Dredging Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.80 Billion |

| Market Size (2030) | USD 7.57 Billion |

| Growth Rate (2025 - 2030) | 5.48% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dredging Equipment Market Analysis by Mordor Intelligence

The dredging equipment market size is valued at USD 5.8 billion in 2025 and is projected to reach USD 7.57 billion by 2030, expanding at a 5.48% CAGR during the forecast period. Rising infrastructure modernization programs, accelerated climate-adaptation works, and the global energy transition keep demand robust even during economic volatility. Ports continue deepening channels for post-Panamax vessels, federal waterways receive record civil-works allocations, and offshore wind developers contract precision seabed services. Equipment owners benefit from multi-year government funding visibility, which reduces revenue cyclicality. Meanwhile, environmental regulation tightens, prompting hybrid-propulsion upgrades and growth in beneficial-use processing systems. Competitive intensity remains moderate because capital barriers deter rapid new entries, yet established contractors still race to acquire autonomous navigation and AI-enabled productivity tools.

Key Report Takeaways

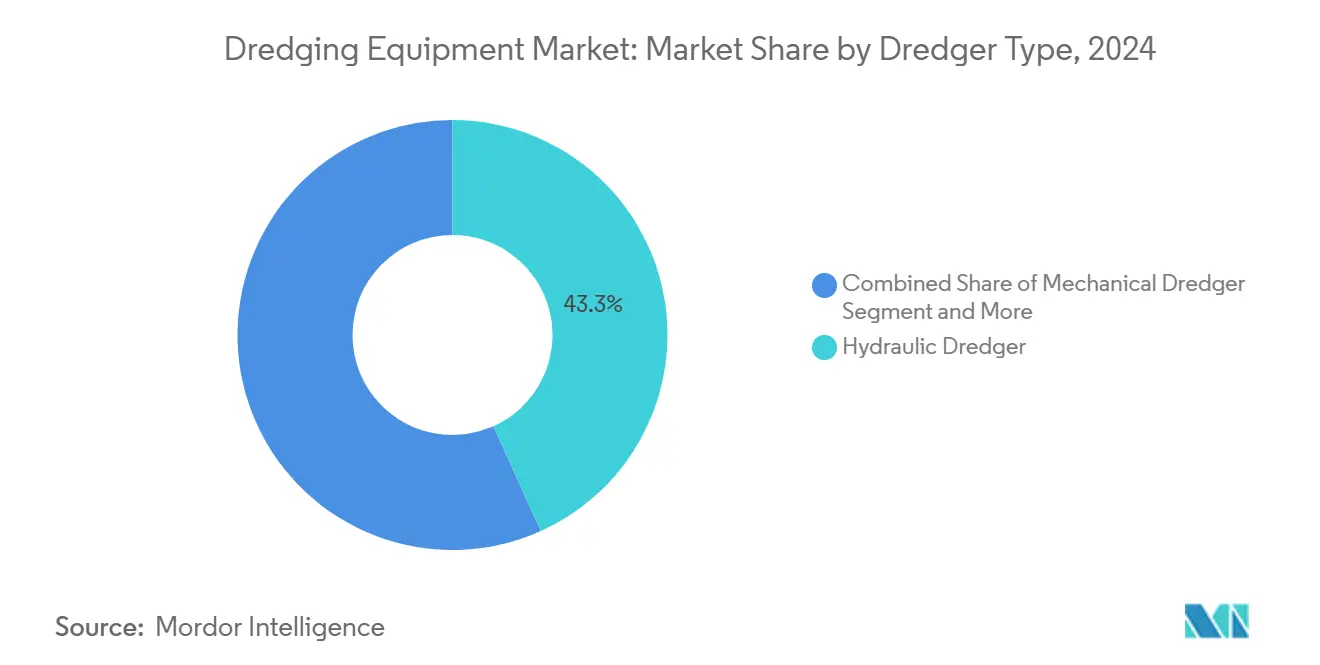

- By dredger type, hydraulic units led with 43.32% of the dredging equipment market share in 2024, while mechanical dredgers recorded the fastest 7.28% CAGR through 2030.

- By application, navigational-channel maintenance accounted for 29.92% of the dredging equipment market size in 2024; offshore renewable-energy construction posts the highest 9.26% CAGR to 2030.

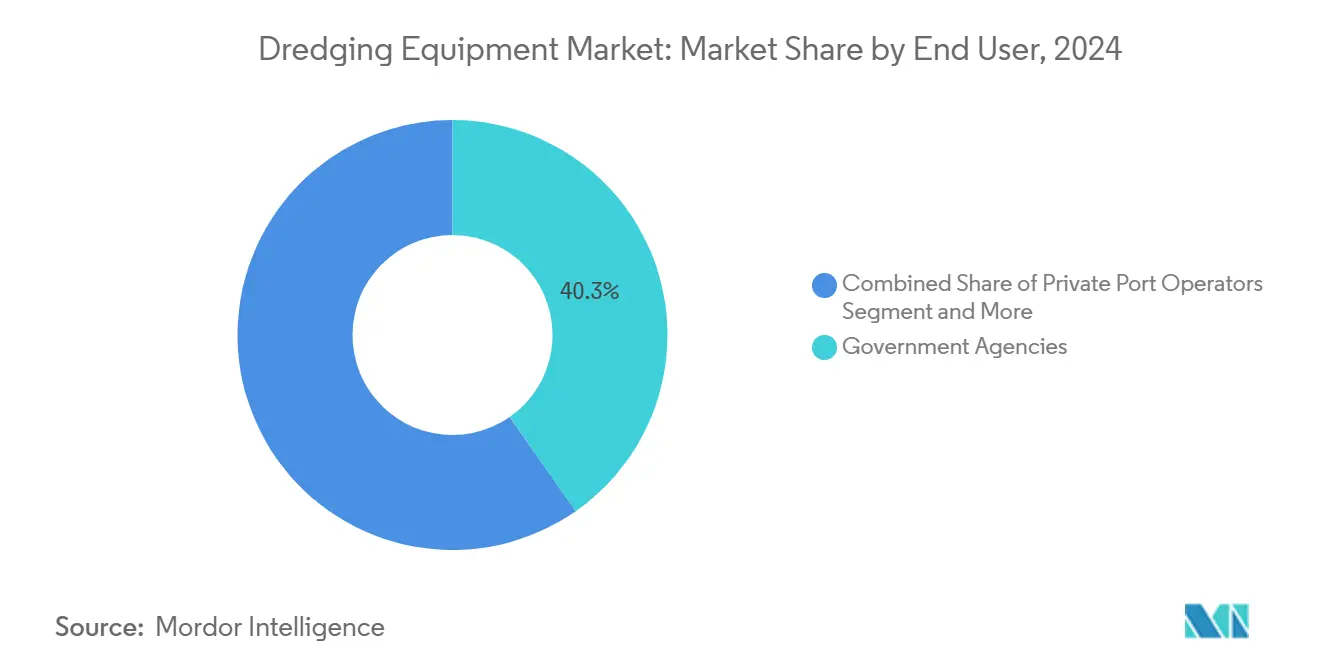

- By end user, government agencies held 40.28% of the dredging equipment market size in 2024, whereas private port operators expanded at a 7.96% CAGR through 2030.

- By ownership model, contractor-owned fleets represented 43.82% of the dredging equipment market share in 2024; project-owned arrangements are rising fastest at an 8.92% CAGR through 2030.

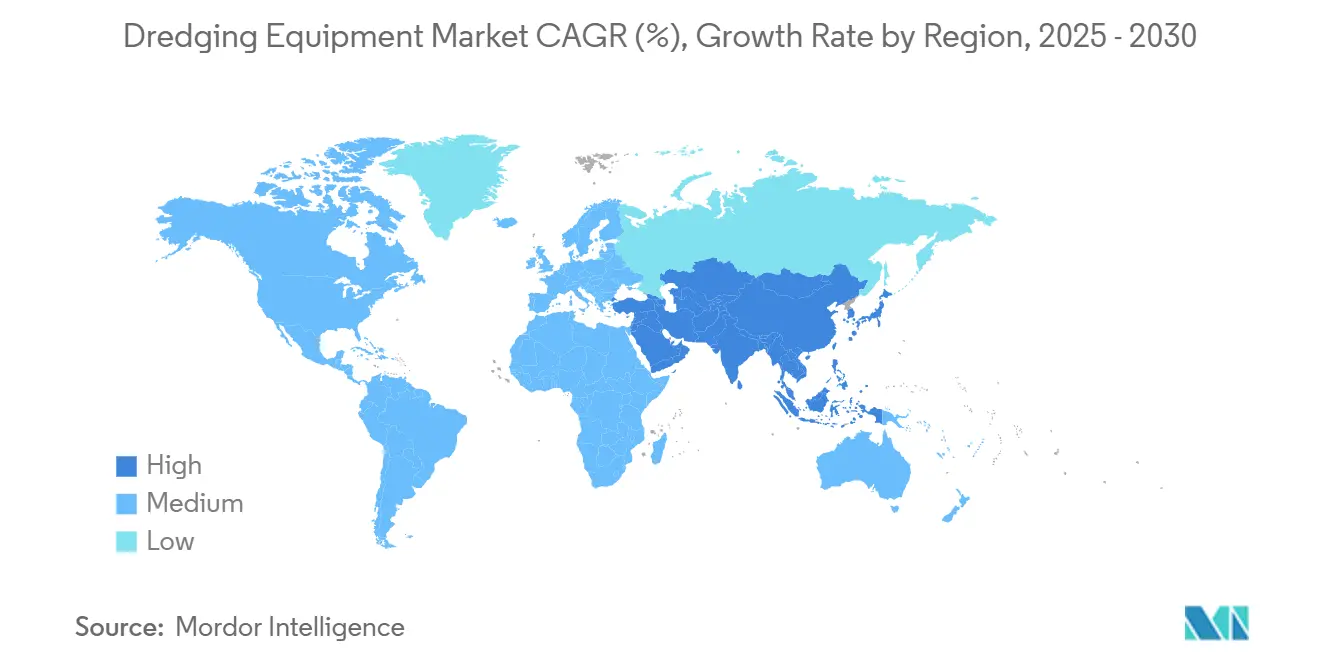

- By geography, Asia-Pacific commanded 34.27% of the dredging equipment market share in 2024 and will maintain the top regional growth at 7.82% CAGR through 2030.

Global Dredging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Port-Capacity Expansion | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Offshore Wind And Cables | +0.9% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Inland-Waterway Upgrades | +0.8% | North America core, spill-over to Europe | Medium term (2-4 years) |

| Autonomous Dredging Tech | +0.6% | Global, early adoption in Netherlands and US | Long term (≥ 4 years) |

| Beneficial Sediment Reuse | +0.5% | Global, strongest in coastal regions | Short term (≤ 2 years) |

| Circular Sand Substitutes | +0.4% | Global, with early gains in Europe and Asia | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Accelerated Port-Capacity Expansion

Mega-projects such as the Houston Ship Channel widening and the Oakland Harbor turning-basin upgrade collectively signal a structural move toward deeper, wider channels. Each initiative involves millions of cubic yards of sediment, compelling fleet owners to modernize pumps, cutter heads, and hopper capacity. Wider drafts deliver sizable economic multipliers; the Mississippi River 50-foot project yields a 7.2-to-1 benefit-cost ratio. Contractors with high-horsepower hydraulic equipment secure premium utilization as ports race to accommodate post-Panamax vessels. That urgency places steady pressure on the dredging equipment market for larger, more energy-efficient assets and drives orders for electric or hybrid dredgers that meet urban-air-quality rules.

Offshore Wind and Subsea-Cable Build-Out

Global offshore wind capacity is forecast to jump from 57 GW in 2021 to 316 GW by 2030, a six-fold expansion that requires precision seabed levelling, foundation trenching, and cable burial [1]“Offshore Wind Outlook 2030,”, WindEurope, windeurope.org. Cable-laying specifications increasingly call for 5–6 feet burial depths to safeguard against fishing gear and anchors, mandating dense geophysical surveys and low-turbidity dredging spreads[2]“Cable Burial Best Practices,”, NYSERDA, nyserda.ny.gov. Vessel scarcity intensifies the opportunity: only a handful of rock-placement and multipurpose installation vessels meet new regulatory emission limits. Orders like Van Oord’s hybrid water-injection dredgers illustrate the technology shift toward energy-optimized hulls and battery support systems. In North America, contractors pivot into this niche, placing million-dollar rock installation vessels into service to capture rising subsea-cable margins.

Government Inland-Waterway Modernization

In 2024, the Water Resources Development Act took significant steps by easing project payback hurdles, introducing a federal cost share for inland-waterway construction, and ensuring full federal funding for maintenance dredging up to 55 feet. These legislative changes enhance the financial feasibility of large-scale projects, paving the way for smoother execution and quicker returns on investment. The policy brings long-term assurance for fleet owners, securing a multiyear project backlog and instilling confidence to invest in advanced equipment, including larger cutter or trailing suction hopper dredgers. Leading contractors derive most of their annual revenue from federal contracts and find the act's provisions particularly beneficial. This policy continuity stabilizes their revenue streams and directly impacts equipment refresh cycles, allowing contractors to upgrade their fleets in line with evolving project demands. The act bolsters the inland-waterway infrastructure sector by tackling funding and operational challenges and promoting sustained market growth.

AI-Enabled Autonomous Dredging Adoption

Prototype autonomous trailing suction hopper dredgers now feature modular navigation suites that integrate LiDAR, dynamic positioning, and machine-learning control loops. Concepts for submerged maintenance dredgers, boasting optimized hull geometries, promise significant propulsion and pump power savings. While these autonomous vessels come with higher capital costs than their conventional counterparts, life-cycle profit modeling suggests they can yield double the returns for owners over 15 years. As a result, early adopters enjoy a pronounced competitive edge, benefiting from reduced crew risks, diminished fuel consumption, and enhanced accuracy in cut volumes, especially in ecologically sensitive areas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Eco-Compliance Costs | -0.7% | Global, strictest in North America and EU | Short term (≤ 2 years) |

| High CAPEX, Long Payback | -0.5% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Skilled-Labor Shortage | -0.4% | North America and EU core, expanding globally | Long term (≥ 4 years) |

| Marine-Fuel Volatility | -0.3% | Global, with acute impact on long-distance projects | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening Environmental-Compliance Costs

In 2025, Colorado introduced its dredge-and-fill permitting program, lengthening documentation timelines and adding complexity to compliance processes. While aiming to enhance regulatory oversight, such state-level statutes inadvertently extend engineering lead times and inflate operating expense forecasts. These extended timelines and increased costs place significant pressure on contractor margins, particularly affecting smaller firms that often lack the resources to absorb such financial and operational burdens. Consequently, this has reduced participation from smaller firms in the dredging equipment market, potentially impacting market competition and innovation.

Volatility in Marine-Fuel Pricing & Availability

Geopolitical disruption in the Suez Canal and Red Sea routinely spikes bunker fuel prices, undermining the economics of multi-month dredging campaigns. Hybrid-powered upgrades, like a recently delivered clamshell dredge that cuts CO₂, offer partial relief but require high upfront capital. Fixed-price project contracts often lack fuel-cost pass-through clauses, creating financial exposure when marine diesel prices jump unexpectedly, particularly on extended deep-water projects

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dredger Type: Hydraulic Dominance Faces Mechanical Resurgence

Hydraulic dredgers accounted for 43.32% of dredging equipment market share in 2024, reflecting preferred use on high-volume channel deepening and land-reclamation projects that demand continuous pump-to-shore capability. Mechanical dredgers, however, post the fastest 7.28% CAGR through 2030, buoyed by tighter environmental windows that reward grab-bucket accuracy and confined-site efficiency. Cutter suction units within the hydraulic segment keep traction in mixed-soil regions thanks to powerful ladder rigs and variable-speed cutting heads tailored for rock interlayers. Electric-drive retrofits at projects such as the Oakland Harbor turning-basin expansion reinforce a trend toward lower-emission hydraulics.

Growth on the mechanical side stems from remediation mandates where turbidity caps favor dig-and-barge workflows, such as the Port of Auckland’s soft-seabed channel deepening. Demand also surfaces in aging river locks that require snagging boulders rather than pumping spoils ashore. Consequently, manufacturers diversify into modular clamshell attachments and low-draft jack-up barges, broadening the dredging equipment market. The dredging equipment industry now markets hybrid thruster packs and barge-mounted filter presses that pair seamlessly with mechanical grabs, signalling an era of integrated multi-tool spreads rather than pure hydraulic or mechanical silos.

By Application: Navigation Maintenance Leads While Offshore Energy Surges

Navigational-channel maintenance retained a 29.92% share of the dredging equipment market size in 2024. Ports that previously required biennial maintenance now face annual campaigns due to intensified storm sedimentation, locking in steady tender volumes.

Nonetheless, offshore renewable-energy construction registers a 9.26% CAGR to 2030, the fastest among all uses, as project developers prepare seabeds for jacket pylons, monopiles, and dynamic cables. Land-reclamation works in Asia remain substantial: the Dover Western Docks revival shifted 720,000 m³ of spoils toward a new logistics estate, confirming continued appetite for urban shoreline expansion. Environmental-remediation jobs also grow, powered by stricter Superfund and EU water-framework directives that require precise cut-thickness confirmation, spurring purchases of multibeam sonar, GPS dig-arms, and dredged-material separation units within the dredging equipment market.

By End User: Government Agencies Dominate While Private Operators Accelerate

Government agencies commanded 40.28% of the dredging equipment market size in 2024 due to federal obligations to maintain navigation safety and flood resilience. Private port operators, however, grow fastest at 7.96% CAGR because supply-chain resiliency pushes terminal owners to deepen berths independent of public-funding cycles.

In New Zealand, the Port of Auckland and privately financed LNG export terminals on the United States Gulf Coast have secured contracts with dedicated mechanical or cutter suction spreads to enhance operational efficiency and meet growing demands. These contracts highlight the increasing reliance on specialized dredging equipment to support infrastructure development and maintain navigational channels. Meanwhile, EPC consortia is making its mark by offering bundled design-build-operate services, which streamline project execution and reduce operational complexities. This approach drives the demand for flexible dredging plants in the dredging equipment market, as stakeholders seek adaptable solutions to address diverse project requirements and optimize resource utilization.

By Ownership Model: Contractor-Owned Model Leads With Project-Owned Gaining Momentum

The contractor-owned model represented 43.82% of the dredging equipment market share 2024, as firms such as Boskalis and Great Lakes deployed global fleets across multiple clients. Project-owned fleets accelerate at 8.92% CAGR during the forecast period, as public-private partnerships acquire purpose-built dredgers for decade-long megaprojects.

Enhanced U.S. federal cost-sharing makes direct equipment purchase feasible for state port authorities, while Asian sovereign wealth funds sponsor purpose-built cutter suction units for reclamation islands. Rental-and-lease pools serve small remediation contracts, ensuring a pathway for mid-tier contractors to participate in specialized works without prohibitive capex.

Geography Analysis

Asia-Pacific controlled 34.27% of the dredging equipment market share in 2024 and maintained the top 7.82% CAGR to 2030. China’s manufactured-sand push reinforces demand for high-throughput hydraulic plants, while environmental curbs encourage low-turbidity mechanical grabs. Deep-sea ports built in Bangladesh, Vietnam, and the Philippines further enlarge the regional orderbook.

North America exhibits mature yet steady growth anchored by unparalleled legislative support. The dredging equipment market for the United States alone is underpinned by concurrent federal channel projects plus inland-waterway lock modernizations. Strong emphasis on beneficial-use and habitat-restoration schemes fuels the procurement of sediment-processing barges and shoreline-placement systems.

Europe remains a technological bellwether. Spotlight innovation in hybrid propulsion and circular-economy material handling. EU recycling mandates nurture an aftermarket for dredge-spoil washing plants, positioning the dredging equipment market for incremental gains despite stricter emission ceilings.

Africa and the Middle East emerge as high-value opportunity corridors. Senegal’s Ndayane deep-water port project removes 10 million m³ of soil, necessitating large-cutter suction dredgers unavailable locally. Gulf petrochemical expansion and Red Sea canal-widening plans drive new-build orders from regional EPC entities, though project financing hinges on fuel-price stability.

Competitive Landscape

The global dredging equipment market is moderately fragmented, with no single player dominating internationally, yet the top five operators still control technologically advanced fleets. Great Lakes reported significant revenue backlog dominated by capital deepening and coastal-protection jobs, while branching into offshore-wind rock installation with the new vessel Acadia.

Mid-size European actors like Jan De Nul and DEME pursue niche specialization in mega-reclamation and inter-array cable trenching. Asian state-linked outfits expand through concessional financing packages, bundling dredging with port-ownership stakes across Belt and Road corridors. Equipment OEMs partner closely with service contractors to co-develop autonomous control suites, sharing R&D costs and reducing time-to-market.

Competitive differentiation increasingly hinges on ESG compliance and digital productivity controls. Operators with hybrid drives and AI-powered production dashboards routinely win tenders stipulating emission caps or precision-cut tolerances. New entrants face twin barriers of high capex and stringent crewing requirements, reinforcing the incumbents’ scale benefits while ensuring steady but not rapid consolidation in the dredging equipment market.

Dredging Equipment Industry Leaders

Damen Shipyards Group

Boskalis Westminster

DEME Group

Jan De Nul Group

Royal IHC (IHC Merwede Holding B.V. )

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Antigua and Barbuda's Cabinet has approved the acquisition of specialized dredging equipment to address delays and restart stalled operations at St John's and Crabbs harbors. This decision aims to enhance the efficiency of harbor activities, ensure the timely completion of ongoing projects, and support the country's maritime infrastructure development.

- May 2025: Italdraghe, in partnership with a renowned Indian shipyard, has signed a significant contract to supply six SGT 450 (18”) cutter suction dredgers (CSD) to the Indian market. This agreement demonstrates Italdraghe's dedication to strengthening its regional presence and addressing the increasing demand for advanced dredging solutions. The collaboration with the Indian shipyard highlights the strategic importance of local partnerships in ensuring efficient production and timely delivery of these cutting-edge dredgers.

Global Dredging Equipment Market Report Scope

| Mechanical Dredger |

| Hydraulic Dredger |

| Others |

| Navigational-Channel Maintenance |

| Port & Harbour Expansion |

| Land Reclamation |

| Offshore Renewable-Energy Construction |

| Environmental Remediation |

| Construction & Mining (Sand Extraction) |

| Disaster Recovery & Flood Control |

| Government Agencies |

| Private Port Operators |

| EPC Contractors |

| Mining & Energy Companies |

| Contractor-Owned |

| Project-Owned (Government/PPP) |

| Rental / Lease Fleet |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| Vietnam | |

| United Kingdom | |

| France | |

| Netherlands | |

| Norway | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Indonesia | |

| Malaysia | |

| Philippines | |

| Singapore | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Dredger Type | Mechanical Dredger | |

| Hydraulic Dredger | ||

| Others | ||

| By Application | Navigational-Channel Maintenance | |

| Port & Harbour Expansion | ||

| Land Reclamation | ||

| Offshore Renewable-Energy Construction | ||

| Environmental Remediation | ||

| Construction & Mining (Sand Extraction) | ||

| Disaster Recovery & Flood Control | ||

| By End User | Government Agencies | |

| Private Port Operators | ||

| EPC Contractors | ||

| Mining & Energy Companies | ||

| By Ownership Model | Contractor-Owned | |

| Project-Owned (Government/PPP) | ||

| Rental / Lease Fleet | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| Vietnam | ||

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Norway | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Indonesia | ||

| Malaysia | ||

| Philippines | ||

| Singapore | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the dredging equipment market in 2025?

The dredging equipment market size stands at USD 5.8 billion in 2025.

Which application is expanding fastest?

Offshore renewable-energy construction posts the highest 9.26% CAGR as wind-farm and subsea-cable projects proliferate.

Why are hydraulic dredgers preferred in large projects?

Their continuous pump-to-shore capability handles huge sediment volumes efficiently, giving them 43.32% market share in 2024.

How does new U.S. legislation impact fleet investment?

The Water Resources Development Act’s 75% federal cost share lowers project risk, prompting public agencies to consider project-owned dredgers.

Which region leads growth through 2030?

Asia-Pacific heads the expansion with a projected 7.82% CAGR driven by port-modernization and land-reclamation activity.

Page last updated on: