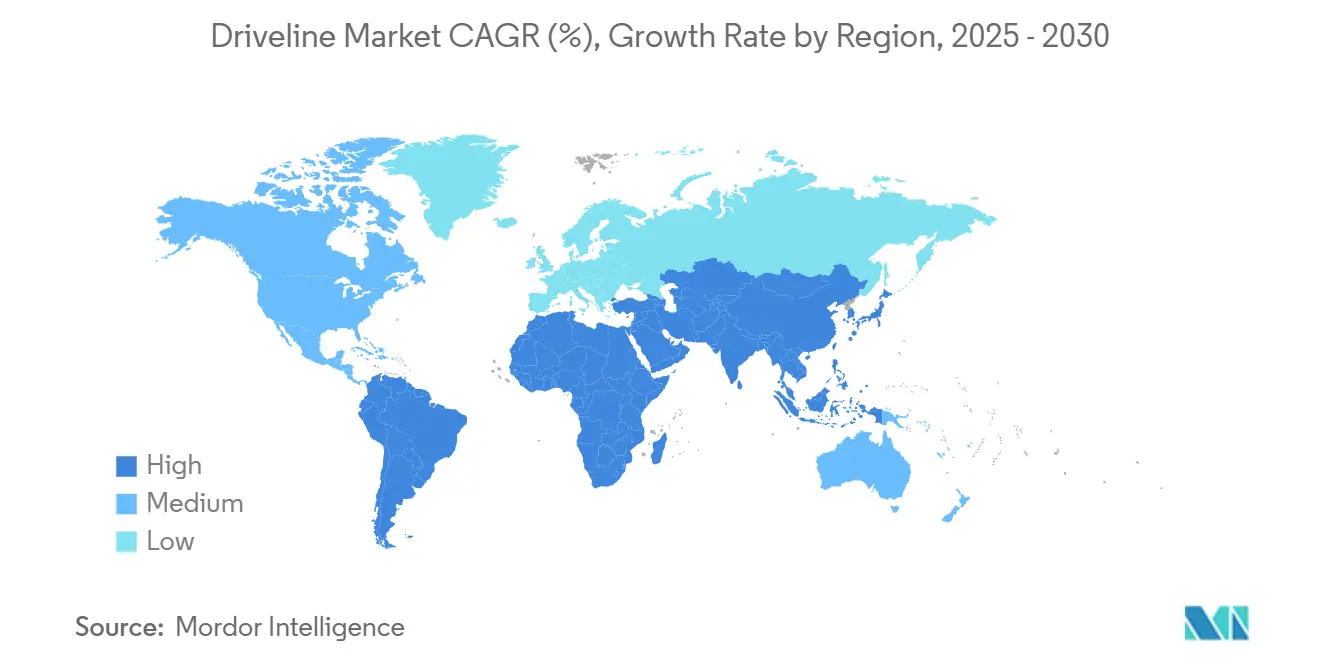

- By geography, Asia-Pacific accounted for 46.32% of the global driveline market in 2024, while the region is expected to grow at a 11.86% CAGR through 2030.

Global Driveline Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for AWD/4WD Vehicles in SUVs and Pickups | +1.8% | North America and Asia-Pacific Core, Spill-Over to Europe | Medium Term (2–4 Years) |

| Stringent Fuel-Efficiency and CO₂ Norms Driving Lightweight Drivelines | +1.2% | Global, With Early Gains in Europe, California, China | Long Term (≥ 4 Years) |

| Rapid Vehicle Production Expansion in Asia-Pacific | +0.9% | Asia-Pacific Core, Spill-Over to Middle-East and Africa | Short Term (≤ 2 Years) |

| Modular E-Axle Platform Standardization Across OEMs | +0.7% | Global | Medium Term (2–4 Years) |

| OTA Driveline-Software Calibration Boosting Redesigns | +0.4% | North America and EU, Early Adoption in Premium Segments | Medium Term (2–4 Years) |

| Commercial-Fleet Electrification Needs High-Torque Drivelines | +0.3% | Global, With Early Gains in Europe, California, China | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Growing Demand for AWD/4WD Vehicles in SUVs and Pickups

Consumer preferences are shifting decisively toward all-wheel and four-wheel drive configurations, particularly in the SUV and pickup truck segments, where traction control and off-road capability command premium pricing. This trend extends beyond traditional markets, with urban buyers increasingly valuing AWD systems for enhanced safety in adverse weather conditions. Ford's 2024 F-150 Lightning demonstrated that electric powertrains can deliver superior torque distribution compared to mechanical systems, achieving 0-60 mph acceleration in 4.0 seconds while maintaining a 10,000-pound towing capacity. Advanced torque vectoring technologies now enable manufacturers to optimize power delivery across individual wheels, creating differentiated driving experiences that justify higher margins. The integration of electronic stability control with AWD systems has become standard, reducing insurance costs and broadening market appeal beyond traditional truck buyers. Regulatory influence from IIHS safety ratings increasingly favors vehicles with advanced traction management systems, particularly in regions with seasonal weather variations.

Stringent Fuel-Efficiency and CO₂ Norms Driving Lightweight Drivelines

The European Union's Euro 7 emissions standards, effective 2025, mandate a 15% reduction in CO₂ emissions from passenger vehicles, compelling manufacturers to pursue aggressive weight reduction strategies across driveline components. Carbon fiber drive shafts now achieve 60% weight savings compared to steel equivalents while maintaining equivalent torque capacity, though at 3x higher material costs. Advanced aluminum alloys and magnesium castings are replacing traditional steel in differential housings and transmission cases, reducing overall driveline weight by 20-25% in premium applications. The Corporate Average Fuel Economy standards in the United States require fleet-wide efficiency improvements of 5% annually through 2030, driving adoption of lightweight materials across all vehicle segments. China's dual-credit policy for new energy vehicles creates additional incentives for weight optimization, as lighter conventional vehicles generate credits that offset electric vehicle production requirements.

Rapid Vehicle Production Expansion in Asia-Pacific

Manufacturing capacity additions across India, Thailand, and Vietnam are reshaping global driveline supply chains, with total regional production capacity increasing by 2.8 million units annually since 2024. Mahindra&Mahindra's[1]"Indian Enterprises Plan to Build USD 1.2 Billion Industrial Park in Pune, www.seetaoe.com. USD 1.2 billion investment in electric driveline manufacturing at its Pune facility represents the largest single commitment outside China. Japanese suppliers, including JTEKT and Aisin, are establishing integrated driveline component facilities across Southeast Asia to serve both domestic and export markets, reducing dependence on Chinese manufacturing. The region's cost advantages in steel processing and aluminum extrusion provide 15-20% manufacturing cost benefits compared to European production, attracting global OEMs to source driveline components locally. Government incentives across ASEAN countries for automotive manufacturing, including Thailand's EV 3.0 policy and India's PLI scheme, are accelerating capacity investments in next-generation driveline technologies.

Modular E-Axle Platform Standardization Across OEMs

Automotive manufacturers are converging on standardized e-axle architectures to achieve economies of scale while reducing development costs and time-to-market for electric vehicles. Schaeffler's modular e-axle platform, adopted by multiple European OEMs, demonstrates how common interfaces and mounting points enable cost reduction of 25-30% compared to bespoke designs. ZF's scalable e-axle family spans power outputs from 50kW to 300kW using common motor technologies and gear ratios, allowing manufacturers to address multiple vehicle segments with minimal engineering variations. This standardization extends to thermal management systems, where common coolant interfaces and heat exchanger designs reduce supplier complexity and inventory requirements. The trend toward platform sharing creates opportunities for tier-1 suppliers to achieve higher volumes while enabling smaller OEMs to access advanced electric driveline technologies without prohibitive development investments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Steel and Aluminum Prices | -1.8% | Global | Short Term (≤ 2 Years) |

| Skateboard EV Architectures Reducing Mechanical Driveline Count | -1.1% | Global, With Early Adoption in Premium EV Segments | Long Term (≥ 4 Years) |

| Thermal-Management Failures in High-Speed E-Axles | -0.6% | Global | Medium Term (2–4 Years) |

| Rare-Earth Magnet Supply Risk for E-Axle Motors | -0.5% | Global, With Highest Impact in Europe and North America | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Volatile Steel and Aluminum Prices

Raw material price fluctuations continue to pressure driveline manufacturers' margins, with steel prices experiencing 35% volatility since 2024 due to Chinese production policies and global trade tensions. Aluminum pricing has proven equally unstable, rising 28% in early 2024 before declining 15% by year-end as recycling capacity expanded. Manufacturers are implementing dynamic pricing mechanisms with OEM customers, though contract negotiations often lag commodity price movements by 6-12 months, creating margin compression during inflationary periods. The shift toward lightweight materials paradoxically increases exposure to price volatility, as carbon fiber and advanced aluminum alloys exhibit greater price sensitivity than traditional steel grades. Long-term supply agreements and vertical integration strategies are emerging as risk mitigation approaches, with Dana Incorporated establishing direct relationships with aluminum smelters to secure predictable pricing.

Skateboard EV Architectures Reducing Mechanical Driveline Count

Electric vehicle platforms increasingly adopt skateboard architectures that integrate motors, batteries, and control systems into the chassis, eliminating traditional driveline components, including drive shafts, differentials, and transfer cases. Tesla's structural battery pack design demonstrates how mechanical complexity can be reduced by 40% compared to adapted ICE platforms while improving crash safety and manufacturing efficiency. Rivian's quad-motor configuration eliminates the need for mechanical torque distribution systems, achieving superior performance while reducing part count and assembly complexity. This architectural shift threatens traditional driveline suppliers' core business models, forcing adaptation toward integrated electric solutions or risk market share erosion. The transition timeline varies by vehicle segment, with luxury EVs leading adoption while commercial vehicles maintain mechanical systems due to durability and serviceability requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Driveline Type: AWD Systems Drive Premium Positioning

All-wheel drive configurations are experiencing the fastest growth at 12.38% CAGR through 2030, despite front-wheel drive maintaining the largest market share at 58.27% in 2024. This growth reflects consumer willingness to pay premiums for enhanced traction and performance, particularly in SUV and crossover segments where AWD systems command USD 2,000-3,000 price premiums. Rear-wheel drive systems remain concentrated in luxury and performance applications, while four-wheel drive configurations serve specialized off-road and commercial applications. The integration of electronic torque vectoring with AWD systems enables manufacturers to differentiate driving dynamics while improving fuel efficiency through selective wheel engagement.

Continental's latest AWD coupling technology achieves 50-millisecond response times for torque distribution, enabling precise handling control that was previously impossible with mechanical systems. Front-wheel drive systems continue to dominate cost-sensitive segments, benefiting from packaging efficiency and manufacturing simplicity. The electrification trend is blurring traditional driveline distinctions, as electric motors enable instant torque delivery to any wheel configuration without mechanical complexity. Regulatory influence from NHTSA safety standards increasingly favors vehicles with advanced traction management capabilities, particularly in regions prone to adverse weather conditions.

By Vehicle Type: Commercial Electrification Accelerates

Passenger vehicles command 67.84% market share in 2024, though hybrid and electric vans represent the fastest-growing segment at 15.46% CAGR through 2030. This acceleration reflects commercial fleet operators' focus on total cost of ownership, where electric drivetrains deliver operational savings despite higher initial costs. Light commercial vehicles are experiencing rapid electrification adoption, particularly in urban delivery applications where range limitations are less constraining. Medium and heavy commercial vehicles maintain traditional mechanical drivetrains due to payload requirements and infrastructure limitations, though high-torque electric systems are gaining traction in specific applications.

Amazon's commitment to 100,000 Rivian delivery vans demonstrates the scale of commercial electrification demand, requiring specialized high-torque e-axle systems capable of frequent stop-start cycles. UPS reported 15% operational cost reduction using electric delivery vehicles in urban routes, driving broader fleet electrification initiatives across the logistics sector. The commercial segment's emphasis on durability and serviceability creates opportunities for modular driveline designs that enable field maintenance and component replacement. Compliance factors including urban emission zones in European cities are accelerating commercial vehicle electrification timelines beyond purely economic considerations.

By Propulsion System: Electric Growth Reshapes Supply Chains

Internal combustion engine drivetrains maintain 71.12% market share in 2024, though electric systems are expanding at 18.59% CAGR through 2030, creating fundamental shifts in supplier relationships and manufacturing requirements. Hybrid drivetrains serve as transitional technology, combining mechanical and electric systems to optimize efficiency across operating conditions. The complexity of hybrid systems requires sophisticated control algorithms and dual-path power delivery, increasing component count and manufacturing complexity. Electric drivetrains enable architectural flexibility impossible with mechanical systems, allowing manufacturers to optimize vehicle packaging and performance characteristics.

BorgWarner's integrated drive module combines electric motor, gearbox, and power electronics into a single assembly, reducing installation complexity while improving thermal management. The transition timeline varies significantly by region, with China leading electric adoption while emerging markets maintain ICE dominance due to infrastructure and cost considerations. Thermal management becomes critical in electric systems, requiring advanced cooling solutions to maintain performance and reliability under high-load conditions. The shift toward electric propulsion creates opportunities for software-defined vehicle architectures, where driveline performance can be optimized through over-the-air updates.

By Transmission Type: DCT Technology Gains Momentum

Automatic transmissions lead with 55.68% market share in 2024, though dual-clutch transmissions are experiencing 14.92% CAGR growth through 2030 as manufacturers seek to combine manual transmission efficiency with automatic convenience. Continuously variable transmissions serve specific efficiency-focused applications, while manual transmissions remain concentrated in cost-sensitive markets and performance applications. The electrification trend is reducing transmission complexity, as electric motors deliver optimal torque characteristics across their operating range without requiring multiple gear ratios.

ZF's 8-speed automatic transmission achieves 5% efficiency improvement over previous generations through advanced hydraulic control and optimized gear ratios, demonstrating continued innovation in conventional systems. Dual-clutch technology enables seamless power delivery during gear changes, improving both performance and efficiency metrics that appeal to premium vehicle buyers. The integration of hybrid systems requires sophisticated transmission control to coordinate electric motor assistance with internal combustion engine operation. Electric vehicles are driving the development of single-speed transmissions optimized for electric motor characteristics, simplifying manufacturing while maintaining performance requirements.

By Component Type: E-Axles Transform Integration

Drive shafts maintain the largest component share at 33.87% in 2024, though e-axles represent the fastest-growing category at 19.74% CAGR as manufacturers integrate electric motors, gearboxes, and power electronics into unified systems. Traditional differentials and axles continue serving mechanical drivetrain applications, while transfer cases remain specialized for four-wheel drive configurations. Transmission units are evolving toward simplified designs optimized for electric motor characteristics, reducing complexity and manufacturing costs.

Magna's e-axle production capacity expansion to 1.2 million units annually by 2026 demonstrates the scale of market transformation toward integrated electric systems. The integration trend extends beyond electric vehicles, with mechanical systems incorporating electronic control modules for enhanced performance and efficiency. Advanced materials, including carbon fiber and aluminum alloys, are enabling weight reduction across all component categories, supporting fuel efficiency improvements. The modularization of e-axle designs enables manufacturers to serve multiple vehicle segments with common platforms, reducing development costs and manufacturing complexity.

By Material: Carbon Fiber Drives Lightweighting

Steel maintains 72.43% market share in 2024 due to cost advantages and manufacturing familiarity, though carbon fiber represents the fastest-growing material at 22.51% CAGR through 2030. Aluminum adoption continues expanding in weight-sensitive applications, offering 40% weight reduction compared to steel while maintaining structural integrity. Carbon fiber applications remain concentrated in premium vehicles and performance applications due to material costs, though manufacturing scale improvements are reducing price premiums.

BMW's carbon fiber drive shaft production demonstrates mass manufacturing feasibility, achieving 60% weight reduction while maintaining equivalent performance characteristics. Advanced steel grades, including ultra-high-strength variants, enable weight reduction while maintaining cost competitiveness, serving mainstream vehicle applications. The material selection increasingly depends on total system optimization rather than individual component performance, requiring integrated design approaches. Recycling considerations are becoming important factors in material selection, particularly for aluminum and carbon fiber applications where end-of-life value recovery is significant.

By Distribution Channel: OEM Integration Dominates

Original equipment manufacturer channels command 82.96% market share in 2024, reflecting the critical integration requirements of modern driveline systems with vehicle control architectures. The aftermarket segment serves replacement and performance upgrade applications, though growing at a 13.08% CAGR as vehicle populations age and enthusiast modifications increase. The complexity of modern driveline systems, particularly electric and hybrid configurations, limits aftermarket opportunities due to integration requirements and safety considerations.

The OEM dominance reflects the increasing integration of driveline systems with vehicle stability control, traction management, and energy management systems that require factory-level calibration. Independent aftermarket suppliers focus on maintenance and replacement parts for aging vehicle fleets, while performance aftermarket serves specialized applications. The electrification trend may reduce aftermarket opportunities as electric drivetrains require less maintenance and have fewer serviceable components compared to mechanical systems. Regulatory influence from vehicle safety standards limits aftermarket modifications to driveline systems, particularly those affecting stability control and emission systems.

Geography Analysis

Asia-Pacific led the driveline market with 46.32% share in 2024, underpinned by China’s massive output, India’s 11.86% CAGR volume surge, and Japan’s precision-manufacturing base. China’s dual-credit regime accelerates EV driveline adoption, while its export of conventional cars sustains ICE component lines. India’s production-linked incentives finance local e-axle and lightweight-casting plants, encouraging suppliers to align with regional capacity plans. Thai and Indonesian policies catalyze integrated battery and driveline supply chains, achieving 15–20% cost advantages over Europe.

North America holds substantial value owing to high-content pickups and SUVs, where four-wheel drive and heavy-duty shafts raise per-vehicle driveline spend. The United States spearheads commercial-fleet electrification, creating demand for high-torque e-axles and robust thermal solutions. Canadian aluminum smelters and Mexican assembly clusters integrate under USMCA provisions, insulating the tri-nation supply base from distant freight shocks.

Europe pursues lightweight materials and strict Euro 7 compliance that drive carbon-fiber and e-axle uptake. Germany’s engineering ecosystem anchors modular-platform development, while France and Italy specialize in niche performance applications. Rising energy costs press suppliers to adopt closed-loop heat reuse in forging and casting shops. Although the regional market grows slower than Asia, its regulatory frontier sets global technical baselines.

Competitive Landscape

The driveline market remains moderately fragmented, with legacy mechanical specialists evolving toward electronics and software. GKN Automotive, Dana, and ZF command leading positions by bundling century-old gearing know-how with e-drive innovations. BorgWarner’s acquisition of Santroll’s motor business strengthens its vertical integration in magnets, windings, and inverters. ZF’s USD 800 million e-axle investment splits capacity between Germany and China, assuring localized supply for global OEM programs.

Strategic themes include platform standardization, vertical integration, and rare-earth mitigation. Dana’s Farasis battery-integration deal extends its value chain into thermal and energy-management systems. Software-defined drivelines gain mindshare as OTA-enabled torque updates promise incremental revenue streams. Supplier collaboration with semiconductor firms deepens, given inverter performance’s dependence on silicon-carbide chips.

New entrants specializing in axial-flux motors, forced-oil-spray cooling, or model-predictive control threaten incumbents by offering subsystem solutions that leapfrog traditional architectures. Still, high capital requirements and stringent ISO 26262 compliance temper disruption pace. Overall, supplier competitiveness hinges on delivering integrated mechanical-electrical-software solutions at automotive-grade quality.

Driveline Industry Leaders

-

GKN Automotive

-

Dana Incorporated

-

ZF Friedrichshafen AG

-

American Axle and Manufacturing

-

BorgWarner Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: ZF Friedrichshafen announced USD 800 million investment in electric driveline manufacturing capacity across Germany and China, targeting 2 million e-axle units annually by 2027. This expansion represents ZF's largest single commitment to electric drivetrain technology and positions the company to serve both European and Asian OEM customers with localized production capabilities.

- August 2024: Dana Incorporated completed acquisition of Farasis Energy's battery integration technology for USD 350 million, expanding capabilities in thermal management and power electronics for e-axle applications. The acquisition enables Dana to offer complete electric driveline solutions including battery cooling and energy management systems.

Global Driveline Market Report Scope

| Front-Wheel Drive (FWD) |

| Rear-Wheel Drive (RWD) |

| All-Wheel Drive (AWD) |

| Four-Wheel Drive (4WD) |

| Passenger Vehicles |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Internal Combustion Engine (ICE) |

| Electric Drivetrain |

| Hybrid Drivetrain |

| Manual Transmission |

| Automatic Transmission |

| Continuously Variable Transmission (CVT) |

| Dual-Clutch Transmission (DCT) |

| Drive Shafts |

| Differentials |

| Axles |

| Transfer Cases |

| Transmission Units |

| Steel |

| Aluminum |

| Carbon Fiber |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Driveline Type | Front-Wheel Drive (FWD) | |

| Rear-Wheel Drive (RWD) | ||

| All-Wheel Drive (AWD) | ||

| Four-Wheel Drive (4WD) | ||

| By Vehicle Type | Passenger Vehicles | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Propulsion System | Internal Combustion Engine (ICE) | |

| Electric Drivetrain | ||

| Hybrid Drivetrain | ||

| By Transmission Type | Manual Transmission | |

| Automatic Transmission | ||

| Continuously Variable Transmission (CVT) | ||

| Dual-Clutch Transmission (DCT) | ||

| By Component Type | Drive Shafts | |

| Differentials | ||

| Axles | ||

| Transfer Cases | ||

| Transmission Units | ||

| By Material | Steel | |

| Aluminum | ||

| Carbon Fiber | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the driveline market in 2025 and how fast will it grow?

The driveline market size reaches USD 432 billion in 2025 and is set to expand at a 5.66% CAGR to 2030.

Which driveline layout is gaining share the fastest?

All-wheel drive systems record the highest growth, projected at a 12.38% CAGR through 2030 on the back of SUV popularity.

Why are e-axles important for future vehicle platforms?

E-axles integrate motor, gearbox, and power electronics, reducing component count and enabling skateboard EV architectures that lower production cost and weight.

What impact do CO₂ regulations have on driveline materials?

Regulations such as Euro 7 encourage automakers to replace steel with carbon fiber and aluminum, trimming driveline weight by up to 60% in some components.

Which region currently leads the driveline market?

Asia-Pacific holds 46.32% share thanks to China’s vast production scale and India’s rapidly expanding capacity.

How are driveline suppliers managing rare-earth magnet risk?

Companies are investing in ferrite and reluctance motor technologies, diversifying sourcing to Vietnam and Australia, and designing magnet-reduced architectures.

Page last updated on: