Surface Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

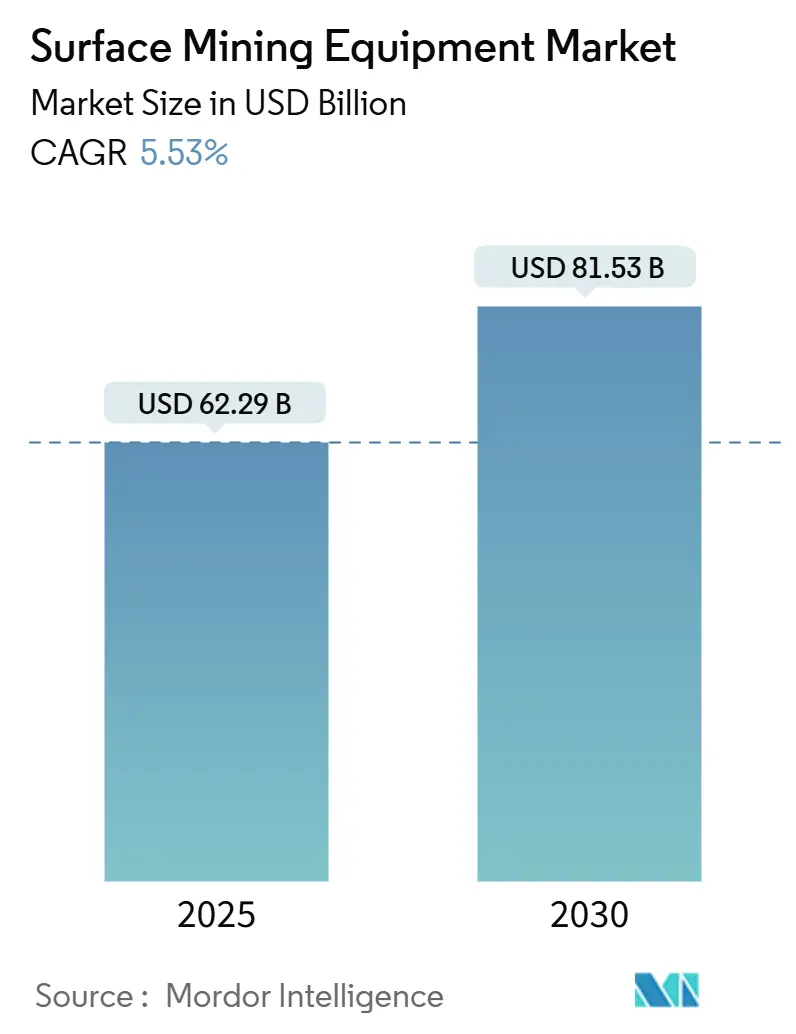

| Market Size (2025) | USD 62.29 Billion |

| Market Size (2030) | USD 81.53 Billion |

| Growth Rate (2025 - 2030) | 5.53% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Surface Mining Equipment Market Analysis by Mordor Intelligence

The Surface Mining Equipment Market Size stood at USD 62.29 billion in 2025 and is forecasted to reach USD 81.53 billion by 2030, advancing at a 5.53% CAGR during the forecast period (2025-2030). Robust demand stems from the accelerating extraction of critical minerals used in electric vehicles, the expansion of large open-pit coal projects in the Asia-Pacific, and the steady replacement of aging diesel fleets. Equipment makers are accelerating autonomous and electric product launches to counter skilled-labor shortages, streamline productivity, and meet tightening emissions mandates. Competitive intensity is rising as established original-equipment manufacturers leverage digital platforms, predictive maintenance services, and battery-electric prototypes to lock in long-term supply contracts. Investment momentum remains resilient despite commodity-price volatility because operators view fleet modernization as essential to lowering unit costs, complying with environmental, social, and governance benchmarks, and sustaining output from deeper, lower-grade deposits.

Key Report Takeaways

- By equipment type, haul trucks captured a 32.28% share of the Surface Mining Equipment Market in 2024, while the excavators segment is projected to register the fastest 6.81% CAGR during the forecast period (2025-2030).

- By power source, diesel held a 73.94% share of the Surface Mining Equipment Market in 2024, whereas the electric equipment segment is expected to grow at a 12.53% CAGR during the forecast period (2025-2030).

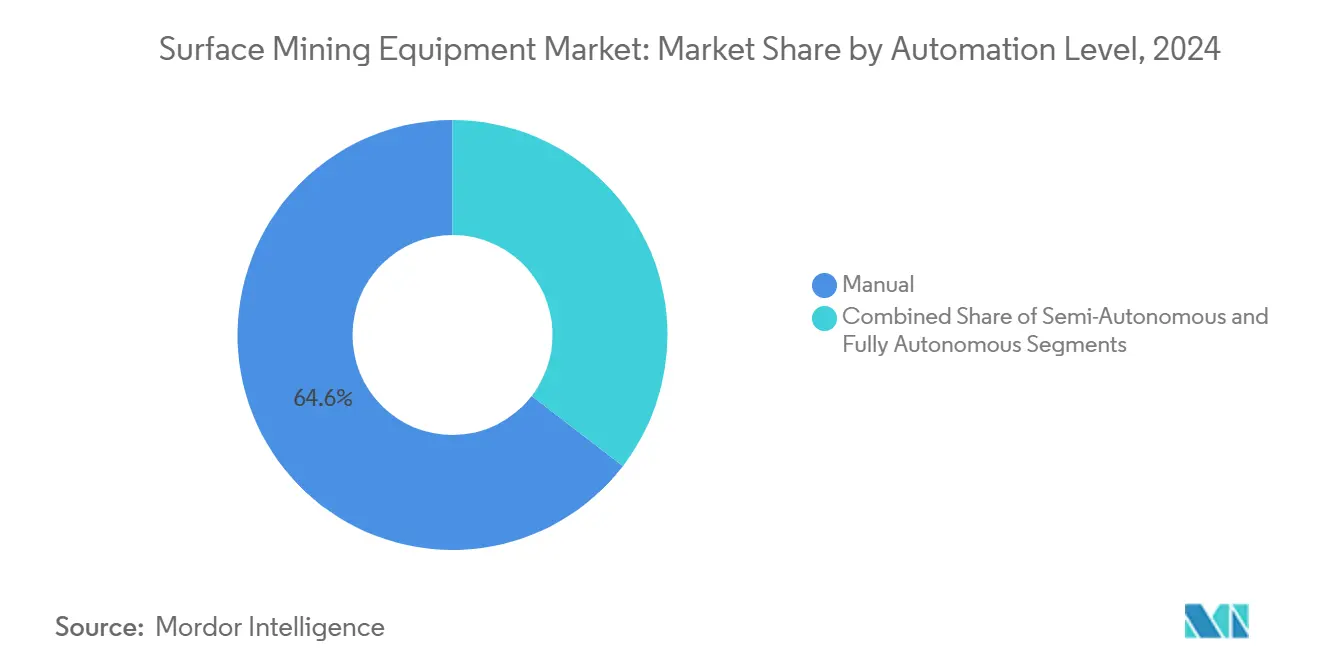

- By automation level, manual operations commanded a 64.56% share of the Surface Mining Equipment Market in 2024. The fully autonomous systems segment is expected to grow at a 14.36% CAGR during the forecast period (2025-2030).

- By application, coal mining accounted for a 43.74% share of the Surface Mining Equipment Market in 2024, with the metal mining segment expected to grow at a 7.14% CAGR during the forecast period (2025-2030).

- By geography, Asia-Pacific dominated the Surface Mining Equipment Market with a 49.98% share in 2024. The South America segment is expected to grow at a 5.62% CAGR during the forecast period (2025-2030).

Market Trends and Insights

Drivers Impact Analysis of Surface Mining Equipment Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for Critical Minerals | +1.3% | Global, with early gains in South America, Australia, Africa | Long term (≥ 4 years) |

| Digital-Mine Initiatives | +1.2% | North America & EU, APAC core, spill-over to MEA | Medium term (2-4 years) |

| Fleet-Replacement Cycles | +1.1% | Global | Short term (≤ 2 years) |

| Open-Pit Coal Projects | +0.8% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| High-Capacity Ultra-Class Haul Trucks | +0.6% | Global | Medium term (2-4 years) |

| Mine-Level ESG Targets | +0.3% | North America & EU, with early adoption in progressive mining regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Critical Minerals for Electric-Mobility Supply Chain

Global lithium requirements are projected to multiply tenfold by 2050, while copper demand could double by 2035. National resource strategies now prioritize investment in copper, lithium, and cobalt projects, especially across Chile, Peru, Argentina, and selected African belts. The mineral rush is forcing operators to procure ultra-class haul trucks, high-capacity excavators, and precise material-handling systems engineered for complex ore bodies.[1]“The Role of Critical Minerals in Clean Energy Transitions,” International Energy Agency, iea.org Regulatory frameworks such as the European Critical Raw Materials Act accelerate procurement because access to compliant supply chains becomes a condition for downstream electric-vehicle subsidies.

Digital-Mine Initiatives Accelerating Fleet-Automation Investments

Globally, a significant fleet of autonomous haul trucks is boosting productivity, reducing operational costs, and markedly improving safety outcomes. These trucks are increasingly being adopted across various industries, showcasing their potential to revolutionize traditional hauling operations. Partnerships between leading miners and equipment makers integrate battery-electric drivetrains with autonomous platforms to satisfy labor and emissions objectives. Predictive-maintenance algorithms, edge-computing nodes, and advanced network technologies such as 5G form the backbone of these deployments. For large-scale operations, the implementation often involves substantial investment. Early adopters have observed marked improvements in equipment availability and a reduction in unexpected breakdowns. Skilled-labor constraints persist for system upkeep and cybersecurity, but integrated training simulators and remote-support centers are alleviating gaps.

Fleet Replacement Cycles for Aging Diesel Equipment

Haulage equipment purchased during the 2010-2015 commodity super-cycle now reaches end-of-life. New regulatory tiers for particulate emissions increase compliance costs for legacy engines, tipping cost-benefit calculations toward full replacement. Recent articulated-hauler launches feature 15% fuel-efficiency gains and modular architecture designed for future hybrid or electric conversions[2]“Volvo Construction Equipment Unveils Brand-New Line-Up of Articulated Haulers,” Volvo Construction Equipment, volvoce.com. Replacement decisions coincide with electrification roadmaps, challenging operators to balance proven diesel reliability with emerging zero-emission alternatives.

Adoption of High-Capacity Ultra-Class Haul Trucks

Ultra-large haul trucks, boasting a significantly higher payload capacity, can substantially cut per-unit transport costs compared to their smaller counterparts. Ultra-class vehicles reduce operator headcount and simplify maintenance scheduling by concentrating capacity into fewer assets. New models incorporate autonomy-ready drivetrains, advanced collision-avoidance sensors, and hybrid-assist systems that recuperate braking energy. Mine-site infrastructure must be upgraded to handle heavier axles and larger loading tools, yet lower operating expenses justify the capex. Batteries with sufficient energy density for ultra-class applications remain under development, making hybridization the near-term pathway.

Restraints Impact Analysis of Surface Mining Equipment Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity-Price Volatility | -1.4% | Global | Short term (≤ 2 years) |

| Supply-Chain Bottlenecks | -1.2% | Global, with acute effects in North America & EU | Medium term (2-4 years) |

| Emission and Land-Rehabilitation Regulations | -0.7% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Skilled-Labour Shortage | -0.3% | Global, with severe impacts in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Commodity-Price Volatility Curbing Capex Cycles

Copper prices reflected significant volatility in 2024, prompting operators to defer fleet purchases until cost visibility stabilizes. Financing models now incorporate performance-based leasing, allowing miners to pay per tonne moved rather than capitalizing equipment upfront. Lending institutions increasingly embed sustainability covenants, linking interest margins to emissions reductions, complicating traditional procurement. Volatility has the most pronounced impact on bulk commodities such as iron ore and thermal coal, where tighter margins magnify budgeting risk.

Supply-Chain Bottlenecks for Advanced Electronics and Batteries

Semiconductor lead times stretched in 2025, while specialized mining-grade battery modules faced allocation limits because automotive demand absorbed cell output. OEMs diversified supplier bases by sourcing engines, drivetrains, and control units from alternate regional vendors, yet certification requirements extended validation timelines. Charging-infrastructure components such as high-capacity inverters and portable substations also experienced delays, limiting rapid electric-fleet rollouts. Substitution strategies occasionally reduced performance, although reliability standards remained non-negotiable under mine-safety regulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Surface Mining Equipment Market Segment Analysis

By Equipment Type:

Haul Trucks Drive Market LeadershipHaul trucks generated a 32.28% share of the surface mining equipment market in 2024, illustrating their pivotal role in large-scale material movement across open pits. The haul trucks' surface mining equipment market size is expected to grow at a 6.81% CAGR during the forecast period (2025-2030) as operators prioritize ultra-class payloads to trim per-ton hauling costs. Emerging designs integrate autonomous kits, collision-avoidance radar, and battery-ready chassis, signaling a shift toward future-proof platforms. Excavators remain essential for overburden stripping and ore loading, with electric mid-size models extending zero-emission mining into confined benches and environmentally sensitive zones.

Growth for bulldozers and loaders aligns with infrastructure expansion within mines, but their incremental demand trails material-movement assets. New grader and dozer variants offer intelligent blade-control and hybrid-assist drivetrains but face longer payback horizons. Equipment makers enhance aftermarket packages with real-time telematics, boosting lifecycle utilization. Compliance with evolving safety standards prompts fleet renewal even in segments where output growth is moderate, reinforcing steady baseline demand for diverse categories within the broader surface mining equipment market.

By Power Source:

Electric Transformation Accelerates Despite Diesel DominanceDiesel engines retained a 73.94% share of the surface mining equipment market in 2024 owing to high energy density, established refueling logistics, and proven durability. Nevertheless, the electric models segment is expected to grow at a 12.53% CAGR during the forecast period (2025-2030), spurred by corporate decarbonization pledges and lower total-cost-of-ownership in suitable duty cycles. With the aid of fast-charging systems and trolley-assist technologies, battery-electric haul trucks can now operate for extended periods, easing concerns about their limited range. Meanwhile, hybrid powertrains are facilitating this transition, delivering significant fuel efficiency gains without necessitating major alterations to the current infrastructure.

Infrastructure scale-up remains a gating factor because grid access, renewable generation, and high-voltage charging are site-specific investments. Organizations transitioning from diesel have reported significant operational cost cuts, despite facing a hefty initial capital investment. These cost reductions are primarily attributed to lower fuel expenses, reduced maintenance requirements, and improved energy efficiency, which collectively enhance long-term financial sustainability. Diesel efficiency gains from advanced combustion, after-treatment systems, and alternative fuels such as renewable diesel will temper market share losses until battery technology matures for ultra-class platforms. Government incentives and carbon-pricing schemes speed adoption, particularly in jurisdictions enforcing aggressive emission ceilings.

By Automation Level:

Manual Operations Yield to Autonomous FutureThe manual equipment segment dominated the surface mining equipment market in 2024, with a 64.56% share, but safety imperatives and labor shortages elevate autonomous deployment priorities. Fully autonomous solutions are forecast to grow at a 14.36% CAGR during the forecast period (2025-2030), a trajectory driven by validated productivity gains, declining sensor costs, and digital-infrastructure investments. Semi-autonomous kits enable retrofit upgrades on existing fleets, broadening addressable Surface Mining Equipment Market demand while lowering up-front risk for cautious operators.

Infrastructure complexity is the largest barrier; reliable high-bandwidth connectivity, low-latency edge computing, and comprehensive geo-fencing are prerequisites. Workforce training also shifts from equipment operation to system monitoring and data analytics, demanding new competency frameworks. Cybersecurity protocols and regulatory certification add time and cost but underpin stakeholder acceptance. Integration with autonomous drilling, blasting, and ore-sorting solutions promises a step-change in mine-wide optimization once interoperability standards mature.

By Application:

Coal Mining Scale Contrasts Metal Mining GrowthCoal operations accounted for a 43.74% share of the surface mining equipment market in 2024, reflecting the scale of Asia-Pacific thermal-coal production needed for power-sector baseload. The Surface Mining Equipment Market Share of coal is expected to erode gradually as decarbonization policies tighten, yet absolute demand remains sizeable through 2030. Equipment selection favors ultra-class haulers and high-capacity draglines that maximize economies of scale in overburden removal.

Metal mining is projected to grow at a 7.14% CAGR during the forecast period (2025-2030) by decade's end as electric-vehicle and renewable-energy supply chains absorb rising volumes of copper, lithium, nickel, and rare earths. Operators invest in deeper pits, in-pit crushing and conveying, and selective ore-handling equipment to cope with declining grades. Mineral mining, including iron ore and industrial raw materials, maintains steady growth because infrastructure stimulus in emerging markets sustains steel demand. Application dynamics, therefore, hinge on policy trajectories, commodity cycles, and technology uptake, shaping the heterogeneous demand matrix that characterizes the Surface Mining Equipment Market.

Geography Analysis

APAC Surface Mining Equipment Market

Asia-Pacific accounts for a 49.98% share in the surface mining equipment market in 2024, underpinned by vast coal operations in China, India, and Indonesia, and by expanding base-metal projects in Australia. Regional surface mining equipment market demand benefits from integrated supply chains, domestic manufacturing capacity, and supportive fiscal frameworks. Electrification pilots gain traction in Japan and South Korea, where technology-oriented regulatory incentives encourage early adoption. Growth is moderated by skilled-labor shortages in advanced digital systems and intermittent policy shifts on coal dependency, yet replacement cycles remain robust in legacy pits.

South America Surface Mining Equipment Market

South America region is expected to grow with a 5.62% CAGR during the forecast period (2025-2030). It will continue outpacing global averages due to copper and lithium project build-outs in Chile, Peru, and Argentina. Investment flows target deeper deposits that require ultra-class equipment, autonomous haulage, and electric drilling solutions. ESG scrutiny prompts deployment of battery-electric prototypes, renewable-energy microgrids, and water-saving beneficiation processes. Infrastructure gaps and permitting timelines pose execution risk, but sovereign strategies that classify critical minerals as national-interest assets provide regulatory clarity.

North America and EMEA Surface Mining Equipment Market

North America is expected to grow with a 4.46% CAGR during the forecast period (2025-2030), driven by modernization programs in established metal and potash mines and emerging federal incentives for domestic critical-mineral supply. High safety standards favor early uptake of advanced collision-avoidance, fatigue-monitoring, and remote-control systems. Canada's oil-sand operations sustain demand for large dozers and specialty haul trucks, while the United States' hard-rock mines explore trolley-assist electrification corridors. Europe is expected to grow by 3.93% during the forecast period, as brownfield mines in Scandinavia, Poland, and Spain emphasize efficiency upgrades over capacity additions. Middle East and Africa achieved 5.13% growth; Gulf-state sovereign funds are allocating capital to African gold and battery-metal ventures, catalyzing surface mining equipment market orders aligned with best-practice sustainability protocols.

Competitive Landscape

Competitive concentration is moderate because the top five manufacturers collectively account for the majority of annual surface-mining equipment revenues. Market leaders differentiate through vertically integrated digital platforms that bundle hardware, software, and services under performance-based contracts. One equipment maker integrated ore-sensing technology into its fleet-management suite, enabling real-time grade control that improves blasting and milling efficiency. Another pioneer surpassed the 700-unit milestone for autonomous haul trucks, creating scale advantages in control-room support, spare-part logistics, and sensor calibration.

Electrification is the most disruptive competitive axis. An OEM unveiled the first 30-tonne electric articulated hauler and refreshed its entire platform with 15% fuel-efficiency gains for diesel variants. Chinese entrants leverage cost competitiveness and rapid product iteration to penetrate price-sensitive markets, capturing share in Russia, Central Asia, and parts of Africa. Collaboration models also evolve: power-train specialists partner with truck builders to co-develop hybrid systems, while battery integrators work with mine operators on charging-infrastructure deployment.

Aftermarket services contribute rising revenue share as predictive analytics cut unplanned downtime and optimize component replacement. Subscription-based software, remote-diagnostics portals, and operator-training simulators deepen customer lock-in. Certification costs for autonomy and high-voltage electrics create entry barriers that shield incumbents, yet provide niches for specialist module suppliers. Intellectual-property regimes, cybersecurity compliance, and lifecycle carbon accounting will increasingly define competitive advantage over simple production scale.

Surface Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Hitachi Construction Machinery Co., Ltd.

Liebherr-International AG

Volvo Construction Equipment

- *Disclaimer: Major Players sorted in no particular order

Surface Mining Equipment Market Companies Covered in this Report

- Caterpillar Inc.

- Komatsu Ltd.

- Hitachi Construction Machinery Co., Ltd.

- Liebherr-International AG

- Volvo Construction Equipment

- Sandvik AB

- Epiroc AB

- Doosan Infracore Co., Ltd.

- Hyundai Construction Equipment Co., Ltd.

- Terex Corporation

- Belarusian Autoworks (BELAZ)

- SANY Group

- XCMG Construction Machinery Co., Ltd.

- JCB Ltd.

- Deere and Company (Wirtgen)

- BEML Limited

Recent Industry Developments in Surface Mining Equipment Market

- September 2025: Cummins and Komatsu signed an agreement to co-develop hybrid powertrains for next-generation surface haulage trucks, expanding collaboration with drive-system supplier Wabtec.

- August 2025: Sandvik introduced an AutoMine Surface Drilling Training Simulator that accelerates operator competence for automated drill rigs.

- February 2025: MacLean Engineering established a Surface Mining Vehicle Division to apply a decade of battery-electric design expertise to underground and surface applications.

- January 2025: Epiroc received a large order from a major iron-ore producer for autonomous drilling and hauling equipment, with deliveries scheduled for Q4 2025.

Global Surface Mining Equipment Market Report Scope

Segmentation Overview

| Bulldozers |

| Excavators |

| Haul Trucks |

| Loaders |

| Others |

| Diesel |

| Electric |

| Hybrid |

| Manual |

| Semi-Autonomous |

| Fully Autonomous |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Equipment Type | Bulldozers | |

| Excavators | ||

| Haul Trucks | ||

| Loaders | ||

| Others | ||

| By Power Source | Diesel | |

| Electric | ||

| Hybrid | ||

| By Automation Level | Manual | |

| Semi-Autonomous | ||

| Fully Autonomous | ||

| By Application | Metal Mining | |

| Mineral Mining | ||

| Coal Mining | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Surface Mining Equipment Market?

The market is valued at USD 62.29 billion in 2025 and is forecast to reach USD 81.53 billion by 2030.

Which equipment category leads global demand?

Haul trucks lead, holding 32.28% revenue in 2024 and remaining pivotal for large-scale material movement across open-pit mines.

How fast is electric equipment adoption growing?

Electric surface-mining equipment is projected to advance at a 12.53% CAGR through 2030, outpacing every other power-source category.

Which region is expected to grow the quickest?

South America is projected to achieve the fastest 5.62% CAGR due to extensive copper and lithium project pipelines.

What impact will autonomy have on future fleets?

Fully autonomous systems are forecast to expand at a 14.36% CAGR, driven by productivity gains and safety improvements.

Page last updated on: