Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

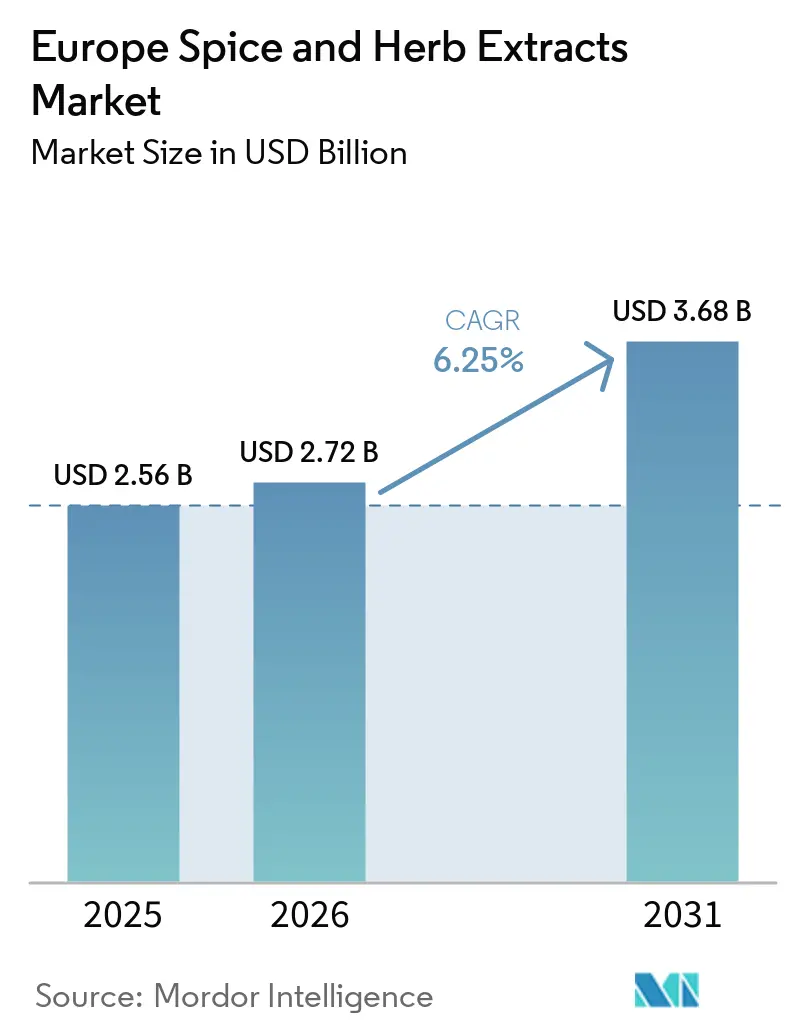

| Base Year Market Size (2025) | USD 2.56 Billion |

| Market Size (2026) | USD 2.72 Billion |

| Market Size (2031) | USD 3.68 Billion |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

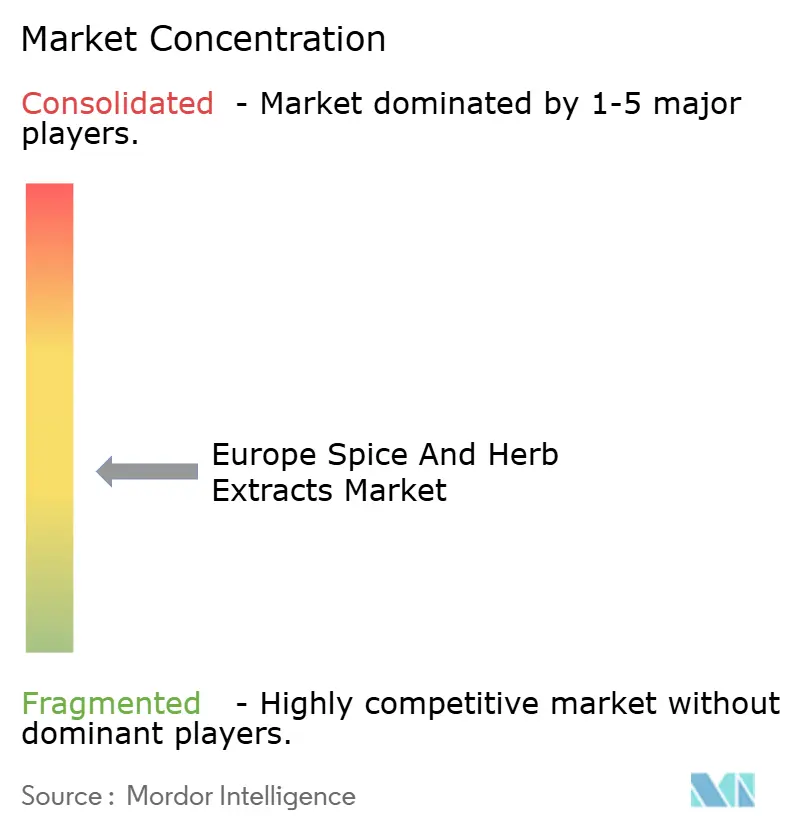

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Spice And Herb Extracts Market Analysis by Mordor Intelligence

The European spice and herb extracts market size is expected to grow from USD 2.56 billion in 2025 to USD 2.72 billion in 2026 and is forecast to reach USD 3.68 billion by 2031 at 6.25% CAGR over 2026-2031. The expansion reflects an alignment of stricter European Food Safety Authority rules that favor natural inputs, rising consumer health awareness, and adoption of extraction technologies that raise bioavailability and shelf stability. Large food processors are reformulating long-standing recipes to convert synthetic colors, flavors, and preservatives into botanical alternatives that satisfy clean-label pledges. Ingredient suppliers with traceable value chains now enjoy pricing power, because manufacturers cannot risk supply disruptions that could derail reformulation schedules. Capital spending on supercritical CO₂ and pulsed-electric-field systems continues to climb as processors target higher throughput, lower solvent use, and greener footprints, reinforcing the market’s premium positioning.

Key Report Takeaways

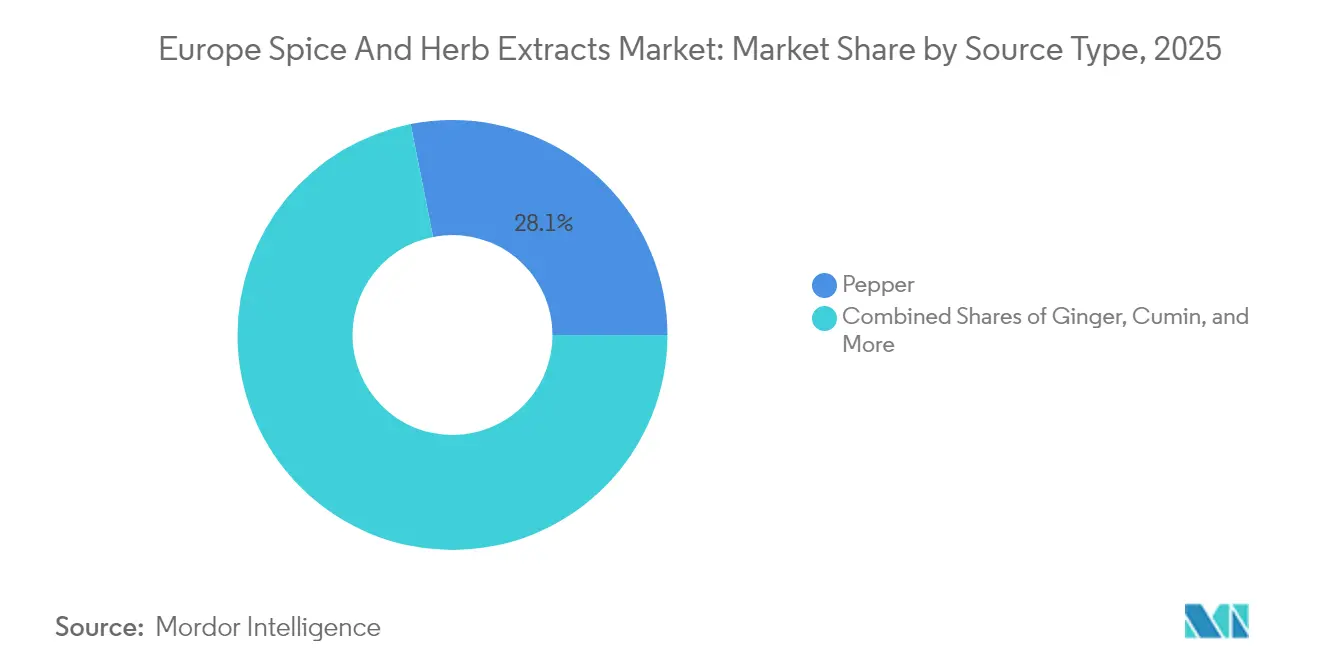

- By source type, pepper extracts held 28.12% of the European spice and herb extracts market share in 2025, whereas ginger extracts are projected to grow at a 7.18% CAGR through 2031.

- By form, liquid oleoresins accounted for 51.48% of the European spice and herb extracts market size in 2025, while micro-encapsulated extracts are set to expand at an 7.73% CAGR to 2031.

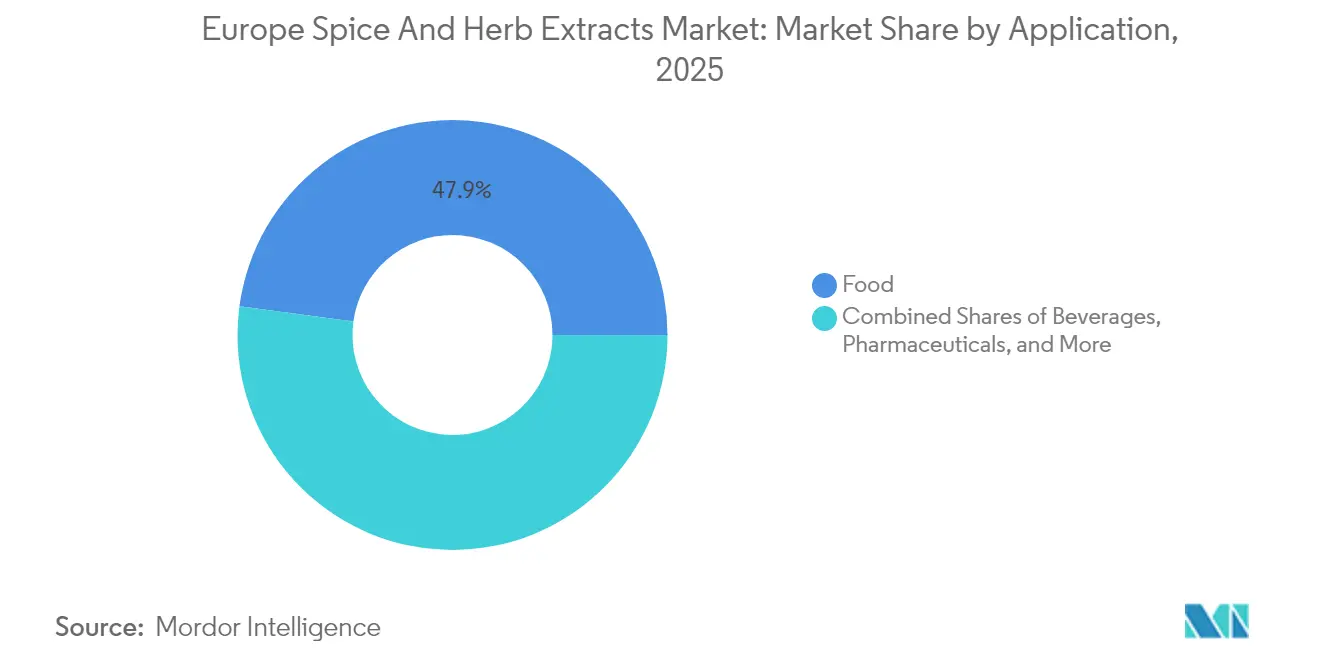

- By application, food maintained a 47.86% revenue share of the European spice and herb extracts market size in 2025; beverage is advancing at a 6.95% CAGR through 2031.

- By geography, Germany led with a 34.18% share of the European spice and herb extracts market in 2025 and is tracking a 6.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Spice And Herb Extracts Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for natural and clean-label ingredients | +1.8% | Germany, France, UK leading the market | Medium term (2-4 years) |

| Increased use of spice and herb extracts in functional and fortified foods and beverages | +1.5% | Germany, Netherlands, Spain, UK | Long term (≥ 4 years) |

| Rising popularity of ethnic/exotic cuisines | +1.2% | Germany, UK, France, owing to the popularity of multi-cuisines | Short term (≤ 2 years) |

| Rise in organic spice and herb preferences | +0.9% | Germany, France, owing to the demand for healthy food claims | Medium term (2-4 years) |

| Technological advances in extraction methods | +0.8% | Germany, Netherlands, France | Long term (≥ 4 years) |

| Expansion of exports by key supplying countries | +0.6% | Netherlands, Germany, Belgium (trade hubs) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Natural and Clean-Label Ingredients

According to recent industry surveys, 73% of European consumers are prioritizing products with fewer synthetic additives, driving significant changes in European food formulation strategies. This shift aligns with the European Food Safety Authority's updated Novel Foods guidance, which will take effect in February 2025[1]Source: European Food Safety Authority, "European Food Safety Authority, “Navigating Novel Foods: What EFSA’s Updated Guidance Means for Safety Assessments,” efsa.europa.eu. The updated guidance simplifies the approval process for botanical extracts while maintaining strict safety standards. This regulatory framework inherently benefits spice and herb extracts over synthetic alternatives, as natural ingredients are supported by established safety profiles and strong consumer acceptance. Food manufacturers are increasingly reformulating their products by replacing artificial colors, flavors, and preservatives with botanical extracts that enhance taste and offer perceived health benefits. This trend is particularly prominent in Germany and France, where clean-label claims are used in premium positioning strategies to justify higher price points. These strategies not only improve profit margins but also provide a sustainable competitive advantage for extract suppliers who can ensure traceability and consistent quality.

Increased Use of Spice and Herb Extracts in Functional and Fortified Foods and Beverages

Spice and herb extracts have evolved from mere flavor enhancers to active ingredients with proven health benefits, marking a significant shift in the functional foods landscape. As European consumers increasingly seek foods that promote specific health outcomes, manufacturers are turning to turmeric for its anti-inflammatory properties, ginger for digestive support, and oregano for its antimicrobial effects, according to the CBI data[2]Source: CBI, "What is the demand for natural ingredients for health products on the European market", cbi.eu. Leading this innovation wave, manufacturers in Germany and the Netherlands are crafting standardized extract formulations that not only meet stringent pharmaceutical-grade quality standards but are also economically viable for food applications. This melding of the nutraceutical and food sectors presents a golden opportunity for extract suppliers, especially those who can consistently deliver bioactive compound concentrations and validate health claims in line with European regulations. Meanwhile, sales of functional beverages in Europe are on track for substantial growth, with projections extending through 2030.

Rising Popularity of Ethnic/Exotic Cuisines

In 2025, European consumers, particularly Millennials and Gen Z, increasingly adopted international flavors, driven by social media and demographic changes. Fusion seasonings, such as Thai-Cajun and Middle Eastern-Mexican blends, led this culinary transformation. These younger generations, who view culinary exploration as a lifestyle expression, created a growing demand for authentic flavor profiles, requiring specialized spice and herb extracts. From 2019 to 2023, European imports of dried chilies experienced an annual growth rate of 5.5%, with Spain dominating consumption and Germany showing significant growth in exotic spice categories. In response, restaurant chains and food manufacturers incorporated these complex spice blends, utilizing concentrated extracts to maintain consistent flavors in large-scale production. This trend has expanded beyond traditional ethnic categories, with European consumers increasingly embracing heat levels and flavor combinations once considered niche. This shift has driven the need for advanced extraction techniques to preserve the volatile compounds essential for delivering authentic taste experiences.

Rise in Organic Spice and Herb Preferences

Over the last two decades, organic food retail sales in the European Union have grown significantly. Germany and France have become the leading markets for organic spices and herbs, creating opportunities for certified suppliers to command premium prices. Consumers in Northern European markets, supported by strong purchasing power, are willing to pay 20-40% more for organic spices that meet environmental and social sustainability standards. This trend highlights the segment's growth potential. European companies are increasingly adopting blockchain technology to improve supply chain transparency. For example, Verstegen's initiatives ensure traceability from farm to final product, addressing consumer concerns about authenticity and production methods. Additionally, the Sustainable Spice Initiative promotes responsible sourcing practices across the European supply chain, providing competitive advantages to extract suppliers who demonstrate environmental stewardship and fair trade compliance. However, the demand for organic certification is driving supplier consolidation, as smaller producers struggle to meet strict documentation and quality control requirements. This creates opportunities for established players to expand their market share through acquisitions and strategic partnerships.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent and evolving European food safety and allergen labeling regulations | -1.1% | EU-wide, particularly Germany, France | Medium term (2-4 years) |

| High cost of implementing advanced extraction technologies | -0.8% | Germany, Netherlands, France | Long term (≥ 4 years) |

| Intense competition from synthetic substitutes | -0.7% | Germany, UK, Poland | Short term (≤ 2 years) |

| Fluctuating prices and inconsistent supply of raw materials | -0.9% | Netherlands, Germany, Belgium (import hubs) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent and Evolving European Food Safety and Allergen Labeling Regulations

The European Food Safety Authority's continuous regulatory updates create compliance burdens that disproportionately affect smaller extract suppliers, with recent guidance on novel foods requiring comprehensive safety dossiers that can cost EUR 200,000-500,000 per application. The Heads of Food Safety Agencies working group has identified 13 substances for potential health risk assessment, including curcumin and piperine, commonly found in spice extracts, creating uncertainty about future market access for certain botanical ingredients, according to the Bundesamt für Verbraucherschutz und Lebensmittelsicherheit[3]Bundesamt für Verbraucherschutz und Lebensmittelsicherheit, “First Report of the HoA Working Group Food Supplements,” bvl.bund.de . Maximum residue level modifications, such as recent changes for propamocarb in radishes, demonstrate the dynamic nature of European food safety regulations that require continuous monitoring and adaptation by extract suppliers. Allergen labeling requirements have become increasingly complex, with cross-contamination risks requiring sophisticated segregation protocols that increase production costs and limit facility flexibility. These regulatory pressures favor established multinational companies with dedicated regulatory affairs teams while creating barriers to entry for innovative, smaller suppliers who may lack resources for comprehensive compliance programs.

High Cost of Implementing Advanced Extraction Technologies

Facilities adopting advanced extraction technologies, such as pulsed electric fields and supercritical CO2 systems, incur capital costs between EUR 1-5 million. The economic feasibility of these technologies depends on achieving a scale that justifies the significant equipment investment. Research indicates that pulsed electric fields can enhance olive oil production efficiency by 12.3% and reduce processing time by 33%. However, smaller producers often prefer renting the equipment instead of purchasing it due to the high initial costs (MDPI). The complexity of modern extraction systems necessitates specialized technical expertise, which commands high wages in European labor markets. This increases operational expenses, requiring either higher product prices or greater throughput to sustain profitability. Additionally, energy costs associated with these advanced methods have risen sharply due to fluctuations in European energy markets. Some facilities report processing cost increases of 15-25%, which cannot be fully passed on to customers. Moreover, companies investing in new extraction technologies face a 12-18 month timeline for validation and regulatory approvals. This extended process creates cash flow challenges, particularly when competing with established suppliers using conventional methods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Pepper Dominance Challenged by Ginger Innovation

In 2025, pepper extracts command a dominant 28.12% market share, thanks to their adaptability in food applications and robust supply chains anchored in major producing nations like Vietnam and India. Meanwhile, ginger extracts are on a rapid ascent, boasting a 7.18% CAGR through 2031, fueled by their rising use in functional beverages and growing consumer awareness of ginger's benefits for digestion and immunity. Cumin and coriander extracts find their niche in ethnic food formulations, while chili extracts are riding the wave of heightened heat tolerance among European consumers, evidenced by a 5.5% annual growth in dried chili imports (CBI). Cardamom and cinnamon extracts cater to premium markets, especially in confectionery and bakery segments, where their authentic flavor profiles command a premium price.

Source type segmentation unveils strategic vulnerabilities in the supply chain. Indian spice exports are grappling with a 12% volume drop in 2024, attributed to contamination challenges and surging freight costs. This scenario paves the way for alternative suppliers from Morocco, Turkey, and Egypt to step in. Oregano and basil extracts, benefiting from their Mediterranean roots, enjoy reduced transportation costs and quicker deliveries to European processing hubs. Thyme extracts, valued both as flavor enhancers and natural preservatives, resonate with the clean-label movement's preference for multifunctional ingredients. These segmentation trends hint at consolidation prospects for suppliers adept at curating diverse source portfolios while upholding stringent quality standards across various botanical categories.

By Form: Liquid Oleoresins Hold Ground While Microencapsulation Accelerates

In 2025, liquid oleoresins held a significant 51.48% share of the European spice and herb extracts market. This dominance can be attributed to their highly concentrated flavor, rapid solubility in oil-based formulations, and an extended shelf life of 18 months under ambient conditions. From a cost-per-use perspective, oleoresins are particularly advantageous in applications such as meat curing and savory sauces, where even small quantities deliver intense sensory impact, making them a preferred choice for manufacturers. Meanwhile, micro-encapsulated extracts are experiencing robust growth, with a CAGR of 7.73%. These extracts are increasingly adopted by cereal, bakery, and snack brands due to their ability to withstand high extrusion temperatures while releasing aroma effectively during consumption.

Encapsulation technology also plays a critical role in protecting carotenoids and polyphenols from oxidation, enabling manufacturers to make "source of antioxidants" claims on snack packaging without the risk of color degradation. Powder extracts continue to be a staple for dry rub applications, offering versatility and ease of use. Essential oils, on the other hand, cater to niche applications in the confectionery segment, where retaining their volatile properties is essential for delivering the desired sensory experience. The availability of diverse extract forms not only expands revenue opportunities across various processing technologies but also mitigates the risk of over-reliance on any single cost factor, ensuring greater stability within the European spice and herb extracts market.

By Application: Food Dominance Faces Beverage Sector Disruption

In 2025, food applications command a dominant 47.86% market share, spanning dairy, meat processing, snacks, and convenience foods. Here, spice and herb extracts play dual roles: enhancing flavors and offering natural preservation. Within this landscape, meat and poultry processing stands out as the largest subsegment. This segment is increasingly leaning towards clean-label trends, opting for natural curing agents, such as Kerry's Accel technology, in place of synthetic sodium nitrite. Meanwhile, beverage applications are on a rapid ascent, projected to grow at a 6.95% CAGR through 2031. This surge is fueled by innovations in functional drinks, which now harness botanical extracts for added health benefits, moving beyond mere flavoring. In specialized arenas like pharmaceuticals and personal care, the purity of extracts and the standardization of bioactive compounds command premium pricing.

Today's consumers are gravitating towards products that not only tantalize the taste buds but also offer functional benefits. For instance, in Europe, health-conscious consumers are increasingly favoring functional beverages that incorporate spice extracts, promoting mental well-being and aiding digestion. In the dairy sector, certain spice extracts' natural antimicrobial properties extend shelf life, eliminating the need for synthetic preservatives. Snack producers are harnessing encapsulation technologies to ensure a consistent flavor release during consumption. Furthermore, as food and pharmaceutical applications converge, extract suppliers see a lucrative opportunity: meeting stringent pharmaceutical-grade quality standards while adhering to the cost structures of the food industry. This application diversity not only mitigates risks for suppliers—offsetting demand fluctuations in one segment with growth in another—but also demands a deep technical expertise across varied regulatory frameworks and quality standards.

Geography Analysis

Germany commanded 34.18% of European spice and herb extracts market share in 2025 and is projected to compound at 6.98% CAGR through 2031. The country hosts over 6,000 food-and-drink manufacturers whose demand for traceable, high-purity inputs shapes supply specifications. Hamburg and Bremen ports streamline raw-material inflows, while tight oversight by the Federal Office of Consumer Protection and Food Safety accelerates approvals for natural formulations over synthetic counterparts, cementing botanical preference.

The United Kingdom, despite post-Brexit customs frictions, continues to import specialized extracts for its robust ethnic-food landscape. British retailers retail more than 50 private-label SKUs of ready-meal curries that rely on standardized chili and cumin oleoresins, sustaining volume growth even as inflation squeezes household budgets. France leverages its gastronomic heritage to position premium extracts in artisanal bakery and charcuterie, emphasizing provenance and appellation integrity that command 10-20% price premiums.

The Netherlands operates as Europe’s main import hub, processing roughly 450,000 t of raw spices for distribution across the continent. Spain and Italy contribute from a supply side, cultivating oregano, rosemary, and basil under Mediterranean climates that allow shorter farm-to-factory cycles, thereby enhancing terpene retention. Poland emerges as a growth hotspot, spurred by FDI in meat processing, while Belgium’s chocolate sector adopts encapsulated cinnamon and cardamom oils to diversify flavor lines. Overall, divergent income levels and culinary preferences create a mosaic of opportunities that nimble suppliers can capture within the European spice and herb extracts market.

Competitive Landscape

The European spice and herb extracts market exhibits moderate fragmentation, reflecting diverse customer requirements across food categories and varying extraction technologies that prevent single-company dominance. This fragmented structure creates strategic opportunities for both multinational ingredient suppliers and specialized regional players who can develop niche expertise in specific botanical sources or application technologies. Major players, including Givaudan, Kerry Group, and DSM-Firmenich, compete through vertical integration strategies that encompass raw material sourcing, extraction processing, and application development, while smaller companies focus on specialized products or regional market penetration.

Technology adoption serves as a primary competitive differentiator, with companies investing in advanced extraction methods like supercritical CO2, microencapsulation, and biotransformation to create unique product offerings that command premium pricing. Symrise's launch of the Mindera® platform demonstrates how plant-based product protection technologies can create new market categories that combine traditional spice extraction with innovative applications.

Strategic partnerships between ingredient suppliers and food manufacturers enable co-development of application-specific solutions, with companies like DSM-Firmenich investing in new production facilities like their Parma, Italy plant to enhance capabilities in concentrated powder flavors and functional blends. The competitive landscape rewards companies who can demonstrate regulatory compliance expertise, with EFSA's evolving novel food requirements creating barriers to entry that favor established players with dedicated regulatory affairs capabilities.

Europe Spice And Herb Extracts Industry Leaders

-

Olam International

-

Sensient Technologies Corporation

-

Kerry Group PLC

-

Kalsec Inc.

-

Dohler Group SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: DSM-Firmenich broke ground on a new state-of-the-art production facility in Parma, Italy, set for completion in Q1 2027, which will enhance capabilities in concentrated powder flavors, culinary blends, and functional blends while creating over 100 jobs. The facility will serve growing market demands in Europe, India, and the Middle East, utilizing advanced technologies for efficient production in the 'Parma Food Valley' location

- March 2025: French alternative asset management firm Tikehau Capital has secured a majority stake in Spain's Juan Navarro García (JNG), a company specializing in the processing and distribution of paprika and oleoresins.

- November 2023: Kalsec opened a new savory innovation centre in Netherlands. To open the centre, the company collaborated with Oost NL (the East Netherlands Development Agency), Foodvalley NL, and Wageningen University & Research. The facility offers solutions for sauces, dressings, and condiments.

Europe Spice And Herb Extracts Market Report Scope

Spice and herb extracts derive from natural or organic flavor sources in the plant. Europe's spice and herb extracts market is segmented by source type, application, and geography. Based on the source type, the market is segmented into celery, cumin, chili, coriander, cardamom, oregano, pepper, basil, ginger, thyme, cinnamon, and others. Others include vanilla, orange, lemon, citrus, and resinoids. Based on the application, the market is segmented into food, beverages, and pharmaceuticals. The food segment is further segmented into dairy, dressings, soups, and sauces; meat and poultry; snacks and convenience foods; and others. The beverage segment is further segmented into soft drinks, tea and herbal drinks, and alcoholic beverages. Based on geography, the market is segmented into the United Kingdom, France, Germany, Italy, Russia, Spain, and the rest of Europe. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Source Type

| Celery |

| Cumin |

| Chili |

| Coriander |

| Cardamom |

| Oregano |

| Pepper |

| Basil |

| Ginger |

| Thyme |

| Cinnamon |

| Other Source Types |

By Form

| Liquid Oleoresins |

| Powder Extracts |

| Essential Oils |

| Micro-encapsulated Extracts |

By Application

| Food | Dairy |

| Dressings, Soups & Sauces | |

| Meat & Poultry | |

| Snacks & Convenience Food | |

| Other Applications | |

| Beverage | Soft Drinks |

| Tea & Herbal Drinks | |

| Alcoholic Beverages | |

| Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Other Applications |

By Geography

| Spain |

| United Kingdom |

| France |

| Germany |

| Russia |

| Italy |

| Poland |

| Belgium |

| Netherlands |

| Rest of Europe |

| By Source Type | Celery | |

| Cumin | ||

| Chili | ||

| Coriander | ||

| Cardamom | ||

| Oregano | ||

| Pepper | ||

| Basil | ||

| Ginger | ||

| Thyme | ||

| Cinnamon | ||

| Other Source Types | ||

| By Form | Liquid Oleoresins | |

| Powder Extracts | ||

| Essential Oils | ||

| Micro-encapsulated Extracts | ||

| By Application | Food | Dairy |

| Dressings, Soups & Sauces | ||

| Meat & Poultry | ||

| Snacks & Convenience Food | ||

| Other Applications | ||

| Beverage | Soft Drinks | |

| Tea & Herbal Drinks | ||

| Alcoholic Beverages | ||

| Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Other Applications | ||

| By Geography | Spain | |

| United Kingdom | ||

| France | ||

| Germany | ||

| Russia | ||

| Italy | ||

| Poland | ||

| Belgium | ||

| Netherlands | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the European spice and herb extracts market?

It is valued at USD 2.72 billion in 2026.

How fast is the European spice and herb extracts market expected to grow?

The market is projected to expand at a 6.25% CAGR from 2026 to 2031.

Which country leads demand for spice and herb extracts in Europe?

Germany holds 34.18% of regional demand and continues to grow at a 6.98% CAGR.

Which botanical source is gaining the most momentum?

Ginger extracts are the fastest-growing source segment at a 7.18% CAGR.

Page last updated on: