Off Highway Vehicle Engine Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 47.94 Billion |

| Market Size (2031) | USD 66.21 Billion |

| Growth Rate (2026 - 2031) | 6.67% CAGR |

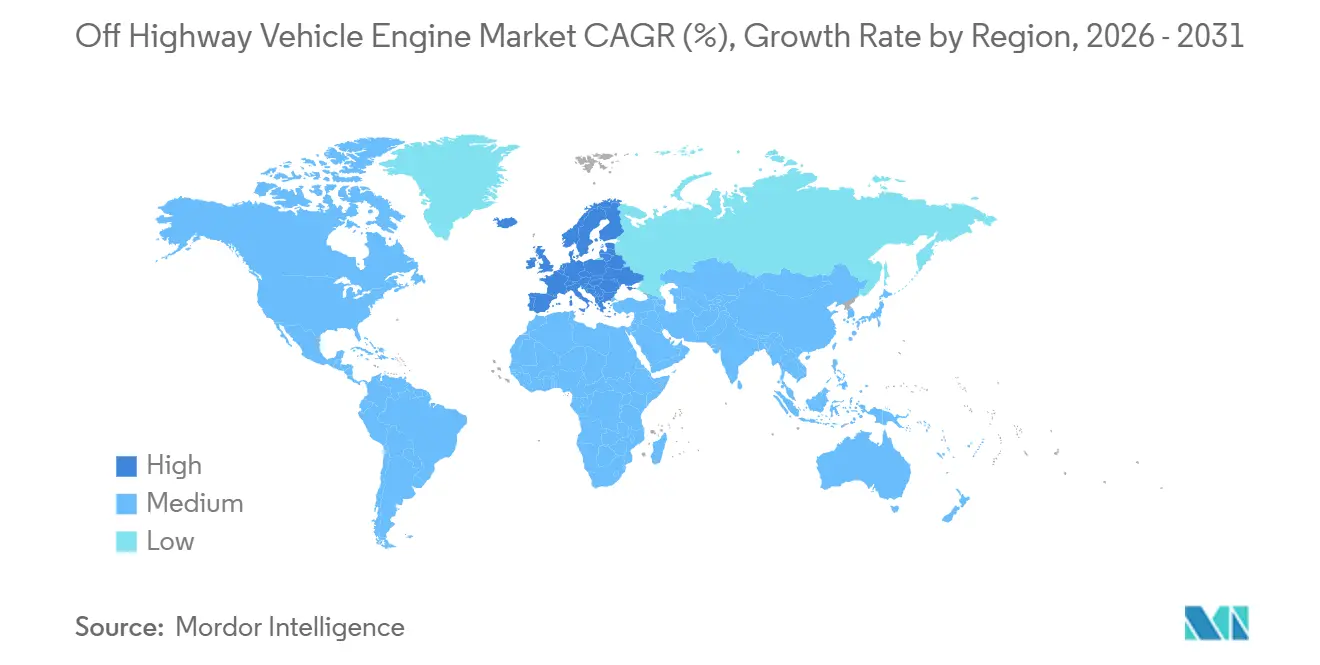

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

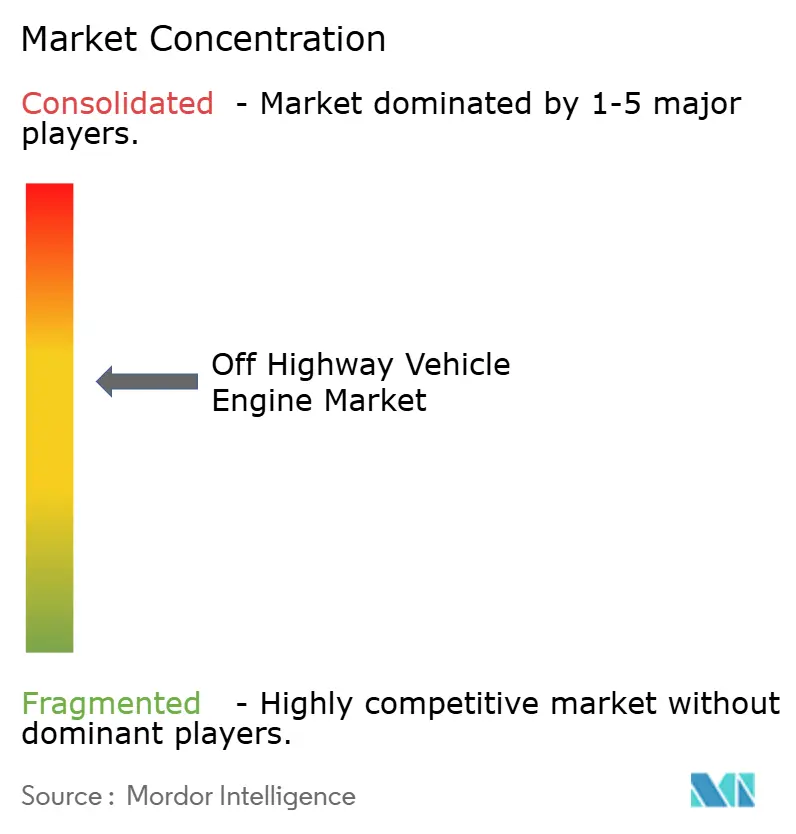

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Off Highway Vehicle Engine Market Analysis by Mordor Intelligence

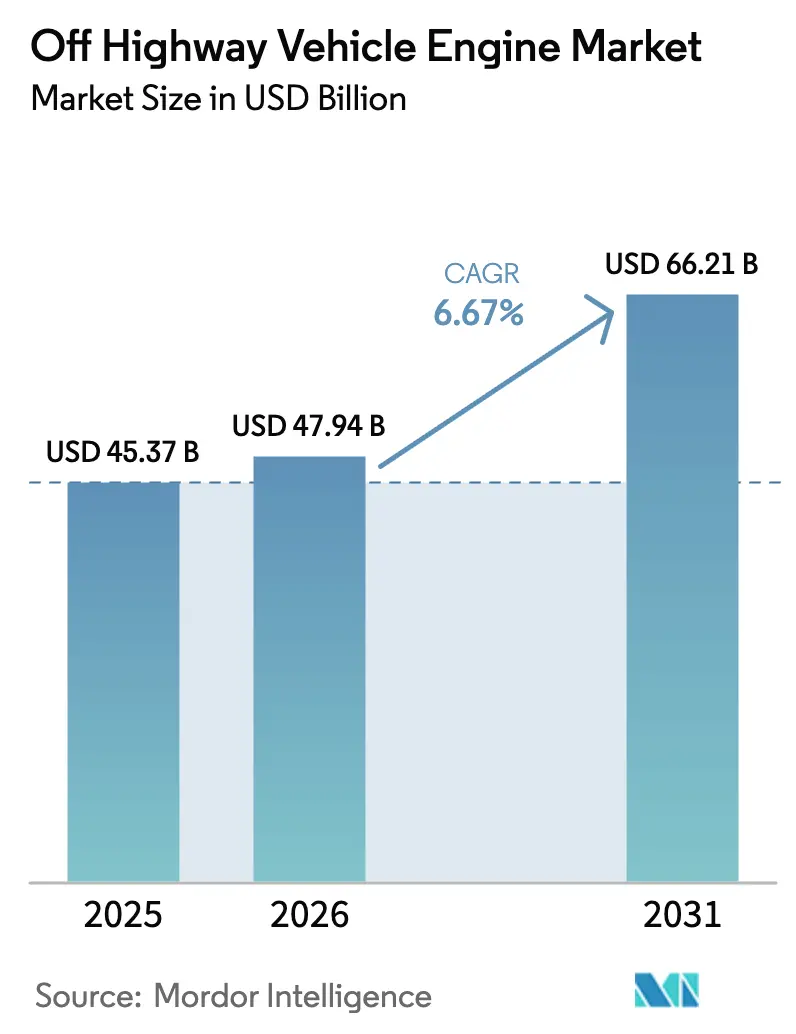

The off-highway vehicle engine market size is projected to be USD 45.37 billion in 2025, USD 47.94 billion in 2026, and reach USD 66.21 billion by 2031, growing at a CAGR of 6.67% from 2026 to 2031. Public‐sector infrastructure programs, large-scale mining for energy-transition metals, and rising farm mechanization form the principal demand pillars for the off-highway vehicle engine market. Contractors in Europe accelerated their purchases ahead of the EU Stage V implementation (2019 onward), while in the U.S., fleets continue to align with EPA Tier 4 Final and monitor CARB’s Tier 5 rulemaking work. However, the retrofit opportunity—especially in rental fleets—now surpasses the pre-buy volume as owners seek to keep older assets in service without breaching nitrogen oxide limits. Compact tractors and mini excavators in the 31-70 horsepower range dominate unit shipments, while mid-sized 3.6-7 liter diesel engines remain the revenue backbone, as they power wheel loaders, articulated dump trucks, and mid-horsepower farm machinery. Diesel continues to account for a notable share of the global fuel mix. Still, hybrid-ready platforms that accept 48-volt batteries or hydrogen tanks are gaining favor as OEMs de-risk future emissions mandates.

Key Report Takeaways

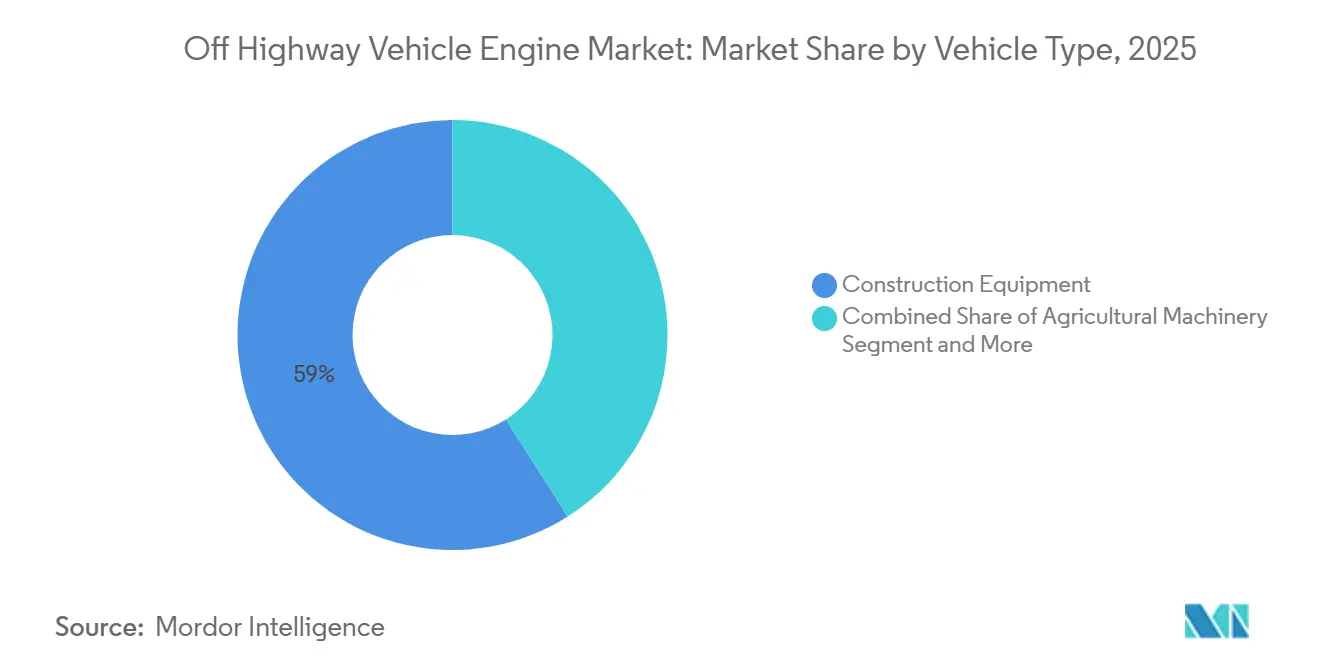

- By vehicle type, construction equipment accounted for 59.04% of the off-highway vehicle engine market share in 2025, while mining equipment is projected to register the fastest 8.33% CAGR through 2031.

- By power output, the 31-70 horsepower band accounted for 65.18% of the off-highway vehicle engine market size in 2025 and is forecast to grow at an 8.12% CAGR through 2031.

- By fuel type, diesel retained 88.33% of 2025 revenue, yet hybrid-electric and fuel-cell variants are advancing at a 6.95% CAGR through 2031.

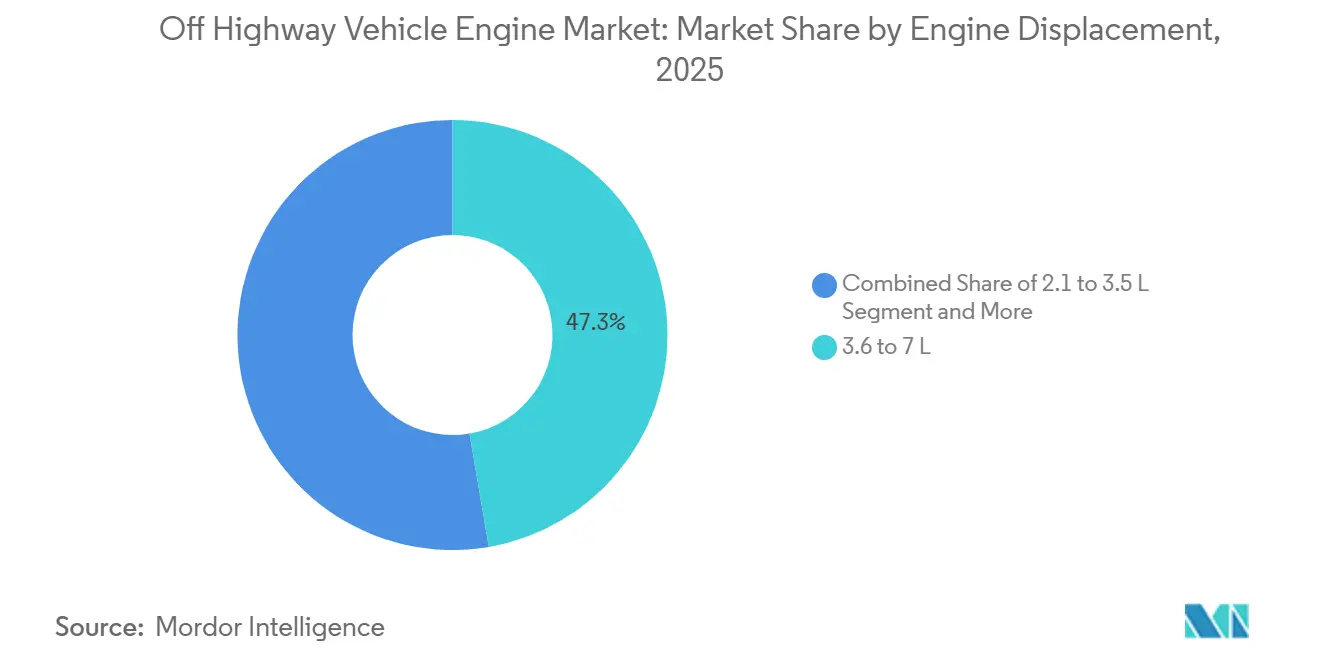

- By engine displacement, 3.6-7 liter units captured 47.25% of 2025 sales; engines below 2 liters are expanding at a 7.48% CAGR through 2031.

- By propulsion technology, conventional ICEs covered 88.41% of the 2025 volume, while battery-electric engines are projected to expand at a 7.86% CAGR through 2031.

- By geography, Asia-Pacific accounted for 39.12% of 2025 turnover, whereas Europe is forecast to post the fastest 7.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Off Highway Vehicle Engine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Massive Global Infrastructure Pipeline | +1.2% | Global, led by Asia-Pacific, Middle East, Africa | Medium term (2-4 years) |

| Growing Mechanization of Agriculture | +1.0% | Asia-Pacific, Sub-Saharan Africa | Long term (≥4 years) |

| Stricter Stage V / Tier 5 Norms | +0.9% | Europe, North America, Japan, South Korea | Short term (≤2 years) |

| Shift to Modular Hybrid Platforms | +0.7% | Global, early uptake in Europe, North America | Medium term (2-4 years) |

| HVO / Renewable-Diesel Compatibility | +0.6% | Europe, California, Canada | Medium term (2-4 years) |

| Telematics-Driven Predictive Maintenance | +0.5% | North America, Europe, major Asian cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Massive Global Infrastructure Pipeline (G7 and BRI)

Global initiatives, such as the G7 Partnership for Global Infrastructure and Investment and China's Belt and Road Initiative, are driving significant investments into roads, ports, and energy assets. These investments are creating substantial demand for heavy machinery in infrastructure projects. Canada's federal budget for the near future highlights a strong focus on transport and green-energy development, further underscoring the need for equipment such as crawler excavators and motor graders. Additionally, host nations often implement EU-style emissions regulations a few years after project completion. This trend benefits engine manufacturers with modular Stage V lines, enabling them to secure both initial equipment sales and subsequent retrofitting opportunities. Suppliers who strategically design components to meet these requirements are positioned to achieve higher lifetime revenue per engine. Historical trends confirm a strong correlation between infrastructure spending and construction equipment utilization, reinforcing the growth potential of the off-highway vehicle engine market.

Growing Mechanization of Agriculture in Asia-Pacific and Africa

In fiscal 2025, Indian farm-equipment credit disbursements experienced significant growth, driven by subsidies that substantially reduce the cost of new tractors. While Europe maintains a high density of tractors per hectare, Sub-Saharan Africa continues to operate at a much lower level, highlighting a considerable opportunity for replacement. In 2024, China's agricultural machinery production saw notable progress, with domestic manufacturers focusing on tractors designed for smallholder farms, equipped with engines suitable for their needs. Large commercial farms in Brazil and Australia favor 120-400 horsepower units with precision guidance, whereas Asian and African growers seek sub-50 horsepower designs financed over seven years, forcing engine builders to regionalize product lines. The bifurcated demand pattern sustains volume growth for compact diesels while supporting margin-rich high-horsepower models.

Stricter Stage V / Tier 5 Norms Triggering Pre-Buy and Retrofit Cycles

Compliance enforcement and fleet policies are increasing the focus on Stage V/Tier 4 Final compliant equipment. Meanwhile, California's proposed Tier 5 regulation aims to significantly reduce nitrogen oxides by the end of the decade. This has encouraged North American fleets to increase their procurement of Tier 4. However, rental companies, which represent a substantial portion of the fleet in the United States, are focusing on retrofitting diesel particulate filters and SCR kits rather than investing in new machinery, thereby extending the operational lifespan of their assets by several years. After-treatment suppliers, such as Donaldson and Dinex, therefore stand to gain recurring retrofit revenue even as new-unit growth moderates. The retrofit dynamic tempers headline sales volatility for the off-highway vehicle engine market while pushing a larger share of revenue into the aftermarket channel.

OEM Shift to Modular Hybrid-Ready Engine Platforms

Cummins offers B4.5 and B6.7 Stage V blocks with factory provisions for 48-volt battery packs so customers can add hybrid kits without chassis changes [1]“Product Press Kit 2024,” Cummins, cummins.com. Deutz unveiled a hydrogen-ready engine that shares most of its components with its diesel version, allowing factories to switch fuel types with minimal adjustments. This modular design reduces capital investment for OEMs compared to standalone electric platforms. However, it may face challenges if battery costs decline significantly in the coming years. As a result, hybrid readiness acts as a temporary strategy rather than a long-term solution for the off-highway vehicle engine sector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification of Compact Equipment | -0.8% | Europe, North America, China, Japan | Short term (≤2 years) |

| After-Treatment Cost vs Buyers | -0.6% | India, Southeast Asia, Africa | Medium term (2-4 years) |

| Price Volatility Squeeze Engine Margins | -0.5% | Global | Short term (≤2 years) |

| Rental Fleets Delay Overhauls | -0.4% | North America, Europe, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Electrification of Compact Equipment

Volvo CE’s ECR25 Electric excavator offers a full workday of runtime and significantly reduces diesel costs, enabling high-utilization contractors to achieve a return on investment within a reasonable timeframe. JCB’s 19C-1E and Caterpillar’s 301.9 electric minis provide comparable economic benefits for indoor or urban projects where zero emissions and low noise are critical. Battery-electric models are steadily gaining traction in Europe's sub-6-ton excavator market, with expectations of substantial growth as charging infrastructure continues to expand. The lower maintenance requirements, which eliminate oil changes and reduce the number of moving parts, further enhance the cost-effectiveness of battery-powered compact excavators. However, this shift primarily impacts smaller engines, while mid- and high-horsepower diesel engines remain largely unaffected for now.

Escalating After-Treatment Cost Vs. Price-Sensitive Buyers

Stage V kits significantly increase the cost of 100-150 horsepower engines, adding a notable percentage to the list price. Additionally, machines operating extensively incur substantial annual expenses for diesel exhaust fluid. In regions such as India and Southeast Asia, where buyers often include small contractors or individual farmers, these additional costs drive demand for older Tier 3 equipment available in secondary markets. In 2024, Mahindra reported that a considerable portion of its Indian tractor customers preferred models without advanced emission systems to reduce upfront costs. This persistent price sensitivity slows the adoption of emissions upgrades, limiting short-term growth in the off-highway vehicle engine market. It also creates opportunities for local suppliers to offer lower-specification products at more competitive prices than global players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Construction Dominates, Mining Accelerates

Construction machinery accounted for 59.04% of 2025 revenue, underscoring its dominance within the off-highway vehicle engine market size. Urbanization across Asia and stimulus-backed infrastructure renewal in the United States and the EU keep crawler excavators, wheel loaders, and backhoe loaders on high utilization schedules. Mining equipment, although smaller in volume, is the fastest riser; its 8.33% forecast CAGR aligns with the soaring demand for copper and lithium in EV supply chains, which require autonomous haul trucks and high-tonnage hydraulic shovels capable of operating for 4,000-5,000 hours per year. Agricultural machinery ranks second overall, with tractor density in Africa poised for multi-decade growth. At the same time, forestry and material-handling niches rely on diesel’s high energy density for remote or continuous-shift operations.

Recurring construction replacement every 7-10 years locks in a dependable baseline volume for engine suppliers, whereas the 12-15 year mining cycle produces a richer aftermarket parts annuity due to higher duty hours. Global OEMs dominate the construction sector but face regional fragmentation in agriculture, where Mahindra leads in India, Deere rules North America, and Weichai powers much of China. This mosaic makes scale economies elusive, yet it also protects specialized players that tailor engines to local regulation and fuel quality.

By Power Output: Mid-Range Engines Command Volume and Growth

The 31-70 horsepower bracket accounted for 65.18% of unit shipments in 2025 and is projected to expand at an 8.12% CAGR through 2031, underscoring its importance to the off-highway vehicle engine market. Compact tractors, skid-steer loaders, and mini excavators dominate this band, benefiting from subsidy programs that target smallholders and urban contractors. Kubota’s V5009 Stage V series exemplifies platform renewal, integrating maintenance-free particulate filters and variable-geometry turbochargers to meet both emissions and fuel-efficiency goals [2]“V5009 Engine Brochure,” Kubota, kubota.com.

Sub-30-horsepower engines power utility vehicles where batteries are already encroaching, while the 71-120-horsepower set serves mid-sized wheel and backhoe loaders. Units above 120 horsepower, although fewer in number, generate premium pricing and aftermarket revenue due to their demanding duty cycles in mining and large infrastructure projects. Suppliers with flexible architectures that span 31-120 horsepower, such as Yanmar and FPT Industrial, amortize R&D costs across volumes exceeding 50,000 units per year, a scale that is unreachable in the 400-horsepower-and-above niche.

By Fuel Type: Diesel Dominance Persists, Alternatives Emerge

Diesel owned 88.33% of the 2025 fuel mix, confirming its lock-in position within the off-highway vehicle engine market share. Its 35-38 MJ L-1 energy density and universal refueling infrastructure keep the total cost of ownership low for remote, high-load applications. Hybrid-electric and hydrogen variants together are projected to grow at a 6.95% CAGR through 2031, although they start from a small base. Volvo Penta’s D5 hybrid and Deutz’s H2 engine demonstrate technical feasibility, yet they face infrastructure and cost hurdles [3]“Hybrid Solutions White Paper,” Volvo Penta, volvopenta.com.

Gasoline and natural gas retain a marginal status, applicable mainly to stationary or light-duty applications. HVO’s plug-and-play compatibility extends the relevance of diesel, especially in Europe, where carbon pricing mitigates the cost premium. The consensus view now predicts that diesel will drop to a comparatively lower share in the next five years, rather than undergo a rapid phase-out, ensuring that every OEM must still invest in clean-diesel evolution, even while incubating electric and hydrogen lines.

By Engine Displacement: Mid-Size Dominates, Compact Grows Fastest

Engines between 3.6 and 7 liters captured 47.25% of 2025 revenue, benefiting from their fit with articulated dump trucks, mid-sized wheel loaders, and 90-140 horsepower tractors. Downsized blocks below 2 liters, however, are the growth champions, with a 7.48% CAGR, as hybrid architectures pair small diesels with electric assist, cutting fuel use without sacrificing torque. Deutz’s TCD 2.9, for instance, delivers up to 100 horsepower from a 2.9-liter package by adopting high peak cylinder pressures.

Engines above 7 liters cater to large mining equipment and high-horsepower dozers, a niche with limited volume but substantial margins. Turbocharging and direct-injection advances blur the historical link between displacement and power, allowing OEMs to meet output targets with lighter, more efficient engines. The trade-off is higher thermal stress, which shortens lubricant life, thereby shifting some savings from fuel to maintenance budgets.

By Propulsion Technology: ICE Leads, Battery-Electric Accelerates

Internal-combustion engines held 88.41% of 2025 shipments, yet battery-electric powertrains are clocking a 7.86% CAGR as charging stations spread across urban job sites. Hybrid systems occupy a middle ground, recapturing braking energy in duty cycles featuring frequent bucket dumps or travel between loads. Fuel-cell solutions capture a nominal share but may gain momentum where hydrogen production is co-located with mining or port operations.

Technology fragmentation will persist: battery packs dominate sub-6-ton machines, hybrids optimize medium excavators, and diesel or hydrogen combustion rules high-horsepower classes. OEMs able to service all three paths—Caterpillar, Komatsu, Volvo CE—stand to gain disproportionate customer stickiness as fleets diversify to meet both emissions and uptime targets.

Geography Analysis

Asia-Pacific controlled 39.12% of the off-highway vehicle engine market in 2025 and is expected to advance at a notable CAGR to 2031. China’s domestic construction boom and India’s significant jump in farm-equipment credit underscore the region’s dual growth engines. Japanese shipments softened, but exporters recouped volume in Southeast Asia, where Belt and Road projects remain active. South Korea’s HX Series excavators, fitted with Stage V engines, target Europe and North America, reflecting Asian OEMs’ push up the value curve.

Europe is the fastest-growing region, with a 7.23% CAGR, driven by Stage V retrofits and HVO adoption. Germany’s rail and renewable program keeps demand steady for mid-sized engines, while France’s precision-farming incentives lift tractor penetration. Post-Brexit trade deals widen export lanes for engine builders in the United Kingdom, like Perkins. Western sanctions curtail Russian demand for high-spec engines, allowing Chinese Tier 3 units to backfill the gap.

North America held a notable share of 2025 turnover, underpinned by the Infrastructure Investment and Jobs Act. In the United States, housing starts reached a significant milestone, driving increased demand for compact equipment. Meanwhile, Canada's extensive green-infrastructure initiative has stimulated purchases of crawlers and graders. In South America, market growth is supported by agricultural expansion in Brazil, particularly in soybean production, which boosts the need for high-horsepower tractors. The Middle East and Africa are experiencing steady growth, driven by large-scale development projects under Saudi Vision 2030 and equipment replacements in South African mines, although the market remains relatively smaller in size.

Regulatory Landscape

Emissions compliance continues to shape off-highway engine specifications and certification costs across major regions. In the United States, fleets and OEMs align with U.S. EPA nonroad compression-ignition requirements (Tier 4 Final), while California adds a second layer of compliance via CARB. Amendments related to California state nonroad engine pollution control standards for in-use off-road diesel-fueled fleets were formalized in January 2025, with phase-in provisions extending through 2036. CARB held a public workshop in February 2026 to discuss draft amendments for potential new off-road diesel engine emission standards, including updates to on-board diagnostics.

In Europe, EU Stage V remains the core framework under Regulation (EU) 2016/1628, with added administrative requirements for machinery that circulates on public roads. Regulation (EU) 2025/14 (adopted in December 2024) set rules for approval and market surveillance of non-road mobile machinery (NRMM) circulating on public roads, strengthening cross-border compliance expectations for OEMs and engine suppliers. Separately, the Netherlands published May 2026 research benchmarking real-world NRMM emissions using a dataset of about 90 mobile machines. This points to policy workstreams examining requirements beyond Stage V, even though no Stage VI standard has been enacted in that jurisdiction.

Value Chain Analysis

The off-highway vehicle engine value chain runs from raw materials and precision components through engine assembly and OEM machine integration, and then into service parts and aftertreatment maintenance in the installed base. Upstream, tier suppliers provide emission- and performance-critical subsystems such as high-pressure fuel systems, turbochargers, electronic control modules, and exhaust aftertreatment (DOC/DPF/SCR). Midstream, engine makers, including vertically integrated equipment OEMs and independent engine suppliers, conduct calibration, emissions certification, and end-of-line testing before shipping engines to construction, agricultural, mining, forestry, and material-handling OEM assembly lines.

Regulatory complexity (EU Stage V and U.S. EPA nonroad rules, plus evolving CARB activity) increases dependence on specialized aftertreatment and controls content, which lifts the role of emissions-component suppliers and software calibration capabilities in the overall cost stack. Downstream, dealer networks and fleet service providers capture recurring revenue from filters, sensors, DEF-related consumables, and repair events, while telematics ecosystems used by major OEMs strengthen parts pull-through and retention. Supply continuity for emissions-critical components remains a sensitivity point because compliant builds require synchronized availability of sensors, electronic modules, and aftertreatment hardware to avoid production interruptions.

Competitive Landscape

The off-highway vehicle engine market remains moderately concentrated: Cummins, Caterpillar, Deutz, Komatsu, and Volvo Penta together hold a significant share of global shipments. Vertically integrated OEMs like Caterpillar and Komatsu bundle engines with equipment, capturing lifecycle parts income, whereas independent suppliers such as Cummins and FPT Industrial court multi-brand customers. Off-highway engines represent a significant revenue stream for Cummins, but currently yield lower margins compared to on-highway lines. The company is working to address this disparity through its modular hybrid platforms.

Deutz took over sales and service for selected off-highway engines previously handled by Rolls-Royce Power Systems (MTU series), expanding Deutz's portfolio and service footprint. JCB’s hydrogen combustion engine targets users who lack fuel-cell infrastructure but must comply with zero-carbon mandates. In Southeast Asia and Africa, Chinese challengers Weichai and Yuchai have gained a significant foothold in the local agricultural segments by offering more cost-effective solutions compared to Western manufacturers. The competitive edge is increasingly reliant on telematics ecosystems; Deere’s JDLink and Caterpillar’s Product Link foster data lock-in, making engine swaps less appealing.

Off Highway Vehicle Engine Industry Leaders

Cummins Inc.

Caterpillar Inc.

Deere & Company

Weichai Power Co., Ltd.

Komatsu Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A whitespace is forming around fuel-flexible and renewable-fuel-compatible industrial engines that reduce integration friction for equipment OEMs while staying within tightening emissions constraints. At CONEXPO-CON/AGG 2026, John Deere introduced JD5 (5.0L) and JD8 (7.5L) industrial engines positioned for renewable diesel and biodiesel compatibility, supporting fleets that want lower-carbon liquid fuels without changing refueling logistics. In parallel, Kawasaki Engines launched production-ready GEOTORQ large spark-ignition engines designed for gasoline and E85 flex-fuel use in construction and agriculture, expanding the addressable market for non-diesel pathways where duty cycles and site fueling allow.

Another opportunity centers on compliance-driven upgrades in controls and aftertreatment that prepare platforms for stricter state-level or regional requirements. CARB continued moving its Tier 5 rulemaking work forward through draft activity and workshops, including February 2026 discussion of potential new off-road diesel standards and on-board diagnostics. That progression increases demand for engines and machine packages that can demonstrate low-load and in-use performance through robust OBD, sensors, and calibrated inducement strategies. Targeted electrification and hybridization in compact and specialized applications also creates room for suppliers that can provide drop-in power modules or hybrid-ready architectures while keeping diesel as the revenue backbone for mid- and high-horsepower equipment; Honda expanded its eGX electric power unit line with three high-output models announced for OEM supply starting in fall 2026, reflecting the OEM push toward packaged electrified power options in smaller power bands.

Recent Industry Developments

- July 2026: Cummins released updated diesel exhaust fluid (DEF) inducement calibrations to support customers operating its engines under emissions-control requirements. The updates reinforce Cummins software and controls capability as a lifecycle lever, helping fleets maintain compliance behavior and uptime without changing hardware.

- May 2026: Caterpillar showed the Cat Battery Electric Power Unit (BEPU) at IFAT 2026 in Munich, highlighting its integration in a Doppstadt SWS 6 Spiral Shaft Separator. Demonstrating a packaged electric power unit in a working equipment application broadens Caterpillar's pathway beyond diesel engines for certain off-highway duty cycles and expands electrified options for OEM integrators.

- May 2024: Caterpillar announced a USD 90 million investment in Texas to prepare facilities for production of the Cat C13D industrial engine, with production slated to begin in 2026. The capacity and manufacturing-readiness spend supports product renewal in core industrial power bands that anchor revenue in construction and other off-highway equipment categories.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the value of engines and hybrid power units that are installed in off-highway equipment at the point of manufacture and used in sectors like construction, agriculture, mining, forestry, and material handling.

Scope exclusions: We exclude retrofit engine replacements, standalone battery packs, and engines sold mainly for stationary generator sets or marine use.

Segmentation Overview

- By Vehicle Type

- Agricultural Machinery

- Construction Equipment

- Mining Equipment

- Forestry and Material-Handling Equipment

- By Power Output

- Less than or equal to 30 HP

- 31-70 HP

- 71-120 HP

- 121-400 HP

- More than 400 HP

- By Fuel Type

- Diesel

- Gasoline

- Natural-/Bio-Gas

- Hybrid-Electric and Fuel-Cell

- By Engine Displacement

- Less than or equal 2 L

- 2.1 to 3.5 L

- 3.6 to 7 L

- More than 7 L

- By Propulsion Technology

- Conventional ICE

- Hybrid

- Battery-Electric

- Fuel-Cell Electric

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Egypt

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by locking down what counts as an off-highway engine and what does not, and then gathering the best public indicators that move demand and pricing. We typically reference sources such as US EPA and EU emissions rules (to map engine families and compliance timelines), government industrial production and construction spending series, customs trade statistics for engine and parts flows, and trade association updates tied to construction and agricultural equipment.

Alongside this, we review company annual reports, investor presentations, earnings call notes, and product catalogs to understand engine lineups, power ranges, and model change cycles. A paid subscription is also used selectively for company financials and for structured news and filings so that assumptions can be cross-checked quickly across regions and time. These desk research inputs are not exhaustive, and many other public and paid sources were also used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work is used to pressure test the desk assumptions, especially around engine mix, OEM build plans, and how pricing changes with emissions upgrades and power bands. We spoke with a spread of OEM-side and supply chain roles (including sales, product, operations, and service teams) and also with industry experts across major demand regions so gaps in public data could be closed with practical checks.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 14% | APAC: 44% |

| Mid tier: 48% | Functional/Unit leaders: 27% | EMEA: 33% |

| Smaller Players: 16% | Managers: 59% | Americas: 23% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up approach, where the main build starts from off-highway equipment activity and then reconstructs engine demand by applying engine fitment and power-band shares across key applications. Results are then cross-checked with selective bottom-up approximations, such as sampled engine ASP by power range multiplied by implied volumes, plus supplier and channel checks, so totals can be adjusted when the first pass looks too high or too low.

In practice, we track a few market fingerprints that consistently explain movements in this space, such as construction equipment shipments and utilization, agriculture tractor and harvester production trends, mining capex cycles, emissions stage changeovers that shift cost and mix, and the split of demand by horsepower bands (including the tail of above-400 HP). When a data point is missing for a smaller country or niche equipment class, the gap is handled using proxy indicators from the closest comparable market and then normalized during validation.

For forecasting, scenario analysis is used with a base case that links demand to equipment production outlooks and macro indicators, and then adjusts for expected mix shift between diesel, alternative fuels, and hybridized platforms. Final forecast paths are refined using the consensus ranges heard in interviews, especially around pricing progression during emissions upgrades and periods of weak equipment build.

Data Validation & Update Cycle

Checks are run in layers so the model stays realistic. The first pass is compared against independent signals, such as equipment build trends by application, known emissions transition timing, and trade and production direction by region. When a variance looks unusual, the inputs are re-checked, and follow-up calls are triggered to confirm whether the issue is mix, pricing, or a scope mismatch.

Before sign-off, the work is reviewed by another analyst who replays the key assumptions and replicates the math for the main roll-ups. The report is refreshed annually, and interim updates are made when material events occur, such as a major regulatory shift or a clear demand break. Right before delivery, a fresh scan is done so clients receive the latest updated view.

Mordor Intelligence's Off Highway Vehicle Engine Market Size Compared Against Other Published Estimates

It is normal to see different market sizes for off-highway vehicle engines because publishers do not always count the same engine scope, the same installation point, or even the same timing for currency conversion and price updates.

By tracking engine fitment by equipment type and power band, and then refreshing exchange-rate timing and emissions driven ASP steps, Mordor Intelligence keeps the total tied to factory-installed off-highway demand and avoids mixing in retrofit replacements or adjacent stationary engine categories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 47.94 B (2026) | |

| Trade Data Aggregator A | USD 28.02 B (2024) | Uses an earlier base year and often frames the market through reported revenues and shipment splits, which can undercount higher horsepower engines and may treat some hybrid power units and OEM-installed content differently. |

| Industry Publisher B | USD 28.60 B (2024) | Built on a 2024 base and a different segmentation lens, which can shift what is included under off-highway engines and how price steps from emissions compliance are applied across applications and regions. |

The spread is mainly explained by year alignment and by what is counted as an off-highway engine sale, especially around hybrids, very high power engines, and whether replacement demand is bundled into the total. Our approach stays repeatable because the market is rebuilt from clear demand drivers, then reconciled with pricing and mix checks before the final number is published.

Key Questions Answered in the Report

What is the current value of the off-highway vehicle engine market?

The off-highway vehicle engine market size reached USD 47.94 billion in 2026 and is projected to reach USD 66.21 billion by 2031.

Which segment leads unit demand by power band?

Engines rated 31-70 horsepower dominate, supplying 65.18% of 2025 shipments and growing at an 8.12% CAGR.

How fast are battery-electric off-highway engines growing?

Battery-electric powertrains are projected to expand at a 7.86% CAGR through 2031, mainly in compact equipment used in urban settings.

Which region grows the quickest to 2031?

Europe is forecast to advance at a 7.23% CAGR through 2031, driven by Stage V retrofits and renewable-diesel adoption.

Page last updated on: