Automotive Drivetrain Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

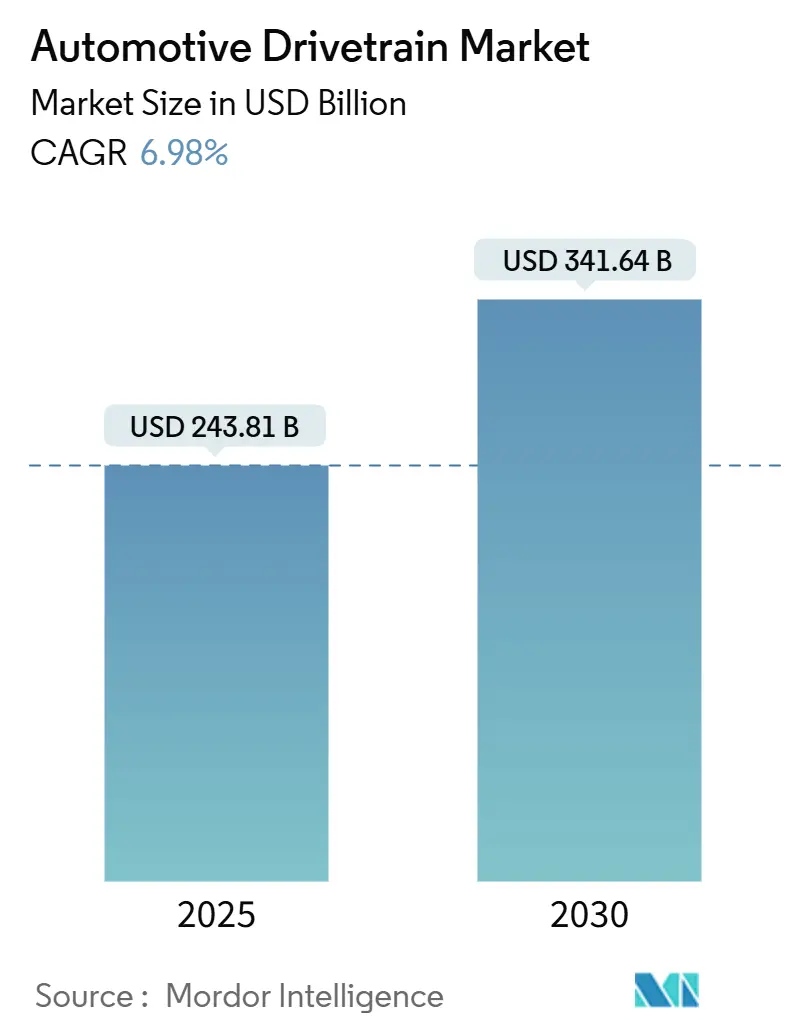

| Market Size (2025) | USD 243.81 Billion |

| Market Size (2030) | USD 341.64 Billion |

| Growth Rate (2025 - 2030) | 6.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Drivetrain Market Analysis by Mordor Intelligence

The automotive drivetrain market size stood at USD 243.81 billion in 2025 and is set to expand to USD 341.64 billion by 2030, advancing at a 6.98% CAGR over 2025-2030. Strong demand for electrified powertrains, regulatory pressure on tailpipe emissions, and rising adoption of all-wheel drive (AWD) SUV models underpin the current growth cycle in the automotive drivetrain market. Hybrid systems keep internal-combustion engine (ICE) technology relevant, while battery-electric vehicle (BEV) architectures gain share through rapid cost declines in motors, inverters, and battery packs. Integrated e-axle modules reduce component count and manufacturing complexity, helping suppliers capture new value pools even as transmission makers pivot to software-defined controls. Competitive tension intensifies as tier-1 suppliers add silicon-carbide power electronics and lightweight materials to defend margins, with supply-chain resilience becoming a key differentiator when sourcing rare-earth magnets and semiconductors.

Key Report Takeaways

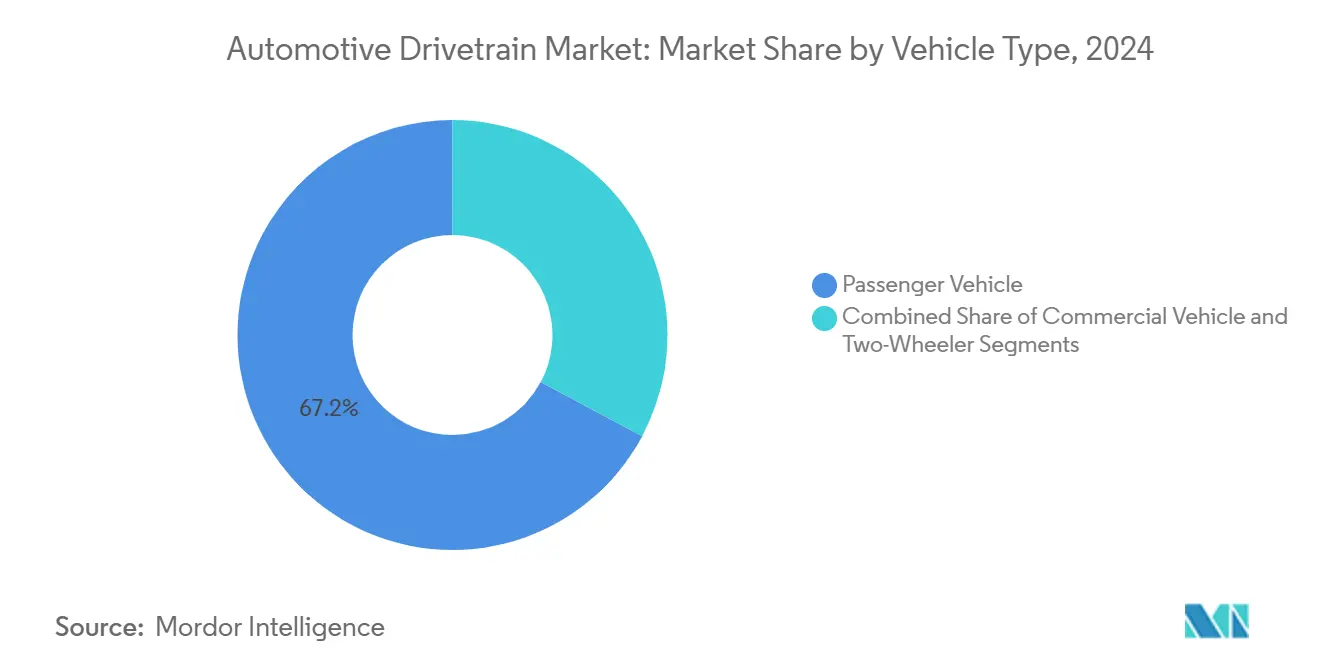

- By vehicle type, passenger vehicles commanded 67.15% of the automotive drivetrain market share in 2024; the same segment is forecast to expand at a 7.13% CAGR to 2030.

- By propulsion, ICE drivetrains carried 63.22% of the automotive drivetrain market share in 2024, whereas BEV components are projected to record a 10.14% CAGR through 2030.

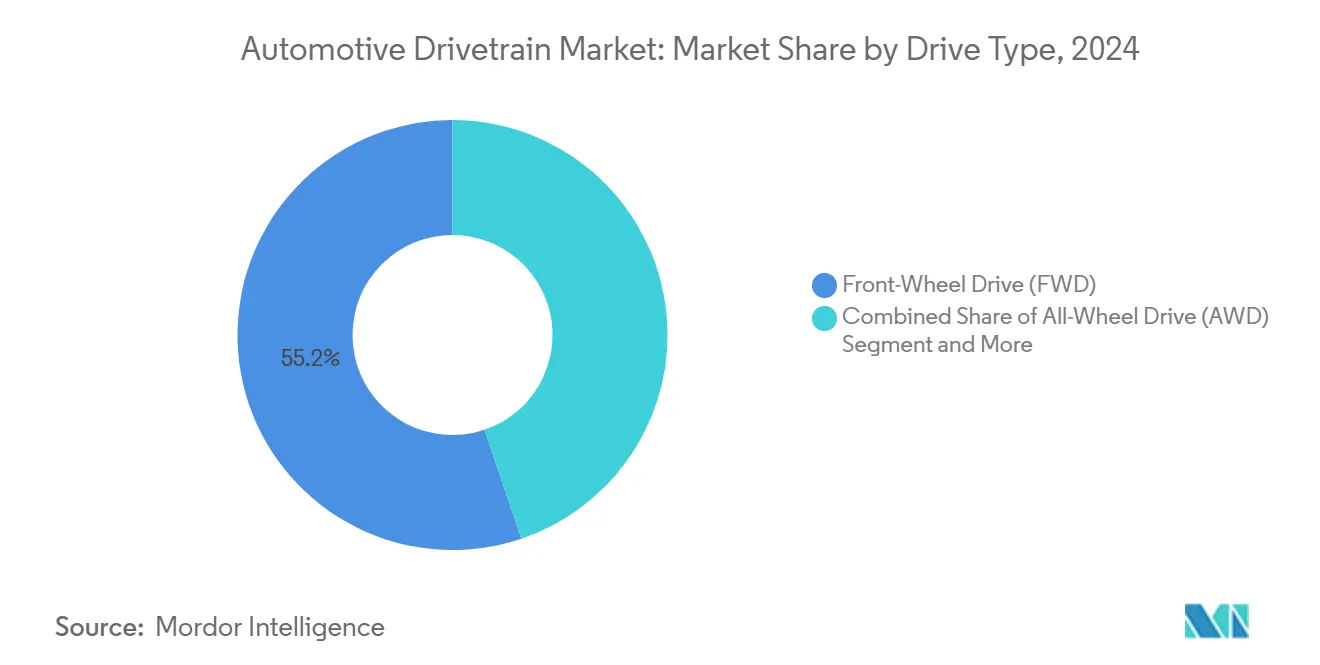

- By drive type, front-wheel drive (FWD) held 55.16% of the automotive drivetrain market share in 2024, while AWD is set to grow at 8.73% CAGR over the forecast window.

- By component, transmissions contributed 42.35% of the automotive drivetrain market share in 2024; e-axles form the fastest-growing category at 8.33% CAGR through 2030.

- By geography, Asia-Pacific dominated with a 47.11% of the automotive drivetrain market share in 2024 and is projected to grow at a 7.45% CAGR to 2030, outpacing all other regions.

Global Automotive Drivetrain Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global EV Sales | +1.8% | Global with Asia-Pacific leading | Medium term (2-4 years) |

| Stricter Emissions & Fuel Rules | +1.2% | Global; EU and California lead | Long term (≥ 4 years) |

| Rapid E-Axle Uptake | +1.1% | Asia-Pacific core | Short term (≤ 2 years) |

| Consumer Tilt Toward SUVs/AWD | +0.9% | North America and EU | Medium term (2-4 years) |

| Software-Defined Powertrains | +0.7% | Global premium segment | Long term (≥ 4 years) |

| Lightweight Materials Boost Efficiency | +0.5% | Developed markets worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global EV Sales Drive Demand for Advanced Drivetrains

Electric car deliveries climbed to 17 million units in 2024, gradually growing year-over-year [1]“Global electric vehicle update 2024,” American Intellectual Property Law Association, aipla.org. Manufacturers responded by scaling dedicated skateboard platforms that embed e-axle modules for compact packaging and high torque density. Chinese OEMs stepped up vertical integration, forcing traditional suppliers to accelerate joint-venture timelines to keep design-in positions. Integrated motor-inverter-gear units cut component count compared with multi-piece ICE drivetrains, lowering assembly costs but shifting more value to electronics specialists. Certification under ISO 26262 functional-safety rules became table stakes for advanced inverter control, signaling the transition from mechanical hardware to software-centric propulsion. As BEV penetration rises, the automotive drivetrain market faces simultaneous margin pressure on legacy parts and fresh revenue streams from high-value integrated modules.

Stricter Emissions and Fuel-Economy Regulations Worldwide

The EPA finalized a 40.4 mpg corporate average fuel-economy target by 2026, while Euro 7 standards introduce real-world driving emission tests that tighten calibration windows. Japan’s Mobility Digital Transformation roadmap seeks 100% electrified sales by 2035, pushing global drivetrain priorities toward hybrids and BEVs [2]“Mobility DX roadmap 2025,” Ministry of Economy, Trade and Industry Japan, meti.go.jp. Automakers consequently invest in fifth-generation hybrid transaxles that cut costs via parts commonality and regional sourcing. Software-defined calibration platforms allow real-time torque and emissions optimization across multiple regulatory regions. These moves amplify hybrid adoption as a bridge solution and add momentum to longer-run BEV scale-up plans, lifting average content value per vehicle for compliant powertrain modules in the automotive drivetrain market.

Rapid Adoption of Integrated E-Axle Architectures

Top suppliers such as Aisin, Schaeffler, and Vitesco fast-tracked e-axle rollouts, and BMW picked Aisin for its next-generation electric SUVs. Consolidating the motor, inverter, and reduction gear into a sealed housing trims weight and eases OEM sourcing. Component aggregation also reduces per-vehicle value for stand-alone transmissions and differentials, intensifying competition among legacy Tier-1s. E-axle modules enable software-based torque curves and over-the-air adjustments, which open up post-sale revenue models. Asian production hubs scale fastest thanks to electronics supply chains, setting new benchmark costs that ripple across the automotive drivetrain market.

Higher Consumer Preference for SUVs and AWD Configurations

SUV and crossover registrations outpaced total light-vehicle growth in both North America and Europe during 2024, reinforcing OEM focus on AWD systems for traction and ride comfort. Intelligent torque-vectoring couplings allocate power dynamically, improving road-holding without the weight of mechanical linkages. Electrified AWD layouts use dual motors to deliver instant torque split, which supports performance branding while enhancing energy recuperation. Premium buyers also link AWD to advanced driver-assistance features, further intertwining drivetrain adoption with safety technology. This preference widens vehicle footprints and raises average drivetrain invoice values, propelling segment revenues within the automotive drivetrain market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain and Material Swings | -1.1% | Worldwide, acute in chip-heavy markets | Medium term (2-4 years) |

| High Cost of Next-Gen Parts | -0.8% | Global with highest pain in emerging economies | Short term (≤ 2 years) |

| Sparse Rural Charging Infrastructure | -0.6% | Emerging markets and low-density areas | Medium term (2-4 years) |

| Thermal Management Limits in E-Drives | -0.4% | Global; critical for performance cars | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Disruptions and Raw-Material Price Volatility

IRENA projected a five-fold increase in rare-earth and lithium demand for e-mobility by 2030, tightening material availability [3]“Critical materials outlook for EVs,” International Renewable Energy Agency, irena.org. Semiconductor lead times stretched past 36 weeks for automotive-grade power chips, with allocation cuts disrupting production forecasts. Some tier-1s diversified into Vietnam, following TBP Auto’s facility ramp-up to de-risk geographic concentration. Spot metal price spikes compel dynamic pricing clauses in supply contracts, complicating OEM cost-planning cycles. Volatility injects uncertainty into the automotive drivetrain market outlook until new mining and fab capacity comes online.

High Cost of Next-Gen Drivetrain Components

Silicon-carbide (SiC) MOSFET inverters outclass silicon types on efficiency, yet cost multiple times more on a per-kilowatt basis. BorgWarner has locked in SiC supply contracts to hedge availability. E-axle modules currently carry lower revenue per vehicle than multi-component ICE drivetrains, eroding short-term margins while capex runs high. Suppliers face dual pressure to amortize R&D over limited near-term volumes and to maintain price parity with mature mechanical systems. The affordability gap slows adoption in cost-sensitive regions, tempering headline expansion in the automotive drivetrain market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: passenger vehicles anchor global value creation

Passenger vehicles delivered 67.15% of the automotive drivetrain market share in 2024, generating the largest revenue pool. Scale advantages let automakers amortize the cost of fifth-generation hybrid transaxles and e-axles across high volumes, supporting a forecast 7.13% CAGR out to 2030. Manufacturers exploit global line-ups to share standard electric drive modules, lowering per-unit cost curves faster than commercial applications.

Continued government incentives for small BEV cars in China and Europe amplify volume, while premium marques raise take-rates for dual-motor AWD sedans. Although smaller in volume, commercial vehicles pull demand for fuel-cell drives and high-torque e-axles that can handle 40-ton gross weights. Two-wheelers show explosive urban-mobility growth, but their lightweight hub motors mean lower revenue capture per unit relative to passenger cars, thereby keeping passenger cars the value anchor in the automotive drivetrain market.

By Propulsion: ICE retains dominance as BEV gains momentum

Internal combustion drivetrains accounted for 63.22% of the automotive drivetrain market share in 2024, reflecting the entrenched global fleet and lower fueling infrastructure risk. Battery-electric components surged at a 10.14% CAGR, aided by falling battery pack prices and zero-emission mandates across Europe, China, and select states in the United States, narrowing the gap in the automotive drivetrain market share by propulsion.

Hybrid electric drivetrains bridge the transition, especially in Japan, where full hybrids reached a significant share of early-2024 new-car registrations. Plug-in hybrids appeal in regions with patchy chargers, while fuel-cell systems stay niche but gain interest for long-haul trucks. The propulsion mix will keep shifting toward BEVs, yet ICE combinations will remain material through 2030 because of installed base servicing and gasoline price elasticity.

By Drive Type: AWD accelerates as SUVs proliferate

FWD architectures supplied 55.16% of the automotive drivetrain market share in 2024, on cost and packaging benefits, anchoring mainstream compact cars in the automotive drivetrain market size discourse. AWD demand, however, grows fastest at 8.73% CAGR as SUVs capture incremental share. Dual-motor BEV SUVs eliminate mechanical propshafts, using software to vector torque with millisecond precision, which unlocks performance trims and premium pricing. Rear-wheel drive (RWD) is relevant in luxury and performance nameplates, where handling dynamics trump cost.

Regional adoption diverges; North America and Scandinavia favor AWD for winter traction, while Southern Europe stays loyal to FWD efficiency. Flex-architecture EV skateboards make it easier for OEMs to swap between two-wheel and all-wheel configurations without extensive retooling, broadening AWD availability across price bands in the automotive drivetrain market.

By Component: transmissions dominate, e-axles surge

Transmission assemblies comprised 42.35% of the automotive drivetrain market share in 2024, bolstered by the large ICE and hybrid install base that still requires multi-ratio gearsets. As BEVs rise, single-speed gearboxes and direct-drive layouts trim traditional revenue; however, specialized two-speed EV gearboxes emerge for performance segments, extending transmission relevance.

E-axles post the highest growth rate at 8.33% CAGR, embedding motor, inverter, and gearing into a sealed unit that OEMs can bolt directly to the chassis. Differentials, driveshafts, and propshafts remain essential for RWD and AWD ICE models but decline proportionally as FWD hybrids and dual-motor EVs delete certain mechanical links. The component landscape continues to rebalance toward integrated electro-mechanical systems that concentrate value and intellectual property inside fewer but more complex modules in the automotive drivetrain market.

Geography Analysis

Asia-Pacific controlled 47.11% of the automotive drivetrain market share in 2024 and should extend its lead with a 7.45% CAGR through 2030, riding China’s BEV production surge and Japan’s hybrid excellence. Chinese battery-electric exports boost regional e-axle output, while Japanese giants license hybrid transaxles to overseas affiliates, reinforcing technology spillovers. South Korea supplies advanced SiC power modules that anchor multiple Asia-Pacific e-drive value chains. India leans on government subsidies to build a domestic supplier base, opening fresh opportunities at both two-wheeler and light-vehicle levels in the automotive drivetrain market.

Europe emphasizes strict emissions compliance and premium vehicle positioning. Euro 7 rules propel demand for lightweight materials and high-efficiency electric drives, and Germany continues to pioneer compact hybrid gearboxes. Eastern European plants produce cost-optimized differentials and shafts for volume OEMs, balancing labor savings with proximity to final assembly. Regional policy coherence on carbon neutrality accelerates lifecycle considerations, channeling R&D funding toward recyclable drivetrains.

North America benefits from a strong SUV appetite and federal incentives embedded in the Inflation Reduction Act. California’s ZEV mandate and updated CAFE standards steer OEM product plans toward mixed powertrains, including plug-in hybrids and long-range BEVs. Canada’s parts suppliers pivot slowly from mechanical gears to integrated e-modules, while Mexico leverages trade pacts and competitive labor to attract new e-axle plants. The resulting cross-border ecosystem sustains content growth per vehicle even as total units plateau, bolstering regional contribution to the automotive drivetrain market.

Competitive Landscape

The automotive drivetrain market shows moderate concentration, with legacy tier-1 companies such as ZF, Aisin, and BorgWarner protecting incumbency via global footprints and multi-year OEM contracts. Transition costs into software and electronics weigh on margins, feeding consolidation momentum exemplified by American Axle’s acquisition of Dowlais, which aims to secure technology depth and volume scale in e-drive systems.

Chinese suppliers gain share by bundling motors and inverters at cost levels tough to match in Europe or North America, pushing incumbent Western firms to fast-track partnerships or joint ventures. Patent filings cluster in torque-vectoring algorithms, battery thermal integration, and over-the-air calibration, raising intellectual-property barriers for late entrants.

ISO 26262 safety certification and UNECE cybersecurity rules favor suppliers with established automotive quality systems. Software-defined drivetrains blur the line between propulsion and ADAS domains, positioning chip vendors and cloud specialists as emerging stakeholders. Competitive success increasingly depends on orchestrating silicon, software, and mechatronics into holistic propulsion platforms, reshaping long-term value capture in the automotive drivetrain market.

Automotive Drivetrain Industry Leaders

ZF Friedrichshafen AG

Aisin Corporation

Magna International Inc.

BorgWarner Inc.

GKN Automotive

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ZF Commercial Vehicle Solutions won a multi-year deal to supply AxTrax 2 electric axles for a new fleet of zero-emission intercity buses built by a leading Indian OEM, cementing ZF’s footprint in South Asia’s coach electrification drive.

- April 2025: Garrett Motion partnered with Shaanxi Hande Axle to co-develop beam-style electric axles for medium- and heavy-duty trucks, reflecting growing demand for high-torque commercial e-drives in China’s logistics sector.

- December 2024: Livguard debuted an integrated drivetrain solution at Electric Vehicle Expo 2024 in New Delhi that merges motors, controllers, batteries, and chargers into one package, signaling India’s push for vertically integrated e-mobility systems.

- September 2024: AVL launched a compact e-axle for 40-ton long-haul trucks with a 1.5-million-kilometer service life, targeting battery-electric and fuel-cell platforms.

Global Automotive Drivetrain Market Report Scope

| Two-Wheeler |

| Passenger Vehicle |

| Commercial Vehicle |

| Battery Electric Vehicle (BEV) |

| Internal Combustion Engine (ICE) |

| Hybrid Electric Vehicle (HEV) |

| Plug-In Hybrid Electric Vehicle (PHEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| All-Wheel Drive (AWD) |

| Front-Wheel Drive (FWD) |

| Rear-Wheel Drive (RWD) |

| Transmission |

| Differential |

| Drive Shaft |

| Axle |

| Propeller Shaft |

| e-Axle |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Vehicle Type | Two-Wheeler | |

| Passenger Vehicle | ||

| Commercial Vehicle | ||

| By Propulsion | Battery Electric Vehicle (BEV) | |

| Internal Combustion Engine (ICE) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Plug-In Hybrid Electric Vehicle (PHEV) | ||

| Fuel Cell Electric Vehicle (FCEV) | ||

| By Drive Type | All-Wheel Drive (AWD) | |

| Front-Wheel Drive (FWD) | ||

| Rear-Wheel Drive (RWD) | ||

| By Component | Transmission | |

| Differential | ||

| Drive Shaft | ||

| Axle | ||

| Propeller Shaft | ||

| e-Axle | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the automotive drivetrain market today?

The automotive drivetrain market size reached USD 243.81 billion in 2025 and is on track for USD 341.64 billion by 2030.

What propulsion technology is growing fastest?

Battery-electric drivetrain components exhibit the highest growth at a 10.14% CAGR through 2030.

Which region leads global drivetrain demand?

Asia-Pacific held 47.11% of 2024 revenue and is projected to grow at 7.45% CAGR, the fastest among all regions.

Why are integrated e-axles important?

E-axles merge motor, inverter and gearing, cutting part count and enabling software-based torque control, which supports faster BEV cost reductions.

Page last updated on: