Port Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 21.66 Billion |

| Market Size (2031) | USD 28.16 Billion |

| Growth Rate (2026 - 2031) | 5.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Port Equipment Market Analysis by Mordor Intelligence

Port equipment market size in 2026 is estimated at USD 21.66 billion, growing from 2025 value of USD 20.55 billion with 2031 projections showing USD 28.16 billion, growing at 5.39% CAGR over 2026-2031. Rising container‐ship sizes, stricter decarbonization rules, and accelerated terminal automation continue to reshape procurement decisions in every major gateway. Container throughput has already set fresh records, with China’s automated ports alone processing 16.04 billion tons of cargo and 300 million boxes in 2024, a 3.4% year-on-year rise [1]“2024 Port Throughput Statistics,” Ministry of Transport of the People’s Republic of China, mot.gov.cn. Geopolitical tensions are also influencing sourcing strategies, evidenced by the United States’ USD 20 billion push to onshore crane manufacturing and harden port cyber-security. Meanwhile, Asia Pacific maintains the largest regional foothold, and cranes remain the most purchased equipment class.

Key Report Takeaways

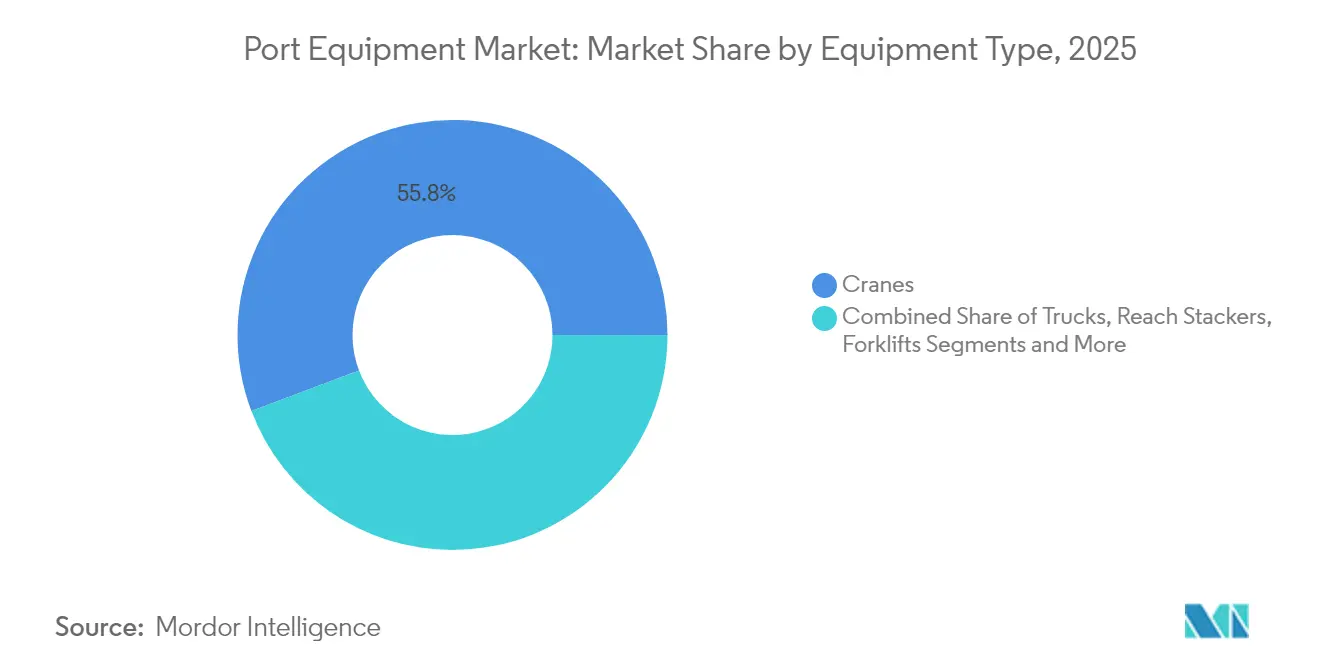

- By equipment type, cranes commanded 55.76% of the port equipment market share in 2025 and are projected to expand at a 6.97% CAGR during the forecast period (2026-2031).

- By application, container handling led the port equipment market with 54.22% of the share in 2025; warehouse and yard logistics are expected to grow at an 8.03% CAGR during the forecast period (2026-2031).

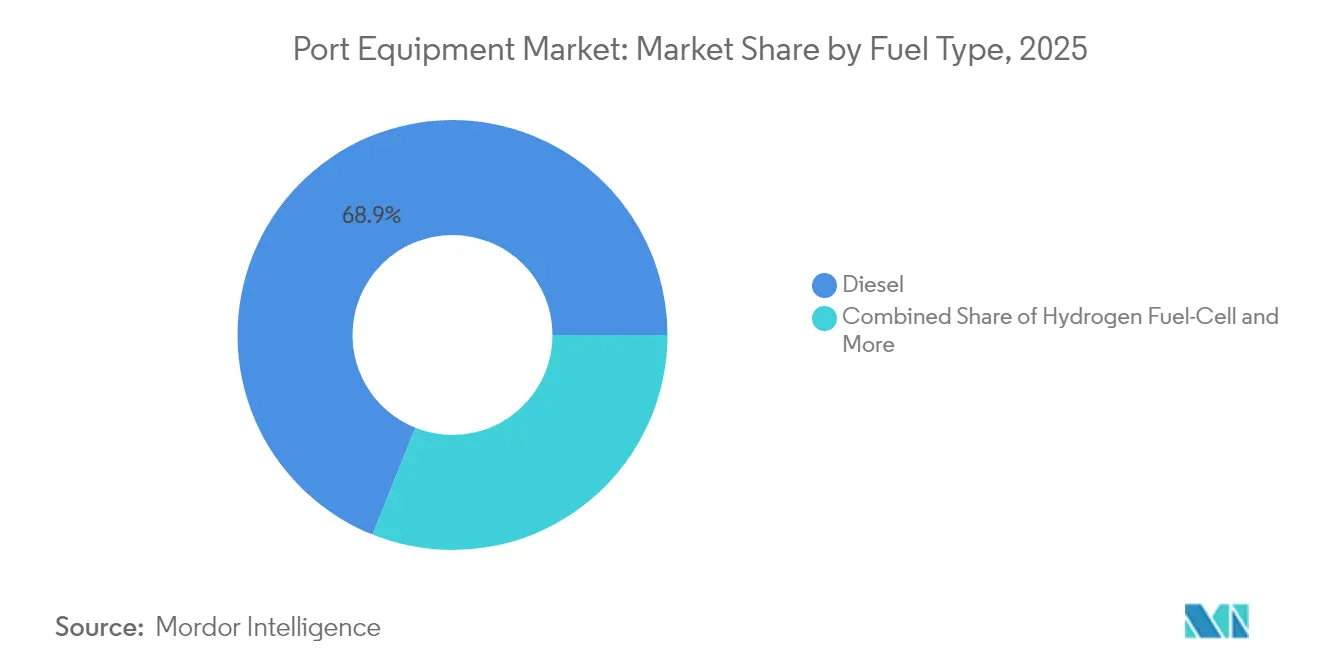

- By fuel type, diesel units accounted for 68.94% of the port equipment market share in 2025, while electric and hybrid models are forecast to post a 8.95% CAGR during the forecast period (2026-2031).

- By operation mode, conventional (manual/semi-auto) accounted for 90.92% of the port equipment market size in 2025, while fully autonomous models are forecast to grow at a 16.05% CAGR during the forecast period (2026-2031).

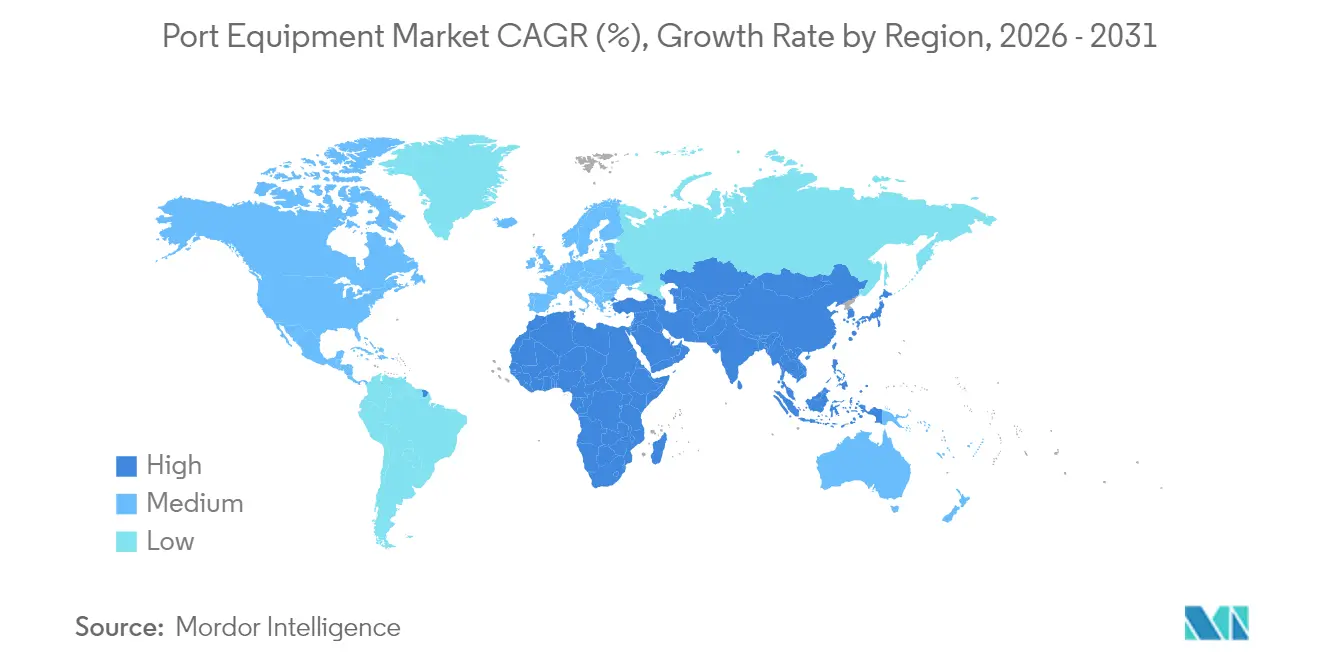

- By geography, the Asia Pacific held 45.88% of the port equipment market share in 2025; the region is anticipated to register a 6.18% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Port Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Container-Ship Sizes | +1.2% | Global hubs | Medium term (2-4 years) |

| Stricter Port-side Decarbonization Mandates | +0.9% | North America and EU; expanding to APAC | Long term (≥ 4 years) |

| Rapid Terminal Automation | +0.8% | APAC core; spill-over to MEA | Medium term (2-4 years) |

| Tariff Threat on Chinese Cranes | +0.6% | North America; secondary in EU | Short term (≤ 2 years) |

| OT Cyber-Security Compliance | +0.4% | Global; led by North America | Medium term (2-4 years) |

| Autonomous, Remotely-Operated Vehicles | +0.3% | APAC and EU early adopters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Container Ship Sizes Driving Demand for Mega-STS And ASC Cranes

Ultra-large container vessels now measure 400 m and carry up to 23,000 TEU, forcing terminals to procure quay cranes with outreach beyond 74 m to clear 24 rows. Each call can require 3,800 trucks and 50 freight trains, straining gate, yard, and rail assets as seen at Hamburg. The Port of Savannah recently took delivery of the East Coast’s largest STS cranes to handle 16,000 TEU ships, adding around 1.5 million TEU of annual capacity. Yet crane productivity has climbed only 90% in two decades versus a 202% jump in bay size, widening operational bottlenecks and stimulating demand for automation and twin-lift spreaders.

Stricter Port-Side Decarbonization Mandates are Accelerating Electric and Hybrid Fleets

California requires 90% zero-emission cargo-handling equipment by 2036, a rule affecting about 33,500 drayage trucks and thousands of terminal assets [2]“In-Use Locomotive & Cargo Handling Rule,” California Air Resources Board, arb.ca.gov. Terminals are reacting: APM Suape allocated USD 47 million for 28 all-electric units to become South America’s first fully electrified site by 2026. An electric STS crane can save USD 3.3 million in diesel and cut 776 t of CO₂ yearly, bolstering the business case. The Zero Emission Port Alliance expects 94% of member purchases to be battery-electric by 2035, underpinning standards for tractors and straddle carriers.

Rapid Terminal Automation to Offset Labor Shortages and Boost Throughput

China already operates 52 automated container and bulk terminals, with Qingdao posting a 15% throughput lift and Yantai a 20% efficiency gain. At Rotterdam, the Maasvlakte II facility realised a 40% productivity jump by pairing remotely-operated STS cranes with battery AGVs. Despite benefits, only 4% of all container terminals are fully automated, largely because projects can cost USD 500 million-USD 1 billion, although phased roll-outs ease disruption.

Tariff Threat on Chinese Cranes Reshaping Regional Sourcing Strategies

Washington has imposed fresh tariffs and offered a USD 20 billion incentive package to build cranes domestically, targeting China’s ZPMC, which holds a significant share in India and a substantial footprint in US facilities. Konecranes and PACECO are forming US partner networks to produce Build America, Buy America-compliant machines, a shift that opens the door for European contenders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-Million-Dollar CAPEX and Long ROI Cycles | -1.1% | Global; acute in emerging markets | Long term (≥ 4 years) |

| Raw-Material Price Volatility | -0.7% | Manufacturing-intensive regions | Medium term (2-4 years) |

| Equipment-Leasing Boom | -0.5% | North America and EU; expanding globally | Medium term (2-4 years) |

| Geopolitical Export-Controls | -0.4% | Restricted markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Multi-Million-Dollar CAPEX and Long ROI Cycles

Automating a terminal can demand USD 500 million–USD 1 billion, with breakeven volumes exceeding 544,000 TEU in a nine-berth design. More than 50% of equipment is now financed externally, and leasing is rising as operators seek to avoid heavy upfront cash outflows [3]“2024 US Equipment Finance Outlook,” Equipment Leasing & Finance Association, elfaonline.org. Extended ROI horizons curb purchasing appetite, giving momentum to equipment-as-a-service contracts that bundle maintenance yet potentially reduce fresh unit sales.

Raw-Material Price Volatility

Steel hit USD 950 t in March 2022 before sliding to USD 579.5 t by July 2024, forcing manufacturers to juggle surcharges and hedge inventories. Hyster-Yale still expects elevated freight and material costs despite strong margins. Electric drivetrains add rare-earth exposure for batteries and motors, making cost management central to competitive bids.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Cranes Dominate Amid Automation Push

The port equipment market size for cranes accounted for 55.76% share in 2025 and is on track for a 6.97% CAGR through 2031. Ship-to-shore models top purchase lists as operators retrofit outreach beyond 74 m to serve 24-row vessels. Projects such as Port Tanjung Pelepas’ five new ULCV quay cranes illustrate the rush to future-proof waterfront assets.Automated stacking cranes are gaining momentum; Hutchison BEST’s seven-block extension lifted yard capacity 25% while lowering truck re-handles. Rubber-tired and rail-mounted gantries are rapidly electrifying, with PSA Halifax contracting eight battery RTGs from Konecranes to create North America’s first fully electric yard. Trucks remain the fastest-growing sub-class as AGVs and terminal tractors integrate autonomy, vision sensors, and clean drivetrains. Toyota’s plan to ship Nagoya-proven AGVs abroad underscores the export potential of Asia-developed technology.

By Application: Container Handling Leads, Warehouse Logistics Accelerates

Container handling absorbed 54.22% of the port equipment market share in 2025 revenue, thanks to record volume expansion and mega-ship cascades. Newbuild STS cranes, yard automatons, and twin-lift spreaders dominate capex plans as ports chase berth productivity gains and shorter vessel dwell. Warehouse logistics, however, is projected to rise at an 8.03% CAGR as e-commerce-driven cross-docking boosts demand for automated mobile robots and intelligent conveyor systems.Bulk cargo handling keeps steady momentum in mineral-rich regions, supported by higher-capacity grabs and continuous ship-unloaders. Ship servicing—mooring, Ro-Ro and passenger terminals, receives targeted investments where cruise and vehicle trades rebound. Port infrastructure construction cycles create episodic spikes in heavy pile-drivers, dredgers, and lifting solutions as governments roll out economic stimulus packages.

By Fuel Type: Electric Transition Accelerates Despite Diesel Dominance

Diesel remains the workhorse with 68.94% of the port equipment market share in 2025, valued for range and refueling speed in remote berths. Regulatory headwinds and TCO economics propel electric and hybrid equipment at a 8.95% CAGR through 2031, making it the most dynamic segment in the port equipment market. Toyota Material Handling’s USD 100 million electric forklift plant illustrates shifting manufacturing footprints as battery demand scales.Hydrogen fuel cell prototypes are moving from pilot to limited fleet status. MITSUI E&S and PACECO fielded the Port of Los Angeles’s first hydrogen RTG, matching diesel performance without grid hooks. Meanwhile, Taylor Machine Works is pairing Cummins-built engines to reach commercial scale. Powertrain diversity is turning into a core spec line-item as operators demand options to meet evolving emissions caps and uptime targets.

By Operation Mode: Conventional Operations Dominate, Autonomous Systems Show Explosive Growth

Manual and semi-automated operations accounted for 90.92% of the port equipment market in 2025, underscoring the enduring reliance on human oversight for complex lifts, exception handling, and berth safety. Conventional fleets benefit from lower upfront costs, established maintenance regimes, and workforce familiarity, making them the default choice for many emerging-market ports. Remote-controlled variants add incremental efficiency without the disruptive capex of full automation, enabling operators to phase upgrades around berth expansions. However, labour shortages, safety requirements, and rising vessel exchanges are exposing productivity ceilings that manual systems struggle to breach.Fully autonomous operations are projected to surge at a 16.05% CAGR through 2031, fuelled by successful deployments such as Qingdao and Yantai, where throughput and efficiency rose 15% and 20% respectively. APM Terminals’ Maasvlakte II demonstrated a 40% productivity uplift by pairing unmanned STS cranes with battery AGVs, validating the return on high-automation capex. Costs remain a barrier—projects can range from USD 500 million to USD 1 billion per terminal, but phased rollouts and performance-based financing are narrowing the gap. Toyota Industries’ plan to export AGVs proven at Nagoya Port, where units achieve 20 mm positioning accuracy, signals a maturing supplier base that should accelerate scale adoption. As technology prices fall and regulatory bodies tighten safety and emissions targets, autonomous systems are set to reshape future order books.

Geography Analysis

Asia Pacific accounted for 45.88% of the port equipment market in 2025 and is forecast to expand at a 6.18% CAGR through 2031. China anchors the region with 52 automated terminals processing 16.04 billion t of cargo a year, reinforcing the port equipment market’s growth engine. Singapore’s PSA Tuas Port typifies regional ambition as it targets 65 million TEU annual capacity through AI-enabled automation. India’s restrictions on Chinese crane purchases are opening opportunities for domestic and non-Chinese suppliers to gain share.

North America generated demand spikes after Washington announced tariffs on Chinese cranes alongside a USD 20 billion incentive for local manufacturing. The United States Coast Guard’s cybersecurity directives are pushing ports to retrofit or replace roughly 200 Chinese-made units, creating a parallel services market. Canada is prioritizing electrification, with PSA Halifax ordering eight battery RTGs as part of a nationwide zero-emission strategy. Together, these factors are reshaping sourcing models and accelerating technology upgrades across the continent.Europe held a substantial revenue share in the port equipment market in 2024 and continues to drive sustainability and digital integration agendas. EUROGATE has rolled out a 5G campus network across Hamburg, Bremerhaven and Wilhelmshaven to support remote operations and real-time diagnostics. The Middle East and Africa are emerging as high-growth zones as governments deploy sovereign infrastructure funds to modernize gateways. DP World has pledged USD 3 billion for African terminal projects, while Saudi Arabia’s NEOM port is installing automated cranes ahead of a 2026 launch. Egypt has also attracted USD 700 million from Hutchison Ports for new facilities at Sokhna and Alexandria, underscoring the region’s rising equipment appetite.

Competitive Landscape

Market concentration is moderate. Kalmar, Konecranes, and ZPMC anchor the leaderboard, but rising players such as Sany and Liebherr are chipping into share by bundling automation suites with localized service offers. Cargotec’s 2024 decision to spin off Kalmar sharpened its product focus on container and heavy material handling, while Konecranes assembled a US supplier network to supply Build America-compliant cranes and widen its electrified yard range.

Differentiation is migrating from pure lifting capacity to integrated software, cyber resilience, and energy flexibility. ZPMC retains a scale advantage, yet security scrutiny in the United States and parts of Europe is opening opportunities for rivals. Liebherr’s USD 2.8 billion zero-emission mining equipment pact with Fortescue hints at cross-industry spill-over, foreshadowing hydrogen and battery modules cascading into port assets.

Equipment-as-a-service offerings are growing. Kalmar and Hyster-Yale now package uptime guarantees and remote diagnostics in subscription form, shifting customer capex to opex and locking in data-rich relationships. Autonomous niche suppliers are partnering with incumbent OEMs to embed perception stacks, further fragmenting intellectual property ownership and revenue pools.

Port Equipment Industry Leaders

Liebherr Group

Kalmar (Cargotec)

Konecranes Oyj

Sany Heavy Industry Co., Ltd.

ZPMC (Shanghai)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Kalmar signed with Maputo Port Development Company to supply five T2i terminal tractors, four heavy forklifts and one medium forklift.

- December 2024: Adani Gangavaram Port introduced two electric grab ship cranes to speed cargo cycles.

- September 2024: Hutchison BEST deployed Southern Europe’s first electric reach stacker in Barcelona.

- July 2024: Konecranes joined a White House initiative to cultivate alternative US manufacturers for large STS cranes.

Global Port Equipment Market Report Scope

The port equipment market covers the latest trends and technological development in the port equipment market, demand of the by Equipment Type (Cranes, Trucks, Reach Stackers, Forklifts, and others), Application (Container handling, ship handling), fuel type (Diesel, Electric, Hybrid) and Geography.

| Cranes | Ship-to-Shore (STS) |

| Rubber-Tyred Gantry (RTG) | |

| Rail-Mounted Gantry (RMG) | |

| Automated Stacking Cranes (ASC) | |

| Mobile Harbor Cranes | |

| Trucks | Terminal Tractors |

| Towing Tractors | |

| Automated Guided Vehicles (AGV) | |

| Reach Stackers | |

| Forklifts | |

| Others |

| Container Handling |

| Bulk Cargo Handling |

| Ship Handling (Mooring, Ro-Ro) |

| Port Infrastructure Construction |

| Warehouse and Yard Logistics |

| Diesel |

| Electric and Hybrid |

| Hydrogen Fuel-Cell |

| Conventional (Manual/Semi-Auto) |

| Fully Autonomous |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Equipment Type | Cranes | Ship-to-Shore (STS) |

| Rubber-Tyred Gantry (RTG) | ||

| Rail-Mounted Gantry (RMG) | ||

| Automated Stacking Cranes (ASC) | ||

| Mobile Harbor Cranes | ||

| Trucks | Terminal Tractors | |

| Towing Tractors | ||

| Automated Guided Vehicles (AGV) | ||

| Reach Stackers | ||

| Forklifts | ||

| Others | ||

| By Application | Container Handling | |

| Bulk Cargo Handling | ||

| Ship Handling (Mooring, Ro-Ro) | ||

| Port Infrastructure Construction | ||

| Warehouse and Yard Logistics | ||

| By Fuel Type | Diesel | |

| Electric and Hybrid | ||

| Hydrogen Fuel-Cell | ||

| By Operation Mode | Conventional (Manual/Semi-Auto) | |

| Fully Autonomous | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the port equipment market?

The port equipment market is valued at USD 21.66 billion in 2026 and is forecast to reach USD 28.16 billion by 2031.

Which equipment type holds the largest revenue share?

Cranes dominate with 55.76% of global revenue in 2025 and are projected to grow at a 6.97% CAGR through 2031.

How fast is electric port equipment growing?

Electric and hybrid models represent the fastest-expanding fuel segment, expected to post a 8.95% CAGR between 2026-2031.

Why is Asia Pacific the largest regional market?

The region benefits from China’s 52 automated terminals, sustained infrastructure spending and a 6.18% CAGR outlook.

Page last updated on: