Organic Herbal Extracts Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

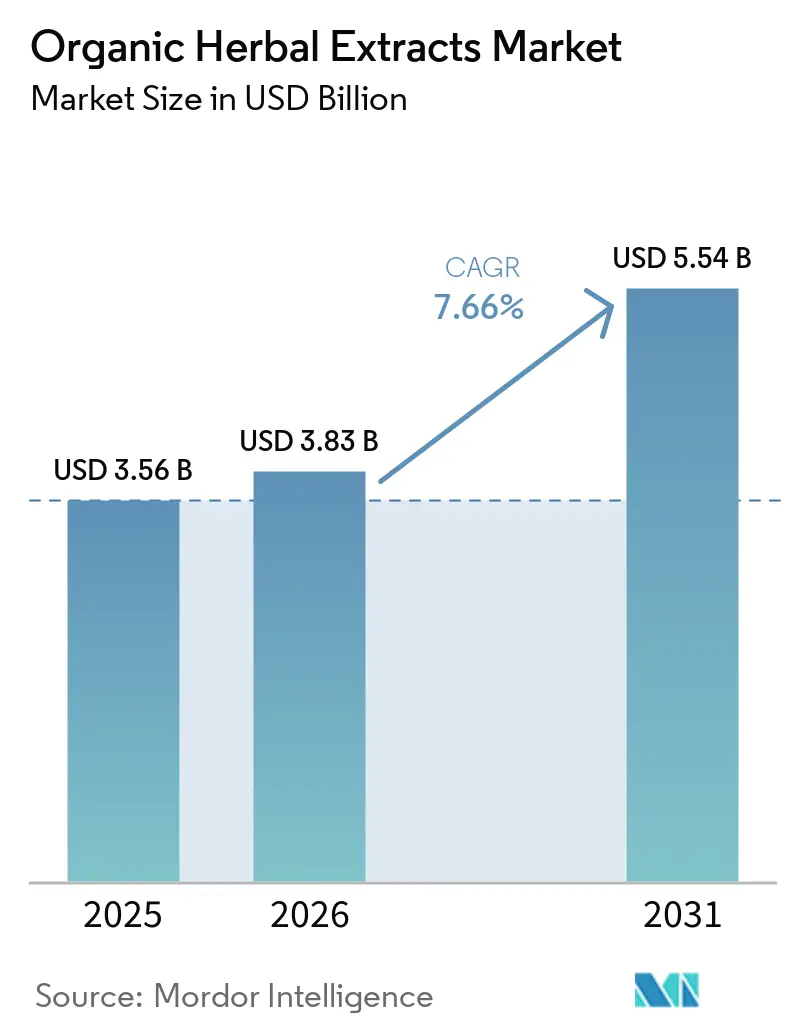

| Market Size (2026) | USD 3.83 Billion |

| Market Size (2031) | USD 5.54 Billion |

| Growth Rate (2026 - 2031) | 7.66% CAGR |

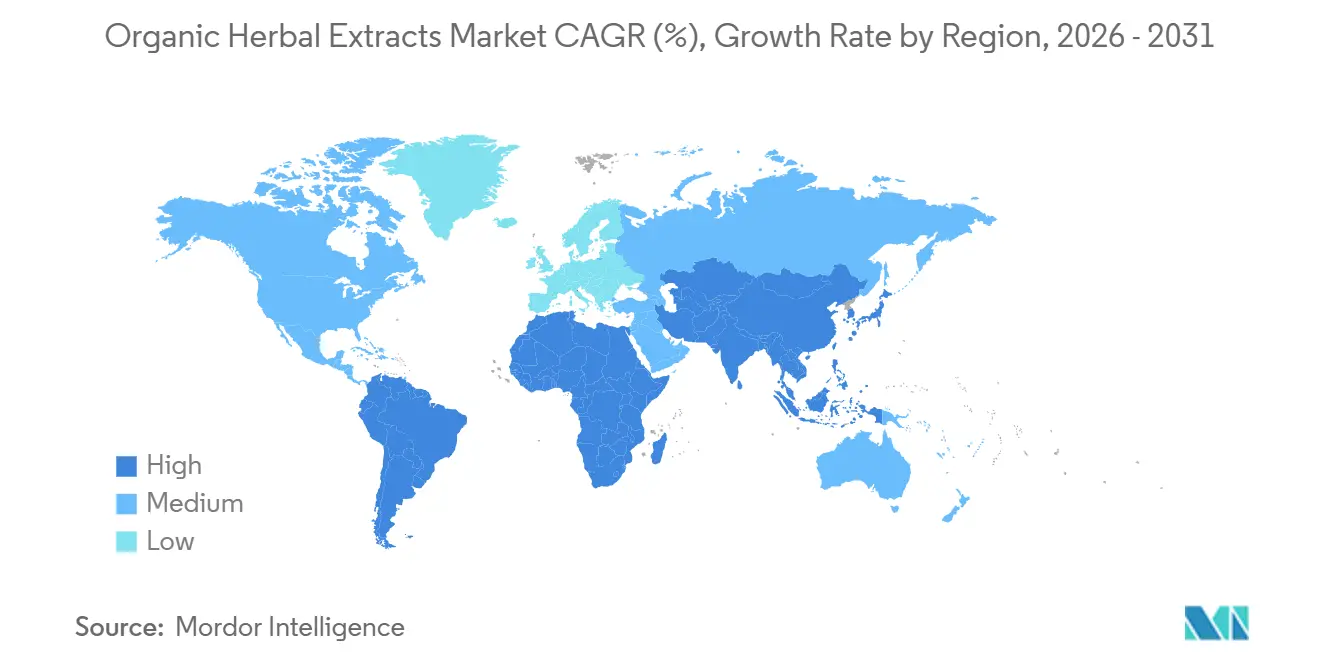

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Organic Herbal Extracts Market Analysis by Mordor Intelligence

The organic herbal extracts market size is projected to expand from USD 3.56 billion in 2025 and USD 3.83 billion in 2026 to reach USD 5.54 billion by 2031, registering a CAGR of 7.66% between 2026 and 2031. The market is segmented by product type, form, and source. Phytochemicals, as a product type, are expected to help overcome bioavailability challenges, making them a key area of interest for manufacturers aiming to improve product efficacy. In terms of form, liquid extracts are likely to drive growth in ready-to-drink (RTD) products, catering to consumers' rising demand for convenient, easy-to-consume options. When it comes to the source, flower-based extracts are expected to command premium pricing due to their perceived health benefits and greater market value. The competitive landscape is moderately consolidated, with mid-tier suppliers utilizing lower production costs to offer more affordable options. At the same time, established players with patented clinical research and dossiers continue to dominate by leveraging their innovation and ability to differentiate products, enabling them to maintain higher price points.

Key Report Takeaways

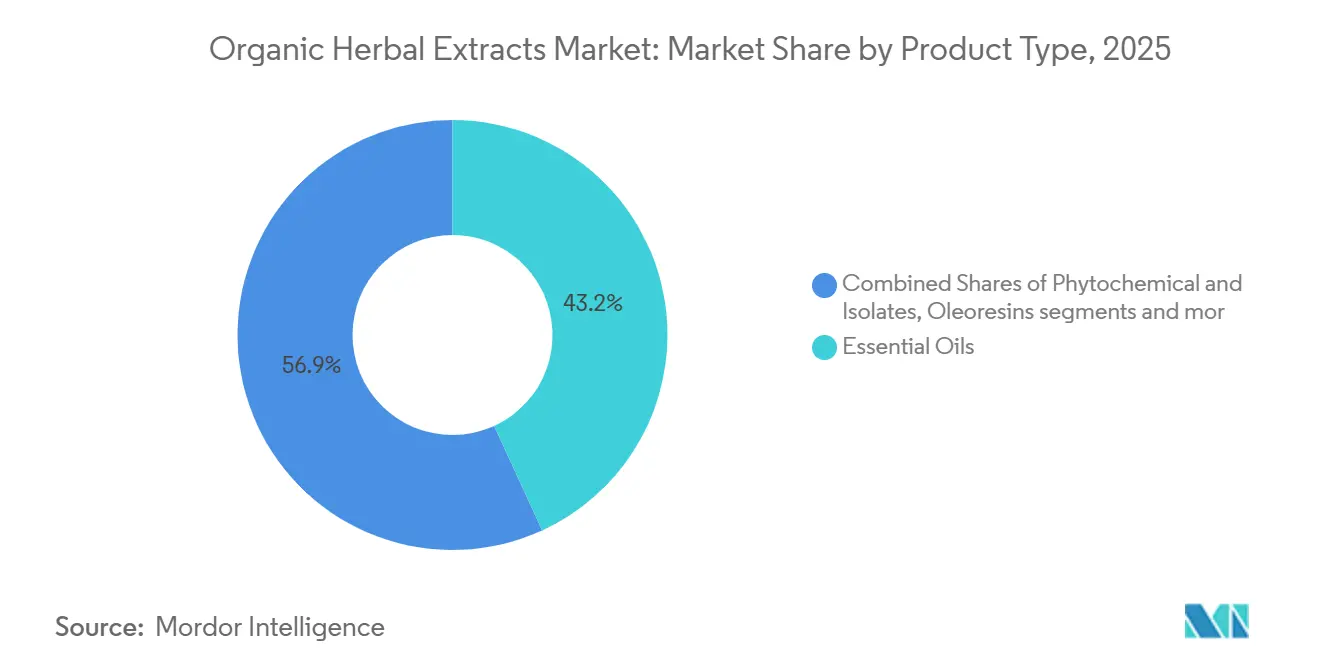

- By product type, essential oils captured 43.15% of the organic herbal extracts market share in 2025; however, phytochemicals and isolates will advance at a 8.67% CAGR through 2031.

- By form, powders accounted for 64.87% of the organic herbal extracts market size in 2025, while liquids are set to grow at a 8.02% CAGR to 2031.

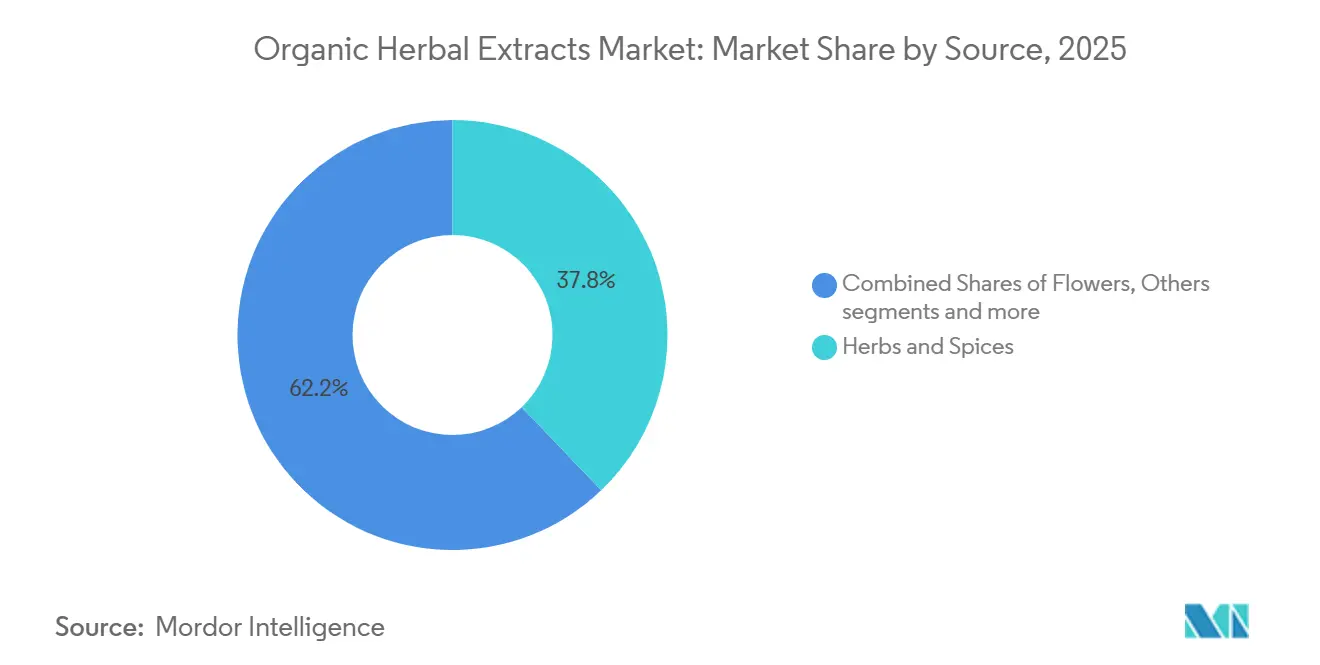

- By source, herbs and spices accounted for 37.83% of the organic herbal extracts market in 2025; flowers will advance at a 9.27% CAGR through 2031.

- By end use, pharmaceuticals commanded 51.06% of the organic herbal extracts market share in 2025; cosmetics and personal care will post the fastest growth, with a 8.14% CAGR to 2031.

- By geography, Asia-Pacific led with 36.34% share of the organic herbal extracts market in 2025, while South America records the highest projected CAGR at 8.77% for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Herbal Extracts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing consumer preference for natural, clean-label, chemical-free products | +1.8% | North America, Western Europe, Global online channels | Medium term (2-4 years) |

| Expanding use of herbal extracts as natural flavoring, coloring, preservative agents | +1.5% | North America, Europe, Asia-Pacific food hubs | Medium term (2-4 years) |

| Rising adoption in plant-based cosmetic formulations | +1.2% | North America, Europe, Urban Asia-Pacific | Short term (≤ 2 years) |

| Growing demand for functional foods and beverages | +1.4% | Global wellness segments | Medium term (2-4 years) |

| Technological advances in supercritical CO₂ extraction | +0.9% | Europe, North America, Asia-Pacific export nodes | Long term (≥ 4 years) |

| Continuous product innovation and new botanical formulations | +1.1% | R&D-intensive regions worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing consumer preference for natural, clean-label, and chemical-free products

The growing preference for natural, chemical-free, and clean-label products is driving the increased use of organic herbal extracts across various industries. As of March 2025, according to the NSF Organization, approximately 74% of global consumers value organic ingredients in personal care products, underscoring a clear shift toward safer, more transparent options[1]Source: NSF Organization, "74% of Consumers Consider Organic Ingredients Important in Personal Care Products", nsf.org. This trend has encouraged manufacturers to move away from synthetic preservatives like BHA and sodium benzoate, opting instead for plant-based alternatives such as rosemary oleoresin. These natural preservatives help maintain product shelf life while aligning with consumer preferences for clean-label formulations. Additionally, the rising interest in health and wellness has boosted the demand for functional products, leading to the inclusion of adaptogenic botanicals in food, nutraceuticals, and personal care items. These extracts not only enhance product functionality but also cater to the growing consumer focus on holistic well-being.

Rising adoption in plant-based cosmetic formulations

The demand for organic herbal extracts is growing as more cosmetic brands focus on plant-based formulations that provide effective results without harmful synthetic ingredients. Natural compounds like bakuchiol are becoming popular as safer alternatives to retinol, offering benefits such as improved collagen production without causing skin sensitivity to sunlight. Similarly, centella asiatica is widely used in high-end Korean and Japanese beauty products for its ability to repair and strengthen the skin barrier. This shift is also driven by the rising number of vegans worldwide, which is expected to reach approximately 88 million people out of a global population of over 8.3 billion by 2026[2]Source: World Animal Foundation, "How Many Vegans Are in the World in 2026? Latest Vegan Stats", worldanimalfoundation.org. The preference for cruelty-free and plant-derived ingredients is fueling this trend. Furthermore, advancements in herbal extract applications are expanding their use beyond skincare. Products such as ready-to-drink beverages and chewable supplements are gaining popularity, driving the growth of ingestible beauty and holistic wellness solutions.

Growing demand for functional foods and beverages enriched with herbal ingredients

The growing use of herbal ingredients in functional foods and beverages is driving the demand for organic herbal extracts. Consumers are increasingly looking for everyday products that offer additional health benefits. For instance, around 74% of United States adults use dietary supplements according to PubMed Central in December 2025, showing a strong preference for ingredients like turmeric, elderberry, and ashwagandha[3]Source: PubMed Central, "Insights into Dietary Supplements as Popular Product Supporting the Diet", pmc.ncbi.nlm.nih.gov. These ingredients are now being incorporated into common food and beverage products. This trend is pushing manufacturers to create products that serve dual purposes, combining nutrition and wellness. Examples include prebiotic botanical blends mixed with kombucha extracts and dietary fiber, which support digestive health. These innovations not only make it easier to develop clean-label products but also expand the use of organic herbal extracts in convenient and functional formats, catering to the growing consumer demand for health-focused options.

Technological advancements in extraction methods, such as supercritical CO₂ extraction

New extraction technologies, especially supercritical CO₂ extraction, are improving the quality and efficiency of organic herbal extracts, which is helping the market grow. This method is more effective than traditional solvent-based techniques, such as ethanol extraction. It enables higher yields and better preservation of key bioactive compounds, resulting in more potent, stable extracts. Additionally, since this process does not use solvents, it meets the growing demand for clean-label and environmentally friendly products, making it appealing to both manufacturers and consumers. While companies in Europe and the United States are leading the adoption of this technology, exporters in countries like China and India are also making significant investments. These investments aim to achieve solvent-free certifications, enhance product differentiation, and tap into higher-value market opportunities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated cost of organic raw materials and certification processes | -1.3% | North America, Europe, Certified global supply | Medium term (2-4 years) |

| Increasing competition from synthetic substitutes | -0.9% | Price-sensitive Asia-Pacific, South America | Short term (≤ 2 years) |

| Complex and fragmented regulatory frameworks | -0.7% | United States, EU, India, China | Long term (≥ 4 years) |

| Stringent quality testing and certification requirements | -0.6% | EU, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Elevated cost of organic raw materials and certification processes

The high costs of organic raw materials and the certification process are major challenges for the organic herbal extracts market. Obtaining organic certification involves a lengthy transition period of approximately three years. During this time, producers must meet strict standards, undergo audits, and comply with regulations, all of which incur significant expenses. These costs are only partially offset by subsidies, leaving manufacturers with a heavy financial burden. Consequently, organic herbal extracts are priced 20–40% higher than conventional alternatives. This price difference makes it difficult for these products to gain traction in price-sensitive markets. Additionally, the higher costs limit their appeal in mass-market product segments, where affordability is a key factor for consumers. As a result, the market faces challenges in achieving broader adoption and penetration.

Increasing competition from synthetic substitutes offering consistent quality and lower cost

The growing competition from synthetic substitutes is creating significant challenges for the organic herbal extracts market. Synthetic alternatives, such as synthetic capsaicin and vanillin, are often preferred due to their lower production costs, which are 30–50% lower than those of natural herbal extracts. This cost advantage makes them highly appealing for industries that prioritize large-scale production and cost efficiency. Additionally, synthetic ingredients offer greater consistency and stability than their natural counterparts. For example, studies have shown that synthetic compounds perform better in applications such as cosmetic emulsions, especially under accelerated-aging conditions. These factors lower costs, improve stability, and consistent quality, making synthetic substitutes a strong competitor, limiting the adoption of organic herbal extracts in certain industrial and mass-market applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Phytochemicals Narrow Bioavailability Gaps

In 2025, essential oils accounted for the largest share of the global organic herbal extracts market, contributing 43.15% to the market value. This strong position is due to their extensive use in industries like food and beverages, cosmetics, and aromatherapy. Consumers trust essential oils for their natural properties, and their versatility makes them suitable for a wide range of applications. Additionally, well-established distribution networks and consistent demand across both developed and emerging markets have further solidified their dominance.

On the other hand, phytochemicals and isolates are steadily gaining popularity at a CAGR of 8.67% through 2031, driven by their increasing use in health-oriented products. These extracts are widely used in nutraceuticals, pharmaceuticals, and fortified foods because of their standardized formulations and proven health benefits. The phytochemicals segment is projected to grow, reflecting the rising consumer preference for plant-based, scientifically validated ingredients. Innovations in extraction technologies are also playing a key role in supporting this growth, enabling manufacturers to produce high-quality herbal extracts that meet evolving consumer demands.

By Form: Liquids Accelerate RTD Penetration

In 2025, powder formats led the organic herbal extracts market, holding a significant 64.87% share. This dominance is primarily due to their longer shelf life, ease of storage, and ease of transportation. Powders are widely used in various applications, including dietary supplements, functional foods, and pharmaceuticals. They also provide greater stability and enable accurate dosage control, making them a practical and reliable choice for manufacturers and consumers. These benefits have established powder formats as the most preferred option in the market.

Liquid extracts, however, are becoming increasingly popular and are expected to grow at a CAGR of 8.02% through 2031, because they are absorbed more quickly by the body and offer higher bioavailability. These extracts are commonly used in products like herbal tinctures, beverages, and liquid supplements. Consumers favor liquid extracts for their convenience and ease of use, as they can be easily added to different formulations. The liquid segment is expected to grow, driven by rising demand for herbal solutions that are easy to consume and deliver faster results, meeting the needs of today’s health-conscious consumers.

By Source: Flowers Capture Premium Pricing

Herbs and spices accounted for the largest share of the global organic herbal extracts market, contributing 37.83% to the total market value in 2025. This dominance is largely due to their widespread use in cooking, traditional medicine, and functional food products. Consumers are drawn to these extracts because they are natural, familiar, and have been used for centuries in various cultures. Additionally, the growing trend toward natural flavoring agents and plant-based health solutions has significantly boosted demand for them. This segment plays a crucial role in driving the market's overall growth.

Floral extracts are becoming increasingly popular, with a forecast CAGR of 9.27% through 2031, especially in the cosmetics, personal care, and wellness industries. These extracts are known for their pleasant fragrances and therapeutic properties, making them a preferred choice for premium skincare and fragrance products. As more consumers prioritize natural and organic ingredients, the demand for floral extracts is expected to grow steadily. Between 2026 and 2031, this segment is forecast to grow, supported by its wide range of applications and alignment with the global shift toward botanical-based, environmentally friendly solutions.

By End Use: Cosmetics Surpass Pharmaceuticals in Growth

In 2025, the pharmaceuticals segment held the largest share of the global organic herbal extracts market, accounting for 51.06% of the total market value. This dominance is attributed to the extensive use of herbal extracts in both traditional and modern medicine, particularly for managing chronic diseases and promoting preventive healthcare. Consumers are increasingly turning to plant-based remedies due to their perceived safety and effectiveness. Additionally, ongoing clinical research and supportive regulatory frameworks are further strengthening the position of herbal extracts in the pharmaceutical sector.

The cosmetics segment is expected to grow at a CAGR of 8.14% through 2031, driven by the rising demand for natural and plant-based ingredients in personal care products. Consumers are becoming more aware of clean beauty trends and are actively seeking chemical-free formulations for skincare and haircare. Organic herbal extracts are gaining popularity due to their functional benefits, such as anti-aging and antioxidant properties, which enhance product appeal. This growing preference for natural solutions is encouraging manufacturers to incorporate herbal extracts into a wider range of cosmetic products.

Geography Analysis

Asia-Pacific led the global organic herbal extracts market in 2025, holding a 36.34% share. The region's dominance is due to its strong production capabilities, easy access to raw materials, and the widespread use of traditional medicine practices. China and India are the main suppliers, supported by growing exports and government programs that encourage the herbal industry. Additionally, countries like Japan and South Korea drive demand for premium products, while Southeast Asian nations focus on cost-efficient production to strengthen their market position.

South America is expected to be the fastest-growing region, with a CAGR of 8.77% during the forecast period. This growth is fueled by the increasing cultivation of organic herbs and rising export opportunities, especially for botanicals used in wellness and flavoring applications. Brazil and Argentina are emerging as key players in global trade, thanks to favorable farming conditions. However, challenges such as inconsistent infrastructure and quality standards remain, leading international buyers to closely monitor product quality and compliance.

North America and Europe together account for lesser share of the market, driven by strict regulatory frameworks and high consumer demand for certified organic products. These regions prioritize quality, traceability, and safety, setting global benchmarks for compliance. On the other hand, the Middle East and Africa are still developing markets, showing gradual growth due to increasing awareness of herbal products and niche botanical exports. However, the overall market in these regions is still in its early stages of development.

Competitive Landscape

The organic herbal extracts market is dominated by a few key players, including Indena S.p.A., Synthite Industries Private Limited, Sabinsa Corporation, Martin Bauer Holding GmbH & Co. KG, and Givaudan SA. These companies hold a significant market share due to their strong research and development capabilities, advanced extraction technologies, and extensive global distribution networks. Their ability to innovate, particularly in developing formulations with improved bioavailability, enables them to meet the needs of industries such as pharmaceuticals, nutraceuticals, and food and beverages.

To stay competitive, major companies are focusing on adopting advanced technologies and integrating their operations vertically. Techniques such as supercritical CO₂ extraction are becoming increasingly popular because they enhance the quality of herbal extracts. Additionally, companies are investing in traceability systems to ensure their products meet organic and fair-trade standards. Many firms are also expanding their reach by acquiring smaller companies and entering direct-to-consumer sales channels, which helps them better address changing consumer preferences and capture more value across the supply chain.

The market is also experiencing consolidation due to stricter regulations and higher quality standards. For example, the introduction of Good Extraction Practice (GEP) guidelines has increased compliance costs, making it harder for smaller companies to compete. This has led to mergers and operational integration among players. Larger companies are focusing on streamlining their processes, reducing production times, and collaborating more effectively on product development. These efforts are intensifying competition and reshaping the market dynamics.

Organic Herbal Extracts Industry Leaders

-

Indena S.p.A.

-

Synthite Industries Private Limited

-

Martin Bauer Holding GmbH & Co. KG

-

Givaudan SA (Naturex)

-

Sabinsa Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Arjuna Natural showcased its ashwagandha extract Somin-On at Vitafoods Europe 2025, highlighting cognitive support benefits for older adults with mild cognitive impairment. The extract, standardized to 2% Sominone, demonstrated significant improvements in memory and cognitive functions in clinical studies, expanding the company's neurological health portfolio.

- February 2025: Sabinsa announced its participation in Natural Products Expo West 2025, showcasing sustainably sourced ingredients including LivLonga (Curcumin C3 Complex), Sabroxy for cognitive support, and CurCousin for metabolic health. The company emphasized products with GRAS status suitable for functional foods applications

Global Organic Herbal Extracts Market Report Scope

Organic herbal extracts are concentrated bioactive compounds derived from organically grown plants, obtained through natural extraction methods without synthetic chemicals or additives. The global organic herbals extracts market is segmented by product type, form, source, end use, and geography. Based on product type, the market is classified into essential oils, standardized dry extracts, oleoresins, and phytochemicals and isolates. Based on form, the market is classified into powder and liquid. Based on the source, the market is classified into herbs and spices, flowers, fruits and vegetables, and others. Based on end use, the market is classified into pharmaceuticals, dietary supplements, food and beverages, cosmetics and personal care, and animal feed and veterinary care. Based on geography, the market is classified into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The market forecasts are provided in terms of value (USD).

| Essential Oils |

| Standardized Dry Extracts |

| Oleoresins |

| Phytochemicals and Isolates |

| Powder |

| Liquid |

| Herbs and Spices |

| Flowers |

| Fruits and Vegetables |

| Others |

| Pharmaceuticals |

| Dietary Supplements |

| Food and Beverages |

| Cosmetics and Personal Care |

| Animal Feed and Veterinary Care |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Essential Oils | |

| Standardized Dry Extracts | ||

| Oleoresins | ||

| Phytochemicals and Isolates | ||

| By Form | Powder | |

| Liquid | ||

| By Source | Herbs and Spices | |

| Flowers | ||

| Fruits and Vegetables | ||

| Others | ||

| By End Use | Pharmaceuticals | |

| Dietary Supplements | ||

| Food and Beverages | ||

| Cosmetics and Personal Care | ||

| Animal Feed and Veterinary Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the organic herbal extracts market be by 2031?

The organic herbal extracts market size is forecast to reach USD 5.54 billion by 2031, growing at a 7.66% CAGR from 2026 to 2031

Which segment will grow the fastest within organic herbal extracts?

Cosmetics and personal care will post the highest 8.14% CAGR through 2031, driven by bakuchiol and centella asiatica adoption

What proportion of the market do essential oils hold?

Essential oils accounted for 43.15% of organic herbal extracts market share in 2025

Which region dominates supply and demand?

Asia-Pacific led with 36.34% share in 2025, thanks to India’s AYUSH exports and China’s high-volume manufacturing base

Page last updated on: