Automotive Traction Motor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

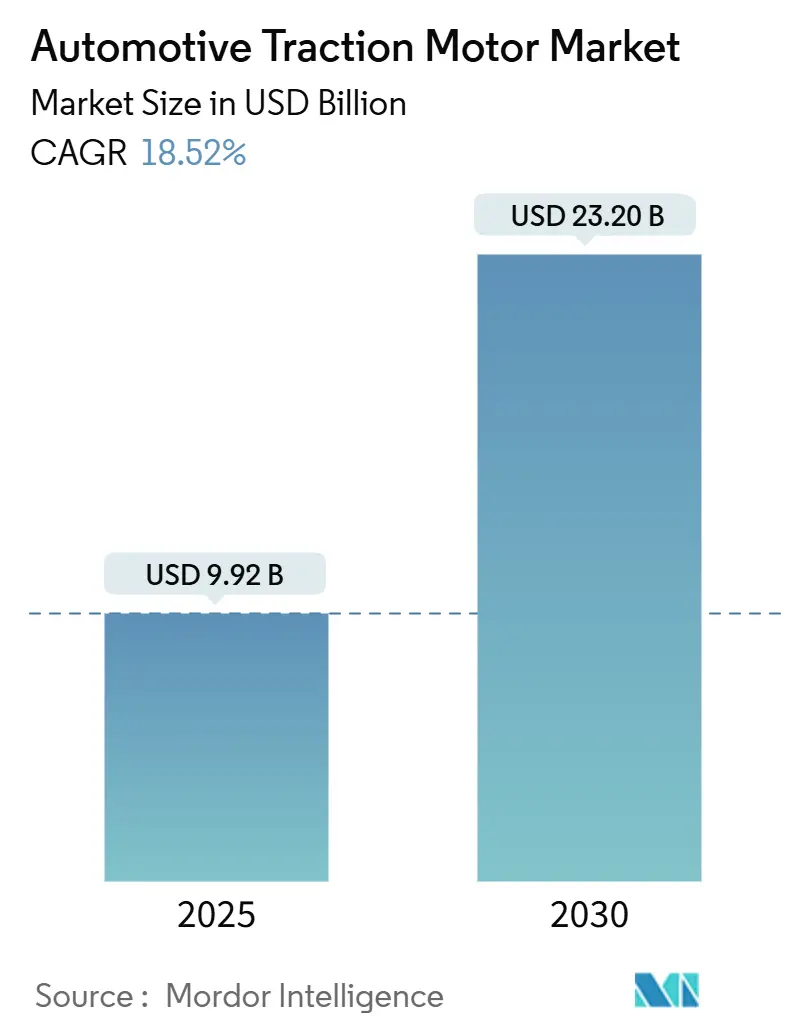

| Market Size (2025) | USD 9.92 Billion |

| Market Size (2030) | USD 23.20 Billion |

| Growth Rate (2025 - 2030) | 18.52% CAGR |

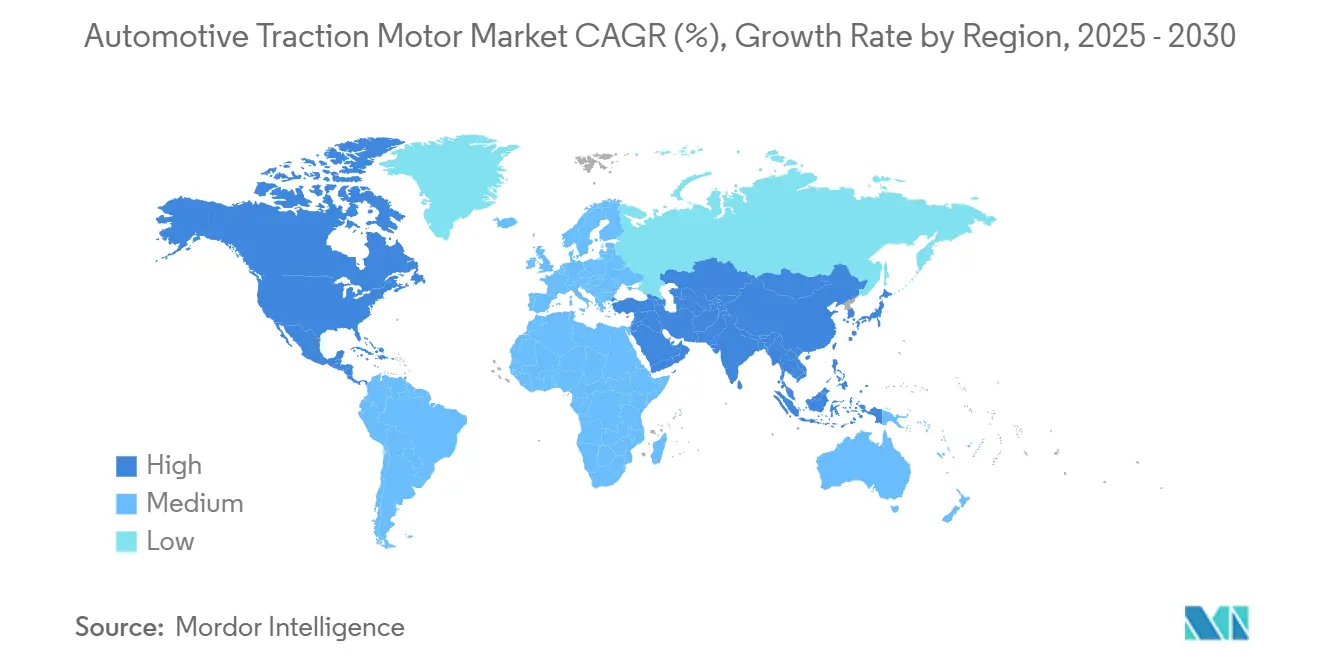

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

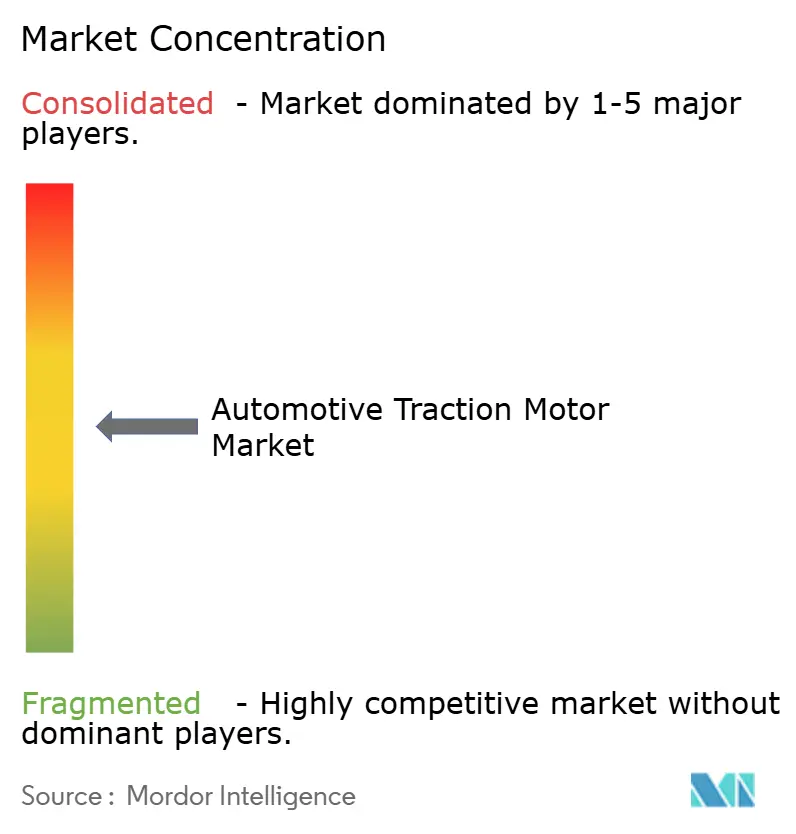

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Traction Motor Market Analysis by Mordor Intelligence

The automotive traction motor market reached USD 9.92 billion in 2025 and is projected to achieve USD 23.20 billion by 2030, reflecting an 18.52% CAGR. Rapid electrification programs, stricter tailpipe-emission limits, and advances in power electronics are keeping the automotive traction motor market on a high-growth path. Permanent-magnet synchronous motors (PMSMs) retain cost and performance advantages for most light-duty vehicles, but switched reluctance motors (SRMs) are winning share where rare-earth savings matter most. Cooling innovation is shifting designs toward hybrid configurations that balance weight with thermal headroom, while 800-V drive platforms push higher voltage levels to gain efficiency. Regional policy incentives are steering new manufacturing footprints to North America and Europe, even as Asia-Pacific remains the volume leader for the automotive traction motor market.

Key Report Takeaways

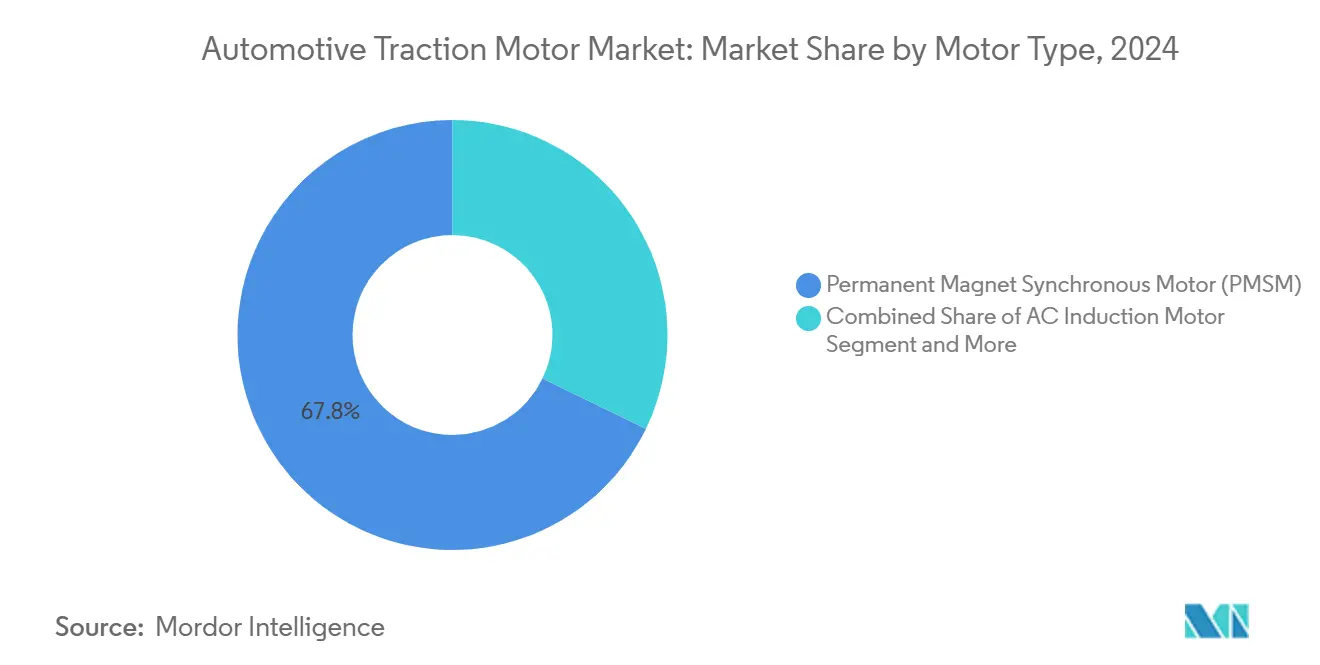

- By motor type, permanent-magnet synchronous motors held 67.82% of the automotive traction motor market share in 2024; switched reluctance motors are forecast to expand at a 19.21% CAGR through 2030.

- By cooling system, liquid-cooled designs commanded 59.38% of the automotive traction motor market size in 2024, while hybrid cooling systems are expected to deliver the fastest growth at a 19.18% CAGR to 2030.

- By application, passenger cars captured a 72.62% revenue share in 2024; electric scooters and motorcycles are projected to advance at a 20.28% CAGR to 2030.

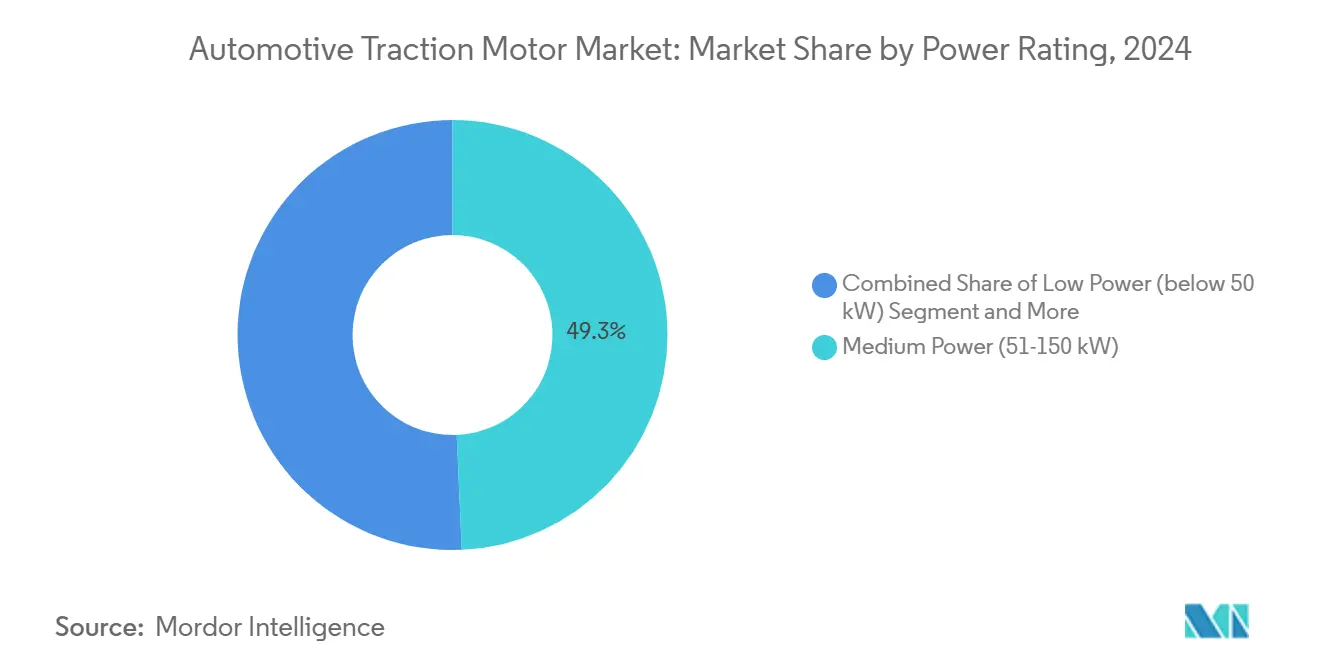

- By power rating, the medium-power segment accounted for 49.31% of the automotive traction motor market size in 2024, whereas high-power motors above 150 kW are projected to grow at 18.65% CAGR.

- By distribution channel, OEM sales represented 89.36% of the automotive traction motor market size in 2024 , yet the aftermarket is set for an 18.94% CAGR through 2030.

- By geography, Asia-Pacific led with 45.18% revenue share in 2024; the North America region is poised for a 20.98% CAGR to 2030.

Global Automotive Traction Motor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Global CO₂/ZEV Mandates | +2.8% | Europe and North America leading, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Next-Gen SiC Inverters Lifting Motor Efficiency | +2.2% | Global, led by developed markets | Medium term (2-4 years) |

| Permanent-Magnet Cost Declines | +2.1% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Rapid Scaling of 800-V E-Axle Platforms | +1.9% | Europe and China core, expanding globally | Short term (≤ 2 years) |

| On-Shoring Incentives for Motor Production | +1.6% | North America and Europe primarily | Long term (≥ 4 years) |

| OEM Vertical Integration to Secure IP | +1.4% | Global, with concentration in United States, Germany, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Global CO₂/ZEV Mandates Accelerate Adoption

The United Kingdom requires 80% of new-car sales to have zero emissions by 2030, enforcing GBP 15,000 penalties per non-compliant vehicle[1]“Zero Emission Vehicle Mandate,”, UK Government, gov.uk. Canada set a 100% zero-emission light-duty target for 2035, reinforcing demand with CAD 1.7 billion (USD 1.27 billion) in purchase incentives through 2025 [2]“Incentives for Zero-Emission Vehicles,”, Transport Canada, tc.canada.ca. The European Union’s Euro 7 regulations, effective 2025, push diesel and gasoline options out of urban segments, compelling automakers to scale the automotive traction motor market quickly. Commercial fleets face fresh city bans on diesel trucks, forcing high-power e-axles into depot cycles. These policies underpin cap-ex for new motor facilities and validate multi-billion-dollar long-term supply contracts.

Next-Gen SiC Inverters Lift Motor Efficiency

ZF’s High 2.0 modules pair silicon-carbide switches with 800-V topologies to reach functional-safety levels and cost targets suited to mass-market platforms. Wolfspeed fabricates SiC substrates for power ranges up to 300 kW, validating volume economics beyond luxury cars. Precision current-vector control boosts PMSM torque density yet equally benefits SRMs that depend on fast phase commutation. Lower switching losses mean smaller cooling jackets, opening design freedom for compact cross-members.

Permanent-Magnet Cost Declines Drive Market Accessibility

Recycled neodymium-iron-boron magnets now cost less than virgin material, easing one of the largest bill-of-materials items in mid-power motors. MP Materials restarted domestic sintered NdFeB production in Fort Worth, targeting 1,000 t annually for General Motors deliveries in late 2025. Localized magnet supply shortens lead times and cuts currency-exchange risk for U.S. plants adjacent to Detroit. Magnet cost parity is most evident in 51–150 kW units, shrinking total system prices that feed mainstream passenger-car adoption. Nissan’s samarium-iron alternative underlines OEM determination to diversify rare-earth inputs and hedge supply shock.

Rapid Scaling of 800-V E-Axle Platforms Enhances Performance

BMW’s Gen6 e-drive integrates rotor, stator, and inverter under an 800-V bus, cutting energy losses and slicing motor weight. Vitesco’s EUR 188 million (USD 205.8 million) Czech expansion assembles high-voltage power electronics for combined inverter, onboard charger, and distribution functions[3]“High-Voltage Electronics Czech Plant,”, Vitesco Technologies, vitesco-technologies.com. Higher voltage trims current, allowing smaller conductors and reduced copper mass in PMSM and SRM designs. BYD’s portfolio roll-out proves that 800-V is no longer confined to premium nameplates. Faster charging and cooler operation make the architecture attractive for above 150 kW commercial stacks with tight thermal constraints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rare-Earth Supply Volatility | -1.8% | Global, with highest impact in Europe and North America | Long term (≥ 4 years) |

| Thermal-Management Design Complexity | -1.2% | Global, concentrated in high-performance applications | Medium term (2-4 years) |

| Grid-Related Peak-Demand Surcharges | -1.1% | North America and Europe, expanding to urban Asia-Pacific | Medium term (2-4 years) |

| Traction-Motor Acoustic/EMI Regulations | -0.9% | Europe and North America primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rare-Earth Supply Volatility Creates Strategic Vulnerabilities

China processes nearly 85% of global rare-earth oxides, and neodymium-dysprosium price swings exceed 40% annually. Such volatility undermines cost forecasts for permanent magnet motors and forces procurement hedges. Automakers fund SRM R&D and ferrite-magnet hybrids to lower exposure, but these alternatives demand new control algorithms and inverter topologies. Recycling covers less than 5% of magnet demand, so infrastructure scale-up is urgent. Trade conflicts or export quotas could disturb supply for years, making contract pricing unpredictable and adding carry costs to inventories.

Thermal-Management Design Complexity Increases Development Costs

High-power motors generate heat fluxes that require oil-spray or triple-port channels, adding 15–25% to the total cost for >200 kW units. 800-V designs aggravate local hotspots that risk demagnetizing NdFeB rotors. Direct-oil winding cooling and embedded heat exchangers demand tight casting tolerances and contaminant control, raising capital outlays for assembly cells. Suppliers need specialized 2-D X-ray CT scans to validate flow passages, lengthening qualification lead times. These factors stretch program budgets and slow entry for newer automotive traction motor market firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Motor Type: PMSM Dominance Faces SRM Challenge

PMSMs accounted for 67.82% of automotive traction motor market share in 2024, reflecting high efficiency, strong torque density, and mature supply chains. SRMs recorded the quickest uptake at 19.21% CAGR, propelled by zero rare-earth content and improving acoustic refinement. AC induction motors stay relevant in the cost-controlled A-segment cars, where inverter simplicity matters, while DC types linger in niche auxiliary drives. BMW’s backing of DeepDrive and Renault-Valeo’s rare-earth-free collaboration signal how OEMs hedge technology bets to stabilize cost curves.

Manufacturing shifts favor SRMs for buses and trucks, where magnets compose a higher cost share of large-diameter rotors. Advances in digital current shaping narrow efficiency gaps with PMSMs, while silicon-carbide switches unlock fast phase transitions that curb torque ripple. As raw-material pressures persist, SRM penetration could reach double-digit automotive traction motor market size contribution by 2030.

By Cooling System: Liquid Dominance with Hybrid Innovation

Liquid-cooled assemblies owned 59.38% of the automotive traction motor market in 2024 because continuous coolant flow supports sustained loads and fast charging. Hybrid schemes are scaling 19.18% CAGR by blending forced air with localized coolant jackets for transient peaks. Air-only systems survive in low-power scooters where duty cycles remain intermittent. The arrival of R290 refrigerant loops improves heat extraction and compliance with climate rules.

Direct-oil winding techniques shrink copper mass and shorten magnetic circuits, enabling slimmer housings. Hybrid setups cut auxiliary pump power by activating liquid loops only above set thermal thresholds, saving range in mild climates. These innovations safeguard durability under 800-V pulses and are pivotal to broadening the automotive traction motor market in heavy-duty cycles.

By Application: Passenger Cars Lead, Two-Wheelers Surge

Passenger cars delivered 72.62% of revenue in 2024, anchored by multi-brand EV model launches and favorable total cost of ownership. Electric scooters and motorcycles accelerate at 20.28% CAGR, powered by Asian two-wheeler electrification incentives. Light commercial vans add steady demand from e-commerce fleets that must meet city zero-emission zones, while class 8 tractors adopt dual-motor e-axles for port drayage.

Musashi Seimitsu’s pact with Log9 Materials for Indian two-wheelers underlines localized motor-battery integration and supply-chain simplification. Predictable urban duty cycles let ride-sharing operators deploy standardized motor platforms, boosting the automotive traction motor market size among low-power classes. Bus OEMs exploit route homogeneity to tailor motor cooling, maximizing kilowatt-hour utilization during depot charging windows.

By Power Rating: Medium Power Dominates, High Power Accelerates

Motors in the 51–150 kW band occupied 49.31% of revenue during 2024 because this range overlaps mainstream crossover and sedan performance needs. Above 150 kW, demand grows 18.65% CAGR as premium SUVs, pickups, and medium-duty trucks electrify. Sub-50 kW units thrive in scooters, forklifts, and auxiliary HVAC compressors where per-kilowatt cost is paramount. Garrett Motion’s partnership with HanDe on heavy-truck e-axles confirms appetite for integrated 350 kW stacks.

Silicon-carbide inverters and high-flux laminations elevate high-power densities, shrinking motor mass without sacrificing torque. Fast-charge targets of 300 kW push designs toward larger diameter rotors to dissipate Joule heat. These workouts will widen the high-power tier's automotive traction motor market size beyond its present niche.

By Distribution Channel: OEM Dominance with Aftermarket Growth

OEM sales made up 89.36% of the automotive traction motor market in 2024, because motor selection, inverter calibration, and vehicle-control matching are finalized during assembly. An 18.94% CAGR is forecast for aftermarket demand as EV fleets age and specialized service networks spread. Remanufacturing centers extend motor life by replacing bearings and reprofiling rotor magnets, meeting sustainability imperatives.

Independent workshops invest in diagnostic rigs that emulate inverter pulse patterns to verify winding insulation. Data-driven predictive maintenance enables uptime guarantees for delivery fleets, unlocking recurring revenue. As warranty periods expire, cost-focused operators will seek refurbished units, nudging aftermarket share toward double digits by 2030.

Geography Analysis

Asia-Pacific generated 45.18% of revenue in 2024, building on China’s integrated battery-motor production clusters and India’s two-wheeler growth. ZF’s Shenyang plant produces modular e-axles covering 100–300 kW power bands with hairpin windings for domestic and export customers. Japan and South Korea contribute controller firmware and laminated-steel alloys, while Vietnam and Thailand lure contract manufacturers with tax holidays. Government NEV quotas and robust charging rollouts should preserve regional leadership in the automotive traction motor market through 2030.

Europe benefits from stringent fleet CO₂ targets and robust premium-EV demand. The Fit-for-55 package aligns carbon pricing with electrification, and Germany funnels R&D grants into drive technologies. Stellantis’ Leapmotor International venture imports cost-efficient Chinese platforms but adds final assembly in European plants to capture incentives. Supply-chain localization remains a hurdle as rare-earth oxides and lamination steel still rely on external producers, adding complexity to scaling the automotive traction motor market across the continent.

North America rides the Inflation Reduction Act’s content rules, sparking the reshoring of motor factories. General Motors allocated part of its USD 4 billion domestic cap-ex to high-volume drive-unit lines. Honda’s CAD 15 billion (USD 10.95 billion) Ontario complex links cathode refining with motor winding, knitting a complete EV value chain in one province. The North America record the strongest growth at 20.98% CAGR, fueled by the governments tax breaks that bundle vehicle plants with renewable-power generation.

Competitive Landscape

The automotive traction motor market is moderately concentrated. Tier-1 suppliers such as Bosch, Continental, and ZF exploit existing OEM relationships and compliance track records. Emerging Chinese specialists leverage cost advantages and state-supported credit lines to win second-tier programs. BorgWarner lifted eProduct revenue 31% in Q2-2025, proving legacy suppliers can pivot successfully.

OEM vertical integration reshapes bargaining power. General Motors’ Ultium Drive unites motor, reduction gear, and inverter to slash component duplication. Tesla, Lucid, and BYD guard large patent portfolios in rotor-bar geometry and winding topology, setting licensing barriers. Smaller assemblers outsource complete e-axles to system integrators that offer one-stop homologation, compressing development cycles.

Functional safety (ISO 26262) and electromagnetic compatibility certifications erect entry hurdles. Suppliers must validate designs in 800-V environments and across global noise standards. Governments that tie incentives to domestic production tilt competition toward local plants, prompting joint ventures or greenfield builds. Those missing regional footprints risk exclusion from procurement shortlists and threaten long-term relevance in the automotive traction motor market.

Automotive Traction Motor Industry Leaders

Tesla, Inc.

BYD Company Limited

Nidec Corporation

Robert Bosch GmbH

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Rivian kicked off construction on a USD 5 billion plant in Georgia, boasting a capacity of 400,000 units, spotlighting the growing investments in electric vehicles (EVs) across the southern United States. This development is expected to significantly impact the automotive traction motor market, as increased EV production drives demand for advanced traction motors

- April 2025: In a significant move, Garrett Motion has joined forces with Shaanxi HanDe to develop e-axles tailored for heavy trucks, with trial runs slated for 2026. This collaboration highlights the growing demand for advanced traction motor technologies in the automotive market, particularly in the heavy truck segment.

Global Automotive Traction Motor Market Report Scope

| AC Induction Motor |

| DC Motor |

| Permanent Magnet Synchronous Motor (PMSM) |

| Switched Reluctance Motor (SRM) |

| Liquid-Cooled |

| Air-Cooled |

| Hybrid Cooling |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Duty Trucks |

| Buses and Coaches |

| Off-Highway Vehicles |

| Industrial Machinery |

| Electric Scooters and Motorcycles |

| Low Power (Below 50 kW) |

| Medium Power (51-150 kW) |

| High Power (Above 150 kW) |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Motor Type | AC Induction Motor | |

| DC Motor | ||

| Permanent Magnet Synchronous Motor (PMSM) | ||

| Switched Reluctance Motor (SRM) | ||

| By Cooling System | Liquid-Cooled | |

| Air-Cooled | ||

| Hybrid Cooling | ||

| By Application | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Duty Trucks | ||

| Buses and Coaches | ||

| Off-Highway Vehicles | ||

| Industrial Machinery | ||

| Electric Scooters and Motorcycles | ||

| By Power Rating | Low Power (Below 50 kW) | |

| Medium Power (51-150 kW) | ||

| High Power (Above 150 kW) | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What CAGR is forecast for global traction motors through 2030?

An 18.52% CAGR is expected for the automotive traction motor market through 2030.

Which motor technology leads electric vehicle adoption?

Permanent-magnet synchronous motors hold 67.82% share, maintaining leadership through efficiency and power density.

Which region delivers the fastest demand growth?

The Middle East and Africa region is forecast to post a 20.98% CAGR as new policies and plants emerge.

How do rare-earth cost swings affect suppliers?

Volatile neodymium and dysprosium prices can alter motor costs by up to 40%, motivating OEMs to pursue rare-earth-free designs

What drives aftermarket expansion in electric traction motors?

A growing EV parc and new remanufacturing capabilities are expected to push the aftermarket toward an 18.94% CAGR by 2030.

Page last updated on: