Dried Herbs Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

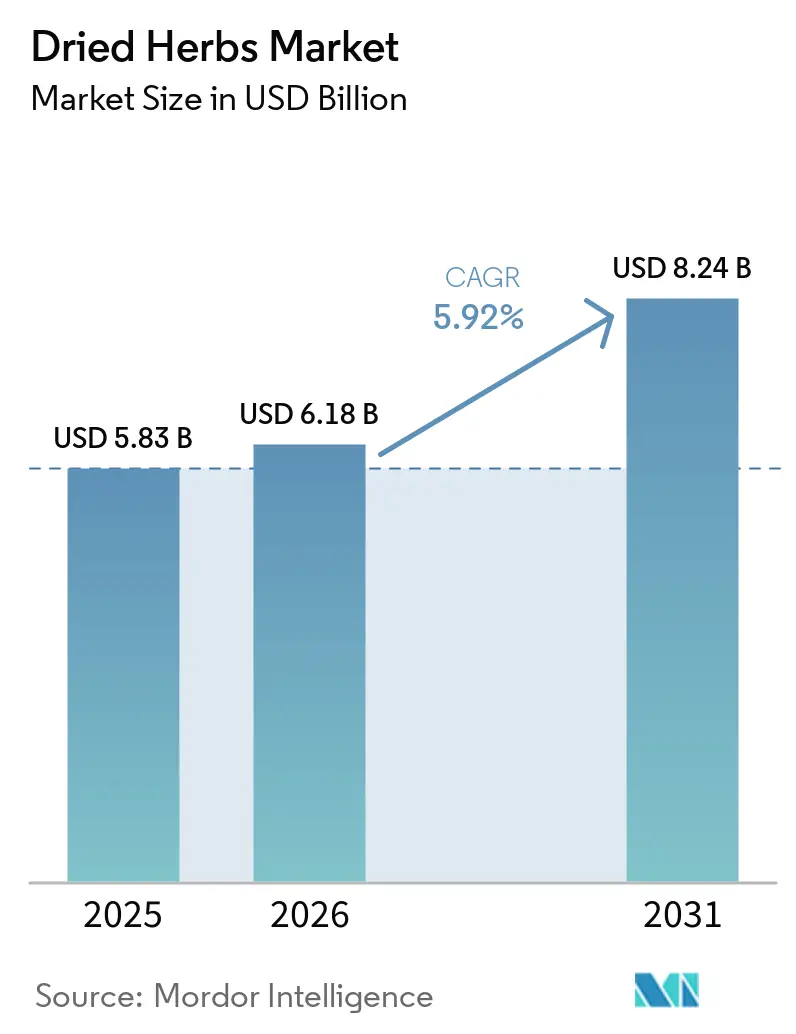

| Market Size (2026) | USD 6.18 Billion |

| Market Size (2031) | USD 8.24 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dried Herbs Market Analysis by Mordor Intelligence

The dried herbs market is projected to grow significantly, with its size estimated at USD 5.83 billion in 2025, USD 6.18 billion in 2026, and reaching USD 8.24 billion by 2031, reflecting a CAGR of 5.92% during the forecast period from 2026 to 2031. This growth is driven by increasing demand from food manufacturers and foodservice operators seeking clean-label seasonings, convenient formats, and authentic global flavors. Additionally, home cooks are increasingly opting for ready-to-use herb blends that save preparation time. Among product types, basil led revenue in 2025 due to its versatility across cuisines, while mint is anticipated to grow the fastest through 2031, supported by its rising use in beverages and nutraceutical products. Powdered and flake formats are gaining popularity over whole leaves because they offer controlled particle sizes and faster rehydration, catering to processors' needs. Furthermore, organic dried herbs are growing faster than conventional options, as retailers prioritize products with third-party certifications.

Key Report Takeaways

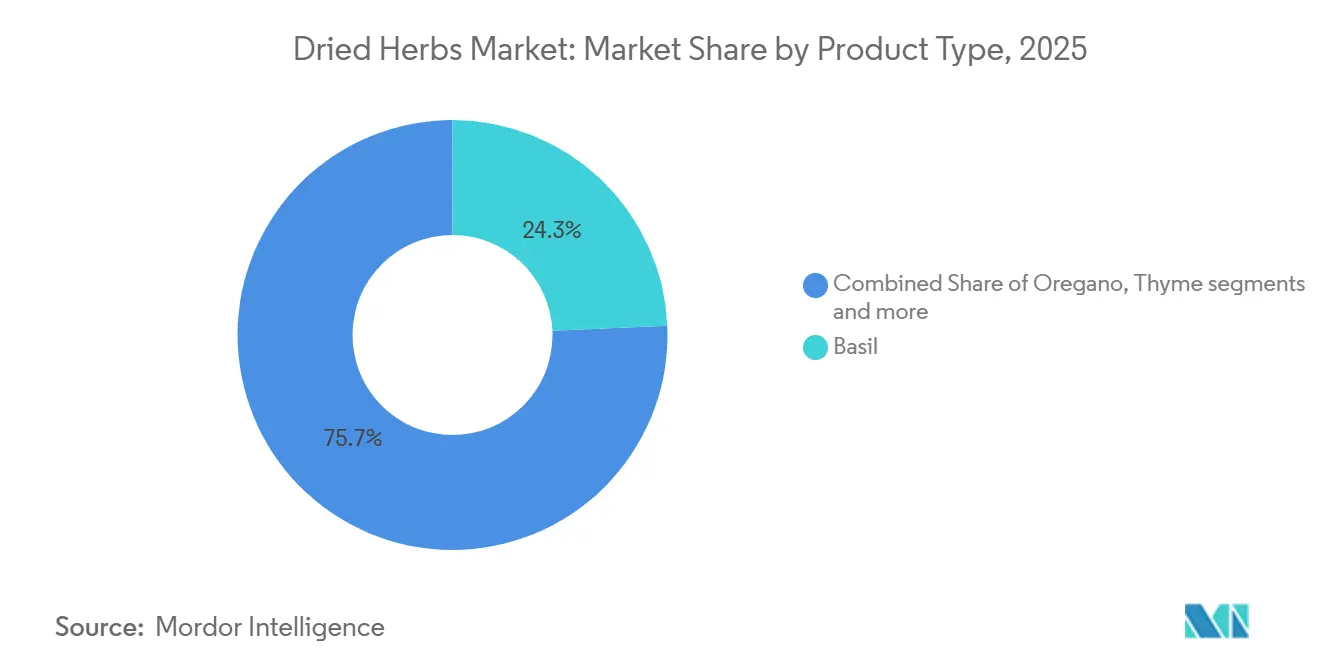

- By product type, basil captured 24.31% of the dried herbs market share in 2025, whereas mint is forecasted to grow at a 7.35% CAGR through 2031.

- By form, whole herbs led with 46.67% revenue in 2025, while powdered and flake formats are advancing at a 6.73% CAGR through 2031.

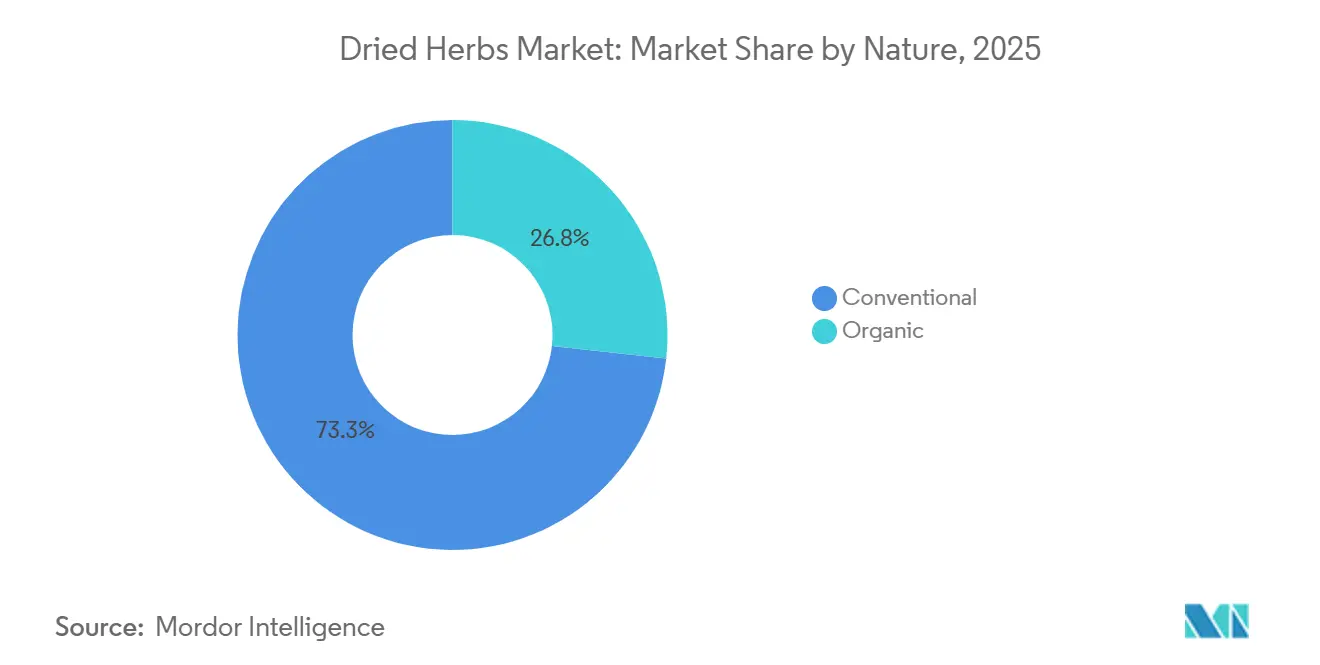

- By nature, conventional products accounted for 73.25% of the 2025 revenue, yet organic products are forecast to grow at a 6.22% CAGR through 2031.

- By end use, the industrial segment held 42.18% share of the dried herbs market size in 2025, and HoReCa is expanding at a 7.41% CAGR through 2031.

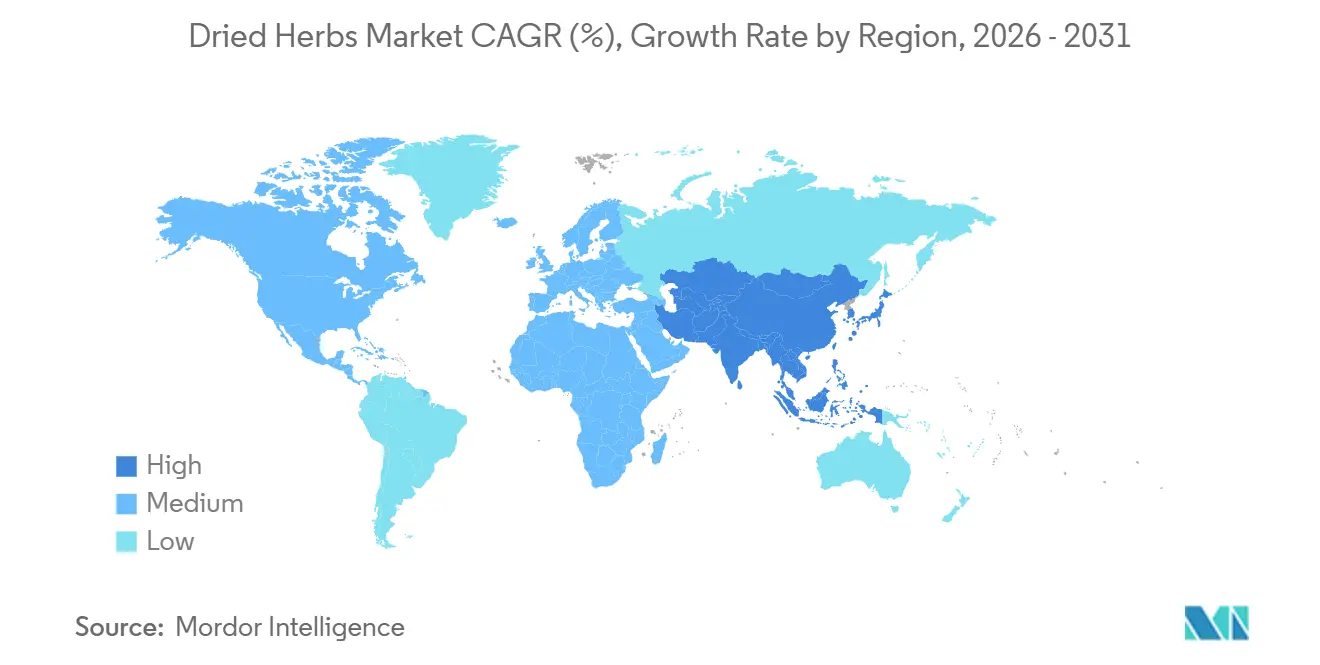

- By geography, North America accounted for 34.53% of the 2025 global value, and Asia-Pacific is projected to post the fastest regional CAGR of 6.82% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Dried Herbs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of spice and herb blends in convenience cooking | +1.2% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Growing popularity of international and ethnic cuisines | +1.0% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Rising consumer preference for natural and clean-label ingredients | +0.9% | North America, Europe, premium Asia-Pacific | Long term (≥ 4 years) |

| Advancements in drying technologies that improve flavor retention | +0.7% | North America, Europe, developed Asia-Pacific | Long term (≥ 4 years) |

| Increasing use of herbs in functional beverages and infusions | +0.8% | North America, Europe, health-driven Asia-Pacific | Medium term (2-4 years) |

| Product innovation in blends, seasonings, and infused herbs | +0.6% | North America, Europe, premium foodservice | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adoption of spice and herb blends in convenience cooking

The growing use of spice and herb blends in convenience cooking is significantly driving the dried herbs market, as consumers increasingly prefer quick, hassle-free meal preparation. According to a June 2024 survey by ScienceDirect, 97% of respondents reported using fresh herbs in food preparation or presentation, with 94% specifically using them to enhance flavor[1]Source: Science Direct, "Sweet basil: An Increasingly Popular Culinary Herb", sciencedirect.com. This strong inclination toward herb-based flavoring is now translating into a growing demand for dried herb formats, which offer greater convenience and longer shelf life. In regions like North America and Western Europe, consumers are increasingly opting for pre-measured spice blends and single-use sachets that streamline cooking processes and save time. Food manufacturers are actively promoting powdered and flake formats for their ease of incorporation into packaged foods. Region-specific blends, such as Italian and Middle Eastern mixes, are also gaining popularity, enabling consumers to recreate authentic flavors at home without advanced culinary expertise.

Growing popularity of international and ethnic cuisines

The increasing demand for international and ethnic cuisines is significantly driving the global dried herbs market, as consumers actively seek diverse and authentic flavors influenced by digital food media and evolving urban dining trends. According to a June 2024 survey by ScienceDirect, 74% of consumers use herbs for their aromatic qualities, while 68% utilize them for garnishing, underscoring their expanding role beyond traditional flavoring[2]Source: Science Direct, "Sweet basil: An Increasingly Popular Culinary Herb", sciencedirect.com . The rising popularity of cuisines such as Thai, Mediterranean, and Latin has further fueled the demand for specific herbs, supported by robust global supply chains from key producers like India. In Western markets, restaurants are increasingly incorporating region-specific herbs, such as Sicilian oregano and Thai basil, to create distinctive menus and cater to consumers seeking genuine culinary experiences. Moreover, herbs and seasonings, once confined to specialty stores, are now widely available in mass retail outlets, with limited-time product offerings contributing to increased consumer demand and higher supplier volumes.

Rising consumer preference for natural and clean-label ingredients

Consumer demand for natural and clean-label ingredients continues to drive the global dried herbs market, as individuals increasingly prioritize products without artificial additives or preservatives. This trend has prompted retailers in key markets such as the United States, Germany, and France to enforce stricter shelf standards, phasing out products that fail to meet clean-label criteria. Consequently, the demand for organic herbs has witnessed steady growth, despite the rising compliance costs associated with certifications under frameworks like USDA and EU regulations. Innovations in processing technologies, including freeze-drying and spray-drying, have further supported this trend by preserving the natural color, aroma, and essential oils of herbs, enabling manufacturers to market them as “minimally processed” and command premium pricing. Moreover, suppliers that emphasize full traceability and transparent sourcing are gaining a competitive edge, particularly in private-label programs, as clean-label positioning fosters consumer trust and drives higher value realization in the market.

Increasing use of herbs in functional beverages and herbal infusions

The growing incorporation of herbs in functional beverages and herbal infusions is significantly driving the global dried herbs market. Ingredients such as mint, basil, and rosemary are increasingly being utilized not only for their culinary value but also for their health and wellness benefits. In regions like North America and Europe, beverage manufacturers are actively innovating, with a surge in herbal-infused product launches that highlight specific benefits—such as mint for promoting breath freshness and basil for its adaptogenic properties. Regulatory frameworks in these regions are relatively flexible, allowing companies to make structure-function claims without undergoing the lengthy pharmaceutical approval process, thereby accelerating product development timelines. Additionally, manufacturers are favoring spray-dried herb powders due to their superior solubility and uniformity, which enhance the consistency of beverage formulations. This rising demand for dried herbs is also driving upstream supply chain growth, prompting increased cultivation in major producing countries such as Egypt, India, and Morocco to meet expanding market demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility linked to seasonal and climate swings | -0.8% | India, Indonesia, Turkey, Mediterranean exporters | Short term (≤ 2 years) |

| Susceptibility to microbial contamination such as Salmonella | -0.6% | North America, Europe, regulated Asia-Pacific | Medium term (2-4 years) |

| Lack of global standards for herb quality and grading | -0.4% | Fragmented supply chains in Asia, Africa, Latin America | Long term (≥ 4 years) |

| Adulteration and mislabeling across the supply chain | -0.5% | High-value herbs in opaque global channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price volatility of raw herbs due to seasonal dependency and climate conditions

Price volatility of raw herbs, driven by seasonal dependency and climate variability, poses a significant challenge in the global dried herbs market, creating uncertainty for suppliers and processors alike. Erratic weather patterns, such as unpredictable monsoons and prolonged droughts, have adversely affected crop yields in major producing countries like Indonesia and India, leading to supply shortages and sharp price fluctuations. High-value herbs, including vanilla, saffron, and black pepper, are particularly vulnerable to sudden price surges, which disrupt procurement strategies and compress profit margins for manufacturers. While buyers attempt to mitigate these risks by diversifying sourcing to regions such as Egypt and Peru, this approach often results in longer lead times and inconsistencies in flavor and quality. Furthermore, the absence of robust futures markets and the substantial capital investment required for implementing climate-resilient agricultural practices hinder producers' ability to stabilize supply chains, exacerbating the volatility in the market.

Susceptibility to microbial contamination, including pathogens such as Salmonella and E. coli

Microbial contamination, particularly from pathogens such as Salmonella and E. coli, continues to pose a significant challenge in the global dried herbs market, driving up compliance costs and complicating operational processes. Regulatory bodies, including the U.S. Food and Drug Administration, have consistently flagged contamination risks in imported herbs and spices, with a 2024 scientific review revealing that around 16.4% of herbal product samples exceeded permissible contaminant limits, primarily due to microbial issues[3]Source: Research Gtae, "Contamination of Herbal Medicinal Products in Low-and-Middle-Income Countries: A Systematic Review", researchgate.net. In response, authorities such as the European Food Safety Authority have implemented stricter thresholds, compelling exporters to adopt advanced treatments, such as steam pasteurization or irradiation, which significantly increase processing costs. Retailers are intensifying audit protocols and demanding enhanced traceability measures, creating hurdles for smaller exporters attempting to penetrate premium markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Basil Dominates, Mint Accelerates on Beverage Demand

Basil continues to hold a dominant position in the dried herbs market, accounting for 24.31% of market share in 2025. Its widespread appeal is driven by its essential role in popular cuisines such as Italian, Mediterranean, and Asian, where it is valued for its distinctive aroma and versatility. Frequently used in sauces, seasonings, and ready-to-cook meals, basil has become a staple ingredient in both home kitchens and professional foodservice settings. The consistent demand across these sectors underscores its importance as a key component in global culinary practices.

Meanwhile, mint is emerging as the fastest-growing segment in the dried herbs market, with a projected CAGR of 7.35% through 2031. This rapid growth is fueled by its increasing application in beverages, confectionery, and health-focused products, where its refreshing flavor is highly sought after. Additionally, mint’s perceived health benefits, such as aiding digestion and promoting overall wellness, have made it particularly attractive to health-conscious consumers. As food and beverage manufacturers continue to innovate with mint-based formulations, its adoption is expanding across various product categories, solidifying its position as a high-growth herb in the market.

By Form: Whole Herbs Lead, Powdered Formats Gain on Industrial Efficiency

Whole-leaf formats continue to dominate the dried herbs market, accounting for a significant 46.67% share in 2025. This dominance is attributed to their natural appearance, robust aroma, and perceived superior freshness compared to processed alternatives. These formats are particularly popular in home cooking and foodservice sectors, especially in cuisines that prioritize authentic flavors and visual appeal. Additionally, whole leaf herbs are highly sought after in premium and organic product categories, further solidifying their stronghold in the market. Their versatility and alignment with consumer preferences ensure their sustained demand across various regions.

On the other hand, powdered and flake formats are rapidly emerging as the fastest-growing segment, with a projected CAGR of 6.73% through 2031. This growth is primarily driven by the increasing demand for convenience, ease of use, and extended shelf life across household and industrial applications. These formats are extensively utilized in packaged foods, seasoning mixes, and ready-to-eat meals, where uniform flavor distribution and consistency are critical. Moreover, food manufacturers are increasingly adopting powdered herbs for their efficiency in large-scale production and formulation processes. As a result, powdered and flake herbs are gaining significant traction, positioning themselves as a key growth area within the market.

By Nature: Conventional Dominates, Organic Gains on Clean-Label Mandates

Conventional dried herbs continue to lead the global market, holding a significant 73.25% share as of 2025. This dominance is attributed to their widespread availability, cost-effectiveness, and strong demand across both household and foodservice sectors. The large-scale production of conventional herbs ensures affordability and accessibility, making them a preferred choice for mass-market consumers. These herbs are extensively utilized in packaged foods, seasoning mixes, and bulk culinary applications, further solidifying their position as the go-to option for everyday use.

On the other hand, organic dried herbs are steadily gaining momentum, with a projected CAGR of 6.22% through 2031. This growth is fueled by rising consumer awareness regarding health, sustainability, and clean-label preferences. Organic herbs appeal to premium consumers who value chemical-free and environmentally sustainable products. Additionally, food manufacturers are increasingly incorporating organic herbs to align with the growing demand for natural and organic product offerings. As a result, organic dried herbs are carving out a niche as a premium and value-added segment within the market.

By End Use: Industrial Leads, HoReCa Surges on Menu Innovation

Industrial processors continue to dominate the global dried herbs market, capturing 42.18% of the total market share in 2025. This leadership stems from their ability to procure large volumes of dried herbs and meet the consistent demand from packaged food manufacturers, seasoning producers, and ready-to-eat meal companies. These processors benefit from the standardized flavoring, extended shelf life, and seamless integration of dried herbs into large-scale production processes. Additionally, their well-established supply chain networks and bulk purchasing power further solidify their stronghold in the market, making them a critical segment driving overall market performance.

On the other hand, the HoReCa (Hotels, Restaurants, and Catering) segment is emerging as the fastest-growing end-use category, with a projected CAGR of 7.41% through 2031. This growth is primarily attributed to the revival of the foodservice industry and the rising consumer inclination toward dining out and exploring diverse cuisines. Chefs and foodservice providers are increasingly incorporating a broader range of dried herbs to enhance the taste, aroma, and presentation of dishes. Furthermore, the growing popularity of global cuisines and premium dining experiences is fueling the demand for high-quality dried herbs, positioning the HoReCa segment as a significant contributor to market expansion.

Geography Analysis

North America continues to dominate the global dried herbs market, contributing 34.53% of the total market value in 2025. This leadership is attributed to stringent regulatory frameworks and a growing emphasis on traceable and safe supply chains, particularly in the United States. Domestic cultivation is expanding across key states, driven by increased supplier audits and heightened food safety concerns. Canada is experiencing rising demand fueled by the popularity of multicultural cuisines, while Mexico remains a critical regional supplier. However, smaller exporters are facing challenges due to escalating compliance costs, leading to greater consolidation within the supply chain.

The Asia-Pacific region is emerging as the fastest-growing market, with a projected CAGR of 6.82% through 2031. This growth is primarily driven by the rising middle-class population and their increasing preference for global cuisines. India and China are leading contributors, supported by robust domestic production and export capabilities. India is scaling its production to meet international demand, while urban centers in China are witnessing a surge in interest in herb-rich and fusion cuisines. Additionally, countries like Indonesia, Thailand, and Vietnam are exploring organic herb production, although they face challenges related to certification and high costs. Meanwhile, Australia and New Zealand depend heavily on imports due to limited domestic production caused by environmental constraints.

Europe, South America, and the Middle East and Africa present a diverse market landscape, characterized by mature demand in some regions and emerging supply opportunities in others. European countries such as Spain, Germany, and the United Kingdom exhibit strong import demand, driven by trends like premiumization and organic product consumption, though compliance with strict regulations remains a challenge. In South America, Peru is enhancing its export capabilities through improved logistics, while Chile and Argentina serve as pivotal regional trade hubs. In the Middle East and Africa, nations like Egypt and Turkey continue to dominate exports despite logistical hurdles, while countries such as Nigeria and South Africa are gradually expanding their production amid regulatory challenges.

Competitive Landscape

The global dried herbs market is characterized by moderate consolidation, with prominent players such as McCormick & Company, Olam Food Ingredients, Ajinomoto Co., Fuchs Group, and Kerry Group dominating the competitive landscape. These companies leverage extensive global sourcing networks, diverse product offerings, and strong partnerships with food manufacturers to maintain their market positions. Through strategic acquisitions and expansions, they are enhancing their capabilities in value-added herb applications. Their ability to ensure consistent quality, adhere to regulatory standards, and secure long-term supply agreements further solidifies their leadership in the market.

Major players are increasingly focusing on integrating advanced technologies to improve traceability, quality assurance, and operational efficiency across the supply chain. Technologies such as near-infrared spectroscopy, blockchain-based tracking systems, and standardized certifications are becoming critical in differentiating suppliers. Food manufacturers are prioritizing partnerships with suppliers that comply with global standards like HACCP and ISO certifications, leading to stable, multi-year contracts. These technological advancements not only create significant entry barriers for smaller competitors but also enable larger firms to maintain pricing power and ensure reliable supply, making technology adoption a key factor in sustaining competitive advantage.

On the other hand, smaller and niche brands are carving out their space by emphasizing transparency, organic sourcing, and ethical trade practices to attract premium consumers. Companies offering Fair-Trade and clean-label products are gaining popularity, particularly in developed markets where consumer preferences are shifting toward sustainable and high-quality options. Additionally, opportunities are emerging in specialized areas such as premium processing techniques, including cryogenic milling, and customized herb blends tailored for ethnic and functional food applications. Mid-sized firms that invest in advanced authentication methods and rigorous quality verification processes are building trust with consumers and securing higher-margin contracts. This evolving dynamic allows niche players to thrive alongside industry giants by targeting differentiated and premium market segments.

Dried Herbs Industry Leaders

-

McCormick & Company

-

OFI (Olam Food Ingredients)

-

Ajinomoto Co.

-

Fuchs Group

-

Kerry Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Marubeni Corporation completed the full acquisition of Royal Euroma, broadening its global herbs portfolio and private-label manufacturing reach.

- September 2024: American Herbal Products Association petitioned the U.S. Trade Representative to eliminate tariffs on Chinese herb imports that inflate supply-chain costs.

- January 2024: McCormick® has unveiled its latest offering, Flavor Maker Seasonings, designed to elevate meals effortlessly. This new line boasts 15 distinct blends, allowing home cooks of all skill levels to enhance dishes – be it ramen or rice – with ease.

Global Dried Herbs Market Report Scope

Dried herbs are plant leaves, flowers, or stems that have been dehydrated to preserve their flavor, aroma, and shelf life for different uses. The global dried herbs market is classified into product type, form, nature, end use, and geography. Based on product type, the market is classified into oregano, basil, thyme, rosemary, mint, parsley, bay leaves, and other product types. Based on form, the market is classified into whole, rubbed/crushed, powdered/flakes. Based on nature, the market is classified into organic and conventional. Based on end use, the market is classified into industrial, horeca/foodservice, and retail. Based on geography, the market is classified into North America, Europe, Asia-Pacific, South America and Middle East and Africa. The market forecasts are provided in terms of value (USD).

| Basil |

| Oregano |

| Thyme |

| Rosemary |

| Mint |

| Parsley |

| Bay Leaves |

| Other Product Types |

| Whole |

| Rubbed/Crushed |

| Powdered/Flakes |

| Organic |

| Conventional |

| Industrial | Food and Beverages Processing |

| Personal Care and Cosmetics | |

| Pharmaceuticals | |

| HoReCa/Foodservice | |

| Retail/Household |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Basil | |

| Oregano | ||

| Thyme | ||

| Rosemary | ||

| Mint | ||

| Parsley | ||

| Bay Leaves | ||

| Other Product Types | ||

| By Form | Whole | |

| Rubbed/Crushed | ||

| Powdered/Flakes | ||

| By Nature | Organic | |

| Conventional | ||

| By End Use | Industrial | Food and Beverages Processing |

| Personal Care and Cosmetics | ||

| Pharmaceuticals | ||

| HoReCa/Foodservice | ||

| Retail/Household | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the dried herbs market today?

The dried herbs market size is USD 5.83 billion in 2025 and is projected to reach USD 7.84 billion by 2030 at a 5.9% CAGR.

What is the current dried herbs market size and its expected value by 2031?

The dried herbs market size is USD 5.83 billion in 2025 and is projected to reach USD 8.24 billion by 2031, reflecting a 5.92% CAGR over 2026-2031.

Which product type leads global sales?

Basil leads with 24.31% of the dried herbs market share in 2025 because of its versatility across multiple cuisines.

How fast is organic dried herb demand growing?

Organic volume is forecast to advance at a 6.22% CAGR through 2031 as retailers enforce clean-label standards.

Which end-use segment is expanding the quickest?

HoReCa revenue is increasing at a 7.41% CAGR through 2031 as restaurants add herb-forward dishes and beverages.

Page last updated on: