Used Construction Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

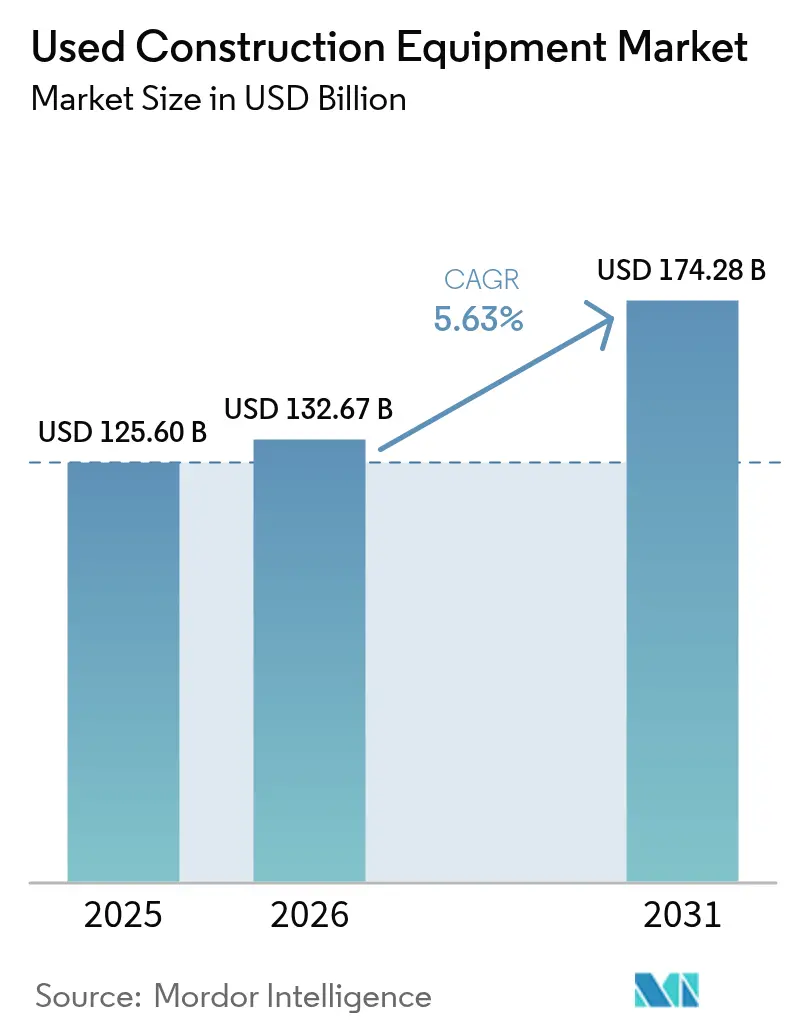

| Market Size (2026) | USD 132.67 Billion |

| Market Size (2031) | USD 174.28 Billion |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

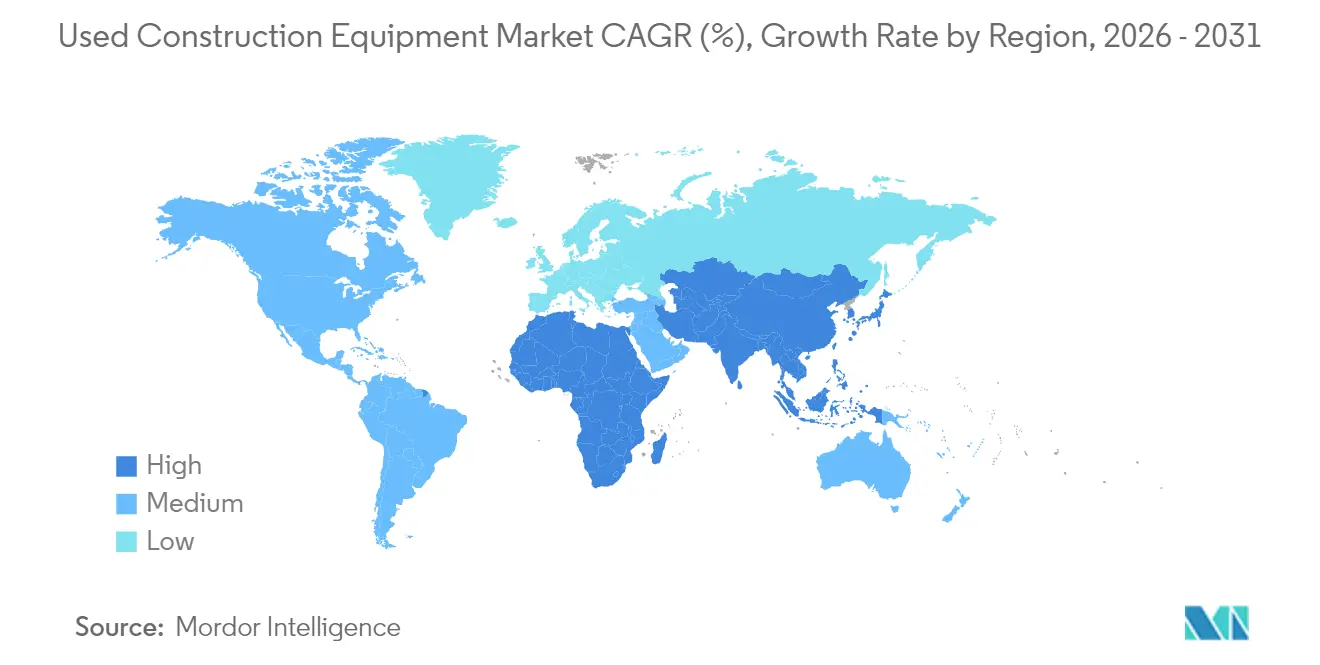

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Used Construction Equipment Market Analysis by Mordor Intelligence

Used construction equipment market size in 2026 is estimated at USD 132.67 billion, growing from 2025 value of USD 125.60 billion with 2031 projections showing USD 174.28 billion, growing at 5.63% CAGR over 2026-2031. Robust infrastructure pipelines in Asia-Pacific, the acceleration of residual values, and supply-chain disruptions that extend original-equipment lead times are recalibrating purchase decisions toward immediately deployable assets. Fleet operators in both mature and emerging regions now treat pre-owned machines as core capacity, compressing traditional replacement windows and reshaping residual value models. The widening gap between project start dates and new-equipment delivery is also stimulating cross-border flows, with dealers shipping inventory from slower to faster growing regions to arbitrage price differentials. Meanwhile, electrification mandates in urban centers are creating two distinct value curves in which compliant electric units command premiums while older diesel machines retain demand in unrestricted territories.

Key Report Takeaways

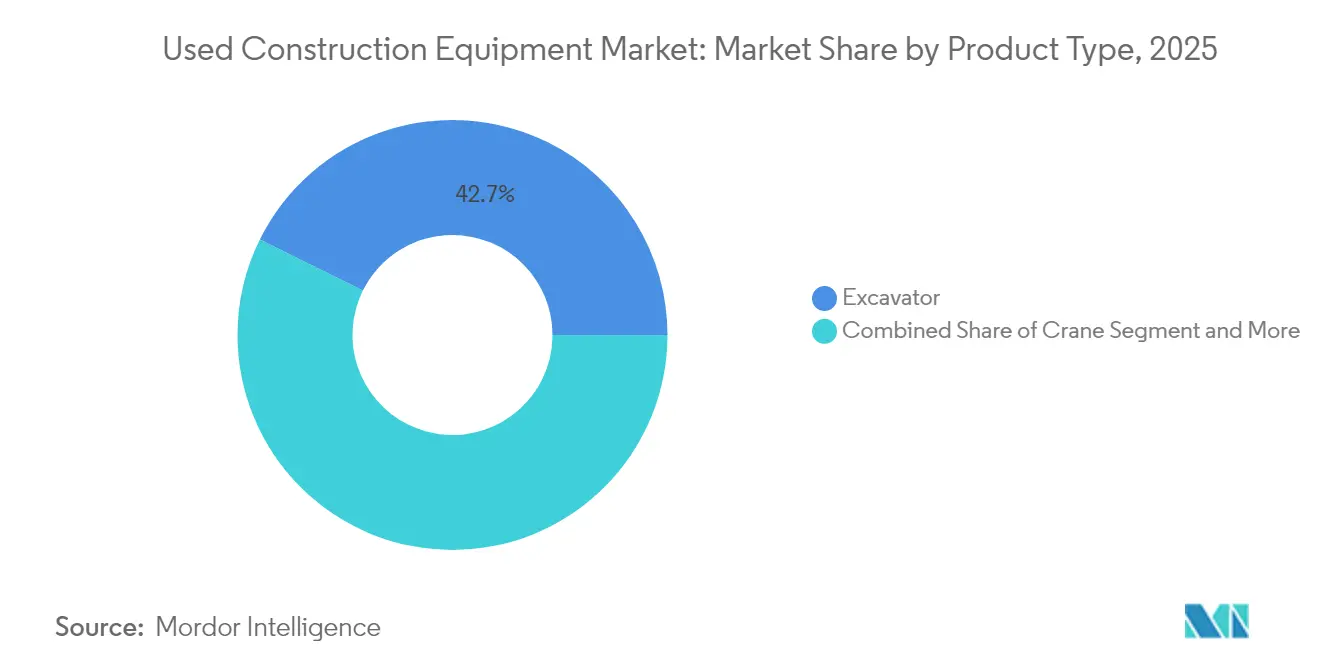

- By product type, excavators held 42.68% of the used construction equipment market share in 2025; cranes recorded the highest 6.42% CAGR forecast to 2031.

- By drive type, internal combustion engines dominated with a 90.92% of the used construction equipment market share in 2025, while electric powertrains are expanding at an 8.08% CAGR to 2031.

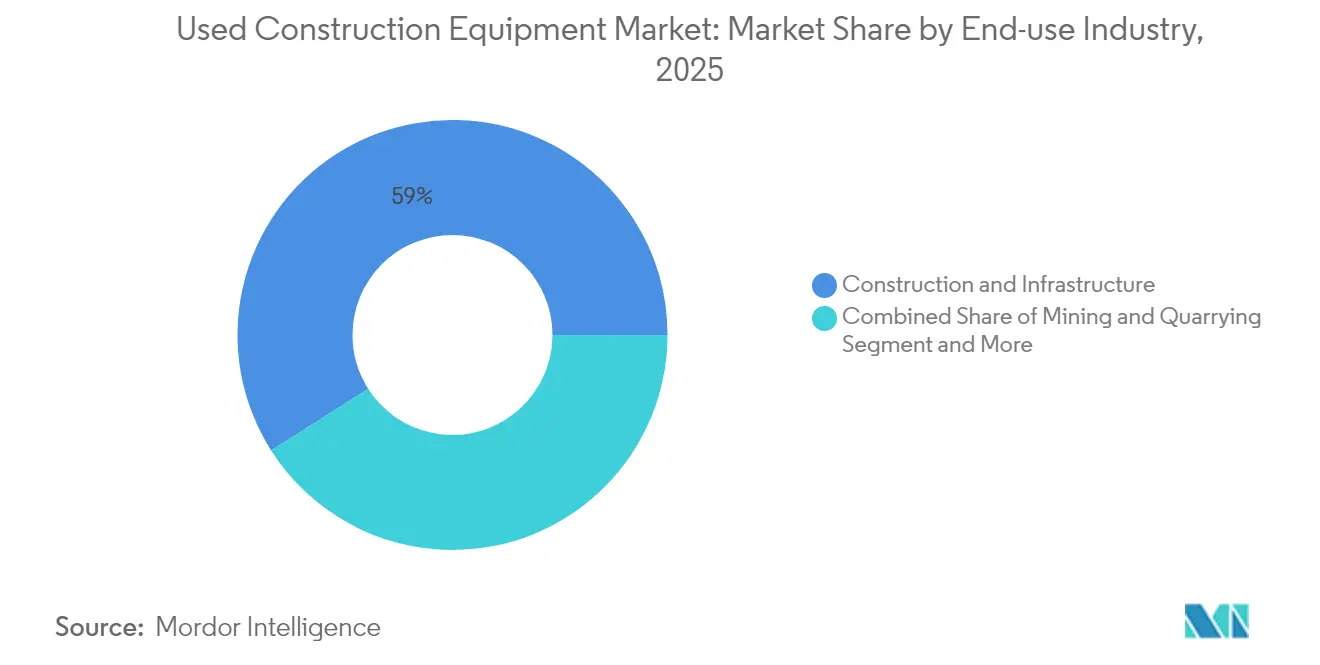

- By end-use industry, construction and infrastructure accounted for 59.02% of the used construction equipment market share in 2025 and are advancing at a 6.15% CAGR through 2031.

- By sales channel, dealers and brokers held a 53.78% of the used construction equipment market share in 2025; auction platforms recorded the highest 7.03% CAGR forecast to 2031.

- By geography, Asia-Pacific commanded 47.62% of the used construction equipment market share in 2025 and leads growth at a 6.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Used Construction Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain-Driven Fleet Renewals | +1.2% | Global with peak impact in North America and Asia-Pacific | Short term (≤ 2 years) |

| Infrastructure Stimulus Emerging Markets | +1.1% | Asia-Pacific core, spill-over to Middle East and South America | Long term (≥ 4 years) |

| Soaring Residual Values Resale ROI | +0.9% | Global, especially Europe and North America | Medium term (2-4 years) |

| Electrification Mandates for Urban Job-Sites | +0.8% | Europe and select North American cities, expanding globally | Long term (≥ 4 years) |

| Rapid Digitalization Auction Platforms | +0.7% | Global with early adoption in North America and Europe | Medium term (2-4 years) |

| OEM Buy-Back and Certified Programs | +0.6% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain-Driven Fleet Renewals

OEM delivery times that stretch 12-18 months have turned used assets into bridge solutions that frequently become permanent parts of the fleet. Contractors now pay high premiums over pre-2024 valuation benchmarks for immediate delivery, particularly in specialty categories where factory output remains constrained. Demand no longer follows legacy economic cycles and instead hinges on construction start dates, creating a structural pull that underpins the used construction equipment market through the near term. Dealers report that standardized models such as 20- to 30-ton excavators and mid-size wheel loaders transact fastest, because parts availability and operator familiarity compress adoption risk. The dynamic is especially intense in North America and the Asia-Pacific, where mega-projects overlap with housing shortages. These conditions sustain above-trend prices and encourage fleet managers to hedge future availability by locking in secondary-market capacity early.

Infrastructure Stimulus in Emerging Markets

Asia-Pacific governments need approximately USD 43 trillion in capital spending through 2035, with India’s USD 1.4 trillion National Infrastructure Pipeline and China’s urban renewal plans headline examples [1]“Meeting Asia’s Infrastructure Needs,” Asian Development Bank, adb.org. Domestic production cannot fully cover near-term demand for standardized equipment, so imports of 3- to 5-year-old machines fill the gap. Dealers in Japan, Europe, and North America increasingly ship compliant units to India, Indonesia, and the Philippines, creating a jump in cross-border flows since 2024. Price arbitrage narrows as buyers in emerging markets gain real-time visibility into global listings, forcing sellers to align asking prices with international benchmarks. Governments often prioritize project speed over equipment age, making lightly used machinery acceptable as long as reliability thresholds are met.

Soaring Residual Values Driving Resale ROI

Typical depreciation curves have contracted significantly, converting disposal from a cost center into a profit source for many owners. Resale upside is altering lease structures, with term lengths shortening to three years so fleets can capture elevated exit values. Buyers are choosing brands and configurations with the strongest secondary-market performance, shifting negotiating leverage toward OEMs that publish transparent buy-back guarantees. Smaller contractors benefit as stronger trade-in positions open access to higher-tier machines that once sat outside their budgets. The feedback loop of tight supply and elevated prices reinforces asset appreciation, further pulling capital into the used construction equipment market.

Electrification Mandates for Urban Job-Sites

London’s Non-Road Mobile Machinery Low Emission Zone and Norwegian city pledges for zero-emission construction sites are pushing electric machines into premium territory, often above diesel equivalents [2]“Non-Road Mobile Machinery Low Emission Zone,” Transport for London, tfl.gov.uk. Contractors win jobs partly based on emission compliance, translating regulatory timelines into tangible equipment demand. Because OEM electric production remains limited, early adopters enjoy scarcity premiums in resale markets. Parallel diesel fleets still dominate rural and heavy-duty tasks, so value curves bifurcate by geography rather than technology alone. Battery improvements are narrowing the performance gap, yet the total cost of ownership already favors electrics in low-utilization urban projects where idle diesel burn and mandated retrofit costs erode margins.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Used-Equipment Price Cycles | -0.8% | Global, highest swings in commodity-dependent regions | Short term (≤ 2 years) |

| Financing Tightness for Older Assets | -0.6% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Regulatory Uncertainty on Engine Retrofits | -0.5% | Europe and North America, extending to Asia-Pacific | Long term (≥ 4 years) |

| Fragmented Inspection-Quality Standards | -0.4% | Global with uneven enforcement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Used-Equipment Price Cycles

Quarterly swings impede financing and disposal decisions, particularly in mining-oriented equipment that tracks commodity super-cycles. In downturns, values of haul trucks and large loaders can halve within 12 months before recovering as metal prices rebound. Small contractors without diversified fleets face balance-sheet stress, sometimes delaying purchases until volatility subsides, which compresses liquidity and amplifies further price drops. Less predictable cash flows also deter lenders, tightening credit just when buyers most need financing to capitalize on discounted inventory.

Financing Tightness for Above 8-Year Assets

Banks are retreating from loans on machines older than eight years because default likelihood rises and residual values become difficult to model. Interest-rate spreads widen, and loan-to-value ratios fall significantly, pushing many transactions to cash. Larger rental fleets can absorb the cost, but small operators find themselves locked out of quality late-life equipment. Peer-to-peer platforms and asset-backed securities provide partial relief, yet their scale is still low and geographic coverage uneven. The financing gap places a practical ceiling on secondary-market liquidity for aging machines, muting total growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Excavators Lead While Cranes Accelerate

Excavators accounted for 42.68% of the used construction equipment market size in 2025, owing to their versatility across site preparation, trenching, and demolition tasks. Ready access to parts and operator familiarity reduces downtime and underpins high absorption in rental fleets. The category’s liquidity attracts both institutional investors and smaller contractors, keeping turnover brisk even during seasonal slowdowns. Cranes are advancing at a 6.42% CAGR through 2031 as urban densification fuels demand for high-reach lifting solutions. Tight OEM production slots for tower and crawler cranes amplify the premium on late-model units with accurate service logs. Sellers can thus capture above-average margins, and buyers accept them because rental alternatives are scarce during peak building cycles. Attachments and material-handling implements add modular flexibility, encouraging contractors to optimize fleets around core carriers and specialized tooling rather than multiple dedicated machines. This modular approach bolsters absorption for quick-coupler systems that accelerate jobsite changeovers.

Rising safety standards are also directing attention to telematics-enabled models that record duty cycles and overload events. Units with complete electronic histories transact faster and at higher values, especially in Europe, where regulatory compliance is strict. Meanwhile, standardized control layouts across major brands ease cross-training, allowing mixed fleets to reallocate operators without productivity penalties. That capability reinforces excavators’ leadership, while specialized lifting still distinguishes cranes as the fastest growth niche within the used construction equipment market.

By Drive Type: ICE Dominance Faces Electric Disruption

Internal combustion engines continue to hold 90.92% of the used construction equipment market share in 2025 due to unmatched energy density and ubiquitous diesel infrastructure. Heavy earthmoving in remote mining and pipeline projects will keep diesel indispensable beyond the forecast horizon. Yet electric machines are showing an 8.08% CAGR and are already pivotal in city centers with decibel limits and carbon budgets. Premiums of 20-30% persist for compliant units because supply is thin and the learning curve for maintenance is steep. Fleets exploiting night-shift work in emission-controlled areas find total operating costs lower for electrics, particularly when local utilities offer discounted off-peak charging.

Hybrid systems are carving a narrow but resilient space, especially on equipment with variable duty cycles, such as telescopic handlers that idle extensively. Diesel-electric drivetrains lower fuel consumption and delay battery replacement schedules, balancing capital cost against operational savings. However, the technology premium narrows as battery prices continue to fall. For now, ICE dominance gives the used construction equipment market essential depth and value stability, while growth in zero-emission zones lays the groundwork for a gradual but irreversible shift to electrics.

By End-use Industry: Construction and Infrastructure Drive Demand

Construction and infrastructure applications controlled 59.02% of the used construction equipment market share in 2025 and are forecast to advance at a 6.15% CAGR as governments pursue backlog reduction in transport, energy, and housing. Megaprojects compress project lead times, forcing contractors to source ready-to-deploy units rather than wait on lengthy build-to-order cycles. Mining and quarrying present a stable base load volume for ultra-class haul trucks and large bulldozers whose secondary value correlates strongly with commodity prices. Agriculture and forestry create seasonal trade flows that keep inventory cycling, though volumes remain small relative to infrastructure.

E-commerce warehouse expansion is stimulating industrial builds that integrate material-handling automation, pushing crossover demand for compact loaders and telehandlers. Contractors now redeploy equipment across segments to maximize utilization; an excavator might dig drainage on an infrastructure site in spring and later load aggregate at a quarry. Such versatility increases fungibility, buoying liquidity and supporting steady price floors.

By Sales Channel: Dealers Dominate While Auctions Digitalize

Dealer and broker networks retained a 53.78% of the used construction equipment market share in 2025 by combining inspection, warranty, and financing packages that de-risk transactions. They excel in heavy or specialized categories where post-sale technical support is critical. Online and physical auctions are expanding at a 7.03% CAGR as global bidding widens customer pools and lowers fees. Digital catalogs, augmented-reality inspections, and escrow services reassure international buyers, making it easier to import equipment from surplus regions.

OEM-certified pre-owned branches overlay the dealer-auction landscape with a branded assurance layer. Premiums of 10-15% are common, yet buyers often accept them because warranties and financing tie-outs streamline procurement. Rental fleet disposals feed all channels, and their well-documented maintenance history keeps clearance rates high. Over time, channel choice is turning into a portfolio decision: fleets mix dealership purchases for critical machines, auction acquisitions for opportunistic buys, and OEM programs for warranty-sensitive deployments.

Geography Analysis

Asia-Pacific held 47.62% of the used construction equipment market share in 2025 and will grow at a 6.74% CAGR through 2031 as India, China, and Southeast Asian nations accelerate spending on transport corridors, renewable power, and housing. India’s National Infrastructure Pipeline and China’s urban renewal policies drive sustained machine absorption, overwhelming local OEM capacity and prompting imports from Japan, Europe, and North America. Equipment transit times shorten due to regional maritime logistics investments, enabling just-in-time arrivals that align with project mobilization schedules.

North America's growth is underpinned by a mature secondary-market ecosystem and steady public-works appropriations in the United States. OEM buy-back programs are most advanced here, allowing contractors to rotate fleets every three to four years without major depreciation hits. Canada’s uptick in resource projects has boosted demand for specialized forestry and pipeline equipment, further deepening liquidity in cross-border trade. Europe exhibits moderate volume but high unit values, driven by stringent emission frameworks that elevate the price of Stage V-compliant machines. Residual values remain strong partly because reimbursement programs in Germany and the Nordics subsidize cleaner equipment adoption. Electric mini-excavators and compact wheel loaders are disproportionately represented in European resales thanks to dense urban markets and early regulatory adoption.

The Middle East and Africa are emerging hot spots, especially Gulf Cooperation Council nations that balance oil revenue diversification with ambitious construction programs. Mega-projects such as NEOM in Saudi Arabia require immediate fleets, favoring imports of reliable late-model machines. Sub-Saharan Africa’s mining expansion sustains demand for several construction equipment, though political risk and logistics still limit broader market depth. South America mirrors commodity cycles; Brazil and Chile purchase heavily during copper and iron-ore upswings, then slow during downturns, injecting volatility but also arbitrage opportunities into global flows.

Competitive Landscape

The competitive arena remains moderately fragmented. The top OEM-aligned certified pre-owned programs and the largest independent auction houses together hold a major share of global transaction value, with the remainder split among thousands of regional dealers and brokers. OEMs such as Caterpillar, Komatsu, Liebherr, and XCMG are capturing secondary-market margin by bundling warranties, telematics subscriptions, and financing into one invoice. Independent dealers respond by specializing in niche categories like foundation drills or slip-form pavers, where OEM involvement is lighter.

Technology adoption is pivotal. Leading players deploy IoT sensors and predictive analytics that report real-time machine health, attracting buyers who value uptime warranties. Komatsu’s acquisition of an AI analytics firm equips its dealer network with predictive maintenance dashboards that guide trade-in valuations, tightening the buy-sell spread [3]“Komatsu Acquires Octodots Analytics,” Komatsu Ltd., komatsu.com. Hitachi partners with energy-storage start-ups to retrofit older excavators with hybrid kits, creating upgrade paths that extend asset life while meeting local emission rules.

Auction houses invest heavily in cloud infrastructure and global logistics alliances to offer one-stop export solutions that compress delivery from six weeks to three. Dealer management systems now integrate with online platforms, giving sellers instant visibility into global price benchmarks and accelerating inventory turnover. Cross-listing equipment across multiple channels maximizes exposure, but also intensifies competition on service quality, forcing slower adopters to modernize or lose market share.

Used Construction Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Deere & Company

Volvo Construction Equipment

Hitachi Construction Machinery Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: JCB India signed an MoU with Shriram Automall India Limited to streamline resale of pre-owned JCB machines, blending manufacturer backing with SAMIL’s phygital marketplace reach.

- December 2024: XCMG Machinery launched its “XCMG Certified Used Equipment” brand, advancing a circular model that prioritizes green lifecycle management for the global construction industry.

- June 2024: Shriram Automall India formed a strategic alliance with Volvo Construction Equipment, leveraging SAMIL’s auction platforms and support services for pre-owned assets.

- May 2024: Liebherr partnered with Krank Technology to introduce the “Used Equipment Marketplace,” its proprietary digital sales platform for selected construction and material-handling lines.

Global Used Construction Equipment Market Report Scope

Pre-owned heavy-duty construction machinery, specially designed for carrying out construction tasks, most commonly earthmoving operations, is referred to as used construction equipment.

The Used Construction Equipment Market is segmented by product type (Crane, Telescopic Handler, Excavator, Material Handling Equipment, Loader and Backhoe, and Others), by drive type ( Internal Combustion Engine, Electric, and Hybrid), and by Geography (North America, Europe, Asia-Pacific, and Rest of World). The report offers the market size and forecast in value (USD Billion) for all the above segments.

| Crane |

| Telescopic Handler |

| Excavator |

| Material Handling Equipment |

| Loader and Backhoe |

| Attachments and Others |

| Internal Combustion Engine |

| Electric |

| Hybrid |

| Construction and Infrastructure |

| Mining and Quarrying |

| Agriculture and Forestry |

| Industrial and Warehousing |

| Dealer / Broker |

| Auction (Physical and Online) |

| Rental Fleet Disposal |

| Direct OEM Certified Pre-owned |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Spain | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Midde East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Crane | |

| Telescopic Handler | ||

| Excavator | ||

| Material Handling Equipment | ||

| Loader and Backhoe | ||

| Attachments and Others | ||

| By Drive Type | Internal Combustion Engine | |

| Electric | ||

| Hybrid | ||

| By End-use Industry | Construction and Infrastructure | |

| Mining and Quarrying | ||

| Agriculture and Forestry | ||

| Industrial and Warehousing | ||

| By Sales Channel | Dealer / Broker | |

| Auction (Physical and Online) | ||

| Rental Fleet Disposal | ||

| Direct OEM Certified Pre-owned | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Midde East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is demand for pre-owned machinery growing in Asia-Pacific?

Asia-Pacific demand is expanding at a 6.74% CAGR to 2031, supported by infrastructure megaprojects that need immediately deployable fleets.

Which equipment category holds the largest share of global resale value?

Excavators lead with 42.68% of worldwide transactions thanks to their versatility and robust dealer support.

Why are residual values rising rather than falling?

Tight OEM supply, longer lead times, and high project urgency have lifted five-year residuals to about 50% of original list prices, making disposal profitable.

How do emissions rules influence purchasing decisions?

Urban zero-emission mandates push buyers toward electric or Stage V-compliant units that can command 20-30% premiums over conventional diesel equipment.

Page last updated on: