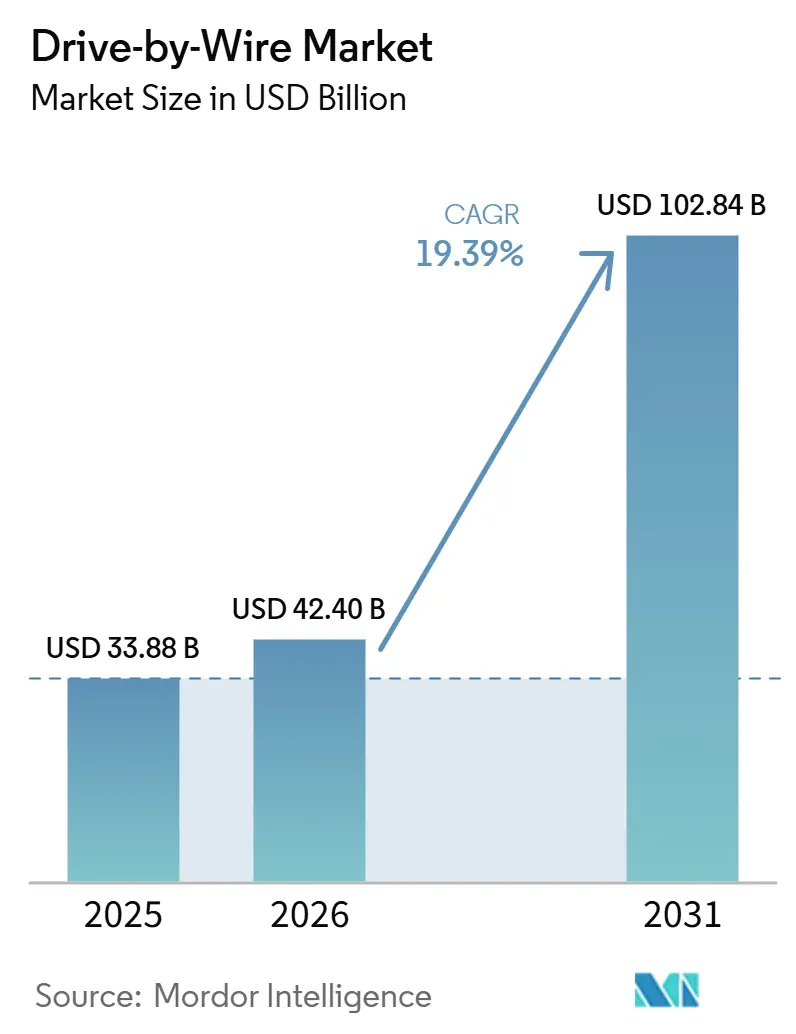

Drive-by-Wire Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 42.40 Billion |

| Market Size (2031) | USD 102.84 Billion |

| Growth Rate (2026 - 2031) | 19.39% CAGR |

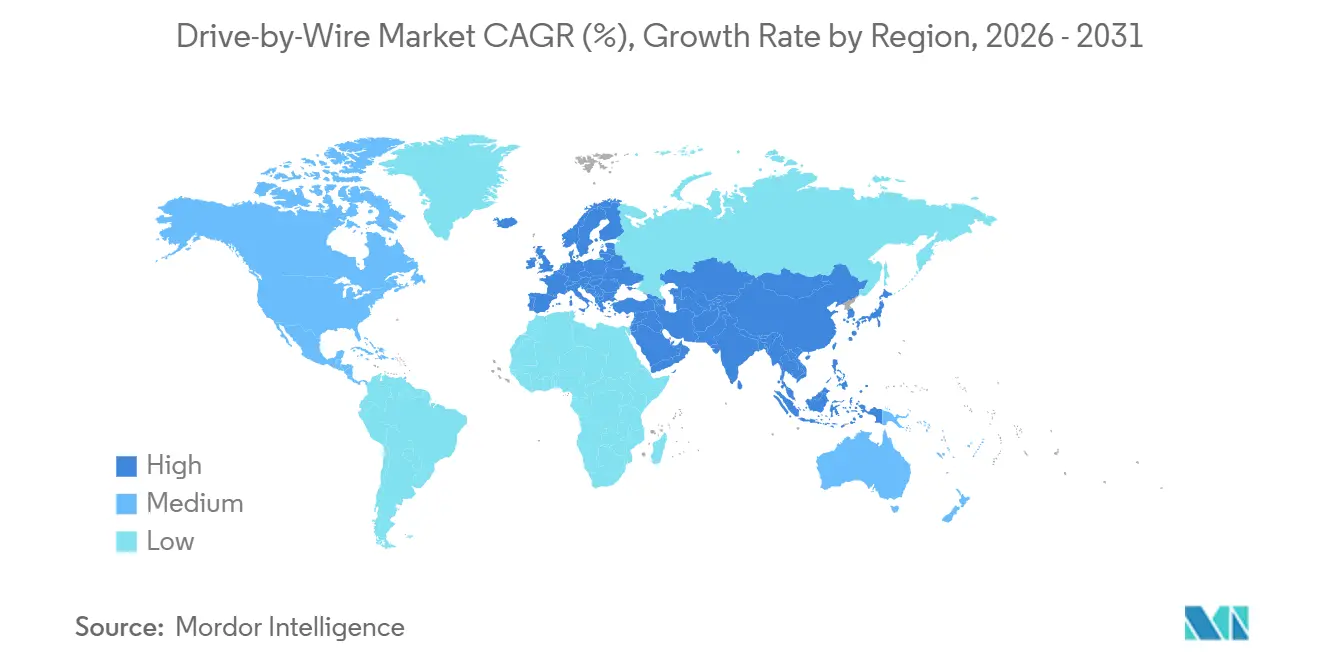

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

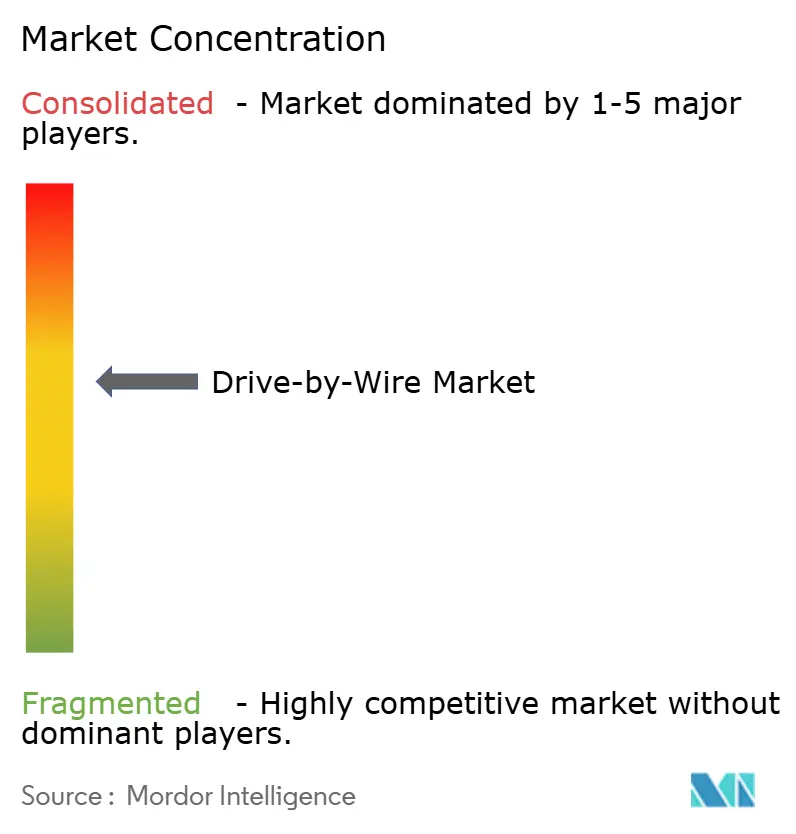

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drive-by-Wire Market Analysis by Mordor Intelligence

The drive-by-wire market size is projected to be USD 33.88 billion in 2025, USD 42.40 billion in 2026, and reach USD 102.84 billion by 2031, growing at a CAGR of 19.39% from 2026 to 2031. Near-term acceleration reflects a synchrony of strict zero-emission rules, maturing ISO 26262 ASIL-D certification pathways that tame functional-safety risk, and zonal electrical topologies that trim wiring-harness weight by up to 40%. China's GB 17675-2025, set to take effect in July 2026, will phase out mechanical steering columns, paving the way for the widespread adoption of steer-by-wire technology. This move also hints at similar reforms in Europe and North America, anticipated within the next two years. Platforms for battery electric vehicles (BEVs) are driving heightened demand. These platforms do away with components like vacuum boosters, throttle bodies, and hydraulic pumps. This not only reduces the bill of materials for each vehicle but also harnesses significant regenerative braking benefits. Tier-1 suppliers, who have proactively integrated cybersecurity and functional safety measures, are reaping the rewards. As OEMs aim to streamline sourcing and cut validation lead times, these suppliers are securing multi-year contracts.

Key Report Takeaways

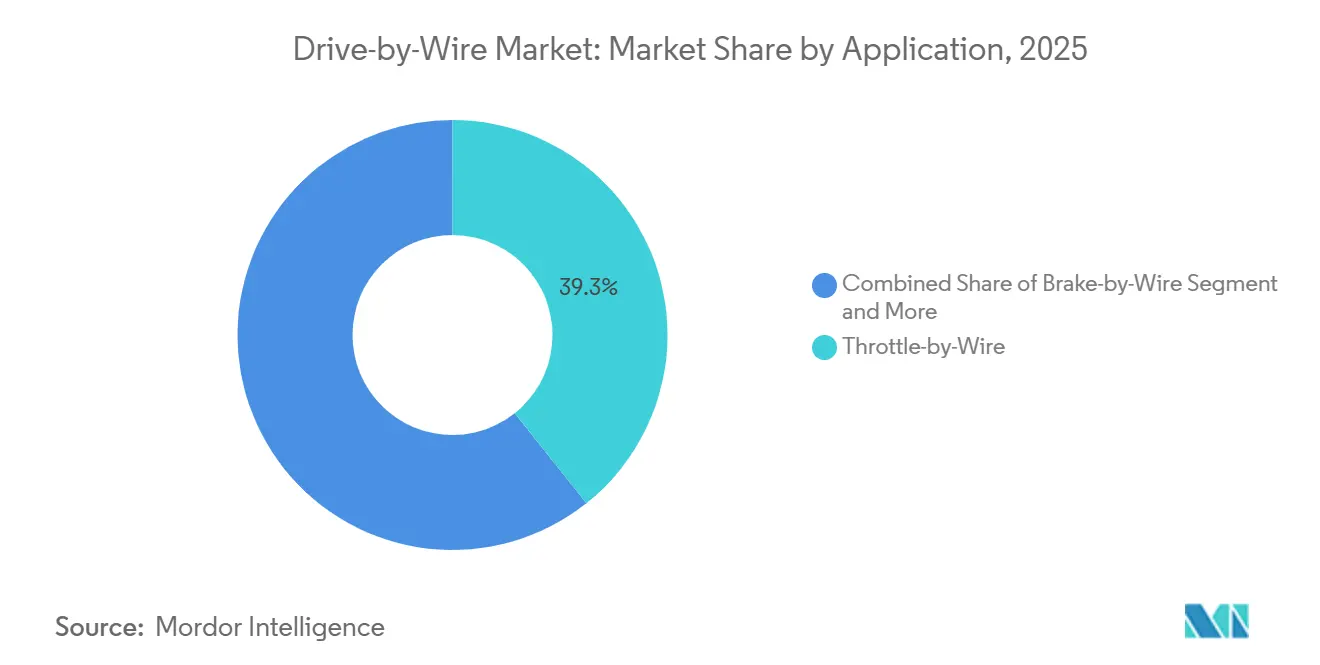

- By application, throttle-by-wire led with 39.25% of the drive-by-wire market share in 2025, while steer-by-wire is forecast to register the fastest CAGR at 21.33% through 2031.

- By vehicle type, passenger cars accounted for 69.11% of 2025 volume, while medium and heavy commercial vehicles are projected to post a 20.15% CAGR through 2031.

- By propulsion, internal-combustion vehicles retained 64.28% share in 2025, whereas battery electric vehicles are forecast to rise at a 21.64% CAGR.

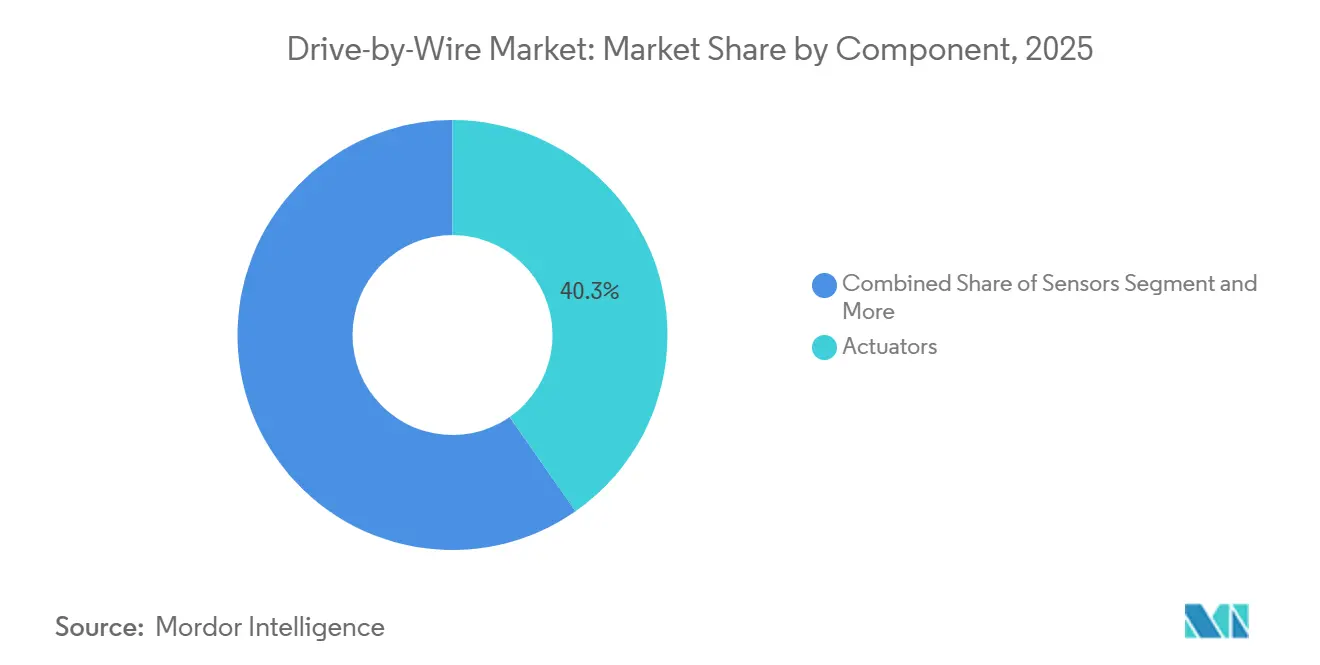

- By component, actuators accounted for 40.33% revenue in 2025, yet electronic control units are expected to grow at a 20.47% CAGR through 2031.

- By actuation technology, electromechanical accounted for a 59.41% share in 2025 and is set to grow at a 19.85% CAGR.

- By geography, Asia-Pacific accounted for 38.06% share in 2025, while Europe is set to expand at a 20.81% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Drive-by-Wire Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADAS and Autonomous Driving Growth | +4.2% | Global; early concentration in China, Germany, and the United States | Medium term (2-4 years) |

| Rising EV Platform Penetration | +3.8% | Asia-Pacific core with spill-over to Europe and North America | Medium term (2-4 years) |

| Weight-Reduction and Fuel-Efficiency | +2.5% | North America, Europe, and China | Long term (≥ 4 years) |

| Cyber-Secure Fail-Operational Architectures | +2.1% | Global; led by UNECE WP.29 signatories | Short term (≤ 2 years) |

| Architectures ReducingHarness Length | +1.9% | North America and Europe; broadening to Asia-Pacific | Medium term (2-4 years) |

| Rare-Earth-Free Motor Directives | +1.3% | Europe with technology transfer to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of ADAS and Autonomous Driving

Level 3+ automation needs deterministic sub-10-millisecond control loops that mechanical linkages cannot meet, making drive-by-wire foundational for future driverless capability. Mercedes-Benz embedded steer-by-wire in the EQS in 2026 and cut urban steering effort significantly. China’s GB 17675-2025 mandates redundancy and deletes the steering column, creating a global precedent [1]“GB 17675-2025,” Ministry of Industry and Information Technology, gbstandards.org. NIO ET9 and XPENG GX marry LiDAR-based path planning with autonomous lane changes, executing them without driver input. UNECE is drafting mirrorless regulations contingent on steer-by-wire redundancy, which would extend BEV driving range by up to 12 kilometers per charge.

Rising EV Platform Penetration

BEV architectures eliminate hydraulic and pneumatic components, making way for brake-by-wire, throttle-by-wire, and integrated power electronics, thereby reducing curb weight. BYD showcased an electro-mechanical brake-by-wire system that improves energy recuperation and significantly reduces brake dust emissions. Toyota’s 2026 RAV4 integrates shift-by-wire technology with electronically controlled brakes, enhancing energy recovery during city driving [2]“RAV4 2026 Specifications,” Toyota Motor Corporation, toyota.com. ZF secured a contract in 2025 for integrated brake control spanning millions of vehicles, underscoring OEM demand for prefabricated BEV chassis modules. China's Phase IV fuel-consumption regulations incentivize regenerative braking, steering local OEMs towards brake-by-wire systems, especially ahead of similar incentives set to roll out in the United States and EU.

Weight-Reduction and Fuel-Efficiency Mandates

NHTSA’s CAFE program for model years 2027-2031 requires a 2% annual increase in fleet efficiency, resulting in a reduction in vehicle mass [3]“CAFE Standards MY 2027-2031,” NHTSA, nhtsa.gov. The drive-by-wire system replaces heavy steel cables with lightweight electronics and software, achieving significant weight reduction. Euro 7 durability tests over long distances show a preference for electronic actuation, which sidesteps hydraulic seal degradation. Japan's Mobility DX Strategy allocates substantial funding to assist OEMs in transitioning to software-defined platforms, with drive-by-wire technology at the forefront. Meanwhile, legacy hydraulic suppliers are shedding low-margin lines and acquiring middleware firms, recognizing that profit margins are now concentrated in software.

Cyber-Secure Fail-Operational E/E Architectures

UNECE WP.29 cybersecurity and software update rules became mandatory in 2024 and push OEMs to implement intrusion detection and secure OTA pipelines. ISO/SAE 21434 cyber rules must coexist with ISO 26262 ASIL-D functional safety, doubling validation effort and lengthening programs by up to 18 months. South Korea, China, and India now harmonize with these global frameworks, ending the practice of regional architectures. Infineon’s XENSIV sensor line embeds hardware security modules and ASIL-D compliance at the die, trimming integrator workload by up to 40%. OEMs respond by bundling actuators, sensors, ECUs, and software into a single contract to shift certification risk upstream to Tier-1 partners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| System Cost and Validation Complexity | -2.7% | Global with pressure in cost-sensitive A/B segments | Short term (≤ 2 years) |

| Functional-Safety Certification Barriers | -1.8% | Global, stricter in Europe and China | Medium term (2-4 years) |

| Scarcity of ISO-26262 Engineers | -1.2% | North America and Europe with emerging gaps in Asia | Medium term (2-4 years) |

| Limited Aftermarket Service Readiness | -0.9% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High System Cost and Validation Complexity

Steer-by-wire systems add a significant premium per vehicle, while brake-by-wire systems also increase costs. These expenses represent a notable markup on A- and B-class cars, which account for a substantial share of global automotive output. Compliance with ISO 26262 ASIL-D standards requires extensive testing, including fault injection and multi-million-kilometer evaluations, resulting in considerable engineering costs per vehicle platform. While IPG Automotive has reduced testing time by virtualizing actuator dynamics, adoption of this approach remains limited to top-tier suppliers. Infineon's one-chip sensors have successfully reduced the bill of materials, and ZF's modular platform shares a high percentage of parts across different vehicle classes, indicating a potential cost reduction in the medium term.

Functional-Safety Certification Barriers

In China, a limited number of accredited labs are authorized to audit ISO 26262, leading to lengthy queues that delay product launches. Faced with high certification costs, many smaller Tier-2 firms are choosing to exit the field. This trend is hastening consolidation, with industry giants like Bosch, Continental, and ZF reaping the benefits. By 2027, Europe’s new Machinery Regulation will broaden safety mandates to encompass construction and agricultural machinery. This expansion is poised to spark a second wave of audits, potentially overburdening the already stretched assessor capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Steer-by-Wire Captures Autonomy Premium

Throttle-by-wire dominated the drive-by-wire market with 39.25% share in 2025. Steer-by-wire accounted for a rising share of the drive-by-wire market and is projected to post a 21.33% CAGR through 2031, as OEMs need column-free cabins for Level 3 automation. In a significant move, Mercedes-Benz integrated the technology into its EQS model set for release in 2026. Meanwhile, several Chinese automakers have planned substantial production capacity for the years 2026-2027. As the adoption of brake-by-wire technology gains momentum, ZF has secured a major order, signaling strong supplier confidence in sustained long-term volumes.

Technologies like shift-by-wire and park-by-wire have already found their way into mainstream vehicles. For instance, Toyota's RAV4, scheduled for 2026, features a reduced tunnel height, enhancing legroom for passengers. While suspension-by-wire remains a niche offering, BYD's demonstration of its performance advantages suggests a potential for wider adoption as costs decrease. Looking ahead, integrated chassis control is set to revolutionize the industry by merging steering and braking systems. This innovation not only reduces the hardware count but also paves the way for mid-priced sedans to achieve Level 3 autonomy by the end of the decade.

By Vehicle Type: M&HCV Electrification Unlocks Commercial Adoption

Passenger cars accounted for 69.11% of the drive-by-wire market share in 2025. Yet, medium- and heavy-duty commercial vehicles will expand at a 20.15% CAGR as electric trucks pursue regenerative braking range boosts. Volvo and Daimler prototypes cut turning circles and clear room for extra batteries once columns vanish.

Light commercial vehicles operate at slower speeds because fleets prize low acquisition costs. However, the Ford E-Transit and Mercedes eSprinter now include brake-by-wire to recover energy during stop-and-go duty. Off-highway vehicles are testing steer-by-wire to support remote control during long shifts and will face mandatory functional-safety rules after Europe enacts its Machinery Regulation in 2027.

By Propulsion Type: BEV Clean-Sheet Advantage

Internal combustion engine (ICE) vehicles held 64.28% share of the drive-by-wire market revenue in 2025. Battery electric vehicles (BEVs) are rapidly increasing their share of the drive-by-wire market and are forecast to grow at a 21.64% CAGR as they replace throttle bodies and hydraulic boosters. BYD's brake-by-wire system captures additional energy, while Toyota's RAV4 ECB system demonstrates efficiency during urban driving.

While hybrids still use some hydraulic components, which is slowing their adoption, the Euro 7 regulation offers a CO₂ credit for vehicles that use brake-by-wire systems to enhance energy regeneration. ZF's modular platform, compatible with BEV, HEV, and ICE programs, shares a significant portion of its components, enabling better scalability and pricing across all propulsion types.

By Component: ECUs Capture Software-Defined Value

Actuators led revenue with 40.33% in 2025, but ECU shipments will rise at a 20.47% CAGR as zonal controllers merge domain brains into five to seven high-compute nodes. GM’s Ultifi pushes steering feel updates remotely, removing workshop visits and turning software into a revenue service.

TE Connectivity and Sensata introduce multi-function packages, leading to the commoditization of sensors. Meanwhile, Elektrobit capitalizes on software licensing, generating annual revenue per vehicle. Wiring-harness companies are shifting to high-voltage Ethernet links, as zonal layouts significantly reduce copper usage.

By Actuation Technology: Electro-Mechanical Dominates on Efficiency

Electro-mechanical systems controlled 59.41% of the drive-by-wire market share in 2025 and will maintain momentum with a 19.85% CAGR thanks to lower energy draw than hydraulic options. ZF's brushless DC motor steering unit achieves high efficiency, while Schaeffler's switched-reluctance prototype not only complies with EU rare-earth limits but does so at a reduced cost.

While electro-hydraulic systems still dominate heavy trucks that require significant force, their market share is waning as electromechanical designs gain traction. In electric trucks, the absence of an engine-driven compressor results in reduced electro-pneumatic braking performance. By integrating inverter and DC-DC modules within the actuator housing, both volumes are minimized, and charging time is reduced, solidifying the dominance of electro-mechanical systems.

Geography Analysis

Asia–Pacific held 38.06% of 2025 revenue, led by China, where GB 17675-2025 removes the steering column from July 2026 and accelerates local steer-by-wire adoption. Japan allocates significant funding under its Mobility DX Strategy, steering domestic brands towards software-defined vehicles reliant on drive-by-wire technology. In 2024, South Korea's Hyundai Mobis secured ASIL-D certification for its integrated chassis controller, paving the way for both export and domestic expansion. While India is still in the nascent stages, the AIS-189 cybersecurity regulations are prompting OEMs to consider brake-by-wire systems for their 2027 launches.

Europe is projected to record a 20.81% CAGR through 2031, the fastest regional pace, as the Critical Raw Materials Act demands rare-earth-free actuators and sparks investment in ferrite and switched-reluctance motors. Mercedes-Benz debuted steer-by-wire in the EQS, and Volkswagen’s E³ 2.0 architecture consolidates ECUs to simplify future installations. The Ecodesign regulation adds traceability costs, nudging OEMs to scale volumes sooner to spread overhead.

North America trails in share yet gains from NHTSA CAFE rules that compel weight reductions best delivered by electronic actuation. GM’s Ultifi zone-controller plan and Ford’s E-Transit brake-by-wire standardization illustrate mainstream uptake. Canada aligns its MVSS efficiency rules with U.S. policy, while Brazil’s PROCONVE L8 emission standard and the UAE autonomous taxi initiative create smaller but growing demand pockets.

Competitive Landscape

In 2025, the top five suppliers—Bosch, Continental, ZF, Nexteer, and JTEKT—accounted for a significant share of the revenue, indicating a moderately concentrated market. Schaeffler and Hyundai Mobis, through vertical integration, managed to price their actuators lower than those of established players, while maintaining their profit margins. In a strategic move, JTEKT announced in February 2026 its commitment to steer-by-wire technology, transitioning from traditional hydraulic power steering. Meanwhile, Honda increased its stake in Hitachi Astemo in 2025 to ensure a secure supply chain.

As OEMs prioritize software readiness, competition has shifted focus from mere hardware performance. They now demand turnkey systems certified to standards such as ISO 26262 and ISO/SAE 21434, leading to accelerated launch schedules. Suppliers that integrate actuators, sensors, ECUs, middleware, and over-the-air infrastructure are reaping multi-platform contracts. In contrast, vendors offering stand-alone parts face relegation to Tier-2 status.

Supply chains are increasingly influenced by regional dynamics. While multinationals set up actuator plants in Jiangsu and Guangdong to cater to Chinese OEMs, they reserve ISO 26262-certified lines in Germany and Slovakia for their European clientele. Semiconductor giants like Infineon, NXP, and Renesas are innovating by merging motor-control, sensing, and cybersecurity functions onto single dies. This not only reduces validation costs but also opens doors for new system integrators.

Drive-by-Wire Industry Leaders

Robert Bosch GmbH

Continental AG

ZF Friedrichshafen AG

Nexteer Automotive

JTEKT Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Mercedes-Benz began EQS production with ZF steer-by-wire, enabling a dynamic 10-degree steering ratio and cutting driver effort by 40% in cities.

- March 2026: XPENG launched the GX crossover using Bosch steer-by-wire to target Level 4 automation while removing the steering column and reclaiming 8-12 liters of cabin volume.

- January 2026: IM Motors launched the LS9 Hyper in China, featuring a steer-by-wire standard, enhancing affordability.

- April 2025: Nexteer unveiled an electro-mechanical brake-by-wire module that discards hydraulic fluid and multiple mechanical parts, aiming at broad OEM adoption.

Global Drive-by-Wire Market Report Scope

The scope includes segmentation by application (throttle-by-wire, brake-by-wire, steer-by-wire, shift-by-wire, park-by-wire, and suspension-by-wire), vehicle type (passenger cars, light commercial vehicles, medium and heavy commercial vehicles, and off-highway vehicles), propulsion type (internal-combustion engine vehicles, hybrid electric vehicles, and battery electric vehicles), component (actuators, sensors, electronic control units, software and middleware, wiring-harness and connectors, and others), and actuation technology (electro-mechanical, electro-hydraulic, and electro-pneumatic). The analysis also covers regional-level segmentation, including North America, South America, Europe, and Middle East, and Africa. Market size and growth forecasts are presented by value in USD.

| Throttle-by-Wire |

| Brake-by-Wire |

| Steer-by-Wire |

| Shift-by-Wire |

| Park-by-Wire |

| Suspension-by-Wire |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Off-highway Vehicles |

| Internal-Combustion Engine Vehicles |

| Hybrid Electric Vehicles |

| Battery Electric Vehicles |

| Actuators |

| Sensors |

| Electronic Control Units (ECU) |

| Software and Middleware |

| Wiring-Harness and Connectors |

| Others |

| Electro-Mechanical |

| Electro-Hydraulic |

| Electro-Pneumatic |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Throttle-by-Wire | |

| Brake-by-Wire | ||

| Steer-by-Wire | ||

| Shift-by-Wire | ||

| Park-by-Wire | ||

| Suspension-by-Wire | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Off-highway Vehicles | ||

| By Propulsion Type | Internal-Combustion Engine Vehicles | |

| Hybrid Electric Vehicles | ||

| Battery Electric Vehicles | ||

| By Component | Actuators | |

| Sensors | ||

| Electronic Control Units (ECU) | ||

| Software and Middleware | ||

| Wiring-Harness and Connectors | ||

| Others | ||

| By Actuation Technology | Electro-Mechanical | |

| Electro-Hydraulic | ||

| Electro-Pneumatic | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the drive-by-wire market in 2031?

It is projected to reach USD 102.84 billion by 2031, expanding at a 19.39% CAGR.

Which application is growing fastest inside drive-by-wire?

Steer-by-wire is expected to record a 21.33% CAGR through 2031 due to its role in Level 3 autonomy and column-free cabin layouts.

Which region will grow fastest in drive-by-wire revenue?

Europe should grow at a 20.81% CAGR as rare-earth-free motor laws stimulate steer-by-wire investment.

What barrier most limits short-term penetration?

High system cost and complex ISO 26262 validation add up to USD 1,200 per vehicle and extend launch schedules by nearly two years, restraining budget-segment adoption.

Page last updated on: