Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

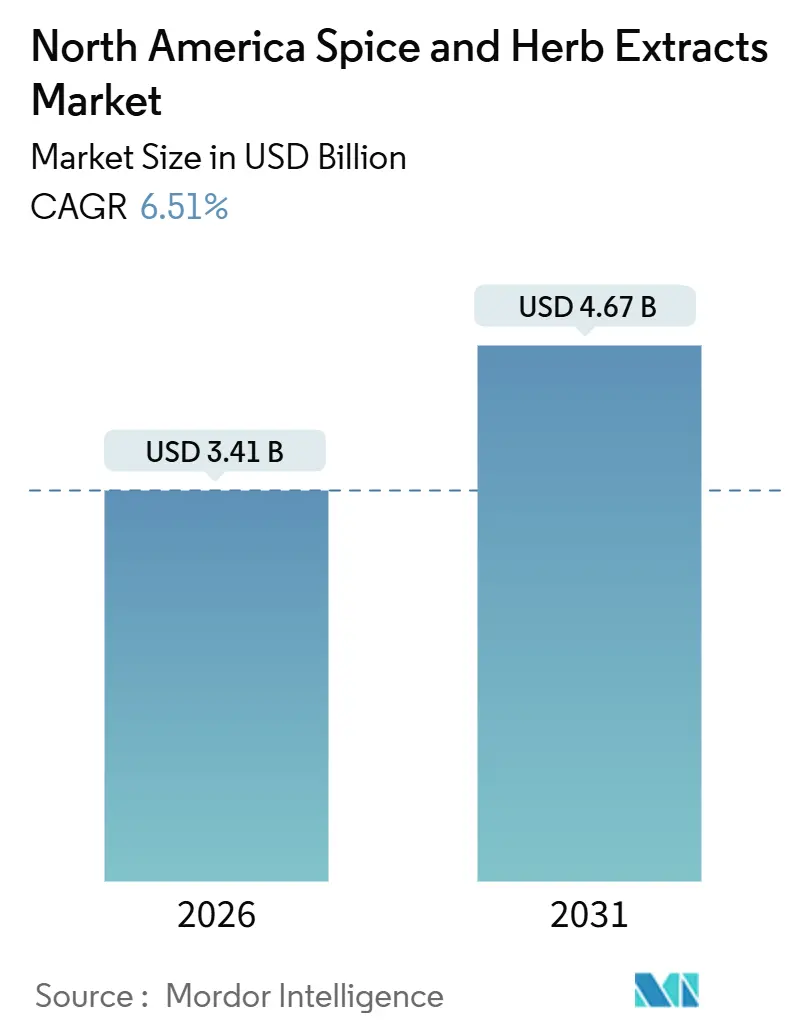

| Market Size (2026) | USD 3.41 Billion |

| Market Size (2031) | USD 4.67 Billion |

| Growth Rate (2026 - 2031) | 6.51% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Spice And Herb Extracts Market Analysis by Mordor Intelligence

The North America spice and herb extracts market size stood at USD 3.41 billion in 2026 and is projected to reach USD 4.67 billion by 2031, advancing at a 6.51% CAGR during the forecast period. Ingredient transparency, clean-label mandates, and technology upgrades are reshaping procurement strategies as processors embed oleoresins, essential oils, and powder extracts into foods, beverages, supplements, and personal-care items. United States demand dominates, but Canada’s regulatory streamlining under the Natural Health Products Regulations is accelerating commercialization cycles, while Mexico’s emerging organic-processing base is attracting foreign direct investment. Retailers such as Whole Foods and Walmart now require front-of-pack disclosure of botanical origins, raising the strategic value of traceable extracts. At the same time, supercritical CO₂ and microencapsulation systems are lowering residual-solvent risks and extending shelf life, helping processors justify premium pricing and secure multiyear supply contracts.

Key Report Takeaways

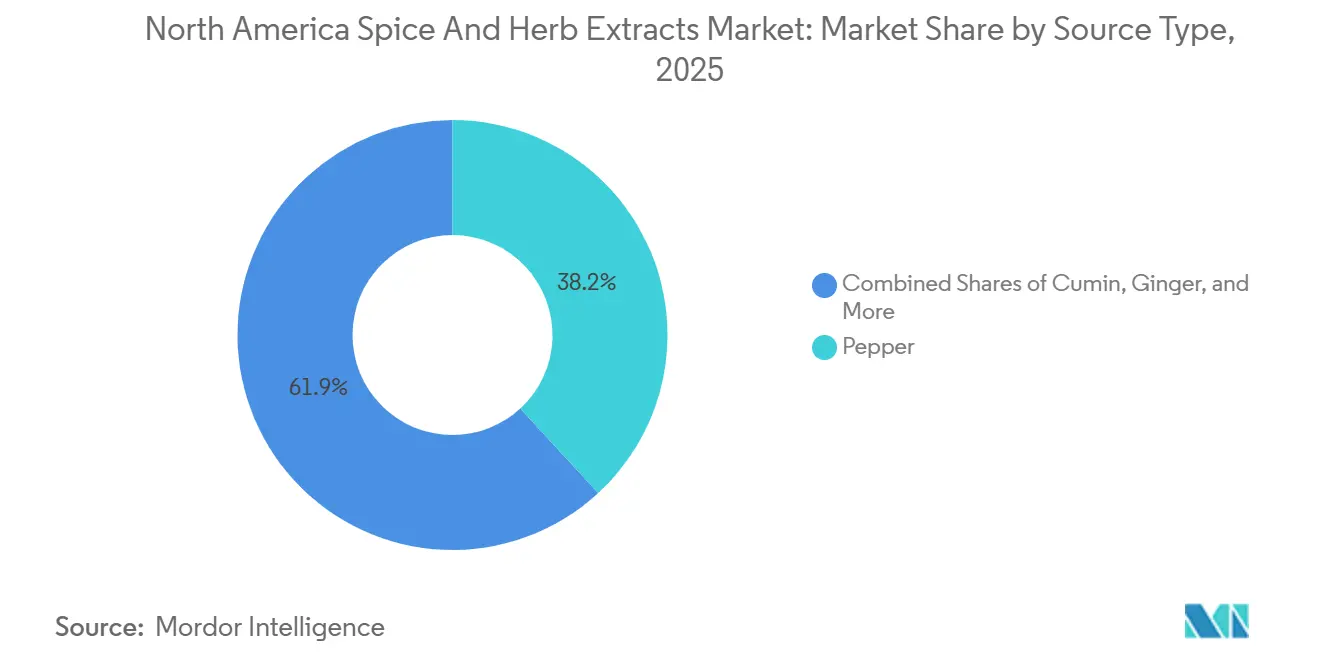

- By source type, pepper captured 38.15% of the North America spice and herb extracts market share in 2025, while ginger is expected to grow at a 7.82% CAGR through 2031.

- By form, liquid oleoresins held 42.51% revenue share in 2025; powder extracts are forecast to expand at an 8.25% CAGR to 2031.

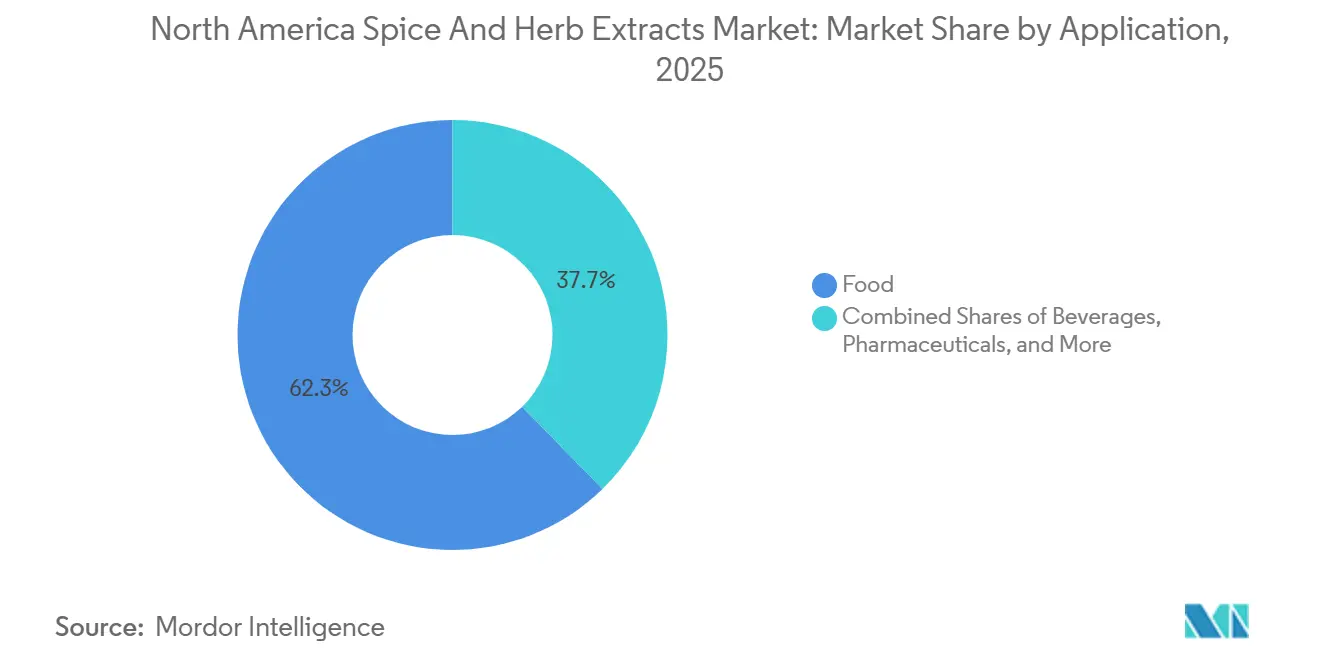

- By application, food accounted for 62.28% of the North America spice and herb extracts market size in 2025, whereas personal care and cosmetics are advancing at a 9.12% CAGR through 2031.

- By geography, the United States commanded 71.22% revenue share in 2025; Canada is projected to post a 9.28% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Spice And Herb Extracts Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing demand for natural and clean-label ingredients | +1.8% | United States, Canada, with spillover to Mexico | Medium term (2-4 years) |

| Rising adoption of spice and herb extracts in functional and fortified food and beverages | +1.5% | United States, Canada | Medium term (2-4 years) |

| Growing appeal of ethnic and exotic cuisines | +1.2% | United States urban centers, Canada metropolitan areas | Short term (≤ 2 years) |

| Preference for organic spices and herbs on the rise | +0.9% | United States, Canada | Long term (≥ 4 years) |

| Advancements in extraction technologies | +0.7% | United States, Canada | Long term (≥ 4 years) |

| Export expansion by major supplying countries | +0.4% | North America, with focus on US import channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand for Natural and Clean-Label Ingredients

Processors are replacing synthetic flavor compounds with spice oleoresins to satisfy transparency mandates from retailers such as Whole Foods and Kroger, which now require suppliers to disclose all flavoring agents on front-of-pack labels. Ingredion's 2025 clean-label survey found that 68% of North American consumers actively avoid products listing "natural flavors" without botanical specificity, pushing formulators toward ingredients like paprika oleoresin and black pepper extract that carry recognizable names. This shift is compressing reformulation cycles, with Kalsec reporting a 22% increase in customer requests for Foreign Exchange Management Act GRAS-certified hop and spice extracts during 2025. The Food and Drug Administration's updated guidance on "natural" claims in January 2025 further tightened definitions, requiring extraction methods that avoid synthetic solvents-a standard that supercritical CO2 and ethanol-based processes inherently meet.[1]Source: U.S. FDA, “Use of the Term ‘Natural’ on Food Labeling,” fda.gov.

Rising Adoption of Spice and Herb Extracts in Functional and Fortified Food and Beverages

Functional-beverage brands are embedding ginger and turmeric extracts into ready-to-drink formats targeting inflammation reduction and immune support, capitalizing on clinical evidence linking curcumin and gingerol to biomarker improvements. A 2024 study in Nutrients demonstrated that 500 milligrams of standardized ginger extract reduced C-reactive protein levels by 14% over 8 weeks, providing formulators with dosage benchmarks for label claims. Doehler's 2025 product catalog introduced microencapsulated cinnamon extract designed for protein shakes, delivering sustained release that masks bitterness while contributing antioxidant capacity. Regulatory frameworks are adapting, with Health Canada granting Natural Health Product Numbers to 17 spice-extract formulations in 2025, up from 9 in 2024, signaling faster pathways for structure-function claims[2]Source: Health Canada, “Natural Health Products Regulations,” canada.ca.

Growing Appeal of Ethnic and Exotic Cuisines

North American restaurants are sourcing cumin, cardamom, and coriander extracts to replicate regional flavor profiles from South Asia, the Middle East, and Latin America, driven by demographic shifts and culinary tourism. The National Restaurant Association's 2025 trends report identified "global fusion" as the second-fastest-growing menu category, with 43% of operators adding dishes featuring harissa, gochugaru, or za'atar spice blends[3]Source: National Restaurant Association, “State of the Restaurant Industry 2025,” restaurant.org. ADM's flavor division launched a line of liquid spice extracts in 2025 tailored for ghost kitchens, offering concentrated cardamom and fenugreek solutions that reduce prep time while maintaining authenticity. Retail channels are mirroring this trend, with Whole Foods reporting a 31% year-over-year increase in sales of products featuring "exotic spice" descriptors during 2025.

Advancements in Extraction Technologies

Supercritical CO2 extraction is displacing solvent-based methods for high-value botanicals, delivering higher purity and eliminating residual hexane concerns that trigger non-compliance with organic certifications. A 2025 patent filed by Synthite Industries detailed a two-stage CO2 process that extracts both volatile oils and non-volatile oleoresins from black pepper in a single run, reducing energy consumption by 28% compared to sequential steam distillation and solvent extraction. Microencapsulation via spray-drying is enabling powder formats that withstand high-temperature processing in extruded snacks, with Kerry Group's 2025 investor presentation highlighting a proprietary maltodextrin matrix that protects curcumin from oxidation during baking. These innovations are lowering the total cost of ownership for mid-sized processors, as modular CO2 systems priced below USD 500,000 enter the market, democratizing access to premium extraction capabilities.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent and evolving European food safety and allergen labeling regulations | -0.6% | United States and Canada exporters to EU | Short term (≤ 2 years) |

| High cost of implementing advanced extraction technologies | -0.5% | Small and mid-sized processors in United States, Canada, Mexico | Medium term (2-4 years) |

| Intense competition from synthetic substitutes | -0.8% | United States, Canada | Short term (≤ 2 years) |

| Fluctuating prices and inconsistent supply of raw materials | -1.1% | North America, with acute impact on US and Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fluctuating Prices and Inconsistent Supply of Raw Materials

Black pepper prices climbed 18% in 2024 following drought conditions in Vietnam's Central Highlands, which account for 34% of global exports, forcing North American processors to activate contingency contracts with Brazilian and Indonesian suppliers at premium rates. Ginger supply tightened in early 2025 when China-responsible for 28% of global production-imposed temporary export quotas to stabilize domestic food inflation, creating a 6-week lead-time gap for oleoresin manufacturers. Cardamom prices remain volatile, oscillating between USD 25 and USD 38 per kilogram during 2025 due to erratic monsoons in Guatemala and India, the two dominant origins, according to the Financial Times. Processors are responding by diversifying sourcing footprints and investing in vertical integration, with McCormick's 2025 annual report disclosing the acquisition of a 500-acre organic turmeric farm in southern India to secure supply for its North American oleoresin operations.

Intense Competition from Synthetic Substitutes

Synthetic vanillin, capsaicin analogs, and nature-identical piperine continue to undercut natural extracts on price, with cost differentials ranging from 40% to 70% depending on the compound and purity grade. A 2025 cost analysis by IFF revealed that synthetic capsaicin for hot-sauce formulations costs USD 18 per kilogram versus USD 62 per kilogram for chili oleoresin standardized to 5% capsaicinoids, creating margin pressure for brands that lack premium positioning. However, regulatory tailwinds are narrowing this gap, as the European Union's Farm to Fork strategy and California's Proposition 65 updates in 2024 imposed stricter disclosure requirements for synthetic additives, prompting reformulation toward natural alternatives. Symrise's 2025 sustainability report noted a 19% increase in customer conversions from synthetic to natural spice extracts, driven by retailer mandates and consumer backlash against "chemical-sounding" ingredients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Pepper Dominates, Ginger Accelerates on Wellness Demand

In 2025, pepper dominated 38.15% of North America's spice and herb extracts market, primarily due to its significant applications in savory foods and nutraceutical blends. A key factor driving its demand is piperine, which enhances curcumin absorption by an impressive 2,000%, making it indispensable in health-focused formulations. Ginger, projected to grow at a robust CAGR of 7.82%, is gaining traction across multiple industries, including functional beverages, anti-nausea pharmaceuticals, and anti-inflammatory cosmetic products. Cumin is increasingly favored in plant-based meat alternatives, effectively masking the off-notes associated with pea protein. Additionally, chili oleoresins remain a cornerstone of the hot sauce segment, as evidenced by Huy Fong Foods' substantial 200 metric-ton supply agreement in 2025, highlighting their critical role in this category.

Herbs such as coriander, cardamom, oregano, basil, and thyme are establishing themselves in high-margin niches, particularly in premium spirits and preservative-free cosmetic products. The cinnamon market is undergoing a notable segmentation into Ceylon and Cassia variants. Ceylon cinnamon, with its lower coumarin content that complies with European Union safety regulations, commands a premium of 35%, reflecting its growing preference among health-conscious consumers. Meanwhile, celery extract remains a vital ingredient in "no nitrate added" meat curing processes, ensuring natural color and flavor while meeting United States Department of Agriculture Food Safety and Inspection Service (FSIS) tolerance requirements, thereby catering to the demand for clean-label meat products.

By Form: Liquid Oleoresins Lead, Powder Extracts Surge on Convenience

In 2025, liquid oleoresins accounted for a 42.51% revenue share, primarily due to their ability to provide precise dosing in applications such as sauces and marinades. On the other hand, powder extracts are anticipated to grow at a robust CAGR of 8.25%, driven by advancements in spray-drying and fluid-bed encapsulation technologies. These processes produce free-flowing, shelf-stable ingredients that are particularly well-suited for use in instant soups and seasoning blends. Essential oils occupy a high-value niche in the market, commanding prices two to three times higher than oleoresins. This premium pricing is attributed to their therapeutic-grade purity and compliance with ISO 4730 specifications, which ensure consistent quality and performance.

Microencapsulated formats represent the fastest-growing subsegment within the market. For instance, Kalsec has developed a dual-layer microencapsulation system that significantly enhances turmeric's bioavailability by 40% by ensuring its release in the intestine. This innovation creates new opportunities for targeted nutritional supplements. However, liquid oleoresins face logistical challenges related to cold-chain requirements, as oxidation rates for ingredients like ginger increase significantly when stored above 25 °C. In contrast, powder formats eliminate the need for chilled logistics, offering a cost-effective solution by reducing freight expenses and ensuring product stability during transportation.

By Application: Food Anchors Revenue, Personal Care Outpaces Growth

In 2025, food applications dominated the North American market for spice and herb extracts, claiming a substantial 62.28% share. This segment encompassed a diverse range, including dairy products, dressings, meats, and snacks. Meanwhile, the personal-care sector is set to witness robust growth, with projections indicating a 9.12% CAGR. This surge is largely attributed to the rising preference for oregano, rosemary, and thyme extracts, which are increasingly replacing synthetic preservatives. This shift not only aligns with market trends but also circumvents the prohibitions outlined in the EU's Annex II. In the pharmaceutical realm, ginger and turmeric, both of pharmacy-grade quality, are securing over-the-counter listings. Their prominence is particularly noted in products targeting digestive health and anti-inflammatory benefits, bolstered by three new Food and Drug Administration GRAS (Generally Recognized As Safe) notices in 2025.

In the food sector, dairy manufacturers are expanding flavor innovation. For instance, Danone's cardamom-infused Greek yogurt, which sold out in just four weeks across Canada, exemplifies the trend. Manufacturers are blending black pepper and cinnamon extracts into yogurts and cheeses to appeal to adventurous palates. On the meat front, processors are turning to rosemary and oregano oleoresins not only for flavor but also as a natural means to combat Listeria and Salmonella. This approach enhances safety and extends shelf life while reducing reliance on synthetic lactates. Snack brands are adopting microencapsulated chili to deliver a gradual heat sensation. Meanwhile, in the beverage sector, alcohol producers are collaborating with extract suppliers to develop signature botanicals for gin and vermouth.

Geography Analysis

The United States held 71.22% of 2025 revenue, anchored by the world's largest processed-food sector and stringent clean-label mandates from retailers such as Target and Walmart, which now require suppliers to disclose extraction methods and botanical origins. Food and Drug Administration regulations under 21 CFR 182 and 184 classify most spice oleoresins as Generally Recognized as Safe, streamlining their incorporation into food formulations without pre-market approval, a regulatory efficiency that European processors lack. McCormick's Baltimore facility, which processes 40% of the company's North American spice extracts, completed a USD 75 million supercritical CO2 expansion in late 2024, increasing oleoresin capacity by 18,000 metric tons annually. California's Proposition 65 updates in 2024 added 6 synthetic flavor compounds to the state's carcinogen list, accelerating reformulation toward natural spice extracts among West Coast food manufacturers.

Canada is forecast to grow at 9.28% through 2031, driven by Health Canada's streamlined Natural Health Products Regulations, which reduced approval timelines from 18 months to 9 months for standardized botanical extracts in 2025. Organic certification under the Canada Organic Regime expanded by 14% in 2025, with 23 new spice-extract processors achieving certification, signaling robust demand for premium, traceable ingredients, according to the Canadian Food Inspection Agency. Quebec-based processors are capitalizing on proximity to the United States Northeast market, offering 48-hour delivery for liquid oleoresins to craft-beverage producers in Vermont and New York.

Mexico's spice-processing sector remains underdeveloped relative to its agricultural output, yet United States Department of Agriculture organic equivalency agreements ratified in 2024 are attracting foreign investment, with Givaudan announcing a USD 30 million extraction facility in Jalisco scheduled to commence operations in 2027, according to Givaudan. Rest of North America, encompassing Central America and the Caribbean, contributes marginally but serves as a critical sourcing origin for vanilla and allspice, with Belize and Jamaica exporting semi-processed oleoresins to US toll manufacturers.

Competitive Landscape

The North America spice and herb extracts market exhibits fragmented competition, as no single player commands more than 12% share and regional toll processors coexist with vertically integrated multinationals. Strategies bifurcate into cost leadership, pursued by high-volume oleoresin suppliers leveraging economies of scale in solvent extraction, and differentiation, exemplified by Kalsec's proprietary hop-extract platform that delivers natural antimicrobial and antioxidant functionality without off-flavors.

White-space opportunities are emerging in microencapsulated formats for controlled-release supplements and heat-sensitive applications, where incumbents lack the spray-drying infrastructure that specialized encapsulation firms like Southwest Research Institute have commercialized. Technology is the primary battleground, with patent filings for supercritical CO2 processes increasing 27% year-over-year in 2025, as firms race to secure intellectual property around energy-efficient extraction and novel botanical combinations.

Emerging disruptors include vertically integrated spice growers in Mexico and Central America that are bypassing traditional brokers to supply extract manufacturers directly, compressing supply chains and capturing margin previously lost to intermediaries. Symrise's 2025 acquisition of a Guatemalan cardamom estate exemplifies this backward-integration trend, securing 600 metric tons of annual raw-material supply while achieving Rainforest Alliance certification that appeals to sustainability-focused customers. ISO 22000 food-safety certification and FSSC 22000 compliance are becoming table stakes, with 18 North American extract processors achieving dual certification in 2025, up from 11 in 2024, as buyers mandate third-party audits to mitigate contamination risks. Smaller players are leveraging toll-manufacturing arrangements to access advanced extraction equipment without capital outlays, a model that Universal Oleoresins expanded in 2025 by opening its Texas facility to contract clients.

North America Spice And Herb Extracts Industry Leaders

Kerry Group plc

Dohler Gmbh

Olam International

DSM-Firmenich

McCormick and Company, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Olam Food Ingredients (OFI) has unveiled Spice Maps, its first comprehensive sustainability framework for spices, targeting pepper, chile, turmeric, onion, cassia, and coconut across key regions like India, Vietnam, Egypt, and the US.

- September 2025: Algalif has introduced Astalíf 15, the world's first 15% natural astaxanthin oleoresin from Haematococcus pluvialis microalgae, produced via supercritical CO2 extraction. This high-potency, solvent-free ingredient enables smaller capsules and efficient formulations for nutraceuticals, foods, beverages, and skincare

- March 2025: Arjuna Natural's Shoden ashwagandha extract has secured Natural Health Product (NHP) status from Health Canada, affirming its safety and efficacy as a calming, antioxidant supplement for stress reduction, sleep enhancement, and anxiety relief.

North America Spice And Herb Extracts Market Report Scope

The North America spice and herb extracts market is segmented by product type and application. Based on product type, the market is segmented into cinnamon, cumin, chili, coriander, cardamom, oregano, pepper, ginger, and other product types. On the basis of application, the market is segmented into food applications, beverage applications, pharmaceuticals. Based on geography, the report provides an analysis of the regional market.

By Source Type

| Celery |

| Cumin |

| Chili |

| Coriander |

| Cardamom |

| Oregano |

| Pepper |

| Basil |

| Ginger |

| Thyme |

| Cinnamon |

| Other Source Types |

By Form

| Liquid Oleoresins |

| Powder Extracts |

| Essential Oils |

| Micro-encapsulated Extracts |

By Application

| Food | Dairy |

| Dressings, Soups and Sauces | |

| Meat and Poultry | |

| Snacks and Convenience Food | |

| Other Applications | |

| Beverage | Soft Drinks |

| Tea & Herbal Drinks | |

| Alcoholic Beverages | |

| Pharmaceuticals | |

| Personal Care and Cosmetics | |

| Other Applications |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Source Type | Celery | |

| Cumin | ||

| Chili | ||

| Coriander | ||

| Cardamom | ||

| Oregano | ||

| Pepper | ||

| Basil | ||

| Ginger | ||

| Thyme | ||

| Cinnamon | ||

| Other Source Types | ||

| By Form | Liquid Oleoresins | |

| Powder Extracts | ||

| Essential Oils | ||

| Micro-encapsulated Extracts | ||

| By Application | Food | Dairy |

| Dressings, Soups and Sauces | ||

| Meat and Poultry | ||

| Snacks and Convenience Food | ||

| Other Applications | ||

| Beverage | Soft Drinks | |

| Tea & Herbal Drinks | ||

| Alcoholic Beverages | ||

| Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Other Applications | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

How large is the North America spice and herb extracts market in 2026?

The market generated USD 3.41 billion in 2026 and is forecast to reach USD 4.67 billion by 2031.

Which source type leads regional sales?

Pepper extracts led with 38.15% revenue share in 2025.

Which application is expanding fastest?

Personal-care and cosmetics uses are advancing at a 9.12% CAGR through 2031.

How fragmented is supplier competition?

No company holds more than 12% share, resulting in a concentration score of 3 out of 10.

Page last updated on: