Automotive Cylinder Liner Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 7.62 Billion |

| Market Size (2031) | USD 9.78 Billion |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

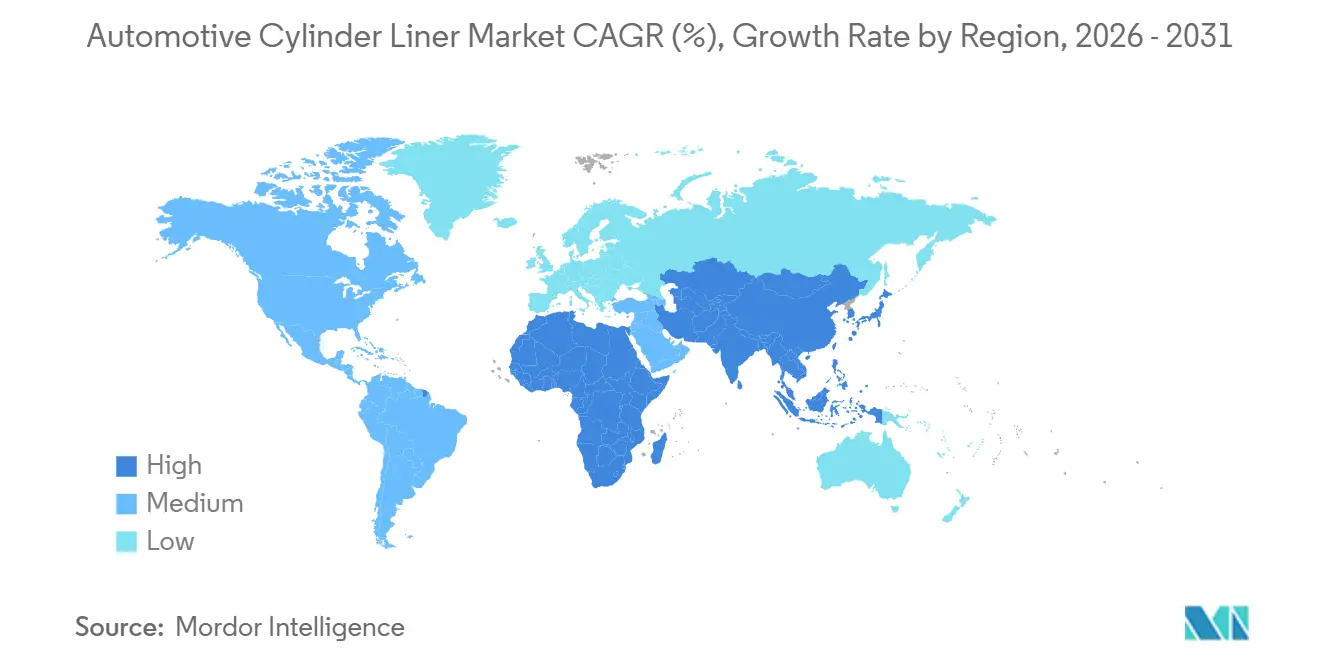

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Cylinder Liner Market Analysis by Mordor Intelligence

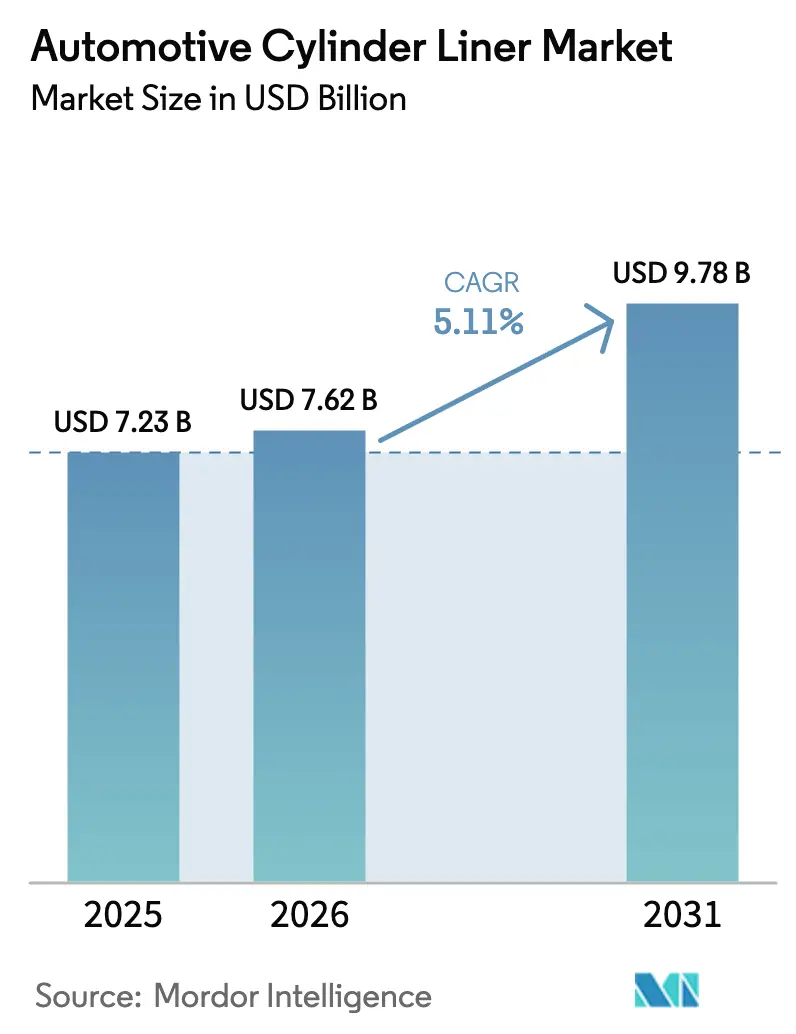

The automotive cylinder liner market size is expected to grow from USD 7.23 billion in 2025 to USD 7.62 billion in 2026 and is forecast to reach USD 9.78 billion by 2031, representing a 5.11% CAGR during the forecast period (2026-2031). This expansion stems from heavy-duty internal-combustion platforms that continue to dominate freight and off-highway equipment, even as electric powertrains chip away at passenger-car demand. Composite liners are outpacing traditional cast iron because their lower mass and superior thermal conductivity help engines meet increasingly stringent emissions limits. Inline configurations remain the volume anchor for cost-sensitive passenger and light commercial vehicles, whereas V-shaped layouts are gaining traction in premium and performance segments that prize power density. Finally, Asia-Pacific’s manufacturing momentum, Middle East and Africa’s localization mandates, and a brisk global remanufacturing sector all underpin steady liner consumption despite electrification headwinds.

Key Report Takeaways

- By material type, cast iron dominated the automotive cylinder liner market with 63.87% of the market size in 2025, while composite liners are poised to demonstrate a 9.96% CAGR through 2031.

- By manufacturing process, sand casting led with a 52.74% share of the automotive cylinder liner market in 2025; hydroforming is projected to expand at an 8.75% CAGR through 2031.

- By cylinder configuration, inline engines captured 70.82% of the automotive cylinder liner market share in 2025, while V-shaped engines are forecast to grow at a 6.51% CAGR through 2031.

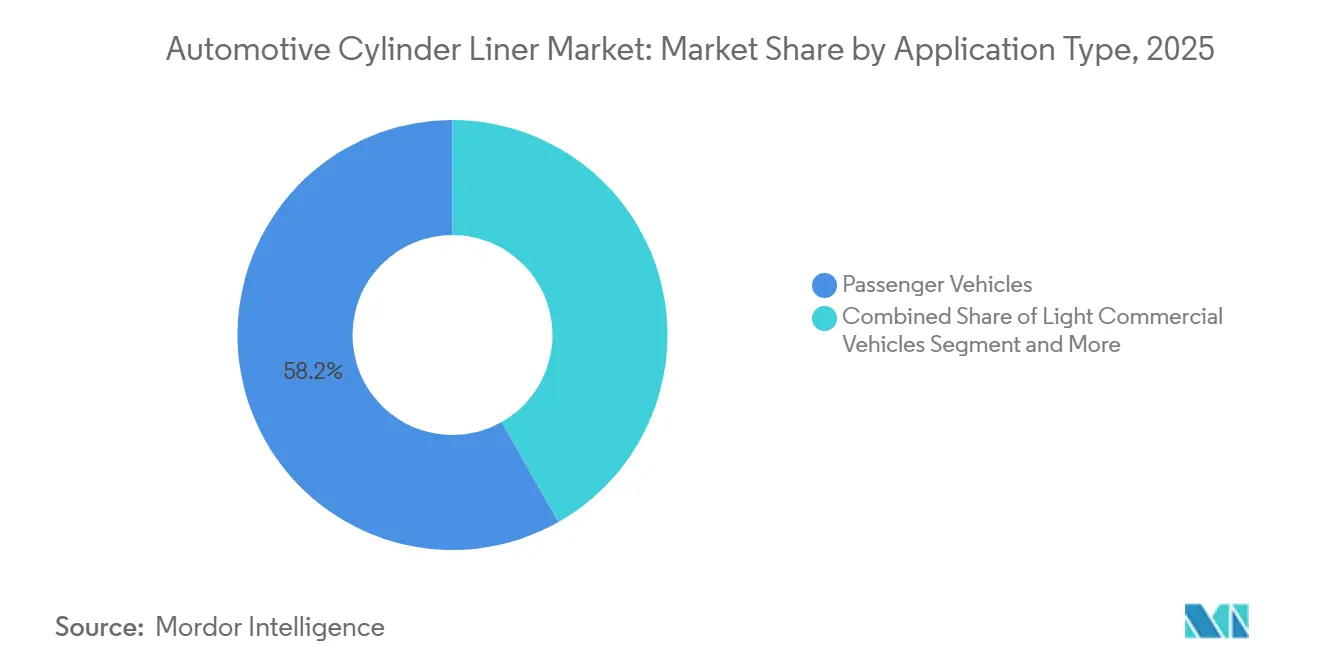

- By application type, passenger vehicles accounted for a 58.23% share of the automotive cylinder liner market in 2025. In contrast, medium- and heavy-duty vehicles are poised to register the fastest growth at a 7.64% CAGR through 2031.

- By surface treatment, honed liners held a 46.15% share of the automotive cylinder liner market in 2025, while nitrided liners are advancing at an 8.18% CAGR, supported by rising durability and wear-resistance requirements.

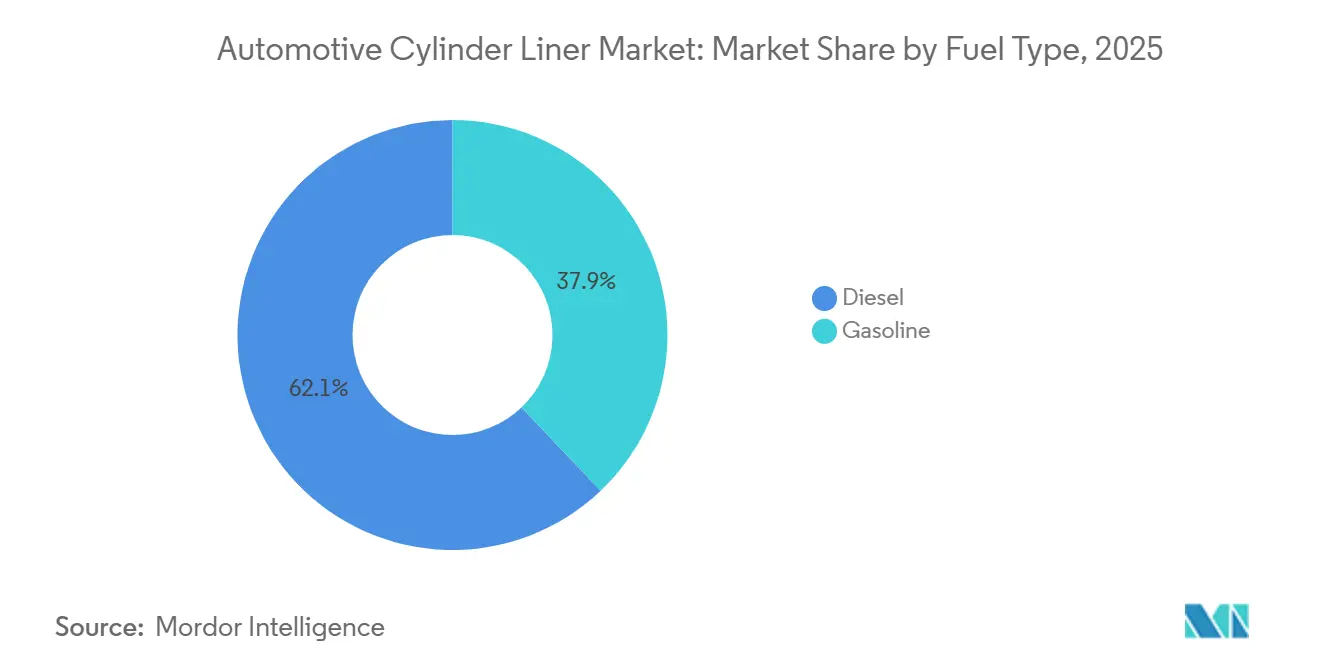

- By fuel type, diesel engines accounted for 62.14% of the automotive cylinder liner market size in 2025; gasoline applications are expected to grow at a 6.85% CAGR through 2031.

- By contact type, wet liners represented a 68.29% revenue share in 2025, while dry liners are projected to advance at a 5.47% CAGR, driven by passenger-car lightweighting strategies through 2031.

- By geography, Asia-Pacific accounted for 41.76% of the automotive cylinder liner market share in 2025, while the Middle East and Africa region is projected to witness the fastest growth at an 8.39% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Cylinder Liner Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification-Resistant Demand from Heavy-Duty ICE Engines | +1.8% | Global, with concentration in North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Tightening Emission Norms | +1.2% | Global, led by Europe and North America regulatory frameworks | Medium term (2-4 years) |

| Rapid Expansion of Remanufacturing and Aftermarket Engine Rebuilds | +0.9% | Asia-Pacific core, with spillover to Middle East and Africa and Latin America | Medium term (2-4 years) |

| Growth of Tier-3 Regional Foundries | +0.7% | South Asia and Southeast Asia, with export potential to Middle East and Africa | Long term (≥ 4 years) |

| Mainstream OEM Shift Toward Modular Engine Platforms | +0.6% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| Fleet Life-Extension Programs | +0.5% | Emerging markets in Asia-Pacific, Middle East and Africa, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification-Resistant Demand from Heavy-Duty ICE Engines

Freight, construction, agriculture, and marine equipment continue to rely on diesel or natural-gas powertrains because current battery chemistries cannot match the required range and uptime. The U.S. Environmental Protection Agency’s Medium- and Heavy-Duty Vehicle roadmap still permits high-efficiency combustion engines through 2040, protecting liner volumes for at least another decade. Volvo’s SuperTruck 2 demonstrated 49.9% peak brake thermal efficiency by pairing friction-reducing liner coatings with optimized combustion strategies. TRATON’s 13-liter Common Base Engine features composite liners to achieve 50% efficiency and has secured multi-year supply deals, solidifying the OEM's commitment to advanced ICE architectures.

Tightening Emission Norms Boosting Lightweight Composite Liners

Euro 7[1]"Euro 7: Deal on new EU rules to reduce road transport emissions," European Parliament, europarl.europa.eu rules, effective 2025, enforce more extended durability and lower NOx thresholds, pushing automakers toward aluminum-silicon liners reinforced with ceramics for superior heat transfer and dimensional stability. Federal-Mogul’s GOE330 compacted-graphite-iron liner, launched in 2024, reduces bore distortion by 27% at far lower cost than full composites and has been adopted by global heavy-duty OEMs. India’s forthcoming Bharat Stage VII standard will mirror these requirements, accelerating the adoption of composites in the market.

Rapid Expansion of Remanufacturing and Aftermarket Engine Rebuilds

Remanufactured engines cost 40-60% less than new assemblies and are priced 45-65% below OEM retail, creating sustained demand for liners in North America and Europe, where regulatory frameworks recognize remanufacturing as a key component of circular-economy infrastructure. U.S. light car and truck aftermarket sales surged in 2025, which will further drive the demand over the forecast period.

Growth of Tier-3 Regional Foundries in South and Southeast Asia

India, Vietnam, and Thailand have established themselves as significant hubs for low-cost automotive cylinder liner manufacturing. These countries are attracting global OEMs and component suppliers due to their competitive production capabilities. Labor costs in these regions are approximately 50–60% lower than those in similar facilities in Europe and North America, enabling the production of high-quality liners at reduced costs. Additionally, the development of local supply chains, advancements in industrial infrastructure, and supportive government policies are positioning these countries as preferred destinations for OEM sourcing and aftermarket production. This trend enables companies to improve their profit margins while maintaining stringent quality standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long-Term EV Adoption in Passenger Cars | -1.4% | Global, with accelerated impact in Europe, China, and California | Long term (≥ 4 years) |

| Volatile Ferrous Metal Prices | -0.8% | Global, with particular impact on cost-sensitive emerging markets | Short term (≤ 2 years) |

| Capital Intensity of Composite Liner Production Lines | -0.6% | Global, with higher barriers in emerging markets | Medium term (2-4 years) |

| OEM In-House Liner Manufacturing Trend | -0.4% | North America and Europe, with selective adoption in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Long-Term EV Adoption in Passenger Cars

The phase-out of ICE vehicles in Europe by 2035 and the implementation of California's Advanced Clean Cars II regulation are accelerating this transition. Leading automotive manufacturers, including Volkswagen, Stellantis, and General Motors, have committed to achieving 50–70% battery electric vehicle (BEV) production by 2030. Additionally, China's New Energy Vehicle (NEV) mandate requires 40% of vehicle sales to be electric or plug-in hybrids by 2030, further reducing ICE demand in the world's largest automotive market. In May 2024, Toyota, Subaru, and Mazda announced a joint initiative to develop compact, high-efficiency engines compatible with synthetic fuels. However, production volumes for these engines are expected to remain significantly lower than those of traditional ICE platforms.

Volatile Ferrous Metal Prices Eroding Supplier Margins

In the first half of 2025, iron ore prices showed significant volatility, falling from approximately USD 105 per metric ton in February to around USD 92 per metric ton in June. These price fluctuations introduced uncertainty for steelmakers and downstream automotive suppliers, making it more difficult to plan production costs, manage inventory, and negotiate multi-month contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Composite Liners Redefine Thermal Management

Cast iron retained 63.87% of the automotive cylinder liner market share in 2025 because of its low raw material cost and compatibility with existing tooling. Composite liners, however, are forecast to expand at a 9.96% CAGR through 2031, propelled by Euro 7 and EPA heavy-duty rules that penalize mass and reward thermal efficiency. The automotive cylinder liner market share for composites is expected to climb rapidly as Federal-Mogul’s GOE330 CGI product offers a mid-price, high-performance bridge solution. Fraunhofer IFAM data show that aluminum-matrix composites can trim engine weight by 20–30% and reduce fuel use by up to 3%, making them attractive for downsized, turbocharged gasoline units.

In parallel, MAHLE’s Monotherm liner integrates internal cooling passages, eliminating the need for separate water jackets and reducing block machining time by 15%. Yet, high capital expenditure—USD 15–20 million per composite line versus USD 5–8 million for cast-iron sand casting—still limits adoption among tier-3 foundries. Consequently, cast iron will remain the volume leader through 2031, while composites capture the bulk of incremental growth.

By Manufacturing Process: Hydroforming Gains on Precision Economics

Sand casting accounted for 52.74% of the automotive cylinder liner market share in 2025, as it effectively handles large-bore, heavy-duty liners at a low tooling cost. Hydroforming, which is advancing at an 8.75% CAGR through 2031, utilizes internal fluid pressure to shape thin-wall tubes and achieve tolerances of ±0.1 mm. Schuler’s 2025 modular cells lowered tooling investment by 30%, making hydroforming viable for mid-volume programs. In line with this shift, Cummins patented a profiled hydroformed liner geometry that withstands 10% higher peak pressures without reinforcing the block, enhancing the automotive cylinder liner market’s technology frontier.

CNC machining and high-pressure die casting still serve premium and lightweight niches, but hydroforming’s blend of accuracy and cost efficiency will erode sand casting’s share over the forecast horizon. Progressive OEMs view net-shape processes as indispensable for achieving Euro 7 durability with reduced mass.

By Cylinder Configuration: Inline Dominance Masks V-Shaped Premiumization

Inline engines accounted for 70.82% of the automotive cylinder liner market share in 2025 due to their simpler manufacturing and lower parts count. The configuration is central to modular platforms such as TRATON’s Common Base Engine, which standardizes liners across truck brands. Nevertheless, V-shaped units in premium SUVs and performance vehicles are projected to grow at a rate of 6.51% through 2031. Automakers such as General Motors and Ford apply plasma-spray coatings to V6 and V8 liners, cutting friction 10-12% while supporting cylinder deactivation strategies. The automotive cylinder liner market, therefore, sees a dual track: high-volume inline production coexisting with a lucrative, lower-volume V-segment that rewards advanced surfaces and materials.

The intricate liner geometry required by V engines to manage uneven heat gradients has led suppliers to adopt coated cast iron or hybrid wall constructions. Premium automakers are integrating these liners with advanced techniques, such as spray-boring or localized nitriding, to minimize oil consumption at high specific outputs. Additionally, rebuilders have identified recurring wear clusters in V engines, prompting the development of proprietary oversized liner programs. These programs aim to restore bore concentricity and enhance service life, particularly in heavy-haul applications.

By Application Type: Passenger Volume Meets Commercial Growth

Passenger vehicles represented 58.23% of the automotive cylinder liner market share in 2025. Medium- and heavy-duty vehicles are expected to grow at 7.64% through 2031, despite battery-electric vehicles' inability to match diesel's energy density for long-haul freight (with a range of more than 500 km) and payload capacity (more than 15 metric tons). Volvo's SuperTruck 2 program achieved a peak brake thermal efficiency of 49.9% using optimized liner coatings, while TRATON's Common Base Engine (13-liter modular platform) secures multi-year liner contracts with MAHLE and Tenneco. Light commercial vehicles, vans, and pickups weighing under 3.5 metric tons occupy a middle ground. Ford's Transit and Ram ProMaster retain diesel options in Europe and Latin America, sustaining wet-liner demand, while their North American variants increasingly adopt gasoline engines with dry liners to meet CAFE standards.

By commercial-vehicle production, India remained a key market in 2025, with Tata Motors, Mahindra & Mahindra, and Ashok Leyland among the top OEMs sustaining strong monthly deliveries and contributing to overall industry growth. China continued to dominate global heavy-duty vehicle output, with leading domestic manufacturers, including FAW, Dongfeng, and Sinotruk, driving production volumes. Off-highway applications including construction, agriculture, and mining maintained steady demand for durable engine components, with OEMs specifying serviceable designs to support long operational lifecycles in harsh environments.

By Surface Treatment: Nitriding Captures Durability Premiums

Honed surface treatments held a 46.15% market share in the automotive cylinder liner market in 2025, offering the lowest cost (USD 0.50-1.00 per liner) and adequate performance for passenger-car and light-commercial applications, where oil-drain intervals typically range from 10,000 to 15,000 km. Nitrided liners, growing at an 8.18% CAGR through 2031, deliver 50-70% fatigue-strength improvements and surface hardness of 800-1200 HV, enabling extended oil-drain intervals (30,000-50,000 km) mandated by Euro 7 and reducing total cost of ownership by 10-15%. Gas nitriding, plasma nitriding, and salt-bath nitriding each offer distinct trade-offs: gas nitriding penetrates 0.3-0.6 mm and requires 20-40 hours at 500-520°C, while plasma nitriding achieves equivalent hardness in 8-12 hours with lower distortion, making it preferred for thin-wall composite liners.

Federal-Mogul's GOE330 CGI liner integrates nitriding with micro-honing to reduce bore distortion by 27% under peak firing pressures, capturing contracts from Cummins and PACCAR for their 2027-model heavy-duty engines. Uncoated liners retain a 20-25% share in cost-sensitive markets (India, Southeast Asia, Latin America), where OEMs prioritize initial price over lifecycle cost. However, this segment is contracting as Bharat Stage VII and equivalent regulations mandate durability improvements. Thermal-spray coatings—plasma-transferred wire-arc (PTWA) and high-velocity oxygen-fuel (HVOF) occupy a premium niche, offering 15-20% friction reduction and enabling cylinder deactivation in GM's and Ford's V8 engines, but account for less than 5% of global volume due to USD 5-8 per-liner costs.

By Fuel Type: Diesel Resilience Anchors Commercial Segments

Diesel fuel types retained 62.14% of the automotive cylinder liner market share in 2025, concentrated in commercial vehicles, off-highway equipment, and marine applications, where energy density (35-38 MJ/liter versus 32-34 MJ/liter for gasoline) and thermal efficiency (40-45% versus 30-35%) justify higher upfront costs and complex aftertreatment systems. EPA's MHDV plan permits advanced diesel engines through 2040, while EU heavy-duty CO2 standards incentivize thermal-efficiency improvements rather than outright bans, sustaining liner demand in Daimler Truck, Volvo, and PACCAR platforms. Cummins' X15 Efficiency Series-achieving 50% brake thermal efficiency, specifies composite liners with nitrided surfaces to withstand peak cylinder pressures exceeding 200 bar. Gasoline engines, growing at a 6.85% CAGR through 2031, benefit from passenger-car hybridization: Toyota's TNGA 2.5-liter Atkinson-cycle engine (used in RAV4 and Camry hybrids) employs dry liners with PTWA coatings to reduce friction in frequent start-stop cycles.

India's Bharat Stage VI regulations, implemented in 2020, mandated the use of diesel particulate filters (DPF) and selective catalytic reduction (SCR), resulting in an 8-10% increase in per-vehicle liner content due to higher peak cylinder pressures and extended durability requirements. Brazil's Rota 2030 program incentivizes flex-fuel engines (ethanol-gasoline blends), which require stainless-steel or composite liners to resist ethanol's corrosive properties, creating a USD 120-150 million niche segment. Natural-gas engines used in municipal buses and refuse trucks—specify wet liners for superior heat dissipation, as stoichiometric combustion generates 10-15% higher exhaust-gas temperatures than diesel.

By Contact Type: Wet Liners Dominate Serviceability-Critical Applications

Wet cylinder liners accounted for 68.29% of the automotive cylinder liner market share in 2025, preferred in heavy-duty, marine, and industrial engines where direct coolant contact enables superior heat dissipation (30 to 40% better than dry liners) and field serviceability; a wet liner can be replaced in 4 to 6 hours versus 12 to 16 hours for a dry liner requiring block disassembly. Scania's 13-liter and 16-liter V8 engines, Volvo's D13 and D16 platforms, and Cummins' X15 all feature wet liners, enabling 1 million km service intervals in long-haul trucks. Caterpillar's C18 and C32 industrial engines, used in mining haul trucks and marine propulsion, employ wet liners with nitrided surfaces to withstand continuous operation at 90 to 95% load for 15,000 to 20,000 hours between overhauls.

Dry liners, growing at a 5.47% CAGR through 2031, dominate passenger cars and light commercial vehicles, where packaging constraints and lower peak cylinder pressures (120 to 160 bar versus 180 to 220 bar in heavy-duty vehicles) favor compact engine blocks with integrated cooling passages. Toyota's TNGA 2.0-liter and 2.5-liter engines, Honda's Earth Dreams 1.5-liter turbo, and Volkswagen's EA888 2.0-liter turbo all use dry liners with PTWA coatings to reduce friction by 10 to 12% and enable cylinder deactivation. Dry liners require tighter bore diameter tolerances (±0.02 mm versus ±0.05 mm for wet) and more precise coolant jacket machining, which raises block manufacturing costs by 8 to 10%. However, this approach saves 2 to 3 kg per engine, a critical advantage under Euro 7 weight penalties.

Geography Analysis

The Asia-Pacific region accounted for 41.76% of the automotive cylinder liner market share in 2025. Foundries in the area, like Samkrg Pistons and Yuchai, capitalized on a 50–60% labor-cost advantage, supplying OEMs throughout ASEAN. Meanwhile, Japanese and Korean manufacturers strategically positioned their plants in Thailand and India, ensuring proximity to customer programs.

Forecasts indicate that the Middle East and Africa region will grow at a CAGR of 8.39% through 2031. Saudi Arabia's Vision 2030, which mandates a 50% local content requirement, is attracting investment in casting and nitriding facilities. In South Africa, the light-truck assembly network, bolstered by 2024 expansions, now supports three liner foundries. Additionally, a government refurbishment fund is extending the service life of public-sector fleets, thereby increasing the demand for wet-liners.

In 2025, North America and Europe accounted for the majority of sales figures. Both the United States and Europe experienced a notable increase in battery-electric vehicle (BEV) adoption. While this trend influenced the demand for passenger-car liners, the heavy-duty sector remained broadly stable. Class 8 truck production held steady at 320,000 units, with industry giants Cummins, Daimler, and PACCAR integrating composite liners into their engines to meet stringent EPA standards. In Latin America, Brazil and Mexico are leading the charge in liner offtake, thanks to flex-fuel initiatives and fleet upgrades. Notably, suppliers like Cyltech Mexico, located near U.S. assembly plants, are benefiting from significant logistics savings.

Regulatory Landscape

Cylinder liner specifications and material choices are increasingly shaped by tailpipe-emissions and durability compliance regimes that raise combustion-system loads and extend useful-life requirements. In the European Union, Euro 7 (Regulation (EU) 2024/1257) tightens emissions and durability obligations, with type-approval consequences from 29 November 2026, when approval authorities refuse type-approval for new M1 or N1 vehicle types that do not comply. This reinforces adoption of higher-wear-resistance liners, improved honing, and advanced coatings to sustain in-service performance.

For heavy-duty applications, the US Environmental Protection Agency continued to advance rulemaking in 2026, publishing proposed amendments in July 2026 for MY 2027 and later heavy-duty highway engines that include new nonconformance penalties. In parallel with tailpipe compliance, manufacturing-site environmental controls are becoming more visible in supplier qualification, with OEM environmental and energy policies and plant permit limits (including VOC caps reported by suppliers) pushing liner producers and adjacent machining and coating operations toward tighter process control and certified management systems.

Value Chain Analysis

The value chain starts with ferrous and alloy inputs, notably grey iron and ductile iron, then moves through melting and casting. Centrifugal and sand casting remain core routes for durability-critical liners, followed by heat treatment and precision machining. Downstream steps typically include CNC turning and boring, plateau and slide honing to achieve tight bore geometry, and metrology to validate roundness, taper, and surface finish before shipment to OEM engine plants or to aftermarket channels supporting remanufacturing and rebuilds.

Surface engineering is the main value-add layer, spanning nitriding and advanced coatings such as PTWA, HVOF, and other thermal spray and thin-film approaches that target friction and scuffing at the liner-piston ring interface. As suppliers manage margin stability amid raw-material volatility, capabilities such as proprietary coatings, texturing, and integrated honing lines, along with vertical integration into foundry operations among larger tier suppliers, are increasingly important for winning heavy-duty, high-durability programs and meeting tighter emissions-driven durability requirements.

Competitive Landscape

Key players, including Mahale GmbH and Tenneco Inc., dominate the automotive cylinder liner market. Together, MAHLE, Tenneco’s Federal-Mogul division, and Nippon Piston Ring account for a significant share of global sales. By operating their own foundries, these three companies shield themselves from fluctuations in ferrous-metal prices, reaping a 20–25% cost advantage. Highlighting the impact of surface-engineering innovation on market dynamics, Federal-Mogul’s GOE330 CGI liner, which boasts a 27% reduction in bore distortion, has swiftly clinched contracts with industry giants Cummins and Daimler Truck.

Tier-2 firms, such as Rheinmetall’s KS Kolbenschmidt and TPR, compete in precision machining and niche materials. At the same time, tier-3 regional players in India, Vietnam, and Thailand are undercutting prices by up to 20% on cast-iron units. OEM in-house casting remains a latent threat: General Motors already makes roughly one-third of its liner needs at the United States engine plants, and Volkswagen covers a quarter of its European requirement at Salzgitter.

Strategic partnerships are therefore critical. MAHLE’s multi-year agreement with TRATON and Tenneco’s supply deal with Volvo lock up 40–50% of heavy-duty demand through 2028, ensuring volume stability while electrification reshapes the light-vehicle space. Additionally, MAN Truck & Bus has awarded MAHLE a contract to provide cutting-edge components, including cylinder liners, for its hydrogen-powered eTGX truck[2]Abhijeet Singh, "MAHLE Secures Contract For Hydrogen Engine Components In MAN hTGX Truck," MOBILITY OUTLOOK, mobilityoutlook.com. Nippon Piston Ring’s joint venture in India increases access to the fast-growing South Asian rebuild volumes[3]"Establishment of NPR AUTO PARTS MANUFACTURING INDIA PRIVATE LIMITED, NPR-RIKEN Corporation, npr-riken.co.jp.

Automotive Cylinder Liner Industry Leaders

-

Mahle GmbH

-

Tenneco Inc.

-

Nippon Piston Ring Co., Ltd.

-

TPR Co., Ltd.

-

ZYNP International Corp.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White-space is most visible where regulations and operating costs push engine makers toward friction reduction and extended durability, while keeping ICE platforms relevant in heavy-duty, off-highway, and hybridized passenger applications. Recent technical work on surface texturing and coatings points to measurable tribology gains, including 2025 bench-test evidence showing that density-gradient surface textures created via precision electrolytic etching cut friction coefficients by up to 31.4%, alongside electrodeposited composite films and texturing that improve scuffing resistance. These outcomes are consistent with the market shift toward nitrided and coated liners, and they provide a technical pathway for suppliers to differentiate beyond commodity cast-iron liners.

Another opportunity lies in scaling advanced manufacturing routes that deliver tighter tolerances and lower mass without prohibitive cost, including hydroforming and higher-precision honing and finishing, to meet durability requirements under Euro 7 and comparable frameworks. On the demand side, commercial-vehicle programs pursuing high-efficiency combustion, including hydrogen ICE initiatives such as MAN Truck & Bus programs supplied with liner-containing component sets, create a niche for material and coating upgrades that tolerate higher peak pressures and altered combustion characteristics. This supports premium liner content per engine even as passenger-car electrification reduces baseline volumes in some regions.

Recent Industry Developments

- April 2026: IP Rings Ltd announced termination of its 1995 share subscription and technical assistance agreement with Nippon Piston Ring Co. Ltd, shifting to a royalty-free technology partnership as NPR divests its 5.56% stake. The change redefines technology access and collaboration economics in piston ring and related cylinder-system components, which can influence sourcing relationships for liner-compatible tribology packages.

- November 2024: MAHLE secured a series production contract from MAN Truck & Bus for the MAN hTGX hydrogen-powered truck, supplying key engine components including cylinder liners. The award reinforces hydrogen ICE as an active development and production pathway in commercial vehicles, supporting demand for specialized liners and surface treatments designed for new combustion conditions.

- October 2024: Tenneco expanded hydrogen internal combustion engine (H2-ICE) testing capabilities with new test cells in Burscheid, Germany and Ann Arbor, Michigan, plus a hydrogen materials test laboratory in Nuremberg, Germany. The added test capacity supports faster validation of critical components such as cylinder liners and coatings for durability under hydrogen combustion, strengthening the supplier ecosystem around H2-ICE platforms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of cylinder liners used in automotive internal combustion engines, counted as the component supplied for new vehicle production and replacement needs across major vehicle categories and regions.

Scope exclusions: It does not count engine blocks, pistons, piston rings, or broader engine remanufacturing services unless the cylinder liner itself is the priced item.

Segmentation Overview

-

By Material Type

- Cast Iron

- Stainless Steel

- Composite Materials

-

By Manufacturing Process

- Sand Casting

- CNC Machining

- Hydroforming

-

By Cylinder Configuration

- Inline

- V-Shaped

-

By Application Type

- Passenger Vehicles

- Light Commercial Vehicles

- Medium and Heavy-Duty Vehicles

-

By Surface Treatment

- Uncoated

- Nitrided

- Honed

-

By Fuel Type

- Gasoline

- Diesel

-

By Contact Type

- Wet Cylinder Liner

- Dry Cylinder Liner

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand drivers that link directly to liner volumes, then checking how quickly the ICE and hybrid mix is changing in each region. Public source types like OICA vehicle production tables, national transport agencies, customs and trade statistics portals, and energy or environment regulators are used to keep the engine and fuel mix assumptions realistic.

We also review standards and technical literature, for example SAE papers, peer reviewed metallurgy and tribology journals, and patent databases, to confirm adoption of coated liners, material shifts, and typical replacement behavior. Annual reports, investor presentations, and reputable automotive press are then used to cross check capacity expansion talk and end market exposure, and a paid subscription for company financials and news is used where public disclosures are limited. This desk source list is not exhaustive, and other public references are used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to stress test assumptions that desk sources cannot fully confirm, including average selling price ranges by material and liner type, channel margin spreads, and how OEM and aftermarket shares shift with vehicle age. We speak with component makers, distributors, and engine or vehicle experts across APAC, EMEA, and the Americas, so regional production patterns and replacement cycles are reflected in the final model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | APAC: 49% |

| Mid tier: 55% | Functional/Unit leaders: 37% | EMEA: 33% |

| Smaller Players: 19% | Managers: 50% | Americas: 18% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool, where vehicle production by region is reconstructed into ICE and hybrid engine builds, then converted into liner demand using cylinder count patterns and wet versus dry liner penetration. Once the base is set, we corroborate totals with selective bottom-up checks using sampled supplier revenues, channel feedback on shipment volumes, and price per liner ranges by material and coating type, then adjust assumptions when the two views do not align.

Key inputs used in the model include passenger and commercial vehicle production trends, the diesel to gasoline and hybrid mix, average cylinders per engine family, liner design shifts (wet versus dry and coated versus uncoated), and replacement rate signals tied to vehicle parc aging. Where direct data is missing for smaller countries, proxy ratios are applied from comparable markets and then normalized back to known regional totals so gaps do not inflate the result.

Forecasts are produced with scenario analysis supported by simple regression-style checks, where drivers such as production outlook, powertrain mix change, and material cost direction are tested together. The final numbers are then reviewed to confirm that implied unit volumes and implied average prices remain consistent with what interviewees report for procurement and aftermarket channels.

Data Validation & Update Cycle

Outputs are validated through several checks, including cross comparing implied liner volumes against engine build indicators, checking that regional shares follow automotive production realities, and reviewing year over year movements for abnormal jumps. If a segment shows a sharp change, we recheck the input driver first, and then follow up with sources again when the variance cannot be explained by production, mix, or pricing.

Before sign-off, a second analyst reviews the assumptions, calculations, and key linkages so the model can be repeated and audited. Reports are refreshed annually, and interim updates are made when material events occur, such as major powertrain policy shifts or large capacity changes. Right before delivery, the latest public releases and news are reviewed again so clients receive an up to date view.

Mordor Intelligence's Automotive Cylinder Liner Market Size Compared With Other Published Estimates

Published market sizes for cylinder liners can look far apart because the math depends heavily on what gets counted, which year is treated as the base, and how pricing is converted and trended across regions. Differences also come from how quickly each model updates the ICE and hybrid mix and whether aftermarket replacement is treated as steady or highly cyclical.

Some external estimates are built from a narrower component definition or a limited set of regions, then expanded with simple multipliers, which can compress the starting value. In Mordor Intelligence, the count is limited to automotive cylinder liners only, and it is broken out by material, fuel type, wet versus dry contact, vehicle type, and region, with assumptions refreshed to January 2026 so shifts in production mix do not lag the market.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.62 B (2026) | |

| Industry Research Publisher A | USD 5.35 B (2024) | Uses an earlier base year and typically reflects a tighter definition around ICE focused demand without clearly showing how hybrid penetration and wet versus dry liner mix are converted into volumes and prices by region. |

| Industry Research Publisher B | USD 6.72 B (2024) | Starts from a 2024 base and extends a long horizon, but the public summary does not explain the pricing build for coated and advanced material liners or how replacement cycles are normalized across regions, which can shift the total. |

Taken together, the spread mainly tracks three things: base year choice, scope clarity on what is counted as a liner sale, and how unit demand is translated into value using consistent price logic. By keeping the variables tied to production, powertrain mix, liner design adoption, and replacement behavior, the model stays traceable and easier to replicate in future refreshes.

Key Questions Answered in the Report

How large is the automotive cylinder liner market in 2026?

The automotive cylinder liner market size is USD 7.62 billion in 2026 and is forecast to reach USD 9.78 billion by 2031.

Which material segment is growing fastest?

Composite liners are projected to record a 9.96% CAGR to 2031 as they help engines meet stricter weight and thermal targets.

Why do wet liners dominate heavy-duty engines?

Wet liners dissipate 30–40% more heat and can be replaced in half a day, which is essential for long-haul trucks that aim for 1 million km service life.

Which region is the largest revenue contributor?

Asia-Pacific leads with 41.76% of global revenue, driven by China’s diesel-engine volume and India’s booming commercial-vehicle output.

How does electrification affect liner demand?

Battery-electric cars reduce passenger-car liner consumption, yet heavy-duty and remanufacturing segments keep overall market revenue on a positive 5.11% CAGR path through 2031.

Who are the leading suppliers?

MAHLE, Tenneco’s Federal-Mogul, and Nippon Piston Ring collectively command major market share, with regional players gaining ground on price.

Page last updated on: